Heavy Fuel Oil Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

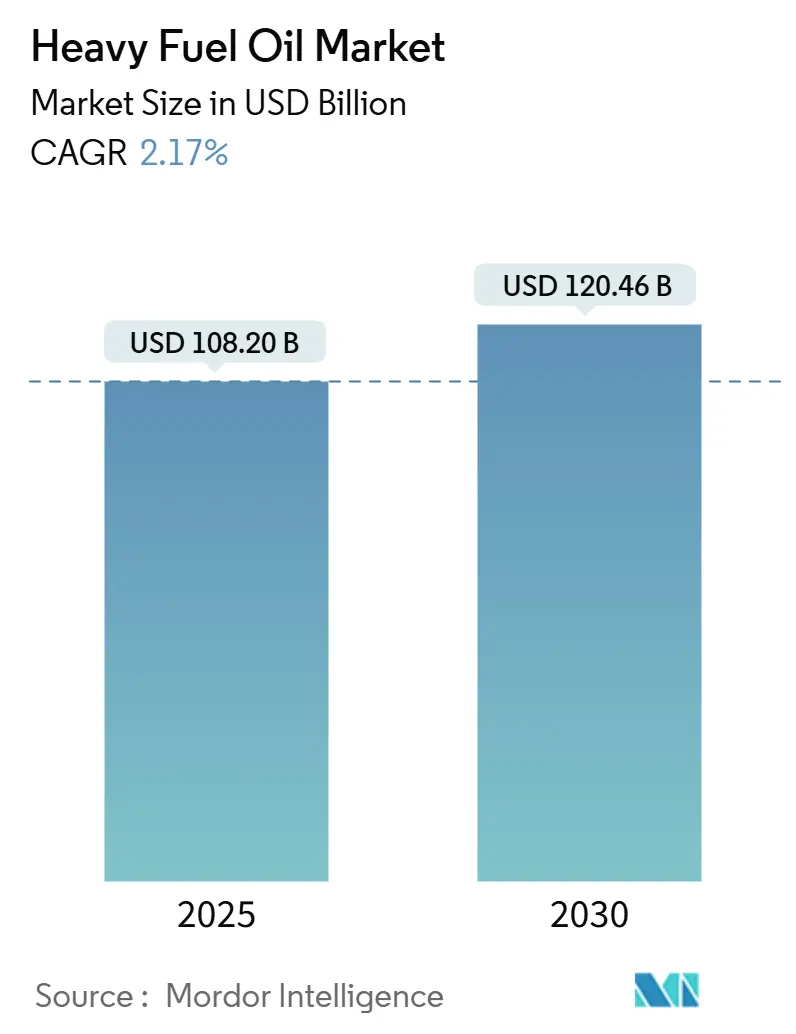

| Market Size (2025) | USD 108.20 Billion |

| Market Size (2030) | USD 120.46 Billion |

| Growth Rate (2025 - 2030) | 2.17% CAGR |

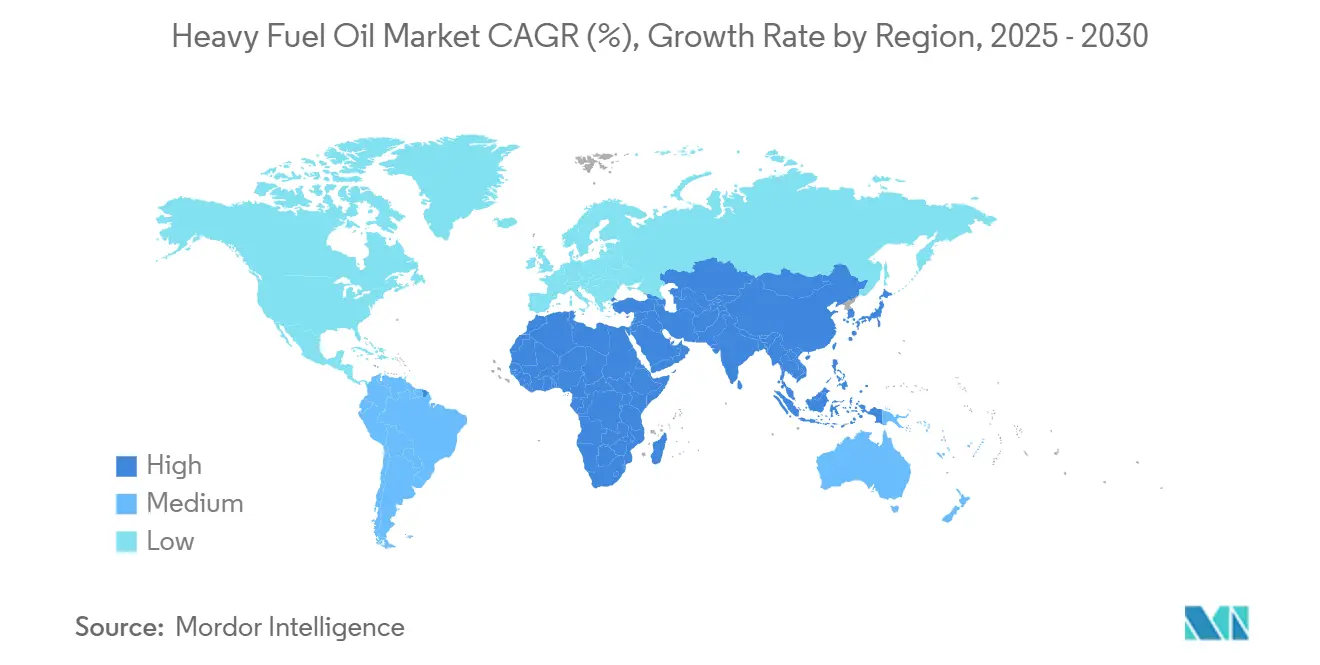

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

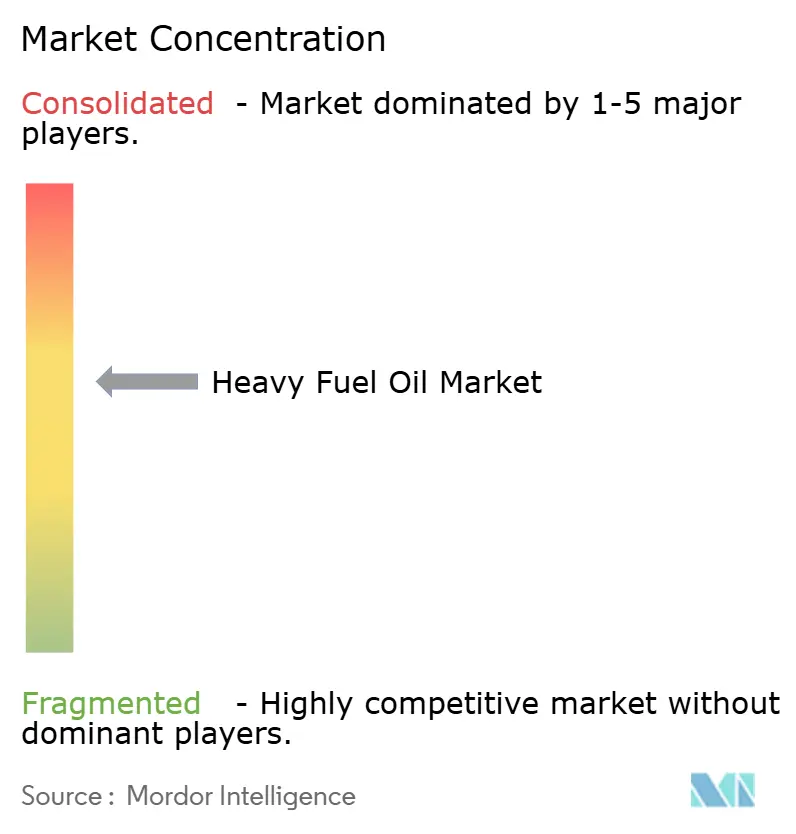

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heavy Fuel Oil Market Analysis by Mordor Intelligence

The Heavy Fuel Oil Market size is estimated at USD 108.20 billion in 2025, and is expected to reach USD 120.46 billion by 2030, at a CAGR of 2.17% during the forecast period (2025-2030).

This growth trajectory reflects a sector balancing escalating greenhouse-gas regulations with enduring industrial and marine demand. Scrubber installations keep High-Sulphur Fuel Oil (HSFO) economically attractive even as Very Low-Sulphur Fuel Oil (VLSFO) gains share under the IMO 0.50% sulfur cap.[1]BIMCO, “The Fuel Oil Market in a Decarbonizing World,” bimco.org Asia-Pacific dominates consumption, propelled by refinery expansions, China’s export-oriented output, and Singapore’s bunkering leadership. Supply-side tightness looms as high-conversion refineries curb residue yields, yet dual-fuel engine orders and HSFO–ammonia blend trials introduce fresh demand avenues. Geopolitical routing shifts, notably Red Sea diversions, lengthen voyage distances and lift bunker requirements, underscoring the market’s resilience.[2]U.S. Energy Information Administration, “Monthly Maritime Fuel Statistics 2025,” eia.gov

Key Report Takeaways

- By product type, High-Sulphur Fuel Oil held 58.1% of the heavy fuel oil market share in 2024; Very Low-Sulphur Fuel Oil is projected to advance at a 7.8% CAGR through 2030.

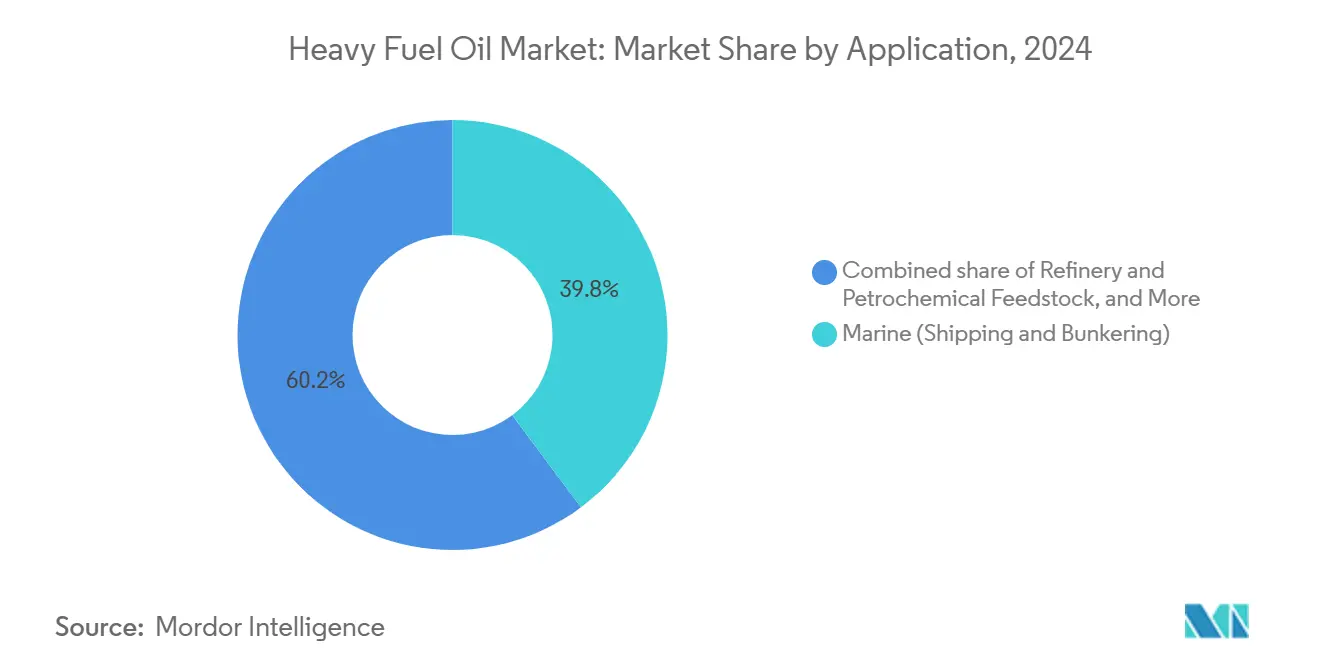

- By application, marine shipping and bunkering accounted for 39.8% of the heavy fuel oil market size in 2024, while industrial heating is projected to grow at a 4.2% CAGR through 2030.

- By geography, the Asia-Pacific region led with a 42.5% revenue share in 2024; it is forecast to expand at a 5.0% CAGR through 2030.

Global Heavy Fuel Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-spread advantage of HSFO over VLSFO | +0.8% | Global, with strongest impact in Asia-Pacific and Europe | Medium term (2-4 years) |

| Rebound of global seaborne trade volumes | +0.6% | Global, particularly Asia-Pacific trade corridors | Short term (≤ 2 years) |

| Scrubber retrofits sustaining HSFO demand | +0.4% | Global maritime routes, concentrated in Europe and Asia | Long term (≥ 4 years) |

| Expansion of captive HSFO power units at LNG export terminals | +0.3% | Middle East, North America, Australia | Long term (≥ 4 years) |

| Dual-fuel 2-stroke engines burning HSFO–ammonia blends | +0.2% | Global maritime sector, early adoption in Europe | Long term (≥ 4 years) |

| Industrial petcoke-to-HFO co-firing in cement kilns | +0.2% | Asia-Pacific, Middle East, emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price-Spread Advantage of HSFO over VLSFO

A persistent USD 150-200 per-ton differential between HSFO and VLSFO has shortened the payback period for scrubber investments to roughly 18-24 months for vessels on high-utilization routes.[3]Ship & Bunker, “HSFO–VLSFO Spread Update 2025,” shipandbunker.com Fleet owners now view scrubbers not only as compliance tools but also as hedges against fuel-price volatility, influencing contract negotiations and new-build specifications. About half of the new oceangoing orders in early 2024 included dual-fuel or scrubber-ready designs, ensuring flexibility amid uncertain regulations. The spread often widens during geopolitical supply squeezes because VLSFO availability is the first to tighten. With the IMO acknowledging a slower-than-expected phase-out of conventional fuels, operators see additional runway for HSFO-linked savings.

Rebound of Global Seaborne Trade Volumes

Post-pandemic trade normalization and route diversions have lengthened average voyage distances, resulting in increased fuel consumption per cargo unit. Red Sea security threats have redirected Asia-Europe traffic around the Cape of Good Hope, adding nearly 6,000 nautical miles and lifting bunker demand by 35-40% per sailing, according to EIA vessel-tracking data. Although transit counts dipped, total fuel burned rose, benefiting operators positioned along the Indian Ocean corridor. Container freight rates climbed sharply on the North European lanes, yet carriers retained HSFO usage to preserve their margins. This structural rerouting is expected to maintain elevated demand for heavy fuel oil in the market even after headline trade tonnage levels off.

Scrubber Retrofits Sustaining HSFO Demand

Roughly 5,200 ships will run with exhaust-gas cleaning systems by the end of 2024, representing only 4% of the fleet, yet consuming close to 15% of marine residual fuel, as retrofits currently concentrate on large container, tanker, and bulker classes. Charter markets reward scrubber-equipped tonnage through premium daily rates when HSFO–VLSFO spreads widen. Falling retrofit costs—now USD 2-4 million per vessel—open adoption to midsize owners. Hybrid open/closed-loop designs add flexibility in stricter ports, preserving the attractiveness of HSFO even under tightening coastal emission controls.

Expansion of Captive HSFO Power Units at LNG Export Terminals

Mega-scale liquefaction plants require reliable backup electricity during maintenance or grid instability. Qatar’s North Field expansion alone is adding more than 2 GW equivalent of HSFO-fired capacity to safeguard LNG throughput, consuming up to 100,000 tons of fuel yearly. Similar configurations are emerging on the U.S. Gulf Coast and in Western Australia as developers prioritize uptime over incremental emissions costs. These captive units create stable, location-anchored demand that is insulated from marine decarbonization pressures, diversifying the heavy fuel oil market footprint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter IMO & EU ETS carbon regulations | -0.9% | Global maritime sector, strongest in EU waters | Short term (≤ 2 years) |

| Fuel-switching to LNG, methanol & biofuels | -0.7% | Europe, North America, progressive Asian markets | Medium term (2-4 years) |

| Declining residue output from high-conversion refineries | -0.4% | Global, particularly impacting Asia-Pacific supply | Long term (≥ 4 years) |

| Arctic port-state limits on black-carbon emissions | -0.2% | Arctic shipping routes, Northern European ports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter IMO & EU ETS Carbon Regulations

The European Union extended its Emissions Trading System to maritime transport in 2024, and FuelEU Maritime imposes a 2% reduction in greenhouse-gas intensity from 2025. Allowance purchases add USD 206 per ton to VLSFO bunker costs this year and could exceed USD 2,400 by 2050. Large liners face multi-billion-dollar compliance outlays, prompting a shift in routes toward non-EU hubs and accelerating the development of low-carbon fuels. The bifurcation between compliant and non-compliant fleets becomes increasingly apparent, dampening HSFO demand in European trades and influencing terminal investment priorities.

Fuel-Switching to LNG, Methanol & Biofuels

Alternative marine fuels are gaining traction as supply chains mature: global LNG bunkering sites now exceed 200, and commercial methanol orders have surpassed 350 vessels in 2024. Singapore authorized B30 biodiesel blends, offering a drop-in pathway for reducing carbon intensity. Yet, biofuel availability covers barely 2% of the world's marine demand, and price premiums remain volatile. Transition speeds diverge by segment; container lines and tankers move first due to scale and predictable routes, while tramp shipping sticks to conventional fuels. This gradual migration restrains, but does not derail, the heavy fuel oil market over the forecast horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: HSFO Dominance Faces VLSFO Acceleration

High-Sulphur Fuel Oil commanded 58.1% of the heavy fuel oil market share in 2024, underpinning the segment’s revenue leadership despite regulatory headwinds. The heavy fuel oil market size attributable to HSFO is expected to expand modestly, driven by the economic benefits of scrubber technology and the fuel’s continued availability. Very Low-Sulphur Fuel Oil, however, registers the fastest 7.8% CAGR through 2030, propelled by compliance-centric operators sailing in emission control zones. Low-sulfur fuel Oil occupies a shrinking niche as owners gravitate to either extreme of the sulfur spectrum. Intermediate Fuel Oil grades (IFO 180/380) remain relevant where viscosity dictates engine performance, especially in industrial heating circuits unable to tolerate lighter distillates.

Fleet renewal strategies amplify the bifurcation: newbuilds either integrate scrubbers or adopt engines certified for VLSFO or low-carbon blends. Refiners respond by tweaking residue upgrading to optimize both HSFO and VLSFO slates, depending on local demand elasticity. Bio-blended residual fuels currently capture less than 1% of the volume but offer a test bed for carbon reduction without wholesale infrastructure changes. Overall, product diversification mitigates the heavy fuel oil market's vulnerability to single-segment shocks, although HSFO’s pricing edge remains the primary demand catalyst.

By Application: Marine Leadership Meets Industrial Momentum

Marine shipping absorbed 39.8% of the heavy fuel oil market size in 2024, reflecting the fuel-intensive nature of transoceanic voyages. Ultra-large container ships can burn 100 tons daily, anchoring predictable offtake for suppliers. However, the segment’s growth moderates under decarbonization rules and the uptake of alternative fuels, opening up space for industrial heating, which is projected to grow at a 4.2% CAGR through 2030. Manufacturers in the cement, metals, and chemicals industries capitalize on HSFO’s stable calorific value and often lower delivered cost compared to pipeline gas in infrastructure-scarce regions.

Power generation remains in decline across OECD economies as renewables gain a larger share of the grid, yet dispatchable HSFO units persist in emerging markets, which are grappling with reliability gaps. Captive refinery and petrochemical boilers also lock in demand because heavy fuel oil serves as both an energy source and a process feedstock. This diversified end-use tapestry distributes consumption risk and underpins the heavy fuel oil market even as the marine sector gradually cleans up its fuel mix.

Geography Analysis

The Asia-Pacific’s 42.5% share in 2024 cements it as the fulcrum of the heavy fuel oil market, aided by the expansion of refinery complexes and the region’s centrality to global trade lanes. China’s record refinery output in 2023 spilled into 2025 via the Jieyang and Shenghong megaprojects, ensuring ample residual streams despite domestic demand moderation. Singapore, which processes more than 50 million tons of bunker sales annually, sets regional price signals even after first-half 2025 volumes dipped amid Red Sea detours. Ongoing approvals for bio-blended bunkers demonstrate regulatory agility rather than retreat, supporting a forecasted 5.0% CAGR to 2030 across the Asia-Pacific region.

Europe ranks second in consumption but faces the stiffest regulatory drag. EU ETS inclusion and FuelEU Maritime escalate compliance costs, hastening fleet fuel-switching and prompting some services to relocate to non-EU hubs. Refinery rationalization compounds supply uncertainty, as more than 60% of global closure candidates are located in Europe, poised to squeeze residual fuel availability within a decade. Nevertheless, robust bunkering infrastructure in Rotterdam, Antwerp, and Gibraltar sustains a sizeable compliant-fuel market anchored in sophisticated logistics and blending capabilities.

North America benefits from heavy-crude inflows and high-conversion refineries capable of tailoring residue output to price cycles. The Gulf Coast, in particular, optimizes heavy feedstocks to meet the demand for bunkering in Latin America and Africa, even as domestic power generation shifts toward gas and renewables. Policy moves, such as California’s refinery closure, could tighten regional supplyalthoughgh pipeline connectivity allows for balancing. The Middle East and parts of Africa leverage low upstream costs to maintain HSFO competitiveness, with captive power generation at industrial and LNG complexes anchoring volume. Taken together, these regional tapestries preserve a globally diversified heavy fuel oil market that dampens localized disruptions.

Competitive Landscape

The heavy fuel oil market exhibits moderate concentration. Integrated majors—ExxonMobil, Shell, Saudi Aramco—blend upstream heft with complex refining networks, while trading houses such as Vitol, Trafigura, and Glencore arbitrage cargo flows and bunker blending margins. ExxonMobil’s USD 30 billion investment plan combines residue upgrading in Singapore with low-carbon R&D, signaling a dual-track strategy that hedges conventional fuel revenue while preparing for cleaner substitutes.[4]Reuters, “ExxonMobil to Invest USD 30 Billion in Low-Carbon and Resid Upgrades,” reuters.com

Trading intermediaries gained prominence during 2024’s logistics disruptions; Vitol recorded a USD 13 billion profit, underscoring the value of storage optionality and risk hedging across volatile spreads. Specialist bunker suppliers, notably Bunker Holding A/S and World Fuel Services, vie on service quality, multi-grade delivery capability, and documentation expertise. Compliance-service integration—encompassing EU ETS reporting and carbon-offset procurement—has emerged as a competitive differentiator, particularly for operators servicing EU-linked trades.

Technology alignment drives strategic divergence. Some firms deepen HSFO-scrubber supply chains, banking on a prolonged spread advantage, while others prioritize VLSFO and biofuel production or invest in methanol infrastructure. Geopolitical fragmentation reinforces regional strongholds, as Middle Eastern refiners dominate African and South Asian demand, U.S. Gulf Coast plants supply the Atlantic trades, and Asian majors leverage their proximity to consumption nodes. This configuration supports a resilient yet dynamic heavy fuel oil market poised for gradual, rather than sudden, structural change.

Heavy Fuel Oil Industry Leaders

Shell

ExxonMobil

BP

Vitol

Trafigura

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Chevron finalized its USD 55 billion acquisition of Hess, gaining Guyana’s heavy-crude output that feeds residual fuel manufacturing.

- June 2025: Marubeni Corporation forged a strategic alliance in the marine fuel sector with SINOPEC FUEL OIL SALES CO., LTD., a subsidiary of China Petroleum & Chemical Corporation.

- June 2024: Saudi Aramco signed USD 25 billion in gas-expansion contracts with Sinopec, reducing domestic HSFO power burn by broadening gas supply.

- June 2024: Canada's Transport Minister declared a domestic ban on heavy fuel oils (HFO) in Arctic waters. The ban, set to be enforced via an Interim Order, comes as the government amends existing regulations.

Global Heavy Fuel Oil Market Report Scope

| High Sulphur Fuel Oil (HSFO) |

| Low Sulphur Fuel Oil (LSFO) |

| Very Low Sulphur Fuel Oil (VLSFO) |

| Intermediate Fuel Oil (IFO 180, IFO 380) |

| Residual Fuel Oil (RFO) |

| Marine (Shipping and Bunkering) |

| Power Generation |

| Industrial Heating |

| Refinery and Petrochemical Feedstock |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| Netherlands | |

| France | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | High Sulphur Fuel Oil (HSFO) | |

| Low Sulphur Fuel Oil (LSFO) | ||

| Very Low Sulphur Fuel Oil (VLSFO) | ||

| Intermediate Fuel Oil (IFO 180, IFO 380) | ||

| Residual Fuel Oil (RFO) | ||

| By Application | Marine (Shipping and Bunkering) | |

| Power Generation | ||

| Industrial Heating | ||

| Refinery and Petrochemical Feedstock | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| Netherlands | ||

| France | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the heavy fuel oil market by 2030?

The heavy fuel oil market is projected to reach USD 120.46 billion by 2030, reflecting a 2.17% CAGR over 2025-2030.

Which region leads global heavy fuel oil demand?

Asia-Pacific holds 42.5% of 2024 volume and is also the fastest-growing region at a 5.0% CAGR to 2030.

How fast is Very Low-Sulphur Fuel Oil growing compared with HSFO?

VLSFO records a 7.8% CAGR through 2030, outpacing HSFO, which grows modestly as scrubbers sustain its cost advantage.

What share does marine shipping hold in heavy fuel oil consumption?

Marine shipping and bunkering account for 39.8% of 2024 demand, maintaining the single-largest application share.

How are EU regulations affecting heavy fuel oil use?

EU ETS and FuelEU Maritime raise compliance costs, encouraging fuel switching and curbing HSFO demand on Europe-linked routes.

Which companies are expanding residue upgrading capacity?

ExxonMobil's Singapore complex, along with Middle East refiners, is adding units that optimize residue conversion for flexible product slates.

Page last updated on: