Automotive Keyless Entry Access Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

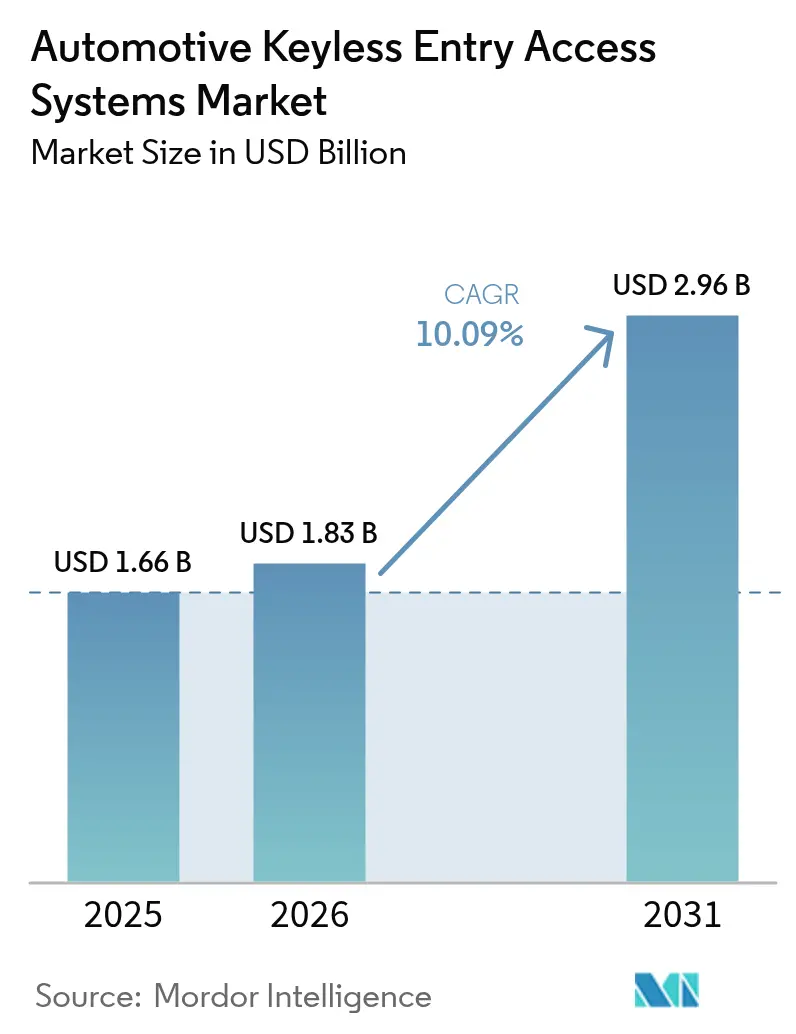

| Market Size (2026) | USD 1.83 Billion |

| Market Size (2031) | USD 2.96 Billion |

| Growth Rate (2026 - 2031) | 10.09% CAGR |

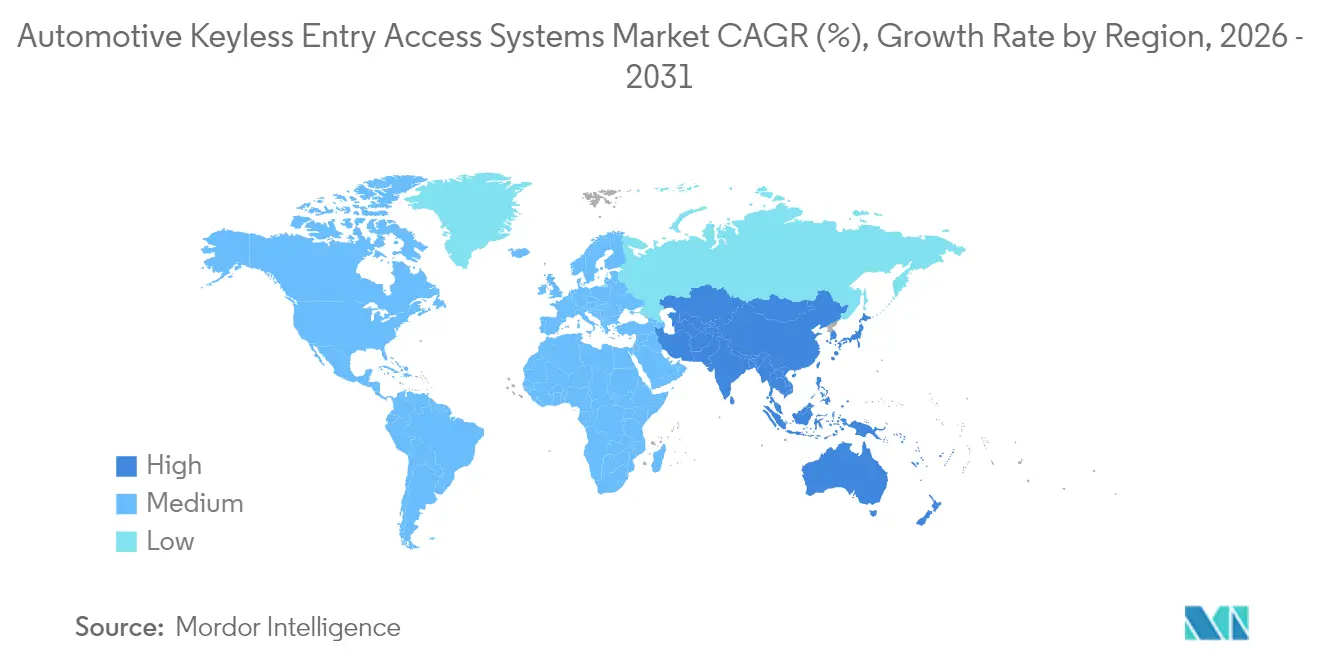

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Keyless Entry Access Systems Market Analysis by Mordor Intelligence

The automotive keyless entry access systems market size is expected to grow from USD 1.66 billion in 2025 to USD 1.83 billion in 2026 and is forecast to reach USD 2.96 billion by 2031 at 10.09% CAGR over 2026-2031. Growing demand for software-defined vehicles, rising security expectations, and tighter cybersecurity regulations underpin this growth. Ultra-wideband (UWB) deployment by leading original-equipment manufacturers (OEMs) offers centimeter-level proximity accuracy that mitigates relay-attack risks. Smartphone-centric “phone-as-a-key” solutions from Apple and Google move the technology from a convenience add-on to a core vehicle subsystem. Asia–Pacific commands the largest regional presence and delivers the fastest CAGR, driven by China’s electric-vehicle output and India’s maturing automotive electronics base.

Key Report Takeaways

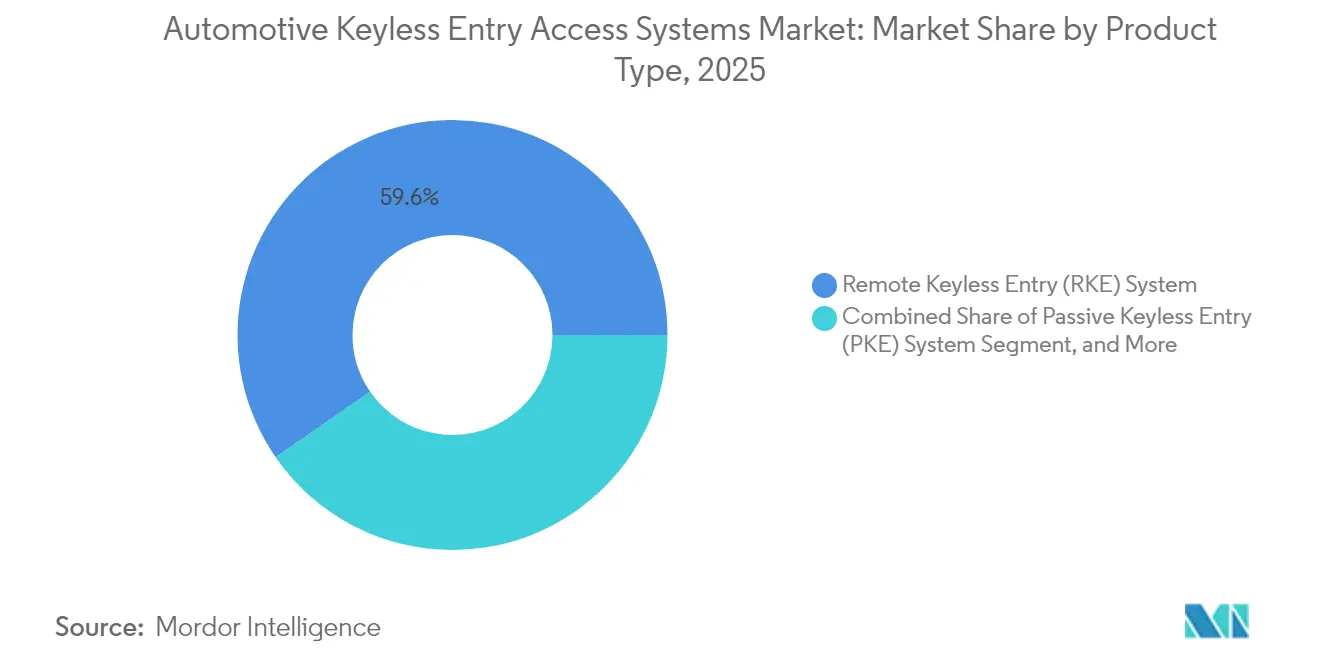

- By product type, Remote Keyless Entry held 59.62% of the automotive keyless entry access system market share in 2025, while Passive Keyless Entry is projected to post an 10.58% CAGR through 2031.

- By technology, radio-frequency solutions accounted for 72.98% of the automotive keyless entry access system market in 2025; Ultra-wideband is advancing at a 10.31% CAGR to 2031.

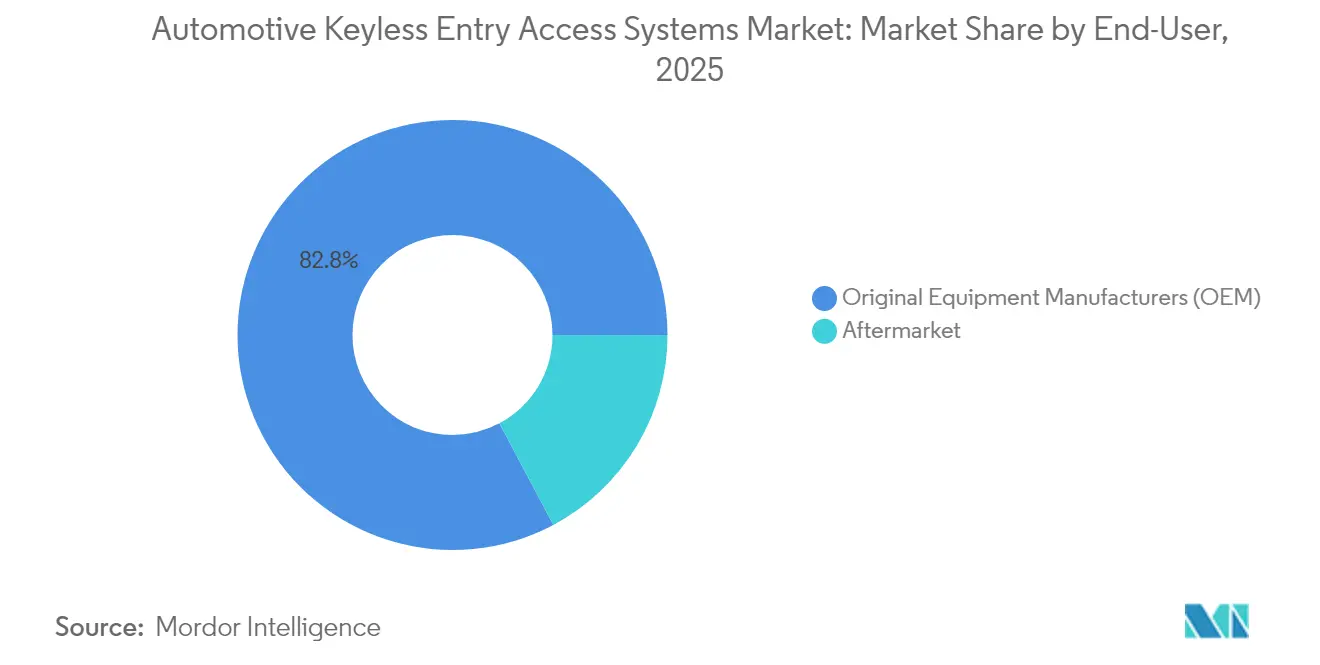

- By sales channel, OEM installations captured 82.77% of the automotive keyless entry access system market in 2025; the aftermarket segment is rising at an 10.22% CAGR.

- By vehicle type, passenger cars represented 71.84% of the automotive keyless entry access system market in 2025; light commercial vehicles are expected to grow at a 10.44% CAGR.

- By geography, Asia–Pacific led with a 48.55% of the automotive keyless entry access system market revenue share in 2025 and is expanding at a 11.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Keyless Entry Access Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Vehicle-Theft Incidence Driving OEM Security Upgrades | +2.1% | Global, with peak impact in North America & Europe | Medium term (2-4 years) |

| Connected and Smart-Car Adoption Boosting Demand for Digital Keys | +1.8% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Premium and EV Penetration Making PKE Standard Equipment | +1.5% | Global, led by China and European markets | Medium term (2-4 years) |

| Big-Tech "Phone-As-A-Key" APIs Expanding OEM Ecosystems | +1.3% | Global, with Apple/Google ecosystem penetration | Medium term (2-4 years) |

| Insurance-Driven Anti-Theft Regulations in US and EU | +1.2% | North America & EU primarily | Short term (≤ 2 years) |

| UWB-Enabled Car-Sharing Platforms (Fleet & MaaS) | +0.9% | Urban centers globally, early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle-Theft Incidence Driving OEM Security Upgrades

Vehicle theft exceeded in the United States during 2024, pressuring manufacturers to harden access-control defenses. Models without immobilizers became the main targets, forcing OEMs to deliver rapid software patches and retrofit kits. Organized crime employs cheap relay-attack devices that clone fob signals within seconds, prompting investment in UWB, motion-sensing fobs, and multi-factor authentication. Insurers adjust premiums based on anti-theft sophistication, aligning corporate risk management with advanced keyless entry deployment[1]“2024 Auto Theft Statistics,” National Insurance Crime Bureau, nicb.org.

Connected and Smart-Car Adoption Boosting Demand for Digital Keys

Apple CarKey and Google Digital Car Key APIs provide turnkey frameworks that let automakers roll out smartphone-based access without bespoke app development. Tesla’s seamless digital integration benchmark raises consumer expectations across all price points. The Car Connectivity Consortium’s Digital Key 3.0 specification combines Bluetooth Low Energy and UWB, letting drivers unlock vehicles hands-free while maintaining cryptographic security[2] “Digital Key Release 3.0,” Car Connectivity Consortium, carconnectivity.org. Digital keys have, therefore,e shifted from luxury add-ons to baseline infrastructure for over-the-air (OTA) vehicle updates and personalized driver profiles.

Premium and EV Penetration Making PKE Standard Equipment

Electric vehicle platforms feature centralized electronics and 48-volt architectures that simplify Passive Keyless Entry integration. Chinese brands such as BYD bundle PKE as standard on high-volume models, resetting consumer expectations in export markets. Luxury marques add biometric layers, palm-print or facial recognition, that cascade to mid-segment cars over time. As premium adoption rises, per-unit hardware costs fall, accelerating mass-market penetration.

Insurance-Driven Anti-Theft Regulations in US and EU

The European Union’s Cyber Resilience Act mandates secure software-update pathways for connected components, including keyless entry modules[3]“Cyber Resilience Act Implications for Automotive,” TUV SUD, tuvsud.com. Canada allocates CAD 1.1 million to pilot biometric-based anti-theft projects, reinforcing policy momentum[4]“Government Funds Vehicle Anti-Theft Projects,” Transport Canada, tc.canada.ca. OEMs that meet these standards gain faster regulatory clearance and lower fleet-insurance costs, whereas low-cost entrants face compliance barriers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Relay-Attack Vulnerabilities Eroding Consumer Trust | -1.4% | Global, particularly affecting premium segments | Short term (≤ 2 years) |

| High BOM Cost For Economy-Segment Models | -0.8% | Emerging markets and cost-sensitive segments | Medium term (2-4 years) |

| Secure-Chip Shortages Amid Smartphone Demand Peaks | -1.1% | Global, with acute impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| EU Draft Law Mandating MFA Could Delay Roll-Outs | -0.6% | European Union primarily, spillover to global OEMs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Relay-Attack Vulnerabilities Eroding Consumer Trust

Social-media tutorials show thieves opening premium vehicles in under 30 seconds using relay amplifiers. Publicized incidents undermine the perceived safety of keyless systems, especially among high-end buyers. Manufacturers respond with encrypted UWB proximity checks and motion-detected sleep modes, yet legacy vehicles remain exposed. Consumer hesitation could delay upgrades until security guarantees strengthen.

High BOM Cost for Economy-Segment Models

Secure elements, RF transceivers, and cryptographic processors add noticeable cost of bill-of-materials to low-margin cars. Automotive semiconductor spend per vehicle is projected to double by 2030, squeezing budgets for entry-level segments. Supply-chain competition with consumer-electronics brands often prioritizes phone production over automotive orders, extending lead times and raising component prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Keys Disrupt Traditional RKE Dominance

Remote Keyless Entry systems held 59.62% of the automotive keyless entry access system market in 2025, leveraging mature RF architecture and attractive cost per vehicle. Passive Keyless Entry is advancing at 10.58% CAGR, aided by EV platform design that simplifies continuous proximity detection. Remote Keyless Entry presently sets the performance baseline, yet PKE’s growth suggests eventual parity. Consumers value hands-free convenience, while fleet operators view the technology as a path to audit-level driver authentication.

Digital keys, although the smallest slice today, record double-digit growth as smartphone saturation nears universality. As APIs mature, aftermarket retrofits factor into the projected upswing, granting older models modern access control without redesign.

By Technology: UWB Challenges RF Supremacy Through Security Innovation

Traditional RF still accounts for 72.98% of the automotive keyless entry access system market size in 2025. Its low cost and familiarity with global certification ensure continued relevance, particularly in price-sensitive vehicle classes. Yet UWB’s 10.31% CAGR stems from its immunity to signal-relay exploits and precise time-of-flight ranging. Apple, Samsung, and Google place UWB chips in phones, enabling OEMs to lean on consumer electronics roadmaps rather than bespoke automotive silicon.

Bluetooth Low Energy remains a bridging protocol, especially useful when vehicles must communicate with phones lacking UWB radios. NFC supports valet and service-mode access, while China’s NearLink may introduce regional divergence. Suppliers now release multi-protocol system-on-chips that bundle RF, BLE, and UWB, cutting board complexity and easing migration.

By End-User: Aftermarket Growth Signals Retrofit Demand Acceleration

OEM installations captured 82.77% of the automotive keyless entry access system market's 2025 revenue, driven by factory-fit digital-access features on high-volume vehicle platforms. The aftermarket posts an 10.22% CAGR as owners of older cars seek enhanced theft protection and smartphone convenience. Fleet managers deploy retrofit kits to limit key handovers and automate driver logs. Regulatory incentives in Canada and rising insurance premiums in the United States further support upgrades.

Continental’s launch of 700 new aftermarket part numbers in 2025 illustrates a commitment to this channel. Independent installers benefit from simplified harnesses and cloud-provisioning tools, reducing labor time. However, warranty concerns and vehicle-specific integration hurdles still limit adoption in some regions.

By Vehicle Type: Commercial Fleets Drive Digital Key Innovation

Passenger cars comprised 71.84% of the automotive keyless entry access system market in 2025 installations, reflecting their dominant production volumes. Light commercial vehicles, however, show a 10.44% CAGR as logistics providers prioritize digital key sharing for multi-driver routes.

Car-sharing ventures require frictionless booking and return, pushing innovation in temporary credentialing and cloud-based audit trails. Rental firms cite lower damage disputes and faster turnaround as key benefits. Heavy trucks adopt the technology more gradually, focusing on driver identification rather than convenience, yet electric-heavy-duty pilots signal future acceleration.

Geography Analysis

Asia–Pacific generated 48.55% of the automotive keyless entry access system market's 2025 revenue and is tracking an 11.03% CAGR. China’s EV surge positions keyless systems as standard equipment even on mid-priced models, forcing foreign competitors to match feature sets. India’s production-linked incentive schemes nurture domestic electronics plants that lower local procurement costs. Japanese suppliers like Denso scale UWB modules for global platforms, while South Korean OEMs extend smartphone-only access across new electric ranges.

North America ranks second by value. Rising theft statistics and insurance pressure make advanced keyless solutions table stakes. Canada funds eight anti-theft projects, anchoring biometric and AI-based upgrades. Mexico’s OEM hubs integrate compliant modules to serve US export programs, spreading secure-element demand across the region. Wide smartphone penetration bolsters digital-key acceptance, and a sizable aftermarket supports retrofits.

Europe benefits from strict cybersecurity mandates. Luxury brands spearhead UWB adoption, while mid-tier models incorporate encrypted BLE. Regulatory clarity under the Cyber Resilience Act grants first movers a compliance edge, shaping supplier shortlists in procurement cycles.

Regulatory Landscape

Type-approval and product-safety regimes are tightening cybersecurity and software-update obligations around connected access functions. UNECE Regulation No. 155 requires OEMs to operate a Cyber Security Management System (CSMS) across the vehicle lifecycle for in-scope vehicle categories, making cyber risk assessment and mitigations a prerequisite for market access in jurisdictions that apply UNECE frameworks. ISO 24089:2023 for automotive software update engineering, with an amendment published in July 2024, also reinforces process expectations for secure update delivery, which becomes a dependency as digital keys and keyless ECUs receive over-the-air software changes.

In the United States, NHTSA continues to frame cybersecurity as a safety risk under the National Traffic and Motor Vehicle Safety Act through guidance and research. FMVSS modernization efforts also indicate ongoing alignment of legacy safety standards with software-defined vehicle architectures. In May 2025, NHTSA issued a proposed rule to remove redundant requirements in FMVSS No. 206 (door locks and retention components), and in March 2026 NHTSA proposed updates to FMVSS No. 103 and No. 104, highlighting continued regulatory maintenance of vehicle access-adjacent safety and control standards. These updates influence OEM design, validation, and compliance documentation for electronic locking and access systems.

Value Chain Analysis

The value chain starts with semiconductor and materials inputs (secure elements, microcontrollers, RF/BLE/UWB transceivers, LF antenna drivers, and plastics or metals for fobs and backup cards), followed by module design and integration by tier-one suppliers that deliver RKE, PKE/PEPS, and digital key controllers to OEMs for vehicle platform integration. Software and cryptography layers, including provisioning tools and credential lifecycle management, increasingly sit alongside hardware, aligning keyless access with software-defined vehicle stacks and OTA update pipelines.

Standardization and interoperability bodies shape downstream integration. The Car Connectivity Consortium (CCC) anchors the digital key ecosystem through specifications and certification programs that validate cross-phone and cross-vehicle behavior using standards-based PKI security, reducing fragmentation for OEM programs that must support Apple and Android device portfolios. Distribution skews toward OEM fitment, while the aftermarket relies on installers and kit providers that can adapt harnessing, pairing, and security provisioning to diverse vehicle architectures. Supply-chain resilience remains a constraint due to dependence on standardized semiconductors; the late-2025 intervention affecting Nexperia highlighted concentration risk in automotive electronic component supply, prompting dual-sourcing and contingency planning among tier-one module manufacturers.

Competitive Landscape

The automotive keyless access system market comprises several tier-one suppliers with differentiated portfolios. Continental, Denso, and Valeo each hold meaningful positions and produce a moderately concentrated field. Continental establishes the Aumovio brand to highlight software-defined strategies, including CoSmA UWB access and over-the-air credential management. Denso leverages long-standing OEM ties in Japan and North America, focusing on secure-element integration with ADAS controllers. Valeo emphasizes NFC-plus-BLE platforms that scale across entry-level trims.

Strategic alliances replace vertical silos. BMW collaborates with Apple to guarantee cross-platform digital-key support, while Hyundai uses Google for Android compatibility. Semiconductor vendors STMicroelectronics and NXP race to supply multi-protocol chipsets, selling reference designs that accelerate time to market.

Acquisition activity is steady: In January 2025, ASSA ABLOY acquired 3millID Corporation and Third Millennium Systems Ltd. to expand biometric expertise, and Samsung explores buying parts of Continental’s display and ADAS units, signaling cross-industry convergence. Cybersecurity proficiency and regulatory compliance increasingly decide bid outcomes, marginalizing firms lacking ISO/SAE 21434 certification.

Automotive Keyless Entry Access Systems Industry Leaders

Continental AG

Denso Corporation

Valeo SA

HELLA GmbH & Co. KGaA

TOKAIRIKA,CO, LTD.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The market is opening around interoperability-led scaling of smartphone-based access, shifting digital keys from bespoke OEM app features to standardized and certifiable implementations. A concrete signal is the Car Connectivity Consortiums June 2026 Plugfest 18 at DEKRA Lausitzring in Germany, which advanced end-to-end testing for Digital Key Version 4 capabilities, including enhanced sharing and fleet access use cases. CCC also reported 27 digital key products certified in the first half of 2026, creating procurement-ready proof points that shorten OEM qualification cycles and support multi-model rollouts across regions.

Security-driven upgrades create room for UWB-enabled PKE and digital access, as well as for multi-protocol solutions that pair NFC as secure fallback with BLE for proximity handshake and UWB for distance bounding to reduce relay-attack exposure. Fleet and mobility operators also add pull for revocable, auditable credentials and role-based sharing, aligning with CCC v4 focus areas and with the emphasis on car-sharing and commercial fleets as innovation channels in the report. On the supply side, semiconductor availability and secure-element sourcing remain gating factors, which supports opportunities for tier-one suppliers and silicon partners to provide certified reference designs, robust provisioning workflows, and continuity plans that reduce program risk for global OEM launches.

Recent Industry Developments

- June 2026: The Car Connectivity Consortium advanced Digital Key Version 4 testing at its 18th interoperability Plugfest at DEKRA Lausitzring in Germany. The work centered on end-to-end behavior for enhanced sharing and fleet access, reinforcing a pathway from premium digital keys toward standardized deployments that support managed, revocable credentials across mixed device and vehicle ecosystems.

- June 2025: Continental began supplying its CoSmA smart device-based digital access system, including UWB transceiver technology, for the Audi Q6 e-tron. The series supply highlights UWB moving into high-volume EV platforms and strengthens the supplier stack around relay-attack mitigation through precise ranging and secure smartphone-centric access.

- March 2024: FORVIA HELLA received additional series production orders for its digital Smart Car Access system. The wins underscore OEM momentum toward digital access architectures and expand the installed base for suppliers that can pair convenience features with security and lifecycle credential management.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from automotive keyless entry and access systems that let a vehicle be locked, unlocked, and authorized for entry, using electronic credentials and sensors integrated in the vehicle and the user device.

Scope exclusions: This sizing excludes general vehicle immobilizers or alarms when they are sold as standalone security modules without a keyless entry or access function.

Segmentation Overview

- By Product Type

- Passive Keyless Entry (PKE) System

- Remote Keyless Entry (RKE) System

- Digital / Phone-as-a-Key System

- By Technology

- RF (315/433 MHz)

- Bluetooth Low Energy (BLE)

- Near-Field Communication (NFC)

- Ultra-Wideband (UWB)

- By End-User

- Original Equipment Manufacturers (OEMs)

- Aftermarket

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Indonesia

- Philippines

- Vietnam

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- Israel

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping how demand forms, which is mainly tied to vehicle production and feature fitment by model and trim. We use public sources such as OICA vehicle production statistics, UN Comtrade trade codes for relevant electronic subassemblies, NHTSA and European Commission vehicle safety and cybersecurity related releases, and standards references from bodies such as ISO and SAE to understand how technologies like UWB, BLE, and NFC are being adopted.

To convert these signals into usable inputs, investor presentations, annual reports, and earnings call transcripts were reviewed for product mix cues, regional exposure, and pricing commentary. Patents and peer reviewed automotive electronics papers helped validate feature roadmaps, including phone as a key and relay attack mitigation. Where needed, a paid subscription focused on company financials and a paid patent database were used to cross check company level context and technology timelines. The sources listed here are illustrative, and many other public references were also used for data collection, cross checks, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test the desk assumptions on fitment rates, OEM versus aftermarket mix, and how ASPs shift when systems move from RKE to PKE and then to digital key add-ons. We spoke with a mix of vehicle OEM ecosystem contacts, component and module specialists, and channel participants across APAC, EMEA, and the Americas, so regional adoption patterns and currency effects could be compared consistently.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | APAC: 38% |

| Mid tier: 48% | Functional/Unit leaders: 38% | EMEA: 35% |

| Smaller Players: 20% | Managers: 50% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where vehicle production by region is reconstructed into an addressable pool, and then filtered by keyless feature penetration and installation channel. The model is then corroborated with selective bottom-up checks, such as sampled ASP times estimated shipment volumes and channel checks on aftermarket replacement demand, which helps adjust totals when one region trends differently.

Key inputs used in the model include passenger and commercial vehicle builds, the share of vehicles fitted with RKE versus PKE, the attach rate of digital key or phone as a key features, the OEM versus aftermarket split, and technology mix shifts toward BLE, NFC, and UWB. ASP progression is treated carefully because a feature upgrade usually changes both the bill of materials and the software content, and local currency movement can change reported USD values even if unit demand stays stable.

For forecasting, scenario analysis is applied around vehicle production recovery cycles and technology adoption speed, and those scenarios are anchored using expert expectations gathered in interviews. Where bottom-up visibility is weaker, we fill gaps using penetration ranges and then validate them with regional consistency checks so the final curve stays realistic.

Data Validation & Update Cycle

Validation is done through multiple checks that compare outputs against independent indicators such as vehicle production totals, technology adoption announcements, and observed OEM installation dominance. If a region shows an unexpected jump, the drivers are re-reviewed and assumptions like ASP movement, channel mix, and currency conversion timing are revisited before the model is signed off.

The work is reviewed in steps, starting with analyst peer review and then a final consistency pass across years, regions, and technology splits. Reports are refreshed annually, and interim updates are triggered when material events occur, such as sharp vehicle production shifts or a major technology transition. Before delivery, the latest pass is completed so clients receive an updated view aligned to the most recent data cuts.

Mordor Intelligence's Automotive Keyless Entry Access Systems Market Sizing Compared With Other Published Estimates

Published market sizes for keyless entry often differ even when the topic sounds the same, because included technologies, pricing assumptions, and the year used for currency conversion can vary. In this space, small changes in how PKE upgrades and digital key features are priced, and when exchange rates are applied, can shift the USD total by a noticeable amount.

Key gaps usually come from mixing older base-year pricing with newer unit volumes, folding adjacent vehicle access functions into the definition, or not validating the OEM versus aftermarket split with current channel feedback. By running variance checks on implied ASPs by technology generation and refreshing currency timing during the annual update, Mordor Intelligence keeps the estimate tied to the 2026 demand pool shown in the report page.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.83 B (2026) | |

| Industry Publisher A | USD 2.16 B (2024) | Uses an earlier base year and a longer horizon, and its total can read higher if 2024 pricing and unit assumptions are carried forward without re-testing ASP upgrades from RKE to PKE and digital key features under a consistent currency timing approach. |

| Industry Publisher B | USD 2.45 B (2022) | Starts from an older year and may bundle a wider set of vehicle access control devices under the same label, which can expand scope beyond keyless entry access systems and make the 2022 USD figure less comparable to a later-year definition. |

Taken together, the spread is mostly explained by year alignment and what is counted as a keyless access system versus a broader access control bucket. Our approach keeps the math traceable by linking vehicle builds to penetration, channel mix, and technology-linked ASP steps, and then checking that the implied values still make sense across regions and years.

Key Questions Answered in the Report

What is driving the rapid growth of the keyless entry system market?

Rising vehicle-theft rates, increasing electric-vehicle penetration, and standardized smartphone-based digital keys are pushing adoption, resulting in a 10.09% CAGR forecast through 2031.

Which region leads the keyless entry system market today?

Asia–Pacific holds 48.55% of global revenue in 2025 owing to China’s large EV output and rapid technology standardization.

How does Ultra-wideband improve vehicle security?

UWB provides centimeter-level distance measurement that blocks relay-attack methods common with traditional RF fobs, enhancing proximity authentication reliability.

What role do regulations play in market expansion?

Policies such as the EU Cyber Resilience Act and Canada’s anti-theft funding mandate tougher cybersecurity, favoring established suppliers and accelerating OEM adoption of advanced keyless systems.

Which product segment shows the highest growth potential?

Passive Keyless Entry leads with a 10.58% CAGR, reflecting its spread from premium to mid-tier vehicles as EV platforms adopt hands-free access as a standard feature.

Page last updated on: