Bilirubin Blood Test Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.5 Billion |

| Market Size (2031) | USD 2.02 Billion |

| Growth Rate (2026 - 2031) | 6.16% CAGR |

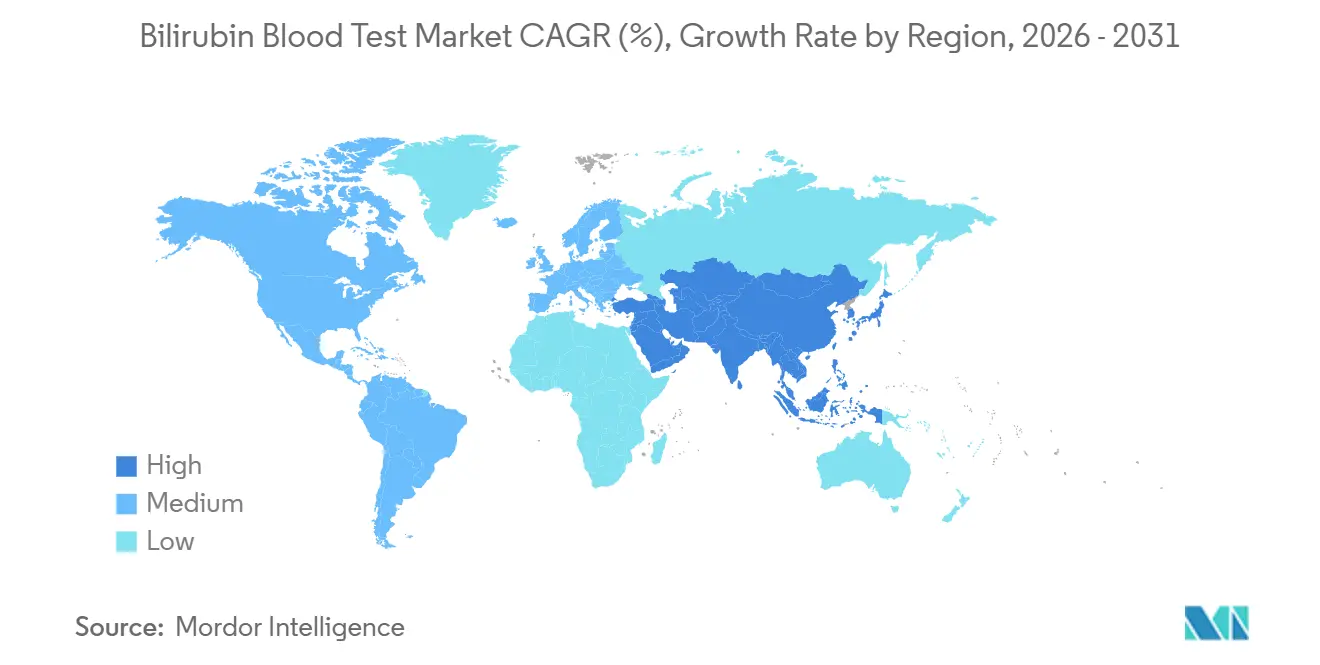

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bilirubin Blood Test Market Analysis by Mordor Intelligence

The Bilirubin Blood Test Market size is expected to increase from USD 1.42 billion in 2025 to USD 1.5 billion in 2026 and reach USD 2.02 billion by 2031, growing at a CAGR of 6.16% over 2026-2031.

Demand stays firm because neonatal jaundice remains a routine testing need, with the condition affecting 60% of term newborns and 80% of preterm newborns globally, which keeps bilirubin measurement central to perinatal care workflows. Testing volumes also remain supported by the liver disease burden, as MASLD affects 38% of adults worldwide and keeps bilirubin embedded in standard liver function panel ordering. North America leads current demand because screening guidance, reimbursement support, and chemistry automation are well established, while Asia-Pacific is set to grow faster as neonatal care capacity expands and procurement of bilirubin testing devices rises across major hospitals. The bilirubin blood test market is also benefiting from a gradual move toward point-of-care and outpatient monitoring, even though laboratory platforms still anchor most testing because clinical thresholds continue to require confirmatory serum measurement. Competition remains moderate rather than highly concentrated, and vendor positioning increasingly depends on platform traceability, assay comparability, service contracts, and the ability to lower capital barriers in neonatal screening settings.

Key Report Takeaways

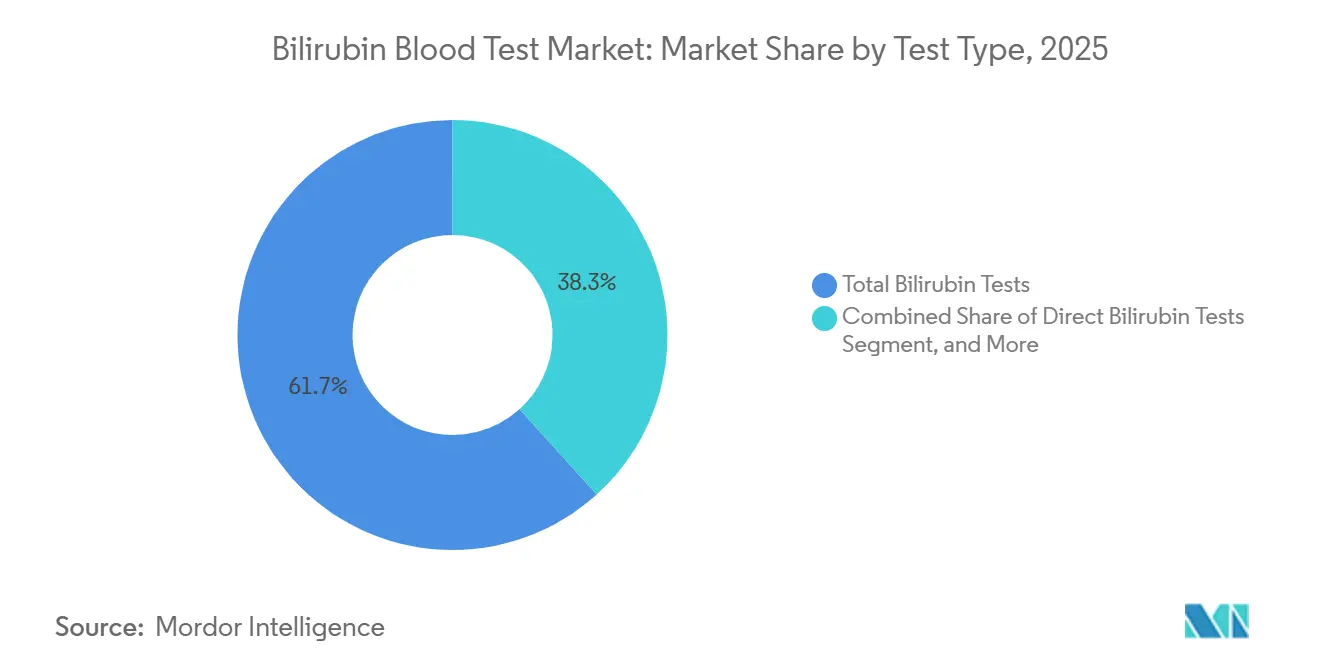

- By test type, total bilirubin tests led with 61.68% share in 2025, while direct bilirubin tests are forecast to grow at 7.94% through 2031.

- By product type, reagents and assay consumables accounted for 63.23% share in 2025, while bilirubin analyzers and meters are projected to grow at 7.66% through 2031.

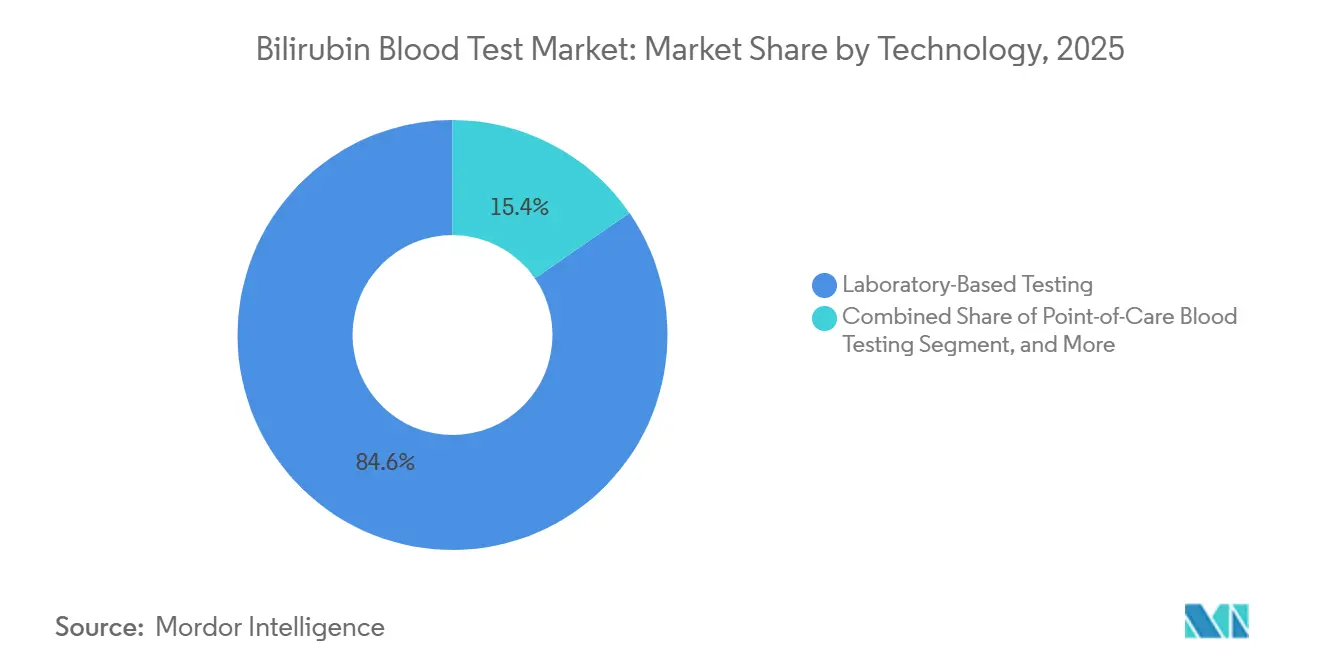

- By technology, laboratory-based testing held 84.62% share in 2025, while point-of-care blood testing is projected to advance at 8.54% through 2031.

- By application, liver function assessment captured 52.71% share in 2025, while neonatal jaundice screening and monitoring are projected to grow at 9.67% through 2031.

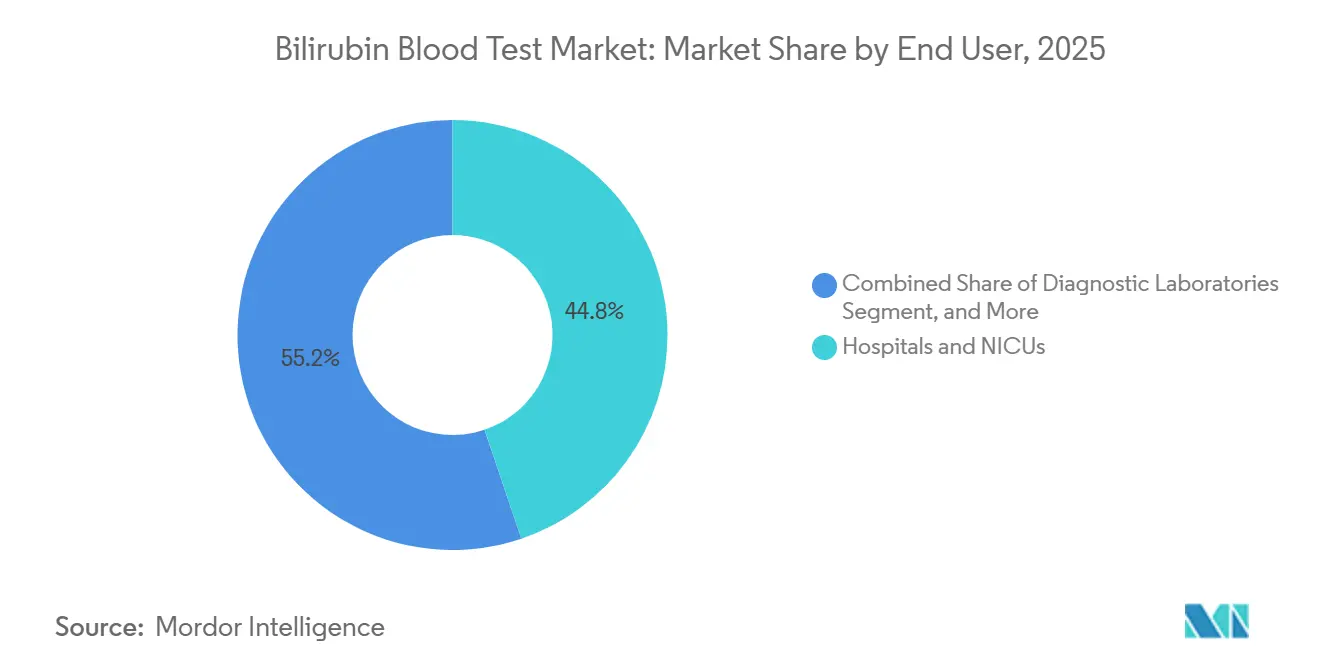

- By end user, hospitals and NICUs held 44.81% share in 2025, while outpatient and ambulatory care centers are forecast to grow at 8.85% through 2031.

- By geography, North America held 48.21% share in 2025, while Asia-Pacific is projected to expand at 8.45% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bilirubin Blood Test Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Neonatal Jaundice Screening Intensity | +1.6% | Global, with strongest effect in North America, Europe, Japan, and Australia | Short term (≤ 2 years) |

| Growing Liver Disease Diagnostic Volumes | +1.2% | Global, with stronger concentration in North America, Europe, and emerging Asia-Pacific and MEA | Medium term (2-4 years) |

| Expansion of Routine Hospital Chemistry Testing | +0.8% | Global, with Asia-Pacific and MEA driving new volume | Medium term (2-4 years) |

| Adoption of Point-of-Care Bilirubin Workflows | +0.8% | North America, Europe, and resource-limited neonatal settings | Short term (≤ 2 years) |

| Increasing Use of Transcutaneous Pre-Screening | +0.6% | Global, especially Japan, Europe, and Australia | Short term (≤ 2 years) |

| Remote Newborn Follow-Up and Digital Jaundice Monitoring | +0.5% | North America and Europe first, followed by Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Neonatal Jaundice Screening Intensity

The bilirubin blood test market is gaining a stable demand base because neonatal bilirubin screening has moved from a preferred practice to a routine care expectation in many hospital systems. The AAP technical report kept predischarge bilirubin measurement central to newborn care, which supports repeated total bilirubin testing and follow-up measurement in at-risk infants.[1]Vinod K. Bhutani, Ronald J. Wong, David Turkewitz, et al., “Phototherapy to Prevent Severe Neonatal Hyperbilirubinemia in the Newborn Infant 35 or More Weeks of Gestation: Technical Report,” Pediatrics, publications.aap.org Australia strengthened this pattern when NSW updated its neonatal jaundice guideline in January 2026 and mandated universal transcutaneous bilirubin screening with broader gestational coverage. The bilirubin blood test market also benefits from a second testing step because jaundiced infants often need conjugated bilirubin measurement when cholestasis must be ruled out early, and Swiss pediatric guidance formalized that pathway through Biliscreen.org in 2026. This means one clinical event can generate screening, confirmation, and fractionation rather than a single assay, which keeps per-patient test intensity structurally high.

Growing Liver Disease Diagnostic Volumes

The bilirubin blood test market is also supported by routine liver disease workups because total bilirubin remains a standard component of liver function testing across primary care and specialist pathways. MASLD affects 38% of adults worldwide, which sustains large panel volumes that include bilirubin alongside other liver markers.[2]Li Wang and Yajie Wang, “Non-Invasive Tests for the Detection of MASLD: Biomarkers and Imaging for Staging Steatosis, MASH, and Fibrosis,” International Journal of General Medicine, dovepress.com This demand is not displaced by newer fibrosis tools because bilirubin is built into multimarker algorithms such as FibroTest, Hepascore, and SteatoTest, which keep the assay tied to noninvasive liver disease assessment. The bilirubin blood test market is further supported by treatment monitoring and diagnostic expansion in MASH and MASLD workflows, including the 2025 acquisition by Fibronostics to broaden noninvasive liver diagnostics capacity. Hemolytic disease adds another recurring layer because 2025 clinical evidence continued to show that total bilirubin and related markers remain practical tools for monitoring intravascular hemolysis in sickle cell anemia.

Adoption of Point-of-Care Bilirubin Workflows

The bilirubin blood test market is seeing faster adoption of point-of-care workflows because portable serum testing devices are narrowing the accuracy gap with central laboratory analyzers. A four-site Ohio study validated the Bilistick System 2.0 against hospital reference platforms and reported an R² of 0.99 with a mean ratio of 1.005, which supports use in settings that need fast bedside decisions.[3]Jonathan D. Toot, Michelle L. Pershing, Aaron L. Berenson, et al., “Point-of-Care Serum Bilirubin as an Efficient and Comparable Alternative to Hospital Based Testing,” Pediatric Research, doi.org A separate South Indian validation showed that 79% of neonatal samples were within ±2 mg/dL of comparator results, which strengthens the case for decentralized testing in public sector hospitals with limited laboratory capacity. Even so, the bilirubin blood test market does not shift away from central labs as quickly as device growth might suggest, because guidelines still require serum confirmation when readings approach treatment thresholds. This keeps point-of-care and laboratory testing in a linked workflow rather than a substitution model.

Remote Newborn Follow-Up and Digital Jaundice Monitoring

The bilirubin blood test market is also being shaped by digital follow-up tools because bilirubin peaks after many newborns have already left the hospital. The AAP framework kept postdischarge follow-up central to safe neonatal management, which supports more structured testing after the inpatient stay ends. Dräger expanded this care model in March 2025 when it launched BiliPredics, a CE-certified and FDA-registered software tool that forecasts bilirubin progression using prior measurements and clinical data. A multicenter German study validated the algorithm and showed median relative prediction error of 8.5% to 9.5% for prediction windows up to 60 hours, which supports earlier intervention planning and more targeted follow-up visits. As these tools spread, the bilirubin blood test market gains from more scheduled outpatient checks rather than relying only on inpatient screening.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Analyzers and Noninvasive Devices | -1.0% | Most visible in South Asia, Sub-Saharan Africa, Latin America, and smaller community sites | Medium term (2-4 years) |

| Need for Serum Confirmation at Clinical Decision Thresholds | -0.5% | Global across all transcutaneous and point-of-care use cases | Short term (≤ 2 years) |

| Assay Standardization and Interference Limitations | -0.7% | Global, especially where treatment pathways were built around specific reference platforms | Medium term (2-4 years) |

| Cross-Platform Assay Bias and Preanalytical Interference Risk | -0.4% | Global, with stronger effect in multi-vendor networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Analyzers and Noninvasive Devices

The bilirubin blood test market still faces a capital barrier because transcutaneous bilirubinometers from established suppliers remain expensive for smaller facilities. A 2025 Japanese study noted commercial device pricing of USD 5,000 to USD 10,000 per unit, which limits adoption in primary and community settings that screen newborns but do not have large equipment budgets. Public procurement data in China still showed that hospitals were budgeting carefully for neonatal transcutaneous units, with Longyan First Hospital tendering 3 units at RMB 13,000 each, equal to USD 1,790 per unit. These cost limits slow wider penetration across the bilirubin blood test market, especially where township hospitals and community clinics must choose between screening equipment and broader chemistry investments. At the same time, low-cost innovation is emerging, and the same Japanese research validated a wearable TcB prototype with a unit cost near USD 100 and clinically meaningful correlation with serum bilirubin, which suggests that pricing pressure could intensify over time.

Assay Standardization and Interference Limitations

The bilirubin blood test market also faces a technical restraint because assay results still vary across platforms and methods. CAP survey data summarized by NIST showed a 27% gap between maximum and minimum peer-group means in neonatal bilirubin testing, and one Dutch laboratory reported a 3-fold rise in phototherapy starts after moving from a diazo method to vanadate oxidation. The IFCC working group is addressing this through a reference method and external quality assessment alignment effort, but the bilirubin blood test market will not see immediate resolution because traceability changes still require regulatory approval across jurisdictions. Preanalytical issues such as hemolysis and lipemia add another layer because they weaken confidence in low-concentration bilirubin results and make comparisons across sites harder. This slows broader ambulatory and cross-institution programs because clinicians remain cautious when results are not clearly comparable between instruments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Direct Bilirubin Fractionation Gaining Diagnostic Urgency

Within the bilirubin blood test market, total bilirubin tests held 61.68% of the bilirubin blood test market share in 2025. This segment remains the first-line assay in neonatal jaundice protocols, liver panels, and comprehensive chemistry testing. The AAP framework kept predischarge bilirubin measurement and repeat follow-up central to newborn care, which supports repeated ordering across multiple encounters. Direct bilirubin tests are projected to grow at 7.94% through 2031 because neonatal cholestasis workups, MASLD-related hepatobiliary assessment, and hemolytic disorder evaluation increasingly require bilirubin fractionation.

Indirect bilirubin remains important even though it is usually reported as a derived value rather than a separately ordered assay. It still shapes clinical classification because clinicians use it to separate pre-hepatic, hepatic, and post-hepatic patterns of jaundice. A 2025 thalassemia study showed that unconjugated bilirubin above 59.8 µmol/L predicted UGT1A1 variant carriage with an area under the curve of 0.90, which supports its relevance in more specialized follow-up pathways. The bilirubin blood test market is therefore shifting from a simple total bilirubin model toward a broader fractionation mix, especially where pediatric hepatology and neonatal referral systems are becoming more standardized.

By Product Type: Analyzer Hardware Momentum Accelerates Alongside Consumable Dominance

Reagents and assay consumables accounted for 63.23% share of the bilirubin blood test market size in 2025. Their lead reflects the recurring revenue structure created by reagent-rental agreements, where platforms are tied to multiyear supply contracts rather than one-time analyzer sales. This model gives established vendors stronger switching protection and steadier revenue visibility across hospital laboratory accounts. Alberta Precision Laboratories reinforced this pattern in 2025 when it implemented Roche Cobas Pure analyzers across regional sites, which supported single-vendor chemistry standardization and locked in ongoing bilirubin reagent demand.

Calibrators and quality controls remain a smaller revenue category, but they are gaining strategic weight as traceability standards tighten and cross-platform comparability becomes a larger procurement issue. The bilirubin blood test industry is likely to see continued interest in pediatric control materials that can support multiple analyzer families and reduce method-to-method drift. Bilirubin analyzers and meters are the fastest-growing product type at 7.66%, supported by dedicated transcutaneous devices and portable serum analyzers. Beckman Coulter’s 2025 study of the DxC 500i in India showed strong analytical performance with a within-lab CV of 1.13% for higher-concentration total bilirubin and an r of 0.984 against comparator systems, which supports deployment in large tertiary settings. The bilirubin blood test market is also seeing longer-term hardware pressure from low-cost wearable TcB development, which could expand neonatal screening access while narrowing the pricing advantage of incumbent device makers.

By Technology: POC Blood Testing Disrupts the Lab-Dominant Paradigm

Laboratory-based testing held 84.62% of the bilirubin blood test market share in 2025. This lead reflects the preference of hospitals for high-throughput chemistry systems that provide standardized bilirubin reporting across broad test menus. Siemens Healthineers reported that Atellica Solution can deliver up to 1,800 tests per hour with STAT bilirubin turnaround in under 10 minutes, which shows why large laboratories still anchor most clinical volume. Even so, point-of-care blood testing is the fastest-growing technology at 8.54%, which reflects expanding use in NICUs, community care, and resource-limited hospitals where transport delays can affect care timing.

Transcutaneous screening systems form the third technology layer in the bilirubin blood test market, but their role remains upstream rather than fully substitutive. A January 2026 Journal of Perinatology study confirmed good correlation between transcutaneous and serum bilirubin, but it also showed that the methods are not interchangeable at treatment thresholds and during phototherapy. Another 2025 study reported that more than 50% of neonates who qualified for hospital admission could be missed if transcutaneous readings were used without serum confirmation. That pattern keeps laboratory and point-of-care serum testing active even as noninvasive screening expands, which is why the bilirubin blood test industry still depends on confirmatory blood-based workflows.

By Application: Neonatal Segment's Outperformance Driven by Protocol Intensity

Liver function assessment held the largest share at 52.71% in 2025 within the bilirubin blood test market. This segment draws volume from chronic liver disease screening, pre-operative chemistry panels, drug safety monitoring, and MASLD staging. Bilirubin remains embedded in fibrosis scoring tools and noninvasive liver assessment algorithms, which keeps testing demand linked to broader hepatology workups rather than isolated bilirubin-specific orders. Neonatal jaundice screening and monitoring is the fastest-growing application at 9.67% through 2031 because universal screening, digital follow-up tools, and early referral pathways are making testing more systematic across the care pathway.

Hemolytic disorder assessment and routine health screening account for smaller shares, but both remain clinically relevant. In hemolytic disease, total and indirect bilirubin continue to function as accessible markers in sickle cell disease, G6PD deficiency, and hereditary spherocytosis follow-up. Routine pre-operative testing keeps bilirubin tied to surgical throughput because it is included in broader metabolic and hepatic chemistry orders. The bilirubin blood test industry, therefore, gains from both high-frequency neonatal use and steady adult panel testing, which helps balance risk across acute and chronic care settings.

By End User: Ambulatory Shift Reshapes Demand Distribution

Hospitals and NICUs held 44.81% share of the bilirubin blood test market size in 2025. They remain the largest end-user base because inpatient neonatal wards, core laboratories, hepatology units, and hematology services all generate repeat bilirubin testing. In the neonatal setting, transcutaneous ward screening followed by confirmatory serum analysis creates a dual-channel testing pattern that favors hospital-based workflows. Diagnostic laboratories remain the second-largest end-user group, and regional chemistry standardization programs such as Alberta’s Roche rollout support further concentration of testing volumes in organized laboratory networks.

Outpatient and ambulatory care centers are projected to grow at 8.85% through 2031 in the bilirubin blood test market. Their growth reflects earlier newborn discharge patterns and the need for follow-up bilirubin checks after the physiologic bilirubin peak shifts beyond the inpatient stay. Maternity and neonatal clinics also remain important, especially in Japan, where TcB screening is used 2 to 3 times daily in the first postnatal days under routine care protocols. The bilirubin blood test market is therefore seeing demand move outward from hospital laboratories into community-facing settings, even though central labs still control the largest installed testing base.

Geography Analysis

North America accounted for 48.21% share of the bilirubin blood test market size in 2025. The region leads because AAP newborn screening guidance is widely embedded in clinical practice and because Medicare reimbursement includes total and direct bilirubin within the hepatic function panel coding structure. The bilirubin blood test market in Canada is also supported by laboratory standardization programs, including Alberta’s 2025 Roche Cobas Pure implementation across regional hospitals. Europe remains a more heterogeneous setting because country-specific protocols coexist with broader NICE-style screening approaches and active IFCC standardization work. Universal screening has still kept testing volumes durable across the region, and pediatric research showed that extreme hyperbilirubinemia-related infant mortality in select European countries fell from 21.4 per million live births in 1990 to 4.2 per million in 2019.

Asia-Pacific is the fastest-growing geography in the bilirubin blood test market, with forecast CAGR of 8.45% through 2031. China is driving part of that expansion through active hospital procurement of neonatal transcutaneous bilirubinometers, including the September 2025 Longyan First Hospital tender for 3 units at RMB 13,000 each, equal to USD 1,790 per unit. India is expanding through point-of-care serum testing, and the 2025 Chennai validation of Bilistick System 2.0 showed clinically useful performance in a high-volume public hospital environment. Japan and Australia add another growth layer because routine TcB use in maternity care and updated universal screening guidance continue to support frequent neonatal bilirubin checks.

The bilirubin blood test market in the Middle East and Africa and in South America remains smaller in absolute size, but both regions carry targeted growth potential. GCC countries benefit from concentrated neonatal care infrastructure, while tertiary hospital networks in South Africa continue to support laboratory-based testing volume. Parts of Sub-Saharan Africa and the Middle East also face elevated bilirubin monitoring need because G6PD deficiency prevalence can range from 15% to 26% in male populations, which increases demand for hemolytic jaundice workups. Latin America remains important for liver-related testing because MASLD prevalence is highest globally in the region at 44.37%, which sustains bilirubin demand within routine hepatology panels.

Competitive Landscape

The bilirubin blood test market is moderately consolidated in high-throughput laboratory systems, where Roche, Siemens Healthineers, Abbott, and Beckman Coulter anchor institutional demand through chemistry platforms, service agreements, and bundled consumables. This installed-base advantage keeps competition centered on assay performance, workflow reliability, and long contract cycles rather than on rapid platform switching. The bilirubin blood test market is less concentrated in neonatal monitoring, where Konica Minolta and Dräger hold defensible positions in transcutaneous screening and bedside workflows. Dräger strengthened that position in March 2025 by launching BiliPredics, which linked predictive software to neonatal bilirubin monitoring and moved competition closer to decision-support-enabled care pathways. Roche also reinforced competitive depth through regional chemistry standardization programs such as Alberta’s 2025 implementation, which increased platform stickiness and recurring reagent pull-through.

Competitive pressure is rising at the edge of the bilirubin blood test market because lower-cost and more portable options are improving quickly. Japanese wearable TcB research showed that a prototype near USD 100 could achieve correlation coefficients of 0.856 to 0.871 against serum bilirubin, which points to future pricing pressure in entry-level screening devices. Smartphone-based screening also adds pressure because the Picterus system was validated across Mexico, Nepal, and the Philippines with better performance than visual assessment and low per-patient cost. QuidelOrtho also broadened its reach in 2026 through a strategic supply agreement with Lifotronic, which expanded menu depth for international immunoassay tenders that typically include routine chemistry testing around the same laboratory procurement cycle.

The bilirubin blood test market is also becoming more sensitive to traceability and comparability, which raises the competitive value of standardization. NIST and IFCC-aligned work has made cross-platform bias harder for laboratories to ignore, especially when one instrument change can alter treatment thresholds or phototherapy decisions. That is pushing procurement teams to weigh reference alignment and external quality performance more heavily when contracts are renewed. Smaller companies such as Reichert, Nova Biomedical, and Bilimetrix remain relevant in specific point-of-care niches, but the broader bilirubin blood test market still favors vendors that combine instrumentation, consumables, service, and compliance support in a single account relationship.

Bilirubin Blood Test Industry Leaders

Abbott Laboratories

F. Hoffmann-La Roche Ltd

Koninklijke Philips N.V.

Siemens Healthineers AG

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: NSW Health (Australia) published an updated Neonatal Jaundice and Hyperbilirubinaemia Identification and Management guideline mandating universal transcutaneous bilirubin screening, extending the protocol to gestations as low as 32 weeks and replacing the previous 2016 guideline; this represents a significant expansion of structured bilirubin screening in Australasia.

- October 2025: Alberta Precision Laboratories (Canada) implemented Roche Cobas Pure chemistry analyzers at regional hospitals as part of a provincial standardization program, replacing legacy platforms and modifying bilirubin reporting limits; the initiative reflects growing regional consolidation of chemistry testing volumes around single-vendor platforms.

- March 2025: Drägerwerk AG & Co. KGaA launched BiliPredics, a CE-certified and FDA-registered predictive bilirubin software developed in partnership with NeoPredics, integrating a pharmacometrics algorithm trained on over 50,000 measurements from approximately 10,000 newborns and capable of forecasting individual bilirubin progression up to 60 hours ahead with EHR integration and 2022 AAP guideline alignment.

Global Bilirubin Blood Test Market Report Scope

A bilirubin blood test measures the amount of bilirubin—a yellow pigment produced when red blood cells break down—in your bloodstream. It is primarily used to evaluate liver function, diagnose conditions like jaundice, hepatitis, and bile duct disorders, and monitor neonatal health.

The Bilirubin Blood Test Market is segmented across several dimensions that highlight its clinical and technological diversity. By test type, it includes total bilirubin tests, direct bilirubin tests, and indirect bilirubin tests. In terms of product type, the market covers reagents and assay consumables, calibrators and quality controls, and bilirubin analyzers and meters. The technology segment spans laboratory-based testing, point-of-care blood testing, and transcutaneous screening systems. By application, bilirubin testing is used for neonatal jaundice screening, liver function assessment, hemolytic disorder assessment, and routine health screening. The end users include hospitals and NICUs, diagnostic laboratories, maternity and neonatal clinics, and outpatient and ambulatory care centers. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, Middle East and Africa, and South America. Forecasts are provided in terms of market value (USD), reflecting the expected financial trajectory of this diagnostic segment.

| Total Bilirubin Tests |

| Direct Bilirubin Tests |

| Indirect Bilirubin Tests |

| Reagents and Assay Consumables |

| Calibrators and Quality Controls |

| Bilirubin Analyzers and Meters |

| Laboratory-Based Testing |

| Point-of-Care Blood Testing |

| Transcutaneous Screening Systems |

| Neonatal Jaundice Screening and Monitoring |

| Liver Function Assessment |

| Hemolytic Disorder Assessment |

| Pre-operative and Routine Health Screening |

| Hospitals and NICUs |

| Diagnostic Laboratories |

| Maternity and Neonatal Clinics |

| Outpatient and Ambulatory Care Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Total Bilirubin Tests | |

| Direct Bilirubin Tests | ||

| Indirect Bilirubin Tests | ||

| By Product Type | Reagents and Assay Consumables | |

| Calibrators and Quality Controls | ||

| Bilirubin Analyzers and Meters | ||

| By Technology | Laboratory-Based Testing | |

| Point-of-Care Blood Testing | ||

| Transcutaneous Screening Systems | ||

| By Application | Neonatal Jaundice Screening and Monitoring | |

| Liver Function Assessment | ||

| Hemolytic Disorder Assessment | ||

| Pre-operative and Routine Health Screening | ||

| By End User | Hospitals and NICUs | |

| Diagnostic Laboratories | ||

| Maternity and Neonatal Clinics | ||

| Outpatient and Ambulatory Care Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving demand for bilirubin blood testing through 2031?

The main demand drivers are universal newborn screening, rising liver disease testing, and wider use of point-of-care and outpatient follow-up pathways. The sector is projected to grow from USD 1.50 billion in 2026 to USD 2.02 billion by 2031 at 6.2% CAGR.

Which region leads current revenue generation?

North America leads with 48.21% share in 2025 because of established neonatal screening protocols, broad hospital automation, and reimbursement support.

Which application is growing the fastest?

Neonatal jaundice screening and monitoring is the fastest-growing application, with forecast CAGR of 9.67% through 2031, supported by universal screening and digital follow-up tools.

Why do laboratory platforms still dominate if point-of-care testing is rising?

Laboratory-based testing held 84.62% share in 2025 because hospitals still need standardized, auditable serum results, especially when clinical thresholds require confirmation.

Which product category generates the most recurring revenue?

Reagents and assay consumables hold the largest product share at 63.23% in 2025 because reagent-rental contracts keep recurring sales tied to installed chemistry platforms.

Page last updated on: