Bilirubin Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.72 Billion |

| Market Size (2031) | USD 3.70 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

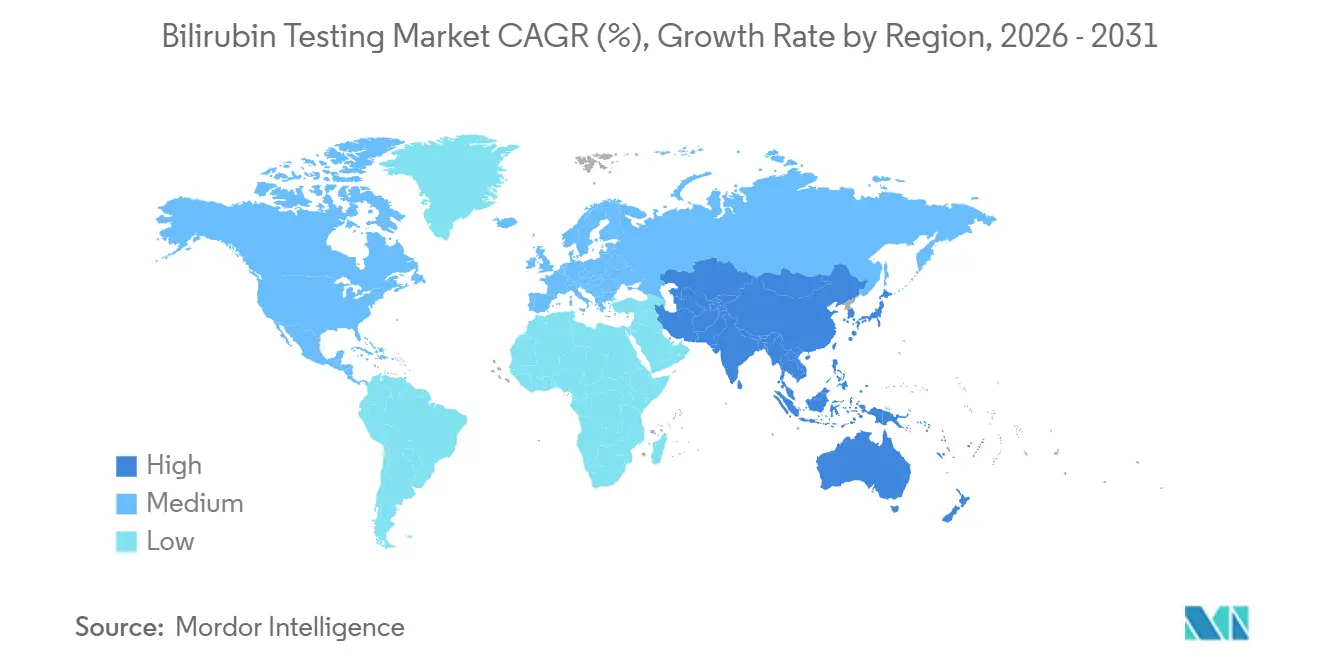

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

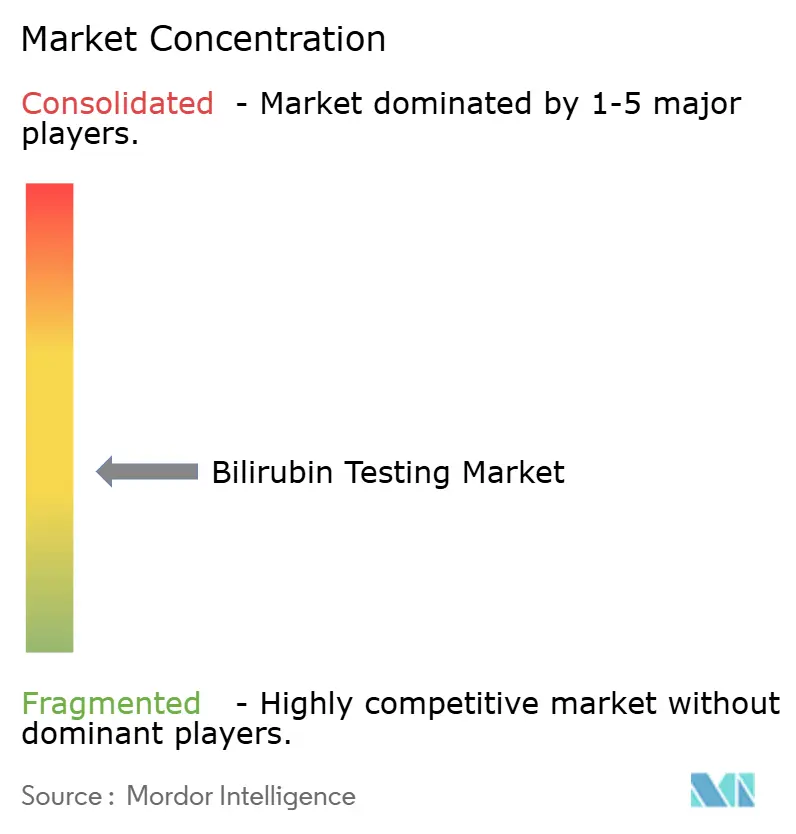

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bilirubin Testing Market Analysis by Mordor Intelligence

The Bilirubin Testing Market size is expected to increase from USD 2.55 billion in 2025 to USD 2.72 billion in 2026 and reach USD 3.70 billion by 2031, growing at a CAGR of 6.38% over 2026-2031.

The bilirubin testing market is experiencing growth due to the formalization of neonatal jaundice screening in hospitals and public health systems, alongside the continued use of bilirubin testing in routine adult liver disease care. Updated guidance from the American Academy of Pediatrics has increased the need for repeated bilirubin checks, as more newborns are monitored in observation pathways instead of receiving immediate phototherapy. This shift has driven higher test volumes per care episode. A similar trend is evident in Asia, where Chinese neonatal guidelines have standardized transcutaneous bilirubin monitoring in primary care, boosting device adoption and repeat testing demand.

Key Report Takeaways

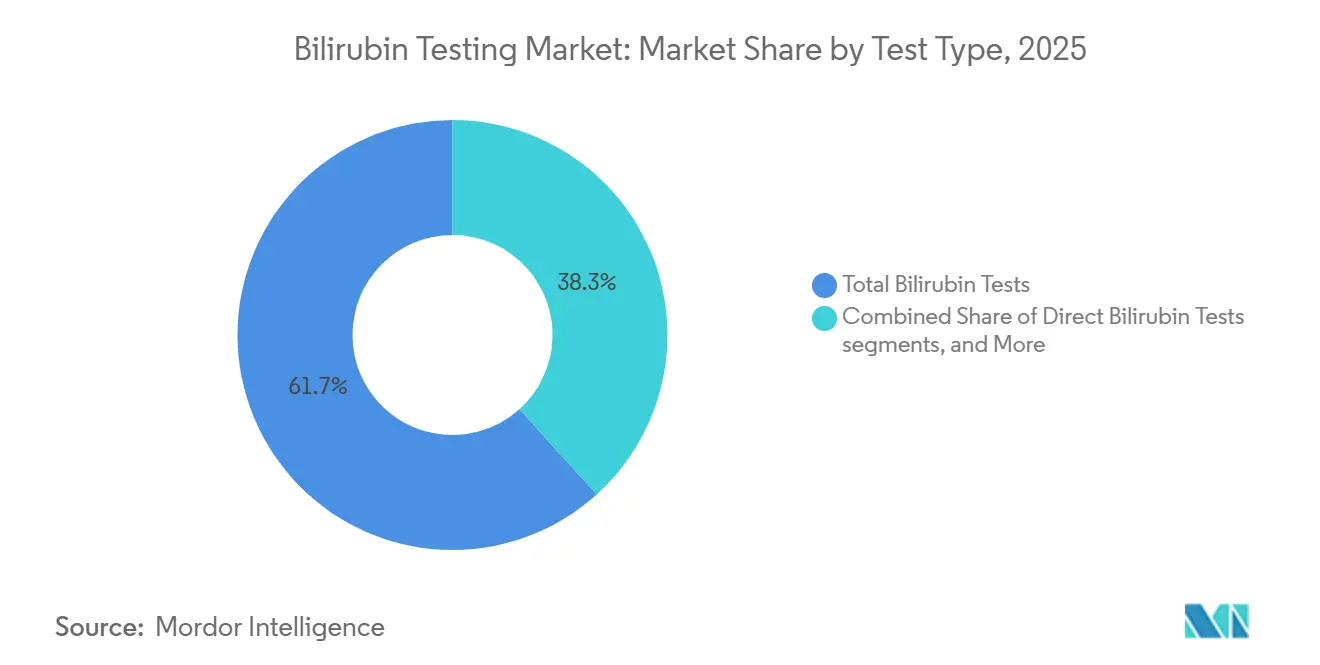

- By test type, total bilirubin tests held 61.68% share in 2025, while direct bilirubin tests are projected to grow at a 6.90% CAGR through 2031.

- By product type, reagents and assay consumables accounted for 58.23% share in 2025, while calibrators and quality controls are expected to expand at a 7.25% CAGR through 2031.

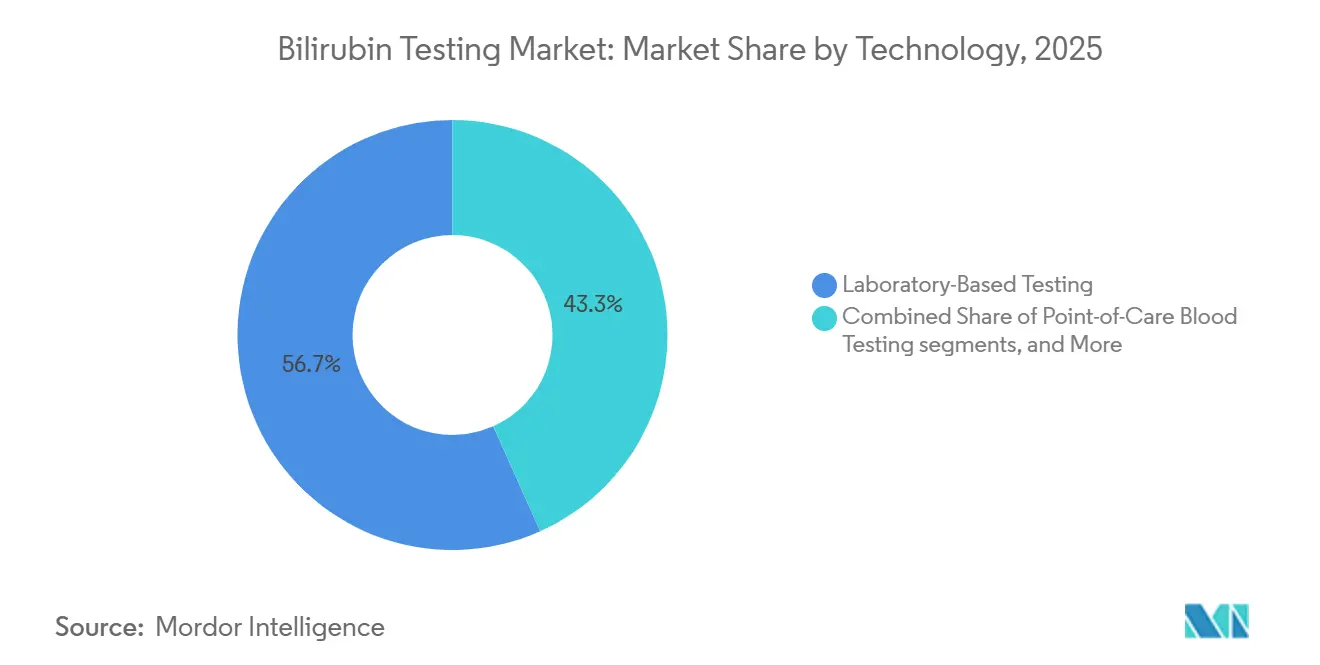

- By technology, laboratory-based testing represented 56.74% share in 2025, while point-of-care blood testing is forecast to advance at a 7.95% CAGR through 2031.

- By application, liver function assessment accounted for 52.71% of the bilirubin testing market size in 2025, while neonatal jaundice screening and monitoring is projected to grow at an 8.20% CAGR through 2031.

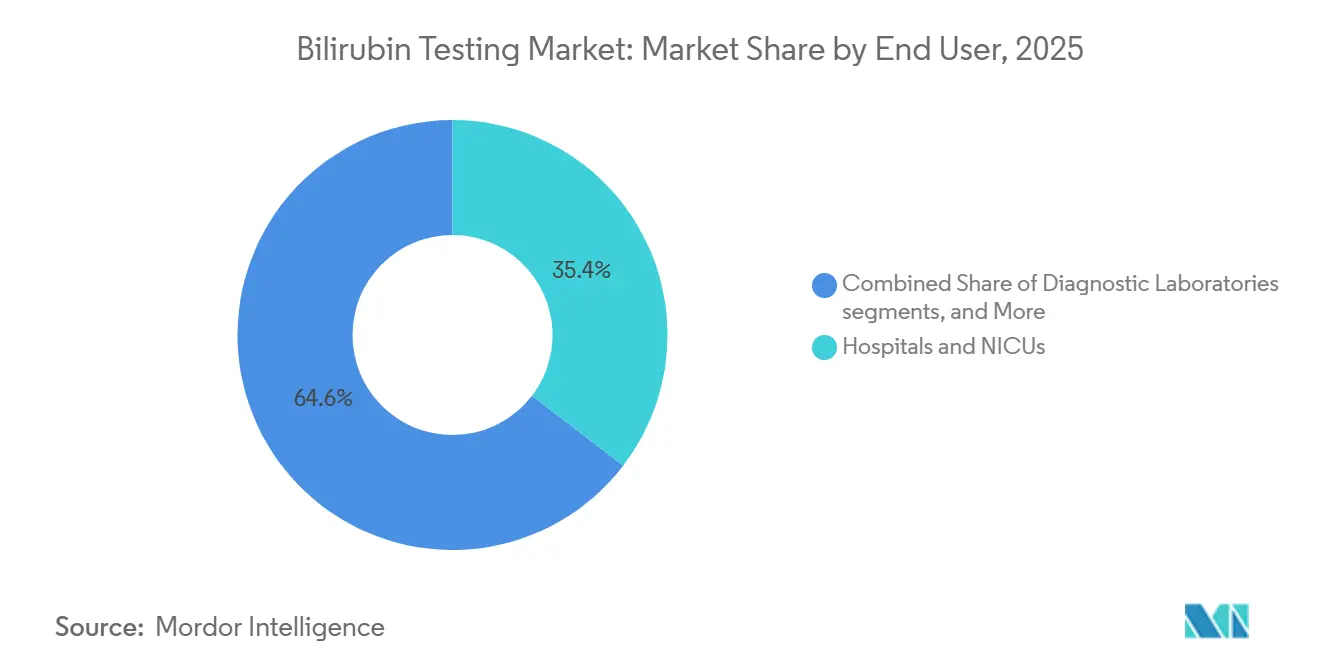

- By end user, hospitals and NICUs represented 35.44% share in 2025, while point-of-care blood testing is forecast to advance at a 6.65% CAGR through 2031.

- By geography, North America held 39.55% of the bilirubin testing market share in 2025, while Asia-Pacific is expected to expand at a 6.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bilirubin Testing Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising neonatal jaundice screening requirements | +1.8% | Global, with highest concentration in Asia-Pacific, North America, and Middle East and Africa | Long term (≥ 4 years) |

| Shift toward non-invasive transcutaneous bilirubin monitoring | +1.4% | North America, Europe, and Asia-Pacific including China, India, and Japan | Medium term (2-4 years) |

| Expansion of point-of-care bilirubin testing in NICUS and community settings | +1.0% | Asia-Pacific core, with spillover into Middle East and Africa and South America | Medium term (2-4 years) |

| Updated hyperbilirubinemia screening guidelines mandating universal testing | +0.8% | North America, Europe, and Australasia | Short term (≤ 2 years) |

| EMR-integrated bilirubin workflows for closed-loop neonatal management | +0.6% | North America and Western Europe | Medium term (2-4 years) |

| Higher validation demand for skin tone accuracy and phototherapy conditions | +0.3% | Global, with near-term focus in North America and the European Union | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Neonatal Jaundice Screening Requirements

Neonatal jaundice, a prevalent condition in newborn care, underscores the importance of bilirubin monitoring, bolstering the market for bilirubin testing. Public health systems are expanding formal screening coverage, transitioning bilirubin testing from an optional procedure to a standard protocol in maternity settings. In January 2026, NSW Health revised its neonatal jaundice management guidelines, introducing universal transcutaneous screening for babies as young as 32 weeks gestation, thereby broadening the screened population in an established care system.[1]NSW Health, “Neonatal Jaundice and Hyperbilirubinaemia Identification and Management Guideline,” NSW Health, health.nsw.gov.au Similarly, in 2025, China mandated transcutaneous bilirubin monitoring within 48 hours of birth at grassroots institutions, integrating national guidance into the daily operations of lower-tier facilities. In India, the Mission ANMOL initiative incorporates bilirubin testing into a comprehensive newborn screening framework, bolstering demand in public facilities catering to large infant populations.

Shift Toward Non-Invasive Transcutaneous Bilirubin Monitoring

Due to the desire for quicker screenings with minimal discomfort, the bilirubin testing market is increasingly favoring non-invasive transcutaneous measurements. This shift is particularly significant in high-volume nurseries and intensive care units, where the speed of workflow can influence discharge and treatment decisions. A 2026 study highlighted the Picterus Jaundice Pro smartphone application, which demonstrated a strong correlation with transcutaneous reference measurements across 215 paired readings, underscoring the growing clinical utility of cost-effective optical tools.[2]World Health Organization, “WHO Recommendations on Postnatal Care of the Mother and Newborn,” World Health Organization, iris.who.int

While serum confirmation remains essential near treatment thresholds, the market is benefiting from the transcutaneous approach, as it diminishes the need for invasive tests prior to escalation.

Expansion of Point-of-Care Bilirubin Testing in NICUs and Community Settings

As hospitals and peripheral centers increasingly adopt point-of-care devices for bilirubin testing, the market is gravitating closer to the bedside. This shift is crucial in environments where central laboratory turnaround times are prolonged, or where immediate results are vital for decisions on observation, discharge, or phototherapy. An October 2025 study in Pediatric Research highlighted the Bilistick 2.0 device's strong diagnostic agreement with reference laboratory methods in a bustling neonatal unit in South India, bolstering its adoption in resource-limited settings.[3]Government of India, “Mission ANMOL,” Government of India, india.gov.in Another 2025 study in the Indian Journal of Clinical Biochemistry underscored the efficacy of capillary point-of-care samples in identifying neonates surpassing the phototherapy threshold, easing the path for outpatient and near-patient testing.[4]Sundaram M., Muthusamy A., Balachandran A., Natarajan M., “Diagnostic Performance of Point-of-Care Bilirubin Testing with Bilistick 2.0 Device at a South Indian Clinical Site,” Pediatric Research, nature.com

Updated Hyperbilirubinemia Screening Guidelines Mandating Universal Testing

Policy shifts increasingly advocate for universal and documented screening, bolstering the bilirubin testing market. Current pediatric guidelines in the U.S. mandate universal bilirubin assessments for newborns at or above 35 weeks within 24-48 hours, elevating bilirubin testing to a standard discharge procedure. In 2025, China echoed this sentiment, aligning both tertiary and primary neonatal care practices with consistent monitoring protocols. The World Health Organization has integrated universal newborn screening for hyperbilirubinemia into its routine postnatal care recommendations, a stance now adopted by several national frameworks in 2025 and 2026. As these guidelines permeate healthcare systems, the market for bilirubin testing solidifies, with test orders becoming a matter of protocol adherence rather than individual physician discretion.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Mandatory serum confirmation near treatment threshold constraining tcb uptake | -0.8% | Global, most acute in mid-tier hospitals in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Cost and service burden of analyzer calibration and uptime maintenance | -0.6% | Asia-Pacific including South and Southeast Asia, Middle East and Africa, and South America | Long term (≥ 4 years) |

| Measurement variability under phototherapy and in high-jaundice conditions | -0.5% | Global, concentrated in high-acuity NICU settings | Short term (≤ 2 years) |

| Limited utilization of bilirubin analyzers outside high-birth-volume care settings | -0.4% | Rural and peri-urban areas in South Asia, Sub-Saharan Africa, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Serum Confirmation Near Treatment Threshold

The bilirubin testing market faces limitations as non-invasive methods cannot fully replace serum testing near treatment thresholds. Clinical protocols require total serum bilirubin confirmation in such cases, meaning transcutaneous devices reduce but do not eliminate invasive sampling. Neonatal bilirubin testing remains complex due to interlaboratory variations and differences in bilirubin fractions, which impact safe decision-making. This sustains demand for reagents, calibrators, and laboratory assays, even as transcutaneous screening expands. Hospitals must maintain dual workflows for screening and confirmation, slowing full substitution for device manufacturers.

Cost And Service Burden Of Analyzer Calibration And Uptime Maintenance

The bilirubin testing market also faces challenges from the operational demands of analyzers, particularly in facilities with limited technical support. Automated chemistry systems require calibration, quality control, preventive maintenance, and method updates, adding recurring costs beyond the instrument purchase. In June 2025, Roche updated its OPE-free Bilirubin Total Gen.3 reagent formulation under EU REACH requirements, requiring laboratories to adjust instrument settings and carry-over procedures to maintain performance. These demands are easier for large hospitals to manage than for smaller facilities, slowing market growth in resource-limited settings despite clear patient needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Total Bilirubin Anchors Routine Clinical Demand

In 2025, Total Bilirubin Tests held 61.68% of the bilirubin testing market share, highlighting their critical role in routine diagnostics. This test is essential for managing newborn jaundice and assessing liver function in adults, ensuring its widespread use across various age groups and healthcare settings. The market's reliance on total bilirubin remains strong due to its integration into major care pathways and its role as the primary marker in standardized protocols, making the segment resilient even with the emergence of new technologies.

Direct Bilirubin Tests are projected to grow at a 6.90% CAGR through 2031, driven by increased focus on conjugated hyperbilirubinemia in neonates and comprehensive hepatobiliary assessments in adults. Clinical Pathology Laboratories updated reporting and reference ranges for direct bilirubin in February 2025, reflecting a more refined clinical approach. Indirect bilirubin testing remains significant for hemolytic disease and G6PD-related assessments, particularly in populations with hereditary risks. The market is expected to see more fractionated panels integrated into workflows, increasing testing volumes per specimen despite pricing pressures.

By Product Type: Reagent Consumables Sustain Recurring Platform Revenue

Reagents and Assay Consumables accounted for 58.23% of the bilirubin testing market in 2025, reflecting the recurring nature of chemistry-based testing. This segment benefits from repeat bilirubin orders processed on automated analyzers, providing a stable revenue base. Laboratories often remain within validated reagent ecosystems, ensuring repeat purchases and reducing vendor switching. This dynamic secures the position of reagent suppliers even during slower equipment procurement periods.

Calibrators and Quality Controls are expected to grow at a 7.25% CAGR through 2031, supported by the expansion of bilirubin testing into decentralized care points. As bedside and near-patient testing increases, new locations drive demand for verification materials. Test cartridges and strips remain vital in point-of-care settings, enabling single-use testing without the maintenance demands of central analyzers, creating a balanced product structure within the market.

By Technology: Laboratory Infrastructure Leads As Point-Of-Care Closes The Gap

Laboratory-Based Testing held a 56.74% share in 2025, underscoring the dominance of central laboratory infrastructure in handling high testing volumes. Hospital networks and independent labs continue to rely on automated systems for confirmatory testing and routine adult hepatology panels. High-throughput chemistry platforms remain critical for maintaining operational efficiency and meeting demand.

Point-of-Care Blood Testing is forecast to grow at a 7.95% CAGR through 2031, making it the fastest-growing technology category. Its appeal lies in faster clinical decision-making, particularly in neonatal care. Suppliers are focusing on simplifying workflows and enhancing infection control, driving adoption in time-sensitive screening scenarios. The market is moving toward a mixed technology model, with laboratories maintaining volume leadership while point-of-care tools capture a growing share of urgent testing needs.

By Application: Neonatal Jaundice Screening Commands The Fastest Growth Trajectory

Liver Function Assessment accounted for 52.71% of the bilirubin testing market in 2025, driven by its routine use in adult hepatology. Bilirubin remains a standard biomarker for hepatitis monitoring, cirrhosis staging, and general hepatic evaluations, ensuring stable demand across diverse patient groups and care settings.

Neonatal Jaundice Screening and Monitoring is projected to grow at an 8.20% CAGR through 2031, driven by formal screening protocols requiring predischarge or early postnatal monitoring. Expanded protocols in mature health systems are increasing testing volumes. Neonatal screening is becoming a key driver of repeat testing activity, complementing the stable demand from adult liver testing.

By End User: Hospitals And NICUs Drive The Majority Of Test Volume

Hospitals and NICUs dominate the bilirubin testing market, managing significant neonatal cases and complex confirmatory workflows. These facilities have the necessary infrastructure and staffing for serial monitoring, making them central to the market. Maternity and neonatal clinics are also gaining relevance as predischarge screenings become standard practice.

Diagnostic laboratories play a critical role in processing outpatient liver function panels, referral workups, and post-discharge samples. While outpatient and ambulatory centers are emerging as cost-effective alternatives for routine follow-ups, laboratories remain integral to the value chain, ensuring a broadening end-user mix while hospitals and NICUs continue to define core demand patterns.

Geography Analysis

In 2025, North America dominated the bilirubin testing market, holding a 39.55% share. This leadership is driven by structured newborn screening programs, widespread access to automated chemistry platforms, and hospitals' adoption of defined bilirubin care pathways. The U.S. remains the largest market in the region due to the integration of universal newborn bilirubin assessments into pediatric care guidelines and continuous updates to testing platforms by major suppliers. In 2026, Roche and Siemens achieved significant U.S. regulatory milestones for bilirubin-related chemistry capabilities, strengthening the installed base and product updates. Canada supports the market with aligned pediatric screening practices, while Mexico contributes through hospital-based diagnostic demand linked to maternal and newborn care.

Asia-Pacific is projected to grow at a 6.76% CAGR through 2031, making it the fastest-growing region in the bilirubin testing market. China's 2025 neonatal guidelines formalized transcutaneous bilirubin monitoring, driving procurement across lower-tier care sites. India is advancing through public healthcare programs that expand affordable diagnostic access and local validation efforts supporting point-of-care bilirubin use in neonatal wards. Countries like Japan, South Korea, and Australia, with mature NICU infrastructures, continue to grow, with Australia demonstrating in 2026 that broader screening protocols can unlock additional volumes.

Europe maintains a strong position in the bilirubin testing market due to structured neonatal care pathways, stable public reimbursements, and high laboratory quality standards. The region's combined use of transcutaneous and laboratory methods sustains demand for both devices and consumables. In the Middle East and Africa, clinical needs are significant, particularly in areas with high incidences of neonatal jaundice and inherited hemolytic conditions, though infrastructure and service capacity remain challenges. South America shows steady growth, supported by public maternity screenings and general diagnostic demand, despite variations in access and purchasing power across countries.

Competitive Landscape

Central laboratory systems dominate the bilirubin testing market, while point-of-care and transcutaneous devices exhibit a more moderately fragmented landscape. Major players like Roche, Siemens Healthineers, Beckman Coulter, and Abbott wield significant influence, as bilirubin testing is a key component of broader chemistry menus, creating switching costs for hospitals. This segment of the market is shaped more by platform relationships, service contracts, reagent compatibility, and regulatory continuity than by competition over single tests. Laboratory suppliers strengthen their positions through menu updates, increased throughput, and method reliability, rather than relying solely on pricing strategies.

In March 2026, Roche enhanced its market position by obtaining FDA 510(k) clearance for its cobas c 703 and cobas ISE neo analytical units, increasing throughput for high-volume hospital laboratories. Siemens Healthineers expanded its chemistry portfolio in February 2026 with FDA clearance for the Atellica CH Diazo Total Bilirubin assay, ensuring the Atellica platform remained current. Roche's 2025 update of its Bilirubin Total Gen.3 reagent formulation, in compliance with EU REACH requirements, highlights the importance of formulation, workflow settings, and compliance in maintaining platform loyalty within established laboratories. These developments reinforce the market's reliance on established chemistry infrastructure for adult liver assessments and neonatal serum confirmations, while posing challenges for smaller laboratories competing with entrenched global platforms in high-volume hospital settings.

On the neonatal front, the bilirubin testing market is more dynamic, with suppliers focusing on user-friendliness, non-invasive designs, portability, and accurate screening. International Biomedical's April 2026 launch of the BiliChek System exemplifies this approach, combining transcutaneous assessment with disposable calibration tips tailored to NICU infection-control standards. As competition grows, particularly regarding optical accuracy across diverse skin tones and phototherapy conditions, validation quality is becoming as critical as hardware design. This evolving landscape fosters innovation and rewards companies that integrate clinical validation with practical workflow benefits.

Bilirubin Testing Industry Leaders

Koninklijke Philips N.V.

F. Hoffmann-La Roche Ltd

Abbott Laboratories

Drägerwerk AG and Co. KGaA

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: International Biomedical introduced the BiliChek System, a non-invasive bilirubin assessment device for NICUs and newborn nurseries, featuring advanced light-based technology and disposable calibration tips for infection control.

- March 2026: Roche received FDA clearance for cobas c 703 and ISE neo units, enabling 2,000 chemistry tests per hour and enhancing the throughput capacity of the cobas pro modular platform for high-volume hospital labs.

- February 2026: Siemens Healthineers obtained FDA clearance for the Atellica CH Diazo Total Bilirubin assay following a 245-day review process.

- January 2026: NSW Health updated its Neonatal Jaundice and Hyperbilirubinaemia guideline, mandating universal transcutaneous bilirubin screening for gestations as early as 32 weeks, replacing the 2016 guideline.

- February 2025: Clinical Pathology Laboratories revised direct bilirubin testing protocols, updating reporting ranges, specimen stability guidance, and newborn-specific thresholds.

Global Bilirubin Testing Market Report Scope

As per the scope of the report, a bilirubin test is a blood test that measures the amount of bilirubin in your blood. Bilirubin is a yellow waste product made when your body breaks down old red blood cells. It travels to the liver, where it is processed and mixed into bile to be removed from the body.

The bilirubin testing market is segmented by test type, product type, technology, application, end-user, and geography. By test type, the market includes total bilirubin tests, direct bilirubin tests, and indirect bilirubin tests. By product type, the market is segmented into reagents and assay consumables, calibrators and quality controls, test cartridges and strips, and dedicated blood bilirubin analyzers. By technology, the market is categorized into laboratory-based testing, point-of-care blood testing, and transcutaneous screening systems. By application, the market includes neonatal jaundice screening and monitoring, liver function assessment, hemolytic disorder assessment, and pre-operative and routine health screening. By end-user, the market is segmented into hospitals and NICUs, diagnostic laboratories, maternity and neonatal clinics, and outpatient and ambulatory care centers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Total Bilirubin Tests |

| Direct Bilirubin Tests |

| Indirect Bilirubin Tests |

| Reagents and Assay Consumables |

| Calibrators and Quality Controls |

| Test Cartridges and Strips |

| Dedicated Blood Bilirubin Analyzers |

| Laboratory-Based Testing |

| Point-of-Care Blood Testing |

| Transcutaneous Screening Systems |

| Neonatal Jaundice Screening and Monitoring |

| Liver Function Assessment |

| Hemolytic Disorder Assessment |

| Pre-Operative and Routine Health Screening |

| Hospitals and NICUs |

| Diagnostic Laboratories |

| Maternity and Neonatal Clinics |

| Outpatient and Ambulatory Care Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Total Bilirubin Tests | |

| Direct Bilirubin Tests | ||

| Indirect Bilirubin Tests | ||

| By Product Type | Reagents and Assay Consumables | |

| Calibrators and Quality Controls | ||

| Test Cartridges and Strips | ||

| Dedicated Blood Bilirubin Analyzers | ||

| By Technology | Laboratory-Based Testing | |

| Point-of-Care Blood Testing | ||

| Transcutaneous Screening Systems | ||

| By Application | Neonatal Jaundice Screening and Monitoring | |

| Liver Function Assessment | ||

| Hemolytic Disorder Assessment | ||

| Pre-Operative and Routine Health Screening | ||

| By End User | Hospitals and NICUs | |

| Diagnostic Laboratories | ||

| Maternity and Neonatal Clinics | ||

| Outpatient and Ambulatory Care Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the bilirubin testing space in 2026?

It is valued at USD 2.72 billion in 2026 and is forecast to reach USD 3.70 billion by 2031 at a 6.38% CAGR.

What is driving demand for bilirubin testing most strongly right now?

Universal newborn screening, wider use of transcutaneous monitoring, and stable demand from liver function testing are the main growth drivers.

Which application area is growing the fastest through 2031?

Neonatal Jaundice Screening and Monitoring is the fastest-growing application, with an 8.20% CAGR through 2031.

Which region leads global demand for bilirubin testing?

North America led in 2025 with a 39.55% share, supported by structured screening protocols and a large installed laboratory base.

Why are point-of-care bilirubin devices gaining attention?

They support faster bedside decisions, require small sample volumes, and are increasingly backed by peer-reviewed validation data in neonatal care.

What still limits full replacement of serum bilirubin testing?

Clinical protocols still require serum confirmation near treatment thresholds, so transcutaneous and point-of-care tools support screening but do not fully replace laboratory testing.

Page last updated on: