Czech Republic Courier, Express, And Parcel (CEP) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

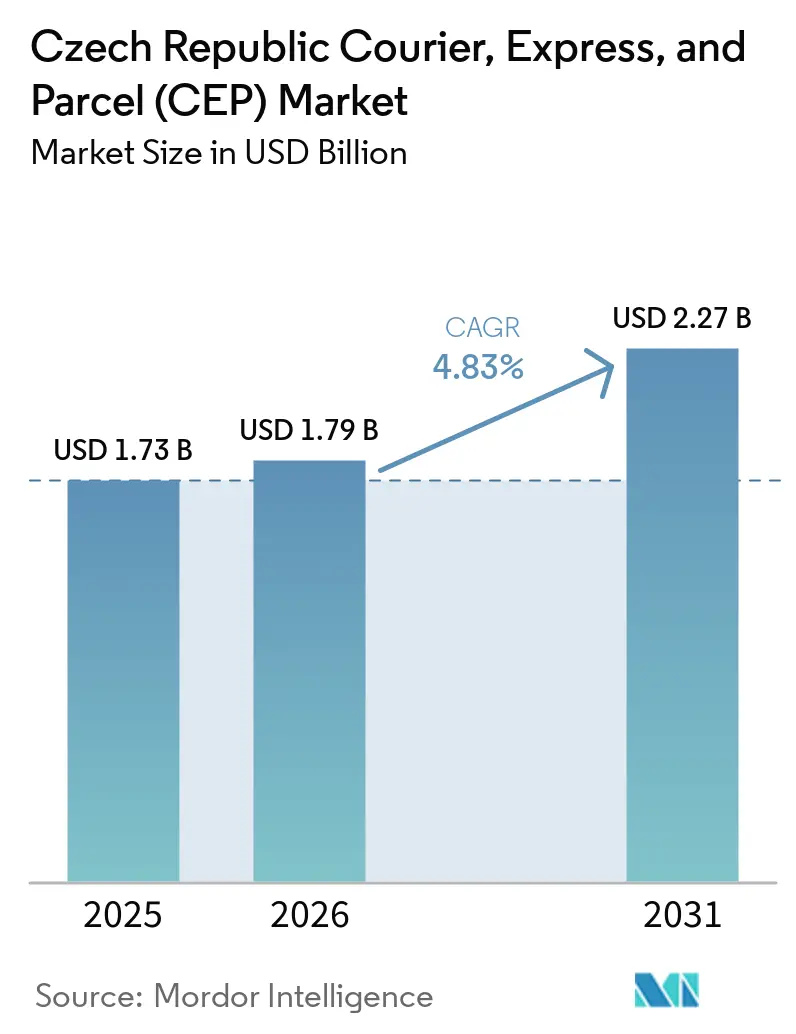

| Base Year Market Size (2025) | USD 1.73 Billion |

| Market Size (2026) | USD 1.79 Billion |

| Market Size (2031) | USD 2.27 Billion |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

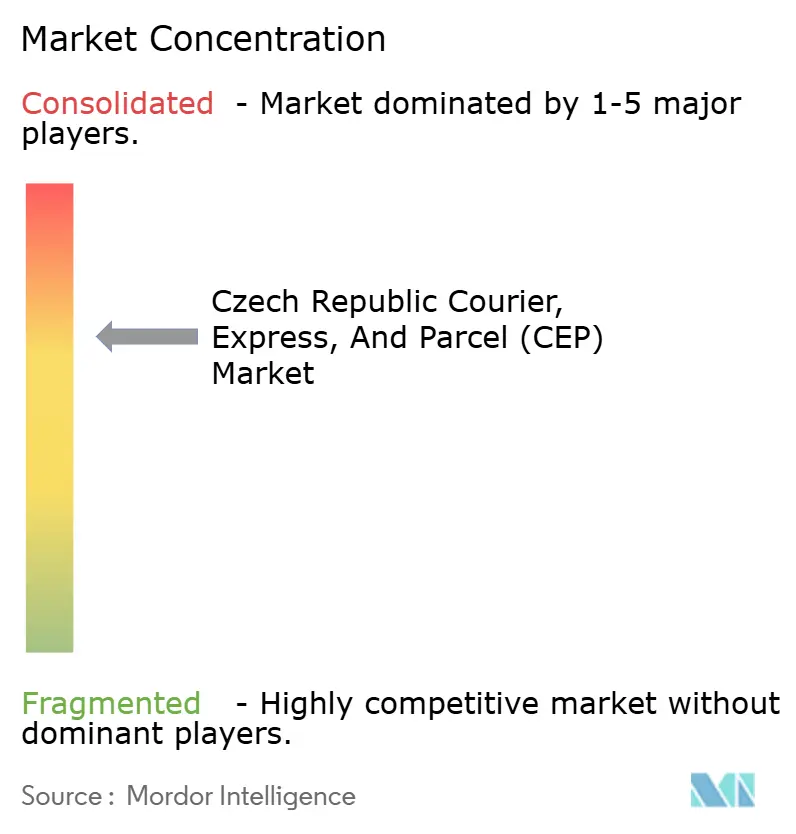

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Czech Republic Courier, Express, And Parcel (CEP) Market Analysis by Mordor Intelligence

The Czech Republic courier, express, and parcel market size is expected to grow from USD 1.73 billion in 2025 to USD 1.79 billion in 2026 and is forecast to reach USD 2.27 billion by 2031 at 4.83% CAGR over 2026-2031.

Structural shifts in reverse-logistics infrastructure, temperature-controlled pharmaceutical mandates, and just-in-time automotive networks are reshaping operating economics across Central Europe. Inbound cross-border e-commerce returns already represent 18-22% of international parcel volumes, a jump enabled by the EU-wide 14-day return rule that took effect in 2025. Temperature-sensitive biologics and vaccines now make up 28% of Czech pharmaceutical exports, lifting demand for IoT-enabled cold-chain parcels that cut spoilage rates below 1.2%. At the same time, Tier-1 automotive suppliers impose penalty clauses for late spare-parts deliveries, pushing carriers toward same-day express services and automated sort centers capable of handling 12,000-15,000 parcels per hour. Rising logistics-park lease rates in Prague and Brno, up 15-18% annually since 2024, are accelerating automation adoption and network redesign to preserve margins.

Key Report Takeaways

- By destination, domestic deliveries led with 66.29% of the Czech Republic courier, express, and parcel market share in 2025, while international shipments are forecast to expand at a 5.3% CAGR through 2031.

- By speed of delivery, non-express services accounted for 74.64% of the Czech Republic courier, express, and parcel market size in 2025; express deliveries are advancing at a 5.49% CAGR over 2026-2031.

- Within the model segmentation, B2C held 50.12% of the Czech Republic courier, express, and parcel market share in 2025, whereas C2C parcels record the fastest growth at 8.01% CAGR to 2031.

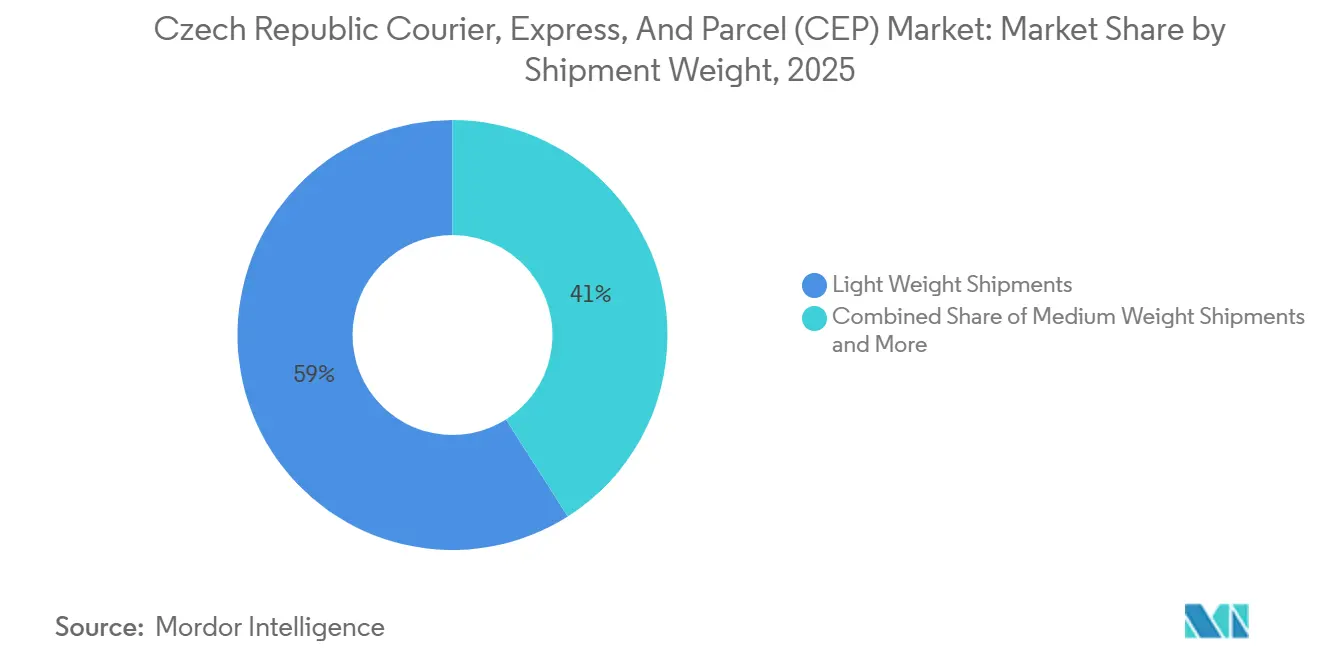

- By shipment weight, light-weight parcels captured 59% of the Czech Republic courier, express, and parcel market size in 2025, yet medium-weight shipments are projected to grow at a 5.67% CAGR during 2026-2031.

- By mode of transport, road transport retained 68.82% of the Czech Republic courier, express, and parcel market share in 2025, and air freight is set to rise at a 5.58% CAGR through 2031.

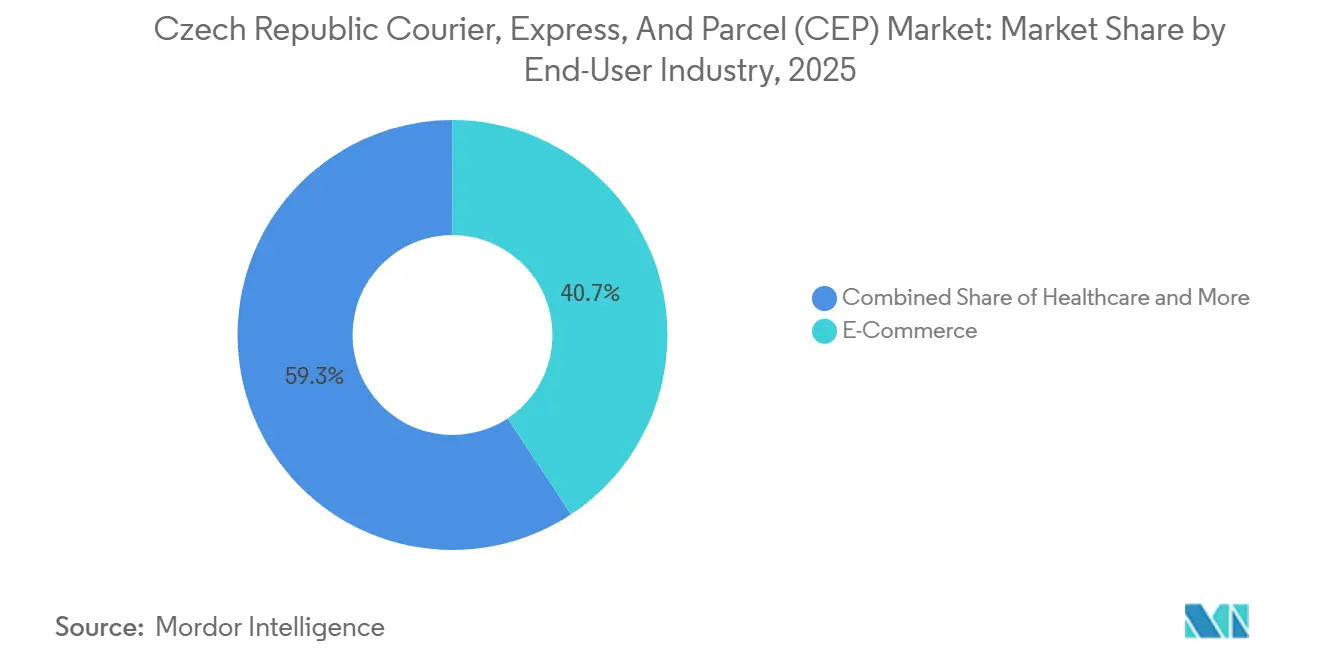

- By end-user industry, e-commerce represented 40.7% of the Czech Republic courier, express, and parcel market size in 2025; healthcare is the fastest-growing end-user at a 5.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Czech Republic Courier, Express, And Parcel (CEP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Boom in cross-border e-commerce returns logistics | +0.9% | National, hubs near Prague and Brno | Medium term (2-4 years) |

| Surging temperature-controlled pharma parcel demand post-EU FMD 2026 | +1.1% | National, with spillover to Slovakia and Poland | Long term (≥ 4 years) |

| Automotive spare-parts same-day delivery for tier-1 suppliers | +0.7% | Mladá Boleslav, Kvasiny, Nošovice clusters | Short term (≤ 2 years) |

| Logistics-property investment wave adding automated sort centers | +0.8% | Prague and Brno metro corridors | Medium term (2-4 years) |

| Pilot programme for nationwide Sunday parcel deliveries | +0.5% | Urban centers countrywide | Short term (≤ 2 years) |

| Prague airport micro-parcel night-sort hub opening 2027 | +0.6% | National, EU connectivity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Boom in Cross-Border E-Commerce Returns Logistics

Return shipments now equal nearly one-fifth of all international parcel inflows as the EU’s 14-day rule standardizes customer expectations. Czech carriers have built dedicated reverse-logistics hubs near key border crossings that pre-sort items for repair, resale, or secondary export. Automated vision systems cut inspection times by about one-third, which improves asset turns for online retailers. The Czech Republic courier, express, and parcel market, therefore, benefits from predictable back-haul volumes that raise line-haul asset utilization. Carriers offering single-invoice forward-and-return solutions gain a service edge that boosts customer retention[1]“Consumer Rights Directive,” European Commission, commission.europa.eu.

Surging Temperature-Controlled Pharma Parcel Demand Post-EU FMD 2026

The 2026 serialization upgrade under the Falsified Medicines Directive requires real-time temperature and custody tracking for every prescription shipment. Biologics already account for more than one-quarter of Czech drug exports, lifting annual cold-chain parcel growth into double digits. IoT sensors and blockchain registries bring spoilage under 1.2%, generating price premiums that far exceed standard parcel yields. The Czech Republic courier, express, and parcel market is seeing targeted fleet purchases of refrigerated vans that open new revenue pools across Central Europe. Long-haul corridor links into Slovakia and Poland magnify the growth runway for regulated healthcare freight[2]“Falsified Medicines Overview,” European Medicines Agency, ema.europa.eu.

Automotive Spare-Parts Same-Day Delivery for Tier-1 Suppliers

Assembly plants in Mladá Boleslav and other clusters now operate with inventory buffers of only a few hours, enforcing strict penalty clauses for late arrivals. Express carriers have responded by leasing micro-fulfillment depots within 30 kilometers of the lines. Same-day lanes for electronic control units and powertrain modules command revenue premiums of roughly 25-30%. The Czech Republic courier, express, and parcel market, therefore, captures new value by blending time-definite service with specialized handling. Electric-vehicle production adds further complexity because batteries require shock monitoring throughout transit.

Logistics-Property Investment Wave Adding Automated Sort Centers

Real-estate spending reached USD 2 billion in 2024, and nearly half funded AI-enabled hubs that sort up to 15,000 parcels per hour. Automation offsets Prague lease inflation that has averaged 16% annually since 2024. Robotic conveyors shrink unit labor cost by one-third and lift processing accuracy. The Czech Republic courier, express, and parcel market gains from faster cut-off times that let retailers promise later order windows. Early movers lock in capacity at favorable rents, squeezing competitors into higher-cost secondary sites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended producer responsibility fees on packaging waste | -0.5% | Nationwide, strongest in e-commerce | Short term (≤ 2 years) |

| Sharp uptick in Prague logistics-park lease rates 2024-2028 | -0.7% | Prague metro; spillover to Brno | Medium term (2-4 years) |

| Green-corridor Nox caps on d5 motorway rerouting trucks | -0.4% | Prague–Plzen–German border | Short term (≤ 2 years) |

| Global microchip shortage delaying automation roll-outs | -0.3% | Nationwide, large facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Extended Producer Responsibility Fees on Packaging Waste

The EPR scheme, effective January 2025, adds up to USD 0.17 per kilogram for non-recyclable materials, lifting reverse-logistics cost by about 10%. Large carriers can absorb compliance overhead, but smaller operators struggle with reporting and material tracking. Switching to recycled cardboard cuts the fee but raises material spend by 15–20% until volumes scale. The Czech Republic courier, express, and parcel market thus sees margin pressure in high-volume fashion e-commerce traffic. Carriers with in-house packaging design teams are quickest to optimize box sizes and limit void space[3]“Packaging Act No. 477/2001 Coll. and EPR Obligations,” Ministry of the Environment Czech Republic, mpo.gov.cz.

Sharp Uptick in Prague Logistics-Park Lease Rates 2024-2028

Prime locations near the D1 and D5 junctions now cost up to USD 8.00 per square meter monthly, compared with about USD 6.00 in 2023. Some networks have moved hubs 40 kilometers outward, adding 12–15% more final-mile distance and fuel spend. Consolidation is accelerating because mid-size firms cannot secure long leases at sustainable rates. The Czech Republic courier, express, and parcel market, therefore, trends toward fewer but larger hubs with heavy automation to maximize floor productivity. Secondary cities such as Brno and Ostrava attract new investment on cost grounds[4]“Logistics and Forwarding Sector Development,” Ministry of Industry and Trade Czech Republic, mpo.gov.cz.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Healthcare Leads Growth

Healthcare parcels clock a 5.95% CAGR, driven by biologics and direct-to-patient diagnostics that rely on cold-chain proof-of-condition. Temperature alarms feed dashboards that pharmacists monitor in real time. The Czech Republic courier, express, and parcel market prices these services at an 18–25% premium over general freight, supporting margin resilience.

E-commerce keeps the largest slice of demand with 40.7% of the Czech Republic courier, express, and parcel market share in 2025, but normalizes after pandemic surges. Manufacturing parcels rise on just-in-time lean flows, especially in automotive electronics. Wholesale and traditional retail traffic adapts by splitting bulk orders into more frequent, smaller consignments that better match shelf turnover.

By Destination: International Momentum Builds on Reverse Flows

Domestic shipments captured 66.29% of the Czech Republic courier, express, and parcel market size in 2025, while international consignments rose at a 5.3% CAGR between 2026 and 2031, outperforming domestic growth thanks to organized return lanes and cold-chain exports. Carriers leverage consolidated back-hauls that cut empty-run mileage, lifting network yield. Czech Republic courier, express, and parcel market participants with border-adjacent depots clear customs in under four hours, speeding cycle times.

Domestic volumes retain two-thirds of traffic, sustained by 9,000 pickup points that keep failed deliveries under 4%. Sunday routes and automotive spare-parts shuttles protect revenue per parcel despite slower volume gains. A stable home-delivery base lets carriers pilot locker roll-outs and dynamic pricing engines before extending tools to cross-border flows.

By Speed of Delivery: Express Carves Out Value

By speed of delivery, non-express parcels held 74.64% of the Czech Republic courier, express, and parcel market share in 2025. Whereas express parcels expand at 5.49% CAGR as automotive and pharma clients demand time certainty. Same-day lanes inside 250-kilometer arcs run on premium tariffs that outpace diesel inflation. The Czech Republic courier, express, and parcel market thus upgrades routing software to balance cutoff times with driver hours.

Standard services still handle three-quarters of volume, anchored by price-sensitive fashion and general merchandise. Automated sort centers raise sort accuracy, reducing rework that erodes slim margins. Blended portfolios let carriers cross-sell express upgrades during seasonal peaks.

By Shipment Weight: Mid-Weight Parcels Accelerate

Medium-weight shipments advance at 5.67% CAGR, propelled by automotive components and home appliances that exceed locker limits. Depots invest in ergonomic lifts and weight-based tariff tools that protect handlers from injury and keep billing transparent. The Czech Republic courier, express, and parcel market also sees hospitals ordering mid-weight medical kits directly to wards, favoring carriers with temperature and shock sensors.

Light-weight traffic still dominates with 59% of the Czech Republic courier, express, and parcel market size in 2025, linked to fashion and electronics. However, commoditized pricing forces operators to find savings in route density and stop sequencing. Heavy shipments above 31.5 kg shift to pallet networks and rail feeders, leaving parcel operators to specialize in value-added handling.

By Mode of Transport: Air Adds Reach

Air cargo posts a 5.58% CAGR as the 2027 night-sort hub unlocks next-day access to most EU capitals. Lower belly-cargo rates on passenger flights entice merchants to upgrade service levels for high-margin SKUs. For the Czech Republic courier, express, and parcel market, the modal mix tilts slightly toward air, despite road retaining nearly 68.82% share.

Road fleets electrify last-mile vans and optimize trailer fills with AI load-planning. Intermodal options linking Rail Freight Corridor 9 to depots in Brno gain traction where cost beats speed. Carriers that master modal switching can flex capacity during fuel spikes or driver shortages.

By Business Model: C2C Surges on Resale Platforms

Consumer-to-consumer parcels grow at a CAGR of 8.01%, as second-hand shopping enters the mainstream. Secure lockers ease after-hours drop-off, and integrated payment-on-delivery apps build trust between peers. The Czech Republic courier, express, and parcel market captures incremental trips because each resale often triggers twice the parcel touches of a conventional e-commerce order.

B2C remains the largest model with 50.12% of the Czech Republic courier, express, and parcel market share in 2025, yet shows mid-single-digit growth, indicating maturing online penetration. Business-to-business lanes edge up slowly as procurement digitizes, but inventories are held leaner. Contract terms increasingly reward on-time metrics over raw price, improving margins for reliability-focused carriers.

Geography Analysis

Prague and Brno corridors generate almost half of all domestic parcel movements due to population concentration and higher discretionary spending. These regions also host the bulk of automated hubs, which process up to 15,000 pieces per hour, doubling legacy throughput. Secondary cities benefit as carriers open spoke depots to bypass congested urban roads.

Cross-border routes into Slovakia and Poland carry rising pharma and fashion returns that now move with pre-cleared digital customs manifests. The Czech Republic courier, express, and parcel market positions consolidation centers within 10 kilometers of major crossings to shave lead time and avoid motorway toll surcharges.

Railroad intermodal links along Corridor 9 add capacity for medium-distance hauls, trimming emissions relative to pure road. Ostrava’s recent FedEx facility anchors northern flows while relieving Prague hub pressure. As a result, delivery windows stay inside 48 hours for 96% of EU addresses, a key competitive metric for multinational merchants.

Competitive Landscape

The 2025 DSV–Schenker merger created a regional heavyweight that controls significant line-haul and warehouse assets. Smaller rivals pivot to niche offerings in cold-chain, reverse logistics, or weekend delivery to avoid head-to-head scale wars. The Czech Republic courier, express, and parcel market, therefore, rewards specialization backed by technology.

Locker networks confer durable advantage through network effects; InPost’s 3,200 units and Zasilkovna’s 9,000 pickup sites lock in consumer convenience. AI route optimizers embedded in sort centers cut miss-sort errors by 40%, further lifting service scores. Carriers unable to match density cooperate through open locker alliances that share fixed costs.

Private-equity investors funnel capital into automation and green fleets, expecting that ESG mandates will translate into customer preference. Early adopters of electric vans report maintenance savings that narrow the total-cost gap within three years. Partnerships with e-commerce giants such as Allegro stipulate carbon reporting, nudging laggards to modernize or risk contract loss.

Czech Republic Courier, Express, And Parcel (CEP) Industry Leaders

Packeta Group sro (Including Zasilkovna sro)

International Distribution Services PLC (Including GLS CZ)

Czech Post

DHL Group

La Poste Group (Including DPD Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: DPD CZ partnered with Packeta to enable deliveries to the Z-BOX locker network, adding over 3,000 locations. This collaboration improves last-mile efficiency and supports e-commerce growth.

- May 2025: UPS Czech Republic rolled out blockchain-enabled cold-chain monitoring for nationwide pharma distribution.

- April 2025: DSV finalized its EUR 14.3 billion (USD 15.8 billion) acquisition of DB Schenker, creating a USD 45.9 billion revenue player with 160,000 staff worldwide.

- March 2025: DPD Czech Republic partnered with Allegro to widen cross-border parcel locker access for Czech shoppers.

Czech Republic Courier, Express, And Parcel (CEP) Market Report Scope

| Domestic |

| International |

| Express |

| Non-Express |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Consumer-to-Consumer (C2C) |

| Heavy Weight Shipments |

| Light Weight Shipments |

| Medium Weight Shipments |

| Air |

| Road |

| Others |

| E-Commerce |

| Financial Services (BFSI) |

| Healthcare |

| Manufacturing |

| Primary Industry |

| Wholesale and Retail Trade (Offline) |

| Others |

| Destination | Domestic |

| International | |

| Speed of Delivery | Express |

| Non-Express | |

| Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Consumer-to-Consumer (C2C) | |

| Shipment Weight | Heavy Weight Shipments |

| Light Weight Shipments | |

| Medium Weight Shipments | |

| Mode of Transport | Air |

| Road | |

| Others | |

| End-User Industry | E-Commerce |

| Financial Services (BFSI) | |

| Healthcare | |

| Manufacturing | |

| Primary Industry | |

| Wholesale and Retail Trade (Offline) | |

| Others |

Key Questions Answered in the Report

How fast is express parcel volume growing in the Czech Republic?

Express consignments are advancing at a 5.49% CAGR between 2026 and 2031, fueled by automotive and pharma demand.

What impact will the 2027 Prague Airport night-sort hub have on delivery times?

The hub will enable next-day reach to 85% of EU destinations, cutting current transit times by one full day for many lanes.

Why are medium-weight parcels gaining share?

Automotive components and home appliances fall into the 5–31.5 kg bracket, driving 5.67% CAGR growth for this weight class.

Which end-user sector is expanding the fastest?

Healthcare parcels lead with a 5.95% CAGR because biologics and direct-to-patient deliveries require temperature-controlled service.

How are rising Prague lease rates influencing network design?

Carriers shift hubs to secondary cities and automate heavily to offset a 15–18% annual jump in prime rents since 2024.

What sustainability measures are carriers adopting?

Fleets are adding electric vans, recyclable packaging, and IoT-based fuel optimization to align with customer ESG targets.

Page last updated on: