Bio Decontamination Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

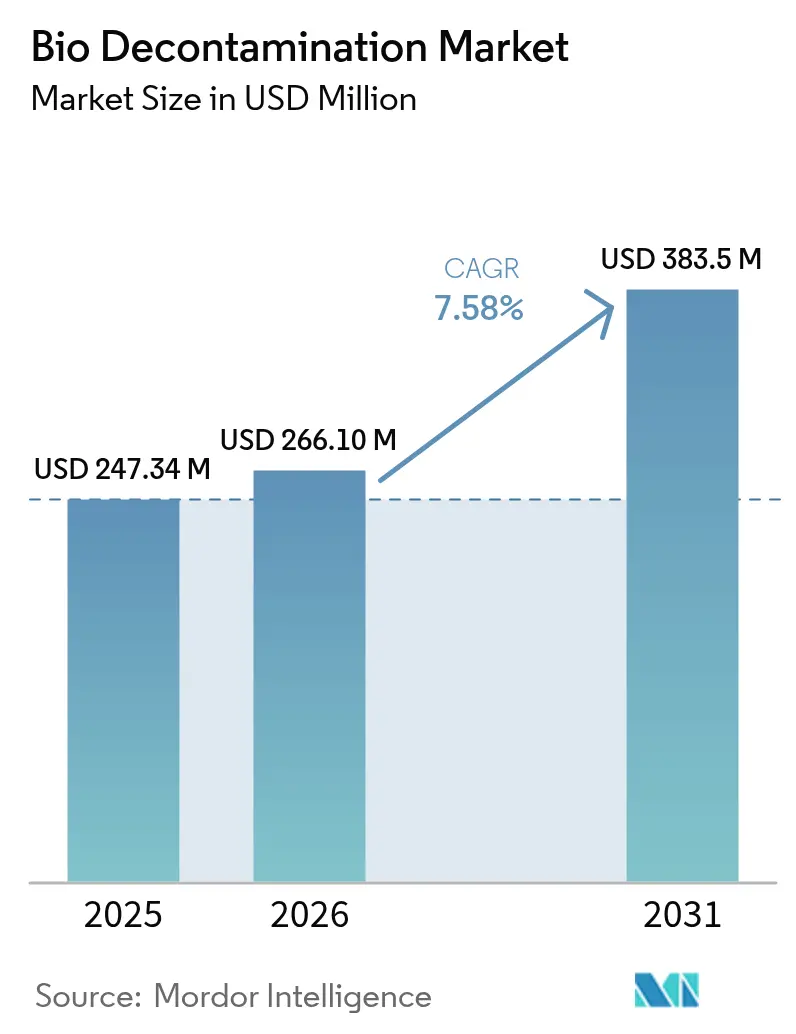

| Market Size (2026) | USD 266.1 Million |

| Market Size (2031) | USD 383.5 Million |

| Growth Rate (2026 - 2031) | 7.58% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bio Decontamination Market Analysis by Mordor Intelligence

The bio decontamination market size was valued at USD 247.34 million in 2025 and estimated to grow from USD 266.1 million in 2026 to reach USD 383.5 million by 2031, at a CAGR of 7.58% during the forecast period (2026-2031). Increased awareness of healthcare-associated infections, regulatory endorsement of vaporized hydrogen peroxide, and investments in biologics manufacturing underpin the current expansion phase of the bio decontamination market. Equipment purchases dominate capital cycles as pharmaceutical producers replace ethylene oxide systems, while consumables gain momentum through the recurring nature of decontamination workflows. North American leadership rests on stringent standards and sustained healthcare spending, but Asia-Pacific’s rapid manufacturing build-out is generating the fastest incremental revenue. Competitive intensity remains moderate, with established suppliers leveraging global service networks and emerging firms introducing hybrid hydrogen peroxide and binary ionization platforms to address material compatibility and cycle-time concerns.

Key Report Takeaways

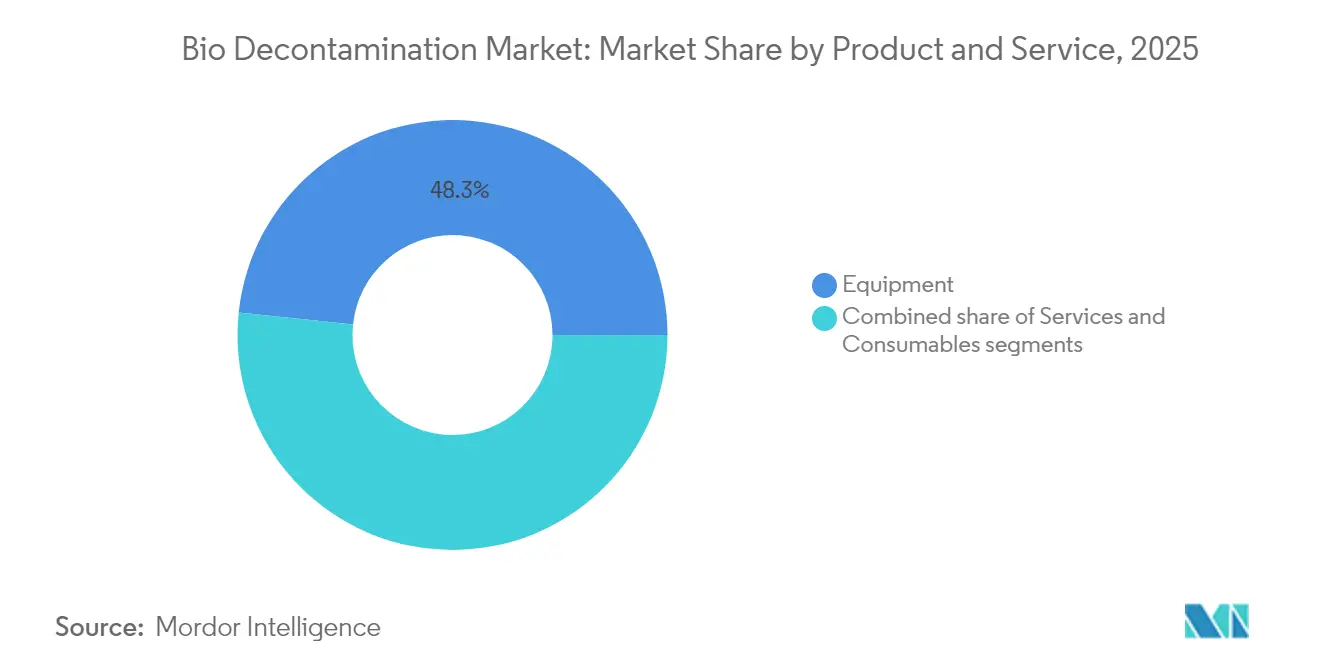

- By product and service, equipment led with 48.33% revenue share in 2025, while consumables are projected to register a 9.10% CAGR to 2031.

- By agent type, hydrogen peroxide held 50.72% of the bio decontamination market share in 2025 and peracetic acid is forecast to expand at an 8.31% CAGR to 2031.

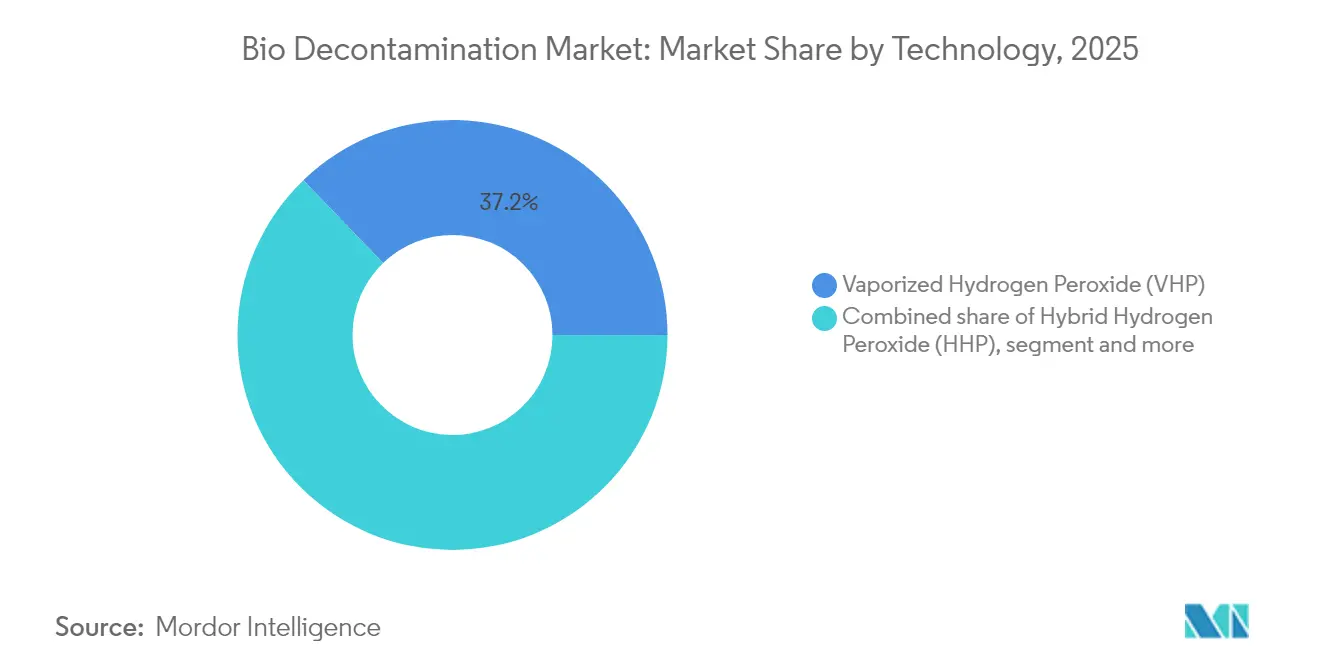

- By technology, vaporized hydrogen peroxide accounted for 37.20% of the bio decontamination market size in 2025 and hybrid hydrogen peroxide is advancing at an 8.55% CAGR through 2031.

- By end user, pharmaceutical and medical-device manufacturers controlled 45.88% revenue in 2025, while life-science research organizations are set to grow at a 9.22% CAGR to 2031.

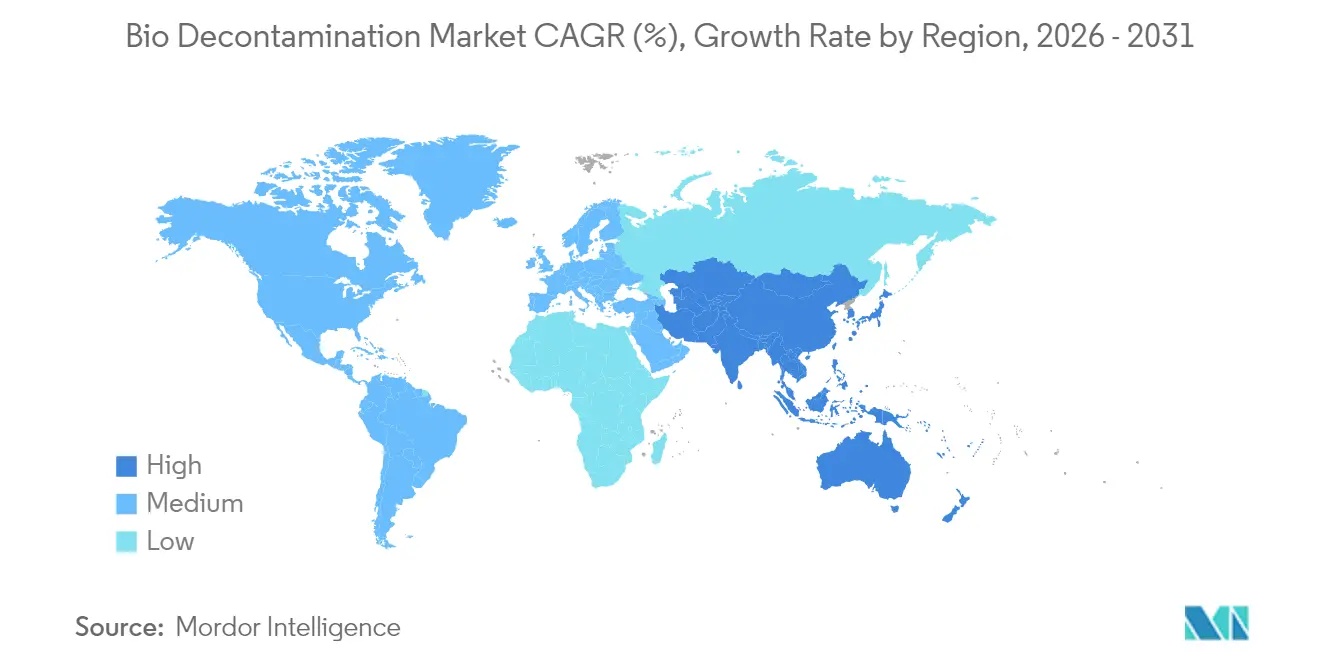

- By region, North America dominated with 41.96% revenue in 2025, whereas Asia-Pacific is predicted to rise at a 9.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bio Decontamination Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of hospital-acquired infections | +1.8% | Global, with higher impact in North America & Europe | Medium term (2-4 years) |

| Growing number of surgical procedures worldwide | +1.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Stringent sterility regulations in pharma manufacturing | +2.1% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Increasing outsourcing of bio-decontamination services | +1.2% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Adoption in ATMP & cell-gene therapy cleanrooms | +0.9% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| Rapid-turnaround biothreat response in aerospace & defense sites | +0.4% | North America, selective European markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Hospital-Acquired Infections

Hospital-acquired infections affect millions of patients each year, with German facilities losing EUR 1,000 per avoidable case, which places direct financial pressure on administrators to upgrade environmental hygiene.[1]BMC Infectious Diseases, “Economic Burden of Nosocomial Infections in German Hospitals,” biomedcentral.com The emergence of Klebsiella pneumoniae ST307, tolerant of 70% of standard biocides, underscores the need for more potent decontamination technologies. Proposed USD 240 million cuts to the US Hospital Preparedness Program would reduce staffing for manual cleaning, which in turn encourages automated no-touch systems that maintain compliance with lean personnel models. The Joint Commission’s 2024 standards emphasize surface cleaning in patient areas, sparking immediate demand for mobile vaporized hydrogen peroxide generators.[2]The Joint Commission, “Revised Infection Prevention and Control Standards,” jointcommission.org In the United Kingdom, NHS England’s 2025 cleanliness benchmarks set rigorous environmental targets that require validated bio decontamination solutions. The CDC’s updated surface disinfection guidance positions environmental services as a core element of safety culture, making automated bio decontamination a strategic investment.

Growing Number of Surgical Procedures Worldwide

Global surgical volumes continue to climb, and each procedure generates multiple instrument reprocessing cycles that rely on dependable decontamination. STERIS reported 14% healthcare service revenue growth in fiscal 2024, largely attributed to higher operating-room throughput. Adoption of minimally invasive techniques raises demand for low-temperature sterilization that protects delicate polymeric components. The FDA’s clearance of vaporized hydrogen peroxide for 3D-printed surgical guides removes a regulatory barrier for personalized implants. Outpatient centers, which hinge on rapid instrument turnover, are installing compact units that finish cycles in under 30 minutes, thus cutting patient wait times. Ageing populations in developed countries guarantee continuing growth in elective interventions, while emerging markets accelerate surgery installations to meet basic healthcare needs. The proliferation of robotic surgery platforms increases the volume and complexity of reusable tools, strengthening the outlook for the bio decontamination market.

Stringent Sterility Regulations in Pharma Manufacturing

The European Union enforced revised GMP Annex 1 in 2024, mandating continuous 5 µm particle monitoring in Grade A and B areas, a change that compels facilities to install integrated decontamination and monitoring packages. Annex 2 now details contamination-control expectations for cell and gene therapies, driving purchases of specialized vaporized hydrogen peroxide isolators. The FDA aligned domestic oversight with Annex 1, creating a unified global compliance requirement that accelerates equipment upgrades inside US biologics plants. Environmental targets related to energy, water, and chemical stewardship promote hydrogen peroxide and peracetic acid, which decompose into benign byproducts. Continuous manufacturing lines favor periodic, automated decontamination that operates without halting production, supporting hybrid hydrogen peroxide systems designed for fast recreation of sterile conditions. Regulatory agencies move toward AI-enabled inspection analytics, increasing demand for decontamination solutions that automatically record every parameter required for audit trails.

Increasing Outsourcing of Bio Decontamination Services

Contract manufacturers are expected to manage 54% of world biologics capacity by 2028, centralizing demand for validated decontamination into a relatively small cohort of facilities.[3]Pharmaceutical Technology, “CMO Share of Global Biologics Capacity,” pharmaceutical-technology.com The biopharmaceutical CMO market reached USD 19.89 billion in 2023, with process development services capturing 34.7% share, reflecting the willingness of sponsors to outsource complex contamination-control operations. Asia-Pacific CMOs expanded floor space rapidly, yet must comply with EU and US sterility rules, stimulating orders for turnkey bio decontamination contracts that include training and documentation. Ecolab’s USD 950 million sale of its surgical solutions line in 2024 freed capital to intensify focus on infection-prevention services, including on-site decontamination programs. Small and mid-sized pharma firms prefer operating-expense models and leverage service providers to gain immediate access to high-specification equipment. The complexity of monoclonal antibody suites reinforces the trend, as contamination events can jeopardize entire commercial campaigns, making outsourced decontamination insurance indispensable.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced equipment | -1.4% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Budgetary constraints in healthcare facilities | -1.1% | Global, acute in resource-limited settings | Medium term (2-4 years) |

| Material-compatibility & safety concerns with chemical agents | -0.8% | Global, regulatory focus in North America & Europe | Long term (≥ 4 years) |

| Lack of standardized validation for large biologics suites | -0.6% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Equipment

A hydrogen peroxide vapor system can list at EUR 50,000, whereas aerosolized alternatives often cost under EUR 10,000, challenging small hospitals that operate on modest capital budgets. The transition away from ethylene oxide further inflates budgets by triggering validation studies and workforce retraining. Healthcare administrators must prioritize among competing investments, and decontamination may rank below imaging equipment when funds are tight. Validation for specialty products such as prefilled syringes adds laboratory costs that raise the total cost of ownership beyond sticker price. Emerging markets face currency volatility that magnifies imported capital-equipment expenses. Finally, complex systems need skilled maintenance, and a shortage of local technicians can extend downtime and increase lifetime costs.

Budgetary Constraints in Healthcare Facilities

A benchmarking study of inpatient cost frameworks showed wide variation in environmental-service spending, revealing a structural hurdle for uniform decontamination adoption. Potential elimination of federal preparedness funding in the United States risks delaying equipment replacement cycles, even as infection-prevention requirements tighten. Resource-limited hospitals often lack robust cleaning protocols and staff training, making sophisticated decontamination technology difficult to justify. Extended patient stays caused by infections reduce day-to-day revenue, compounding the capital-shortage problem. Public facilities in emerging regions must spread scarce funds across basic diagnostic and treatment needs, so automated systems remain aspirational. Reimbursement models now require demonstrable clinical and financial returns, and economic data on bio decontamination is still limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product and Service: Equipment Dominance Drives Capital Cycles

Equipment captured 48.33% of 2025 revenue in the bio decontamination market, underscoring how capital assets remain the backbone of contamination-control strategies. Large pharmaceutical plants adopt fixed vaporized hydrogen peroxide chambers to replace aging ethylene oxide units, spurred by the FDA’s 2024 Category A recognition that lowered regulatory uncertainty. Service revenues grow as hospitals and contract manufacturers embrace leasing models that bundle preventive maintenance and consumable supply, reducing up-front expenditure. Consumables, including hydrogen peroxide cartridges and single-use delivery nozzles, are growing at a 9.10% CAGR because higher cycle frequencies are mandated by stricter cleaning protocols. Integrated asset-as-a-service agreements, which guarantee uptime and include remote performance monitoring, are reshaping vendor–customer relationships by shifting risk toward suppliers. The bio decontamination market continues to see OEMs diversify into managed-service tiers that provide validation support and regulatory documentation. Over the forecast horizon, equipment suppliers will concentrate on modular systems that fit within pre-fabricated cleanrooms, cutting installation time for greenfield biologics facilities. Service providers are also incorporating digital twins that simulate chamber performance, which helps operators plan maintenance windows without disrupting production. Sustainability metrics drive interest in reclaim systems that reduce hydrogen peroxide consumption, ensuring future growth in both consumable and upgrade kits.

Consumables benefit from varied end-user segments, including pharmacies that run daily instrument cycles and biosafety laboratories that decontaminate high-risk agents. The increase in turnaround frequency directly feeds volume demand for single-use spray heads and catalyzers, making consumables the fastest contributor to incremental revenue. In emerging geographies, distributors bundle consumables with remote validation software to overcome staff shortages, allowing facilities to meet EU GMP standards without owning advanced analytic tools. The bio decontamination market is therefore experiencing a gradual shift in revenue mix toward recurring streams, a trend likely to accelerate as more hospitals outsource non-core processes. Over the next five years, equipment renewals will peak as ethylene oxide is phased down, after which consumable and service revenue will form the bulk of vendor cash flow. Overall, the combined trajectory of equipment and consumables keeps the bio decontamination market on a stable multi-year expansion path.

By Agent Type: Hydrogen Peroxide Leadership Faces Peracetic Acid Challenge

Hydrogen peroxide retained 50.72% bio decontamination market share in 2025, supported by decades of efficacy data and broad regulatory acceptance. Its decomposition into water and oxygen aligns with corporate sustainability goals, encouraging adoption across pharmaceutical, medical device, and hospital settings. Enhanced efficacy against resistant spores sustains its popularity, and innovation in plasma-activated water boosts kill rates while retaining material compatibility. However, peracetic acid, posting an 8.31% CAGR, is gaining ground due to environmental credentials and strong performance in surface applications, including advanced oxidation for wastewater treatment that aligns with zero-liquid-discharge policies. Chlorine dioxide maintains relevance for whole-facility fumigation, particularly during refurbishments when large volumes must be treated quickly. Nitrogen dioxide sterilization, operating at room temperature and low concentrations, shows promise for complex combination products that cannot tolerate heat, radiation, or high humidity. The others category, featuring ozone and hypochlorous acid, caters to niche applications yet faces stability issues limiting mainstream use.

Emerging agents battle established incumbents on the axes of cycle time, residue, and material compatibility. Peracetic-acid blends combined with surfactants achieve shorter contact times, making them attractive for high-throughput hospitals. Research in plasma-enhanced hydrogen peroxide underscores the agent’s flexibility as operators can dial concentrations to match bioburden without harming sensitive plastics, extending its leadership position. Combination chemistries such as chlorine dioxide with UV-C aim to deliver rapid kill in high-volume instrument reprocessing units, although cost remains a barrier. Future market share shifts will hinge on regulatory acceptance for novel agents and demonstration of consistent efficacy in real-world conditions. Vendors that can validate multi-agent platforms gain a competitive edge, appealing to facilities that must decontaminate diverse substrates under a single quality system. Overall, intense innovation ensures that the bio decontamination market will remain technologically dynamic, with hydrogen peroxide’s dominance challenged but not yet displaced.

By Technology: Vaporized Hydrogen Peroxide Dominance Challenged by Hybrid Innovations

Vaporized hydrogen peroxide technology accounted for 37.20% of 2025 revenue in the bio decontamination market and continues to benefit from extensive validation files covering an array of industries. The dry-vapor approach forms sub-micron droplets that reach shadowed surfaces without leaving corrosive residues, a property valued in cleanrooms filled with sensitive sensors. Gas plasma systems, though mature, maintain a niche for heat-sensitive laparoscopic tools, aided by CDC guidance confirming compatibility with 95% of tested devices. Hybrid hydrogen peroxide platforms, combining fine-mist delivery with catalytic conversion, are the fastest movers at an 8.55% CAGR, offering cycle times under 20 minutes while mitigating condensation risks. Cold atmospheric plasma is emerging for food and packaging decontamination, widening addressable opportunities for technology vendors. UVC LED arrays deliver rapid surface disinfection in waste handling areas, though limited penetration confines them to adjunct roles.

Artificial-intelligence modules embedded in next-generation chambers monitor humidity, temperature, and peroxide concentration in real time, automatically adjusting parameters to remove human error. Integration with building management systems enables remote safety interlocks that shut down HVAC when decontamination begins, which satisfies Annex 1 demands for traceable environmental controls. Micro-sensor networks track residuals to certify readiness for re-entry, minimizing downtime in high-value biologics suites. Hybrid systems also appeal to contract manufacturers who must juggle varying material types across client portfolios, thus driving unit shipments. US government initiatives to replace ethylene oxide add momentum, as hybrid hydrogen peroxide shows comparable sterility assurance levels without producing hazardous ethylene chlorohydrin byproducts. Long term, technology portfolios that combine speed, documentation, and environmental compliance will dominate procurement lists, shaping the competitive rhythm of the bio decontamination market.

By End User: Pharma Manufacturing Leads, Life Sciences Accelerates

Pharmaceutical and medical-device producers held 45.88% revenue in 2025, reflecting stringent GMP mandates that prioritize validated decontamination pathways. Cell and gene therapy suites, which involve manual interventions, rely on automated vaporized hydrogen peroxide isolators to mitigate operator-borne contamination. Hospitals remain sizeable customers because growing surgical caseloads and tighter accreditation rules drive replacement of manual cleaning with no-touch systems. Life-science and biotechnology research organizations are advancing at a 9.22% CAGR as venture capital funds pour into novel modalities, each demanding aseptic work environments.

Dedicated aerospace and defense facilities splash a small yet strategic revenue pool, requesting rapid-turnaround systems to support biothreat response. Contract manufacturers support blockbuster monoclonal antibodies and vaccine campaigns, creating steady order flow for both fixed chambers and mobile units. Increasing prevalence of decentralized manufacturing centers for advanced therapies spreads adoption into secondary geographies, widening the bio decontamination market. Research incubators need flexible, bench-top chambers that scale with laboratory growth, which presents a new sales channel for niche suppliers. The broader healthcare shift toward outpatient procedures requires compact units that fit ambulatory surgery centers, further diversifying the end-user matrix and reinforcing healthy demand.

Geography Analysis

North America commanded 41.96% revenue in 2025, anchored by the United States where FDA guidance and ANSI/AAMI ST24 revisions spur steady equipment upgrades. Federal recognition of vaporized hydrogen peroxide as Category A reduced regulatory friction, enabling faster procurement cycles for device manufacturers. Canada adopts similar frameworks, while Mexico’s grow-your-own drug-manufacturing initiatives add base-load demand for mid-tier chambers. The region also benefits from consolidation among hospital systems, which standardize equipment lists and negotiate multi-site service contracts, supporting predictable pull-through of consumables.

Asia-Pacific is the fastest-growing territory, posting a 9.98% CAGR to 2031, driven by Chinese and Indian biologics expansions, as well as supply-chain realignments prompted by the 2024 US Biosecure Act. Indian CDMOs, which handled USD 15.63 billion work orders in 2023, must now demonstrate US-equivalent sterility compliance, propelling orders for hybrid hydrogen peroxide suites. Japan and South Korea allocate national R&D budgets toward biopharmaceutical innovation, fueling decontamination spend in pilot and commercial facilities. Australia’s Therapeutic Goods Administration demands rigorous sterility dossier submissions, encouraging early adoption of AI-infused validation software bundled with chambers.

Europe posts stable mid-single-digit growth, heavily influenced by Annex 1 and Annex 2 enforcement. Germany’s pharmaceutical cluster around Frankfurt invests in advanced airborne decontamination for continuous production lines, while the United Kingdom’s biotech hubs leverage venture funding to install modular cleanrooms equipped with VHP generators. Southern European nations catch up on infection-control modernizations, focusing on public hospital refurbishments where chlorine dioxide fumigation reduces refurbishment downtime. The Middle East and Africa region remains nascent but benefits from GCC government programs targeting premium healthcare infrastructure. South America, led by Brazil, gradually adopts hydrogen peroxide systems to align with WHO infection-prevention goals, though fiscal constraints slow rollout. The geographic spread ensures multi-vector growth, safeguarding the long-term trajectory of the bio decontamination market.

Competitive Landscape

Market concentration is moderate, with the top five players accounting for roughly 45% of global revenue, which leaves ample room for specialized challengers. STERIS recorded 6% topline expansion in fiscal 2025, supported by double-digit service growth and the rollout of hyper-cycle VHP chambers. Ecolab divested its surgical solutions unit to focus on infection prevention, freeing capital to scale its Bioquell VHP service network. Getinge expanded its bioprocess footprint through acquisitions of High Purity New England and Healthmark, broadening its portfolio of filtration and compliance consumables. TOMI Environmental Solutions secured a USD 450,000 custom system contract at a Rhode Island university and earned Disinfection and Decontamination Products Company of the Year 2025, highlighting its competitive rise. Sonata Scientific introduced an ethylene oxide abatement platform that reaches 99% destruction efficiency, positioning itself for facilities that cannot yet abandon ethylene oxide but must meet emission ceilings.

Strategic moves center on capacity expansion, portfolio diversification, and regulatory positioning. Vendors bundle digital validation suites to satisfy Annex 1 traceability, an edge that pure-play equipment suppliers struggle to match. Partnerships with CMO networks give established brands recurring service revenue and early access to new facility projects. Sustainability pledges push competitors to advertise low-energy cycles and biodegradable consumables, resonating with ESG-oriented investors. In emerging markets, suppliers establish local training academies to ease skill shortages and reduce downtime, supporting customer retention. R&D pipelines focus on hybrid delivery formats and real-time residual monitoring, key differentiators in bids for high-value biologics lines. Overall, moderate concentration coexists with active innovation, shaping an environment where niche advances can secure profitable niches before incumbents counter.

Bio Decontamination Industry Leaders

Ecolab

JCE Biotechnology

Zhejiang Tailin Bioengineering Co., Ltd.

Steris Plc

Tomi Environmental Solutions Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sonata Scientific unveiled the Helios MP500 ethylene oxide control technology, reaching 99% destruction efficiency and scheduling initial unit deployment in July 2025.

- March 2025: TOMI Environmental Solutions secured a USD 450,000 contract for a SteraMist Custom Engineered System at a Rhode Island university, extending its footprint among New England biotech institutions.

- September 2024: US Congress passed the Biosecure Act, restricting federal contracts with Chinese biotech firms and opening opportunities for Indian contract manufacturers.

- January 2024: The FDA designated vaporized hydrogen peroxide as an Established Category A sterilization method for medical devices, reducing regulatory barriers to adoption.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the biodecontamination market as all equipment, consumables, and contracted services that use chemical or hybrid physical-chemical agents, most notably vaporized or hybrid hydrogen peroxide, chlorine dioxide, peracetic acid, and nitrogen dioxide, to eliminate microbial loads in cleanrooms, isolators, critical hospital spaces, and life-science production suites. Revenues reflect new system sales, single-use consumables, and fee-based room or facility cycles executed for end users during 2025.

Scope exclusion: routine manual wipe-downs employing generic hospital disinfectants are outside this market.

Segmentation Overview

- By Product and Service

- Equipment

- Services

- Consumables

- By Agent Type

- Hydrogen Peroxide

- Chlorine Dioxide

- Peracetic Acid

- Nitrogen Dioxide

- Others

- By Technology

- Vaporized Hydrogen Peroxide (VHP)

- Hybrid Hydrogen Peroxide (HHP)

- Gas Plasma

- Others

- By End User

- Pharmaceutical and Medical-Device Manufacturing Companies

- Life-Sciences and Biotechnology Research Organizations

- Hospitals and Healthcare Facilities

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed validation engineers at pharmaceutical fill-finish plants, infection-control nurses in tertiary hospitals, regional sterilization service providers, and North American as well as Asia Pacific regulators. These discussions clarified true cycle pricing, agent consumption rates, and adoption hurdles, letting us adjust desk-derived figures and stress-test key assumptions.

Desk Research

Mordor analysts began with public datasets that quantify potential demand pools, such as WHO hospital-acquired infection incidence, FDA 483 sterility citations, UN Comtrade exports of hydrogen peroxide generators, and Eurostat surgical procedure volumes. Industry bodies, including ISPE, Parenteral Drug Association, and the International Confederation of Contamination Control Societies, provided guidance on standard cycle frequencies and validated kill log targets. Company 10-Ks and selected filings on D&B Hoovers outlined installed cleanroom footprints and typical replacement cycles, while Dow Jones Factiva news searches helped flag recent capacity additions. This list is illustrative rather than exhaustive; many additional open and paid references informed our desk work.

Market-Sizing & Forecasting

A top-down demand pool was built from cleanroom square meter inventories, surgical theater counts, and average decontamination cycle schedules, which are then priced using blended ASPs supplied during interviews. Select bottom-up checks, supplier revenue roll-ups and shipment snapshots from Volza, were layered in to reconcile totals. Core variables tracked include annual HAI incidence, new biotech plant completions, hydrogen peroxide spot prices, regulatory audit frequency, and typical cycle duration; these shape both current size and elasticity. Multivariate regression with lagged HAI data and plant build-outs drives our 2025-2030 projection, and scenario analysis frames upside from stricter Annex 1 enforcement. Data gaps in supplier revenues were bridged with modest usage rate proxies rather than speculative extrapolations.

Data Validation & Update Cycle

Outputs pass anomaly checks against independent infection and capex benchmarks, followed by peer review and a lead analyst sign-off. Models refresh annually, with interim tweaks triggered by material events, such as major recalls and new GMP rules; a last-mile sanity pass is run right before report publication.

Why Mordor's Bio Decontamination Baseline Commands Reliability

Published estimates often differ because firms pick dissimilar scopes, agent baskets, and refresh cadences.

Key gap drivers include divergent inclusion of service revenues, varying ASP inflation paths, and whether retrofit sales are counted or not. Mordor anchors on a cycle-level revenue view, applies quarterly FX updates, and revisits usage assumptions with practitioners every year, thereby reducing stale data risk.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 247.3 M (2025) | Mordor Intelligence | - |

| USD 219.9 M (2025) | Global Consultancy A | Excludes consumables; uses static ASPs |

| USD 241.5 M (2024) | Industry Association B | Counts equipment only; no service cycles |

| USD 238.0 M (2023) | Trade Journal C | Older base year; single region demand uplift |

Taken together, the comparison shows that once all revenue streams and the latest plant build-outs are folded in, Mordor's figure provides a balanced, transparent baseline that decision makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size and expected growth rate of the bio decontamination market?

The market is valued at USD 266.1 million in 2026 and is forecast to reach USD 383.5 million by 2031, advancing at a 7.58% CAGR.

Which product category generates the most revenue and which grows the fastest?

Equipment accounts for 48.33% of 2025 revenue, while consumables post the highest growth with a 9.10% CAGR to 2031.

Which recent regulatory decisions are accelerating adoption of new decontamination technologies?

In January 2024 the FDA classified vaporized hydrogen peroxide as an Established Category A sterilization method, cutting barriers to ethylene-oxide alternatives.

Which is the fastest growing region in Bio Decontamination Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which geographic region is expanding the quickest and why?

Asia-Pacific shows a 9.98% CAGR through 2031, propelled by Chinese and Indian pharmaceutical capacity build-outs and supply-chain diversification after the 2024 US Biosecure Act.

What technologies are gaining traction as replacements for ethylene oxide sterilization?

Vaporized and hybrid hydrogen peroxide systems are leading substitutes because they combine rapid cycles, broad material compatibility, and growing regulatory acceptance.

Page last updated on: