Banknotes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.21 Trillion |

| Market Size (2031) | USD 11.27 Trillion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

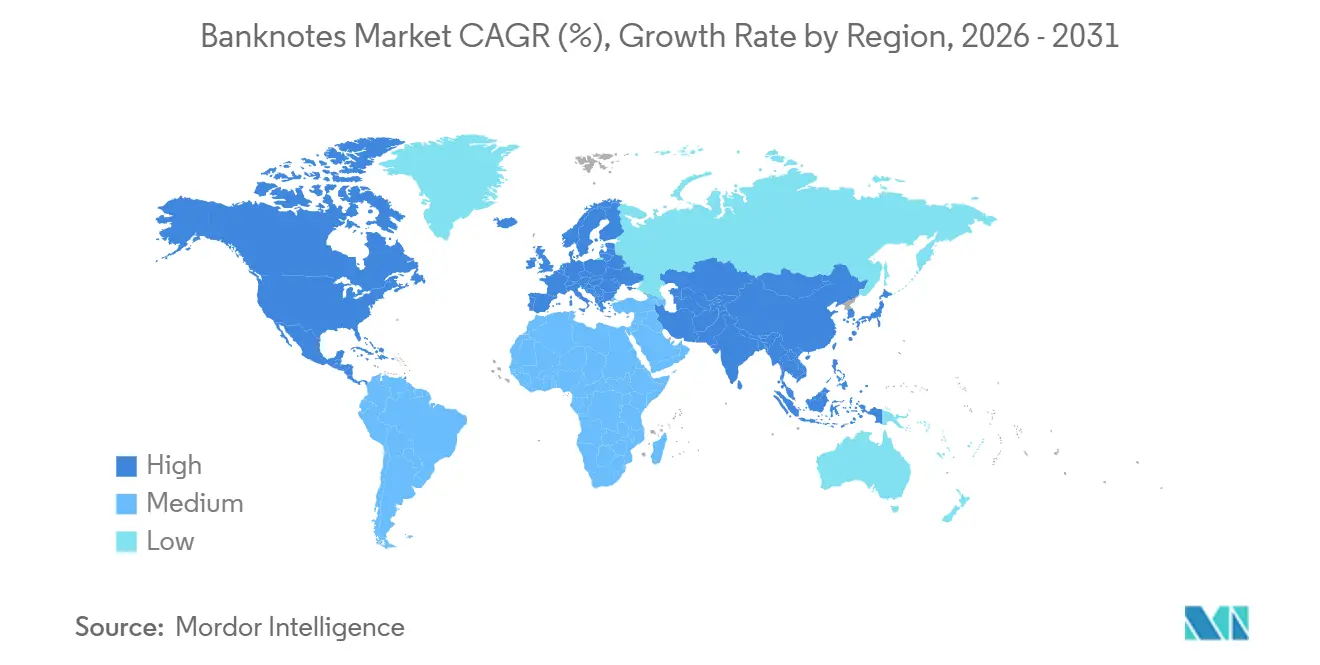

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

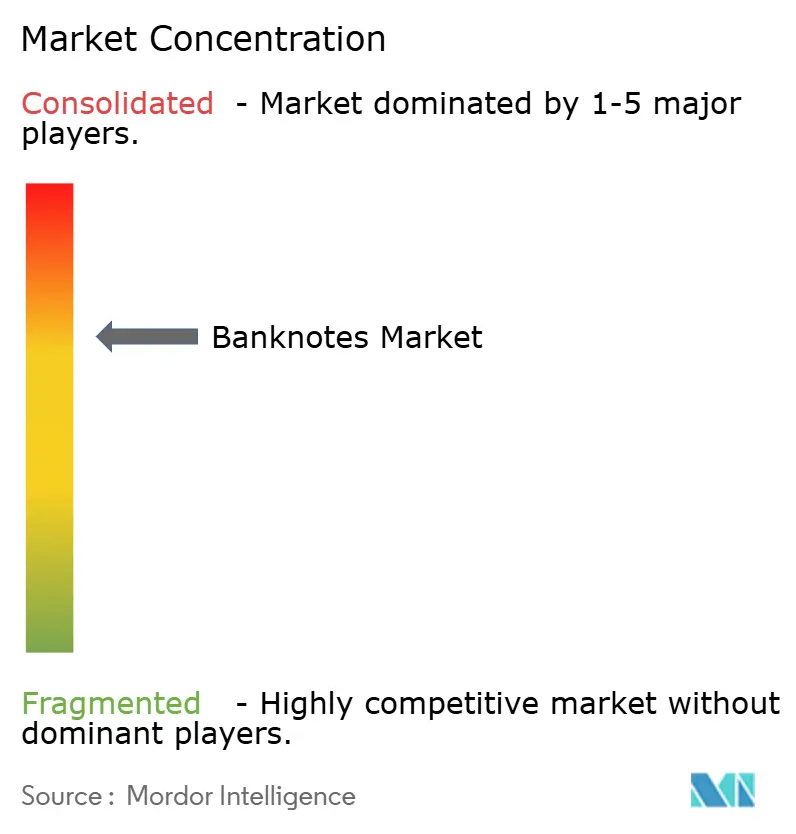

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Banknotes Market Analysis by Mordor Intelligence

The Banknotes Market size was valued at USD 8.79 trillion in 2025 and is estimated to grow from USD 9.21 trillion in 2026 to reach USD 11.27 trillion by 2031, at a CAGR of 4.12% during the forecast period (2026-2031).

The banknotes market continues to expand, even as digital payments grow, because physical currency still serves as a fallback store of value and an offline payment tool in many economies. A large part of the banknotes market demand also comes from informal and cash-reliant activity in emerging countries, where digital access is still uneven, and the Central Banking Currency Benchmarks 2024 survey showed that the median central bank expected cash in circulation to rise by 5% in 2024, with reported values up 8.6% and volumes up 2% across surveyed jurisdictions. In the banknotes market, competition remains strongest around long-term sovereign printing contracts and proprietary substrate and security-feature supply, where a small group of established firms still shapes design and production choices. The banknotes market is also being supported by a new upgrade cycle focused on machine-readable features, as banks and cash recyclers need notes that can withstand high-speed authentication and sorting. At the same time, the banknotes market faces pressure from lower transactional print demand in advanced economies, high capital costs associated with polymer conversion, and procurement uncertainty linked to digital currency experiments and sustainability requirements.

Key Report Takeaways

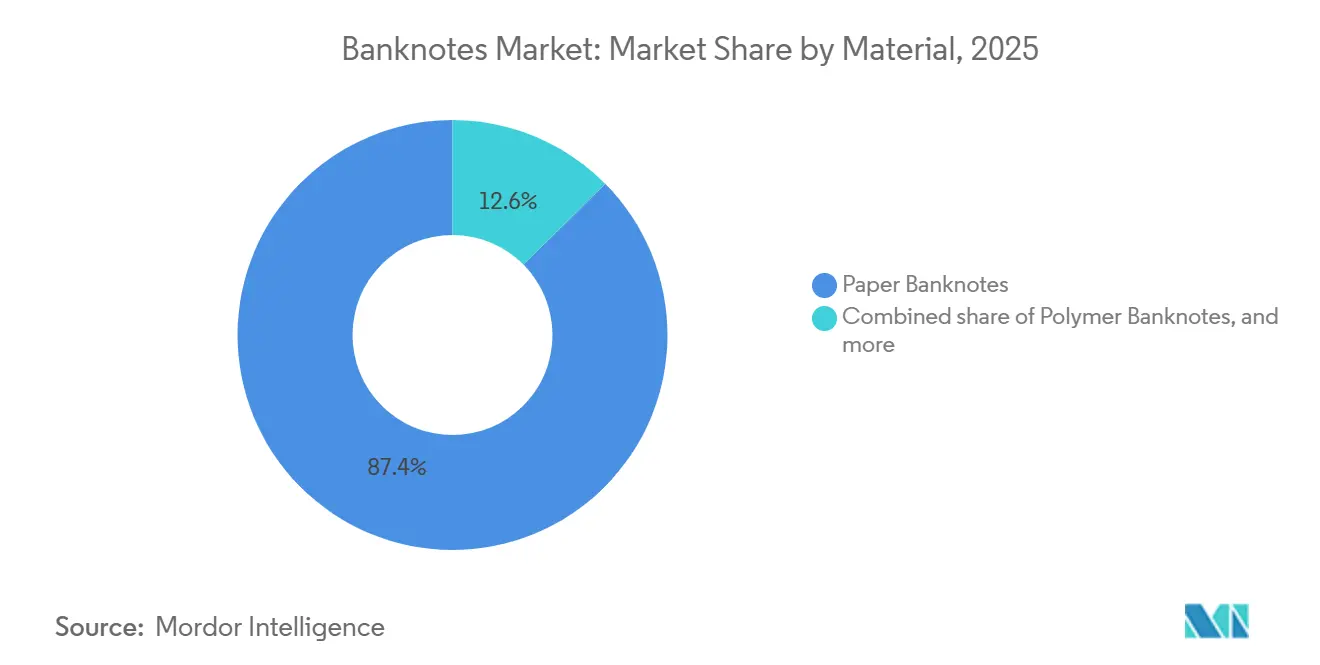

- By material, paper captured 87.4% of the banknotes market share in 2025, while polymer is projected to grow at 12.2% CAGR through 2031.

- By security feature, substrate-embedded features accounted for 46.7% of the banknotes market share in 2025, while optical variable devices are projected to grow at a 7.7% CAGR through 2031.

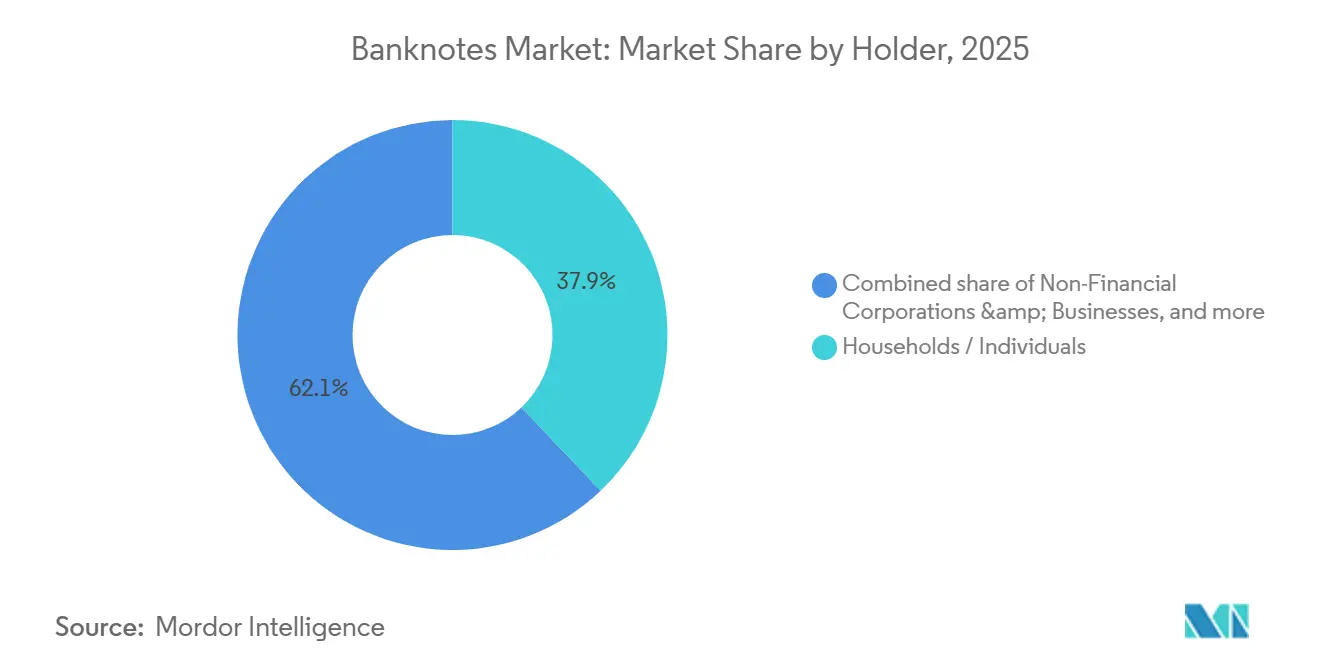

- By holder, households and individuals held 37.9% of the banknotes market share in 2025, while non-financial corporations and businesses are projected to grow at 5.7% CAGR through 2031.

- By geography, North America held 36.2% of the banknotes market share in 2025, while Asia-Pacific is projected to grow at 6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Banknotes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Anti-Counterfeit Currency Upgrades | +1.0% | Global, with early intensity in South Asia and Sub-Saharan Africa | Medium term (2-4 years) |

| Expansion of Cash Circulation in Informal and Emerging Economies | +0.8% | Asia-Pacific core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Shift Toward Polymer and Hybrid Substrates for Longer Note Life | +0.6% | Global, led by Asia-Pacific and MEA adopters | Medium term (2-4 years) |

| Central Bank Redesign and Note Replacement Cycles | +0.5% | Global, concentrated in Europe and North America | Short term (≤ 2 years) |

| Machine-Readable Features for Cash Automation and Sorting | +0.3% | North America and Europe | Medium term (2-4 years) |

| Low-Visibility Authentication for High-Denomination and Special Issue Notes | +0.2% | Global, focus on G20 and high-denomination series | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need for Anti-Counterfeit Currency Upgrades

The banknotes market is seeing stronger demand for security upgrades in countries where note circulation is still rising quickly. India’s Reserve Bank data, as cited in the source draft, showed that detected fake 500 rupee notes increased 20.5% year over year to 141,907 pieces in FY26, while total banknote volumes in circulation increased 10.5% in the same period[1]CNBCTV18.COM Fake ₹500 notes rise over 20% in FY26 as cash circulation grows: RBI - CNBC TV18. The banknotes market is also being shaped by the fact that authentication no longer stops at central bank vaults, as ATMs and cash recyclers now verify notes at the teller and branch levels. That shift is shortening the effective security refresh cycle in high-volume markets, as older feature sets are under greater stress from both counterfeiting and machine handling. ECB counterfeit authentication standards and fitness protocols also continue to influence procurement specifications beyond Europe, which is pushing more central banks toward layered, machine-verifiable note security.

Expansion of Cash Circulation in Informal and Emerging Economies

The banknotes market is still supported by rising cash holdings in emerging economies, where notes serve both transactional and precautionary needs. India’s currency in circulation reached INR 41.68 trillion (approximately USD 496 billion) in FY26, even as UPI volumes remained very high, indicating that cash and digital payments serve different roles rather than replacing one another on a one-for-one basis. The SBI research note cited in the source draft also found that the gap between ATM withdrawals and currency in circulation widened to INR 9,127 per capita in FY26 from INR 1,804 in FY24, suggesting stronger cash held outside the banking system as emergency reserves[2]BUSINESS-STANDARD.COM Gap between ATM withdrawals and cash in circulation widens, says SBI | Finance News - Business Standard. The BIS reported that adult digital payment use in emerging market and developing economies rose from 35% to 57% between 2014 and 2021, yet cash demand also increased during that period. The banknotes market, therefore, remains linked to broad financial inclusion gaps and to the continued role of physical notes as the only liquid financial asset for many users. A peer-reviewed study in Economic Expressions Letters also supported the connection between informality and sustained demand for smaller note denominations.

Shift Toward Polymer and Hybrid Substrates for Longer Note Life

The banknotes market is moving steadily toward polymer and hybrid materials because the cost case is now more established. Central Banking’s 2024 survey found that polymer substrates represented 23.3% of printed banknotes across 30 jurisdictions, and many paper-only issuers had already identified polymer adoption as a policy objective. Costa Rica’s central bank data, as cited in the source draft, showed lifecycle savings of 74% per note for the CRC 1,000 polymer series against cotton equivalents, supported by a service life that was 5 times longer[3]DELFINO.CR Billetes de polímeros: una ventaja ideal para la Costa Rica verde. The banknotes market is also shifting because suppliers are addressing sustainability concerns that once slowed polymer adoption, including reduced-plastic-content hybrid substrates and bio-renewable polymer inputs. G+D said its Hybrid Green Banknotes substrate reduced plastic content by 86% versus standard polymer while maintaining comparable durability. IACA’s 2026 award for CCL Secure’s GUARDIAN ENVIRO further showed that recyclability and feedstock provenance are becoming part of mainstream central bank procurement evaluation.

Central Bank Redesign and Note Replacement Cycles

The banknotes market continues to depend on redesign cycles that trigger large, visible sovereign procurement waves. The ECB selected 2 design themes for the next euro series in January 2025, and the timeline cited in the source draft points to a final design decision by the end of 2026, with circulation starting progressively from 2028[4]ECB.EUROPA.EU https://www.ecb.europa.eu/euro/banknotes/future_banknotes/html/index.en.html. The Bank of England’s tender for a contract running from March 2028 to February 2038, with a possible extension to 2041, showed how a single sovereign program can support supplier utilization for a decade. The banknotes market is also being shaped by redesign programs that are increasingly phased by denomination over several years rather than executed in a single short issuance event. De La Rue reported an order book of GBP 338 million (approximately USD 433 million) in November 2024, signaling a heavy pipeline of overlapping redesign and supply programs moving into the 2026 to 2028 delivery window. This creates steadier demand visibility for large suppliers, but it also increases pressure on companies that do not control enough substrate and print capacity in advance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Substitution by Digital Payments and Card Usage | -1.2% | North America, Western Europe, East Asia | Long term (≥ 4 years) |

| High Capital Intensity of Secure Printing and Substrate Conversion | -0.7% | Global, concentrated in lower-income sovereign printers | Medium term (2-4 years) |

| Longer Procurement Cycles and Sovereign Approval Dependencies | -0.4% | Global | Medium term (2-4 years) |

| Sustainability Pressure on Cotton-Based and Security-Coated Note Waste Streams | -0.2% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Substitution by Digital Payments and Card Usage

The banknotes market is under pressure in advanced economies, where digital channels are reducing cash transactions. The Federal Reserve’s CY 2026 print order of 3.8 billion to 5.1 billion notes was 8.2% to 13.3% below the CY 2025 order range, which reflected lower replenishment needs in the United States for lower-value notes that now circulate less intensively. The banknotes market is still growing in value terms, but the volume mix is changing because the denominations most exposed to digital substitution are also the highest in terms of piece count. That creates pressure on print economics even when higher-value denominations remain in demand for reserve holding and international use. The IMF also warned that even unsuccessful CBDC pilots can unsettle existing cash systems through expectation effects, which adds another layer of uncertainty to long-cycle procurement planning.

High Capital Intensity of Secure Printing and Substrate Conversion

The banknotes market still faces a major structural barrier: the high cost of converting legacy paper-printing infrastructure to polymer-capable operations. The source draft stated that a full-scale sovereign conversion can require investments of USD 100 million or more across inking, drying, and lamination systems, and it also noted that low-volume central banks may face payback periods that stretch beyond 15 years. Pakistan’s Security Papers Limited awarded a paper-machine upgrade to G+D worth EUR 8.297 million (USD 9 million) in 2024, simply to modernize substrate processing capacity ahead of a new design series. The banknotes market also becomes more concentrated when only a few large suppliers can finance these transitions, raising procurement governance issues in some countries. Kenya’s five-year single-sourced contract with G+D, valued at KES 14.2 billion (USD 109 million) in the source draft, became the subject of a Senate inquiry in 2025, which showed how capital intensity and vendor concentration can lengthen approval cycles and increase procurement scrutiny.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Paper Dominates While Polymer Reshapes Economics

Paper accounted for 87.4% of the banknotes market size in 2025, and that lead reflected the very large installed base of cotton-fiber printing infrastructure across sovereign printers worldwide. The banknotes market still relies heavily on paper because that installed base represents decades of sunk capital, trained labor, and procurement processes that cannot be changed quickly. Even so, the paper’s leading position is increasingly tied to legacy capacity rather than to stronger forward economics. The source draft noted that paper share is already declining in regions where polymer pilots have been completed and where lifecycle savings have been verified. That means the current balance in the banknotes market remains stable in the near term, but it is no longer as secure over the full forecast period.

Polymer is projected to expand at a 12.2% CAGR from 2026 to 2031, making it the fastest-growing material segment in the banknotes industry and the clearest growth engine within the banknotes market. The source draft linked that growth to second-wave adoption across Southeast Asia, Africa, and Latin America, where procurement risk and unit-cost barriers are falling. It also cited the Bangko Sentral ng Pilipinas completing its first full polymer series across all major denominations in December 2024 using CCL Secure’s GUARDIAN substrate. Fiji’s launch of its first fully polymer series in December 2025 further showed that smaller issuers are now moving beyond trials and toward full adoption. Hybrid formats also remain strategically important because they allow central banks to improve durability and sustainability without committing to a full polymer switch immediately.

By Security Feature: Substrate-Embedded Entrenched, OVDs Gain Momentum

Substrate-embedded features accounted for 46.7% of the segment in 2025, giving them the largest share of the banknotes market among security features. The banknotes market still relies on watermarks, security threads, and fiber inclusions because these elements are embedded in the note architecture and tied to long-term supplier contracts. Those contracts often run for 5 to 10 years per denomination, making rapid switching difficult even when newer technologies offer better public authentication performance. This is why substrate-embedded features remain deeply entrenched across the banknotes market, especially in long-running sovereign series. Their position is less about novelty and more about procurement continuity, proven reliability, and compatibility with existing print lines.

Optical variable devices are projected to grow at a 7.7% CAGR from 2026 to 2031, and that pace indicates where the banknotes market is allocating its next feature investments. Central banks are favoring Level 1 public-authentication tools for higher denominations because they provide immediate visual confirmation without specialized equipment. The source draft noted that G+D launched its RollingStar Venus thread in 2025 and secured several multi-year contracts tied to nanostructure-based color effects. It also cited Authentix’s December 2025 launch of PICO secure, described as the first production-qualified nano-optic plasmonic OVD for currency. Machine-readable and tactile printed elements still matter, but the growth curve within the banknotes market is shifting toward more visible and harder-to-copy optical effects that work across both paper and polymer formats.

By Holder: Households Anchor Demand While Corporates Lift Growth

Households and individuals accounted for 37.9% of the banknotes market in 2025, making them the largest holder group. That lead came from precautionary cash holding rather than from pure day-to-day transaction use, and the source draft repeatedly tied this behavior to resilience during crises and payment disruption. The ECB’s 2025 bulletin emphasized that the tangibility, offline resilience, and broad acceptance of cash become more important during periods of disruption. Several European and national authorities also continued to encourage households to maintain cash reserves as part of contingency planning, which reinforced the defensive role of physical notes. This keeps household demand important even in economies where digital payment adoption is already high.

Non-financial corporations and businesses are projected to grow at a 5.7% CAGR from 2026 to 2031, making them the fastest-expanding holder segment in the banknotes market. The source draft linked this growth to retail, hospitality, transport, and agricultural supply chains in emerging economies where cash-intensive operations are still scaling faster than digital coverage. The same draft also noted that this demand is not only about higher note volumes, but also about a greater need for mid-denomination notes that feature richer security features. Brazil’s central bank commentary in January 2025 supported the idea that cash is increasingly held as a store of value rather than being used only for daily circulation. Financial institutions and the public sector remain relevant in the banknotes market as well, especially where cross-border reserve holdings extend demand for major currencies far beyond their home regions.

Geography Analysis

North America held 36.2% of the banknotes market share in 2025, making it the largest regional market. That scale continued to rest on the role of the United States dollar in global reserves and trade settlement rather than on domestic transactional cash growth alone. The Federal Reserve’s CY 2026 print order covered 3.8 billion to 5.1 billion notes with a value range of USD 108.9 billion to USD 139.6 billion, and the USD 100 denomination alone accounted for USD 75.8 billion to USD 87.7 billion of that value. The source draft said this mix pointed to a currency stack increasingly managed for store-of-value and international reserve use. North America also remains relevant to the banknotes market because Canada’s long-term sovereign supply model supports a stable baseline, while Mexico continues to issue polymer denominations with its own security and procurement path.

Asia-Pacific is forecast to grow at a 6% CAGR from 2026 to 2031, making it the fastest-growing regional market for banknotes. The source draft linked this growth to South and Southeast Asia, where circulation growth and polymer transition programs are occurring simultaneously. It noted that India’s currency in circulation increased 11.9% in FY26 to INR 41.68 trillion, approximately USD 496 billion, even as digital payment activity remained at record levels. It also cited CCL Secure’s supply agreement with the State Bank of Vietnam for GUARDIAN polymer substrate for the VND 200,000 denomination in March 2026, alongside ongoing polymer use in the Philippines, Indonesia, and Thailand. The source draft further pointed to China Banknote Printing and Minting Corporation’s paper-plastic composite substrate with translucent windows and flexible OLED elements as a sign that state-owned capacity in Asia-Pacific is building its own feature architecture base.

Europe remains one of the most important strategic regions in the banknotes market because the next euro redesign program creates one of the largest visible procurement pipelines in the forecast period. The source draft also linked this to the Bank of England’s long-duration banknotes tender, which keeps European sovereign procurement at the center of supplier capacity decisions through the end of the period. The Middle East and Africa are active issuance zones as well, and the Central Bank of Uzbekistan signed separate memoranda with De La Rue and Oberthur Fiduciaire in April 2026 for cooperation on secure products and banknotes production. South America is also moving through a broader polymer transition, with the source draft citing Bolivia’s Series B launch in 2025 and Paraguay’s 2025 to 2029 institutional plan tied to a new banknotes family. Taken together, these regional patterns show that the banknotes market is not driven by one global trend, but by a mix of reserve currency demand, redesign cycles, and substrate modernization.

Competitive Landscape

The banknotes market is moderately concentrated at the print-contract tier, where De La Rue, Giesecke+Devrient, Oberthur Fiduciaire, Crane Currency, and several state-controlled printers still account for most sovereign volumes. The banknotes market remains difficult to enter because central bank contracts often run for 5 to 10 years and are tied to exact substrate, feature, and compliance requirements. That structure gives incumbents long revenue visibility while also making supplier switching slow and costly for issuers. The source draft cited Atlas Holdings’ USD 330 million acquisition of De La Rue in April 2025 and Crane Currency’s USD 300 million acquisition of De La Rue’s Authentication division in May 2025 as major changes to the competitive boundary between finished note printing and security features. These deals did not change end demand directly, but they did reshape how the banknotes market is organized across printing, authentication, and polymer capability.

The banknotes market is also becoming more competitive at the materials and feature layer, where proprietary technology can lock in future print choices before a central bank even awards the full production contract. De La Rue reported an order book of GBP 338 million, approximately USD 433 million, in late 2024, which showed that its refocused currency business entered 2025 with stronger visibility. G+D’s Currency Technology segment generated EUR 1,222.5 million, approximately USD 1,320 million, in 2025, while group order intake reached EUR 3,596 million and backlog rose to EUR 2,550 million. The source draft also noted G+D’s February 2026 patent filing for dual-layer luminescent banknotes features with UV-A differentiation, which fits its broader strategy of building recurring value through feature upgrades and device compatibility. In the banknotes market, that matters because future competitive advantage is no longer defined only by print capacity, but also by who controls substrate, optical effects, and machine-readable design standards.

Several white-space opportunities are shaping the next phase of the banknotes market. Eco-substrates are one of them, as CCL Secure’s GUARDIAN ENVIRO and G+D Louisenthal’s Green LongLife show how sustainability criteria are moving into central bank request-for-proposal scoring. Nano-optic security elements are another opening, with Authentix PICO secure and G+D’s Venus foil both pushing a newer class of visible feature that still lacks a single dominant scaled supplier. Format innovation is also emerging as a real competitive theme, and the source draft cited Bundesdruckerei’s STELLA concept and Covestro’s Autentium mono-polymer substrate as signs that efficiency and recyclability may become stronger purchase criteria. Smaller firms such as Spectra Systems and Landqart are gaining space where issuers want more supply security and less dependence on a single incumbent, which means the banknotes market remains concentrated, but not closed.

Banknotes Industry Leaders

De La Rue plc

Giesecke+Devrient GmbH

Crane Currency

Bundesdruckerei GmbH

Canadian Bank Note Company, Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: CCL Secure received the IACA 2026 Excellence in Currency Award for Best New Banknote Feature, Product or Process for GUARDIAN ENVIRO, its bio-renewable polymer substrate incorporating tall oil and used cooking oil inputs, signaling eco-substrate as an emerging competitive differentiator in central bank procurement evaluation.

- April 2026: The European Central Bank had decided to stop producing and issuing the 500 euro banknotes as part of the new Europa series, while the note remained legal tender and kept its value. The move was made over concerns that the high-denomination bill could facilitate illegal activities, and issuance was planned to end around late 2018 when new 100 euro and EUR 200 euro notes were introduced.

- April 2026: The Central Bank of Uzbekistan signed separate memoranda of understanding with De La Rue and Oberthur Fiduciaire at the Global Currency Forum in Antalya, formalizing cooperation on secure banknotes production and the adoption of modern printing technologies, signaling active Central Asian sovereign procurement for both companies in the near term.

- March 2026: CCL Secure announced a supply agreement with the State Bank of Vietnam for GUARDIAN polymer substrate covering the VND 200,000 denomination, extending the company's Southeast Asian polymer supply network and reinforcing GUARDIAN's position as the region's dominant polymer banknotes substrate.

Global Banknotes Market Report Scope

| Paper Banknotes |

| Polymer Banknotes |

| Hybrid Banknotes |

| Substrate-Embedded Features (watermarks, security threads, etc.) |

| Optical Variable Devices (holograms, color-shifting inks, etc.) |

| Tactile & Printed Security Features (microprinting, intaglio, etc.) |

| Machine-Readable Features (UV, IR, magnetic, etc.) |

| Households / Individuals |

| Non-Financial Corporations & Businesses |

| Financial Institutions |

| Government & Public Sector |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Material | Paper Banknotes | |

| Polymer Banknotes | ||

| Hybrid Banknotes | ||

| By Security Feature | Substrate-Embedded Features (watermarks, security threads, etc.) | |

| Optical Variable Devices (holograms, color-shifting inks, etc.) | ||

| Tactile & Printed Security Features (microprinting, intaglio, etc.) | ||

| Machine-Readable Features (UV, IR, magnetic, etc.) | ||

| By Holder | Households / Individuals | |

| Non-Financial Corporations & Businesses | ||

| Financial Institutions | ||

| Government & Public Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Singapore | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the global banknotes space?

The banknotes market size is expected to move from USD 8.79 trillion in 2025 to USD 9.21 trillion in 2026 and reach USD 11.27 trillion by 2031, at a 4.1% CAGR over 2026-2031.

Why is physical currency still growing despite digital payment adoption?

Cash still serves as an offline backup, a store of value, and a practical tool in informal and underbanked economies, which is why circulation can rise even when digital payment use also expands.

Which material segment leads and which one is growing fastest?

Paper led with 87.4% share in 2025, while polymer is projected to grow fastest at 12.2% CAGR through 2031, supported by better durability and stronger lifecycle economics.

Which security feature category is gaining the most traction?

Substrate-embedded features remained the largest at 46.7% share in 2025, but optical variable devices are growing fastest at 7.7% CAGR as issuers seek stronger public authentication and anti-counterfeit performance.

Which region offers the strongest growth outlook through 2031?

Asia-Pacific is projected to record the fastest growth at 6% CAGR, supported by circulation growth, polymer adoption, and new note technology development across South and Southeast Asia.

What are the main risks suppliers face in this space?

The biggest risks are digital substitution in mature economies, the high cost of substrate conversion, and slower sovereign approval cycles that can delay awards and raise capital exposure.

Page last updated on: