Biosensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

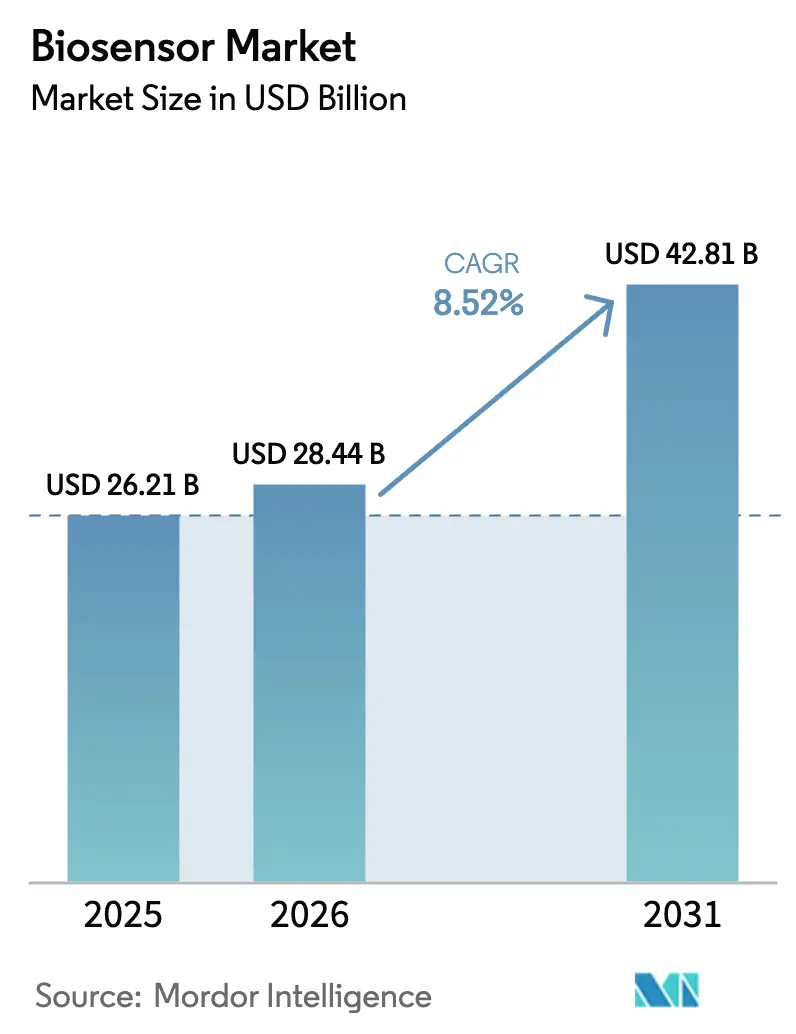

| Market Size (2026) | USD 28.44 Billion |

| Market Size (2031) | USD 42.81 Billion |

| Growth Rate (2026 - 2031) | 8.52% CAGR |

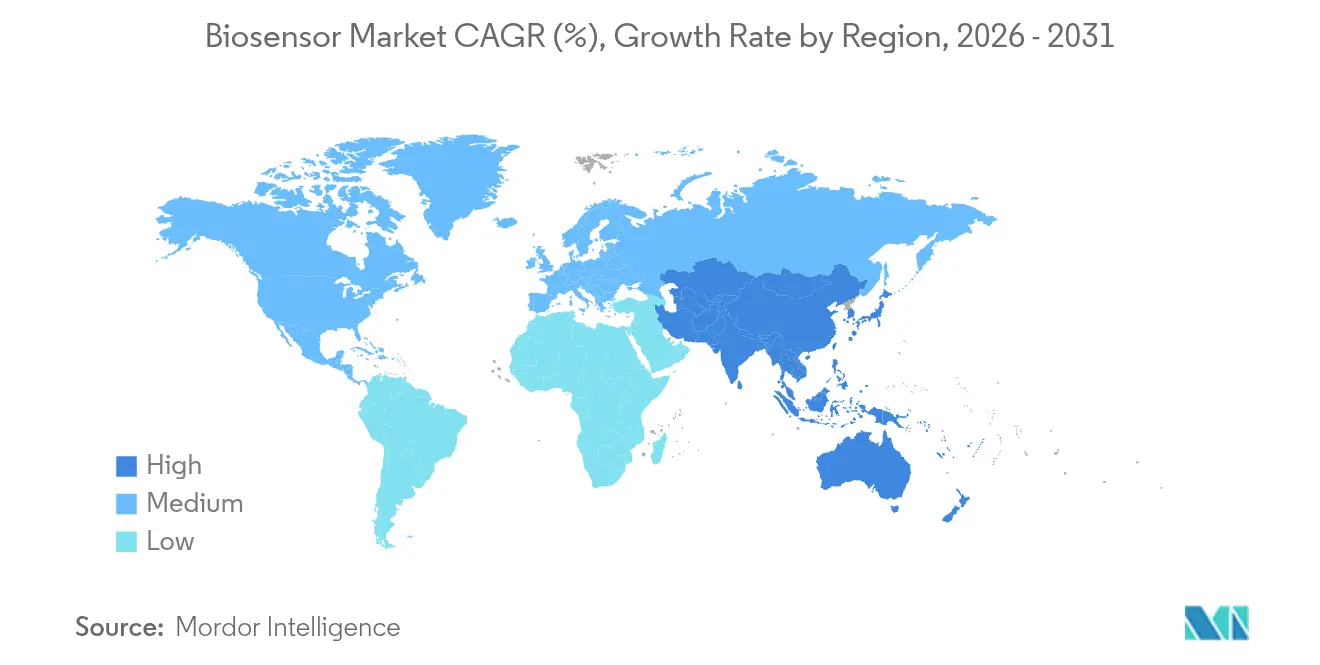

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biosensor Market Analysis by Mordor Intelligence

The biosensor market size was valued at USD 26.21 billion in 2025 and estimated to grow from USD 28.44 billion in 2026 to reach USD 42.81 billion by 2031, at a CAGR of 8.52% during the forecast period (2026-2031). Rising prevalence of chronic diseases, the migration of care from hospitals to homes, and the maturing ecosystem of AI-enabled diagnostics collectively reinforce this expansion trajectory. Continuous glucose monitoring remains the anchor application, yet rapid uptake of multi-analyte wearables signals a shift toward holistic, consumer-centered health management. Non-medical uses—from food safety to environmental monitoring—add volume, while regulatory initiatives that position point-of-care testing as a frontline tool accelerate adoption in both developed and emerging economies. At the same time, high validation costs and multi-jurisdictional compliance obligations temper market entry, creating protective barriers for incumbents with deep regulatory expertise.

Key Report Takeaways

- By product type, medical biosensors held 64.58% of 2025 revenue, while wearable patch and embedded biosensors are projected to register a 9.88% CAGR between 2026 and 2031.

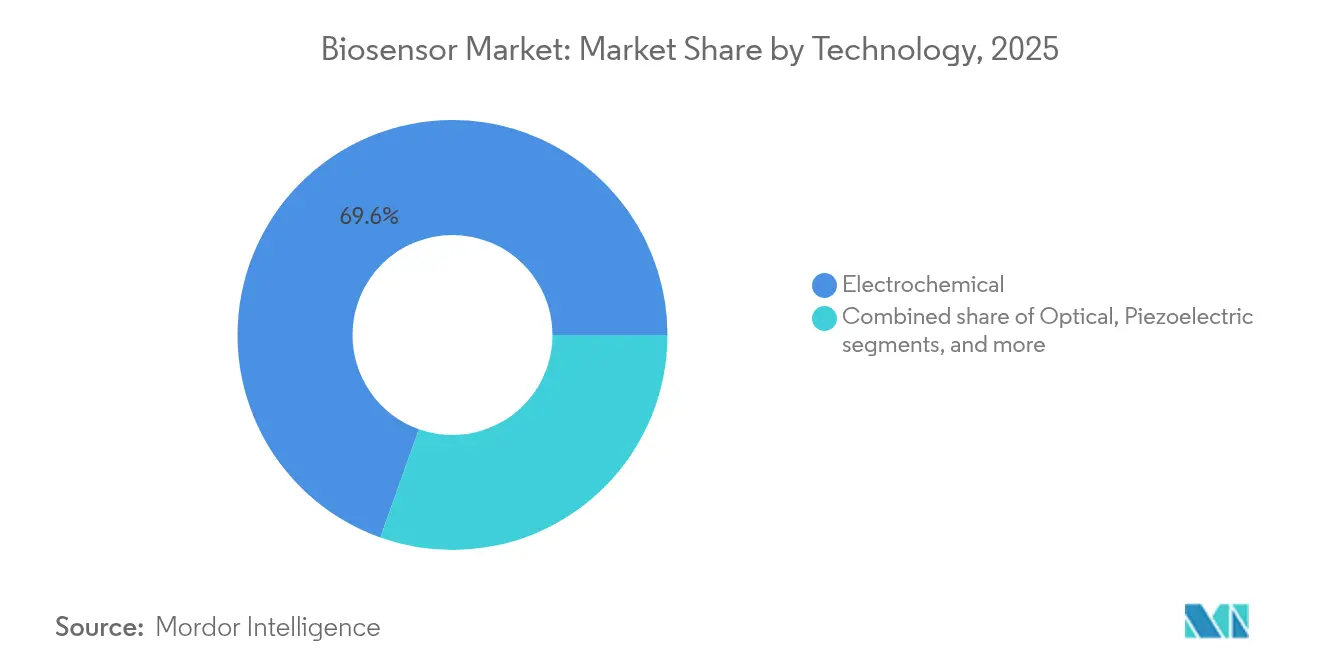

- By technology, electrochemical platforms accounted for 69.55% of 2025 sales, whereas optical biosensors are expected to expand at a 10.12% CAGR through 2031.

- By end-user, point-of-care testing captured 56.78% of demand in 2025, while home healthcare diagnostics is forecast to grow at an 10.73% CAGR over the same period.

- By geography, North America commanded 35.12% of the 2025 market, yet Asia-Pacific is anticipated to log the fastest regional growth with a 9.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biosensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for point-of-care diagnostic solutions | +2.1% | Global, strongest in North America & Europe | Medium term (2-4 years) |

| Expanding applications of biosensors in food safety and environmental monitoring | +1.3% | Global, accelerated in Asia-Pacific | Long term (≥4 years) |

| Integration of artificial intelligence and IoT for real-time biosensor analytics | +1.8% | North America & EU leading, APAC rapid follower | Medium term (2-4 years) |

| Increasing investments in wearable and implantable medical devices | +1.5% | Global, venture-capital concentration in North America | Short term (≤2 years) |

| Advancements in nanomaterials enhancing sensor sensitivity and miniaturization | +1.2% | Global, R&D leadership in developed markets | Long term (≥4 years) |

| Government initiatives supporting personalized medicine and preventive healthcare | +0.9% | North America & EU primarily, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Point-of-Care Diagnostic Solutions

Point-of-care testing slashes turnaround time from days to minutes, rapidly informing treatment choices and lowering readmission rates. FDA clearance of Dexcom’s Stelo over-the-counter continuous glucose monitor in March 2024 removed prescription barriers and validated retail distribution pathways[1]Food and Drug Administration, “Dexcom Stelo 510(k) Clearance,” fda.gov. Hospitals benefit from bed-day savings, while payers back the approach as preventive care curbs high-cost acute events. Laboratories, however, face revenue erosion, prompting a pivot toward value-added consultative services. AI algorithms bundled with sensors mitigate operator variability, allowing accurate use in community clinics and rural pharmacies. Together these dynamics expand the biosensor market beyond traditional clinical silos.

Increasing Investments in Wearable and Implantable Medical Devices

Biolinq raised USD 58 million in 2024 followed by USD 100 million Series C in 2025 to commercialize micro-sensor technology for multi-analyte monitoring. Venture capital inflows reflect conviction that continuous, unobtrusive sensing will become a daily wellness staple. The wearable biosensor segment is projected to post a 38.8% CAGR to 2025, propelled by a convergence of consumer electronics design and medical-grade accuracy. Capital abundance, however, raises competitive density, which could compress prices once multiple FDA-cleared options inhabit the same indication. Proven reimbursement pathways and regulatory compliance remain decisive advantages for incumbents.

Advancements in Nanomaterials Enhancing Sensor Sensitivity and Miniaturization

Two-dimensional MXene coatings amplify electron mobility, boosting electrochemical biosensor response times by 30% compared with conventional carbon inks[2]National Center for Biotechnology Information, “MXene-Enhanced Electrochemical Biosensors,” pmc.ncbi.nlm.nih.gov. Gold-nanoparticle surface functionalization delivers femtomolar detection thresholds for cancer biomarkers, paving the way for early screening via minimally invasive samples. These performance gains support downsizing, which in turn lengthens wear-time and enriches data continuity. Nanomaterial supply chains remain regionally concentrated, bringing geopolitical risk that firms manage through dual sourcing. Successful commercial integration hinges on translating lab-scale sensitivity into manufacturable, repeatable performance.

Government Initiatives Supporting Personalized Medicine and Preventive Healthcare

National health systems in the United States, Germany, and Japan launched reimbursement codes between 2024 and 2025 for remote physiologic monitoring of cardiometabolic parameters[3]Centers for Medicare & Medicaid Services, “Remote Physiologic Monitoring Codes,” cms.gov. Subsidized device procurement lowers patient out-of-pocket costs, lifting adoption curves among seniors and low-income populations. Public-private R&D grants finance early-stage biosensor prototypes, shortening academic-to-industry transfer cycles. Policymakers increasingly view real-time biomarker tracking as vital infrastructure for early disease interception, aligning fiscal incentives with commercial objectives. Yet expanding coverage raises scrutiny over cybersecurity and data sovereignty, compelling vendors to embed rigorous protection protocols at design stage.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High development and validation costs of biosensor platforms | -1.4% | Global, higher impact in emerging markets | Medium term (2-4 years) |

| Stringent regulatory approval processes across major regions | -1.1% | North America & EU primarily, expanding globally | Long term (≥4 years) |

| Limited standardization of biorecognition elements and manufacturing protocols | -0.8% | Global, particularly challenging for cross-border production | Medium term (2-4 years) |

| Concerns over data privacy and cybersecurity in connected biosensor ecosystems | -0.9% | Global, with heightened scrutiny in Europe & North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Development and Validation Costs of Biosensor Platforms

End-to-end biosensor commercialization, from bench to scale manufacturing, can surpass USD 100 million once clinical trials and cybersecurity testing are included. Smaller firms often exhaust capital during pivotal studies, a reality underscored by LifeScan’s bankruptcy filing in 2025. Cybersecurity mandates introduced in 2024 force additional software validation, lengthening time-to-market. Larger incumbents counterbalance these outlays with high-volume production and established reimbursement streams. The cost barrier discourages new entrants yet simultaneously preserves pricing discipline for regulatory-cleared products, thereby sustaining profitability for those who clear the hurdle.

Stringent Regulatory Approval Processes Across Major Regions

The FDA’s 2024 guidance expanded post-market reporting for connected devices and tightened change-control documentation. The European Union’s Health Technology Assessment Regulation adds another evaluation layer before payer adoption, prolonging the pathway from CE Mark to national reimbursement. Divergent cybersecurity statutes in Canada and Australia further fragment compliance roadmaps, demanding resource-intensive parallel submissions. While such rigor heightens patient safety, it extends gestation periods and erodes early-mover advantage. Vendors with global regulatory teams and pre-sub consultations secure smoother approvals, erecting entry barriers that fortify incumbent positions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Medical Biosensors Sustain Leadership Amid Wearable Surge

Medical biosensors commanded 64.58% of 2025 revenues, a position built on three decades of clinical evidence supporting glucose, cardiac, and infectious disease assays. The segment benefits from entrenched reimbursement and clinician familiarity, insulating demand during economic downturns. Yet wearable patch and embedded variants are expanding at a 9.88% CAGR to 2031, leveraging consumer electronics design to attract wellness-focused buyers. In 2025, Abbott introduced the Lingo platform to gauge ketones, lactate, and glucose simultaneously, broadening its user base beyond diabetics. Food toxicity sensors gained momentum as regulators intensified surveillance, while agriculture biosensors addressed soil nutrient depletion and pesticide residues. Industrial bioreactor monitoring remains a niche characterized by low unit volume but high price points.

Steady reimbursement unlocks new data-subscription models where providers bill for remote monitoring rather than the device itself. Growth in non-medical verticals is also notable: CRISPR-based food safety biosensors measure Salmonella contamination within 20 minutes, sidestepping lab culture delays. Environmental agencies adopt heavy-metal detection networks that integrate graphene-oxide electrodes, reflecting an urgent need to track industrial effluents at ppb sensitivity. As a result, the biosensor market experiences cross-sector fertilization, with medical players repurposing platforms for agri-food and industrial insights.

By Technology: Electrochemical Dominance Confronts Optical Momentum

Electrochemical formats held 69.55% share in 2025, anchored by low power requirements, scalable screen-printing, and proven reliability in glucose monitoring. Cost-effectiveness makes them attractive for single-use strips and disposable sensors used during epidemics. Nonetheless, optical systems are advancing at 10.12% CAGR through 2031 thanks to label-free detection and compatibility with non-invasive sample matrices. In February 2025, Korean researchers validated an optical biosensor detecting methylated DNA at 25 fg/mL, demonstrating oncology screening potential. Piezoelectric sensors, though smaller in revenue, deliver ultra-high sensitivity for pathogen detection in sterile bioprocessing. Thermal and nanomechanical technologies occupy specialized niches but exhibit rising research interest as MEMS fabrication costs fall.

Hybrid architectures that merge electrochemical transduction with optical readouts are surfacing, especially in multi-analyte wearables. MXene-coated electrodes improve electron transfer kinetics, reducing limit-of-detection and supporting miniaturization. Meanwhile, photonic integrated circuits drive down optical sensor bill-of-materials, making them increasingly competitive in volume applications. As intellectual property around pure electrochemical glucose sensing matures, vendors diversify toward optical and acoustic modalities to refresh portfolios and circumvent patent cliffs.

By End-User: Point-of-Care Testing Dominates While Home Healthcare Accelerates

Point-of-care settings captured 56.78% of 2025 demand, reflecting hospital and clinic appetite for rapid triage tools that decompress overloaded laboratory services. Decentralization gained further impetus during the COVID-19 aftermath as providers institutionalized near-patient diagnostics to manage infection control. Home healthcare, however, is projected to grow fastest at 10.73% CAGR as population aging and value-based care incentivize remote monitoring. The global continuous glucose monitoring market alone is on track to reach USD 20 billion by 2028, fueled by devices designed for self-application with smartphone connectivity.

Outside healthcare, food and beverage processors integrate inline biosensors to certify batch quality in real time, curbing recall risks. Research laboratories harness high-sensitivity platforms for biomarker discovery and drug-mechanism validation, shortening preclinical timelines. Environmental agencies deploy wireless sensor arrays across rivers and industrial corridors for pollution surveillance, creating data sets that inform policy interventions. Security and biodefense stakeholders also invest, with multi-agent detectors capable of identifying biothreats within 3 minutes. Overall, the expanding scope of use cases cements the biosensor market as core infrastructure across public health and industrial ecosystems.

Geography Analysis

North America retained 35.12% of 2025 revenues, supported by sophisticated reimbursement schemes, strong venture capital networks, and a responsive regulatory regime. FDA authorization of over-the-counter CGM devices established a template for consumer-direct distribution, further widening access. To hedge against market saturation, incumbents pivot to wellness applications and multi-analyte wearables. Elevated healthcare expenditure levels also incentivize payers to reimburse preventive diagnostics that reduce costly acute episodes, reinforcing sustained demand for biosensors.

Asia-Pacific is forecast to post a 9.08% CAGR to 2031, underpinned by accelerating urbanization, expanding middle-class purchasing power, and government funding for digital health infrastructure. China’s domestic manufacturers scale fermentation-monitoring analyzers that compete on cost while meeting emerging export standards. India and Southeast Asian nations adopt low-cost glucose and cardiac markers to manage rising diabetes and cardiovascular prevalence. Divergent regulatory pathways across the region prompt multinational firms to set up localized design and testing centers to align products with national quality standards. Consequently, partnerships with regional distributors become instrumental in navigating heterogeneous reimbursement and procurement policies.

Europe grows steadily as stringent MDR compliance drives premiumization. The CE-marked Roche SmartGuide demonstrates the region’s willingness to approve AI-enhanced devices when cybersecurity and data-privacy criteria are met. Government payers increasingly couple device reimbursement with outcome-based contracts, encouraging suppliers to integrate analytics that verify therapeutic benefit. Meanwhile, Latin America, the Middle East, and Africa remain nascent yet high-potential zones where infectious-disease testing and water-quality monitoring offer immediate application value. Suppliers entering these markets prioritize rugged, battery-efficient designs and training programs for non-specialist users to surmount resource constraints.

Competitive Landscape

The biosensor market is moderately consolidated, with the top five companies controlling close to 60% of global revenue. Abbott, Dexcom, and Roche leverage decades-long regulatory traction and large installed bases, allowing them to scale production and negotiate favorable reimbursement. Abbott’s 2024 agreement with Medtronic to integrate FreeStyle Libre sensors into insulin pumps underscores ecosystem alliances aimed at locking in patients and providers. Dexcom focuses on algorithmic upgrades that push predictive alerts to smartwatches, extracting subscription fees for premium analytics. Roche integrates AI to broaden competitive appeal in Europe’s privacy-sensitive environment.

M&A activity intensifies as diversified instrumentation companies such as Bruker and Danaher acquire niche biosensor developers to expand into real-time biomolecular interaction analysis. Strategic licensing deals are also prevalent: iRhythm obtained exclusive rights to BioIntelliSense multiparameter sensor technology for ambulatory cardiac monitoring in September 2024. These arrangements allow incumbents to insert cutting-edge sensing modalities into established distribution channels without the latency of internal R&D. Emerging players seek differentiation through ultra-miniaturization, multi-analyte capability, or deep-learning analytics, yet face the hurdle of securing cost-intensive clinical validation.

Competitive advantage increasingly centers on data ecosystems rather than discrete hardware. Vendors that couple sensors with HIPAA-compliant cloud platforms and reimbursement-ready analytics create end-to-end solutions that embed themselves in clinical workflows, making displacement difficult. Regulatory literacy, especially in cybersecurity, becomes a non-negotiable asset as oversight bodies escalate software scrutiny. Overall, market actors balance innovation with compliance, recognizing that sustaining share requires both technical excellence and regulatory endurance.

Biosensor Industry Leaders

Abbott Laboratories

F. Hoffmann-La Roche Ltd

Medtronic Plc

Siemens Healthineers

Dexcom Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Abbott partnered with Beta Bionics to combine its dual sensor with the iLet Bionic Pancreas for real-time diabetes management.

- July 2025: Abbott reported 7.4% sales growth in Q2 2025, with its medical-devices arm up 13.4% and completion of enrollment in the FlexPulse U.S. IDE trial for the TactiFlex Duo PFA system.

- June 2025: Tandem Diabetes Care announced integration of its automated insulin delivery with Abbott’s forthcoming dual glucose-ketone sensor to help users detect rising ketones early.

- April 2025: Biolinq closed a USD 100 million Series C round led by Alpha Wave Ventures to advance precision multi-analyte sensors toward commercialization.

- September 2024: iRhythm Technologies licensed BioIntelliSense multiparameter sensors for ambulatory cardiac monitoring applications.

- August 2024: Abbott and Medtronic initiated a global collaboration linking FreeStyle Libre with Medtronic’s insulin pumps, targeting 11 million intensive insulin users.

Global Biosensor Market Report Scope

Biosensors are analytical devices that integrate biological detecting elements with a sensor system and a transducer. Biosensors stand out for their enhanced selectivity and sensitivity compared to other diagnostic devices. Biosensors' primary applications span ecological pollution monitoring, agriculture, and the food industry.

The study tracks the revenue accrued through the sale of types of biosensor products by various players globally. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report's scope encompasses market sizing and forecasts for the various market segments.

The biosensor market is segmented by product type (medical, food toxicity, bioreactor, agriculture, environment, and other product types), technology (thermal, electrochemical, piezoelectric, and optical), end-user industry (home healthcare diagnostics, POC testing, food industry, research laboratories, and security & biodefense), and geography (North America, Europe, Asia, Australia and New Zealand, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Medical Biosensors |

| Food Toxicity Biosensors |

| Bioreactor Biosensors |

| Agriculture Biosensors |

| Environmental Biosensors |

| Wearable Patch & Embedded Biosensors |

| Electrochemical |

| Optical |

| Piezoelectric |

| Thermal |

| Nanomechanical |

| Point-of-Care Testing |

| Home Healthcare Diagnostics |

| Food & Beverage Industry |

| Research Laboratories |

| Security & Biodefense |

| Environmental Monitoring Agencies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Medical Biosensors | |

| Food Toxicity Biosensors | ||

| Bioreactor Biosensors | ||

| Agriculture Biosensors | ||

| Environmental Biosensors | ||

| Wearable Patch & Embedded Biosensors | ||

| By Technology | Electrochemical | |

| Optical | ||

| Piezoelectric | ||

| Thermal | ||

| Nanomechanical | ||

| By End-User | Point-of-Care Testing | |

| Home Healthcare Diagnostics | ||

| Food & Beverage Industry | ||

| Research Laboratories | ||

| Security & Biodefense | ||

| Environmental Monitoring Agencies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the growth outlook for the biosensor market through 2031?

The biosensor market is projected to expand from USD 28.44 billion in 2026 to USD 42.81 billion by 2031, reflecting an 8.52% CAGR driven by demand for point-of-care diagnostics and AI-enabled wearables.

Which region is expected to grow fastest in biosensors?

Asia-Pacific is forecast to register a 9.08% CAGR through 2031 thanks to expanding healthcare access, rising chronic disease prevalence, and supportive government digital health policies.

Which technology segment shows the highest growth?

Optical biosensors exhibit the fastest growth at a 10.12% CAGR due to their non-invasive operation and high sensitivity in complex biological matrices.

What is the leading end-user category today?

Point-of-care settings hold 56.78% of demand, but home healthcare diagnostics is the quickest-growing segment with an 10.73% CAGR as remote monitoring gains traction.

How are companies differentiating in this market?

Competitive advantage is shifting toward integrated platforms that couple sensing hardware with predictive analytics, secure cloud ecosystems, and proven reimbursement pathways.

What key recent regulatory milestone has influenced market dynamics?

In March 2024, the FDA authorized the first over-the-counter continuous glucose monitor, a move that broadened retail access and catalyzed further investment in consumer-direct biosensor solutions.

Page last updated on: