Bilirubin Meters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

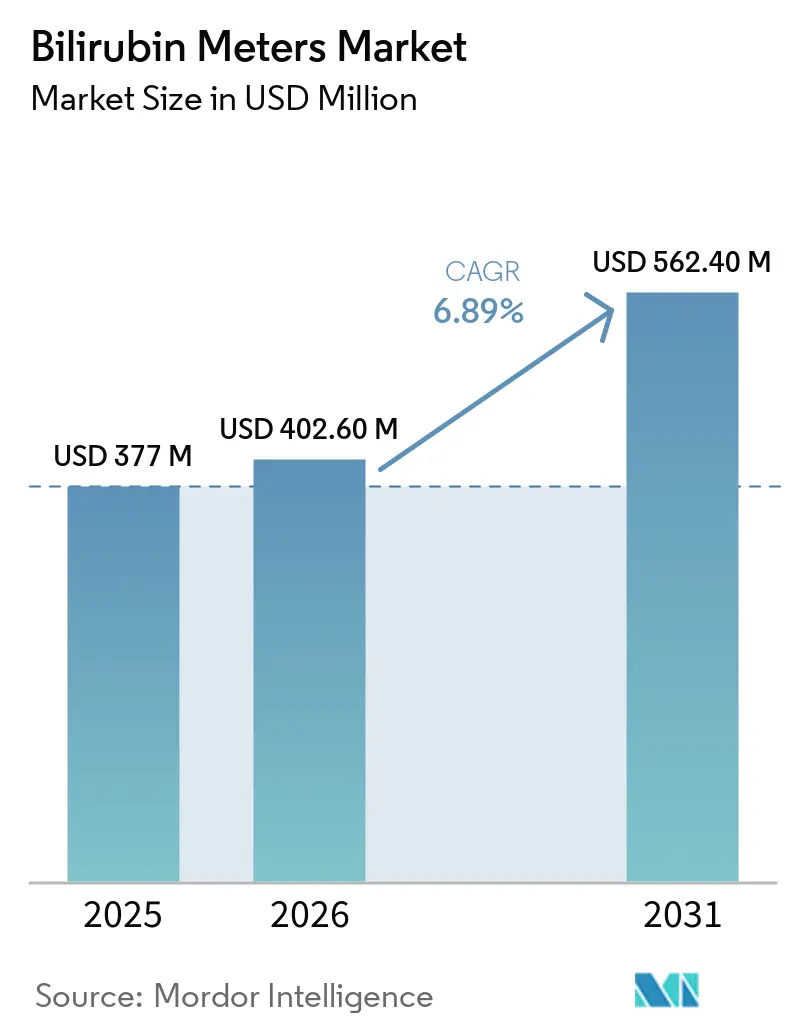

| Market Size (2026) | USD 402.60 Million |

| Market Size (2031) | USD 562.40 Million |

| Growth Rate (2026 - 2031) | 6.89% CAGR |

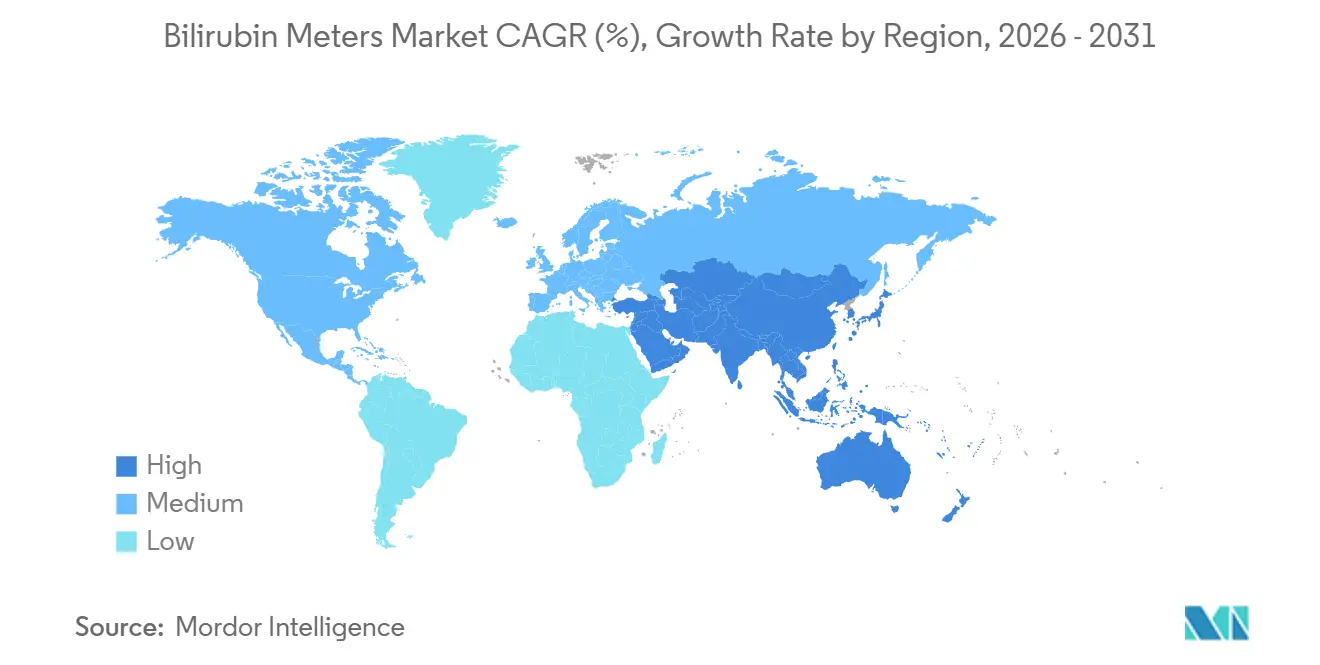

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bilirubin Meters Market Analysis by Mordor Intelligence

The Bilirubin Meters Market size is expected to increase from USD 377 million in 2025 to USD 402.60 million in 2026 and reach USD 562.40 million by 2031, growing at a CAGR of 6.89% over 2026-2031.

This growth path reflects compulsory predischarge screening guidelines in high-income countries, an annual increment of 18 million live births across Asia-Pacific, and sensor algorithms that have narrowed the accuracy gap between transcutaneous and serum assays. Hospitals in the United States and Canada already treat bilirubin measurement as a default newborn vital sign, while India’s Mission ANMOL bundles the test into a 56-parameter screen delivered to 250,000 babies per year[1]Government of India, “Mission ANMOL,” India.gov.in. Vendor competition is intensifying as platform giants such as Drägerwerk and Philips defend their share against point-of-care specialists offering smartphone-based optics validated in peer-reviewed trials. Reimbursement variability, however, continues to dampen adoption in South Asia and Sub-Saharan Africa, where a single transcutaneous reading can cost more than daily household income.

Key Report Takeaways

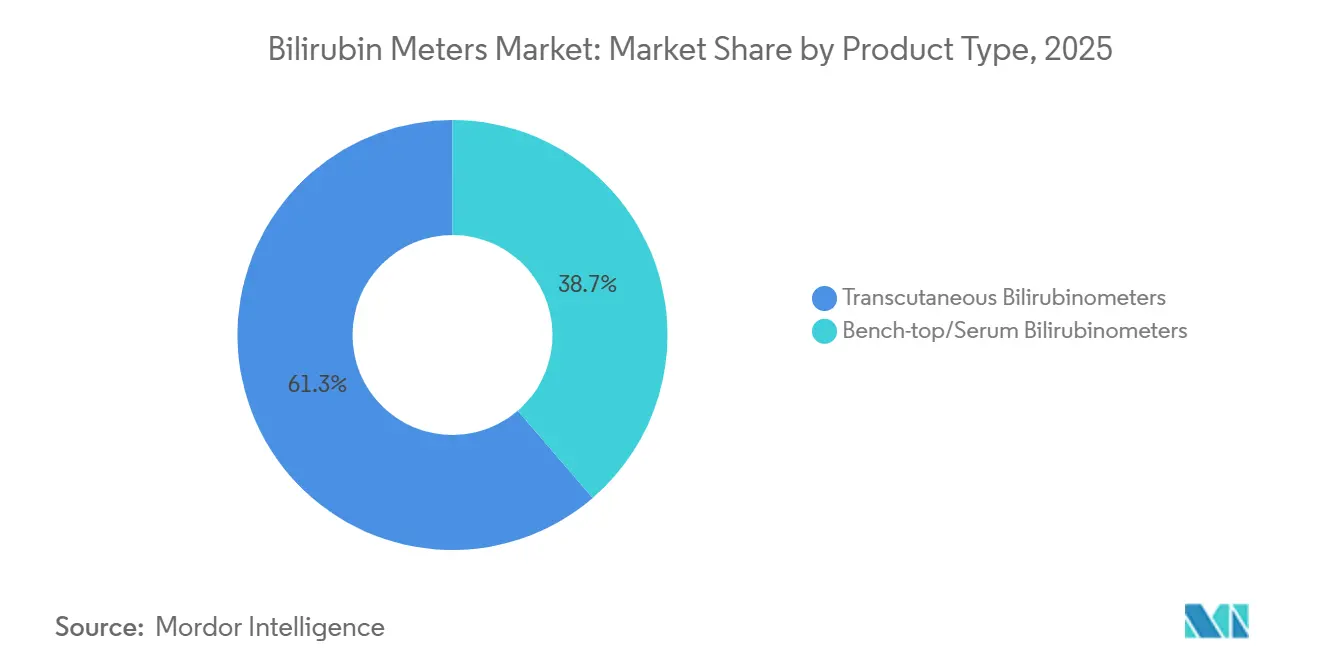

- By product type, transcutaneous devices led with 61.30% of the bilirubin meters market share in 2025, while bench-top serum analyzers are projected to post the quickest 8.36% CAGR through 2031.

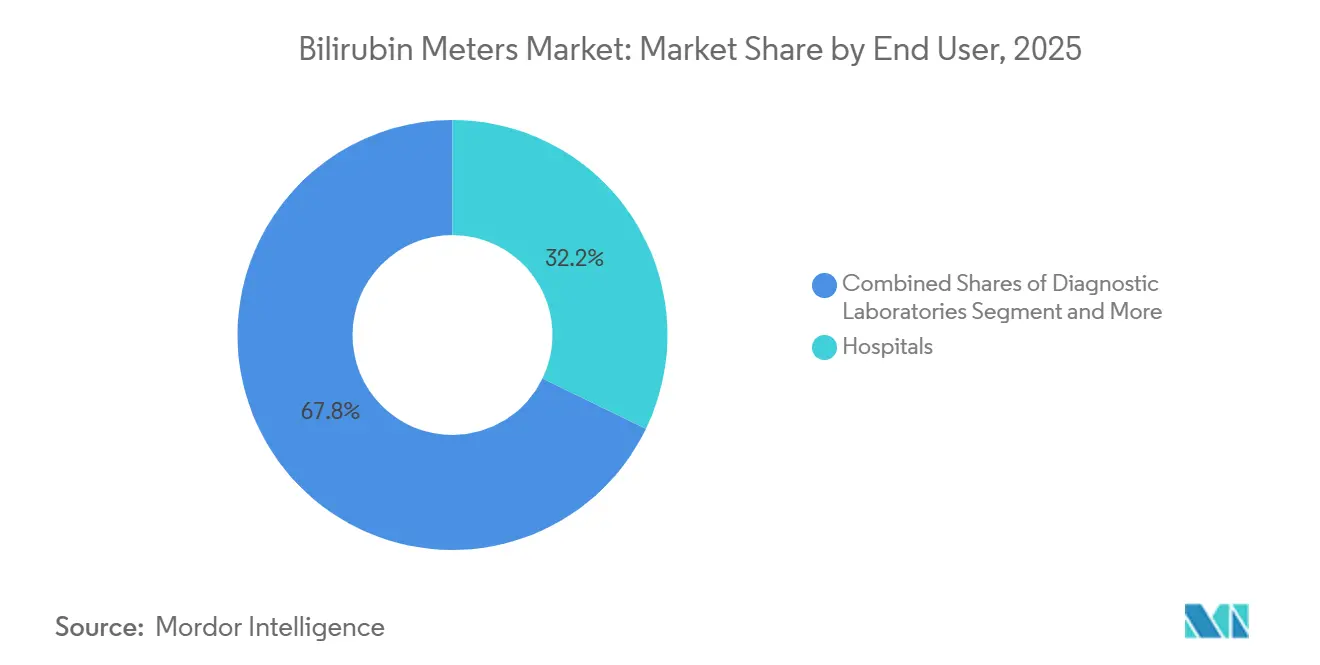

- By end user, hospitals captured 32.18% of 2025 revenue; neonatal clinics and birth centers are forecast to expand at 8.56% CAGR, the fastest pace in the segment.

- By application, screening accounted for 63.98% of the bilirubin meters market size in 2025 and is advancing at an 8.74% CAGR through 2031.

- By geography, North America dominated with 37.18% share in 2025, whereas Asia-Pacific is on track for the highest 7.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bilirubin Meters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High neonatal jaundice prevalence; universal predischarge screening momentum | +1.8% | Global, with the strongest uptake in North America, Western Europe, and urban APAC | Medium term (2-4 years) |

| Shift to non-invasive TcB screening reduces blood draws and readmissions | +1.5% | North America, EU, Australia; pilot programs in India, Brazil | Short term (≤ 2 years) |

| APAC birth volumes and neonatal capacity expansion raise device demand | +1.3% | APAC core (China, India, Indonesia), spill-over to Middle East & Africa | Long term (≥ 4 years) |

| EHR/HIS connectivity and workflow automation drive hospital procurement | +1.0% | North America, Northern Europe, select APAC metros (Singapore, Seoul) | Medium term (2-4 years) |

| Algorithmic/sensor advances (multi-wavelength, AI) improve accuracy | +0.7% | Global R&D hubs; clinical validation in North America, EU, Japan | Long term (≥ 4 years) |

| Remote/community TcB programs for post-discharge monitoring | +0.5% | North America, Scandinavia, pilot zones in India (Delhi, Karnataka) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Neonatal Jaundice Prevalence and Universal Predischarge Screening Momentum

Six of every ten term newborns and eight of every ten preterm infants exhibit visible jaundice during the first week of life, prompting guideline bodies to press for routine testing across delivery wards. India’s Mission ANMOL shows how middle-income health systems can operationalize the mandate at scale by integrating bilirubin with 55 other newborn screens in a single visit. This regulatory alignment transforms discretionary testing into a standard-of-care expectation, driving multiyear budget allocations for capital devices and consumables. As screening becomes universal, vendors that can bundle equipment financing and staff training into turnkey contracts stand to gain.

Shift to Non-Invasive TcB Screening Reduces Blood Draws and Readmissions

A heel-stick serum draw averages eight minutes of staff time versus two minutes for a transcutaneous scan, creating an immediate 40% labor saving per screening episode [2]National Institute for Health and Care Excellence, “Jaundice in Newborn Babies,” Nice.org.uk. A 2024 JAMA Pediatrics cohort study tied universal TcB adoption to a 32% drop in jaundice-related readmissions within one year. Workflow efficiency is magnified in U.S. maternity wards processing up to 5,000 deliveries each year, where the switch frees nursing teams for lactation support and discharge education. Device makers have responded by embedding barcode scanners and HL7 FHIR data exchange so readings auto-populate the electronic health record and trigger alerts when phototherapy thresholds loom. Yet the necessity for serum confirmation near treatment cutoffs tempers the total addressable volume, keeping laboratory assays in play.

APAC Birth Volumes and Neonatal Capacity Expansion Raise Device Demand

Asia-Pacific registers roughly 18 million births a year, nearly half the global total, and national programs are investing to match neonatal capacity with demographic pressure. China’s 14th Five-Year Plan targets 2.4 NICU beds per 1,000 live births by 2027, implying 12,000 incremental beds that must be equipped with diagnostic instrumentation. India’s fiscal 2025-2026 budget allocates INR 3,200 crore (USD 385 million) for neonatal devices in districts where facility deliveries still lag. These structural expansions create predictable procurement cycles that favor vendors offering multi-year service coverage and localized technical support. Nonetheless, fewer than 30% of South Asian public hospitals hold earmarked funds for point-of-care diagnostics, forcing bilirubin meters to compete against ventilators and incubators in bundled tenders.

EHR/HIS Connectivity and Workflow Automation Drive Hospital Procurement

Seventy-eight percent of U.S. maternity hospitals required HL7 FHIR-compliant data exchange for neonatal diagnostics in 2025, making plug-and-play connectivity a deal-breaker for capital purchase committees. Drägerwerk’s JM-105 and Konica Minolta’s JM-103 push TcB values directly to patient charts, shortening documentation time by an average 18 minutes per shift in Kaiser Permanente trials. Decision-support logic then flags cases above age-specific nomograms, cutting median time-to-phototherapy by 4.2 hours and avoiding coding errors that lead to reimbursement denials. The same connectivity backbone supports remote midwife programs in Denmark and Norway, where Bluetooth-enabled devices transmit post-discharge readings for pediatrician triage. As hospital systems elevate interoperability in tender scoring, vendors without seamless HIS integration risk relegation to niche or developing-country opportunities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| TcB requires confirmatory TSB near thresholds; post-phototherapy limits | -0.9% | Global, particularly impactful in resource-constrained settings lacking laboratory access | Short term (≤ 2 years) |

| High upfront cost; patchy reimbursement in emerging markets | -0.7% | South Asia, Sub-Saharan Africa, Latin America (excluding Brazil, Argentina metros) | Medium term (2-4 years) |

| Divergent guidelines (NICE vs AAP) dampen universal screening adoption | -0.4% | United Kingdom, parts of Western Europe; limited impact in North America, APAC | Short term (≤ 2 years) |

| Substitution by multi-parameter blood-gas/chemistry analyzers in labs | -0.3% | North America, EU hospital laboratories consolidating point-of-care testing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

TcB Requires Confirmatory TSB Near Thresholds and Post-Phototherapy Limits

Optical bilirubinometry underestimates values above 15 mg/dL and becomes unreliable after phototherapy, when skin reflectance changes foil algorithms. NICE guidelines, therefore, impose serum confirmation whenever TcB readings fall within 3 mg/dL of treatment cutoffs. In Ghana, this double-testing pushed per-infant costs to USD 8.50, versus USD 3.20 for TcB-only workflows, eroding the economic case in public hospitals [3]The Lancet Global Health, “Cost-Effectiveness of Universal Bilirubin Screening,” Thelancet.com. Laboratories equipped with Radiometer ABL90 FLEX or Siemens RAPIDPoint 405 platforms already measure bilirubin alongside blood gases, enabling clinicians to bypass standalone devices in critical-care settings. Unless TcB vendors can lift post-phototherapy accuracy, serum assays will retain a foothold.

High Upfront Cost and Patchy Reimbursement in Emerging Markets

A transcutaneous meter priced at USD 5,000 equals six to ten months of a district hospital’s operating budget in Sub-Saharan Africa. Consumables add USD 1.50-3.00 per test, costs often transferred to families where daily income can be lower. Only 18% of surveyed public facilities in India, Kenya, and Nigeria had ring-fenced neonatal diagnostic budgets in 2025, forcing procurement managers to chase donor grants or opt for multi-parameter analyzers that stretch limited funds. Ethiopia’s 2024 filtered-sunlight phototherapy trial slashed severe hyperbilirubinemia by 60% without precision meters, underscoring the leapfrog risk for traditional vendors. Until pricing and reimbursement align, scale-up in low-resource geographies will lag demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Transcutaneous Dominance Meets Serum’s Precision Push

Transcutaneous devices captured 61.30% of 2025 revenue, validating hospital preference for non-invasive workflows that cut collection time by 75% and integrate smoothly with electronic records. The bilirubin meters market size for transcutaneous systems is projected to climb steadily as universal screening makes a device mandatory for every delivery ward. Bench-top serum analyzers, however, are forecast to post the brisker 8.36% CAGR through 2031, buoyed by laboratory consolidation onto multi-parameter blood-gas instruments that can process bilirubin alongside six other chemistries. Correlation coefficients between transcutaneous and serum values still range from 0.76 to 0.92, so one in three infants screened will need serum confirmation, safeguarding residual demand.

Clinicians weigh accuracy against workflow: Drägerwerk’s JM-105 embeds five-wavelength optics and barcode scanners that flag near-threshold values for confirmatory draws, while QuidelOrtho’s Vitros BuBc Slide delivers conjugated and unconjugated fractions vital for biliary atresia diagnosis. As algorithmic advances lift transcutaneous precision, remaining differentiation may hinge on consumable costs and calibration stability. Vendors that wrap disposable probe tips and cloud analytics into subscription bundles could lock accounts before AI-based smartphone apps disrupt the entry-level tier of the bilirubin meters market.

By Application: Screening Surges While Diagnosis Consolidates

Screening represented 63.98% of the 2025 volume, and its 8.74% CAGR makes it the prime engine of the bilirubin meters market. The AAP mandate and the WHO framework compel every live birth in high-income nations to undergo either transcutaneous or serum measurement, turning intermittent testing into a default clinical step. Targeted screening persists where reimbursement hurdles block universal rollout, but even here, national initiatives such as Mission ANMOL demonstrate scalable models that pair TcB meters with midwife tablets for rural outreach.

Diagnosis and therapeutic monitoring grow at a slower clip as laboratories fold bilirubin into existing blood-gas platforms. Radiometer’s ABL90 FLEX and Siemens RAPIDPoint 405 satisfy NICU needs within multi-parameter panels, reducing standalone analyzer appeal. Still, differential diagnosis of conjugated hyperbilirubinemia and post-phototherapy surveillance keeps a niche alive for rapid, highly-specific assays. Innovators that shorten serum turnaround to under five minutes or enable reliable post-phototherapy TcB readings could rekindle demand in the diagnostic tier of the bilirubin meters market.

By End User: Hospitals Anchor Volume, Clinics Drive Growth

Hospitals contributed 32.18% of 2025 revenue, anchored by delivery centers logging up to 5,000 births annually and valuing EHR-linked meters that collapse nurse documentation time. Their purchasing cycles favor vendors with 24/7 on-site service and multiyear consumable contracts. Neonatal clinics and birth centers, though smaller, are forecast to grow at 8.56%, the fastest rate among users, as insurers nudge low-risk deliveries to outpatient settings and Scandinavian midwife networks adopt cloud-connected TcB kits.

Diagnostic laboratories hold a smaller slice of the bilirubin meters market share but are buffered by consolidation trends that concentrate test menus onto fewer, high-throughput platforms. Home-care remains experimental; Denmark’s early-discharge pilot showed a 28% readmission cut, yet the FDA has not clarified regulatory status for consumer-operated TcB devices. Should over-the-counter clearance materialize, a rental-based distribution model could unlock latent demand among pediatricians eager to replace office visits with remote monitoring.

Geography Analysis

North America held 37.18% share in 2025, underpinned by 3.6 million annual U.S. births, comprehensive insurance coverage, and guideline alignment that embeds bilirubin measurement into every discharge checklist. Device penetration is now replacement-cycle driven; hospitals upgrade to Wi-Fi-enabled models or pursue consumable-saving alternatives. Canada mirrors this maturity, while Mexico’s uneven facility coverage leaves rural clinics reliant on visual assessment.

Asia-Pacific is the growth epicenter, projected at a 7.98% CAGR to 2031 as China and India scale NICU beds and national screening programs. Although the bilirubin meters market size in the region is smaller than North America’s today, sheer birth volumes and rising institutional deliveries create outsized upside. Reimbursement gaps persist; fewer than 30% of South Asian public hospitals have ring-fenced diagnostic budgets, but state schemes and philanthropic grants offer episodic boosts.

Europe trails in volume growth, restrained by NICE’s caution that discourages blanket TcB adoption. Germany and France retain targeted protocols, while Spain seeks EU funds to pilot universal screening in 2027. Middle East & Africa and South America suffer infrastructure deficits; only a few of Sub-Saharan public hospitals own a TcB meter. Brazil’s SUS reimburses screening in public maternity wards but not in private clinics, splitting the market. Novel low-cost interventions such as filtered-sunlight phototherapy could allow these regions to bypass traditional meters altogether.

Competitive Landscape

The bilirubin meters market displays moderate concentration: the top five manufacturers, Drägerwerk, Philips, Siemens Healthineers, Konica Minolta, and Radiometer, control a significant share of global revenue through hospital contracts. Transcutaneous leaders stake differentiation on multi-wavelength optics and HL7-compliant data streams, bundling disposable probe tips to lock in consumable revenue. Serum-analyzer suppliers defend laboratory territory by embedding bilirubin into multi-parameter chemistry panels, enabling one-sample workflows that cut reagent waste.

Portfolio expansion via acquisition is gathering pace. Natus Sensory’s February 2026 purchase of TheraB Medical adds an FDA-cleared wearable phototherapy device, positioning the buyer to package screening and treatment under a single purchase order. International Biomedical’s disposable-tip model shifts 40% of lifetime value into consumables, insulating hardware margins. Disruptors leverage AI and commodity cameras: a 2024 JAMA Pediatrics study achieved 0.85 correlation between smartphone images and serum bilirubin, foreshadowing a software-only tier. Regulatory agencies have yet to codify accuracy thresholds for these apps, but low-resource clinics may adopt them ahead of formal approval.

Technology competition centers on bias correction for dark-skinned infants, post-phototherapy accuracy, and calibration drift over multiyear use. Vendors that can marry five-wavelength sensors with self-calibrating algorithms and cloud-based analytics are likely to defend premium price points. Meanwhile, multi-parameter blood-gas analyzers mount a substitution threat in consolidated hospital laboratories, pressuring standalone bench-top sales.

Bilirubin Meters Industry Leaders

Drägerwerk AG & Co. KGaA

Koninklijke Philips N.V.

Siemens Healthineers

Konica Minolta, Inc.

Radiometer Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Natus Sensory, an ARCHIMED portfolio company, acquired TheraB Medical. The acquisition expands Natus's newborn-care portfolio beyond screening into treatment.

- January 2026: Natus Sensory acquired cloud-software firm Keriton to integrate feeding, growth, and jaundice data into a unified NICU dashboard.

Global Bilirubin Meters Market Report Scope

As per the scope of the report, bilirubin meters, or bilirubinometers, are medical instruments designed to measure bilirubin levels in the body, primarily as a screening tool for neonatal jaundice. While traditional laboratory methods require invasive blood draws, modern transcutaneous bilirubin (TcB) meters offer a non-invasive alternative. These portable, handheld devices operate on the principle of optical spectroscopy by directing light into the infant's skin, usually on the forehead or sternum, and measuring the intensity of the returned wavelengths to estimate bilirubin concentration in subcutaneous tissues.

The bilirubin meters market is segmented by product type, end user, application, and geography. Based on product type, the market is segmented into transcutaneous bilirubinometers and bench-top/serum bilirubinometers. By end user, the market is segmented into hospitals, neonatal clinics & birth centers, diagnostic laboratories, and home care. By application, the market is segmented into screening and diagnosis & monitoring. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Transcutaneous Bilirubinometers |

| Bench-top/Serum Bilirubinometers |

| Hospitals |

| Neonatal Clinics & Birth Centers |

| Diagnostic Laboratories |

| Home Care |

| Screening |

| Diagnosis & Monitoring |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Transcutaneous Bilirubinometers | |

| Bench-top/Serum Bilirubinometers | ||

| By End User | Hospitals | |

| Neonatal Clinics & Birth Centers | ||

| Diagnostic Laboratories | ||

| Home Care | ||

| By Application | Screening | |

| Diagnosis & Monitoring | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the bilirubin meters market in 2026 and how fast is it growing?

The bilirubin meters market size reached USD 402.6 million in 2026 and is forecast to post a 6.89% CAGR through 2031.

Which product type holds the largest share of bilirubin devices?

Transcutaneous meters led with 61.30% of bilirubin meters market share in 2025, owing to their non-invasive workflow advantage.

Which end-user segment will expand fastest to 2031?

Neonatal clinics and birth centers are expected to grow at an 8.56% CAGR by 2031 as payers move routine screening into outpatient settings.

What is driving bilirubin meter adoption in Asia-Pacific?

Rising birth volumes, capacity expansion to 2.4 NICU beds per 1,000 births in China, and India’s Mission ANMOL universal screening initiative are propelling uptake.

Page last updated on: