Biomass Briquette Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

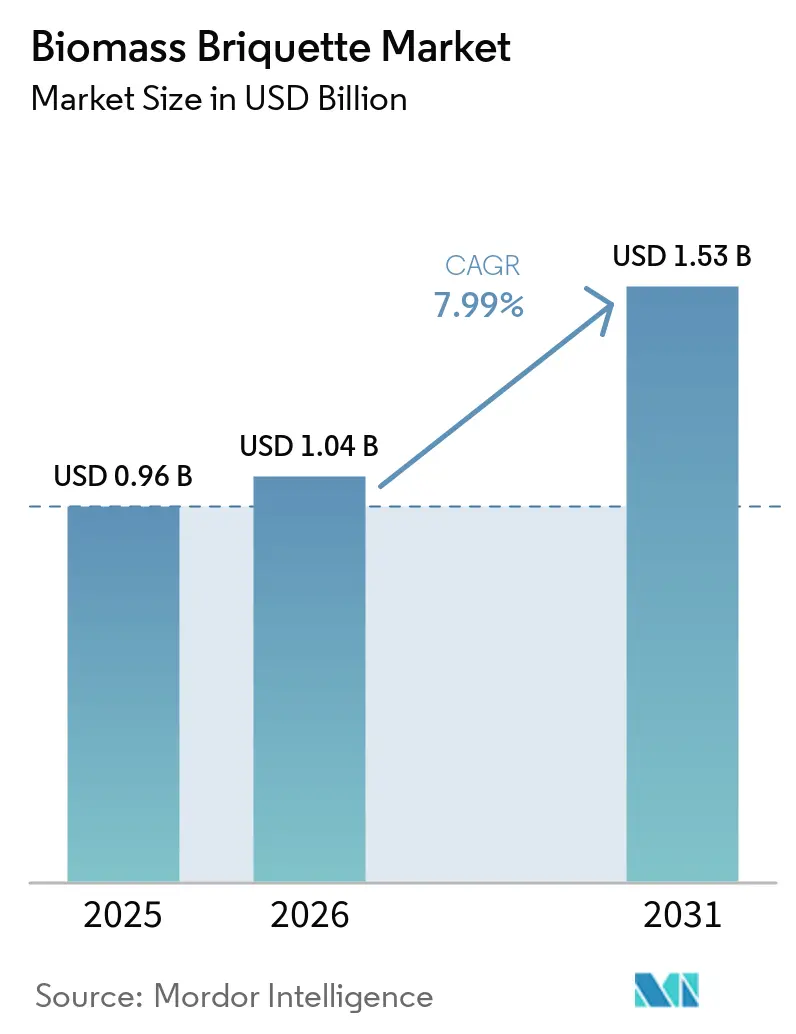

| Market Size (2026) | USD 1.04 Billion |

| Market Size (2031) | USD 1.53 Billion |

| Growth Rate (2026 - 2031) | 7.99% CAGR |

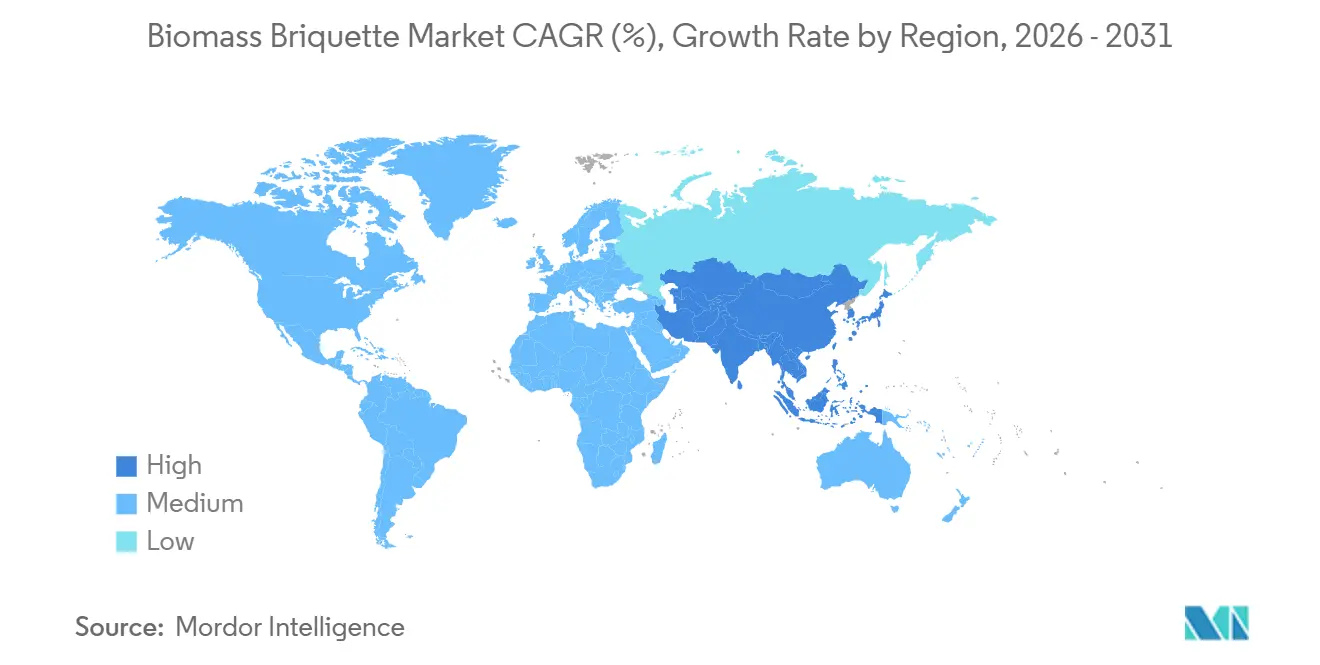

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

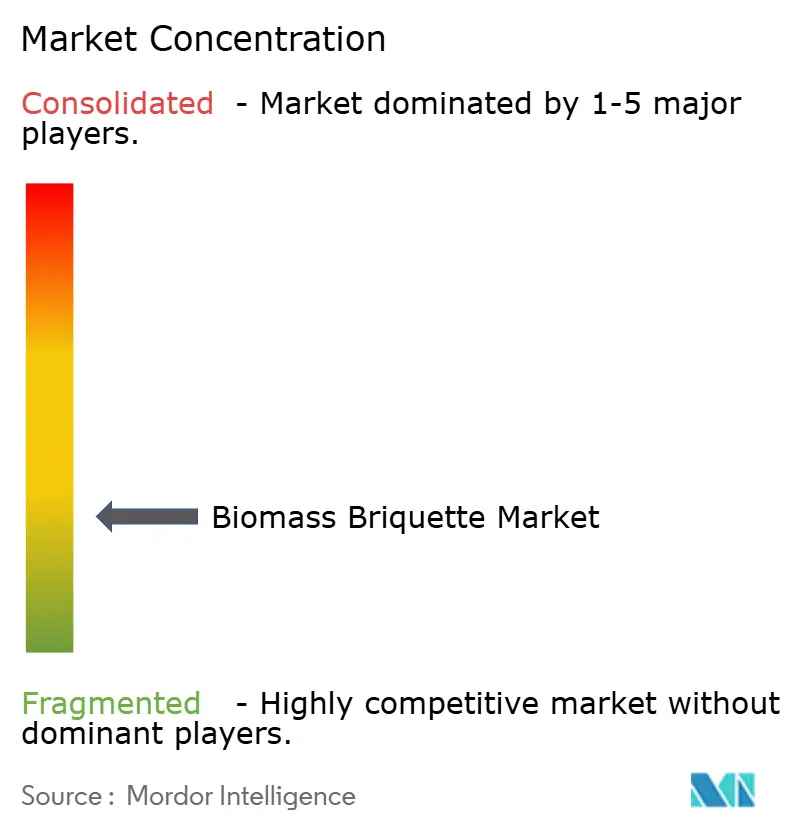

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biomass Briquette Market Analysis by Mordor Intelligence

The Biomass Briquette Market size is projected to expand from USD 0.96 billion in 2025 and USD 1.04 billion in 2026 to USD 1.53 billion by 2031, registering a CAGR of 7.99% between 2026 and 2031. Accelerating policy support for 5%–7% biomass co-firing at coal plants, rapid cost declines in torrefaction reactors, and stricter maritime fuel standards are steering utilities and shipping lines toward low-sulfur solid biofuels. At the same time, clean-cooking programs in Sub-Saharan Africa and South Asia are broadening the addressable household base, while the EU Carbon Border Adjustment Mechanism (CBAM) is redirecting trade to higher-density torrefied variants.[1]European Commission, “Carbon Border Adjustment Mechanism,” ec.europa.eu Feedstock competition with the wood-pellet export sector and a temporary liquefied natural gas (LNG) surplus in Southeast Asia temper near-term pricing power, but rising carbon prices and expanding boiler-retrofit subsidies counterbalance these headwinds.

Key Report Takeaways

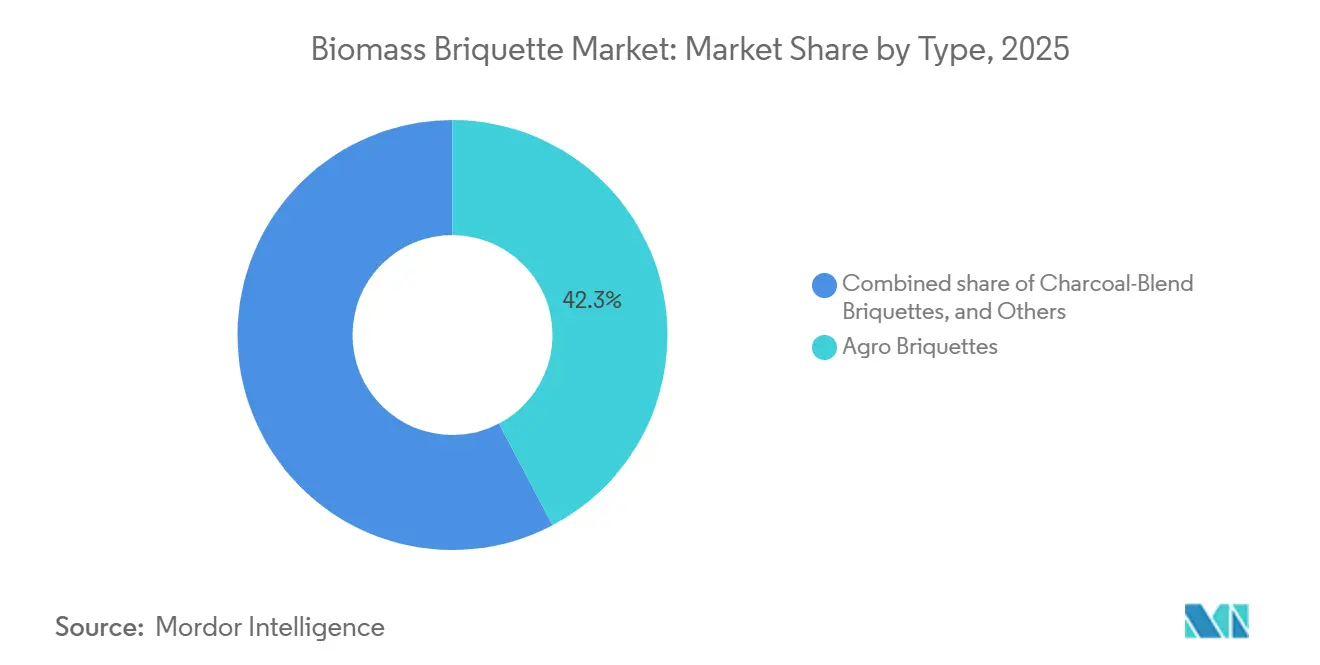

- By type, agro briquettes commanded 42.3% of the biomass briquette market share in 2025. Torrefied briquettes are projected to expand at a 10.3% CAGR, the fastest among types.

- By raw material, sawdust accounted for 29.5% of feedstock demand in 2025, while rice husk is advancing at a 9.5% CAGR.

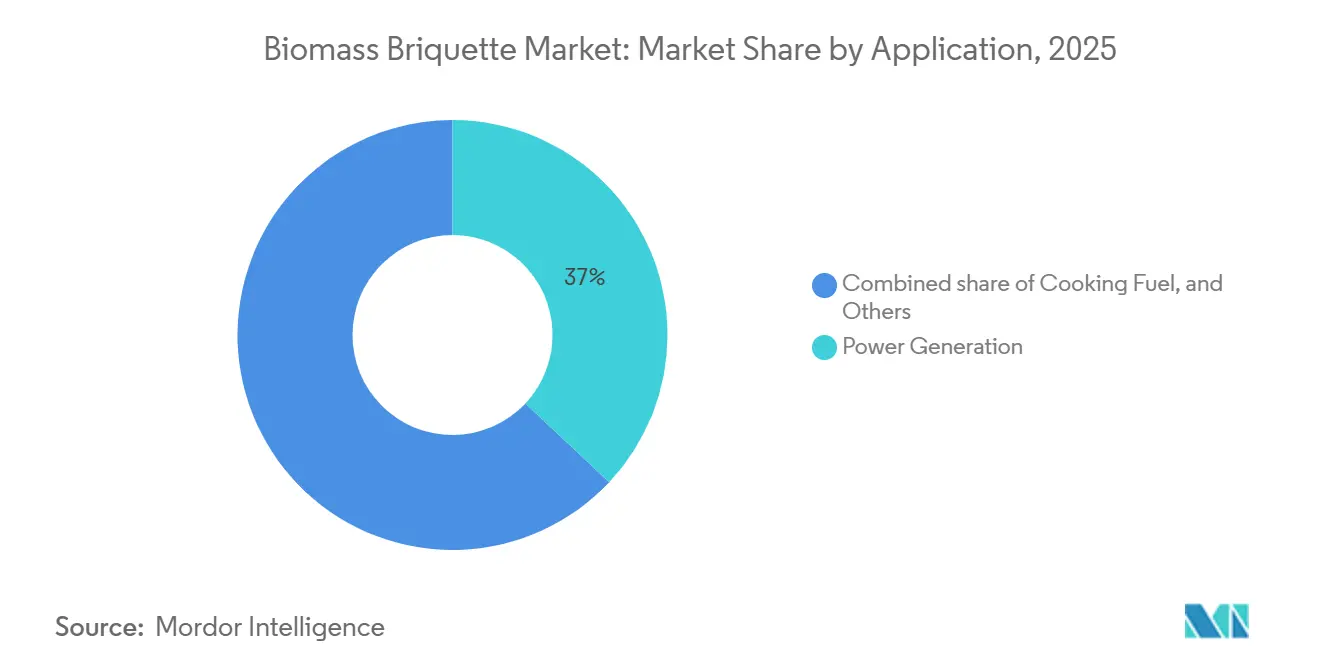

- By application, power generation held 37.0% of demand in 2025; cooking fuel is growing at 9.9% per year through 2031.

- By Geography, asia-pacific led with 48.9% revenue share and is forecast to grow at 8.8% annually through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biomass Briquette Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government co-firing mandates in coal plants | +1.8% | Asia-Pacific, Europe | Medium term (2-4 years) |

| Surge in boiler retrofits for solid biofuels | +1.2% | Europe, North America | Short term (≤2 years) |

| Rural electrification programs in Sub-Saharan Africa | +0.9% | Sub-Saharan Africa | Long term (≥4 years) |

| EU CBAM spill-over | +1.0% | Europe, North Africa, Turkey | Medium term (2-4 years) |

| Commercial-scale torrefaction breakthroughs | +1.5% | Global | Medium term (2-4 years) |

| Maritime sector switch to low-sulfur solid fuels | +0.7% | Global ports | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Government Co-firing Mandates in Coal Plants

India, Indonesia, and Poland now stipulate biomass blends of 5%-10% by energy content at coal stations, creating predictable offtake volumes for briquette suppliers.[2]Press Information Bureau, “Biomass Co-firing in Thermal Power Plants,” pib.gov.in India alone co-fired 164,976 metric tons by March 2025, while Indonesia’s PLN targets 3.2 million metric tons annually by 2028. Poland tops up each percentage point above 5% with a EUR 15 per MWh subsidy.[3]European Commission, “Carbon Border Adjustment Mechanism,” ec.europa.eu ISO 17225-8 testing is emerging as the de facto quality gate.

Surge in Boiler Retrofits for Solid Biofuels

Industrial and district-heating operators in the United Kingdom, Denmark, and Canada are converting legacy coal and oil boilers, spurred by carbon-pricing schemes and subsidy pools totaling GBP 120 million in the UK alone. Ørsted’s GBP 400 million Avedøre retrofit eliminated 1.2 million metric tons of coal a year. Canada’s Clean Fuel Regulations now extend credits to industrial heat users that shift to certified briquettes.[4]Government of Canada, “Clean Fuel Regulations,” canada.ca

Rural Electrification Programs in Sub-Saharan Africa

World Bank-funded gasifier projects in Kenya, Uganda, and Tanzania are replacing charcoal with briquettes, covering 47,000 households. Nigeria’s Rural Electrification Agency deployed 250 kW briquette generators in 35 villages, offsetting diesel imports priced at USD 1.20 per liter. The African Development Bank’s Desert to Power initiative targets 10 million new connections by 2030.

EU Carbon Border Adjustment Mechanism Spill-over

From January 2026, importers must disclose embedded GHG emissions; briquettes made on coal-heavy grids in Turkey now attract a levy, redirecting demand to torrefied products that deliver 22 MJ/kg and lower freight emissions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-priced LNG glut in Southeast Asia | -1.3% | Southeast & South Asia | Short term (≤2 years) |

| High intra-continental logistics cost | -0.9% | Africa, South America, rural Asia | Medium term (2-4 years) |

| Stricter particulate-matter norms on household stoves | -0.6% | Europe, North America | Medium term (2-4 years) |

| Competing demand from pellet export industry | -0.8% | North America, Nordics, Russia | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Low-priced LNG Glut in Southeast Asia

Spot LNG below USD 10 per MMBtu kept Thai and Philippine industries on gas through early 2026, delaying briquette boiler conversions. An Asian Development Bank survey showed 62% of Vietnamese plants mothballed retrofits when gas slipped under USD 9 per MMBtu.

High Intra-continental Logistics Cost for Low-density Briquettes

Road freight of sawdust briquettes over 1,000 km in Sub-Saharan Africa costs USD 35–45 per metric ton, or up to 40% of plant-gate prices. Torrefaction lifts bulk density to 800 kg/m³, but the 25% price premium curbs uptake beyond export channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Torrefaction Unlocks Coal-Parity Performance

Torrefied Briquettes are on course to expand at a 10.3% CAGR, far above the biomass briquette market average, reflecting utilities’ need for hydrophobic, high-energy products that slipstream into existing coal conveyors. The biomass briquette market size for torrefied variants is projected to reach USD 450 million by 2031, commanded by high-heating-value shipments to Europe and Northeast Asia. Agro Briquettes remain cost-advantaged at USD 100-130 per metric ton and held 42.3% of the biomass briquette market share in 2025.

Wood Briquettes continue to serve premium residential heat markets thanks to 0.5%-2.0% ash and predictable combustion profiles. Charcoal-Blend Briquettes, with 10%-20% charcoal fines, are popular among African households for fast ignition and reduced smoke. Emerging categories such as algae-based briquettes remain pilot-scale until waste-collection and regulatory hurdles are cleared.

By Raw Material: Rice Husk Scales on Co-Firing Momentum

Rice husk is accelerating at a 9.5% CAGR as Indonesia and Vietnam monetize residues through 10% co-firing pilots, elevating its share of the biomass briquette market size for raw materials. Sawdust remained dominant at 29.5% in 2025, but pellet-sector pull has tightened supply and nudged prices up by 12% year-on-year.

Bagasse, abundant in Brazil and India, requires energy-intensive drying yet benefits from proximity to sugar mills. Groundnut Shells and Coconut Husks capture low-opportunity-cost feedstocks for cooking-fuel briquettes in West Africa and the Philippines. Forest residues gain traction in Nordic district-heating schemes that demand FSC-certified inputs to comply with EU sustainability criteria.

By Application: Cooking Fuel Captures Clean-Energy Transition

Cooking Fuel is forecast to grow at 9.9% annually as donor-funded stove rollouts bypass liquefied petroleum gas bottlenecks. Nigeria’s 250,000 improved cookstoves reduce indoor PM by 60% versus three-stone fires. Power Generation retained 37.0% of demand in 2025, underpinned by co-firing mandates in India, Indonesia, and Poland.

Industrial Process Heating is next in line as carbon-credit payouts shorten payback to four years for Canadian pulp mills burning certified briquettes. Commercial and Institutional Heating enjoys tariff-protected contracts, while Residential Space Heating in Europe faces subsidy-driven competition from heat pumps.

Geography Analysis

Asia-Pacific accounted for 48.9% of 2025 revenue and will expand at 8.8% annually, anchored by India’s 5%–7% co-firing rule and China’s small-coal-unit retirements. Indonesia targets 3.2 million t/y rice-husk blends by 2028, and Japan imports torrefied briquettes to earn feed-in-tariff credits despite USD 35–50 per metric ton ocean freight.

Europe ranks second, propelled by GBP 120 million in UK boiler-retrofit grants and Denmark’s Avedøre conversion. CBAM’s embedded-carbon reporting favors high-energy torrefied products, while Nordic countries channel forestry residues into district heating for >80% GHG savings.

North America advances on the back of southeastern U.S. sawdust briquette exports to Japan and South Korea and Canada’s Clean Fuel Regulations, which credit industrial heat users who switch from natural gas. South America’s growth is led by Brazil’s bagasse surplus and Colombia’s coffee-husk initiatives. The Middle East and Africa remain dominated by clean-cooking programs using rice-husk and groundnut-shell briquettes.

Competitive Landscape

The biomass briquette market is fragmented. C.F. Nielsen and RUF are supplying modular lines, while integrators such as Vyncke and ECOSTAN wrap boiler retrofits into long-term briquette offtakes. Torrefaction capex averages USD 250 per annual metric ton but is slated to fall 50% by 2028 as ANDRITZ brings twin-screw reactors to market. Perpetual Next's proposed large-scale biomethanol project in Estonia highlights the industry's focus on achieving economies of scale, distinguishing it from smaller or less competitive biomass initiatives.

Maritime trials by Maersk and CMA CGM on briquette-fuelled auxiliares chase EUR 200/t CO₂-eq FuelEU Maritime credits. Patent filings for lignin binders accelerate as producers scramble to meet the EPA’s 1.3 g/h stove PM limit. ISO 17225-8 certification defines cross-border trade baselines, advantaging quality-assured suppliers over informal small mills.

Biomass Briquette Industry Leaders

Radhe Industrial Corporation

C.F. Nielsen A/S

RUF Briquetting Systems

ECOSTAN

Biomass Briquettes UK Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Nigeria rolled out 250,000 cookstoves for rice-husk briquettes.

- January 2026: Singapore bunker sales of biofuel blends hit 880,000 tons.

- October 2025: The EU Deforestation Regulation imposed geolocation rules for wood fuels.

- March 2025: Georgetown County announced plans for a USD 4 billion biomass plant at a former paper mill, expected to create up to 500 jobs.

Global Biomass Briquette Market Report Scope

A biomass briquette is a renewable biofuel produced by compressing loose organic waste into dense, solid blocks or cylinders. It is an environmentally friendly and cost-efficient alternative to traditional fossil fuels such as coal, charcoal, and firewood.

The Biomass Briquette Market is segmented into type, raw material, application, and geography. By type, the market is segmented into agro briquettes, wood briquettes, torrefied briquettes, charcoal-blend briquettes, and other types. By raw material, the market is segmented into sawdust, rice husk, bagasse, groundnut shells, coconut husk and shell, corn stover and straw, forestry residues, and mixed agricultural waste. By application, the market is segmented into power generation, industrial process heating, commercial and institutional heating, residential space and water heating, cooking fuel, and other applications. The report also covers the market size and forecasts for the biomass briquette market across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Agro Briquettes |

| Wood Briquettes |

| Torrefied Briquettes |

| Charcoal-Blend Briquettes |

| Others |

| Sawdust |

| Rice Husk |

| Bagasse |

| Groundnut (Peanut) Shells |

| Coconut Husk and Shell |

| Corn Stover and Straw |

| Forestry Residues |

| Mixed Agricultural Waste |

| Power Generation |

| Industrial Process Heating |

| Commercial and Institutional Heating |

| Residential Space and Water Heating |

| Cooking Fuel |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Agro Briquettes | |

| Wood Briquettes | ||

| Torrefied Briquettes | ||

| Charcoal-Blend Briquettes | ||

| Others | ||

| By Raw Material | Sawdust | |

| Rice Husk | ||

| Bagasse | ||

| Groundnut (Peanut) Shells | ||

| Coconut Husk and Shell | ||

| Corn Stover and Straw | ||

| Forestry Residues | ||

| Mixed Agricultural Waste | ||

| By Application | Power Generation | |

| Industrial Process Heating | ||

| Commercial and Institutional Heating | ||

| Residential Space and Water Heating | ||

| Cooking Fuel | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the biomass briquette market ?

The recycled base oil market stands at USD 1.04 billion in 2026 and is expected to reach USD 1.53 billion by 2031, expanding at a 7.99% CAGR over 2026-2031.

Which segment will grow the fastest through 2031?

Torrefied Briquettes are expected to post the highest growth at 10.3% CAGR thanks to coal-parity performance and CBAM incentives.

Why is rice husk gaining popularity as a feedstock?

Utility-scale co-firing pilots in Indonesia and Vietnam are monetizing rice-husk residues, driving a 9.5% CAGR for this feedstock.

How are boiler retrofits affecting demand?

Subsidies in the UK, Denmark, and Canada shorten payback periods, boosting industrial demand for certified briquettes.

What is the main geographical driver of market volume?

Asia-Pacific, led by India and China, commands 48.9% of revenue and grows at 8.8% annually on mandated biomass co-firing.

How do torrefied briquettes help shipping lines?

They qualify for near-zero well-to-wake emissions under IMO rules, generating valuable FuelEU Maritime credits.

Page last updated on: