Microcarrier Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.27 Billion |

| Market Size (2031) | USD 3.01 Billion |

| Growth Rate (2026 - 2031) | 5.79% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

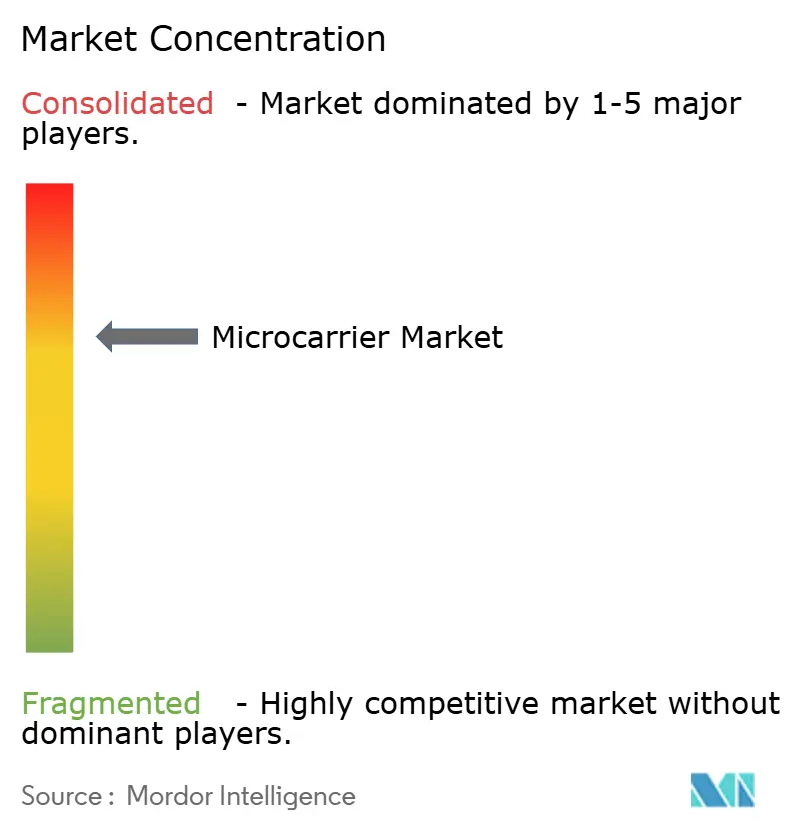

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Microcarrier Market Analysis by Mordor Intelligence

Microcarrier market size in 2026 is estimated at USD 2.27 billion, growing from 2025 value of USD 2.15 billion with 2031 projections showing USD 3.01 billion, growing at 5.79% CAGR over 2026-2031. Demand is propelled by cell-based vaccines, the wider biologics pipeline, and the shift toward continuous manufacturing platforms that enable higher cell densities, smaller facility footprints, and lower utility consumption. Growing investment in cultivated-meat R&D is accelerating interest in edible, biodegradable substrates, while single-use bioreactors and integrated process-analytical technologies are improving batch-to-batch consistency and shortening changeover times [1]Ping Xia, "Development of Biomimetic Edible Scaffolds for Cultured Meat Based on the Traditional Freeze-Drying Method for Ito-Kanten (Japanese Freeze-Dried Agar)," MDPI, mdpi.com. Automation, magnetic separation, and thermo-responsive materials are reducing labor requirements by up to 40%, supporting cost-containment strategies in commercial operations. Collectively, these factors keep the microcarrier market on a steady growth trajectory despite headwinds linked to biologics price pressure and scale-up complexities.

Key Report Takeaways

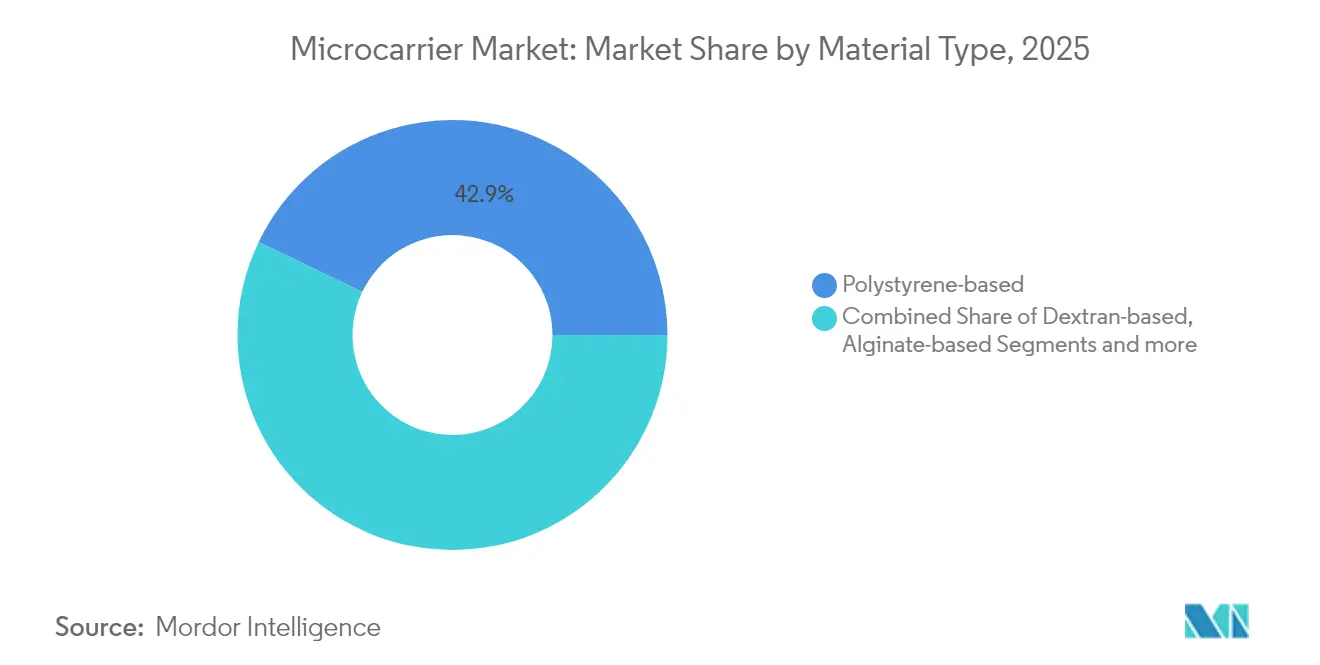

- By material type, polystyrene carriers led with 42.88% of the microcarrier market share in 2025, whereas alginate carriers are expanding at a 6.55% CAGR through 2031.

- By application, vaccine manufacturing accounted for 38.55% of the microcarrier market size in 2025; cell therapy is forecast to grow at a 6.38% CAGR to 2031.

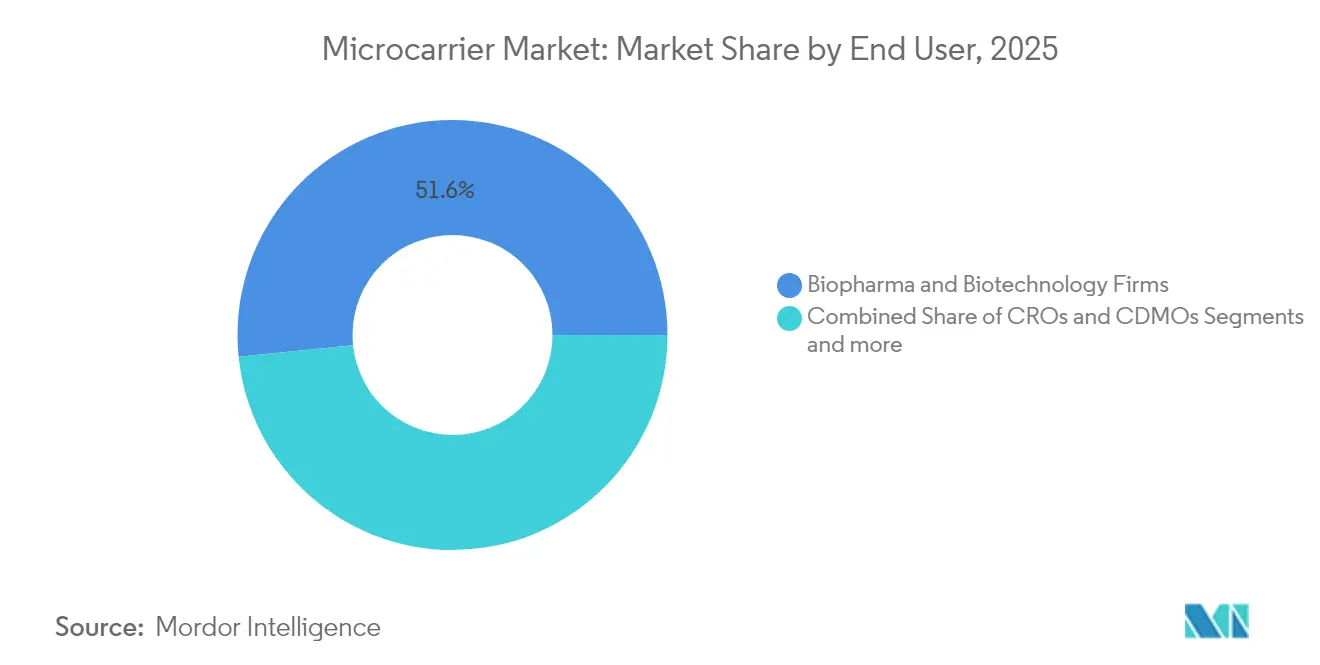

- By end user, biopharma and biotechnology firms held 51.62% of the microcarrier market size in 2025, while CROs and CDMOs are advancing at a 6.48% CAGR.

- By scale of operation, commercial-scale facilities commanded 57.05% of the microcarrier market size in 2025, and pilot-scale projects are increasing at a 6.53% CAGR.

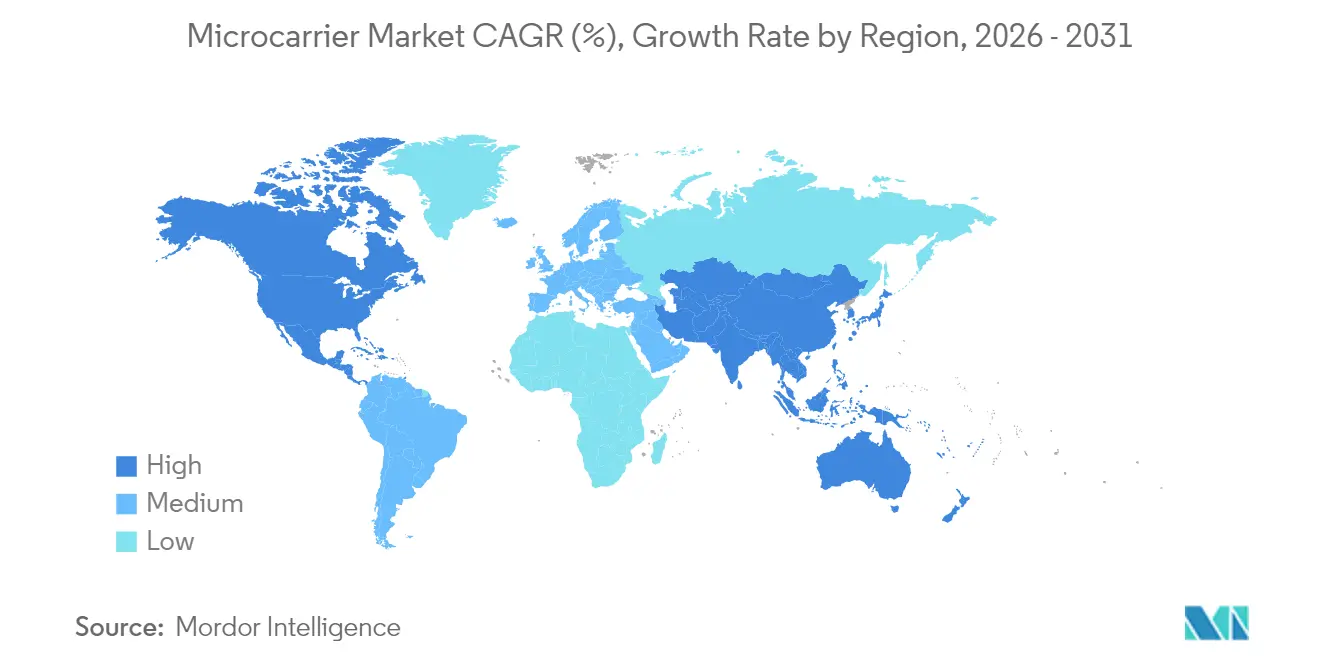

- By geography, North America contributed 42.31% of the microcarrier market share in 2025; Asia-Pacific is set to climb at a 6.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microcarrier Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for cell-based vaccines & therapeutics | +1.2% | North America, Europe; rising in Asia-Pacific | Medium term (2–4 years) |

| Expansion of biologics & biosimilar capacity | +1.8% | Global; strongest progress in emerging Asia-Pacific markets | Long term (≥ 4 years) |

| Surge in funding for cell & gene therapy R&D | +0.9% | North America, Europe; spreading to Asia-Pacific | Short term (≤ 2 years) |

| Adoption of single-use bioprocess platforms | +0.8% | Leading biomanufacturing hubs worldwide | Medium term (2–4 years) |

| Growth of cultivated-meat production | +0.6% | Early adoption in North America & Europe; scaling in Asia-Pac | Long term (≥ 4 years) |

| Magnetic & thermo-responsive carriers | +0.5% | Advanced manufacturing regions worldwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Demand for Cell-Based Vaccines & Therapeutics

Accelerated mRNA and viral-vector programs need adherent cell culture systems capable of exceeding 20 million cells/mL, well above the 5–8 million cells/mL typical of suspension cultures. Regulatory streamlining now shortens development timelines to 7–10 years for select modalities, stimulating sustained orders for scalable microcarrier platforms. Pandemic-era investment in domestic vaccine capacity cemented the role of optimized microcarriers that shrink reactor footprints by as much as 70%, easing capital constraints for smaller firms. Personalized-medicine pipelines demand flexible, small-batch bioreactors, further reinforcing microcarrier adoption. Collectively, these factors add 1.2 percentage points to the forecast CAGR of the microcarrier market.

Expansion of Biologics & Biosimilar Manufacturing

Biologics revenue surpassed USD 300 billion in 2025, while governments in China and India injected over USD 15 billion into green-field biopharma capacity over the past two years. Continuous perfusion systems achieve 10-fold volumetric productivity and 50% media savings, but their high cell-density operation depends on rugged microcarriers that tolerate sustained shear. Biosimilar developers seek carrier chemistries that faithfully replicate originator culture conditions, raising the bar for surface-modification precision. The BIOSECURE Act is redirecting Western outsourcing toward India’s CDMOs, where inquiry volumes jumped more than 40% in 2024, expanding the global footprint of the microcarrier market.

Surge in Global Funding for Cell & Gene Therapy R&D

Venture investment in cell and gene therapy exceeded USD 12 billion in 2024, and GMP-safer, animal-component-free carriers became a procurement priority. Automated harvest modules linked to thermo-responsive or magnetic microcarriers cut operator time by 30–40%, alleviating skilled-labor bottlenecks [2]Cellular Origins, "Cellular Origins and Fresenius Kabi sign development agreement for scalable automation of CGT manufacturing," cellularorigins.com. Allogeneic platforms call for large-scale expansions, compelling developers to validate carriers that preserve phenotype across multiple passages. Emerging facilities in Asia-Pacific and Latin America now insist on globally proven carriers to satisfy cross-border regulatory submissions, broadening geographic demand for the microcarrier market.

Shift Toward Single-Use Bioprocessing Platforms

Disposable bioreactors make up more than 60% of new biologics installations, and carriers must remain stable under gamma irradiation and long-term refrigerated storage. Real-time PAT integration guides nutrient-feed profiles, pushing productivity 15–25% higher than traditional batch modes. Elimination of cleaning validation frees 20–30% of capacity, an advantage that resonates with virtual biotech firms and multi-client CDMOs. Regulators increasingly recognize the contamination-control and traceability strengths of single-use ecosystems, removing adoption barriers and amplifying the growth of the microcarrier market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of biologics & cell-based therapies | -0.7% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Shear-stress & aggregation issues in carrier cultures | -0.5% | Global, particularly in large-scale manufacturing | Medium term (2-4 years) |

| Lack of regulatory-cleared biodegradable microcarriers | -0.3% | Global, with stricter requirements in North America & Europe | Medium term (2-4 years) |

| Supply-chain volatility for specialty polymers & coatings | -0.2% | Global, concentrated in polymer manufacturing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Biologics & Cell-Based Therapies

Manufacturing accounts for 40–60% of end-user prices in cell therapies, far above the 10–15% typical for small-molecule drugs. Emerging-market payers therefore restrict reimbursement, curbing facility builds and muting demand for new microcarrier installations. While scale-up promises economies of scale, it also introduces validation costs that smaller firms struggle to absorb, delaying commercialization timelines. Extensive carrier characterization can add USD 2–5 million to regulatory filings, deterring novel-material entrants and tempering growth in the microcarrier market.

Shear-Stress & Aggregation Issues in Carrier Cultures

In reactors above 1,000 L, turbulent eddies can exceed 1 Pa of shear, damaging fragile cell lines and reducing yield variability targets of under 5% batch-to-batch. Aggregates larger than 500 µm hamper oxygen delivery, forcing operators to implement costly low-shear impellers or wave-bag alternatives. New polymer coatings and micro-carrier shapes offer partial relief, yet may sacrifice attachment efficiency or harvest ease. The resulting trade-offs necessitate extensive process-development cycles, extending time-to-market and shaving 0.5 percentage points off the microcarrier market CAGR forecast.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Alginate Carriers Drive Sustainability Shift

Polystyrene carriers retained a 42.88% share of the microcarrier market size in 2025 as the long-standing workhorse for viral vaccine and monoclonal-antibody lines. Their surface chemistry is well understood, lot-to-lot consistency is high, and regulatory files are mature, lowering qualification hurdles. However, the growing environmental focus of biopharma and the ascent of cultivated-meat producers are redirecting R&D budgets toward biodegradable alginate, chitosan, and cellulose variants. The alginate cohort is charting a 6.55% CAGR, the fastest across material classes, benefiting from its edible profile and ability to gel under Ca²⁺ gradients, a prized attribute for muscle-fiber scaffolding in cultured meat.

Hybridformulations now merge rigid synthetic cores with bio-active outer layers, delivering mechanical resilience during high-shear perfusion runs while presenting natural ligands for delicate stem cells. Magnetic polystyrene cores coated in collagen fragments enable auto-separation and gentle detachment, trimming harvest times by 30–40% in commercial plants . Thermo-responsive poly-N-isopropyl-acrylamide shells release cells upon a 5 °C temperature drop without enzymatic insult, preserving membrane-bound proteins vital to cell-therapy potency. The regulatory push toward chemically defined, animal-component-free processes further stimulates demand for synthetic-plant hybrids, upholding growth momentum in the microcarrier market.

By Application: Cell Therapy Manufacturing Accelerates

Vaccine production absorbed 38.55% of the microcarrier market size in 2025 as influenza, polio, and more recently mRNA-based platforms rely on adherent lines for antigen or virus propagation. Decades of process optimization keep barrier-to-entry high for challengers, ensuring stable demand. Yet cell-therapy pipelines—spanning CAR-T, mesenchymal stromal cells, induced pluripotent stem cells, and NK cells—are driving a 6.38% CAGR, outpacing every other use case. Regulatory approvals for allogeneic “off-the-shelf” immunotherapies demand reactors that can bank billions of cells per lot with lot-release timelines under two weeks, a benchmark achievable only with intensified microcarrier cultures.

Automation suites integrating sensor-rich harvest skids now support inline washing, concentration, and fill-finish activities, slashing vein-to-vein time for CAR-T candidates from 20 days to under 12 days. Downstream, edibility is becoming a critical design parameter for cultured-meat carriers that must degrade or remain consumable without altering texture or taste. R&D segments, including tissue engineering and organ-on-chip, continue to adopt microcarriers for scalable proof-of-concept studies, gradually widening the microcarrier market application base.

By End User: CDMOs Capture Outsourcing Wave

Biopharma and biotech firms owned 51.62% of the microcarrier market size in 2025, reflecting their direct control of intellectual property and need for bespoke process solutions. However, CROs and CDMOs are experiencing the sharpest rise at a 6.48% CAGR as big pharma de-risks capital exposure by outsourcing late-stage and commercial manufacturing. Multitenant facilities in the United States, Europe, India, and Singapore now stock multiple microcarrier types on consignment, offering turnkey cell-culture suites that compress tech-transfer timelines from 12 months to under 6 months.

Strategic tie-ups with equipment majors let CDMOs pair proprietary magnetic or thermo-responsive carriers with software-driven perfusion skids, packaging an end-to-end intensified solution. Academic–industry alliances further blur traditional user boundaries, as university translational centers adopt GMP-compliant microcarriers to attract philanthropic grants and venture spinouts. Government labs — particularly those pursuing pandemic-preparedness programs — add a modest but stable revenue stream, emphasizing the resilience of the microcarrier market across user categories.

By Scale of Operation: Pilot Scale Drives Innovation

Commercial sites accounted for 57.05% of the microcarrier market size in 2025 thanks to established monoclonal-antibody and vaccine franchises operating 2,000 L and 5,000 L stirred-tank bioreactors. Nonetheless, pilot-scale activity (50 L–500 L) is registering a 6.53% CAGR as cell-and-gene-therapy sponsors refine workflows before committing to mega-plants. Intensified perfusion runs at pilot scale now match historical commercial titers, shifting decision-making toward smaller, parallel trains rather than single large tanks, a paradigm well suited to flexible single-use facilities.

Process-development teams employ design-of-experiments software coupled with PAT-enabled reactors to screen carrier types, agitation profiles, and feeding regimens within weeks, accelerating the transition from IND to pivotal trials. Laboratory-scale systems (<10 L) continue to underpin proof-of-concept, with modular benchtop rigs mirroring the fluid dynamics of commercial trains to derisk scale-up. This multiscale integration cements the importance of microcarriers, ensuring the microcarrier market remains central to next-generation bioprocess maps.

Geography Analysis

North America captured 42.31% of 2025 revenue, supported by mature GMP infrastructure, robust venture funding, and proximity to regulators that often set global validation benchmarks. Skilled-labor shortages and premium operating costs are nudging firms toward dual-shore models, yet the region retains leadership in high-value cell-and-gene therapies and maintains one of the densest clusters of microcarrier innovation pipelines.

Asia-Pacific is the fastest-growing territory at a 6.68% CAGR, underpinned by government subsidies, lower labor overhead, and expanding biosimilar exports. China allocated more than USD 8 billion to biopharma industrial parks in 2024, featuring purpose-built single-use suites that standardize microcarrier processes from seed train to harvest. India’s CDMO complex saw inbound project inquiries soar by over 40% following U.S. supply-chain legislation, prompting capacity expansions in Hyderabad and Bangalore. Japan and South Korea focus on regenerative medicine and cell-therapy commercialization, demanding advanced carriers with traceable supply chains to satisfy strict pharmacopoeial standards.

Europe shows steady, environmentally focused growth, with circular-economy directives incentivizing biodegradable carriers and closed-loop water systems. Industrial policy supports continuous manufacturing pilot plants in Germany, the Netherlands, and Ireland, ensuring that the microcarrier market maintains momentum amid rising energy costs. Emerging regions in the Middle East, Africa, and South America are building foundational capability, often through technology-transfer agreements and modular GMP suites, gradually enlarging the microcarrier market footprint.

Regulatory Landscape

Microcarriers used in cell and gene therapy (CGT) bioprocessing are commonly handled as ancillary materials, bringing them under expectations aligned to ISO 20399:2022. In the United States, FDA CBER guidance and the broader set of FDA cellular and gene therapy guidances shape sponsor expectations around raw-material characterization, traceability, and change control, which raises documentation requirements for microcarrier suppliers, particularly for animal-origin-free and chemically defined surfaces.

In May 2026, FDA finalized guidance on Chemistry, Manufacturing, and Controls (CMC) flexibilities for developing human CGT products for a BLA. This framework supports performance-based qualification packages for materials used in intensified and patient-specific manufacturing, while keeping extractables and leachables and other material risks in focus as they can affect critical quality attributes. Characterization approaches aligned with FDA-recognized consensus standards (for example, ASTM F2027-16 for raw materials in tissue-engineered medical products) remain relevant inputs to compliance strategies.

Competitive Landscape

The top 10 suppliers account for an estimated 50% of global revenue, reflecting moderate consolidation. Incumbents leverage decades of surface-chemistry data, validated quality systems, and global distribution, positioning their microcarrier portfolios as low-risk choices for regulators and big pharma alike. Patent activity centers on magnetic composite cores, thermo-responsive hydrogel shells, and manufacturing processes that integrate in-line analytics and machine learning for lot-release prediction.

Strategic alliances are common: microcarrier specialists partner with sensor, reactor, and automation vendors to deliver plug-and-play intensification packages that compress facility start-up timelines from 36 months to under 24 months. Sustainability differentiation is rising: suppliers now publish life-cycle assessments, carbon footprints, and recyclability metrics to win ESG-conscious bids from European and North American clients. White-space opportunities persist in edible microcarriers for cultivated meat, where only a handful of start-ups have achieved pilot-plant validation, and in ultra-shear-resistant carriers tailored to perfusion rates above 3 vessel volumes per day.

Price competition remains limited because qualification costs lock customers into multi-year supply contracts. However, regional entrants in China, India, and South Korea are undercutting incumbents by 10–15% on commodity polystyrene lines, forcing established firms to move up the value chain with hybrid carriers and digital services. Overall, technology depth rather than raw price defines competitive advantage, underpinning continuous growth in the microcarrier market.

Microcarrier Industry Leaders

-

Thermo Fisher Scientific

-

Merck KGaA

-

Eppendorf AG

-

Danaher Corporation

-

Sartorius AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Commercial-scale vaccine and biologics manufacturing continues to anchor demand for mature, regulator-familiar microcarrier chemistries, while the clearest whitespace sits in workflows that combine intensified adherent culture with closed automation. Opportunities are strongest around platforms that reduce seed-train burden, support high-density stirred-tank and perfusion workflows, and improve batch-to-batch consistency through process analytical technology integration, which matches the shift toward single-use and continuous manufacturing reflected in current operations.

Innovation at the product and workflow level also creates room in harvest simplification and end-to-end logistics. Dissolvable or degradable microcarriers that remove filtration-intensive steps, along with microcarrier-assisted cryogenic storage concepts that integrate attachment, cryopreservation, and thawing to reduce post-thaw handling, are practical targets. Published 2026 research demonstrations of integrated, scalable mesenchymal stromal cell manufacturing platforms that eliminate a traditional seed train indicate active progress on higher volumetric productivity and more standardized upstream operations, while also pointing to unresolved engineering needs around shear heterogeneity and growth-surface discontinuities. Those gaps leave room for differentiated carrier designs and mixing strategies.

Recent Industry Developments

- March 2026: Cellevate AB entered a strategic collaboration with InVitria Inc. to pair specialized cell culture media with the Cellevat3d nanofiber microcarrier platform for viral vaccine production. The combination aims to improve upstream yield and consistency by co-optimizing media and carrier performance as a single workflow rather than as separate inputs.

- January 2026: Kuraray initiated US sales of its SCAPOVA CL and SCAPOVA AS PVA-based microcarriers following their earlier launch. The expansion increases access to synthetic, biocompatible microcarriers for regenerative medicine and other adherent-cell workflows that emphasize consistent material supply and scalable processing.

- July 2025: Sartorius completed the acquisition of MatTek, a producer of human cell-based microtissues and 3D models. Adding these 3D biology capabilities strengthens Sartorius offerings around advanced cell models used in development and process optimization, complementing upstream tools and materials used in microcarrier-enabled production.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the microcarrier market is sized as the value generated from products used to expand adherent cells on microcarriers in bioreactors and related cell culture workflows, including supporting consumables and selected lab and production equipment sold for these use cases.

Scope exclusions: We exclude cell lines, finished biologic drugs, and contract manufacturing service revenues, even when microcarriers are used during production.

Segmentation Overview

-

By Material Type

- Polystyrene-based

- Dextran-based

- Alginate-based

- Collagen-/Gelatin-based

- Others

-

By Application

- Vaccine Manufacturing

- Cell Therapy

- Others

-

By End User

- Biopharma and Biotechnology Firms

- CROs and CDMOs

- Academic & Research Institutes

- Others

-

By Scale of Operation

- Laboratory Scale

- Pilot Scale

- Commercial Scale

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand environment where microcarriers are purchased and consumed, then linking it to supply-side signals. We reference public source types such as the US FDA databases for biologics and vaccines, NIH and other grant award portals for funded cell and gene therapy work, and ClinicalTrials.gov for the flow of cell therapy and vaccine trials that influence scale-up needs.

To keep assumptions grounded, we also review sources such as the World Health Organization for vaccine programs, OECD and national statistical agencies for R&D intensity and manufacturing indicators, and USPTO or similar patent filings to understand technology direction in microcarrier materials and coated surfaces. Company annual reports, investor presentations, and press releases help interpret pricing moves and capacity announcements. We selectively use paid subscriptions for company financials, patent analytics, and shipment-level trade reads where product coding allows. These examples are not exhaustive, and we reviewed additional public sources to collect data points, validate patterns, and clarify open questions.

Primary Interviews and Surveys

Primary discussions are used to pressure test what we built from desk inputs, especially around how microcarriers are selected, how frequently consumables are reordered, and how equipment purchases track the move from R&D into process development and commercial scale. We speak with stakeholders across suppliers, bioprocess users, and distribution channels. For this global market, we cover APAC, EMEA, and the Americas so regional adoption timing and price realization can be compared consistently.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 16% | APAC: 46% |

| Mid tier: 47% | Functional/Unit leaders: 31% | EMEA: 31% |

| Smaller Players: 22% | Managers: 53% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a mix of top-down and bottom-up checks. The top-down path reconstructs demand from the adherent cell culture footprint across bioprocessing and scale-up activity, then allocates spend to microcarriers, related consumables, and supporting lab and production equipment. To keep the model practical, we track inputs such as the count and stage mix of relevant clinical trials, biologics and vaccine manufacturing intensity, the shift toward single-use bioreactors, and the share of adherent cell processes that use microcarriers versus alternative formats.

Results are corroborated with selective bottom-up approximations, including sampled price points for key consumables, usage frequency per run, and channel checks on how equipment bundles are typically sold alongside microcarrier workflows. When inputs are missing for smaller countries or early-stage applications, gaps are handled through proxy ratios tied to R&D spending and biomanufacturing activity, then adjusted after interviews.

For forecasting, we use scenario analysis so adoption can flex with the pace of cell and gene therapy scaling, vaccine program variability, and material innovation. The time series is smoothed using exponential trends where signals are stable. Final growth rates are cross-checked with what experts consider realistic for capacity additions, procurement cycles, and expected pricing progression.

Data Validation & Update Cycle

Validation is done in layers so one weak data point does not swing the outcome. We compare modeled totals against independent signals such as regional biomanufacturing expansion, funding and trial momentum, and observed procurement patterns for consumables versus equipment, then investigate any sharp jumps that do not match the story in the data.

Before sign-off, the model and assumptions go through stepwise analyst reviews, and follow-up outreach is triggered when interview feedback conflicts with desk signals or when pricing and mix shifts look unusual. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the most current view at the time of publication.

Mordor Intelligence's Microcarrier Market Size Measured Against Other Published Estimates

Published sizes for microcarriers can look far apart even when the topic sounds the same. Each estimate draws the line differently around what is counted and how fast adoption is assumed to expand. The table helps show that the spread usually comes from scope choices, base year alignment, and how consumables and equipment are treated in the value build.

The benchmark table shows a higher 2026 value. In Mordor Intelligence's model, the market includes not only microcarrier beads but also related equipment and consumables used in the same adherent cell growth workflows (for example, bioreactors, reagents, cell counters, and culture vessels), which can lift the total versus narrower product-only reads.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.27 B (2026) | |

| Industry Publisher A | USD 1.95 B (2024) | Uses a different base year and may present the market closer to core microcarriers and recurring consumables, with equipment treated as a separate line item or only partially captured, which shifts the total downward versus a workflow-led scope. |

| Research House B | USD 1.68 B (2024) | Leans on a product-split view where consumables dominate and equipment is smaller, and the forecast path is more aggressive, so the starting value can be lower even if the long-term number rises faster due to adoption assumptions and price progression. |

Overall, the comparison points to two practical drivers, which are what is counted around the microcarrier workflow and which year is used for the headline value. By keeping inputs tied to observable bioprocess activity and by clearly separating consumables from equipment within the same use case, the final size is easier to audit and repeat across regions.

Key Questions Answered in the Report

What is the current size of the microcarrier market?

The microcarrier market size reached USD 2.27 billion in 2026 and is forecast to climb to USD 3.01 billion by 2031.

Which material dominates the microcarrier market?

Polystyrene-based carriers led with 42.88% of the microcarrier market share in 2025, thanks to their established regulatory acceptance.

Why is Asia-Pacific the fastest-growing region?

Government investment exceeding USD 8 billion in bioprocess infrastructure, coupled with lower operating costs and biosimilar expansion, is driving a 6.68% CAGR in Asia-Pacific.

How are magnetic microcarriers improving manufacturing efficiency?

Magnetic cores enable inline separation, reducing harvest cycles from hours to minutes and cutting labor costs by up to 40%.

What challenges limit large-scale microcarrier cultures?

High shear stress and cell-carrier aggregation in reactors above 1,000 L can damage cells and lower yields, requiring advanced impeller designs or specialized carrier coatings.

How will single-use technologies influence future demand?

With over 60% of new biologics facilities adopting disposable systems, carriers compatible with gamma irradiation and real-time analytics are set to capture a growing share of the microcarrier market.

Page last updated on: