Hemoglobin Testing Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.28 Billion |

| Market Size (2031) | USD 5.91 Billion |

| Growth Rate (2026 - 2031) | 6.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hemoglobin Testing Devices Market Analysis by Mordor Intelligence

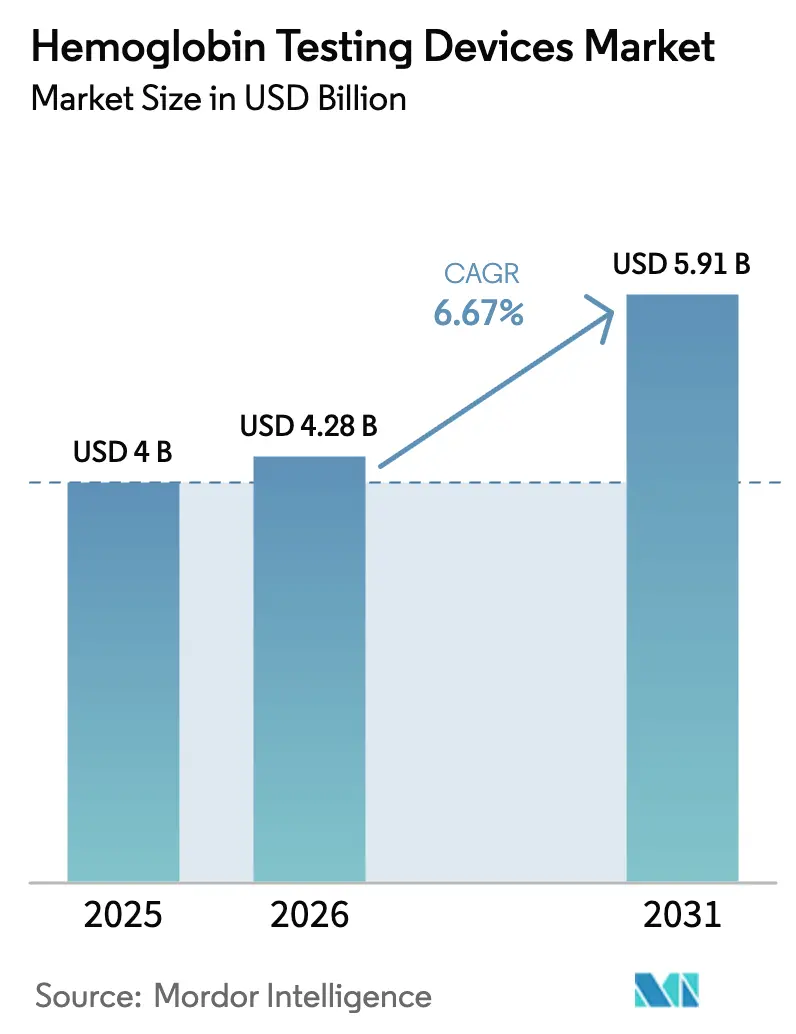

The Hemoglobin Testing Devices Market size was valued at USD 4 billion in 2025 and is estimated to grow from USD 4.28 billion in 2026 to reach USD 5.91 billion by 2031, at a CAGR of 6.67% during the forecast period (2026-2031).

Hospital demand for rapid perioperative monitoring, large-scale anemia screening mandates in low- and middle-income countries, and an installed-base replacement cycle in high-income laboratories are driving value growth even as average selling prices edge lower. Policy emphasis on maternal and child health, tighter blood-donation standards, and the aging population with chronic kidney disease and heart failure are expanding the daily test volume base of the Hemoglobin testing devices market. Continuous innovation in reagent-saving photometric analyzers, middleware-enabled data integration, and CLIA-waived handheld platforms is accelerating the migration of tests from core labs to near-patient settings, yet accuracy concerns for noninvasive optical monitors temper the overall growth trajectory. Competitive strategies now revolve around reagent economy, throughput optimization, and ecosystem partnerships that lock in consumable revenue streams across the device life cycle.

Key Report Takeaways

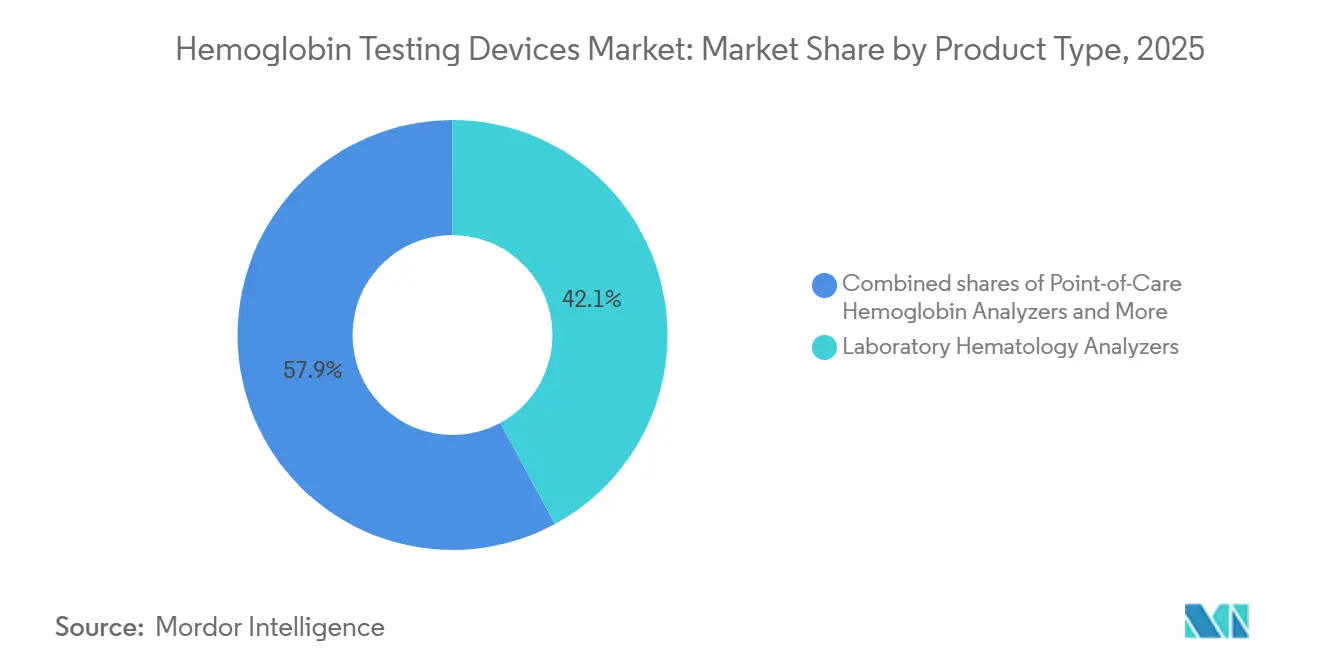

- By product type, laboratory hematology analyzers led with 42.09% of the Hemoglobin testing devices market share in 2025. Point-of-care hemoglobin analyzers are advancing at 7.78% CAGR through 2031.

- By technology, photometric or spectrophotometric instruments commanded a 45.67% share of the hemoglobin testing devices market in 2025, and near-infrared/pulse CO-oximetry will grow at a 8.62% CAGR through 2031.

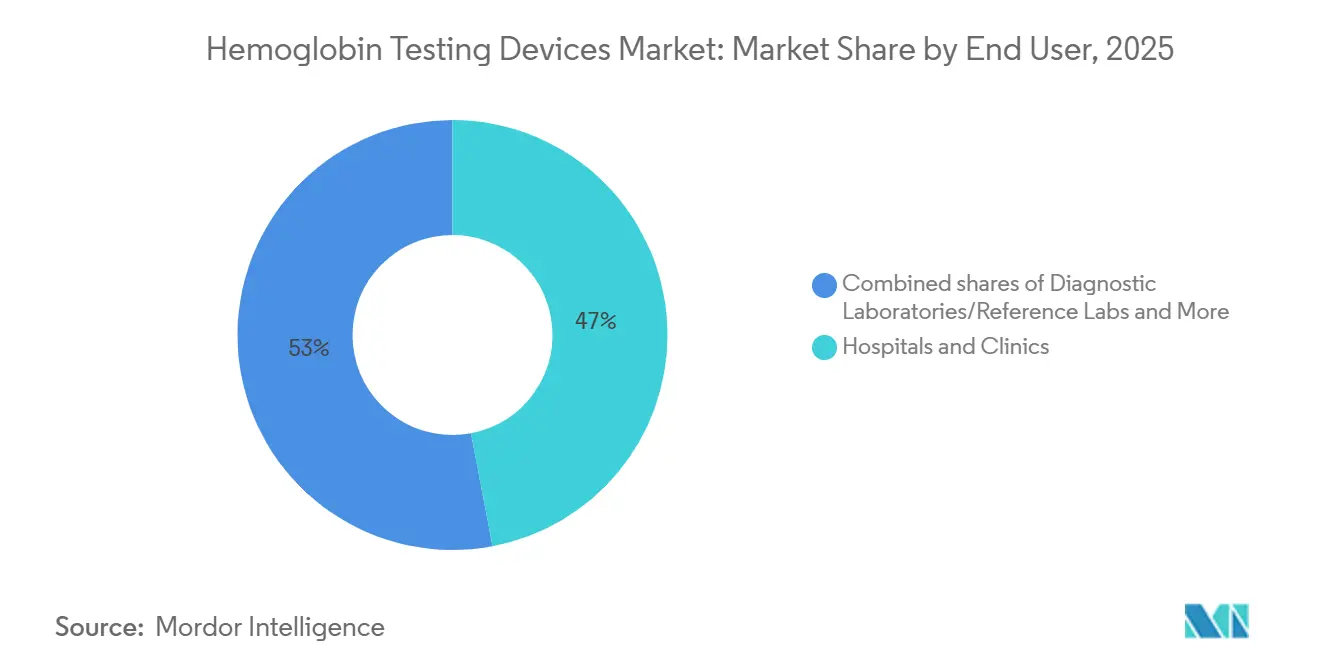

- By end users, hospitals and clinics accounted for 47.03% revenue share in 2025, while home care & community health programs are set to post the highest 9.45% CAGR through 2031 within the hemoglobin testing devices market.

- By application, anemia screening and diagnosis accounted for 40.12% of the hemoglobin testing devices market in 2025 and is projected to be the fastest-expanding application, with a 8.31% CAGR to 2031.

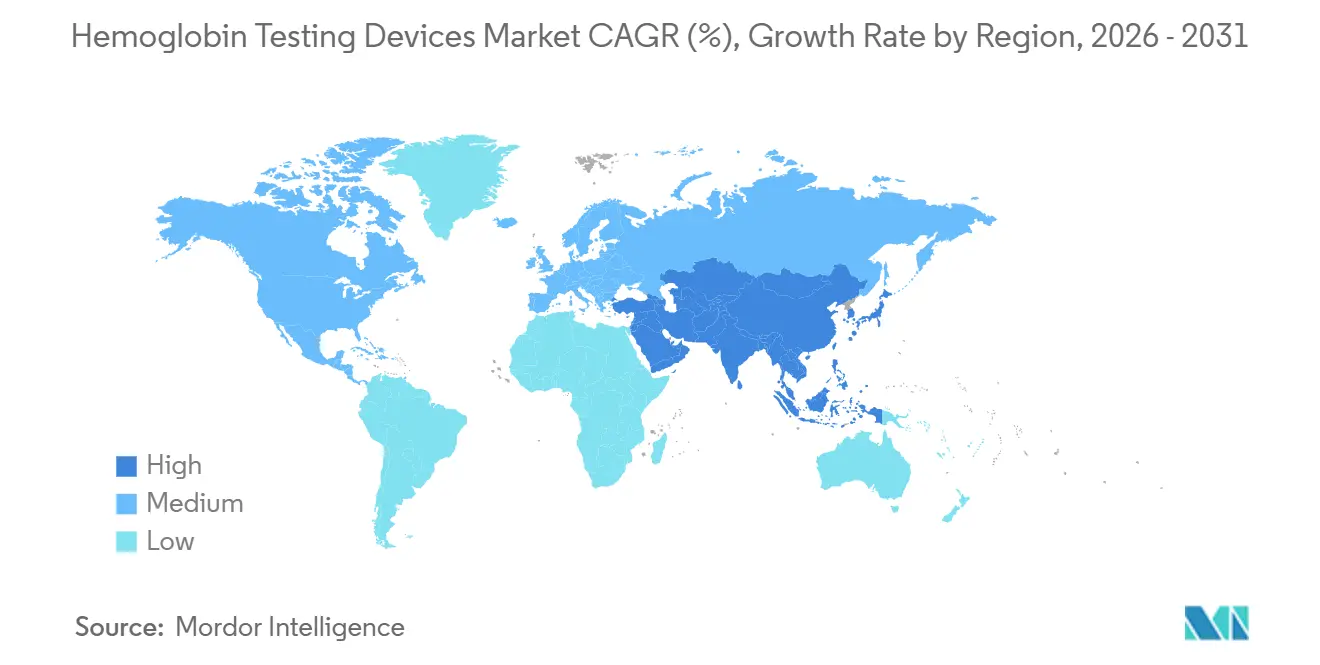

- By geography, North America held 49.54% of the Hemoglobin testing devices market share in 2025, yet Asia-Pacific will deliver the strongest regional CAGR at 8.51% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hemoglobin Testing Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High and rising anemia burden across LMICs and aging populations | +1.8% | Global, peak in South Asia, Sub-Saharan Africa, aging OECD | Long term (≥ 4 years) |

| Shift toward point-of-care hemoglobin testing for rapid decisions | +1.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Strong installed base and replacement cycle of hematology analyzers | +1.2% | North America, Europe, Japan, China, India | Medium term (2-4 years) |

| Public-health screening and blood-donation programs mandate Hb testing | +1.0% | Global, highest in India, Brazil, Mexico, Sub-Saharan Africa | Long term (≥ 4 years) |

| Perioperative blood management programs adopting continuous SpHb | +0.7% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| CLIA-waived Hb analyzers enabling new sites | +0.5% | United States, early in Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High And Rising Anemia Burden Across LMICs And Aging Populations

More than 1.9 billion individuals, or 24% of the world’s population, were anemic in 2024, with prevalence exceeding 40% in children under five and women of reproductive age in South Asia and Sub-Saharan Africa [1]Pan American Health Organization, “Guideline on haemoglobin cutoffs to define anaemia,” paho.org. India’s National Family Health Survey-5 data still show anemia in 57% of women and 67% of children, highlighting a vast underserved diagnostic need. In Latin America, the mean hemoglobin level among Mexican women declined amid cuts to nutrition programs, sustaining community-level demand for screening. Simultaneously, an aging OECD cohort grapples with renal and cardiac comorbidities that require frequent hemoglobin checks, cementing dual-track growth for the Hemoglobin testing devices market.

Shift Toward Point-Of-Care Hemoglobin Testing For Rapid Decisions

Emergency departments, operating suites, and mobile donor stations increasingly require sub-5-minute hemoglobin turnaround. The AABB standards, effective April 2026, mandate quantitative testing for all double-RBC collections, accelerating uptake of handheld analyzers over legacy copper-sulfate baths. Siemens Healthineers’ epoc system delivers wireless results in under 1 minute from 92 µL of whole blood, easing workflow congestion [2]Siemens Healthineers, “epoc Blood Analysis System,” siemens-healthineers.com. FDA guidance in 2024 on skin-tone bias in optical sensing is pushing vendors to validate their devices across diverse populations, improving trust in CLIA-waived platforms and widening the market for hemoglobin testing devices.

Strong Installed Base And Replacement Cycle Of Hematology Analyzers

Sysmex controls a significant share of the global analyzer footprint, locking laboratories into cyclical upgrades as instruments reach their 10-year service ceiling. HORIBA’s Yumizen H2500, cleared in 2024, uses only six reagents, offering operating-cost relief that entices mid-volume labs. Siemens Healthineers added the Atellica HEMA 570/580 in 2025, signaling intensified competition around throughput and reagent economy, further stimulating the Hemoglobin testing devices market.

Public Health Screening And Blood Donation Programs Mandate Hb Testing

The WHO now recommends hemoglobin measurement at the first antenatal visit and at 26 weeks, representing roughly 140 million tests a year for the estimated global pregnancies. Brazil requires CBC at 12 months for every infant, with retesting 30-45 days after iron therapy, doubling consumable use in pediatric clinics. Blood banks worldwide are upgrading to automated screening systems as the Hemoglobin testing devices market benefits from mandatory quantitative thresholds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accuracy/bias concerns for noninvasive Hb at low Hb and varied skin tones | -0.9% | Global, with heightened scrutiny in North America and Europe post-FDA guidance | Short term (≤ 2 years) |

| Budget and reimbursement pressures limiting analyzer upgrades in mature markets | -0.7% | North America, Western Europe, Japan | Medium term (2-4 years) |

| Microcuvette/consumable costs and supply constraints depress POC utilization | -0.5% | Global, with acute impact in LMICs and resource-constrained health systems | Medium term (2-4 years) |

| Data integration/middleware gaps hinder scaling across decentralized sites | -0.4% | Global, most pronounced in United States, Canada, and fragmented European health systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accuracy And Bias Concerns For Noninvasive Hb At Low Hb And Varied Skin Tones

Multiple studies show Masimo SpHb can miss transfusion triggers when true hemoglobin is below 10 g/dL, while darker skin reduces optical signal quality, leading the FDA to tighten validation guidance in 2024 [3]U.S. Food and Drug Administration, “Pulse Oximeter Guidance,” fda.gov. Ugandan field data also reported capillary bias in several handheld devices, complicating anemia screening in resource-poor settings. The perception gap constrains near-term uptake of noninvasive monitors in the Hemoglobin testing devices market.

Budget And Reimbursement Pressures Limiting Analyzer Upgrades In Mature Markets

CMS cut the 2025 Clinical Laboratory Fee Schedule by 1.3%, squeezing U.S. labs and postponing planned analyzer replacements. Japanese fee reductions similarly stretch equipment lifespans to 15 years. Vendors address this by bundling middleware and reagent contracts, yet overall capital outlay remains slow, damping growth in the hemoglobin testing devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: POC Invasive Analyzers Outpace Laboratory Segment

Point-of-care invasive analyzers are set to post a 7.78% CAGR through 2031, the fastest clip among all product groups, as recent CLIA-waived clearances allow them into pharmacies, WIC clinics, dialysis units, and ambulatory surgical centers that lack full laboratory infrastructure. Portable benchtop units sit in dialysis suites and same-day surgery rooms, where staff need quantitative results before discharge or erythropoiesis-stimulating-agent dosing. The AABB’s 35th edition standards, effective April 2026, mandate such readings for every double red-cell collection and are phasing out copper-sulfate drop tests in blood centers.

Laboratory hematology analyzers still held 42.09% of the Hemoglobin testing devices market share in 2025, buoyed by Sysmex’s large global installed base and a gradual migration from 3-part to 5-part differentials that add parameters such as immature granulocytes and reticulocyte hemoglobin content. Sysmex’s FDA-cleared XR-Series and HORIBA’s IVDR-certified Yumizen H500 CRP layer advanced analytics onto familiar photometric engines, helping laboratories justify upgrades even as budget ceilings lengthen equipment life cycles to 10-15 years.

By Technology: Noninvasive Pulse CO-Oximetry Surges Despite Accuracy Scrutiny

Photometric or spectrophotometric instruments controlled 45.67% of the Hemoglobin testing devices market share in 2025, a position cemented by low reagent expense and the International Council for Standardization in Hematology’s endorsement of the cyanmethemoglobin reference method. HORIBA’s six-reagent Yumizen H2500 demonstrates how cost trimming keeps this technology attractive for mid-volume hospitals. Independent work from Chile confirmed that such analyzers deliver reliable red-cell indices for β-thalassemia screening when paired with confirmatory HbA2 tests, reinforcing their frontline diagnostic role.

The sharpest growth line, however, belongs to noninvasive pulse CO-oximetry, projected at an 8.62% CAGR through 2031, even though multiple studies show the technology can overestimate by up to 2 g/dL when true values fall below 10 g/dL. Perioperative guidelines from ESAIC and EACTS/EACTAIC endorse continuous hemoglobin trending to fine-tune transfusion triggers, a recommendation that is placing Masimo’s SpHb sensors into new cardiac and orthopedic theaters across Europe and North America.

By End User: Hospitals Dominate Yet Decentralization Accelerates

Hospitals and clinics contributed 47.03% of 2025 revenue, sustaining a 9.45% CAGR, as complex surgeries and sepsis pathways increase test frequency. Diagnostic reference labs consolidate outreach work, leveraging 120-test-per-hour analyzers to lower test costs. Blood banks, spurred by the AABB standard, are switching to handheld quantitative screens, boosting the Hemoglobin testing devices market for donation workflows. Ambulatory surgical centers and dialysis chains adopt CLIA-waived devices to satisfy same-day discharge and ESA dose-adjustment protocols, diffusing equipment placement across thousands of non-acute sites.

By Application: Anemia Screening Leads, Perioperative Monitoring Fastest

Anemia screening and diagnosis accounted for 40.12% of the market in 2025, and is expected to advance at 8.31% CAGR as India, Brazil, and Sub-Saharan Africa continue mass programs. The Hemoglobin testing devices market size for perioperative and critical-care monitoring, however, is poised for the sharpest climb, bolstered by guideline-driven transfusion management that values real-time data. Dialysis anemia management holds steady with chronic 10-11.5 g/dL targets, while donor screening adds recurring handheld test volume throughout the forecast window.

Geography Analysis

North America commanded 49.54% of the Hemoglobin testing devices market share in 2025, supported by a dense installed base of laboratory analyzers and early adoption of CLIA-waived handheld platforms. The region’s hospitals are embedding perioperative blood-management protocols that require near-real-time hemoglobin values, while retail pharmacies and WIC clinics widen device placement beyond acute-care environments. Despite a 1.3% cut to the 2025 Clinical Laboratory Fee Schedule, U.S. laboratories continue to upgrade middleware so that older analyzers can feed electronic medical records, lengthening hardware lifecycles but sustaining reagent demand. Canada mirrors this pattern, with provincial health authorities approving CLIA-waived analyzers for community dialysis centers, creating a parallel distribution channel that sidesteps hospital procurement committees.

Asia-Pacific is projected to post the fastest CAGR of 8.31% through 2031, reflecting large-scale public health screening in India, China, and Indonesia. India’s Anemia Mukt Bharat initiative has already deployed digital hemoglobinometers at the village level, yet the National Family Health Survey-5 still shows anemia in the majority of women and children, underscoring unmet diagnostic needs. China is adding dual testing for neonatal G6PD and hemoglobin on Mindray BS-2800M platforms, accelerating deployment in county hospitals and maternal-child centers. While Japan faces fee pressures that extend analyzer lifespans to 15 years, reagent-saving models from local suppliers are still entering secondary hospitals, cushioning revenue erosion. Collectively, these trends will lift the Asia-Pacific Hemoglobin testing devices market size to rival Europe before the end of the forecast period.

Europe held the second-largest regional position in 2025, driven by perioperative guidelines that mandate real-time hemoglobin monitoring in Germany, France, and the United Kingdom. CE IVDR requirements are prompting analyzer software retrofits and new placements, exemplified by HORIBA’s Yumizen H500 CRP certification that targets small laboratories seeking combined CBC + CRP workflows. In the Middle East and Africa, anemia prevalence above 40% among women of reproductive age is catalyzing procurement of ruggedized point-of-care devices for rural clinics. South America is expanding infant CBC mandates, with Brazil requiring confirmatory hemoglobin tests 30-45 days after iron therapy, generating repeat consumable revenue. Taken together, these developments sustain global geographic momentum even as mature markets focus on middleware upgrades over new hardware, ensuring balanced growth for the Hemoglobin testing devices market.

Competitive Landscape

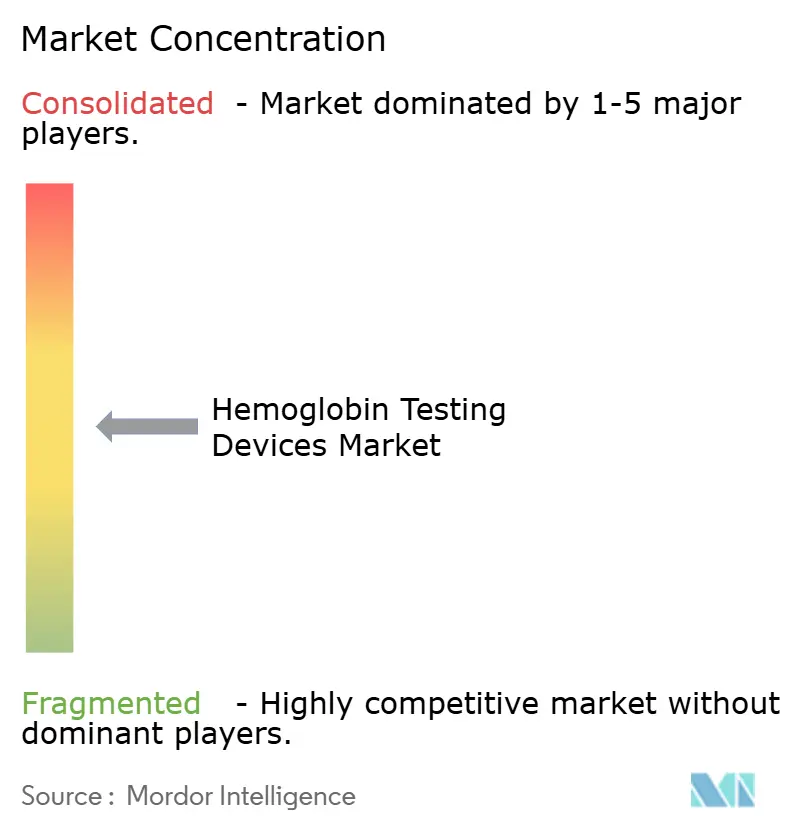

The Hemoglobin testing devices market is moderately concentrated. The top five suppliers control the majority of laboratory analyzer placements yet hold far less sway over handheld and optical segments. Sysmex defends its installed base through middleware alliances with Roche, while HORIBA and Siemens Healthineers court mid-volume accounts with reagent-saving designs. Abbott and Erba Mannheim target space-constrained satellite labs with compact instruments. Masimo’s SpHb faces validation headwinds that allow invasive co-oximetry vendors to claim leadership in accuracy. Overall, technology differentiation now hinges on total cost of ownership, data integration, and regulatory agility as CE-IVDR and FDA bias guidance reshape product road maps.

Hemoglobin Testing Devices Industry Leaders

Abbott Diagnostics

Siemens Healthineers

F.Hoffman La Roche

Sysmex Corporation

HORIBA Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Hemanext One System received FDA clearance, automating donor hemoglobin screening and component preparation.

- March 2026: Mindray’s BS-2800M G6PD/Hb assay gained Chinese validation for combined neonatal G6PD and hemoglobin testing.

Global Hemoglobin Testing Devices Market Report Scope

As per the scope of the report, hemoglobin testing devices, or hemoglobinometers, are specialized medical instruments used to measure the concentration of hemoglobin in blood. These devices range from large-scale Automated Hematology Analyzers (AHAs) used in clinical laboratories to portable, digital point-of-care (POC) systems designed for rapid results in field settings or home monitoring.

The hemoglobin testing devices market is segmented by product type, technology, end users, application, and geography. Based on product type, the market is segmented into laboratory hematology analyzers (3-part differential analyzers, 5-part and advanced differential analyzers), point-of-care hemoglobin analyzers (handheld analyzers and portable/benchtop analyzers), and noninvasive hemoglobin monitors (spot-check monitors and continuous multi-parameter monitors). By technology, the market is segmented into Photometric/Spectrophotometric, Co-oximetry, and Near-infrared/Pulse CO-oximetry. By end users, the market is segmented into hospitals & clinics, diagnostic laboratories/reference labs, blood banks & plasma centers, ambulatory surgical centers, home care & community health programs, and dialysis/nephrology centers. By application, the market is divided into anemia screening & diagnosis, maternal & child health screening, perioperative & critical care monitoring, dialysis/CKD anemia management, and other applications.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Laboratory Hematology Analyzers | 3-part differential analyzers |

| 5-part and advanced differential analyzers | |

| Point-of-Care Hemoglobin Analyzers (invasive) | Handheld analyzers |

| Portable/benchtop analyzers | |

| Noninvasive Hemoglobin Monitors (pulse CO-oximetry) | Spot-check monitors |

| Continuous multi-parameter monitors |

| Photometric/Spectrophotometric (azidemethemoglobin/HiCN) |

| Co-oximetry (invasive blood gas analyzers) |

| Near-infrared/Pulse CO-oximetry (noninvasive SpHb) |

| Hospitals & Clinics |

| Diagnostic Laboratories/Reference Labs |

| Blood Banks & Plasma Centers |

| Ambulatory Surgical Centers |

| Home Care & Community Health Programs |

| Dialysis/Nephrology Centers |

| Anemia Screening & Diagnosis |

| Maternal & Child Health Screening |

| Perioperative & Critical Care Monitoring |

| Dialysis/CKD Anemia Management |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Laboratory Hematology Analyzers | 3-part differential analyzers |

| 5-part and advanced differential analyzers | ||

| Point-of-Care Hemoglobin Analyzers (invasive) | Handheld analyzers | |

| Portable/benchtop analyzers | ||

| Noninvasive Hemoglobin Monitors (pulse CO-oximetry) | Spot-check monitors | |

| Continuous multi-parameter monitors | ||

| By Technology | Photometric/Spectrophotometric (azidemethemoglobin/HiCN) | |

| Co-oximetry (invasive blood gas analyzers) | ||

| Near-infrared/Pulse CO-oximetry (noninvasive SpHb) | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Laboratories/Reference Labs | ||

| Blood Banks & Plasma Centers | ||

| Ambulatory Surgical Centers | ||

| Home Care & Community Health Programs | ||

| Dialysis/Nephrology Centers | ||

| By Application | Anemia Screening & Diagnosis | |

| Maternal & Child Health Screening | ||

| Perioperative & Critical Care Monitoring | ||

| Dialysis/CKD Anemia Management | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the Hemoglobin testing devices market be by 2031?

It is forecast to reach USD 5.91 billion, growing at a 6.67% CAGR from 2026 to 2031.

Which segment leads revenue within Hemoglobin testing devices?

Laboratory hematology analyzers held 42.09% share in 2025 and remain the largest revenue contributor.

Why is Asia-Pacific the fastest-growing region?

Government-funded anemia screening, rapid lab construction, and chronic kidney disease prevalence boost an 8.51% CAGR in the region.

What technology dominates current installations?

Photometric or spectrophotometric methods account for 45.67% of 2025 revenue due to low reagent cost and established standards.

Page last updated on: