Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 12.48 Billion |

| Market Size (2026) | USD 13.29 Billion |

| Market Size (2031) | USD 18.03 Billion |

| Growth Rate (2026 - 2031) | 6.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Wood Pellet Market Analysis by Mordor Intelligence

The Europe Wood Pellet Market size is projected to be USD 12.48 billion in 2025, USD 13.29 billion in 2026, and reach USD 18.03 billion by 2031, growing at a CAGR of 6.29% from 2026 to 2031.

The market is powered by coal-to-biomass conversions in utilities, fresh incentives for negative-emission BECCS, and resilient residential heating demand amid volatile fossil-fuel prices. Vertically integrated suppliers are rushing to secure long-term offtake agreements as supply-chain localization efforts reduce exposure to Russian feedstock, while torrefied pellets gain momentum because they match coal’s energy density. Pricing pressure persists, however, as sawmill closures tighten residue availability and EU sustainability rules lift compliance costs.[1]Bioenergy Europe, “Statistical Report 2025: Biomass Supply, Transformation & Consumption,” bioenergyeurope.orgCompetitive dynamics favor players that control feedstock, logistics, and carbon-credit monetization across the entire value chain.

Key Report Takeaways

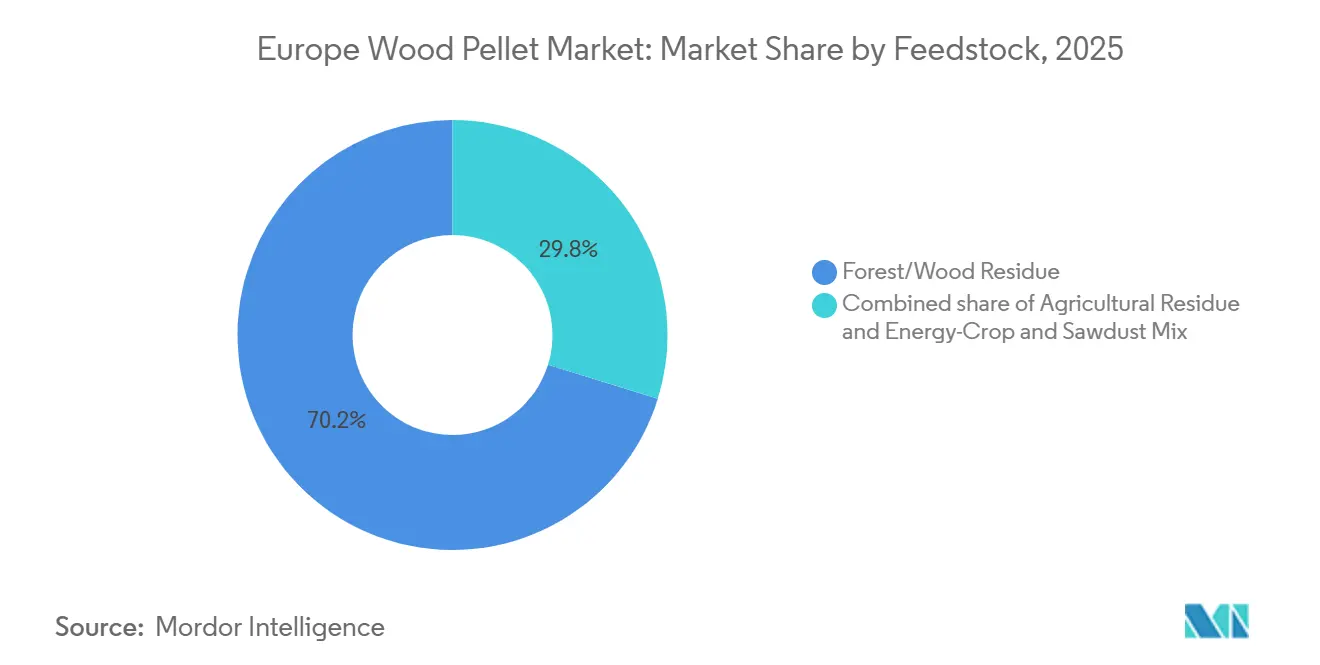

- By feedstock, forest and wood residues captured 70.2% of Europe's wood pellet market share in 2025, while agricultural residues are expanding at a 7.8% CAGR through 2031.

- By grade, utility-grade pellets accounted for 55.8% of the European wood pellet market size in 2025; torrefied pellets are accelerating at a 9.4% CAGR to 2031.

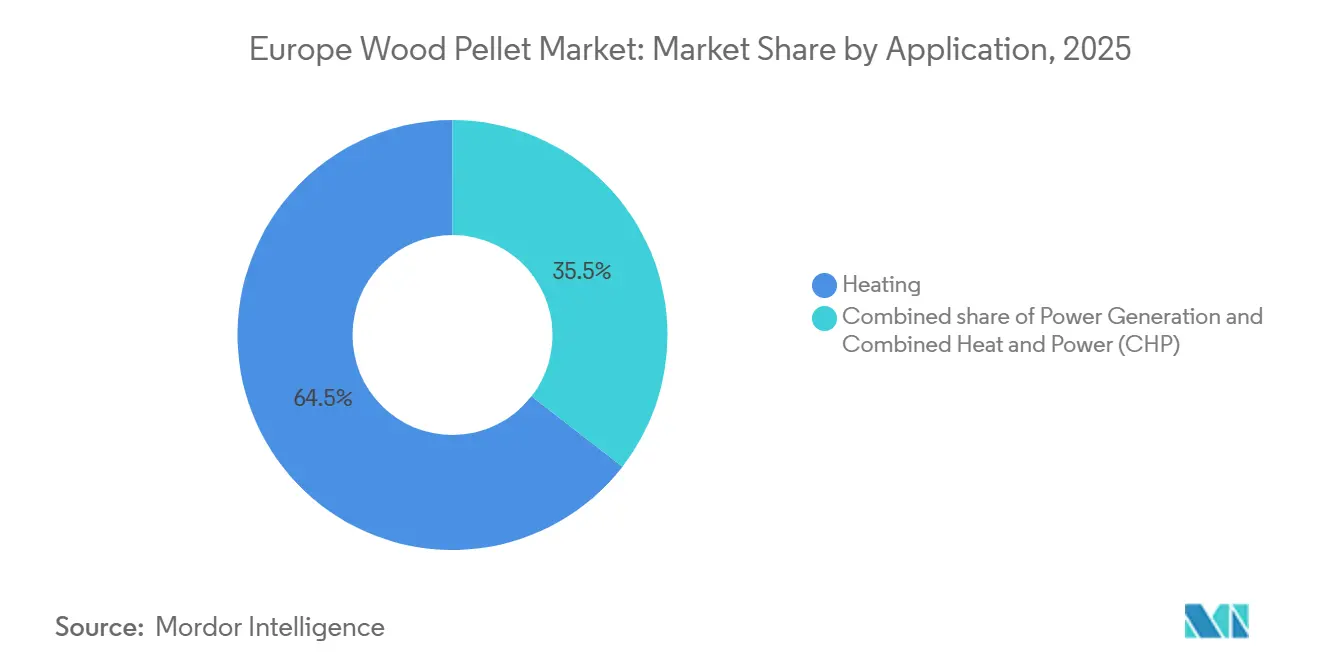

- By application, heating commanded a 64.5% share of the European wood pellet market size in 2025, whereas combined heat and power installations are advancing at an 8.9% CAGR through 2031.

- By end-user, industrial and utility users held 53.9% of the European wood pellet market share in 2025 and are set to grow at an 8.5% CAGR between 2026 and 2031.

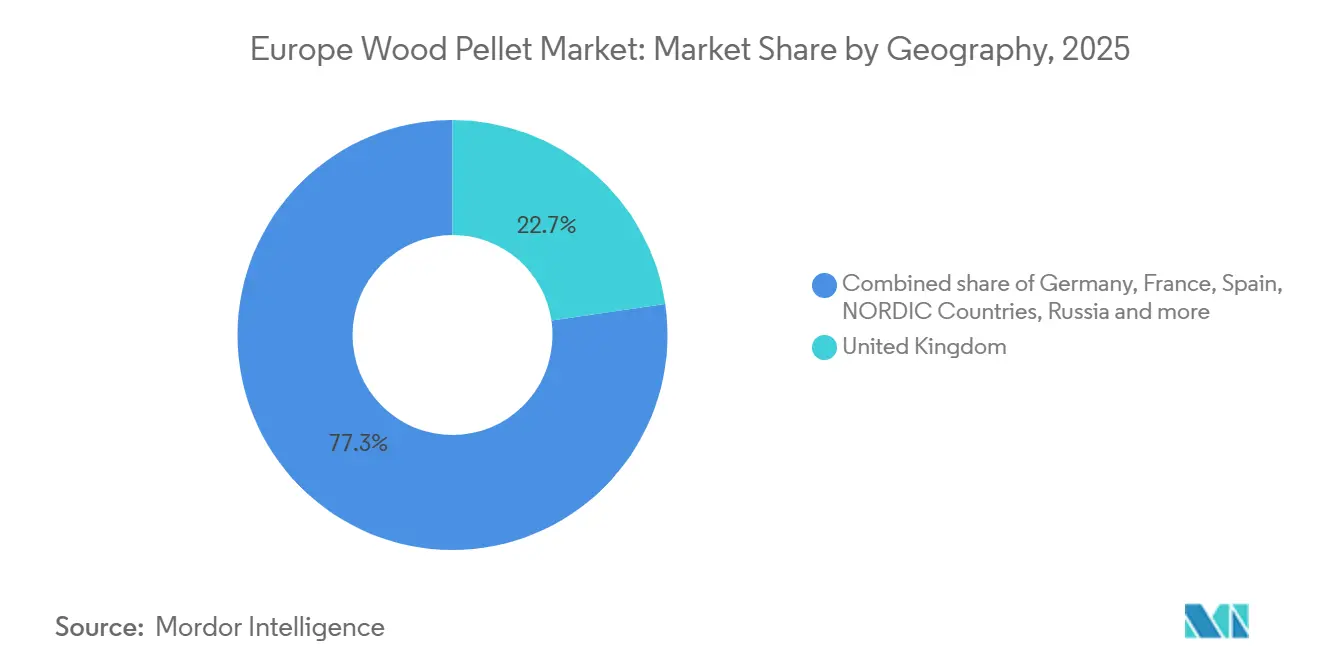

- By geography, the United Kingdom led with 22.7% revenue share in 2025; Nordic Countries posted the fastest growth at 9.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Wood Pellet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust residential heating demand amid record fossil-fuel prices | 1.20% | Germany, France, Austria, Nordic Countries | Short term (≤ 2 years) |

| Accelerated coal-to-biomass conversion of EU power plants | 1.50% | United Kingdom, Germany, Spain | Medium term (2-4 years) |

| New EU-ETS incentives for negative-emission BECCS projects | 0.90% | United Kingdom, Nordic Countries | Long term (≥ 4 years) |

| Surge in heat-pump / pellet-hybrid boiler retrofits | 0.80% | Germany, Netherlands, Rest of Europe | Medium term (2-4 years) |

| Fast-track permitting for post-Russia supply-chain localization | 0.70% | EU27 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust Residential Heating Demand Amid Record Fossil-Fuel Prices

Gas prices in Europe stayed elevated through 2024, making wood pellets a cost-competitive option for space heating in single-family homes and small businesses. Austria maintained solid boiler installations thanks to unchanged incentives, while Germany and France still absorbed considerable volumes despite subsidy revisions. ENplus certification encouraged cross-border pellet trade by guaranteeing burn quality. The share of residential demand reached 7% of total European consumption in 2024.[2]USDA Foreign Agricultural Service, “United Kingdom Biofuels Annual Report 2024,” usda.gov Although Germany’s August 2024 BEG reform curtailed standalone biomass subsidies, residential suppliers are smoothing earnings by expanding into appliance financing and doorstep retail programs. Vertical integration is therefore becoming essential to offset the inherent volatility of spot-based sales.

Accelerated Coal-to-Biomass Conversion of EU Power Plants

Drax Group’s restart of Unit 4 in 2024 injected about 3 million t of extra pellet demand and revived UK biomass electricity output. New projects, such as ArcelorMittal’s Torero facility in Belgium, illustrate biomass applications in hard-to-abate industries by delivering bio-coal to steel blast furnaces. Spain’s La Robla plant, backed by the European Investment Bank, shifted to domestic agricultural residues, cutting logistics emissions and broadening feedstock flexibility.[3]European Investment Bank, “La Robla Biomass Plant Financing,” eib.org Retrofit economics remain favorable because existing grid connections and turbines are reused, but post-2027 policy uncertainty in the UK may halve offtake, underscoring the need for diversified demand portfolios. EU cascading-use principles, which prioritize residues over roundwood, likewise cap future supply scalability.

New EU-ETS Incentives for Negative-Emission BECCS Projects

Revisions adopted in 2024 allow utilities to monetize negative emissions when biomass combustion is paired with carbon capture and storage. Drax plans full-scale BECCS integration by 2027, targeting the sale of high-value EU Allowances alongside renewable electricity. EU carbon prices fluctuated between EUR 60-90 t in 2024, meaning that negative-emission credits could surpass power revenues. However, projected capture retrofits cost roughly GBP 2 billion per plant, testing the adequacy of support frameworks. Profitability, therefore, hinges on predictable carbon prices and timely disbursement of BECCS incentives, which together will determine whether utilities expand pellet contracts or pivot toward other negative-emission technologies.

Surge in Heat-Pump / Pellet-Hybrid Boiler Retrofits

Hybrid systems that combine air-source heat pumps with pellet burners grew rapidly in Germany and the Netherlands in 2024, enabling households to toggle between fuels as prices fluctuate. Germany’s BEG reform now restricts new biomass incentives to hybrid installations, quickening adoption in rural areas where gas grids are absent. These hybrids trim pellet usage by up to 40% yet raise equipment sales for firms like Viessmann and Ökofen, which launched smart-control models in 2025. Producers must revise demand forecasts because hybrid flexibility dampens winter consumption spikes but stabilizes year-round take-off, reshaping residential segment dynamics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Termination of national pellet boiler subsidies in core markets | -1.10% | Germany, Netherlands, France | Short term (≤ 2 years) |

| Rising competition from heat-pump-only solutions | -0.80% | Germany, France, Netherlands, Rest of Europe | Medium term (2-4 years) |

| Feed-wood fiber scarcity & price spikes post-Ukraine war | -0.80% | EU27 | Short term (≤ 2 years) |

| EUDR sustainability compliance costs | -0.70% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Termination of National Pellet Boiler Subsidies and Heat-Pump Competition

Germany scrapped standalone biomass incentives in August 2024, causing a 55% plunge in boiler sales from 2023 to 2024. France recorded an even steeper 73% drop as incentives shifted toward electric heat pumps. The Netherlands stopped subsidizing biomass heat in new homes, funneling funds exclusively to electrification. Accelerated manufacturing scale in China lowered heat-pump equipment prices by 15-20%, eroding pellets’ cost advantage. Urban air-quality rules also tightened particulate limits, limiting pellet uptake in dense areas. Together, subsidy withdrawal and cheaper electric alternatives weaken residential demand, forcing producers to rely more heavily on industrial buyers that negotiate longer-term contracts at thinner margins.

Feed-Wood Fiber Scarcity, Price Spikes, and EUDR Compliance Costs

European pellet output slipped 7% in 2024 to 22.7 million t because construction slowdowns shuttered sawmills, slashing residue flows. Bark-beetle infestations further degraded timber quality and redirected salvage wood into energy, heightening feedstock competition with panel-board makers. Industrial pellet spot prices rebounded in late 2024 as Drax's ramp-up absorbed surplus volumes. Starting December 30, 2025, for large operators, the EU Deforestation Regulation obliges traceability, satellite monitoring, and TRACES uploads for every shipment, adding EUR 2-5 t to production costs and squeezing small producers.[4]European Commission, “EU Deforestation Regulation Implementation,” europa.eu Compliance timelines, combined with tight residue supply, compress margins and encourage consolidation among non-integrated players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Forest Residues Anchor Supply, Agricultural Streams Gain Momentum

Forest and wood residues generated 70.2% of the European wood pellet market size in 2025, reflecting robust sawmill networks and mature ENplus logistics. Agricultural residues, however, are rising at a 7.8% CAGR, aided by mobile pelletizing platforms that shrink transport energy by 38%. Spain’s La Robla plant validated local straw sourcing to cut supply-chain emissions. Even though agricultural streams carry higher ash (2-5%) and lower energy density, the EU Deforestation Regulation treats them preferentially, spurring trial blends at CHP units. Producers are adopting advanced sieving and additive dosing to manage quality variability, signaling a longer-term pivot toward multi-feedstock procurement strategies.

Over 2026-2031, forest residues will still underpin the European wood pellet market, but agricultural inputs provide the incremental growth needed to meet utility demand while easing pressure on over-harvested forests. Blending also hedges against residue shortages when housing cycles slow sawmill output. Stakeholders that can certify diverse feedstock pools stand to capture new contracts as utilities seek compliance-ready pellets.

By Grade: Utility Pellets Dominate, Torrefied Variants Disrupt Coal Replacement

Utility-grade white pellets accounted for 55.8% of the European wood pellet market share in 2025, supplying large-scale power projects that value low delivered cost over premium specs. The European wood pellet market size for torrefied variants is expanding at a 9.4% CAGR, catalyzed by ANDRITZ’s 60,000 t Joensuu Biocoal plant in Finland. Torrefaction raises energy density to 22-28 GJ t, enabling coal-plant co-firing without major retrofit. Early adopters include ArcelorMittal, which feeds torrefied pellets into steel furnaces, demonstrating cross-sector potential. Capital intensity remains EUR 100-150 t cap, so deployment concentrates near residue-rich clusters where CHP waste heat can supply the drying step. As more European coal units face retirement, utilities weigh torrefaction as a transitional decarbonization pathway.

Industry consensus sees torrefied pellets reaching double-digit share by 2031, particularly in Northern and Central Europe, where coal assets represent dispatchable capacity. Standard and premium grades will maintain relevance in residential boilers, but growth moderates as hybrids and heat pumps take hold. Manufacturers that diversify across grade portfolios will mitigate demand swings while capturing high-margin torrefied contracts.

By Application: Heating Leads, CHP Captures Industrial Efficiency Gains

Heating applications commanded 64.5% of Europe's wood pellet market size in 2025, spanning residential stoves, commercial buildings, and district-heating networks. Combined heat and power systems, however, are growing at 8.9% CAGR as industrial sites monetize both steam and electricity under national feed-in frameworks. THEURL's Austrian complex, commissioned in autumn 2025, marries an 80,000 t pellet line with on-site generation at 85% efficiency. CHP adoption is also buoyed by the EU's Carbon Border Adjustment Mechanism, which rewards low-carbon process heat in export-oriented metallurgy and chemicals.

Power-only generation stagnated in 2024 amid subsidy uncertainty, though Drax's restart provided a temporary lift. Looking forward, BECCS retrofits could rekindle growth, but their timeline hinges on carbon-credit liquidity. Animal-bedding demand remains a niche outlet, absorbing lower-grade output during energy market lulls. Diversified producers that can switch between heating and CHP grades will weather policy shifts more effectively.

By End-User: Residential Base Erodes, Industrial Demand Scales

Residential consumers absorbed 53.9% of Europe's wood pellet market share in 2025, and while Industrial & Utility segment is forecast to grow at an 8.5% CAGR as coal-to-biomass conversions and BECCS projects proliferate. Residential users, once the growth engine, face subsidy roll-backs and heat-pump competition, causing boiler sales to plunge 55% in Germany and 73% in France during 2024. Commercial institutions such as schools and hotels maintain moderate demand where district-heating links are absent.

The European wood pellet market will increasingly revolve around industrial offtake contracts that bundle fuel supply with carbon-credit sharing. Producers must recalibrate product mix, emphasizing high-volume utility pellets and torrefied grades while maintaining a smaller, premium certified line for niche retail channels. Residential decline nonetheless frees up capacity that can be redirected to export or industrial hybrids, cushioning revenue volatility.

Geography Analysis

The United Kingdom ruled the European wood pellet market with a 22.7% share in 2025 and is advancing at an 8.6% CAGR, primarily because Drax alone imported 9.641 million t in 2024, equal to roughly one-third of total continental demand. U.K. transitional support for BECCS extends into 2031, offering revenue security, yet post-2027 subsidy reductions could cut Drax demand by 50%, exposing import volumes to downside risk.

Germany remains Europe’s second-largest producer at near 3 million t in 2024 but saw residential sales shrink after subsidy cuts. Industrial CHP retrofits partially offset the decline as factories chase decarbonization targets. France charts a similar course, with residential weakness but rising industrial steam projects.

Nordic Countries combine production strength with aggressive CHP deployment. Sweden burned 1.9 million t in district networks during 2023, while Finland hosts the Joensuu torrefaction plant, cementing regional leadership in advanced biomass processing. Spain, though smaller, illustrates feedstock diversification by pivoting to straw at the La Robla plant. Eastern Europe and Austria offer pockets of residential resilience, with Austria sustaining boiler installations thanks to stable incentives.

EU Deforestation Regulation compliance will reshape trade lanes post-2025, favoring shipments with granular geolocation data. Supply-side tightness may foster intra-European sourcing, but capacity expansion hinges on residue availability and permitting. Overall, geographic demand is drifting from Central-European households toward U.K. BECCS and Nordic-centered industrial CHP, reshaping logistics and contracting patterns.

Competitive Landscape

The European wood pellet market remains moderately fragmented, yet vertical integration is rising. Enviva, the top U.S. exporter, filed Chapter 11 in March 2024 and then emerged five months later with USD 1.3 billion in fresh financing, highlighting the capital strain of trans-Atlantic supply chains. The firm sold its Sampson plant for USD 94 million and restarted Hamlet to concentrate on high-margin assets.

ANDRITZ demonstrated technology leadership by bringing Finland’s Joensuu torrefaction unit online in May 2025, giving utilities a coal-compatible fuel without retrofitting boilers. Drax leverages long-term contracts and in-house port infrastructure to secure supply for its four biomass units. Graanul Invest and Scandbio dominate the Baltic and Nordic markets, respectively, each integrating forestry, production, and logistics.

White-space growth centers on torrefaction build-outs and hybrid boiler ecosystems that merge pellets with heat pumps, using smart controls to switch fuels automatically. Mobile pelletizers backed by EU-funded pilots lower feedstock transport costs, enabling on-farm agricultural pellet production. Increased certification costs under the EU Deforestation Regulation may drive smaller standalone mills to consolidate or exit, lifting market concentration over the next five years.

Europe Wood Pellet Industry Leaders

AS Graanul Invest

Drax Group plc

Enviva Inc.

Stora Enso Oyj

Scandbio AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Nextwood Two, an Austrian holding company, has filed a merger report to acquire KUREKSS. KUREKSS, a lumber producer and exporter, operates a sawmill in the Ventspils region and owns SIA Kurzemes granulas, a company that produces and sells wood pellets.

- February 2025: Drax Group plc unveiled its full-year 2024 financial results, highlighting a robust uptick in both operational and financial metrics for its North American wood pellet division. Additionally, the company saw a notable surge in biomass power generation. In 2024, Drax's wood pellet production reached 4 million metric tons, marking a 5% increase from the 3.8 million metric tons produced in 2023.

- August 2024: Koehler Group, a Germany-based paper and energy firm, has revealed that its subsidiary, Zollikofer Group, has taken over French fuelwood and biomass supplier SAS REKO Energie Bois (REKO). The financial details of the acquisition remain undisclosed.

- February 2024: Graanul Invest announced the launch of the premium pellet brand, g Graanul, which is expected to provide Baltic customers with an affordable, high-quality renewable energy solution. This launch is an initiative taken by the company to broaden its network and presence in the Baltic region.

Europe Wood Pellet Market Report Scope

Wood pellets are renewable fuels manufactured from compressed sawdust or wood chips. They can be used to heat houses and businesses as a biomass fuel. Wood pellets can be made from forest residues and low-quality logs that can be handled as rubbish.

The European wood pellet market is segmented by feedstock, grade, application, and geography. By feedstock, the market is divided into forest residue, agriculture residue, energy crop, and sawdust mix. By grade, the market is segmented into utility-grade, premium-grade, standard-grade, and others. By application, the market is segmented into heating and power generation. The report also covers the market size and forecasts across major countries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Feedstock

| Forest/Wood Residue |

| Agricultural Residue |

| Energy-Crop and Sawdust Mix |

By Grade

| Utility-Grade (White) |

| Premium-Grade |

| Standard-Grade |

| Torrefied “Black” Pellets |

By Application

| Heating |

| Power Generation |

| Combined Heat and Power (CHP) |

By End-user

| Residential |

| Commercial |

| Industrial and Utility |

| Animal Bedding |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| NORDIC Countries |

| Russia |

| Rest of Europe |

| By Feedstock | Forest/Wood Residue |

| Agricultural Residue | |

| Energy-Crop and Sawdust Mix | |

| By Grade | Utility-Grade (White) |

| Premium-Grade | |

| Standard-Grade | |

| Torrefied “Black” Pellets | |

| By Application | Heating |

| Power Generation | |

| Combined Heat and Power (CHP) | |

| By End-user | Residential |

| Commercial | |

| Industrial and Utility | |

| Animal Bedding | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe wood pellets market in 2026?

The sector is projected to surpass USD 13.29 billion in 2026.

What is driving industrial demand for pellets?

Utilities are converting coal units to biomass and planning BECCS retrofits to earn high-value negative-emission credits, pushing industrial contracts higher.

Why are torrefied pellets gaining popularity?

Torrefaction lifts energy density to coal-like levels, allowing co-firing without costly boiler modifications and improving outdoor storage stability.

How will the EU Deforestation Regulation affect suppliers?

From late 2025, producers must upload geolocation data and due-diligence files in TRACES, adding EUR 2-5 t to costs and favoring larger, certified operators.

Which countries are the biggest pellet importers?

The United Kingdom tops the list, relying on imports for more than 90% of its demand, followed by Denmark and the Netherlands for CHP applications.

What is the outlook for residential pellet heating?

Sales are weakening in Germany and France after subsidy cuts, but hybrid heat-pump systems keep a niche role in rural areas without gas grid access.

Page last updated on: