Biomass Solid Fuel Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 28.77 Billion |

| Market Size (2030) | USD 47.03 Billion |

| Growth Rate (2025 - 2030) | 10.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

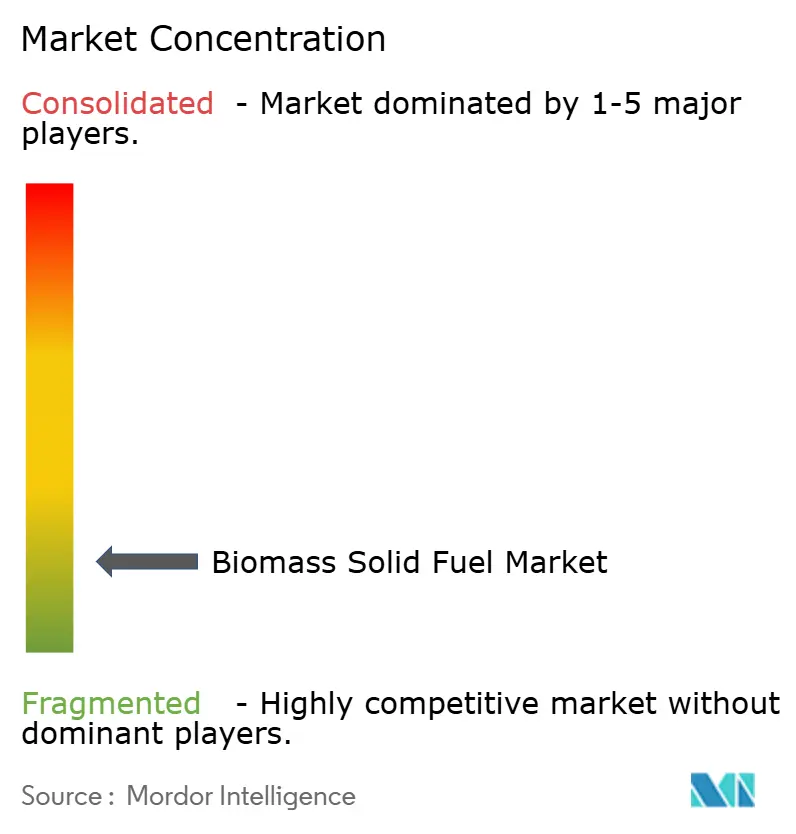

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biomass Solid Fuel Market Analysis by Mordor Intelligence

The Biomass Solid Fuel Market size is estimated at USD 28.77 billion in 2025, and is expected to reach USD 47.03 billion by 2030, at a CAGR of 10.33% during the forecast period (2025-2030).

Near-term momentum rests on stricter decarbonization rules in the European Union, buoyant policy support in Asia-Pacific, and cost-cutting breakthroughs in densification that trim logistics expenses by up to 30%. Utilities are fast-tracking coal-to-biomass conversions to comply with carbon pricing schemes, while corporate buyers aligned with RE100 and SBTi frameworks scale long-term offtake commitments that favor certified feedstock. Steam-explosion technology is improving pellet durability, helping suppliers satisfy the higher energy-density needs of the maritime sector. At the same time, tighter forest-biomass criteria effective in Europe from 2026 and shrinking subsidies in South Korea inject caution, compelling producers to sharpen operational efficiency and verification practices.

Key Report Takeaways

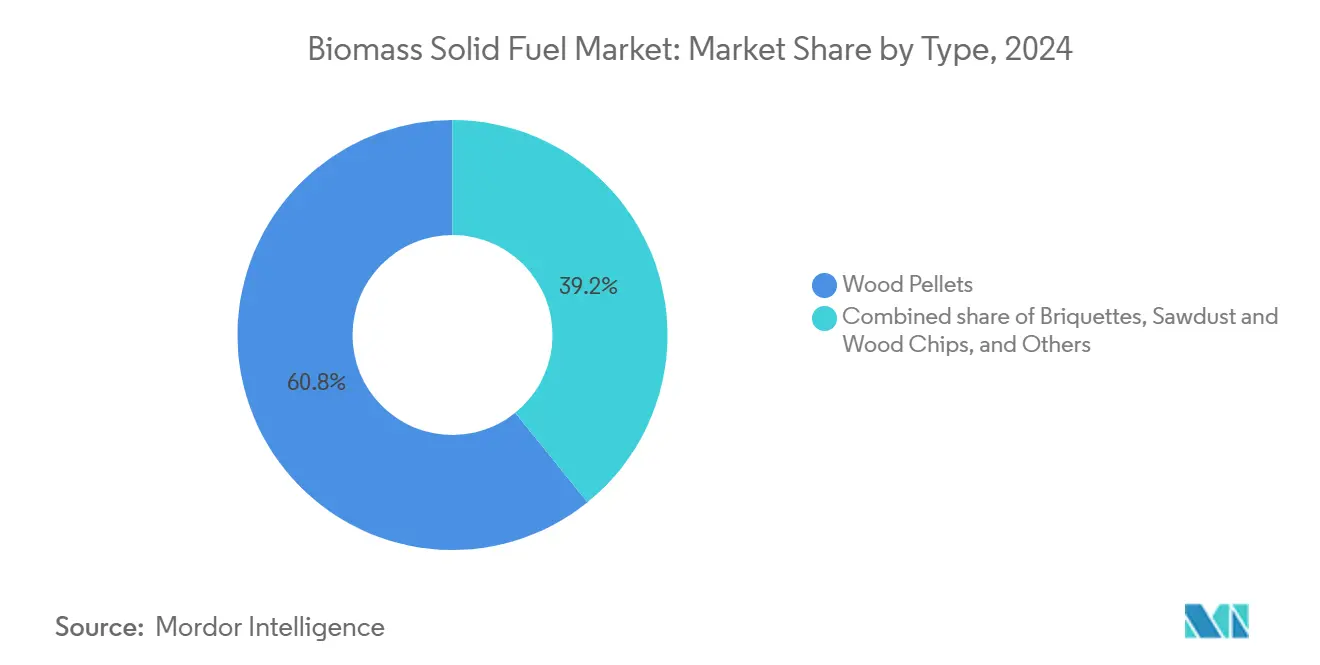

- By type, wood pellets led with 60.8% revenue share in 2024; torrefied and black pellets are projected to advance at a 21.4% CAGR through 2030.

- By application, utility-scale power generation captured 43.5% of the biomass solid fuel market share in 2024 and is poised to grow at a 10.9% CAGR to 2030.

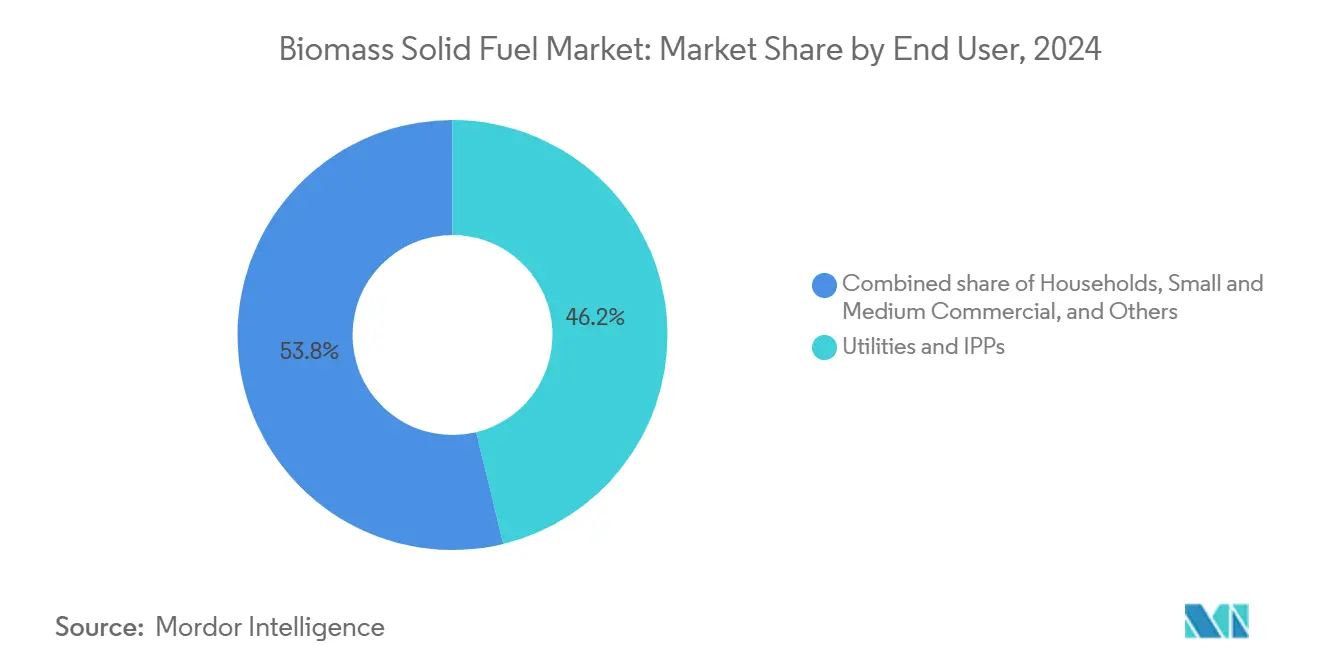

- By end user, utilities and independent power producers accounted for 46.2% of the biomass solid fuel market size in 2024 while expanding at a 10.6% CAGR through 2030.

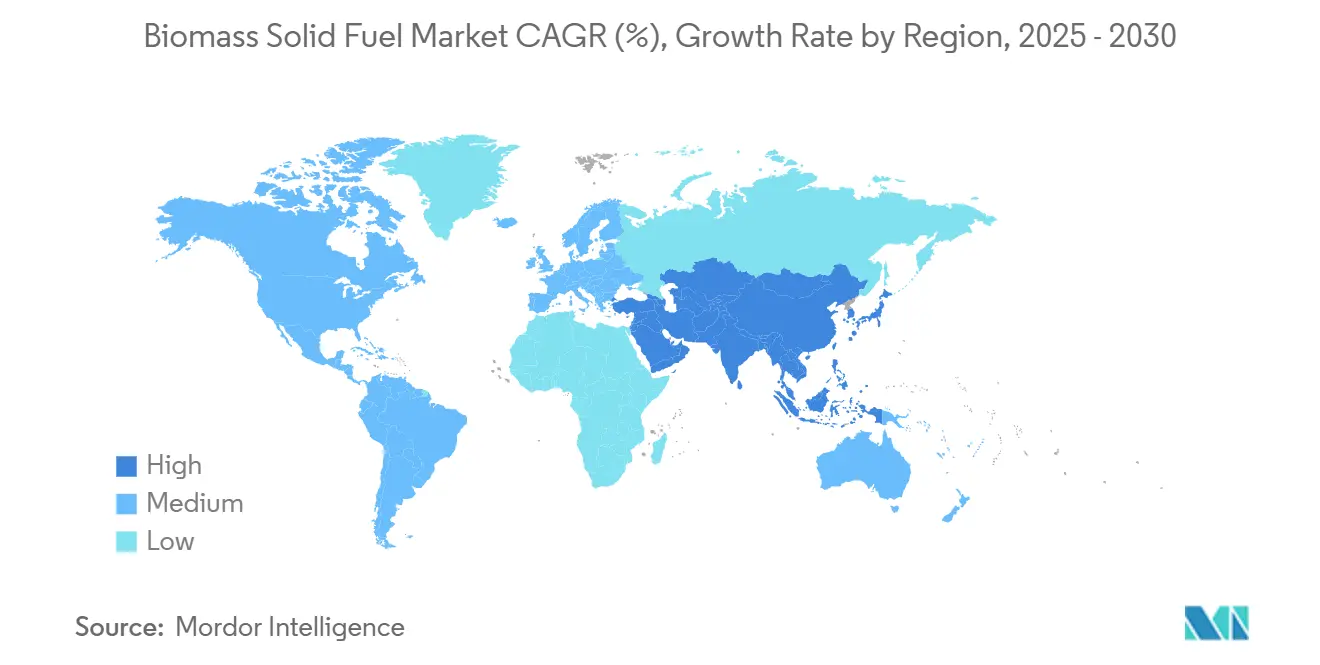

- By geography, the Asia-Pacific accounts for the largest share of 38.1% and is also projected to register a CAGR of 11.2% through 2030

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biomass Solid Fuel Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid decarbonisation mandates in the EU heating sector | 2.80% | Europe, with spillover to North America | Medium term (2-4 years) |

| Expansion of industrial co-firing projects in coal-to-biomass conversions | 2.10% | Global, concentrated in Asia-Pacific and North America | Long term (≥ 4 years) |

| Carbon-neutral corporate procurement programmes (RE100, SBTi) | 1.70% | Global, led by North America and Europe | Medium term (2-4 years) |

| Maritime demand for torrefied pellets as drop-in bunker fuel | 1.40% | Global shipping routes, key ports in Europe and Asia | Long term (≥ 4 years) |

| Abundant sawmill residue supply in SE-Asia driving export volumes | 1.20% | Southeast Asia production, global export markets | Short term (≤ 2 years) |

| Commercialisation of steam-explosion densification cutting logistics cost | 0.90% | Global, early adoption in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Decarbonization Mandates in the EU Heating Sector

Member states must reach 42.5% renewable energy in final consumption by 2030, and heating is the fastest lever to pull. Austria logged 19,181 new pellet-boiler installations during early 2024, with subsidies meeting 75% of capital cost, up to EUR 18,000 per unit. Germany mirrors this policy, offering up to 70% subsidy coverage, though potential political shifts may revise terms after 2025. The revised cascading principle under RED III gives material uses priority over energy, forcing utilities to compete for premium-grade pellets. Supply chains are pivoting toward lower-cost Brazilian imports that undercut Baltic shipments by more than USD 50 per tonne on a delivered basis. Facing these economics, Utilities are favoring long-term offtake deals to lock in certified volumes at predictable prices.

Expansion of Industrial Coal-to-Biomass Conversions

Power firms are pushing co-firing blends from 10% toward full fuel substitution, avoiding stranded-asset risks. Babcock & Wilcox retrofitted a Michigan plant to run on woody biomass and integrated carbon capture, targeting net-negative 550,000 tCO₂ annually.[1]Babcock & Wilcox, “SolveBright carbon capture integrated into biomass retrofit,” babcock.comHanwha Energy’s planned combined-heat-and-power switch in South Korea underlines broader Asian uptake even as subsidy cuts loom. Steam-explosion pretreatment boosts calorific value, letting pulverized units burn biomass without extensive mill upgrades. The upfront engineering costs favor incumbent utilities that own fuel-handling systems, widening the moat against smaller entrants.

Carbon-Neutral Corporate Procurement Programs

RE100 members’ electricity use now surpasses South Korea’s annual demand, bringing direct biomass contracts into focus. The Science Based Targets initiative encourages beyond-value-chain mitigation, nudging firms toward projects with verifiable sequestration benefits. Limited to 2% renewable penetration, Japanese buyers view biomass co-firing as an interim bridge. Sumitomo co-develops cellulosic ethanol for sustainable aviation fuel, signaling deeper vertical integration. Corporate buyers prefer long-term agreements backed by traceability audits, raising the bar for documentation across the biomass solid fuel market.

Maritime Demand for Torrefied Pellets as Drop-In Bunker Fuel

ISO 8217:2024 lets marine fuels contain up to 100% FAME, while the EU’s FuelEU Maritime rule caps fleet greenhouse-gas intensity from January 2025. Torrefied pellets reach 10,500 BTU/lb, nearly on par with coal, and remain hydrophobic—traits prized for onboard storage.[2]CIMAC, “ISO 8217:2024 marine fuel standard explained,” cimac.com BHP’s pilot voyages on bio-derived blends proved engines need minimal hardware changes. Despite price premiums, shipowners are now signaling 2- to 3-year offtake tenders to ensure supply at scale once regulation kicks in.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock competition with panelboard & pulp industries | -1.80% | Global, concentrated in North America and Northern Europe | Medium term (2-4 years) |

| Sustainability & land-use scrutiny by NGOs and financiers | -1.30% | Global, particularly Southeast Asia and North America | Long term (≥ 4 years) |

| EU RED III tightening forest-biomass criteria from 2026 | -0.90% | Europe, with global supply chain implications | Short term (≤ 2 years) |

| Rising insurance premiums for pellet-plant fire/explosion risk | -0.70% | Global, concentrated in fire-prone regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Feedstock Competition with Panelboard & Pulp Industries

Panelboard mills offer premium pricing for fine sawdust, diverting up to 15% of residue that would otherwise feed pellet lines. Advanced mills marketed by ANDRITZ process mixed species efficiently, sharpening competition.[3]ANDRITZ AG, “Advanced panelboard lines for mixed hardwood residues,” andritz.com Kraft pulp plants upgrading into biorefineries extract lignin, ethanol, and green chemicals, enabling higher margins than commodity energy pellets. In the United States, the forest-products sector contributed USD 24.1 billion in 2024 output, giving it negotiating muscle for feedstock. Pellet producers must therefore secure longer rotation contracts or co-locate capacity near secondary harvest residues to sidestep bidding wars.

Sustainability & Land-Use Scrutiny by NGOs and Financiers

Civil-society groups warn Southeast Asian pellet exports risk deforesting up to 10 million ha of tropical forest by 2040. The EU’s new deforestation-free regulation forces importers to prove legality and traceability for each consignment. Lenders now require robust certification before approving project finance, limiting capital access for plants lacking transparent land-tenure documentation. The Fern network argues that legality alone does not equal sustainability, prompting investors to demand ecological performance metrics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Torrefied Innovation Drives Premium Growth

Wood pellets dominate the biomass solid fuel market, but torrefied variants headline growth. The segment commanded a 60.8% share in 2024, while torrefied and black pellets will post a 21.4% CAGR to 2030. Steam-explosion densification raises durability and reduces freight expenditure by 30%, spurring uptake among utilities that need coal-substitute grindability. Briquettes retain a niche in European households where existing stoves favor larger formats. Agricultural-residue pellets, abundant in Southeast Asia, struggle with variable ash content that complicates quality certification. Despite this, rising palm-kernel exports suggest a path for standardized grading systems to unlock latent volumes. Torrefied fuels meet maritime energy-density thresholds, positioning suppliers that build capacity now to capture bunker-fuel demand once FuelEU Maritime rules start. The biomass solid fuel market size for torrefied products is forecast to rise from USD 2.02 billion in 2024 to USD 5.35 billion by 2030.

The torrefaction process records up to 96% thermal efficiency, creating a near-coal calorific value without sulfur emissions. Investors favor plants that integrate torrefaction and pelletizing to minimize double-handling costs, while end users require pellets with >97% durability. The agricultural-residue subsegment benefits from lower feedstock prices yet faces silo-storage challenges due to higher potassium content that elevates slagging risks. Supplier differentiation rests on testing protocols that assure combustion stability in pulverized boilers.

By Application: Utility Dominance Accelerates Transition

Utility-scale power generation held a 43.5% share in 2024 and will lead growth at a 10.9% CAGR. Carbon–pricing trajectories in the EU and Canada penalize unabated coal, incentivizing full replacements with certified pellets. Combined heat and power attracts industrial sites where steam demand aligns with onsite electricity generation, producing efficiencies above 80%. Investment cost ranges from EUR 3,410 to EUR 5,970 per kW, yet operating expenses fall sharply when low-grade residues are available. Residential heating expanded briskly in 2024 thanks to generous EU boiler incentives, but heat-pump adoption could temper further uptake after 2026. Commercial buildings prefer multi-megawatt pellet boilers that offer steady baseload and predictable maintenance schedules, helping them lock in cost savings over heating oil across a 15-year horizon.

The biomass solid fuel market size for utility applications is expected to climb from USD 11.24 billion in 2024 to USD 22.15 billion by 2030. Industrial heat users beyond CHP are exploring torrefied pellet blends to hit ISO 50001 energy-efficiency targets without retrofitting process furnaces. As carbon costs escalate, the economics tilt toward high-density biomass over liquefied natural gas imports in Europe and Northeast Asia.

By End User: Utilities Lead Infrastructure Transformation

Utilities and independent power producers controlled 46.2% of 2024 demand and will rise in lockstep with their pipeline of conversion projects. Long-term offtake deals now exceed five years on average, reflecting aversion to spot-market volatility. Industrial end users are moving toward onsite biomass boilers that secure process-heat independence and de-risk fuel-price swings. The biomass solid fuel market share held by utilities will widen as they integrate feedstock sourcing with power-plant retrofits. Small commercial consumers add incremental growth where pellet boiler replacements coincide with building renovations, though each project’s scale limits aggregated tonnage. Households anchor residual demand, especially in Alpine and Nordic regions, where winter heating days remain high. Suppliers catering to this segment bank on continued government rebates and tighter emissions caps on heating oil.

Utilities see strategic merit in co-locating pellet plants near port facilities to lower maritime freight for surplus volumes. Insurance premiums on fire risks have moved 12% higher since 2023, pushing operators to invest in spark-detection systems and nitrogen-blanketed silos that reduce ignition probability.

Geography Analysis

Asia-Pacific held a 38.1% share in 2024 and is projected to expand at a 11.2% CAGR. Japan’s palm-kernel shell imports hit 670,000 t in March 2025, while wood-pellet inflows grew 29% year-on-year to 685,000 t as new units such as the 46 MW Imari plant came online. South Korea’s December 2024 subsidy rollback curtails new projects, but retrofits already in construction continue under grandfathered terms. China aims for 58 million t of standard-coal-equivalent biomass by 2030, focusing on agricultural residues. Indonesia, Malaysia, and Thailand are scaling exports, yet mounting deforestation scrutiny may prompt stricter feedstock audits.

Europe enforces the world’s most stringent sustainability screens. Pellet consumption slipped 1.2% in 2023 to 24.5 million t after a mild winter, but residential boiler subsidies cushioned the decline. Austria’s record installations underline policy potency in stimulating demand. Finland and Sweden face resource-allocation clashes as cascading use principles prioritize timber for material applications over energy. From 2026, tighter RED III rules require producers to demonstrate forest-biomass compliance, likely spurring supply diversification outside the Baltic region.

North America dominates export supply, shipping 8.87 million t in 2024, up 3% year-on-year. Domestic consumption dipped 14%, reflecting cheaper natural-gas prices and mild winters. Drax’s USD 12.5 billion investment plan for US plants could redirect tonnage inward, shifting the biomass solid fuel market equilibrium toward tighter global seaborne balances. USA Bioenergy’s long-dated supply deal for a USD 2.8 billion sustainable-aviation-fuel complex locks in 2.2 million t of feedstock, shrinking export availability but raising in-region value capture.

Competitive Landscape

The biomass solid fuel market is fragmented yet sharpening. Enviva exited bankruptcy in December 2024 after shedding USD 1 billion in debt, enabling construction of its 11th Alabama facility with 1 million t annual capacity. Drax unified its North American subsidiaries under one brand and announced a USD 12.5 billion US build-out, underscoring consolidation and vertical-integration themes. Technology is the new battleground: producers deploying steam-explosion systems cut freight costs and meet durability specs crucial for maritime customers. The PEFC General Assembly approved RED III-aligned chain-of-custody standards in May 2025, giving certified firms a competitive edge in EU markets.

Smaller mills grapple with rising insurance costs linked to fire hazards, and certification fees now average USD 1.20 per tonne. White-space opportunities emerge in supplying torrefied pellets to shipping lines seeking compliant bunker fuel, a niche forecast to reach 7 million t by 2030. Strategic alliances between feedstock owners and technology licensors are accelerating, as seen in Sumitomo’s tie-up to co-produce ethanol and SAF from woody residues. Investors gauge market positioning on access to low-cost residues, in-house densification technology, and secured long-term contracts with creditworthy offtakers.

Biomass Solid Fuel Industry Leaders

Enviva Inc.

Drax Group plc

AS Graanul Invest

Lignetics, Inc.

Andritz AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Japan’s palm-kernel shell imports hit 670,000 t in March 2025, up 21% year-on-year, while pellet arrivals rose 29% to 685,000 t as new biomass plants commenced operations.

- February 2025: JX Nippon Oil & Gas Exploration and Sumitomo began a Louisiana BECCS project targeting 32 million gal/y of sustainable aviation fuel from woody residues.

- August 2024: South Korea eliminated Renewable Energy Credits for new biomass plants and initiated a phased-down of existing incentives starting January 2025.

- September 2024: Drax announced a USD 12.5 billion investment program for US biomass power capacity.

Global Biomass Solid Fuel Market Report Scope

| Wood Pellets |

| Briquettes |

| Sawdust and Wood Chips |

| Agricultural Residue Pellets |

| Torrefied Pellets and Black Pellets |

| Others (e.g., Char-briquettes, Coconut-shell pellets) |

| Residential Heating |

| Commercial and Institutional Heating |

| Industrial Heat Generation |

| Utility-scale Power Generation |

| CHP (Combined Heat and Power) |

| Households |

| Small and Medium Commercial |

| Large Industrial |

| Utilities and IPPs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Wood Pellets | |

| Briquettes | ||

| Sawdust and Wood Chips | ||

| Agricultural Residue Pellets | ||

| Torrefied Pellets and Black Pellets | ||

| Others (e.g., Char-briquettes, Coconut-shell pellets) | ||

| By Application | Residential Heating | |

| Commercial and Institutional Heating | ||

| Industrial Heat Generation | ||

| Utility-scale Power Generation | ||

| CHP (Combined Heat and Power) | ||

| By End User | Households | |

| Small and Medium Commercial | ||

| Large Industrial | ||

| Utilities and IPPs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the biomass solid fuel market expected to grow between 2025 and 2030?

It is projected to expand at a 10.33% CAGR, lifting annual revenue from USD 25.79 billion in 2024 to USD 47.03 billion by 2030.

Which region currently leads demand for biomass solid fuel?

Asia-Pacific holds 38.1% of global demand thanks to Japan’s and South Korea’s sizable import programs and China’s residue-utilization push.

Why are torrefied pellets attracting maritime interest?

Their higher energy density of about 10,500 BTU/lb and hydrophobic nature allow drop-in use under ISO 8217:2024 without major engine modifications.

What policy change in Europe could affect forest-biomass supply after 2026?

The EU will tighten sustainability criteria for forest biomass under RED III, requiring stricter traceability and carbon-savings verification.

How did Enviva’s restructuring alter competitive dynamics?

Shedding USD 1 billion in debt improved its balance sheet, enabling fresh investment in a 1 million t/y Alabama plant and signaling renewed capacity growth.

What challenges does feedstock competition pose to pellet producers?

Panelboard and pulp mills pay premium prices for the same residues, forcing pellet plants to secure longer contracts or pivot to lower-grade biomass streams.

Page last updated on: