Silicon Battery Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

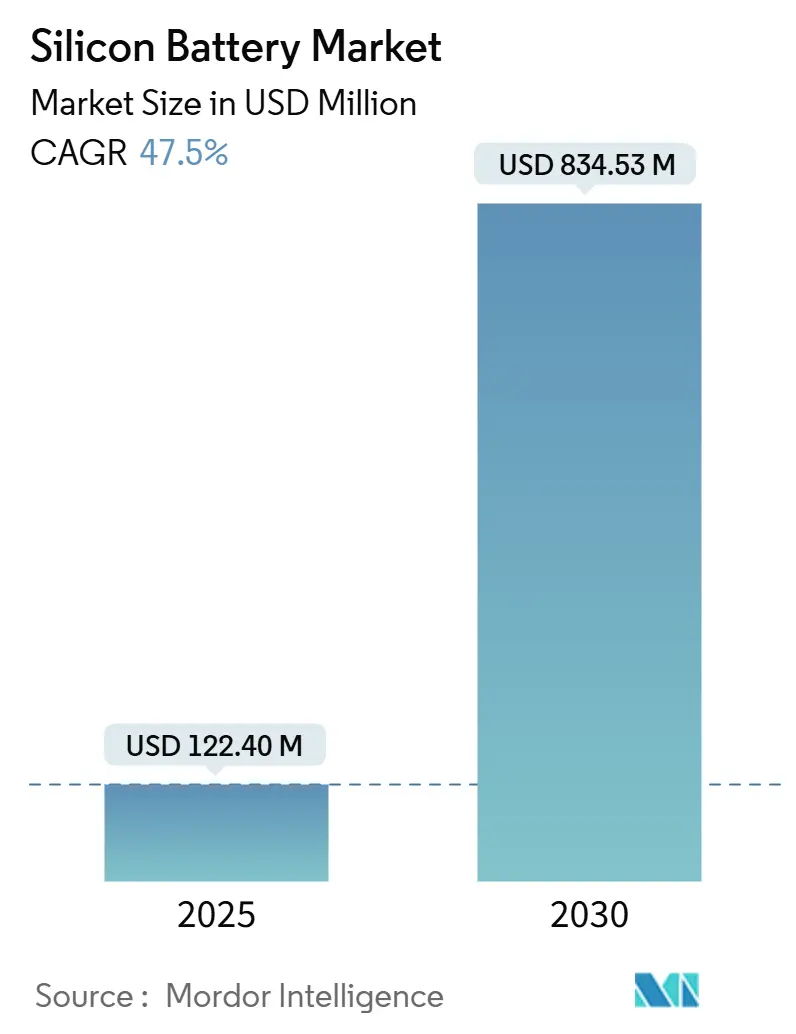

| Market Size (2025) | USD 122.40 Million |

| Market Size (2030) | USD 834.53 Million |

| Growth Rate (2025 - 2030) | 47.50% CAGR |

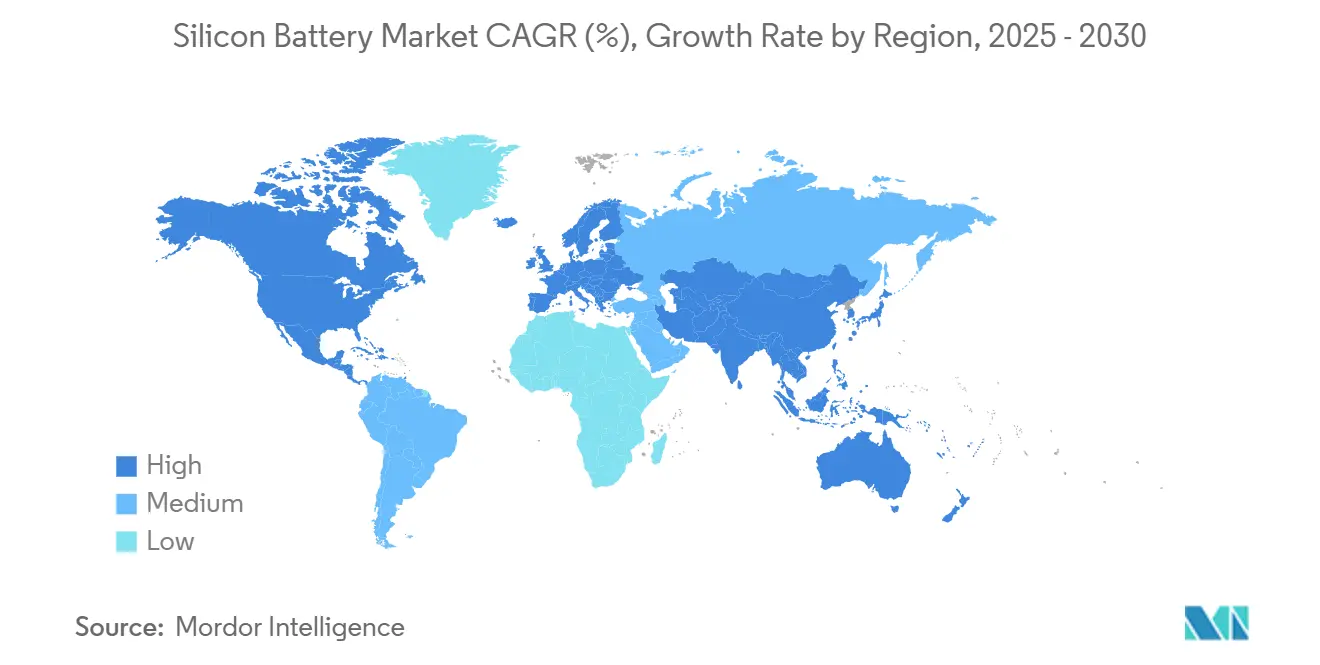

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silicon Battery Market Analysis by Mordor Intelligence

The silicon battery market size stands at USD 122.40 million in 2025 and is projected to reach USD 834.53 million by 2030, reflecting a 47.5% CAGR over the forecast period. Robust growth stems from silicon’s ten-fold higher theoretical capacity versus graphite, rising automotive demand for 400-plus-mile electric-vehicle (EV) ranges, and federal incentives that localize supply chains in North America. Large-scale materials funding, such as Sila Nanotechnologies’ USD 375 million Series G raise, confirms investor confidence in mass-production readiness. Commercial deployments already demonstrate 900 Wh/L energy density smartphone batteries and 67-day stratospheric flight cells, signaling performance validation across consumer electronics and aerospace segments. Meanwhile, dry-electrode manufacturing lines cut solvent use and reduce production costs by up to 15% while enabling higher silicon loading.

Key Report Takeaways

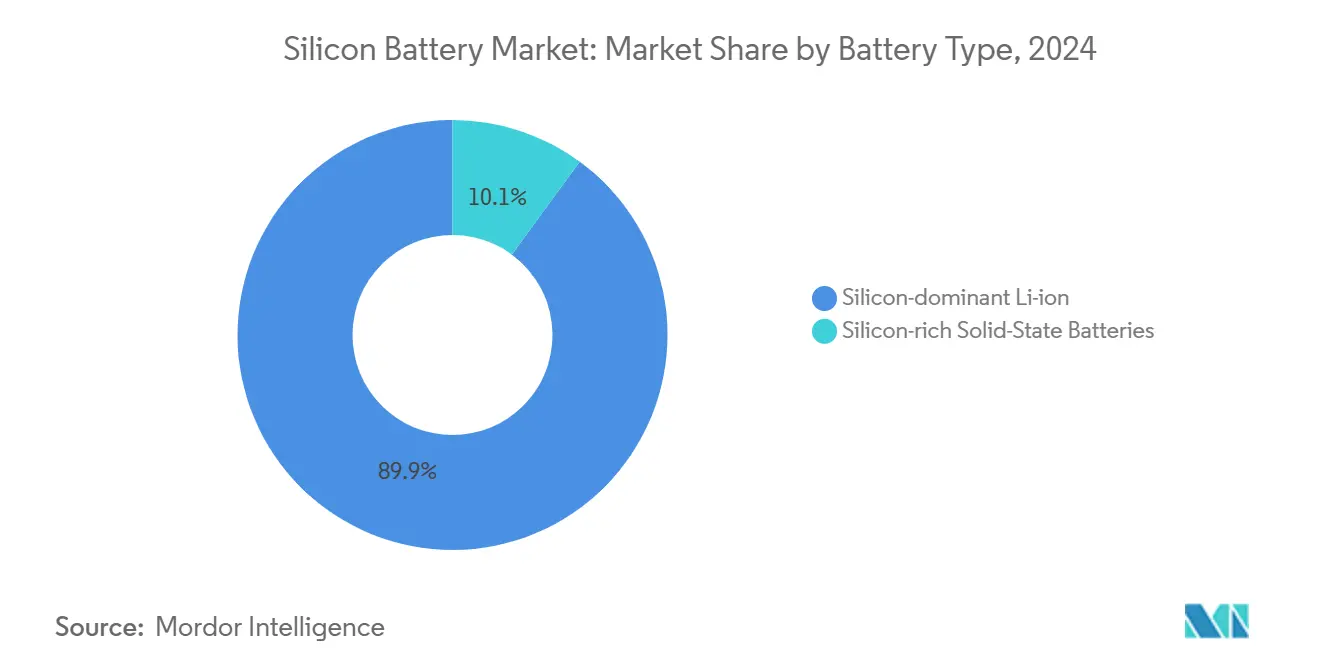

- By battery type, silicon-dominant lithium-ion cells led with 89.91% of silicon battery market share in 2024; silicon-rich solid-state cells are forecast to advance at a 49.43% CAGR through 2030.

- By silicon material, silicon–carbon composites accounted for 46.73% of the silicon battery market size in 2024, while silicon nanowires exhibit the highest 48.23% CAGR to 2030.

- By form factor, pouch cells captured 51.32% revenue share in 2024; prismatic cells register the fastest 49.14% CAGR to 2030.

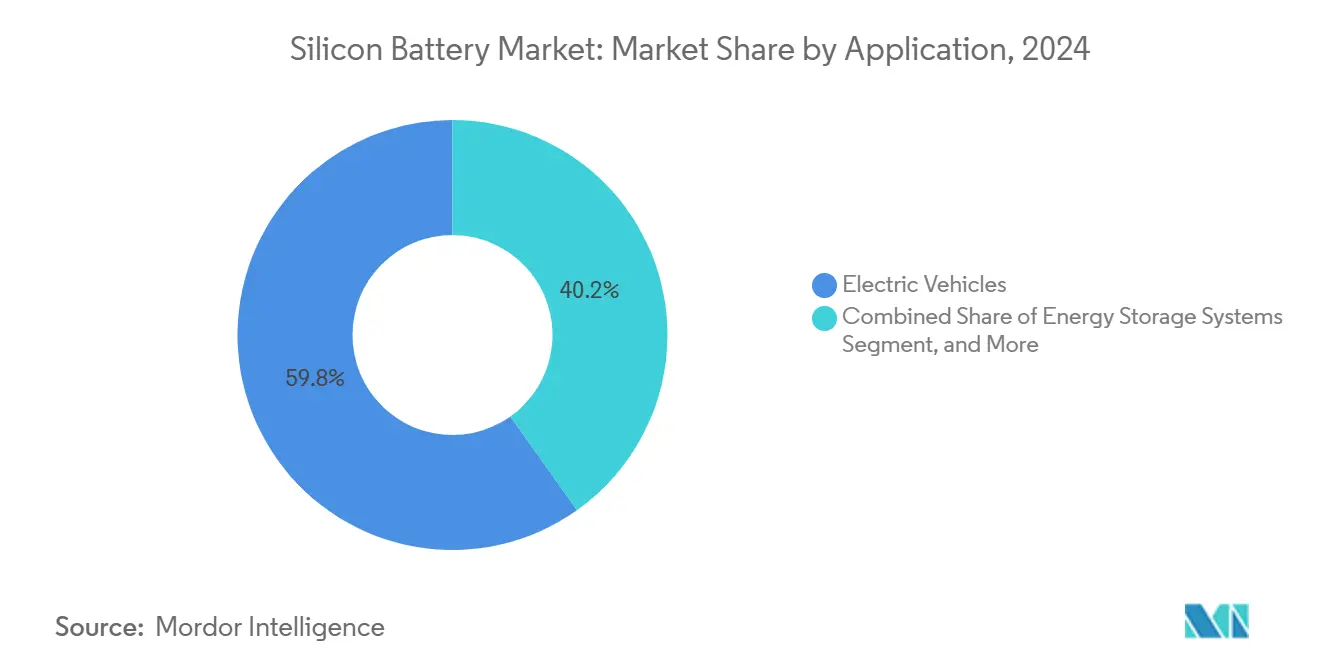

- By application, electric vehicles held 59.84% of the silicon battery market size in 2024, whereas aerospace and defense is expanding at a 48.91% CAGR through 2030.

- By geography, Asia-Pacific commanded 54.97% share of the silicon battery market in 2024, and North America records the strongest 47.87% CAGR between 2025-2030.

Global Silicon Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for higher-energy-density EV packs | +12.5% | China, Europe, North America | Medium term (2-4 years) |

| Accelerating cost declines in nano-silicon production | +8.7% | Asia-Pacific, North America | Short term (≤2 years) |

| Rapid scale-up of dry-electrode manufacturing lines | +6.3% | North America, EU, Asia | Medium term (2-4 years) |

| Mass-commercialization of 5–20 Ah e-bike batteries | +4.8% | Asia-Pacific, Europe | Short term (≤2 years) |

| OEM localization mandates for silicon supply chains | +7.2% | North America, Europe, Asia-Pacific | Long term (≥4 years) |

| AI-optimized silicon-carbon composite architectures | +5.9% | North America, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Higher-Energy-Density EV Packs

Automakers must achieve 400-mile driving ranges without raising battery pack mass, pushing adoption of silicon-enhanced anodes that deliver 20-40% more gravimetric capacity than graphite. Mercedes-Benz committed to Sila Nanotechnologies’ Titan Silicon for future G-Class models, validating commercial readiness at automotive scale. [1]Sila Nanotechnologies, “Sila to Build Next Generation Batteries in Washington State,” silanano.com BMW’s five new high-voltage assembly plants integrate cell formats designed for 10-plus % silicon content, highlighting OEM-level traction. Higher volumes accelerate learning curves that further reduce silicon material cost.

Accelerating Cost Declines in Nano-Silicon Production

Group14’s USD 614 million Series C funding supports a 4,000-t/yr plant that lowers silicon-carbon composite cost per kilogram by an estimated 40-60% through economy-of-scale reactors and spray-drying process intensification. [2]Group14 Technologies, “Press Release SCC55 Performance,” group14.technology Parallel initiatives recycle semiconductor-grade scrap into spherical Si-C powder, shrinking raw-material spend while improving sustainability profiles.

Rapid Scale-Up of Dry-Electrode Manufacturing Lines

Dry-coating eliminates N-methyl-2-pyrrolidone solvents, cuts energy consumption in drying ovens, and allows electrode areal capacities above 6 mAh/cm². Pilot lines installed by multiple U.S. cell manufacturers achieve uniform silicon dispersion and lower tortuosity, enabling 10-minute fast-charge performance without thermal runaway.

Mass-Commercialization of 5–20 Ah E-Bike Batteries

Premium e-bike producers adopt 20-Ah silicon-carbon batteries that extend range by 25% while holding price premiums consumers accept. Volume orders de-risk production ramps, giving materials suppliers predictable offtake agreements and operating leverage. Cycle-life data from two-wheel applications feeds back into automotive validation loops, compressing development timelines for larger packs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volumetric expansion-induced anode degradation | -8.4% | Global | Medium term (2-4 years) |

| Fragmented IP landscape inflating licensing costs | -5.7% | North America, Europe | Long term (≥4 years) |

| Battery-grade silane supply concentration | -4.9% | Asia-Pacific | Short term (≤2 years) |

| Limited binder compatibility for high-silicon loads | -4.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volumetric Expansion-Induced Anode Degradation

Silicon swells by up to 280% on lithiation, fracturing electrode matrices and accelerating capacity fade. Laboratory tests show 15% silicon-doped cells generate higher surface temperatures under mechanical abuse, highlighting safety implications. [3]ScienceDirect, “Impact of Silicon Content on Mechanical Abuse,” sciencedirect.com Amprius addresses the issue with porous architectures achieving 1,500-cycle life at 80% retention, but large-scale replication across all pack formats remains work in progress.

Fragmented IP Landscape Inflating Licensing Costs

More than 1,300 battery-related patents were issued during 2024 alone, many covering overlapping silicon anode chemistries, structures, and manufacturing methods. Start-ups may face double-digit royalty burdens when scaling commercial production, raising barriers to entry until patent pools or cross-licensing frameworks mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Silicon-Dominant Architectures Lead Market

Silicon-dominant lithium-ion batteries represented 89.91% of silicon battery market share in 2024, benefiting from compatibility with existing wet-slurry coating lines and supply chain continuity. At a 49.43% CAGR, silicon-rich solid-state variants are expected to narrow the gap as pilot plants prove 844 Wh/L prototypes with 12-minute fast-charge capability. Manufacturers prefer silicon-dominant packs for near-term EV launches, ensuring a stable revenue base while de-risking next-generation tooling. Solid-state producers, meanwhile, partner with premium vehicle brands and aerospace programs where performance outweighs cost, creating dual-path technology maturation.

Market acceptance accelerates as cycle-life hurdles fall: Enovix demonstrated 900 Wh/L AI-1 smartphone cells rated for 1,000 cycles, validating 100% active silicon anode feasibility. Continuous improvements in pre-lithiation, binder elasticity, and electrolyte additives erode remaining lifetime gaps versus graphite. Consequently, the silicon battery market size for solid-state cells is projected to reach USD 56 million by 2027 before entering high-volume automotive contracts.

By Silicon Material Type: Composites Dominate Current Applications

Silicon–carbon composites account for 46.73% of silicon battery market size in 2024 as carbon acts as a mechanical buffer, preventing catastrophic electrode failure while maintaining conductivity. Group14’s SCC55 shows 3,000-cycle life with 50% higher energy density than graphite, underscoring the composite approach. Silicon nanowires, growing at 48.23% CAGR, deliver 2,330 mAh/g capacities by offering free-surface volume to absorb expansion.

In the medium term, composite suppliers expand capacity faster because they retrofit into existing anode lines. Nanowire players focus on vertically integrated production, targeting premium aerospace cells first. Blended SiO/graphite powders fill mass-market niches by boosting energy density 20-25% with minimal process change. Continuous R&D in binder chemistries and nano-porous carbon cages suggests convergence: hybrid composite–nanowire electrodes that leverage strengths of both material classes.

By Form Factor: Pouch Cells Lead Despite Prismatic Revival

Pouch designs held 51.32% of 2024 shipments as flexible aluminum casing tolerates silicon swelling, allowing higher volumetric energy density without rigid constraints. Prismatic cells record a 49.14% CAGR following Korean firms’ EUR-scale investments that embed safety tabs and pressure relief features suitable for silicon-heavy chemistries.

Dry-coated silicon electrodes increasingly favor prismatic geometry for uniform stack pressure and thermal distribution. Volkswagen’s commitment to prismatic cell-to-pack architecture further tilts OEM roadmaps. Cylindrical formats remain relevant for power tools and entry-level EVs due to high line-speed advantages, yet they integrate ≤10% silicon loads to manage radial stress. Over time, material breakthroughs may permit higher silicon percentages in cylindrical cells, expanding use cases.

By Application: Electric Vehicles Drive Demand Growth

Electric vehicles dominated with 59.84% of silicon battery market size in 2024 as automakers race to 400-mile range and 10-minute charge targets. Mercedes-Benz, Panasonic, and Sila signed multi-year offtake agreements covering 1 million cars annually from 2026 onwards. Aerospace and defense, advancing at 48.91% CAGR, leverages silicon’s 500 Wh/kg potential for solar-powered high-altitude platforms like Zephyr, which flew 67 days nonstop on Amprius cells.

Consumer electronics capitalize on volumetric gains: Enovix’s 7,350 mAh smartphone pack doubles operating life within the same footprint. Energy-storage-system providers test high-silicon modules for space-constrained commercial buildings, although cycle-life cost metrics still favor LFP chemistries in utility arrays. Medical device innovators explore nanostructured silicon solid-state micro-cells for smart implants, broadening downstream diversification.

By Form Factor: Manufacturing Innovation Drives Adoption

Dry‐electrode roll-to-roll lines, inspired by Maxwell acquisition learnings, now coat 10-µm active silicon films directly onto copper without solvent ovens cutting factory OPEX by 15% and CO₂ emissions by 25%. Prismatic cell vendors scale the technology first due to flat-plate geometry, achieving uniform compression critical for silicon longevity. Pouch cell R&D teams iterate dielectric stack seals to withstand internal pressure rise, targeting 800+ cycles at 80% retention.

As process know-how diffuses, suppliers of slurry mixers, calendaring rolls, and laser notching systems retrofit equipment to handle higher particle-size distributions found in silicon composites. This ecosystem maturity lowers capital intensity for new entrants and accelerates mainstream adoption, supporting the silicon battery market’s rapid ascent toward the next USD 1 billion threshold.

Geography Analysis

Asia-Pacific controlled 54.97% of silicon battery market revenue in 2024, anchored by China’s 67.8% share of global silicon-anode capacity and a policy environment that subsidizes gigafactory builds and semiconductor-grade silane output. Korean champions Samsung SDI and LG Energy Solution invest in Hungary and Arizona sites, respectively, exporting know-how back into regional hubs to reinforce prismatic leadership. Japan’s materials firms supply electrolyte additives that suppress silicon expansion, rounding out an integrated supply chain that keeps landed costs low.

North America posts the fastest 47.87% CAGR as the Inflation Reduction Act and Department of Energy grants de-risk domestic raw-material projects. Group14’s 7,200 t/yr silane plant and Sila’s Moses Lake facility collectively backstop sufficient capacity for more than 1 million EVs a year by 2027. U.S. cell makers pair domestic silicon with locally refined lithium to maximize tax credits, tightening value capture within the region.

Europe maintains steady growth under the EU Battery Regulation 2023/1542, which imposes lifecycle carbon limits and recycled-content thresholds that favor energy-dense chemistries. BMW’s “local-for-local” strategy spreads battery assembly across five countries, reducing logistics emissions while securing political goodwill. Meanwhile, Lyten’s acquisition of a Northvolt storage systems site signals incoming production scale for 3D-graphene-reinforced silicon cells.

Middle East and Africa and South America currently contribute low-single-digit shares but leverage rich lithium and silicon feedstocks to court downstream investment. Pilot projects in Chile align mining output with anode processing, while UAE free-trade zones court U.S. and Korean firms looking for tariff-neutral export bases. Over the long term, regional diversification mitigates single-country supply-risk exposure in the silicon battery market.

Competitive Landscape

Market structure is moderately fragmented: the combined share of the top five players Samsung SDI, LG Energy Solution, Panasonic, Group14 Technologies, and Sila Nanotechnologies stands near 62%, creating room for nimble specialists. Enovix holds 190 patents protecting 100% active silicon cell architecture, and Group14 licenses SCC55 material under multi-year take-or-pay contracts, cementing technology moats. Start-up Amprius secures contract manufacturing capacity exceeding 500 MWh, allowing asset-light scaling toward aerospace orders.

Strategic alliances dominate. Mercedes-Benz secured exclusive quantities of Titan Silicon, while Panasonic collaborates with U.S. material vendors to raise silicon content past 10% in its next-gen 4680 cells. Licensing costs shape entry strategies: newcomers either develop proprietary porous structures to skirt crowded patent zones or join consortia pooling foundational IP. Equipment vendors such as dry-coater suppliers and advanced electrolyte firms gain pricing power as their technologies prove essential for high-silicon yields.

White-space opportunities emerge in medical implants, drones, and grid-edge storage, where niche specifications command premium pricing. Firms that integrate vertically—from silane gas to finished packs capture more margin and insulate against feedstock volatility. Expect selective consolidation as incumbents acquire start-ups with differentiated chemistries or process know-how to shorten learning curves and defend market share.

Silicon Battery Industry Leaders

Amprius Technologies, Inc.

Sila Nanotechnologies Inc.

Enovix Corporation

Enevate Corporation

Group14 Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: QuantumScape began construction of a 1 GWh pilot line after unveiling an 844 Wh/L silicon-rich solid-state prototype able to charge 10–80% in 12 minutes.

- July 2025: Lyten acquired Europe’s largest battery-energy-storage manufacturing operation from Northvolt, creating a regional base for silicon-rich cells.

- July 2025: Enovix launched the AI-1™ platform delivering 7,350 mAh smartphone batteries with 900 Wh/L energy density.

- June 2025: Group14 Technologies reported 50% higher energy density material ready for 10-minute charge commercialization.

Global Silicon Battery Market Report Scope

| Silicon-dominant Lithium-ion Batteries |

| Silicon-rich Solid-State Batteries |

| Silicon–Carbon Composites |

| Silicon Nanowires |

| Silicon Oxide/Graphite Blends |

| Other Silicon Material Types |

| Pouch Cell |

| Prismatic Cell |

| Cylindrical Cell |

| Electric Vehicles |

| Consumer Electronics |

| Energy Storage Systems |

| Aerospace and Defense |

| Medical Devices |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Battery Type | Silicon-dominant Lithium-ion Batteries | ||

| Silicon-rich Solid-State Batteries | |||

| By Silicon Material Type | Silicon–Carbon Composites | ||

| Silicon Nanowires | |||

| Silicon Oxide/Graphite Blends | |||

| Other Silicon Material Types | |||

| By Form Factor | Pouch Cell | ||

| Prismatic Cell | |||

| Cylindrical Cell | |||

| By Application | Electric Vehicles | ||

| Consumer Electronics | |||

| Energy Storage Systems | |||

| Aerospace and Defense | |||

| Medical Devices | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the silicon battery market in 2030?

The silicon battery market is forecast to reach USD 834.53 million by 2030, rising from USD 122.40 million in 2025.

Why are silicon anodes viewed as critical for next-generation EVs?

Silicon offers up to 10 times the theoretical capacity of graphite, enabling 20–40% higher energy density and helping automakers achieve 400-mile ranges without heavier packs.

Which region will grow fastest through 2030?

North America records the highest 47.87% CAGR, helped by federal incentives and large-scale domestic silicon-material plants.

What is the main technical hurdle for silicon batteries?

Volumetric expansion during lithiation causes anode cracking and capacity fade, though porous architectures and elastic binders are extending cycle life beyond 1,500 cycles.

How are manufacturers reducing silicon battery costs?

Scale-up investments, dry-electrode processing, and recycling of semiconductor-grade silicon scrap collectively lower per-kilogram material costs by up to 60%.

Which application outside EVs shows the fastest growth?

Aerospace and defense grows at 48.91% CAGR as ultra-light, high-energy silicon cells power high-altitude drones and satellite platforms.

Page last updated on: