Global Industrial Microbiology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

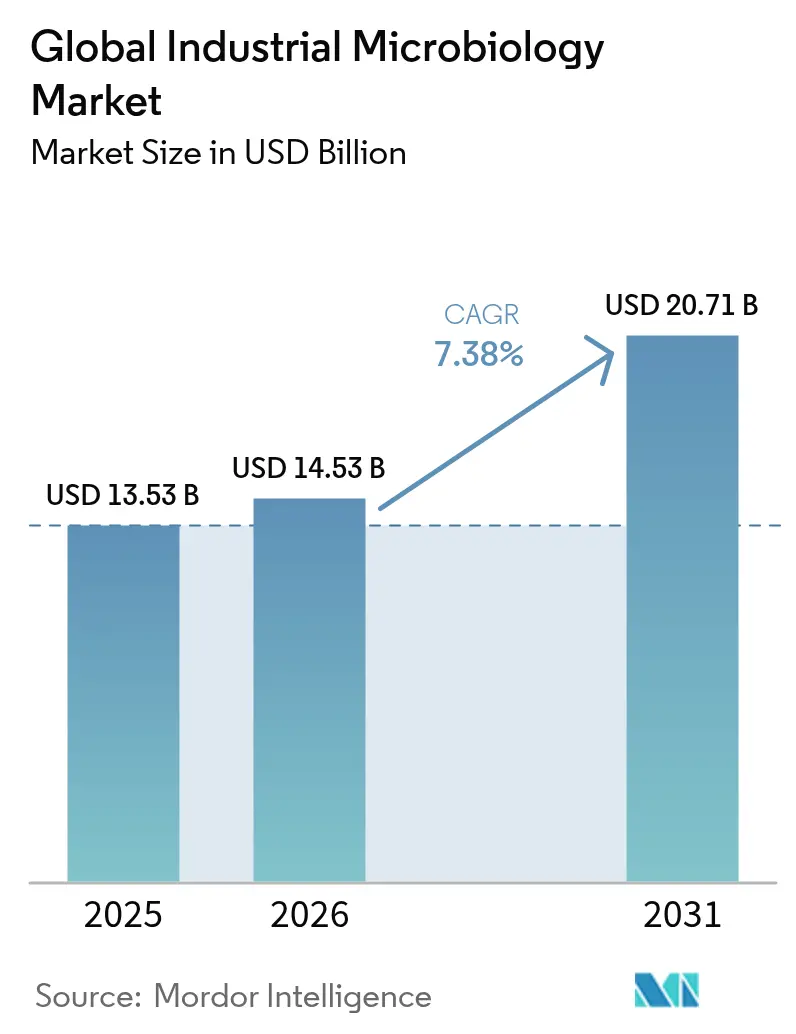

| Market Size (2026) | USD 14.53 Billion |

| Market Size (2031) | USD 20.71 Billion |

| Growth Rate (2026 - 2031) | 7.38% CAGR |

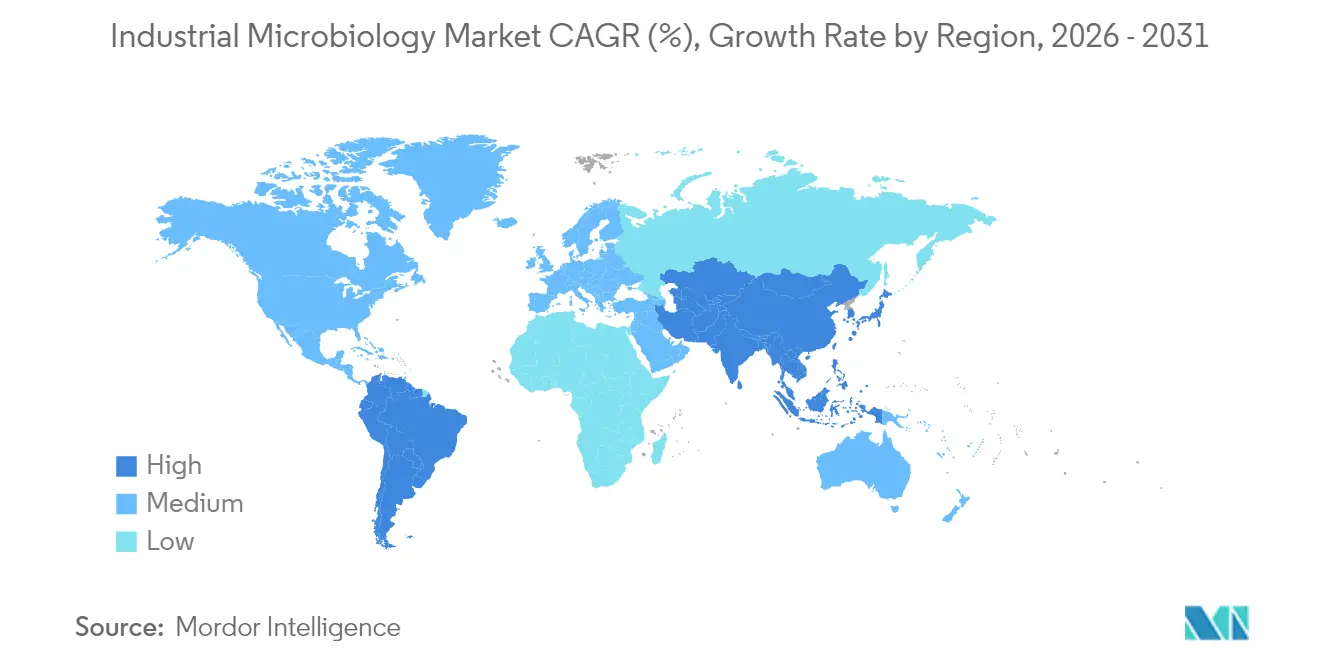

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

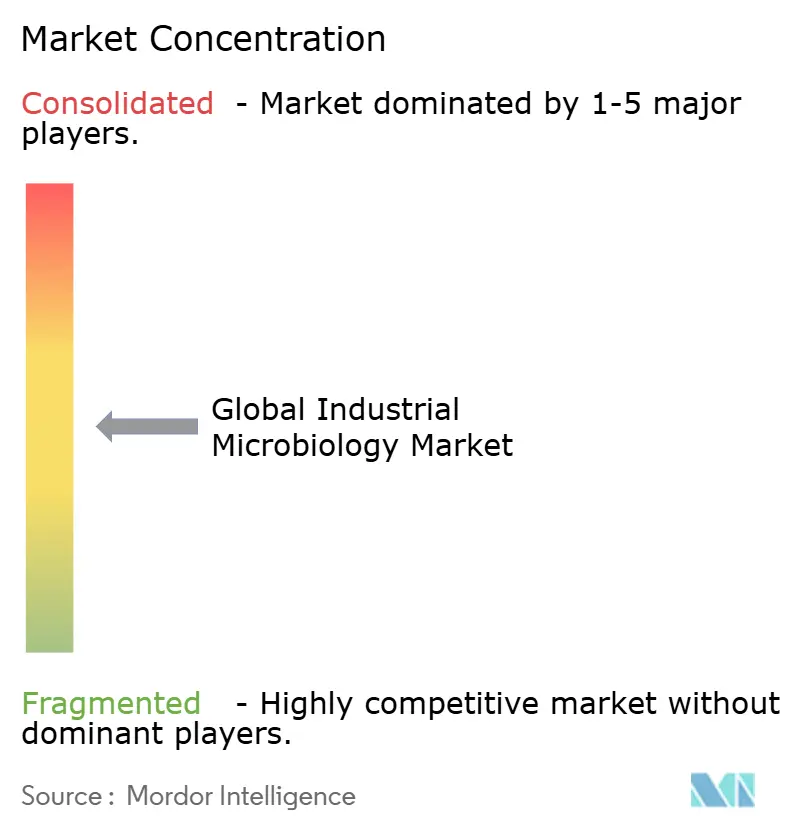

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Industrial Microbiology Market Analysis by Mordor Intelligence

Industrial microbiology market size in 2026 is estimated at USD 14.53 billion, growing from 2025 value of USD 13.53 billion with 2031 projections showing USD 20.71 billion, growing at 7.38% CAGR over 2026-2031. Demand is widening beyond traditional quality-control testing as bioprocessing, precision fermentation, and ESG-driven waste-bioremediation projects create fresh revenue pools for service providers. Rapid sterility and endotoxin screening requirements originating from cultivated-meat facilities, together with stricter GMO oversight in multiple jurisdictions, are reshaping validation protocols across the global supply chain. Supplier disruptions—in particular BD’s shortage of BACTEC blood-culture vials in 2024—have amplified interest in multisource procurement strategies and automated inventory tracking to secure laboratory uptime. Competitive intensity is accelerating as leading vendors pursue acquisitions, single-use bioreactor innovations, and AI-driven contamination-detection software to differentiate on speed, data integrity, and cybersecurity resilience.

Key Report Takeaways

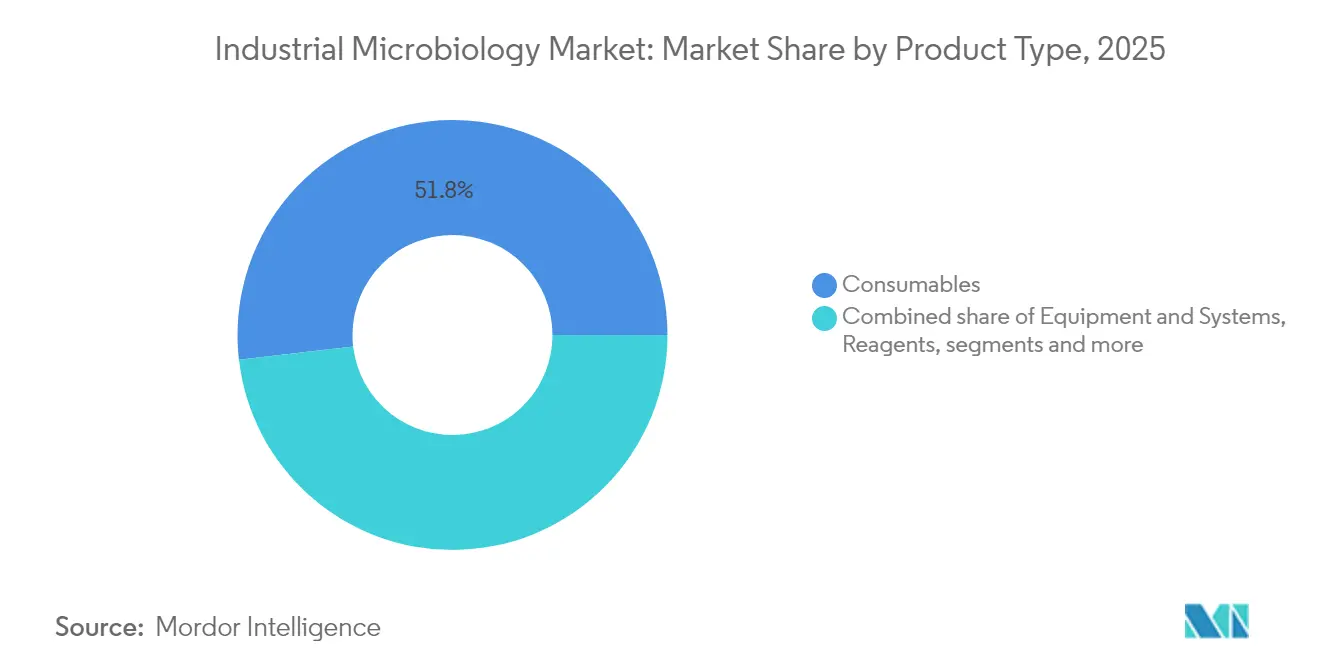

- By product type, consumables led with 51.84% revenue share in 2025, while reagents are projected to expand at a 9.04% CAGR through 2031.

- By application, food & beverage held 32.05% of industrial microbiology market share in 2025; pharmaceutical & biotechnology is advancing at a 9.96% CAGR to 2031.

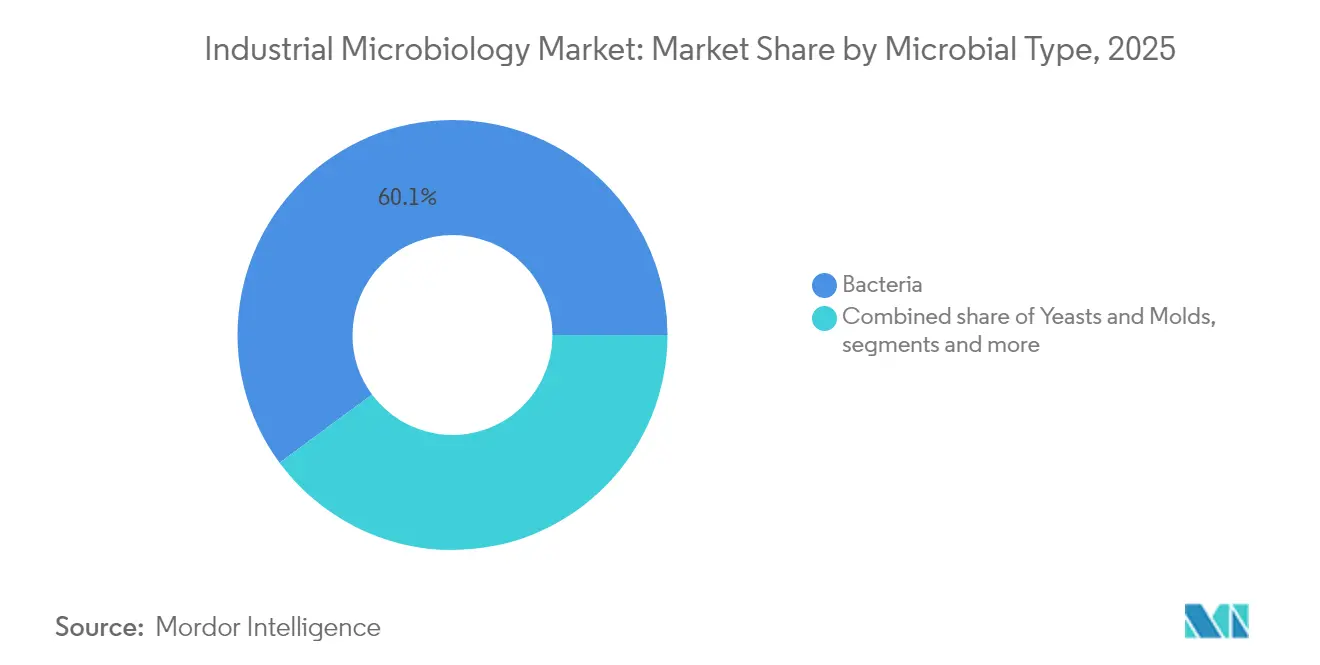

- By microbial type, bacteria accounted for 60.12% share of the industrial microbiology market size in 2025, whereas viruses & phages show the fastest 9.34% CAGR through 2031.

- By test type, bioburden testing commanded 45.58% share of the industrial microbiology market size in 2025, and endotoxin testing is set for a 9.01% CAGR to 2031.

- By geography, North America captured 36.34% of industrial microbiology market share in 2025, while Asia-Pacific is forecast to rise at a 10.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Microbiology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for nutraceuticals & fermented products | +1.8% | Global, APAC leading growth | Medium term (2-4 years) |

| Rising concern for food safety & stringent regulations | +1.5% | North America & EU expanding globally | Short term (≤ 2 years) |

| Increasing R&D spend & biopharma pipeline expansion | +1.2% | North America, EU, APAC acceleration | Long term (≥ 4 years) |

| Expansion of industrial fermentation for biofuels & enzymes | +0.9% | Global, industrial hubs | Medium term (2-4 years) |

| Rapid QC needs in cultivated-meat manufacturing | +0.6% | North America & EU early adoption | Long term (≥ 4 years) |

| ESG-funded microbiome waste-bioremediation projects | +0.4% | Global, EU regulatory leadership | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Nutraceuticals & Fermented Products

Surging probiotic consumption across Asia, highlighted by Zuellig Pharma’s decade-long alliance to distribute OMNi-BiOTiC strains in Indonesia, Philippines, and Taiwan, is pushing laboratories to offer localized strain-characterization services alongside metabolite profiling. The industrial microbiology market is therefore pivoting from pathogen detection toward deeper functional analytics that quantify bioactivity and regional taste preferences. Manufacturers are also tailoring formulations to match local regulatory requirements, which accelerates demand for rapid microbial-quality testing infrastructure in emerging economies. The widening palette of fermentation-derived ingredients—ranging from umami seasonings to bio-based sweeteners—is adding new QC checkpoints for contaminants and off-target metabolites. These shifts collectively sustain recurring consumable uptake and cement long-term reagent contracts for leading suppliers.

Rising Concern for Food Safety & Stringent Regulations

Recent Listeria-linked recalls involving supplement shakes prompted regulators to enforce tighter turnaround targets for contamination confirmation, spurring adoption of high-throughput PCR and whole-genome-sequencing workflows.[1]Contagion, “Listeria Outbreak Linked to Prairie Farms Supplement Shakes,” contagionlive.com The FDA’s updated Pharmaceutical Microbiology Manual demands harmonized endotoxin and antimicrobial-effectiveness assays that integrate seamlessly with 21 CFR 11-compliant data-capture systems. Vendors such as bioMérieux responded with the 3P ENTERPRISE platform, pairing digital environmental monitoring with audit-ready electronic records. Blockchain-supported supply-chain transparency adds another documentation layer, compelling QC labs to generate tamper-proof microbial test reports. Collectively, these pressures increase spending on automated incubators, rapid readers, and middleware that can cut result cycles while meeting evolving global benchmarks.

Increasing R&D Spend & Biopharma Pipeline Expansion

Thermo Fisher’s USD 2 billion, four-year U.S. capacity upgrade underscores the sector’s focus on large-scale biologics, cell, and gene-therapy manufacturing. Sartorius’ EUR 560 million expansion, coupled with its collaboration with LFB Biomanufacturing, aligns equipment suppliers with rising demand for high-throughput sterility, mycoplasma, and genetic-stability assessments.[2]Sartorius, “Sartorius and LFB BIOMANUFACTURING Collaborate on Cell Line Development,” sartorius.com Precision-fermentation initiatives, exemplified by BASF and Acies Bio’s renewable-methanol platform, further inflate the need for strain-stability monitoring and pathway-validation assays. As biologics are projected to approach 45% of global pharmaceutical sales by 2028, specialized industrial microbiology market offerings—such as rapid endotoxin kits and viral-vector safety screens—are becoming integral to GMP compliance. Long-term, integrated single-use systems equipped with automated QC loops are expected to solidify vendor lock-in across large CDMOs.

Expansion of Industrial Fermentation for Biofuels & Enzymes

Novonesis emerged from the EUR 3.7 billion merger of Novozymes and Chr. Hansen and now runs more than 23 manufacturing sites and almost 40 R&D centers. The combined scale equips the company to meet rising demand for industrial enzymes and other fermentation-derived ingredients. This consolidation signals the sector’s drive to expand fermentation capacity and pushes process developers to install advanced microbial-monitoring tools that raise efficiency while cutting batch-failure rates across varied production settings Novonesis.[3]Novonesis, “Combination of Novozymes and Chr. Hansen Completed,” novonesis.comThermo Fisher’s new single-use DynaDrive bioreactor improves productivity by 27%, reflecting the need for closed-loop contamination control in high-value enzyme and biofuel lines biopharmaapac.com. ESG mandates are incentivizing bio-refineries to adopt 24/7 automated microbial monitoring to certify sustainability claims. Consequently, service providers offering predictive analytics and cloud-based dashboards gain a competitive edge in the industrial microbiology market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory conflicts over GMOs in food sources | -0.8% | Global, EU–US divergence pronounced | Medium term (2-4 years) |

| Escalating product recalls heightening scrutiny | -0.6% | North America & EU | Short term (≤ 2 years) |

| Supply-chain volatility in specialty culture media inputs | -0.5% | Global, developing regions vulnerable | Short term (≤ 2 years) |

| Cyber-security risks to automated microbiology data systems | -0.3% | Global, automated facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Conflicts Over GMOs in Food Sources

Divergent frameworks for CRISPR-edited crops create compliance complexity as the EU proposes dual regulatory pathways for new genomic techniques, while the U.S. leans on harmonization through the ICH. Testing laboratories servicing global clients must therefore maintain parallel protocols, certifications, and reporting formats, increasing operating costs and stretching skilled-labor capacity. China’s heightened biosafety oversight further obliges exporters to demonstrate traceability of genetically modified microorganisms from strain lineage to final product. As patent volumes for CRISPR crops exceed 1,900 yet lack uniform treatment, QC providers in the industrial microbiology market face uncertainty when planning capital investments in GMO-specific analytical platforms. These discrepancies slow cross-border adoption of rapid microbial assays tailored to engineered organisms.

Supply-Chain Volatility in Specialty Culture Media Inputs

The transfer of 3M’s food-safety line to Neogen forced laboratories to validate packaging and documentation changes across Petrifilm plates and Molecular Detection reagents, temporarily straining throughput. BD’s BACTEC vial shortage highlighted the fragility of single-source supply models, prompting hospitals to ration tests and source interim alternatives that risked result variability. Post-pandemic backlogs leave 80% of microbiology laboratories short-staffed, complicating contingency-planning efforts. Although initiatives such as Fisher Scientific’s SureTRACE offer enhanced provenance tracking, high-purity agar, protein hydrolysates, and specialty dyes still depend on geographically concentrated raw-material producers. Persistent input volatility therefore restrains the industrial microbiology market’s near-term growth until multisupplier qualification pipelines mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables Sustain Revenue Streams

Consumables represented 51.84% of global revenue in 2025, underscoring their vital role in day-to-day operations. Reagent volumes rise with each automation cycle, and the industrial microbiology market size attached to consumables is projected to grow at 7.22% CAGR to 2031 as high-throughput instruments demand larger lot-qualified batches. Media & culture preparations expand in tandem with stricter environmental-monitoring guidelines for pharmaceutical clean rooms. RFID-enabled vials and plates improve inventory accuracy and support remote batch-release verification, deepening laboratory reliance on branded disposables.

The equipment & systems segment benefits from single-use technologies that cut cleaning validation steps by 50%, yet its share grows more gradually because capital budgets follow multi-year cycles. Filtration and centrifugation innovations favor closed-system configurations that block adventitious microbes upstream. Automated colony-counters reduce analyst hours, which translates into higher throughput and greater reagent pull-through for suppliers. Such synergies help vendors defend margins even as competition intensifies.

By Application Area: Pharmaceutical Acceleration Outpaces Food Dominance

The food & beverage sector held 32.05% of industrial microbiology market share in 2025 on the back of global HACCP standards. However, the pharmaceutical & biotechnology segment is forecast to deliver a 9.96% CAGR through 2031, expanding the industrial microbiology market size for endotoxin, mycoplasma, and sterility testing kits. Growth is strongest in cell- and gene-therapy manufacturing, where rapid release testing can shave weeks off product lead-times.

Environmental testing is gaining traction as ESG-directed remediation funds sponsor microbiome-based clean-up of oil, heavy metals, and PFAS at industrial sites. Agricultural applications increasingly involve soil-health profiling using plant-growth-promoting rhizobacteria, while cosmetic brands invest in microbiome-friendly formulations that require live-culture stability assessments. These diversified use-cases spread risk for service providers and underpin broader instrument penetration across verticals.

By Microbial Type: Viruses & Phages Challenge Bacterial Dominance

Bacteria continued to account for 60.12% of global revenue in 2025, reflecting their prominence in fermentation and safety testing. Yet viruses & phages are growing at a 9.34% CAGR as gene-therapy vector production and phage-therapy trials progress. This shift drives procurement of high-sensitivity qPCR panels and next-generation sequencing workflows able to separate therapeutic vectors from adventitious agents.

Yeasts & molds retain importance where mycotoxin compliance is strict, notably in grain and beverage chains. Emerging synthetic-biology constructs blur classical taxonomy, obliging laboratories to deploy bioinformatics pipelines that map entire microbial communities. The industrial microbiology market therefore sees rising demand for modular platform assays able to toggle between bacterial, viral, and eukaryotic targets without complex revalidation.

By Test Type: Endotoxin Testing Gains Momentum

Bioburden testing led with 45.58% share in 2025, but endotoxin testing’s 9.01% forecast CAGR points to heightened vigilance around pyrogen contamination in biologics. The industrial microbiology market size for rapid endotoxin kits grows further as the FDA encourages alternatives to Limulus amebocyte lysate that reduce animal use. AI-enabled UV-absorbance spectroscopy can now cut sterility-test cycle time from 14 days to under 30 minutes, reshaping release-workflows for advanced therapies.

The “Others” category, covering genetic-stability, viral-clearance, and environmental monitoring assays, expands as continuous bioprocessing pushes manufacturers to embed real-time microbial surveillance. MilliporeSigma’s Aptegra CHO assay trims genetic-stability testing costs by 43%, exemplifying how next-generation sequencing redefines QC economics.

Geography Analysis

North America’s leadership stems from mature GMP enforcement and ongoing capital investment such as Thermo Fisher’s USD 2 billion U.S. upgrade program, which expands local single-use media output and strengthens supply resilience. Canadian biotech clusters leverage favorable R&D tax credits to develop microbial consortia for plant-based foods, whereas Mexican producers focus on cross-border harmonization to meet USMCA food-safety audits. Cybersecurity frameworks targeting automated data systems further differentiate regional vendors that embed role-based access controls and encrypted backups.

Asia-Pacific’s double-digit trajectory arises from China’s state-backed biologics plants seeking global cGMP accreditation, India’s vaccine and biosimilar exporters, and Japan’s functional-food incumbents requiring advanced strain-stability analytics. Government support for mRNA facilities in South Korea and Australia also accelerates demand for rapid QC solutions. Regional suppliers that localize consumable production reduce lead times and skirt import duties, capturing share from established multinationals.

Europe balances regulatory rigor with green-transition incentives. The EU’s push for ISCC Plus certification drives uptake of renewable-plastic consumables, as demonstrated by Sartorius’ 50% fossil-plastic reduction milestone. Germany and France spearhead bioprocess-4.0 pilot plants deploying predictive microbial analytics, while the UK channels public funding into phage-therapy R&D. Divergent GMO rules, however, oblige multi-national labs to run dual protocols, mildly constraining cross-border efficiencies.

Competitive Landscape

The industrial microbiology market exhibits moderate consolidation: Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification arm broadens its downstream footprint, while the contemplated USD 4 billion divestiture of its microbiology unit signals portfolio pruning to focus on high-growth adjacencies. bioMérieux, Merck KGaA’s MilliporeSigma, and Danaher’s Cytiva advance automation strategies that integrate sample prep, incubation, detection, and compliance archiving in one ecosystem. Novonesis leverages its expanded enzyme library to cross-sell QC reagents into food and biofuel accounts.

Private-equity interest is rising, evidenced by outreach to Thermo Fisher on the potential microbiology-unit sale and by BD’s intent to spin off its USD 3.4 billion Diagnostics & Biosciences arm, which could reshape competitive alignments. Smaller innovators like Tetsuwan Scientific attract seed funding for AI-driven robotic scientists that automate repetitive bench tasks, threatening to lower barriers for new entrants. Vendors investing early in cybersecurity-by-design obtain a reputational edge, as data-integrity audits become central to vendor-selection criteria across pharma and food customers.

Pricing pressure remains contained because consumable stickiness offsets equipment-margin dilution, and multi-year service contracts lock in software subscriptions. Still, labs continue to negotiate dual-sourcing agreements to buffer supply shocks. Suppliers that can guarantee continuity via regionally-redundant plants enjoy preferential status in OEM qualification lists, reinforcing barriers for late-stage challengers.

Global Industrial Microbiology Industry Leaders

bioMerieux SA

Bio-Rad Laboratories Inc.

Thermo Fisher Scientific Inc.

Becton Dickinson and Company

Qiagen NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Thermo Fisher evaluates USD 4 billion sale of its microbiology unit, potentially opening acquisition opportunities for consolidation-focused investors.

- April 2025: Thermo Fisher launches 5 L DynaDrive single-use bioreactor, boosting productivity by 27% and scaling to 5,000 L for CDMOs.

- March 2025: Sartorius gains ISCC Plus certification for French and UK sites, enabling a 50% fossil-plastic reduction in Ambr bioreactors.

- February 2025: Thermo Fisher acquires Solventum’s purification & filtration business for USD 4.1 billion, expecting USD 125 million in synergies by year five.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the industrial microbiology market as the yearly revenue earned from purpose-built media, reagents, single-use filtration or detection consumables, plus fermentation, sterility testing, and environmental monitoring equipment that deliberately grow, detect, or control microorganisms inside factories, breweries, bio-refineries, and remediation plants. Activities restricted to patient diagnosis or academic basic research remain outside this boundary.

Clinical diagnostic microbiology kits and outsourced laboratory services are not covered.

Segmentation Overview

- By Product Type

- Equipment & Systems

- Fermentation Systems

- Bioreactors & Fermenters

- Filtration & Centrifugation Systems

- Others

- Consumables

- Media & Culture Preparations

- Petri Dishes & Vials

- Other Consumables

- Reagents

- Enzymes & Buffers

- Others

- Equipment & Systems

- By Application Area

- Food & Beverage Industry

- Pharmaceutical & Biotechnology Industry

- Agricultural Industry

- Environmental Industry

- Cosmetic / Personal-Care Industry

- Other Application Areas

- By Microbial Type

- Bacteria

- Yeasts & Molds

- Viruses & Phages

- By Test Type

- Sterility Testing

- Bioburden Testing

- Endotoxin Testing

- Others

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with quality control managers at pharmaceutical fermenters, beverage technologists, single-use equipment suppliers, and regulators across North America, Europe, and Asia; their insights validated usage rates, price corridors, and imminent rule changes before we froze assumptions.

Desk Research

We began by mapping production volumes, recall notices, and test intensity through open portals such as the USDA recall dashboard, EU Rapid Alert System for Food and Feed, OECD bioeconomy indicators, and US FDA inspection citations. Company 10-Ks, investor decks, and quality manuals sharpened average selling prices, while Questel patent clusters flagged emerging bioprocess tools. Revenue splits were cross-checked in D&B Hoovers and Dow Jones Factiva, giving us an auditable first pass across regions. These examples represent only a slice of the wider document set consulted.

Market-Sizing & Forecasting

A top-down construct links batch counts, test frequencies, and replacement cycles to spending pools; selective bottom-up roll-ups of media and equipment sales then act as reasonableness checks. Key variables like media consumption per 1,000-liter run, filter change frequency, precision fermentation capacity additions, and regional GMP inspection intensity feed a multivariate regression supplemented by scenario analysis for policy swings. Channel check ranges bridge gaps until the two approaches converge.

Data Validation & Update Cycle

Outputs pass anomaly screens, peer review, and senior sign-off. Models refresh every twelve months, with mid-cycle updates triggered by material capacity or regulatory shocks, so clients always receive the latest baseline.

Why Our Industrial Microbiology Baseline Commands Reliability

Published values often differ because publishers choose different cut-off years, product baskets, pricing ladders, and update rhythms.

We ground our 2025 baseline of USD 13.53 billion on the full stack of consumables and capital goods and recalibrate variables whenever fresh field evidence emerges.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.53 B (2025) | Mordor Intelligence | - |

| USD 11.12 B (2022) | Global Consultancy A | Older base year, reagent-only scope |

| USD 14.44 B (2024) | Regional Insights Firm B | Excludes capital goods, fixed 3% price uplift |

The comparison shows that our disciplined scope selection, variable tracking, and annual refresh deliver a transparent, balanced baseline that decision makers can rely on.

Key Questions Answered in the Report

What is the current size of the industrial microbiology market?

The market is valued at USD 14.53 billion in 2026 and is projected to reach USD 20.71 billion by 2031.

Which region is growing fastest?

Asia-Pacific is forecast to expand at a 10.05% CAGR through 2031, driven by biopharmaceutical capacity additions and rising probiotic consumption.

Why are endotoxin tests in higher demand?

Biologics production is expanding, and regulators are tightening pyrogen limits, pushing endotoxin testing to a 9.01% CAGR—faster than any other test category.

How are suppliers responding to stricter food-safety rules?

Leading vendors now embed digital environmental monitoring, blockchain-ready documentation, and rapid PCR platforms to meet real-time traceability and 21 CFR 11 compliance needs.

What role does automation play in competitive advantage?

Integrated platforms that unite sample prep, incubation, detection, and data integrity lower turnaround times and improve audit readiness, helping vendors secure multi-year service contracts.

Page last updated on: