Biorationals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

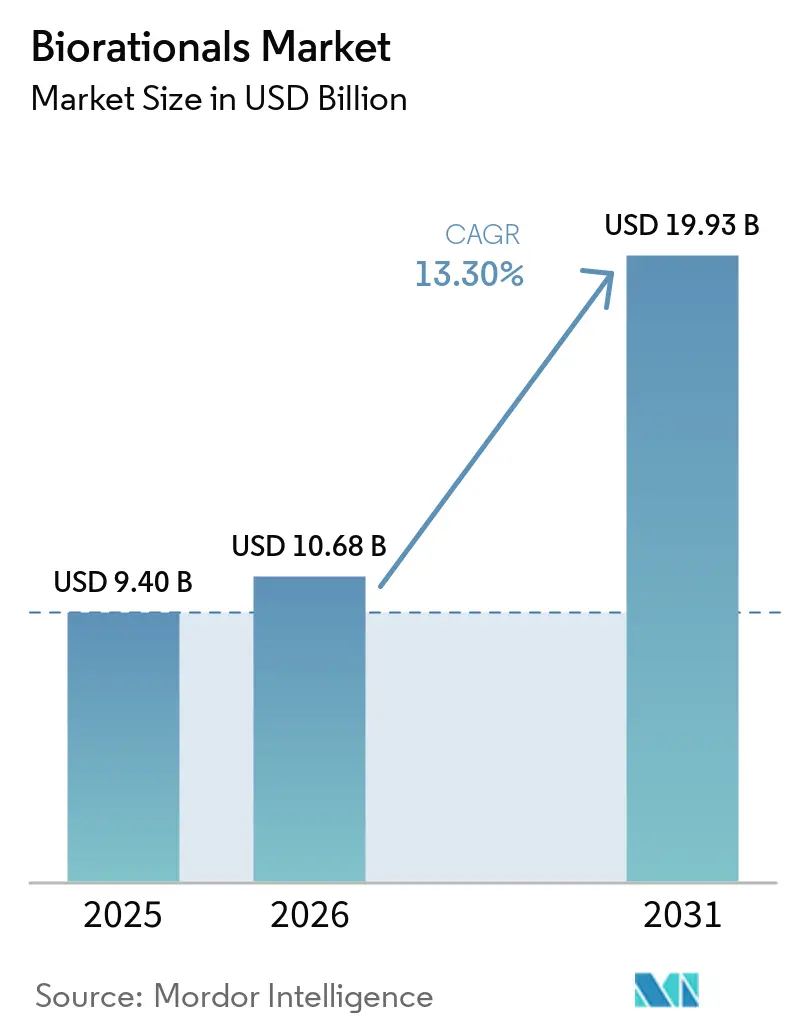

| Market Size (2026) | USD 10.68 Billion |

| Market Size (2031) | USD 19.93 Billion |

| Growth Rate (2026 - 2031) | 13.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biorationals Market Analysis by Mordor Intelligence

The biorationals market size was valued at USD 9.4 billion in 2025 and estimated to grow from USD 10.68 billion in 2026 to reach USD 19.93 billion by 2031, registering a CAGR of 13.3% during the forecast period (2026-2031). Heightened residue regulations, retailer mandates for traceability, and government incentives are accelerating the shift from conventional chemistries toward microbial, botanical, and semiochemical products. Environmental Protection Agency (EPA) actions that delisted 72 synthetic pesticide inert ingredients in 2025, together with the European Union’s efficacy-benchmarking rule for biologicals that starts in 2026, have reduced grower confidence in chemicals while validating performance-ready biorationals[1]Source: United States Environmental Protection Agency (EPA), News Releases from Region 07 EPA, epa.gov. Large retailers are also imposing zero-detectable-residue thresholds, turning adoption from a sustainability preference into a shelf-access requirement. Subsidies such as the United States Department of Agriculture (USDA) Climate-Smart Commodities grants and European agri-environment schemes are lowering net costs, and precision-application hardware is narrowing the historical field-persistence gap, positioning the biorationals market for sustained double-digit expansion.

Key Report Takeaways

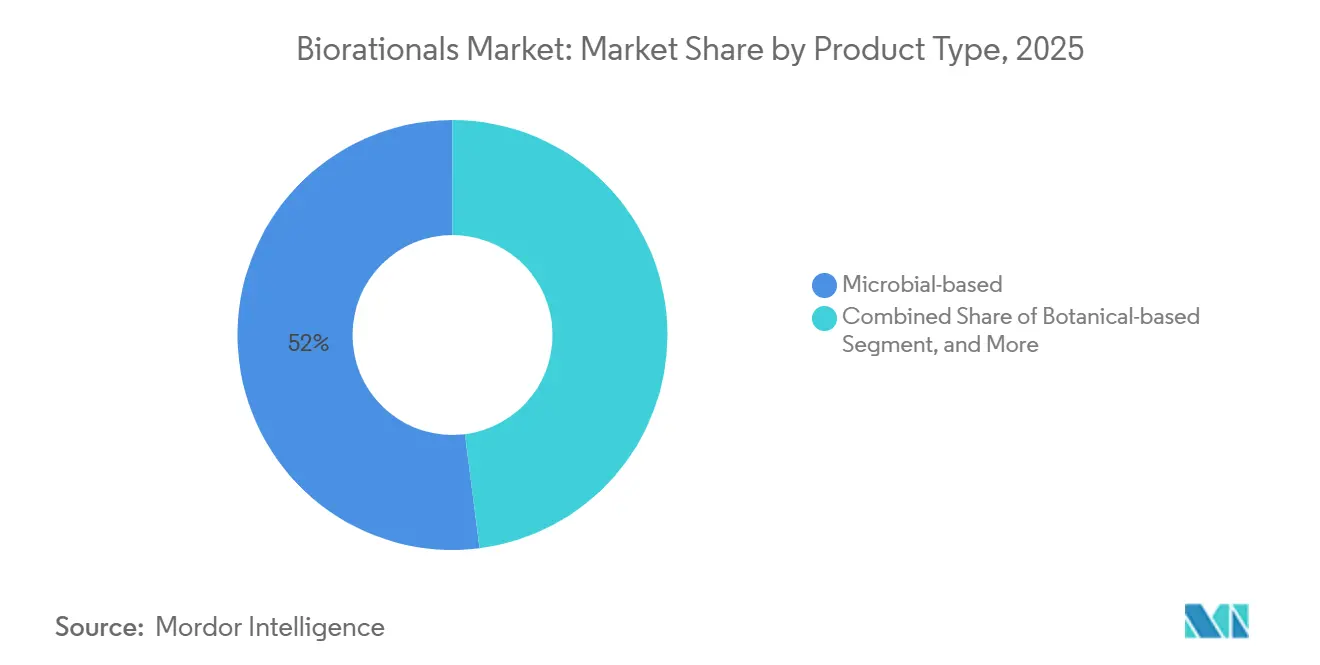

- By product type, microbial-based solutions captured the largest share of the biorationals market in 2025, at 52%. The semiochemical-based products are projected to expand at the fastest CAGR of 19.8% from 2026 to 2031.

- By mode of application, foliar spray accounted for the largest share of revenue at 63.5% in 2025, while seed treatment is the fastest-growing mode at a 20.1% CAGR from 2026 to 2031.

- By source, bacteria accounted for the largest share, 39%, in 2025, while virus-derived agents are forecast to grow at a 22.3% CAGR from 2026 to 2031, making them the fastest-growing segment.

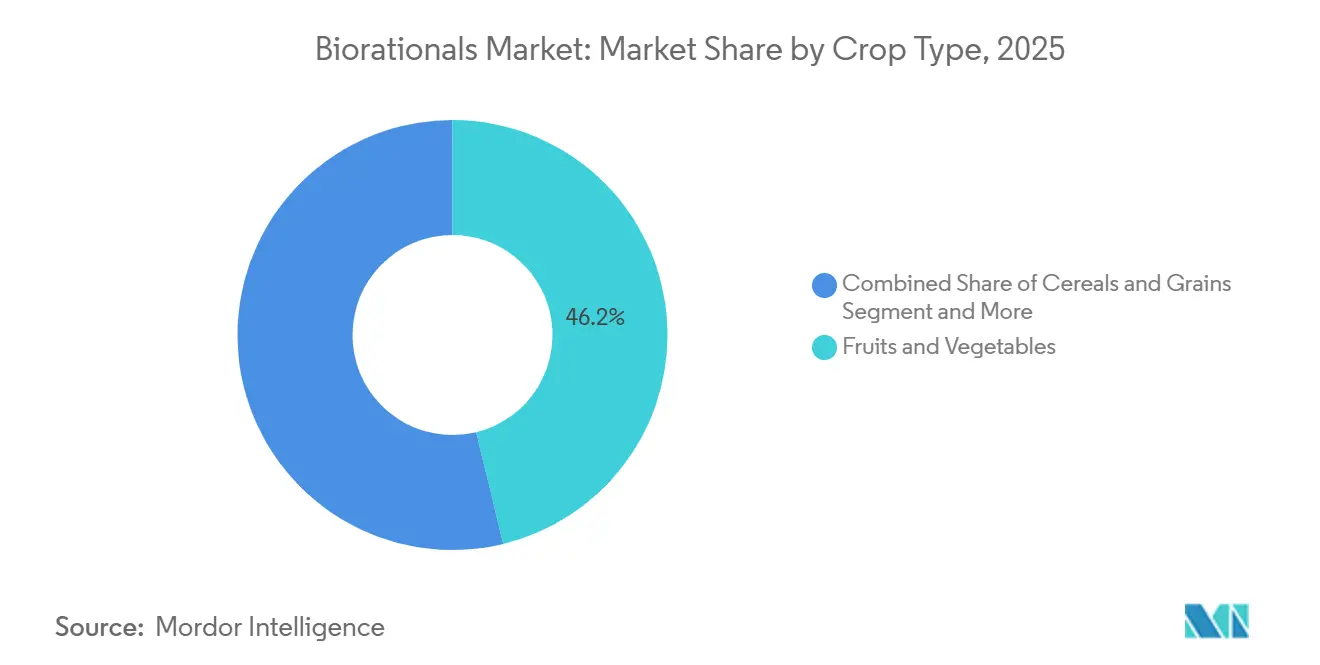

- By crop type, fruits and vegetables led with 46.2% revenue, making it the largest share in 2025, whereas oilseeds and pulses are advancing at the fastest CAGR of 18.4% from 2026 to 2031.

- By formulation, liquid products accounted for the largest share of 58% in 2025 sales; dry formulation-based granules, powders, and encapsulated pellets are the fastest-growing segment at 17.6% from 2026 to 2031, addressing seed-treatment or soil-application niches where moisture sensitivity requires alternate carriers.

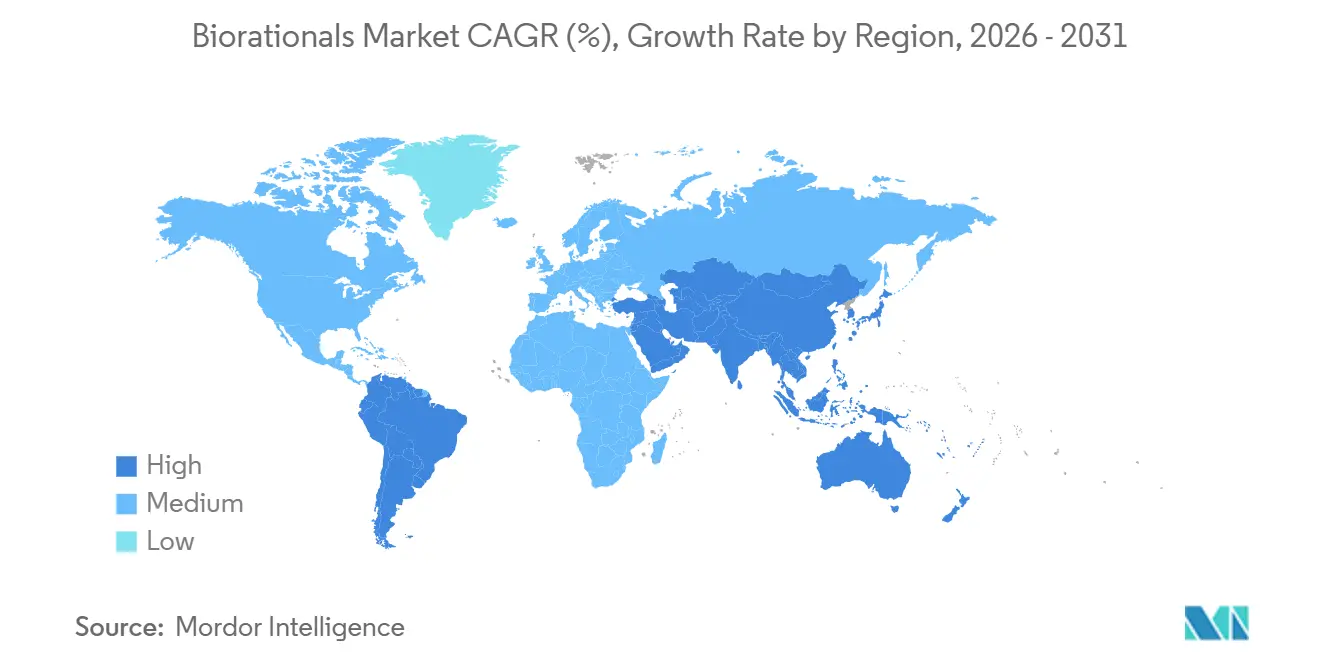

- By geography, North America remains the largest revenue share at 44% in 2025 in the biorationals market and Asia-Pacific is the fastest-growing region with the market size expanding at 15.4% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biorationals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on high-residue synthetic pesticides | +2.8% | Global with strict enforcement in European Union, North America, China | Short term (≤ 2 years) |

| Demand for residue-free produce from food retailers | +2.3% | North America and European Union core, expanding into Asia-Pacific | Medium term (2-4 years) |

| Government subsidies for sustainable agriculture tools | +1.9% | North America, European Union, India, Australia | Medium term (2-4 years) |

| Rapid commercial success of microbial consortia products | +1.6% | Brazil, United States, India | Short term (≤ 2 years) |

| Adoption of drone-enabled ultra-low-volume biological spraying | +1.4% | North America, European Union, China, pilots in Brazil | Medium term (2-4 years) |

| CRISPR-tailored biocontrol strains targeting invasive pests | +1.2% | North America and European Union, frameworks emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Bans on High-Residue Synthetic Pesticides

Heightened maximum-residue-level enforcement is shrinking the chemical toolkit and redirecting crop-protection spending. The Environmental Protection Agency (EPA) 2025 cancellation list removed neonicotinoids and organophosphates that dominated United States corn and soybean programs, creating immediate openings for Bacillus thuringiensis and Metarhizium anisopliae products. The European Union's pesticide regulation establishes Maximum Residue Levels (MRLs) for a broad range of food and feed products. When no specific pesticide limit is defined, a default threshold of 0.01 mg/kg is applied, ensuring minimal allowable residue levels in traded agricultural goods, driving a transition toward biorationals[2]Source: European Commission, EU legislation on maximum residue levels (MRLs), food.ec.europa.eu.

Demand for Residue-Free Produce from Food Retailers

Large grocers have embedded third-party residue testing into supplier contracts. In October 2025, Walmart U.S. revealed plans to eliminate synthetic dyes and several other additives from its private-label food products by 2027. This move reflects a broader shift in both consumer expectations and retailer strategies toward cleaner, more transparent ingredient standards. Comparable standards at Costco and Tesco are cascading downstream to regional distributors. The pressure is acute in berries, leafy greens, and tree fruits that move from harvest to shelf in days, increasing the risk of failure. Early-adopter growers secure wholesale price premiums, and Japan’s tighter import tolerances amplify incentives in Asia-Pacific export hubs.

Government Subsidies for Sustainable Agriculture Tools

Public funding is de-risking adoption by offsetting start-up costs. The USDA Climate-Smart Commodities program will support short-term pilot partnerships to boost the production and sale of climate-friendly commodities. Rural development in the EU is financed under the Common Agricultural Policy through the European Agricultural Fund for Rural Development (EAFRD). The 2021–2027 allocation is approximately €95.5 billion (USD 103.6 billion), with €8.1 billion (USD 9.6 billion) added from the Next Generation EU initiative [3]Source: European Commission, Agriculture and rural development, Recovery plan for Europe, agriculture.ec.europa.eu. Such programs are most generous in regions where chemical restrictions and environmental compliance costs are highest, tipping cost-benefit analyses in favor of biorationals.

Rapid Commercial Success of Microbial Consortia Products

Multi-strain formulations are dispelling efficacy doubts that dogged early biologicals. Microbial biopesticides, particularly those derived from Bacillus and Pseudomonas, are experiencing significant commercial growth due to their effectiveness in pest control and their role in enhancing crop productivity. Research indicates that these biological agents can suppress plant pathogens, promote plant growth, and increase yields through mechanisms such as antibiosis, competition, and the induction of plant resistance. Synergistic interactions among strains improve performance in variable soils, prompting companies to screen for compatibility rather than single-organism optimization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lower field persistence relative to chemicals | -1.3% | Global, intensified in high-ultraviolet and arid zones | Short term (≤ 2 years) |

| Fragmented global registration pathways | -0.9% | Asia-Pacific and Africa, moderate friction in Latin America | Medium term (2-4 years) |

| Shortage of cold-chain infrastructure in emerging markets | -0.7% | Sub-Saharan Africa, Southeast Asia, parts of South America | Medium term (2-4 years) |

| Supply risk for rare botanical actives | -0.6% | Global, concentration in India and East Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lower Field Persistence Relative to Chemicals

Many microbial and botanical actives degrade within days, requiring multiple reapplications and raising operational costs. Bacillus thuringiensis loses half its potency within 72 hours under high solar radiation, compared with two to three weeks of protection from neonicotinoids[4]. Encapsulated Metarhizium spores extended viability, but such technologies are not yet mainstream. Until formulation advances scale, growers in high-ultraviolet geographies will continue to rely on synthetic standards when cost per hectare dictates.

Fragmented Global Registration Pathways

Absence of mutual-recognition accords multiplies dossier costs. A product cleared by the Environmental Protection Agency must be resubmitted to Brazil’s Health Surveillance Agency (ANVISA), India’s Central Insecticides Board, and the European Food Safety Authority (EFSA), each demanding unique data. India’s extra state-level approvals add up to two years, discouraging tailored strain development for local pests. Varying approval timelines and layered regulatory frameworks, particularly in regions requiring additional local or state clearances, can significantly delay market entry. These prolonged and uncertain processes reduce incentives for companies to invest in localized innovation and hinder the creation of solutions tailored to specific pest conditions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Microbial Solutions Drive Market Leadership

Microbial-based solutions generated the largest market share of 52% of 2025 revenue, protecting their dominant position through extensive field data and well-known regulatory pathways. Semiochemical products, although representing a smaller base, are anticipated to register the fastest growth at 19.8% CAGR 2026-2031, as autonomous drones deploy pheromone dispensers across orchards and vineyards. Botanical formulations continue to serve specialty niches that demand zero-day pre-harvest intervals, whereas the “others” category of microbial metabolites and growth regulators captures incremental share as fermentation yields improve.

The shift toward multi-strain products is reshaping competitive benchmarks. Consortia built around Bacillus, Trichoderma, and Streptomyces deliver functional redundancy, ensuring consistent efficacy across acidic and alkaline soils. Semiochemicals leverage precision-application hardware to lower labor cost, unlocking scale in perennial crops. Botanicals remain exposed to supply shocks, and high extraction costs limit penetration in broad-acre cereals. Strategic investment in consortia positioning and drone-compatible pheromone formats will define future winners in the biorationals market.

By Source: Viral Agents Target Resistant Lepidopterans

Bacteria contributed the largest market share, 39% of 2025 revenue, underpinned by industrial-scale fermentation economics and versatility against insects, fungi, and nematodes. Virus-derived agents hold niche status today, yet are anticipated to expand at a fastest rate of 22.3% CAGR during 2026-2031, propelled by clustered regularly interspaced short palindromic repeats (CRISPR) enhanced baculoviruses that overcome pest resistance. Fungal entomopathogens and plant-extract categories retain significant shares but face formulation and regulatory headwinds in certain jurisdictions.

Cell-culture advances are lowering viral production costs, enabling precise control of host-specificity without collateral ecosystem effects. Encapsulation technologies extend fungal spore viability to match standard spray intervals. Plant extracts appeal to certified-organic markets but undergo rigorous toxicology scrutiny in the European Union, inflating time to market. Balanced portfolios spanning bacteria, fungi, and viruses hedge against resistance cycles and regulatory uncertainty, reinforcing portfolio resilience in the biorationals market.

By Crop Type: Specialty Crops Dominate Value Capture

Fruits and vegetables accounted for the largest market share of 46.2% of 2025 revenue as zero-tolerance residue policies in Japan and the European Union elevate biologicals from option to necessity. Oilseeds and pulses are forecast to grow at the fastest rate of 18.4% CAGR from 2026-2031, due to escalating rust and pod borer pressure in South America and Asia-Pacific. Cereals and grains remain slower adopters because lower per-hectare margins limit appetite for repeated sprays, while municipal restrictions on synthetic applications are expanding use in turf and ornamentals.

Specialty-crop growers operating under protected culture rely on controlled-environment parameters to maximize microbial longevity, producing predictable returns that justify premium inputs. Oilseed incentives, particularly government-backed sustainability credits in Brazil and Argentina, accelerate transitions to microbial fungicides. In cereals, the ban on neonicotinoid seed treatments in the European Union nudges growers toward Bacillus firmus nematicide coatings, though widespread shift depends on cost compression. Export-oriented pulses in India and Canada provide another beachhead for the biorationals market.

By Formulation: Liquids Lead but Dry Innovations Gain Ground

Liquid suspension concentrates captured the largest market share of 58% of 2025 sales due to ease of tank mixing and compatibility with standard sprayers. Encapsulation and UV-protective additives are forecast to keep liquids growing at the fastest rate of 17.6% CAGR from 2026-2031. Dry formulations, including wettable powders and water-dispersible granules, cater to seed-treatment and in-furrow niches where controlled release extends microbial persistence.

Encapsulated Metarhizium products demonstrated 10-day field viability in 2025 United States trials, narrowing the efficacy gap with chemicals and improving value perception. Liquids enjoy favorable regulatory treatment in the European Union, where dust-off concerns slow approvals for dry powders. Fertigation-compatible liquids allow simultaneous nutrient and microbial application, a compelling advantage in high-value horticulture. Balanced investment in advanced encapsulation will remain critical for formulators targeting broad-acre segments in the biorationals market.

By Mode of Application: Seed Treatment Surges on Precision Planting

Foliar spray dominated with the largest market share of 63.5% of 2025 revenue due to flexible timing and broad crop compatibility. Seed treatment, however, is projected to outpace all modes with the fastest 20.1% CAGR from 2026 to 2031, as polymer coatings protect microbes from mechanical and thermal stress during planting. Soil treatments find advocates in nematode-infested regions, whereas post-harvest applications grow slowly as retailers eliminate fungicide residues from the cold-chain supply.

Variable-rate planters equipped with microbial injectors align seed treatment rates with soil microbiome data, reducing cost per hectare and enhancing stand establishment. Drone-guided foliar programs lower input volumes by targeting pest hotspots, and in-furrow liquid systems retrofit easily onto conservation-tillage equipment. Post-harvest yeast and bacterial coatings that suppress storage molds are gaining traction in export-oriented fruit chains, rounding out multi-stage protection strategies in the expanding biorationals market.

Geography Analysis

North America remains the largest revenue share at 44% in 2025 and has shown strong momentum toward sustainable agriculture, driven by tightening regulatory oversight on chemical pesticides and increased public funding for environmentally friendly farming practices. In parallel, the U.S. Environmental Protection Agency continues to promote and regulate safer alternatives, such as biopesticides, while the United States Department of Agriculture has committed significant funding to conservation and regenerative agriculture initiatives that encourage reduced chemical inputs.

Europe is growing due to its crop protection landscape, which is increasingly shaped by stringent pesticide regulations and sustainability policies within the European Union. Germany and France spearhead adoption through organic-farming mandates and retailer residue clamps. Weeds remain a major constraint on crop yields and can negatively affect ecosystems and human health, while concerns over the environmental and regulatory impacts of synthetic herbicides continue to rise. Consequently, Agroecological Weed Management (AWM) is emerging as a sustainable alternative that relies on ecological principles and reduced chemical use. While botanical-extract dossiers face longer European Food Safety Authority reviews, companies that front-load toxicology data secure first-mover advantages.

Asia-Pacific is the fastest-growing region at 15.4% CAGR from 2026 to 2031, as China has announced major agricultural initiatives as part of its 15th Five-Year Plan for 2026–2030, while India’s organic acreage reached 4.2 million hectares. China aims to reduce pesticide use on fruits and vegetables by 10% in the coming years. India wrestles with fragmented state approvals that slow launches, yet national residue-free export ambitions drive adoption in pulses and spices. Cold-chain shortages still constrain microbial shelf life in Southeast Asia, creating space for locally fermented products and room-temperature stable botanicals.

Competitive Landscape

The top five players controlled the global revenue in 2025, signaling moderate concentration and ample scope for regional specialists. Multinational agrochemical companies such as Sumitomo Biorational Company LLC (Valent BioSciences), Bayer AG, Syngenta Crop Protection AG, BASF, and Corteva Agriscience embed predictive-disease algorithms into digital platforms that recommend optimal biological spray windows, improving return on investment for risk-averse row-crop growers. Smaller innovators like Vestaron and Biobest focus on high-margin greenhouse niches where controlled climates extend microbial persistence and justify premium prices.

Sumitomo Biorational Company LLC (Valent BioSciences) is enhancing the market by delivering highly effective biological solutions for vector control, particularly mosquito management. Its eco-friendly, proprietary formulations are accelerating the transition from conventional chemical pesticides to more sustainable alternatives. The U.S. Environmental Protection Agency's authorization of RNAi-based solutions such as ledprona signals a significant shift in the biorationals market, bringing highly precise, next-generation pest control technologies.

Overall, the market is being shaped by consolidation, strategic alliances, and innovation driven by intellectual property, as companies compete to develop safer, more effective, and regulation-compliant biological alternatives to conventional chemical pesticides. Growing regulatory requirements and sustainability goals are also speeding up the transition toward bio-based solutions across key agricultural regions. In addition, partnerships between large agrochemical firms, biotech companies, and research organizations are playing a vital role in advancing product development and enabling large-scale commercialization.

Biorationals Industry Leaders

Bayer AG

Syngenta Crop Protection AG

BASF

Corteva Agriscience

Sumitomo Biorational Company LLC (Valent BioSciences)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Sumitomo Biorational, MGK, and Valent North America have announced plans to merge into a single entity, Sumitomo Biorational Company LLC, which will be established in April 2026 as part of Sumitomo Chemical Company. The new organization, headquartered in Libertyville, will function as a global center dedicated to advancing biorational innovation.

- February 2025: Sustainable agriculture is set to advance through a new global partnership between Syngenta Crop Protection and Ceres Biotics. The collaboration focuses on delivering innovative biological solutions to farmers worldwide.

- June 2024: Bayer AG aims to launch around ten major innovations over the next decade, backed by a strong R&D pipeline with potential peak sales exceeding Euros 32 billion (USD 37.7 billion). The portfolio includes next-generation solutions in herbicides, biotech-enhanced crops, and advanced insect and pest control technologies.

- April 2024: Bayer AG is working toward introducing its first biological insecticide for arable farming. Through a new partnership with AlphaBio Control, Bayer has secured exclusive marketing rights for this innovative product, designed to help farmers manage crop pests more sustainably. The product is anticipated to be launched by 2028.

Global Biorationals Market Report Scope

Biorationals are pest management products derived from natural or biological sources that target specific pests with minimal impact on humans, animals, and the environment. They include biopesticides, biostimulants, pheromones, and plant-based extracts used in sustainable agriculture. The biorationals market report is segmented by product type (microbial-based, botanical-based, semiochemical-based, and other product types), by source (bacteria, fungi, viruses, plant extracts, and biochemical semiochemicals), by crop type (cereals and grains, fruits and vegetables, oilseeds and pulses, and other crop types), by formulation (liquid and dry), by mode of application (foliar spray, seed treatment, soil treatment, and post-harvest), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Microbial-based |

| Botanical-based |

| Semiochemical-based |

| Other Product Types |

| Bacteria |

| Fungi |

| Viruses |

| Plant Extracts |

| Biochemical Semiochemicals |

| Cereals and Grains |

| Fruits and Vegetables |

| Oilseeds and Pulses |

| Other Crop Types |

| Liquid |

| Dry |

| Foliar Spray |

| Seed Treatment |

| Soil Treatment |

| Post-harvest |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Product Type | Microbial-based | |

| Botanical-based | ||

| Semiochemical-based | ||

| Other Product Types | ||

| By Source | Bacteria | |

| Fungi | ||

| Viruses | ||

| Plant Extracts | ||

| Biochemical Semiochemicals | ||

| By Crop Type | Cereals and Grains | |

| Fruits and Vegetables | ||

| Oilseeds and Pulses | ||

| Other Crop Types | ||

| By Formulation | Liquid | |

| Dry | ||

| By Mode of Application | Foliar Spray | |

| Seed Treatment | ||

| Soil Treatment | ||

| Post-harvest | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the market size of biorationals market and at what CAGR it is anticipated to grow?

The biorationals market size was valued at USD 10.68 billion in 2026 to reach USD 19.93 billion by 2031, registering a CAGR of 13.3% during the forecast period (2026-2031).

Which product category is growing the fastest within biological crop protection?

Semiochemical solutions are projected to expand at 19.8% CAGR from 2026-2031 as drones and autonomous sprayers slash labor involved in pheromone deployment.

How significant is seed-treatment adoption for biorationals?

Seed treatment is the fastest-growing application mode at a 20.1% CAGR from 2026-2031, aided by polymer coatings that shield microbes during variable-rate precision planting.

Why is Asia-Pacific emerging as the highest-growth region?

China aims to reduce pesticide use on fruits and vegetables by 10% in the coming years.

What challenges restrain broader uptake of biologicals in cereals and grains?

Short residual activity raises per-hectare costs, and fragmented registration pathways add multi-year lags, deterring investment where commodity margins are thin.

Which technological advances could reshape competitive dynamics?

CRISPR-edited microbes, RNA-interference platforms, and AI-guided ultra-low-volume sprayers promise targeted control, lower volumes, and faster regulatory acceptance, favoring firms that integrate biology with hardware and data analytics.

Page last updated on: