Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

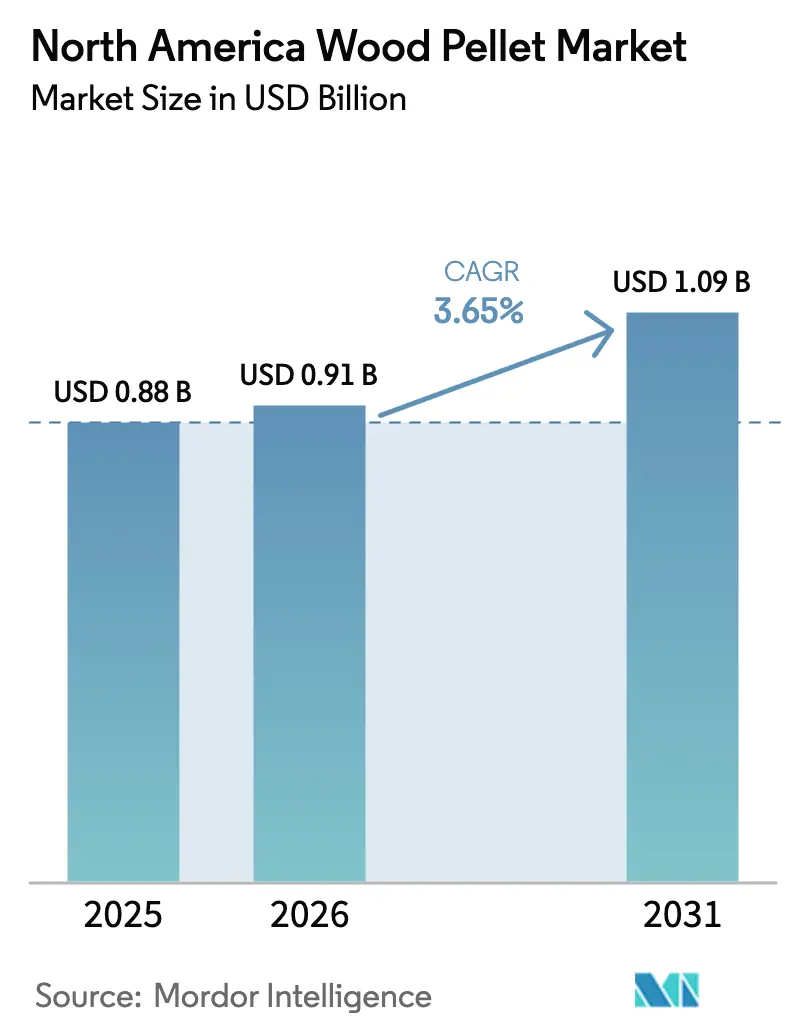

| Base Year Market Size (2025) | USD 0.88 Billion |

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.09 Billion |

| Growth Rate (2026 - 2031) | 3.65% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Wood Pellet Market Analysis by Mordor Intelligence

The North America Wood Pellet Market size is expected to increase from USD 0.88 billion in 2025 to USD 0.91 billion in 2026 and reach USD 1.09 billion by 2031, growing at a CAGR of 3.65% over 2026-2031.

Growth reflects a maturing residential-heating base that is balanced by rising utility-scale power generation and industrial thermal demand. Vertically integrated producers are reinforcing supply chains, while feedstock diversification into agricultural residues and short-rotation crops is buffering mills against sawmill curtailments. Utility demand is accelerating as federal and state renewable mandates converge with carbon-capture incentives, and torrefied black pellets are gaining traction because their higher energy density cuts freight cost per gigajoule. At the same time, residential sales face headwinds from generous heat-pump rebates, and ESG scrutiny is pushing investors to favor mills that hold Sustainable Biomass Program or Forest Stewardship Council certification. Logistics inflation, fiber-supply tightening, and the capital intensity of new torrefaction lines are tempering the near-term growth outlook, yet overall market momentum remains positive as negative-emissions business models emerge.

Key Report Takeaways

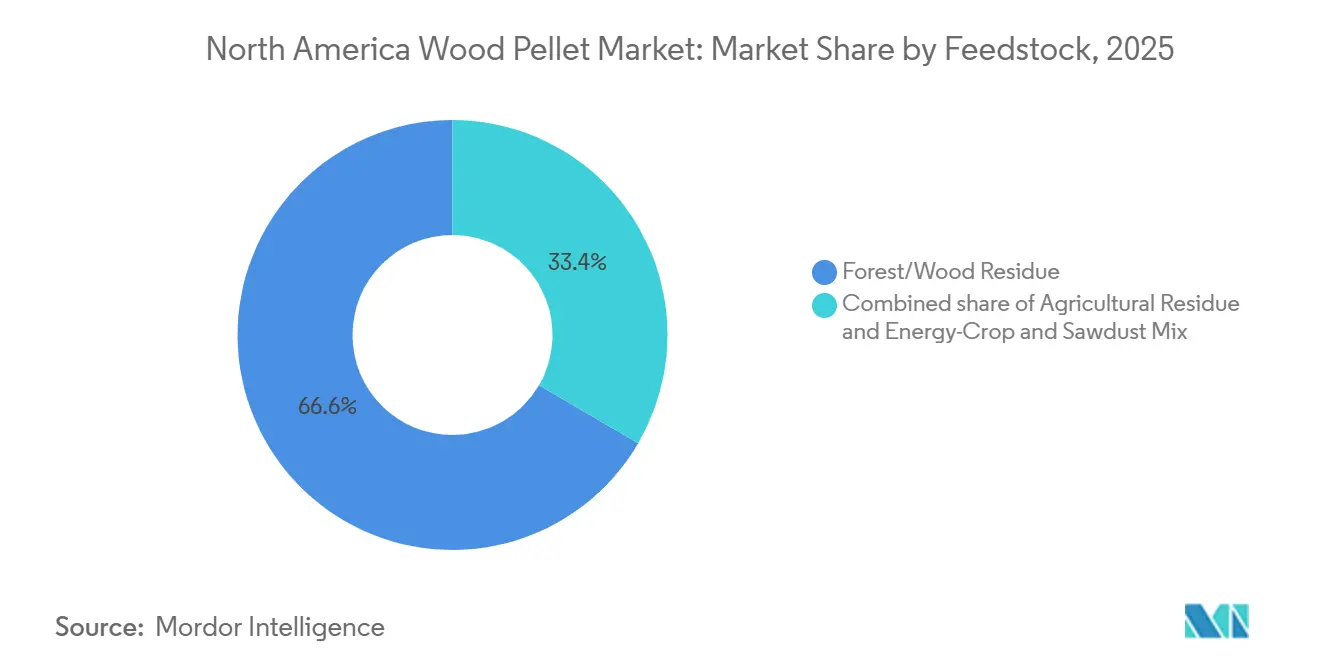

- By feedstock, forest and wood residue led with 66.6% of the North America wood pellet market share in 2025, whereas agricultural residue pellets are forecast to expand at a 4.8% CAGR through 2031.

- By grade, utility-grade white pellets captured 58.2% revenue share in 2025, while torrefied black pellets are projected to post the fastest 8.4% CAGR to 2031.

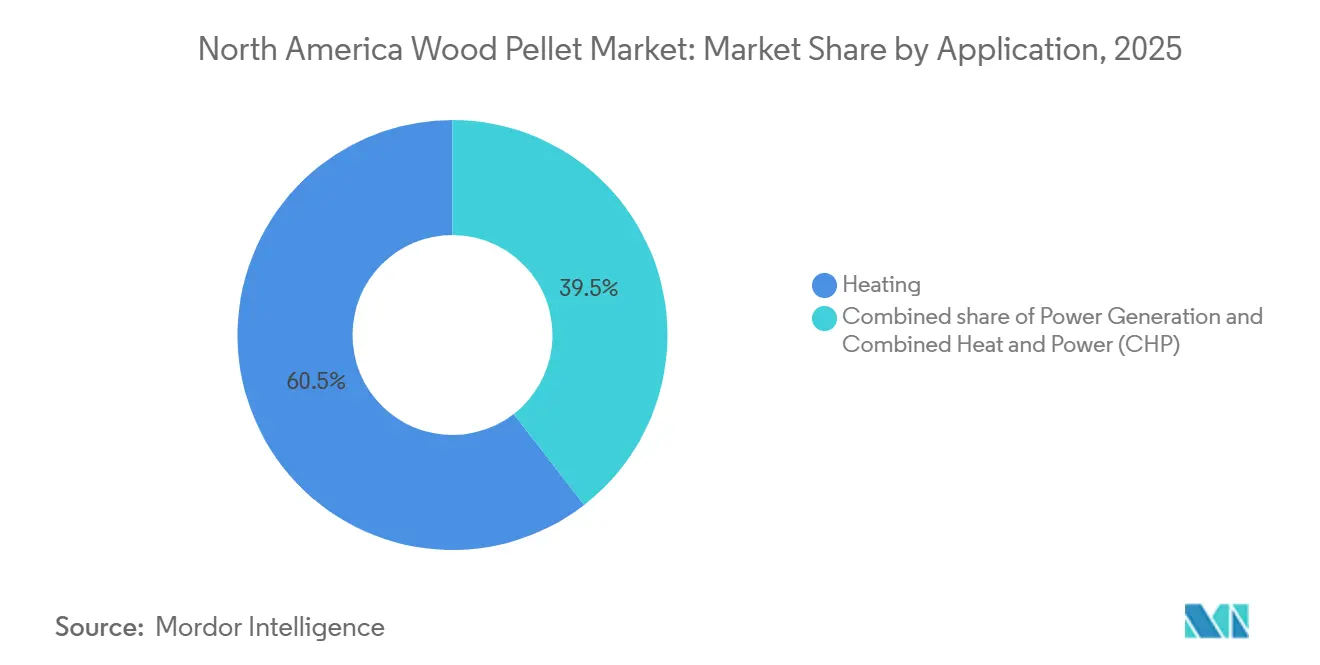

- By application, heating accounted for a 60.5% share of the North America wood pellet market size in 2025, yet power generation is advancing at a 7.9% CAGR during 2026-2031.

- By end-user, residential customers held a 50.9% share in 2025, and the industrial and utility segment is set to grow at a 7.5% CAGR through 2031.

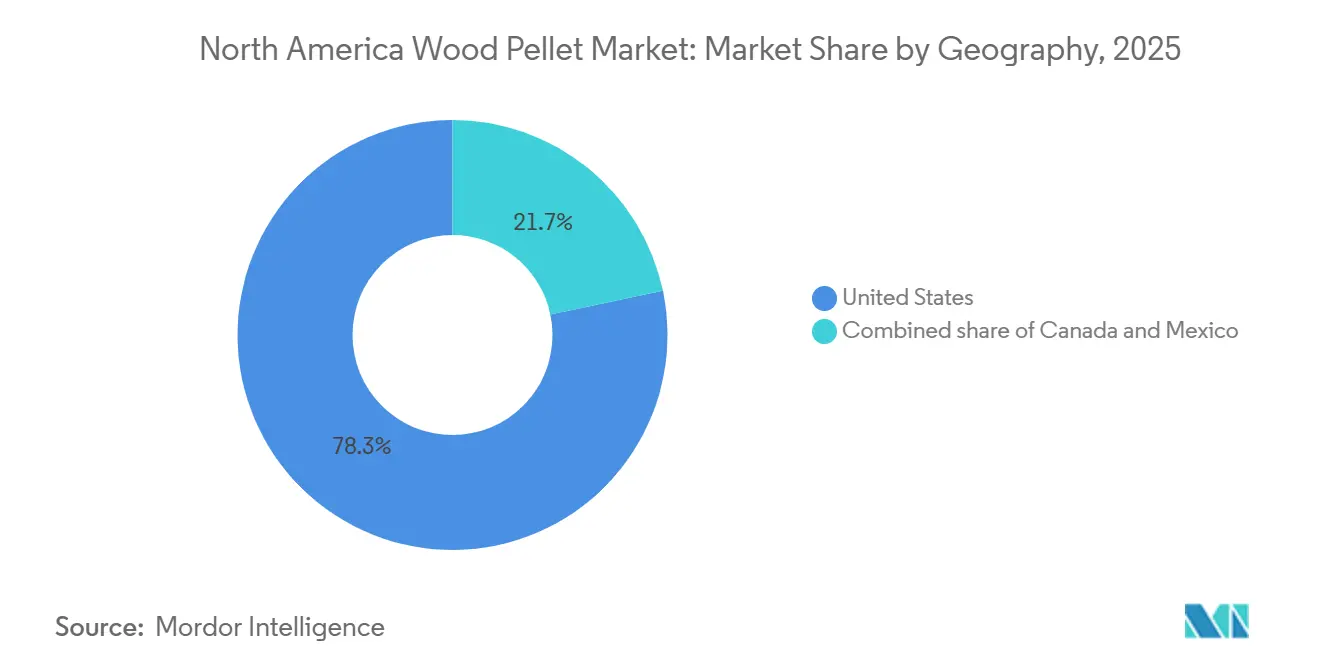

- By geography, the United States dominated with a 78.3% share in 2025, whereas Canada is poised for the swiftest 4.2% CAGR out to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Wood Pellet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal and state renewable targets drive utility demand | 1.2% | United States (Southeast production corridor, Midwest utilities) | Long term (≥ 4 years) |

| Volatile fossil-fuel prices enhance pellet competitiveness | 0.8% | United States and Canada (residential heating markets, northern states/provinces) | Short term (≤ 2 years) |

| Clean Fuel Regulations credits in Canada stimulate uptake | 0.6% | Canada (British Columbia, Alberta, Quebec) | Medium term (2-4 years) |

| Torrefied-pellet technology boosts energy density and lowers logistics cost | 0.5% | Global (export-oriented producers in US Southeast, Canadian mills targeting Asia-Pacific) | Medium term (2-4 years) |

| Carbon-neutral corporate thermal certificates emerge | 0.4% | United States and Canada (corporate procurement, voluntary carbon markets) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Federal and State Renewable Targets Drive Utility Demand

State renewable portfolio standards and enhanced federal clean-energy incentives continue to anchor the offtake strategies of electric utilities. Drax committed USD 12.5 billion to build new U.S. biomass power plants by 2030, and each project is being designed with carbon-capture systems to qualify for premium 45Q credits.[1]Farhat Eamon Akil, “Drax Aims for $12.5 Billion US Power Push Drawn by Subsidies,” Bloomberg Law, bloomberglaw.com Georgia Power likewise proposed 80 MW of biomass capacity under contracts exceeding 30 years to lock in dispatchable generation and hedge gas-price volatility.[2]Dave Williams, “Georgia Power Seeks PSC Approval to Build Plants That Burn Wood Pellets,” Augusta Chronicle, augustachronicle.com Regulators are validating this approach; in March 2024, the Michigan Public Service Commission ruled that dispatchable biomass remains vital for resource adequacy, rejecting early contract terminations.[3]Michigan Public Service Commission, “MPSC Rejects Early Termination of Two Consumers Energy Contracts,” michigan.gov These decisions reinforce the view that wood pellets are a bridge fuel capable of meeting near-term decarbonization targets while preserving grid reliability.

Volatile Fossil-Fuel Prices Enhance Pellet Competitiveness

Propane and heating-oil price spikes during the 2025-26 winter narrowed the cost gap with pellets, improving payback periods for stove and boiler upgrades. Henry Hub natural gas averaged USD 4.30 per MMBtu, yet rural households paid the propane equivalent of USD 27.50 per MMBtu, while delivered premium pellets cost roughly USD 15 per MMBtu.[4]U.S. Energy Information Administration, “Weekly Retail Propane Prices,” eia.gov The arbitrage is most compelling in off-pipeline regions of the Northeast, Upper Midwest, and Atlantic Canada, although the Inflation Reduction Act’s USD 2,000 federal heat-pump tax credit, alongside state rebates up to USD 8,000, is incentivizing homeowners to electrify. Residential pellet suppliers must therefore emphasize predictable fuel costs and local sourcing to remain competitive, particularly as utilities introduce time-of-use tariffs that favor overnight heat-pump operation.

Clean Fuel Standard Credits in Canada Stimulate Uptake

Canada’s Clean Fuel Regulations assign lifecycle carbon-intensity scores and allow compliant wood pellets to generate tradable credits, creating a secondary revenue stream for industrial users. British Columbia’s CAD 65 carbon tax (USD 48) and Alberta’s Technology Innovation and Emissions Reduction system further enhance pellets’ cost advantage over natural gas. As a result, food processors, pulp mills, and district heating networks are adopting pellets to meet both energy and compliance goals, underpinning Canada’s 4.2% CAGR through 2031. Drax’s February 2025 agreement to supply certified pellets for sustainable aviation fuel production illustrates the commercial premium placed on transparent carbon accounting.

Torrefied-Pellet Technology Boosts Energy Density and Lowers Logistics Cost

Torrefaction raises pellet calorific value to 20-22 GJ t⁻¹, trimming freight charges per gigajoule by roughly 15% and enabling higher co-firing ratios in coal boilers. ANDRITZ validated commercial performance in 2025 with an 85% mass yield plant in Finland, while Drax added pilot torrefaction capacity to its Aliceville, Alabama mill during its USD 50 million expansion. Although single-line capital costs of USD 50-100 million limit adoption to well-capitalized incumbents, utilities are willing to pay a 10-15% premium for hydrophobic black pellets that avoid moisture-related degradation and lower retrofit costs. The 8.4% CAGR forecast for torrefied pellets signals industry confidence that energy density and coal-compatibility will outweigh their higher upfront price.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Logistics inflation squeezes pellet margins | -0.6% | United States and Canada long-haul corridors and export ports | Short term (≤ 2 years) |

| Sawmill curtailments tighten fiber supply | -0.5% | U.S. Southeast and Pacific Northwest, Canadian interior | Medium term (2-4 years) |

| ESG scrutiny on forest biomass dampens investment | -0.4% | Global portfolios impacting North American exporters | Long term (≥ 4 years) |

| Rapid heat-pump adoption in cold-climate states | -0.3% | U.S. Northeast, Upper Midwest, Ontario, Quebec | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Logistics Inflation Squeezes Pellet Margins

Railroad tariff increases and trucking cost inflation pushed delivered pellet prices higher in 2025. For Southeast mills serving Midwest utilities, rail can account for up to 40% of delivered cost, especially when ports such as Savannah and Mobile experience congestion that triggers demurrage fees. Producers with torrefaction lines partially offset these costs by shipping more energy per tonne, yet the USD 50-100 million capex requirement sidelines smaller operators. Retail-oriented mills face their own pressure as short-haul trucking rates rise faster than stove-grade pellet prices, forcing some to consolidate or close.

Sawmill Curtailments Tighten Fiber Supply

Weak housing activity cut lumber output in 2024-25, reducing low-cost sawdust and chip availability. Mills competed with pulp producers for residual fiber or experimented with corn stover and wheat straw, which carry higher ash content and require boiler adjustments. High ash levels raise maintenance costs for end users and dilute margin for producers, while British Columbia’s mountain-pine-beetle timber depletion compounded shortages in Canada’s interior. The result is a dual challenge of higher feedstock prices and capital outlays for preprocessing agricultural residues.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Residue Diversification Hedges Fiber Risk

Forest and wood residues commanded 66.6% of the North America wood pellet market share in 2025, reflecting the dominance of sawdust, chips, and forest thinnings sourced from integrated timber operations. Agricultural residue pellets, however, are projected to register a 4.8% CAGR to 2031 as producers hedge against sawmill curtailments that constrained fiber supply during 2024-25. Agricultural feedstocks such as corn stover and wheat straw can theoretically provide 200-300 million dry tonnes annually, but seasonal collection logistics, variable moisture, and higher ash contents of 3-6% complicate scale-up. Producers that master preprocessing and ash-mitigation technologies can capture industrial and utility demand, provided they secure boilers capable of handling less-pure fuels.

Toward the end of the decade, short-rotation woody crops like hybrid poplar and willow may supply select mills willing to invest in dedicated plantations, enabling predictable yields on marginal land. Although these energy crops remain a niche today, their strategic value lies in stable pricing and carbon-sequestration benefits that appeal to ESG-minded buyers. The feedstock landscape is therefore bifurcating: commodity white pellets destined for residential stoves remain wood-residue dominant, while industrial and utility buyers increasingly accept diversified blends to secure volume and carbon-credit eligibility.

By Grade: Torrefied Pellets Target Utility Coal Replacement

Utility-grade white pellets accounted for 58.2% of 2025 revenues, serving power plants under multi-year offtake agreements. Premium-grade pellets, distinguished by moisture below 8% and ash under 0.5%, capture residential and commercial users who prioritize low maintenance. Standard-grade material fills the middle tier for small industrial boilers that tolerate slightly higher impurities. Torrefied black pellets, however, are forecast to grow at an 8.4% CAGR through 2031, fueled by their 20-22 GJ/t energy density and hydrophobic properties.

ANDRITZ’s 2025 commercial line proved that mass and energy yields above 85% and 95% are attainable, while Drax’s Alabama pilot signals U.S. commitment to scale. Torrefied pellets eliminate the need for covered storage and minimize moisture-linked degradation during trans-Pacific shipments, opening Asian and Middle Eastern markets that were previously risky for white pellets. Utilities value the ability to co-fire at higher rates without costly boiler derates, reinforcing the premium pricing potential despite higher production capex. The grade mix is therefore expected to evolve toward a dual-track system: affordable white pellets for heating and premium black pellets for utility and industrial buyers focused on logistics savings and carbon strategy.

By Application: Power Generation Outpaces Heating

Heating retained a 60.5% share of the North America wood pellet market size in 2025, supported by mature stove penetration in rural areas without natural-gas service. Nonetheless, power generation is set to expand at the fastest 7.9% CAGR from 2026-31 as utilities convert coal units or build dedicated biomass plants equipped with carbon-capture systems. Drax’s USD 12.5 billion investment road-map exemplifies the move toward negative-emissions facilities that leverage enhanced federal tax credits.

Combined heat and power (CHP) remains a strategic niche, with efficiency levels reaching 65-80% and more than 4,700 U.S. installations in operation. Industrial campuses and institutional buildings that can harness waste heat present a steady demand stream for pellets, especially in regions with carbon pricing. Residential demand, by contrast, faces intensified competition from subsidized heat pumps, forcing pellet suppliers to position on fuel-price stability and local economic benefits.

By End-User: Industrial and Utility Segments Lead Growth

Residential buyers maintained a 50.9% market share in 2025, yet the segment is expected to lose ground as electrification rises in cold-climate states. Industrial and utility users are projected to grow at a 7.5% CAGR, buoyed by long-term power-purchase agreements and Clean Fuel Standard credits that monetize lifecycle emissions reductions. Commercial facilities, including schools and hospitals, occupy a middle space, attracted by lower fuel costs than heating oil but cautious about retrofit outlays. Animal-bedding users, who often accept off-spec pellets, represent a small but steady outlet for by-product volumes that fail premium-grade specifications.

Regulatory decisions underscore pellets’ role in reliability planning. When Michigan’s Public Service Commission declined to cancel two biomass PPAs, it affirmed that dispatchable pellet generation remains critical for reserve margins. Industrial operators also value the credit revenue from provincial carbon markets, as evidenced by British Columbia’s CleanBC program at CAD 65/t CO₂e. These dynamics suggest the demand center of gravity will move from households to larger industrial and utility off-takers seeking both energy and compliance value.

Geography Analysis

The United States dominated with a 78.3% share of the North America wood pellet market in 2025, leveraging Southeast production clusters near export ports and Midwest utilities. Drax’s expansion of its Aliceville, Alabama, facility and Georgia Power’s 80 MW biomass proposal highlight the integration of feedstock supply, generation assets, and long-term PPAs that secure revenue visibility. Residential sales face structural pressure as the Inflation Reduction Act’s heat-pump incentives accelerate electrification in northern states, although the Michigan Public Service Commission decision confirms regulatory support for biomass plants where reliability is a concern. ESG scrutiny from asset managers such as Legal & General, which issued stringent deforestation policies in 2024, is tightening certification requirements and pushing U.S. mills to adopt SBP or FSC audits.

Canada, while representing a smaller base, is forecast to grow fastest at 4.2% CAGR through 2031. Federal Clean Fuel Regulations and provincial carbon pricing in British Columbia, Alberta, and Quebec reward low-carbon pellets with tradeable credits, boosting industrial boiler conversions and CHP installations. Drax’s 2025 memorandum with Pathway Energy to supply sustainable aviation fuel feedstock underscores Canada’s positioning as a certified, traceable source of biomass for next-generation fuels. That said, the interior British Columbia fiber supply is tightening as mountain-pine-beetle salvage winds down, forcing mills to source coastal fiber at a higher cost, which could constrain regional margins.

Mexico remains a marginal player due to limited forestry infrastructure and competing uses for agricultural residues in domestic biogas projects. While torrefied-pellet exports to Asia could unlock growth, the capital expense of torrefaction lines and port upgrades poses a significant barrier. Unless new policy incentives or foreign direct investment materialize, Mexico is likely to contribute only a small share of regional volume through 2031.

Competitive Landscape

North America’s market is moderately concentrated, with Enviva and Drax controlling a significant slice of export-oriented capacity. Drax cemented its position by acquiring Pinnacle Renewable Energy in 2021, extending its reach into the Pacific Northwest and improving access to Asian markets. Enviva, after restructuring in 2024, divested certain Southeast assets, creating space for regional firms such as Lignetics, Highland Pellets, and Pacific BioEnergy to capture local heating accounts. These mid-tier players compete on delivered cost, customer service, and turnkey boiler solutions rather than scale.

Strategy divergence is evident. Large incumbents are channeling capital into torrefaction and bioenergy-with-carbon-capture projects to capture premium carbon credits, while regional producers pivot toward agricultural residues to mitigate wood-fibre risk and to serve short-haul customers less exposed to rail tariffs. Technology vendors marketing mobile torrefaction units offer potential disruption by allowing densification close to the harvest site, thereby reducing raw biomass haulage.

Certification standards are becoming a gating factor. European utilities and global investors increasingly mandate SBP or FSC chain-of-custody, pushing uncertified mills to upgrade or risk exclusion. As a result, new entrants face high capital and compliance hurdles, although opportunities remain in commercial-scale CHP, district heating, and industrial thermal applications that value proximity and service flexibility over export scale.

North America Wood Pellet Industry Leaders

Enviva Partners LP

AS Graanul Invest

Drax Group PLC

Fram Renewable Fuels LLC

Lignetics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Drax signed a preliminary deal with Pathway Energy to supply certified pellets for sustainable aviation fuel starting in 2029, contingent on Pathway’s final investment decision.

- September 2024: Drax announced a USD 12.5 billion plan to build U.S. biomass power plants equipped with carbon capture, targeting first operations by 2030.

- September 2024: Georgia Power sought regulatory approval for three biomass plants totaling 80 MW, anchored by a 30-year PPA with Altamaha Green Energy and shorter contracts with International Paper.

- March 2024: Michigan Public Service Commission blocked early termination of two Consumers Energy biomass PPAs, citing grid reliability concerns.

North America Wood Pellet Market Report Scope

Wood pellets are renewable fuels manufactured from compressed sawdust or wood chips. They can be used to heat houses and businesses as a biomass fuel. Wood pellets can be made from forest residues and low-quality logs that can be handled as rubbish.

The North America wood pellet market is segmented by feedstock, grade, application, and geography. By feedstock, the market is divided into forest/wood residue, agriculture residue, and energy-crop and sawdust mix. By grade, the market is segmented into utility-grade, premium-grade, standard-grade, and torrefied “black” pellets. By application, the market is segmented into heating, power generation, and combined heat and power (CHP). The report also covers the market size and forecasts across major countries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Feedstock

| Forest/Wood Residue |

| Agricultural Residue |

| Energy-Crop and Sawdust Mix |

By Grade

| Utility-Grade (White) |

| Premium-Grade |

| Standard-Grade |

| Torrefied “Black” Pellets |

By Application

| Heating |

| Power Generation |

| Combined Heat and Power (CHP) |

By End-user

| Residential |

| Commercial |

| Industrial and Utility |

| Animal Bedding |

By Geography

| United States |

| Canada |

| Mexico |

| By Feedstock | Forest/Wood Residue |

| Agricultural Residue | |

| Energy-Crop and Sawdust Mix | |

| By Grade | Utility-Grade (White) |

| Premium-Grade | |

| Standard-Grade | |

| Torrefied “Black” Pellets | |

| By Application | Heating |

| Power Generation | |

| Combined Heat and Power (CHP) | |

| By End-user | Residential |

| Commercial | |

| Industrial and Utility | |

| Animal Bedding | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America wood pellet market in value terms for 2026?

The North America wood pellet market size was USD 0.91 billion in 2026.

What CAGR is forecast for North American wood pellet demand through 2031?

Aggregate demand is projected to rise at a 3.65% CAGR between 2026 and 2031.

Which feedstock type is expected to expand fastest by 2031?

Agricultural residue pellets are forecast to grow at a 4.8% CAGR as mills diversify away from sawmill by-products.

Why are torrefied pellets attracting utility buyers?

Torrefied pellets offer higher energy density, better moisture resistance, and compatibility with existing coal-fired boilers, reducing freight and retrofit costs.

How do Canadian carbon policies influence pellet adoption?

Clean Fuel Regulations and provincial carbon pricing create tradeable credits, widening pellets cost advantage and driving a 4.2% CAGR for Canadian demand.

What challenges threaten residential pellet-heating growth?

Accelerating heat-pump adoption, generous tax incentives, and shifting utility tariffs are eroding the economic appeal of pellet stoves for households in cold-climate regions.

Page last updated on: