Metal-Air Battery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

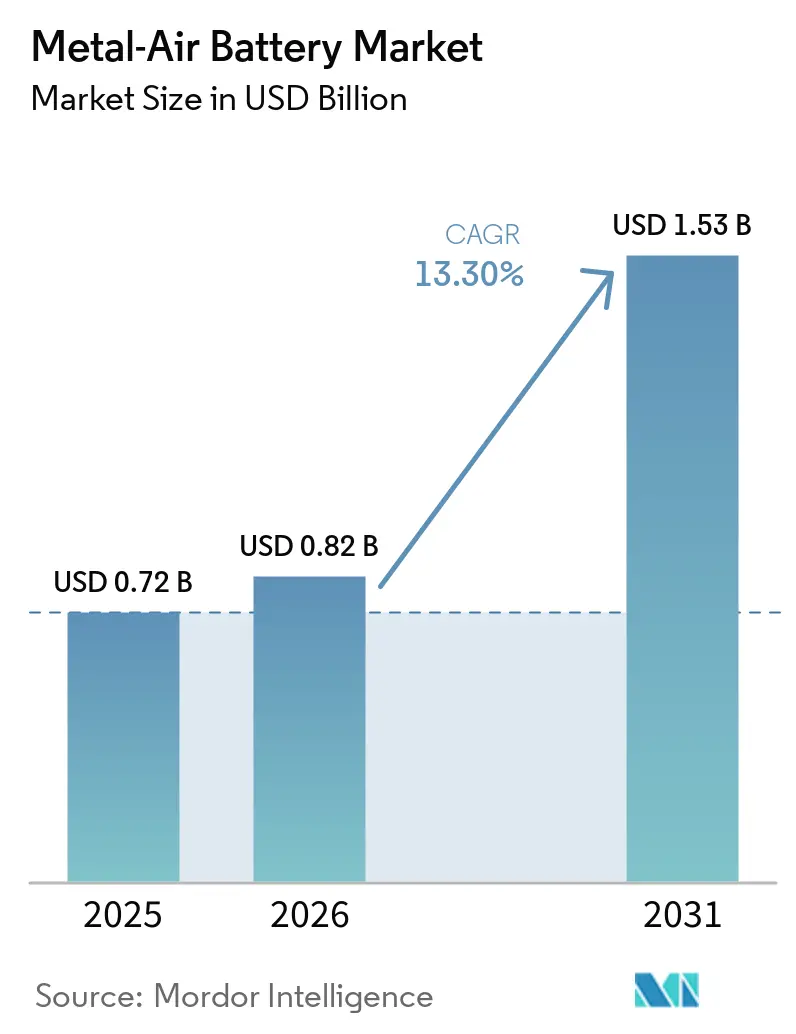

| Market Size (2026) | USD 0.82 Billion |

| Market Size (2031) | USD 1.53 Billion |

| Growth Rate (2026 - 2031) | 13.30% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal-Air Battery Market Analysis by Mordor Intelligence

The metal-air battery market size is expected to increase from USD 0.82 billion in 2026 to USD 1.53 billion by 2031, growing at a CAGR of 13.3% over 2026-2031. Technical progress in bifunctional air-cathode catalysts, a widening cost gap between zinc or aluminum and lithium or cobalt feedstocks, and the first multi-gigawatt-hour procurement agreements are setting a faster pace for commercial adoption. Form Energy’s 12 GWh iron-air contract with Crusoe for artificial-intelligence data-center backup illustrates how multi-day discharge is moving from demonstrations into mainstream utility and industrial procurement portfolios. Automakers and fleet operators are exploring metal-slurry refueling schemes to sidestep grid-dependent fast charging, while government grants in the United States, Canada, and the European Union are underwriting pilot manufacturing lines that shorten time to market. Defense agencies seeking silent, lightweight soldier power add another early-adopter niche, and falling zinc and aluminum prices have strengthened the relative cost advantage of these chemistries against volatile lithium and cobalt inputs.

Key Report Takeaways

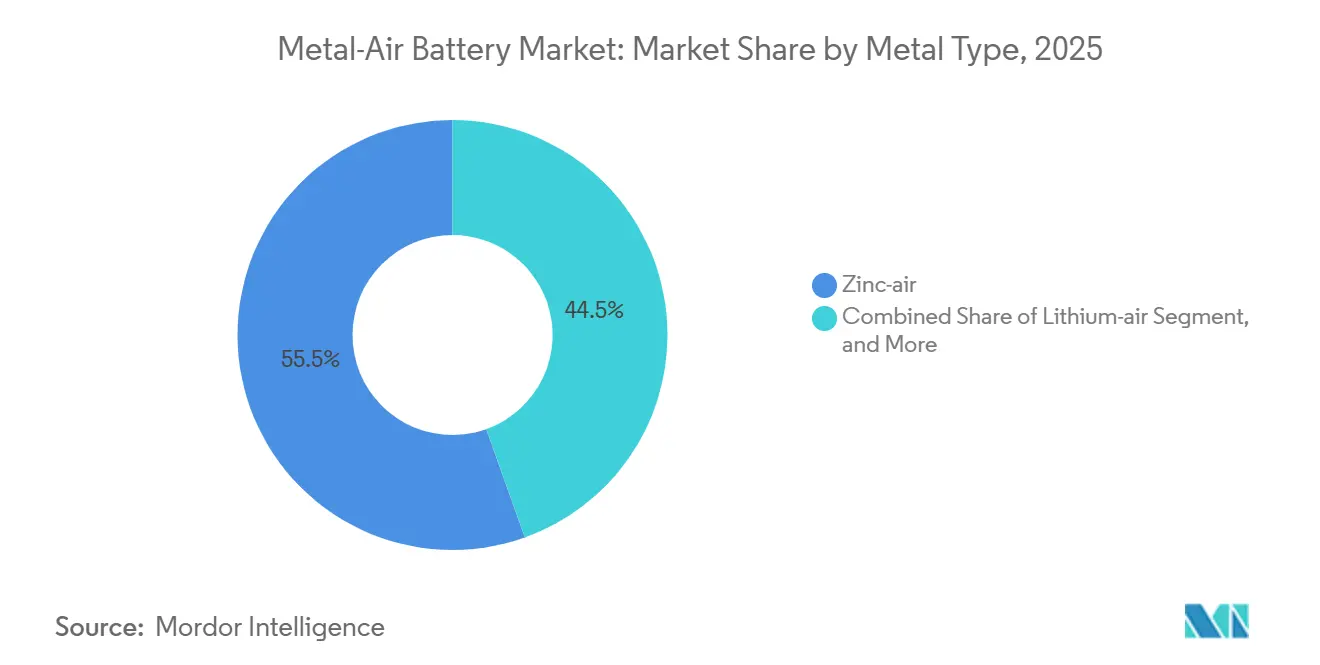

- By metal type, zinc-air led with 55.47% of the metal-air battery market share in 2025, whereas iron-air is projected to record the highest 13.86% CAGR between 2026 and 2031.

- By battery type, primary cells captured 60.19% of the metal-air battery market size in 2025, while secondary systems are forecast to expand at 13.92% through 2031.

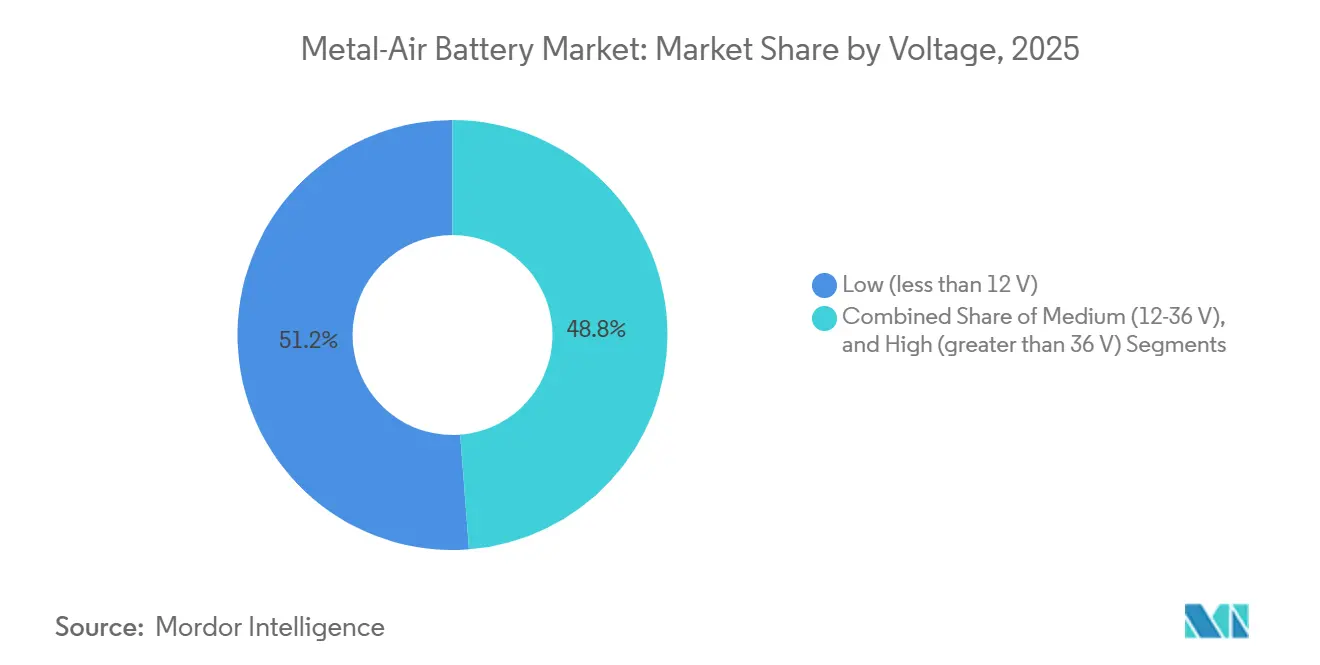

- By voltage, low-voltage units held 51.22% of the metal-air battery market in 2025, and high-voltage systems are on track for a 13.81% CAGR through 2031.

- By application, electric vehicles accounted for 48.53% of revenue in 2025, yet stationary energy storage is the fastest-growing segment at a 14.04% CAGR through 2031.

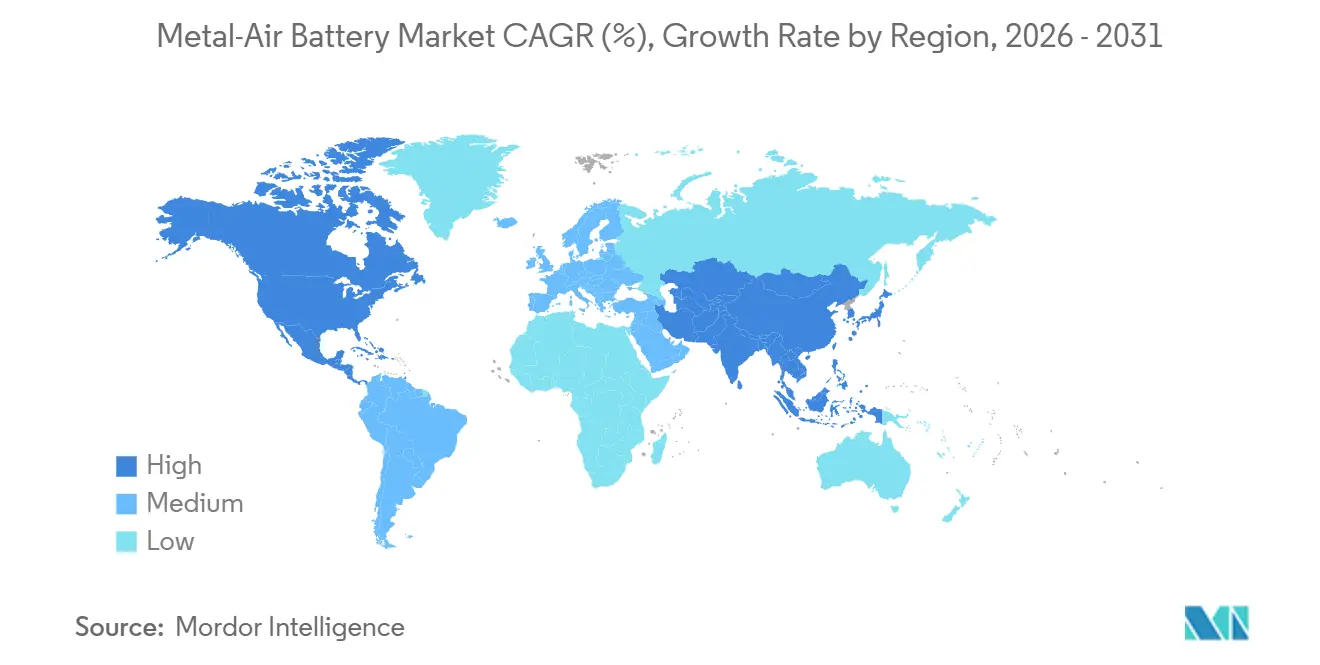

- By geography, Asia-Pacific commanded 53.79% of the metal-air battery market in 2025, whereas North America is expected to post the strongest 14.08% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Metal-Air Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advances In Rechargeable Zinc-Air And Lithium-Air Chemistries | +2.8% | Global with strong activity in China, South Korea, Europe, and North America | Medium term (2-4 years) |

| Rapid Electric-Vehicle Adoption Requiring Ultra-High Energy Density Packs | +2.5% | Asia-Pacific core with spillover into North America and Europe | Short term (≤ 2 years) |

| Declining Zinc And Aluminum Prices Versus Lithium And Cobalt | +1.9% | Global, strongest in Asia-Pacific and South America | Medium term (2-4 years) |

| Government Funding For Long-Duration Storage Pilots | +2.1% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Swappable Metal-Slurry Refuel Stations For Commercial Electric-Vehicle Fleets | +1.4% | Asia-Pacific leading, pilots in North America and Europe | Long term (≥ 4 years) |

| National Defense Push For Silent, Lightweight Soldier Power | +1.0% | North America and Europe, selective uptake elsewhere | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advances in Rechargeable Zinc-Air and Lithium-Air Chemistries

Breakthrough bifunctional catalysts reported during 2025 and 2026 increased zinc-air cycle life above 10,000 hours and narrowed the voltage gap between charge and discharge. These improvements reduce thermal management loads and pave the way for secondary zinc-air packs that can rival lithium-ion on total cost in stationary storage. Research groups are also converging on solid-state electrolytes with protected lithium anodes, placing lithium-air on a credible path toward commercialization. The combined progress strengthens confidence among utilities and data-center operators that multi-day discharge solutions can meet warranty requirements, stimulating procurement pipelines.

Rapid Electric-Vehicle Adoption Requiring Ultra-High Energy Density Packs

Global electric-vehicle sales surpassed 14 million units in 2024 and continue to climb. Automakers seek chemistries delivering 500 km per charge without heavier packs. Metal-air batteries promise three-to-five-fold higher theoretical specific energy compared with lithium-ion. Memoranda of understanding between Phinergy, Hindalco, and Indian Oil target aluminum-air packs that swap aluminum plates in minutes, reshaping refueling logistics. Pilot fleets in China and India are testing range-extender modules, and regulatory incentives for zero-tailpipe emissions accelerate the timeline for commercial platforms.

Declining Zinc and Aluminum Prices Versus Lithium and Cobalt

Lithium-ion cathode metals remained volatile in 2025, with cobalt spiking to roughly USD 56,414 per tonne. Zinc and aluminum prices stayed near historical averages, bolstered by oversupply and lower energy inputs in key smelting regions. The widening cost delta increases the total cost of ownership advantage for zinc-air or aluminum-air systems in grid and backup roles. New refineries, such as Alpha HPA’s high-purity alumina facility in Australia, are expanding the supply of premium aluminum feedstock, indirectly easing input constraints for aluminum-air developers.

Government Funding for Long-Duration Storage Pilots

Public agencies in California, Germany, and Canada allocated multimillion-dollar grants to zinc- and iron-air demonstrations between 2024 and 2026. Horizon Europe funded HIPERZAB, ZABAT, and HEMZAB to derisk rechargeable zinc-air manufacturing, while the California Energy Commission backed EnZinc and e-Zinc. These initiatives bridge laboratory innovations and commercial deployment, as evidenced by Form Energy’s aggregate 75 GWh project backlog.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Cycle Life Compared With Mature Lithium-Ion Chemistries | -1.7% | Global, with higher impact where daily cycling is essential | Short term (≤ 2 years) |

| Air-Cathode Carbon Dioxide Poisoning And Catalyst Degradation | -1.3% | Global, most acute in regions with elevated atmospheric CO₂ or industrial pollution | Medium term (2-4 years) |

| Immature Large-Scale Manufacturing Supply Chain | -1.0% | Global, but especially constraining in North America and Europe where gigawatt-hour facilities are still ramping | Medium term (2-4 years) |

| Competition For Decarbonized High-Purity Aluminum Feedstock | -0.8% | North America, Canada, and Europe where inert-anode smelter pilots tighten premium aluminum supply | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Cycle Life Compared with Mature Lithium-Ion Chemistries

Laboratory iron-air systems have logged up to 1,696 hours, and rechargeable zinc-air cells now exceed 10,000 hours in the best cases, yet both remain below lithium-ion norms of 3,000-5,000 cycles. Daily-cycling applications, such as frequency regulation or passenger vehicles, therefore still default to lithium-ion. Form Energy positions iron-air for 100-hour discharge at weekly or monthly cycling intervals, sidestepping the heaviest duty profiles. Continued advances in electrolyte carbonation suppression and dendrite control remain prerequisites for broader deployment.

Air-Cathode Carbon Dioxide Poisoning and Catalyst Degradation

Ambient CO₂ reacts with alkaline electrolytes to form carbonates that block active sites on the air cathode. Recent dual-cathode and CO₂-tolerant electrolyte designs dilute the impact, yet they add engineering complexity and cost. Urban regions with poor air quality face faster performance decay, limiting use cases unless operators install scrubbing modules. Horizon Europe projects are pursuing carbonate-resistant catalyst coatings, but commercialization is unlikely before 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Metal Type: Iron-Air Gains Momentum on Long-Duration Demand

Zinc-air batteries are projected to retain a 55.47% share of the metal-air battery market in 2025, primarily due to their continued use in hearing aids and medical electronics, which rely on these batteries for their dependable performance as primary cells. The iron-air segment, supported by Form Energy’s extensive multiproject pipeline, is expected to gain a larger share of the metal-air battery market. This segment is expected to register the highest compound annual growth rate (CAGR) of 13.86% during the forecast period of 2026-2031, driven by increasing adoption in various applications.[1] Form Energy, “Form Energy Project Portfolio,” formenergy.com

The growing number of multi-day discharge contracts in grid balancing and data center backup operations underscores the economic viability of iron-air batteries. These batteries are particularly suited for applications where trade-offs between cycle life and round-trip efficiency are acceptable in exchange for a lower cost per stored kilowatt-hour. Concurrently, aluminum-air battery developers are capitalizing on the abundance of aluminum feedstock and the ability to quickly swap metal plates. This approach addresses critical concerns such as range anxiety and refueling downtime, especially in commercial fleet operations. On the other hand, while lithium-air battery technology has shown progress in solid-state prototype development, its mainstream adoption remains outside the current forecast window due to its early-stage nature and ongoing challenges in commercialization.

By Battery Type: Secondary Chemistries Accelerate on Enhanced Catalysts

Primary cells accounted for 60.19% of the metal-air battery market in 2025, driven by their established use in healthcare devices, such as hearing aids, and consumer electronics. These cells continue to dominate due to their reliability and cost-effectiveness in applications requiring consistent performance. Meanwhile, advancements in bifunctional catalysts have significantly extended the lifespan of secondary zinc-air batteries, enabling them to operate for nearly 10,000 hours. This development has opened up new opportunities for their use in stationary energy storage systems and mobility applications, contributing to a projected 13.92% compound annual growth rate (CAGR) for rechargeable zinc-air batteries during the forecast period.

Established players like Duracell, Panasonic, and GP Batteries maintain their stronghold in the button-cell segment, leveraging their extensive distribution networks and brand recognition. However, emerging companies such as EnZinc and Zinc8 are making strides toward scaling modular zinc-air battery packs for applications including community microgrids and commercial buildings.[2]EnZinc, “EnZinc Secures California Energy Commission Grant,” enzinc.com The shift in the metal-air battery market toward secondary configurations is expected to accelerate as manufacturing capacities in regions like the United States and Europe expand to gigawatt-hour annual output levels, further driving innovation and adoption in this segment.

By Voltage: High-Voltage Architectures Lead Utility Uptake

Low-voltage products below 12 V maintained a 51.22% share in 2025, primarily due to the continued dominance of hearing-aid batteries in this segment. These products cater to the specific needs of medical devices and other low-power applications, ensuring their sustained market presence. However, high-voltage strings above 36 V are projected to grow the fastest, with a 13.81% CAGR, driven by increasing adoption in grid-scale energy storage systems and traction applications. Companies like Form Energy are leveraging advancements in iron-air technology to string together thousands of cells, achieving megawatt-class stack voltages. These stacks can directly interconnect with medium-voltage transformers, significantly reducing the need for additional balance-of-plant hardware, thereby improving overall system efficiency and cost-effectiveness.

In the automotive sector, aluminum-air battery packs are being designed for 400-V architectures, aligning with the voltage requirements of existing electric vehicle drivetrains. This compatibility makes them a promising solution for commercial fleet applications. Additionally, research groups have successfully demonstrated dual-cathode zinc-air modules capable of sustaining nearly 92% round-trip efficiency at elevated voltages. These advancements are encouraging original equipment manufacturers (OEMs) to initiate trial projects to further explore the potential of zinc-air technology in high-voltage applications. Such developments are expected to drive innovation and adoption across various sectors, contributing to the overall growth of the metal-air battery market.

By Application: Stationary Storage Outpaces Mobility Use Cases

Electric mobility accounted for 48.53% of 2025 revenue, yet utilities and data centers drove the highest 14.04% CAGR outlook for stationary installations. The increasing adoption of renewable energy sources, such as solar and wind, has created a growing need for long-duration energy storage solutions. Metal-air batteries, with their ability to provide extended discharge durations, are well-suited to address these challenges. Long-duration discharge aligns with renewable integration requirements and avoids the degraded round-trip efficiency penalty that fast-cycling imposes on metal-air chemistries. Form Energy's March 2026 agreement with Crusoe for 12 gigawatt-hours of iron-air batteries to support artificial intelligence data centers exemplifies how stationary storage is transitioning from pilot projects to commercial-scale deployments, with deliveries beginning in 2027.[3]Form Energy, “Form Energy and Crusoe Agreement,” formenergy.com

Utility firms in California and Minnesota, hyperscale data-center operators, and independent power producers have queued multi-hundred-megawatt-hour procurements to meet the rising demand for reliable and efficient energy storage systems. Additionally, military programs are contributing incremental demand for lightweight, silent field systems, which are essential for tactical operations. These military applications complement civilian market growth without significantly altering the total addressable volume, further solidifying the role of metal-air batteries across diverse sectors.

Geography Analysis

Asia-Pacific accounted for 53.79% of the 2025 metal-air battery market, driven by China’s extensive manufacturing capabilities, India’s strategic aluminum-air collaborations, and Japan’s advancements in catalyst science. China is advancing battery-swapping infrastructure through CATL's Choco-Swap ecosystem, which launched in December 2024 with plans to reach 1,000 stations by 2025 and a mid-term target of 10,000 stations, creating a template for metal-slurry refueling systems applicable to aluminum-air and zinc-air batteries.[4]Contemporary Amperex Technology Co. Limited, “CATL Launches Battery Swap Ecosystem,” catl.com The region benefits from policies that promote local supply chain development and ambitious transportation electrification goals, creating a conducive environment for market growth. Additionally, the presence of key players and ongoing investments in research and development further solidify Asia-Pacific's dominance in the market.

North America is projected to exhibit the highest 14.08% forecast CAGR for 2026-2031. This growth is supported by state-level mandates for long-duration energy storage, funding initiatives from the Department of Energy, and the establishment of Form Energy’s manufacturing facility in West Virginia. These factors contribute to a robust domestic ecosystem that spans from foundational research to large-scale field deployment. Furthermore, Canada’s focus on low-carbon aluminum production through the ELYSIS venture enhances the region’s feedstock sustainability, providing additional support for market expansion.

Europe remains committed to fostering academic-industry collaborations under the Horizon Europe program, allocating EUR 15 million (approximately USD 16.2 million) toward the commercialization of zinc-air batteries. National grid operators in countries like Germany and the United Kingdom are increasingly incorporating multi-day storage solutions into capacity auctions. This strategic focus positions Europe for a significant surge in demand in the future, contingent on achieving key demonstration milestones. The region’s emphasis on innovation and regulatory support continues to drive advancements in metal-air battery technologies.

Competitive Landscape

The metal-air battery market remains moderately fragmented. In the primary-cell niche, Duracell, Panasonic, and Maxell maintain a stronghold on pricing power, primarily due to their established brand loyalty in the medical device sector. These companies continue to dominate the market by offering reliable, efficient solutions tailored to the needs of the medical electronics industry. In the rechargeable and long-duration segments, Form Energy leads the market with over 75 GWh under contract, showcasing its dominance in the sector. Phinergy and Hindalco have established a strong presence in the aluminum-air battery route, while EnZinc and e-Zinc are making significant strides in zinc-air grid modules, further diversifying the competitive landscape.

Strategic partnerships play a pivotal role in scaling operations and driving innovation. For instance, Phinergy’s collaborations with Hindalco and Indian Oil have been instrumental in anchoring domestic metal sourcing and streamlining refueling logistics, ensuring a robust supply chain. Similarly, e-Zinc has partnered with Sandia National Laboratories to expedite the validation of advanced electrode technologies, highlighting the importance of research and development in maintaining a competitive edge. Emerging competitors in the market are focusing on enhancing air-cathode durability, developing proprietary electrolyte blends, and adopting capital-light electrode fabrication methods to reduce costs and improve efficiency.

However, the market faces several entry barriers, including the need for proprietary catalyst intellectual property, expertise in large-format cell assembly, and the establishment of efficient recycling or metal plate return systems. Companies that successfully secure low-carbon metal supplies or license CO₂-resistant air cathodes are expected to gain a competitive advantage. These advancements will likely enable them to achieve higher scores in public tenders for long-duration storage projects, creating a positive feedback loop that drives economies of scale and further market growth.

Metal-Air Battery Industry Leaders

Phinergy Ltd.

NantEnergy Inc.

Log9 Materials Scientific Private Limited

Form Energy, Inc.

Abound Energy, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Form Energy and Crusoe sealed a 12 GWh contract for an iron-air battery to back artificial-intelligence data centers, with production slated for the West Virginia facility.

- March 2026: Nth Cycle signed a 10-year USD 1.1 billion mixed-hydroxide precipitate offtake agreement with Trafigura to process 12,000 t of battery black mass annually.

- March 2026: Qiyuan Green Power confirmed 1,900 automated battery swaps for Rio Tinto’s Oyu Tolgoi mine haul trucks between Dec 2025 and Feb 2026, cutting 720 t of CO₂.

- February 2026: NEO Battery Materials, Korea Zinc, and Taesung agreed to commercialize composite copper collector foils for drone and micromobility battery packs by year-end 2026.

Global Metal-Air Battery Market Report Scope

The metal-air battery market is the global industry focused on the development, production, and commercialization of batteries that generate electricity through the electrochemical reaction between a metal (such as zinc, aluminum, lithium, or iron) and oxygen from ambient air. These batteries are characterized by their high theoretical energy density, lightweight design, and potential for cost efficiency, making them suitable for a wide range of applications, including electric vehicles, stationary energy storage systems, military and defense electronics, and consumer and medical devices.

The Metal-Air Battery Market Report is Segmented by Metal Type (Zinc-air, Aluminum-air, Lithium-air, Iron-air, and Other Metal Type), Battery Type (Primary, and Secondary), Voltage (Low, Medium, and High), Application (Electric Vehicles, Stationary Energy Storage, Military and Defence Electronics, Consumer and Medical Electronics, and Other Application), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Zinc-air |

| Aluminum-air |

| Lithium-air |

| Iron-air |

| Other Metal Type |

| Primary (Non-rechargeable) |

| Secondary (Rechargeable) |

| Low (less than 12 V) |

| Medium (12-36 V) |

| High (greater than 36 V) |

| Electric Vehicles |

| Stationary Energy Storage |

| Military and Defence Electronics |

| Consumer and Medical Electronics |

| Other Application |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Metal Type | Zinc-air | |

| Aluminum-air | ||

| Lithium-air | ||

| Iron-air | ||

| Other Metal Type | ||

| By Battery Type | Primary (Non-rechargeable) | |

| Secondary (Rechargeable) | ||

| By Voltage | Low (less than 12 V) | |

| Medium (12-36 V) | ||

| High (greater than 36 V) | ||

| By Application | Electric Vehicles | |

| Stationary Energy Storage | ||

| Military and Defence Electronics | ||

| Consumer and Medical Electronics | ||

| Other Application | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the metal-air battery market by 2031?

The metal-air battery market size is forecast to reach USD 1.53 billion by 2031, reflecting a CAGR of 13.3% from 2026, according to Mordor Intelligence.

Which metal type is expanding fastest in commercial deployments?

Iron-air systems lead growth at a forecast 13.86% CAGR for 2026-2031, driven by multi-day storage contracts such as Form Energys backlog, Mordor Intelligence reports.

How large was the zinc-air share of the market in 2025?

Zinc-air accounted for 55.47% of the metal-air battery market share in 2025, based on Mordor Intelligence findings.

Which geographic region will see the highest growth rate through 2031?

North America is expected to post a 14.08% CAGR during 2026-2031 as new plants and public funding accelerate adoption, according to Mordor Intelligence.

What major barrier limits broader electric-vehicle use of metal-air batteries?

Shorter cycle life compared with lithium-ion remains the primary hurdle, although recent catalyst advances have extended zinc-air lifespans to over 10,000 hours in laboratory tests.

Page last updated on: