Cardless ATM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

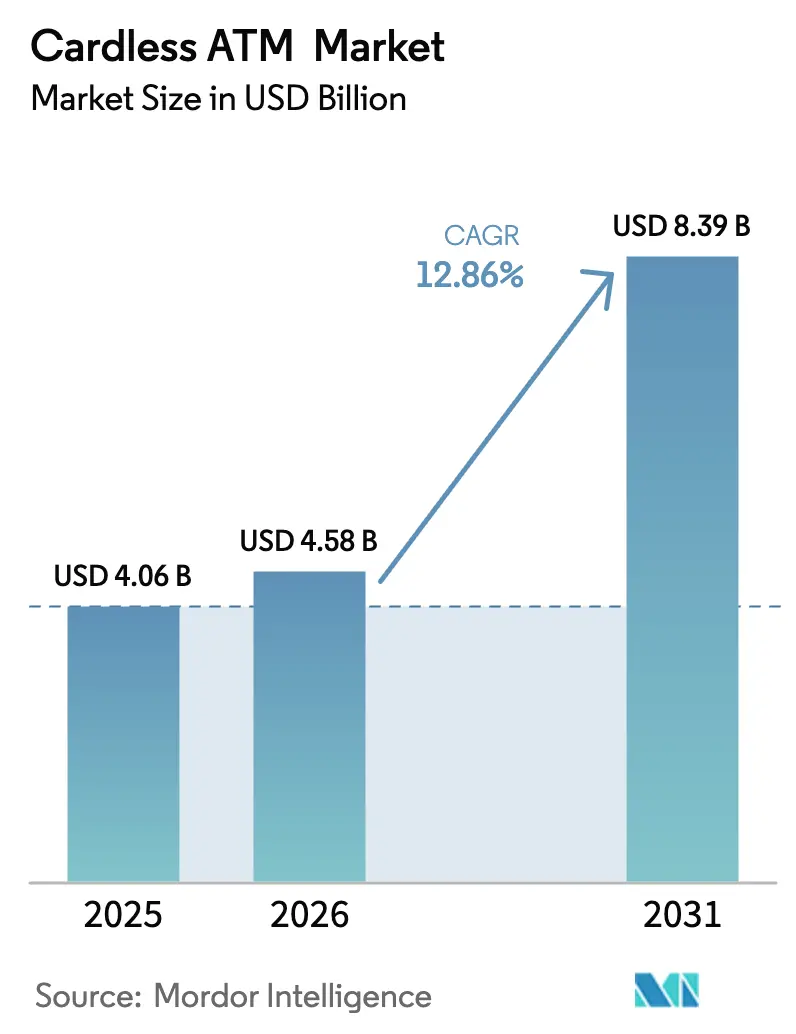

| Market Size (2026) | USD 4.58 Billion |

| Market Size (2031) | USD 8.39 Billion |

| Growth Rate (2026 - 2031) | 12.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardless ATM Market Analysis by Mordor Intelligence

The cardless ATM market size is expected to grow from USD 4.06 billion in 2025 to USD 4.58 billion in 2026 and is forecast to reach USD 8.39 billion by 2031 at 12.86% CAGR over 2026-2031. Mobile banking’s reach now exceeds 3.2 billion users, and banks view cardless functionality as a core service rather than a premium add-on. NFC remains the principal access technology, but rapid biometric adoption shows banks pivoting from proximity-based to identity-based security. Emerging “ATM-as-a-Service” partnerships between banks and white-label operators accelerate deployment while containing retrofit costs. Regionally, North America provides scale and early technology pilots, whereas Asia-Pacific’s regulatory initiatives and smartphone-first habits make it the fastest-expanding arena for the cardless ATM market.

Key Report Takeaways

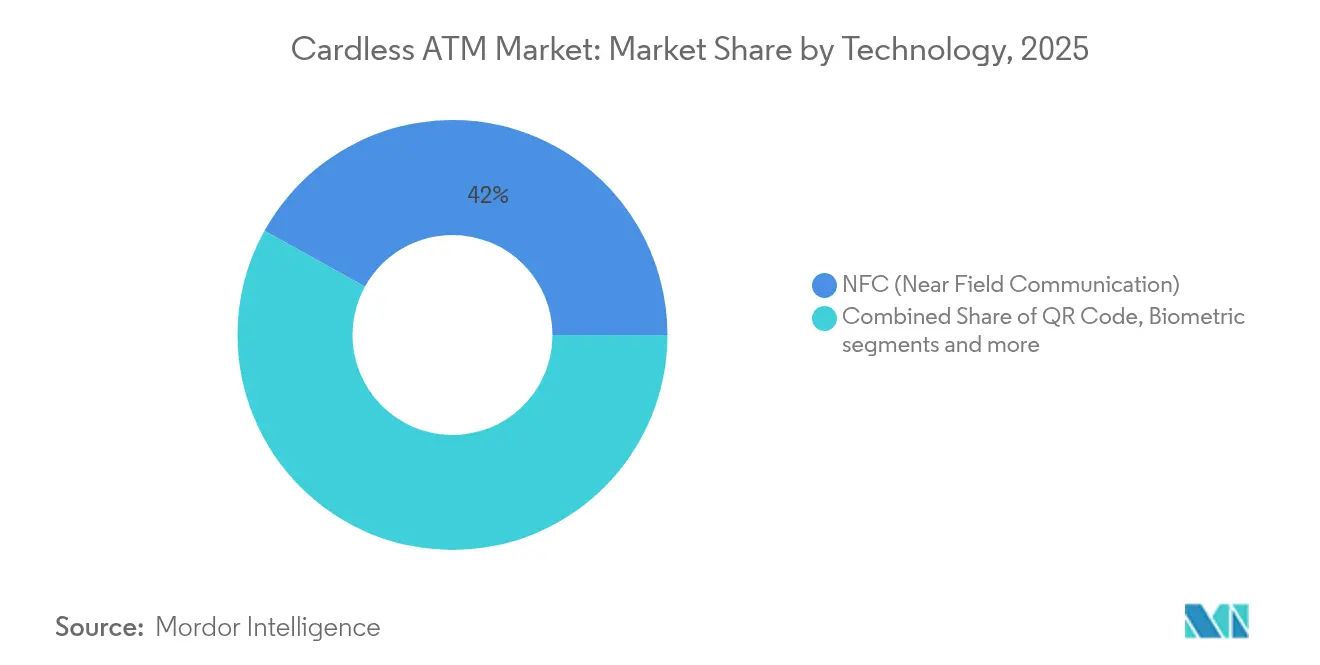

- By technology, NFC led with 41.95% of the cardless ATM market share in 2025; biometric authentication is forecast to advance at a 14.25% CAGR through 2031.

- By ATM location, on-site branch ATMs held 46.80% revenue share in 2025, while white-label and drive-through installations are set to rise at a 13.62% CAGR to 2031.

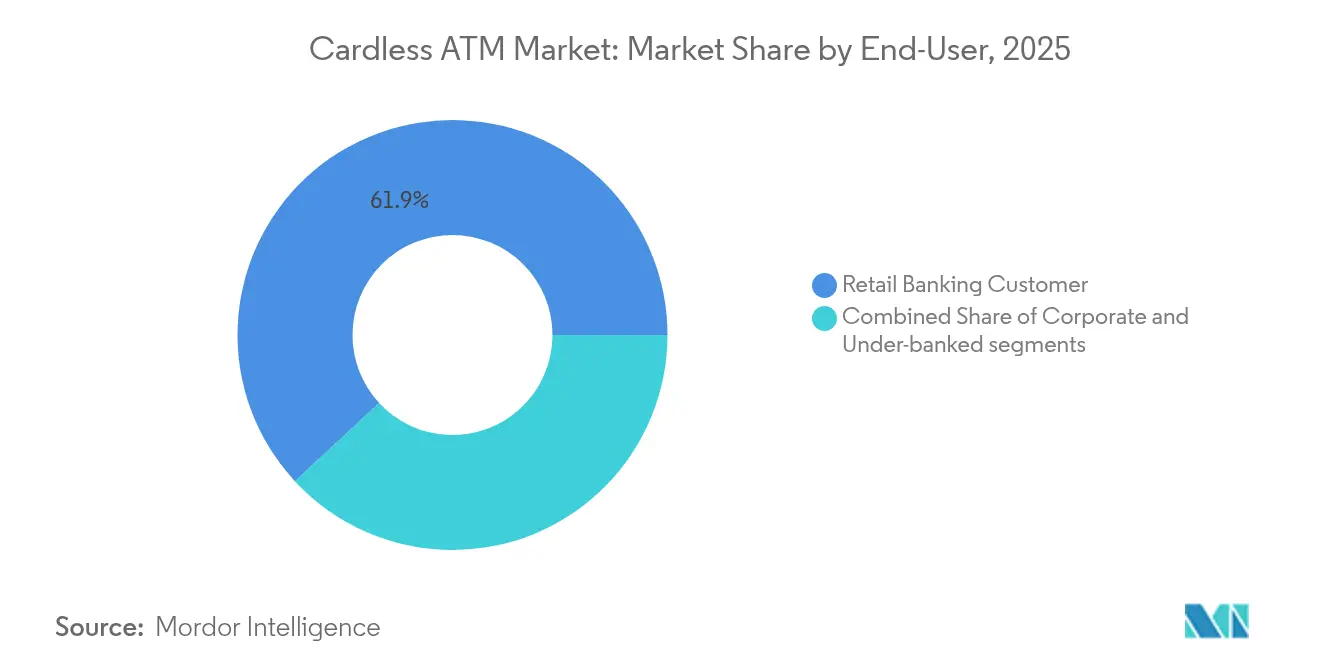

- By end-user, retail banking customers accounted for 61.90% share of the cardless ATM market size in 2025, whereas the under-banked segment is expanding at a 13.08% CAGR through 2031.

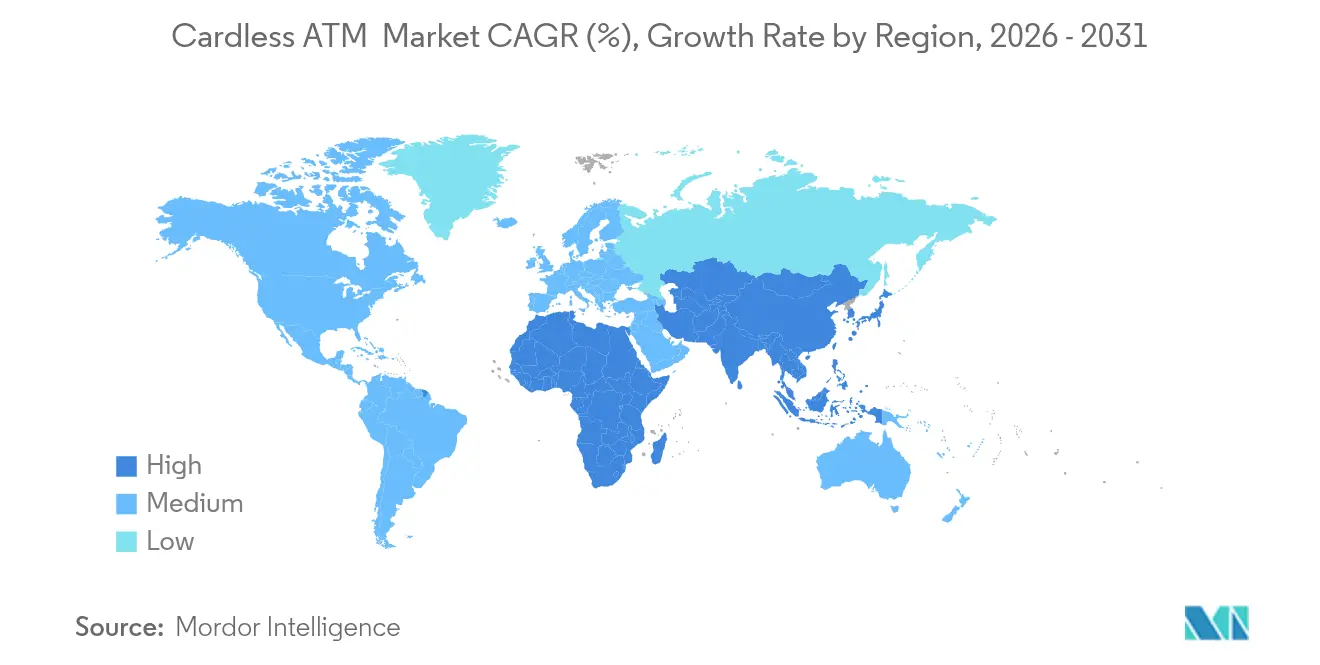

- By geography, North America commanded 33.10% of 2025 revenue, but Asia-Pacific is projected to post the quickest regional CAGR at 14.02% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardless ATM Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in mobile banking adoption | +3.3% | Global with Asia-Pacific leadership | Medium term (2–4 years) |

| Increasing demand for contactless transactions post-pandemic | +2.6% | North America & Europe; spreading globally | Short term (≤ 2 years) |

| Banks’ cost-optimization by reducing card-issuance expenses | +2.0% | Global, mainly developed markets | Long term (≥ 4 years) |

| Integration of open-banking APIs enabling third-party withdrawals | +1.3% | Europe in front; North America following | Medium term (2–4 years) |

| Regulatory push for financial inclusion via national digital IDs | +1.0% | Asia-Pacific core; MEA & Latin America emerging | Long term (≥ 4 years) |

| Rise of “ATM-as-a-Service” models for fintechs | +0.8% | North America & Europe; Asia-Pacific next | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surge in Mobile Banking Adoption

Mobile banking now reaches more than 3.2 billion users worldwide and underpins demand for cardless withdrawals. Markets with mature app ecosystems transition 40% faster toward digital cash access as banks reuse existing in-app authentication for ATM entry. Gen Z’s expectation of friction-free switching between mobile apps and physical touchpoints encourages banks to present cardless ATM entry as a baseline service. In return, institutions report shorter customer onboarding cycles and higher digital engagement. Early adopters secure a defensible lead, compelling slower banks to accelerate mobile platform upgrades to retain share in the cardless ATM market. This shift also enables banks to reduce dependency on plastic cards, aligning with broader ESG and cost-cutting goals. Mobile-first strategies are increasingly central to competitive positioning, especially in emerging markets where app-based banking leapfrogs legacy infrastructure.

Increasing Demand for Contactless Transactions Post-Pandemic

Pandemic-primed contactless habits are sticky: 29% of UK card activity in 2024 already flowed through digital wallets[1]Dentons, “UK Digital Payments Landscape 2024,” dentons.com . ATM manufacturers and banks share the goal of quicker, cleaner cash access by sidestepping card handling. Biometric authentication trims transaction time by 35%, raising throughput in busy branches. As a result, contactless infrastructure becomes a prerequisite for retention: banks lagging on cardless rollouts risk account attrition, especially in urban markets where convenience benchmarks are dictated by fintech entrants. This trend is reinforced by customer expectations for tap-to-access functionality across all service channels, not just point-of-sale. Financial institutions now view contactless readiness not only as a user convenience but as a competitive hygiene factor.

Banks’ Cost-Optimization by Reducing Card-Issuance Expenses

Physical card issuance typically costs USD 3–5 per unit. Multiplied across tens of millions of account renewals, the operational outlay steers banks toward digital credentials. Cardless withdrawals curtail replacement and logistics expenses while shrinking skimming exposure at the ATM. Institutions that embed cardless options report lower fraud remediation costs, freeing budgets for experience-focused upgrades. These savings compound under thinning margins, making cardless ATM deployment a board-level cost priority rather than a discretionary tech project. In high-volume markets, the shift also reduces pressure on contact centers by lowering the incidence of lost card reports. Some banks have even reallocated physical card budgets toward enhancing mobile security layers and geofencing capabilities. As digital-native users become the dominant customer segment, the expectation of seamless, card-free access is reshaping how institutions model their infrastructure investment returns.

Integration of Open-Banking APIs Enabling Third-Party Withdrawals

Europe’s PSD3 blueprint compels banks to publish standardized APIs, allowing licensed providers to initiate cash withdrawals on customers’ behalf. This regimen turns ATMs into open platforms rather than closed proprietary endpoints. Banks that offer rich developer documentation and granular access controls draw fintech partners who bring incremental volume. Those slow to adapt risk losing brand visibility when third-party apps aggregate ATM access under their own banners. As ATM usage becomes decoupled from direct bank interfaces, customer loyalty may shift toward the most seamless access point rather than the underlying account provider. Forward-leaning banks are already piloting API monetization models tied to ATM transactions initiated via third-party ecosystems. PSD3’s push toward interoperability positions API maturity as a key differentiator in Europe’s evolving retail banking landscape.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security concerns around mobile/biometric authentication | -1.6% | Global, privacy-sensitive regions | Short term (≤ 2 years) |

| High retrofit CAPEX for legacy ATM fleets | -1.0% | Mature markets with aging machines | Medium term (2–4 years) |

| Fragmented proprietary app standards limit interoperability | -0.8% | Global, regional differences | Long term (≥ 4 years) |

| Rural 5G/edge-compute gaps slow biometric verification | -0.5% | Emerging markets, rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Security Concerns Around Mobile/Biometric Authentication

A USD 100,000 phishing incident that hit 125 Fifth Third Bank clients in 2024 illustrated how fraudsters target mobile credential workflows. Unlike password resets, biometric leaks are permanent, so any breach dents consumer confidence far longer. Banks must layer risk scoring, device telemetry, and real-time anomaly detection around biometric flows. Investment in customer education, explaining why the same face unlock that secures a phone can safely open an ATM, becomes critical for further penetration of the cardless ATM market. Additionally, regulators are beginning to scrutinize biometric risk frameworks, urging banks to demonstrate post-breach accountability and resilience. Financial institutions that transparently disclose security protocols and offer opt-in flexibility tend to retain higher trust in biometric-enabled banking.

High Retrofit CAPEX for Legacy ATM Fleets

Upgrading an older cabinet to support NFC readers, wide-angle cameras, and secure edge processors can cost USD 30,000–40,000 per terminal[2]InformationWeek, “The Hidden Cost of ATM Upgrades,” informationweek.com . Regional banks juggling hundreds of units often stage rollouts across dense urban sites first, leaving rural machines on magnetic-stripe tech. As a result, customer journeys fragment: the same account holder experiences cardless convenience downtown yet still needs a plastic card in smaller towns. This uneven distribution slows network-wide impact on the cardless ATM market until machines cycle out naturally or banks adopt shared white-label pools. For smaller institutions, these costs compete with other digital priorities like app redesigns or core banking migrations. Public-private incentives or vendor financing programs may be necessary to bridge the rollout gap in lower-revenue geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Biometrics Move from Proof-of-Concept to Mainstream

NFC retained 41.95% of the cardless ATM market share in 2025, buoyed by universal smartphone compatibility and the ease of tapping a phone to a reader. Biometric authentication, however, is projected to clock a 14.25% CAGR through 2031, the fastest rate across technology groups. This trajectory is tied to tier-1 banks such as JPMorgan Chase extending face and fingerprint sign-in to the ATM fleet, making identity-based access the norm rather than an outlier.

The upgrade path reflects how security preferences migrate from convenience toward assured identity. Multifactor biometric stacks-combining facial, voice, and fingerprint templates, cut takeover fraud by double-digit percentages, justifying higher hardware costs. QR-codes retain relevance where handset diversity or privacy rules limit biometric capture, while Bluetooth Low-Energy serves niche use cases like gated venues needing short-range interaction. Banks balancing multiple techniques on a single chassis future-proof their estate and widen customer eligibility, enlarging overall participation in the cardless ATM market.

By ATM Location: White-Label and Drive-Through Models Gain Momentum

On-site branch machines still generated 46.80% of 2025 revenue, yet cost-pressured banks increasingly outsource low-margin physical distribution to specialized operators. White-label locations inside convenience chains and drive-through formats are poised to expand at a 13.62% CAGR through 2031. NCR Atleos’ 55,000-strong Allpoint network epitomizes this shift, offering fee-free access that simultaneously deepens customer stickiness for participating challenger banks. These outsourced networks reduce the fixed overhead associated with ATM maintenance, compliance, and cash logistics. As branch footprints shrink, white-label partnerships allow banks to preserve physical access without diluting digital transformation budgets.

The logistics playbook hinges on aligning machine density with footfall analytics: terminals migrate from marginal branch lobbies to petrol forecourts, grocery aisles, and quick-service restaurants. Drive-through lanes satisfy time-compressed consumers who now expect curbside cash in the same motion as click-and-collect groceries. The resulting distribution model converts capital-intensive ATM ownership into service-level agreements, creating elastic supply for the cardless ATM market. Data-driven deployment also improves service uptime and fraud monitoring, as third-party operators integrate predictive maintenance and cloud-based oversight. Ultimately, this flexible approach allows financial institutions to scale physical infrastructure on-demand without locking into multi-year asset cycles.

By End-User: Financial Inclusion Expands the Addressable Base

Retail banking users kept 61.90% share of 2025 transactions, but under-banked citizens, often paid in cash yet smartphone-literate, represent the highest-growth audience at 13.08% CAGR through 2031. India’s interoperable UPI-ATM framework shows how national digital ID rails can unlock no-card access in remote districts. This model is increasingly cited as a blueprint for scalable, low-cost financial inclusion across emerging economies. As more developing countries adopt similar digital public infrastructure, cardless ATMs become an essential access point for populations previously served only by informal networks.

For banks, servicing the under-banked pairs social obligation with commercial upside: low-cost digital onboarding replaces labor-intensive branch openings, while biometric checks lower fraud risk in accounts lacking lengthy credit history. Corporate treasurers adopt cardless withdrawals for ad-hoc field payments, but growth is steadier because limits and audit rules impose extra verification layers. Meanwhile, micro-entrepreneurs and gig workers-often excluded from traditional credit rails-use cardless ATM access to bridge digital earnings and real-world liquidity needs. This dual-track adoption fuels not only transaction volumes but also demand for flexible KYC and onboarding frameworks. Overall, inclusivity initiatives expand the perimeter of the cardless ATM market, attracting both mainstream and previously excluded users.

Geography Analysis

North America contributed 33.10% of the global 2025 revenue. High smartphone saturation and aggressive retail rollouts by JPMorgan Chase and Bank of America position the United States as a proving ground for high-definition facial recognition and palm-vein scans. Security lapses, such as the Fifth Third Bank phishing event, accelerate layered defense investment, emphasizing the need for continuous anomaly monitoring. Canada mirrors U.S. adoption with Interac’s mobile-verified cash pilot, while Mexico leans on QR-code implementations to serve an under-banked population that prefers cash for small-ticket retail purchases.

Asia-Pacific is the growth pacesetter with a forecast 14.02% CAGR to 2031. India spearheads adoption via the UPI-ATM initiative, making cardless withdrawals available at more than 15,000 machines in both urban and tier-3 cities. In China, fully mobile consumer behavior converges with sophisticated QR and NFC acceptance, generating fertile ground for biometric ATM upgrades as local handset makers embed secure elements by default. Southeast Asian fintechs partner with incumbent banks to co-brand terminals, enabling overseas workers to remit funds home and extract cash without plastic cards.

Europe shows steady but policy-driven momentum. PSD3 enforces open-banking compliance, standardizing the API overlay across member states and facilitating multi-bank “super-ATM” rollouts tested in the United Kingdom. Spain will host Revolut’s extra-large touchscreen prototype in 2026, demonstrating fintech influence on form factor. Nordic markets-long pioneers in cashless retail-still keep rural ATMs operational, but dual-mode layouts combine card and cardless workflows to satisfy tourists. In the Middle East and Africa, finger-vein services launched by Arab Bank prove biometrics resonate in culturally diverse cash ecosystems, while South African retailers integrate white-label machines to soften branch closure impact.

Competitive Landscape

The cardless ATM market is moderately concentrated. NCR Atleos leads infrastructure deployments, extending its Allpoint and Cashzone networks across North America and into new European territories through a February 2025 Italian entry. Diebold Nixdorf collaborates with Mastercard to offer app-based deposit and withdrawal flows, bolstering relevance at a time when branch footprints shrink. Cardtronics, now part of NCR Atleos, activated more than 11,000 cardless-ready terminals by April 2025 and plans another 8,000 during the forecast window .

Platform strategies dominate: rather than bespoke two-party integrations, vendors expose APIs letting multiple banks ride the same estate. This hub-and-spoke model accelerates go-live timelines and keeps ATM uptime high with shared service contracts. Fintech entrants such as PopID differentiate via front-end identity modules that piggyback on established switch networks, carving out specialist biometric layers without owning physical boxes. Consolidation continues as Euronet agreed to buy 1,141 Baltic machines from Swedbank, illustrating how banks exit hardware ownership to refocus on digital channels.

White-space opportunities persist. Rural connectivity gaps prevent high-grade facial recognition, prompting niche vendors to supply ruggedized QR units optimized for low bandwidth. Sports-betting venues adopt drive-through cash kiosks to facilitate omnichannel payout flows. Across segments, the decisive battleground shifts from box count to experience integration: the player that unifies cash access, digital wallet top-ups, and real-time fraud analytics in one SDK gains brand-agnostic stickiness, fueling deeper adoption across the cardless ATM market.

Cardless ATM Industry Leaders

Citigroup Inc.

JPMorgan Chase & Co.

Wells Fargo

Barclays Bank

Bank of America

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: 7-Eleven partnered with NCR Atleos to deploy surcharge-free ATM services across over 4,000 U.S. locations through the Allpoint Network, enhancing cardless transaction capabilities.

- April 2025: Cardtronics enabled over 11,000 ATMs for cardless withdrawals using the FIS Cardless Cash system, with an additional 8,000 ATMs scheduled for deployment in coming months

- March 2025: Cashmallow partnered with RCBC to enhance cross-border remittance services and enable cardless ATM withdrawals in the Philippines, expanding financial accessibility for overseas workers

- February 2025: NCR Atleos expanded its Cashzone network into Italy, enabling convenient cardless cash access through partnerships with local retailers and financial institutions.

Global Cardless ATM Market Report Scope

Cardless ATMs provide access to your account and allow you to withdraw cash without the need for a card. Instead, they rely on account verification via text message or a banking app on your smartphone. There are several ways that cardless ATMs can function.

The study gives a brief description of the cardless ATM market and includes details on cash withdrawals and deposits, reduced card dependency, and enhanced security. The cardless ATM market is segmented by type, technology, application, and geography. By type, the market is segmented into on-site ATMs, off-site ATMs, and other types. Others include voice recognition, near-field communication, virtual card numbers, and dynamic authentication methods. By technology, the market is segmented into near-field communication (NFC), quick response (QR) codes, and biometric verification. By application, the market is segmented into banking and retail. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East, Africa, and South America.

The report offers market size and forecasts for the cardless ATM market in value (USD) for all the above segments.

| NFC (Near-Field Communication) |

| QR-Code |

| Biometric (Fingerprint, Face, Palm-Vein) |

| Mobile-App OTP / Token |

| Bluetooth Low-Energy (BLE) |

| On-Site (Branch) ATMs |

| Off-Site / Retail ATMs |

| Other (White-Label,Drive-Through ATMs) |

| Retail Banking Customers |

| Corporate Customers |

| Under-banked Population |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Technology | NFC (Near-Field Communication) | |

| QR-Code | ||

| Biometric (Fingerprint, Face, Palm-Vein) | ||

| Mobile-App OTP / Token | ||

| Bluetooth Low-Energy (BLE) | ||

| By ATM Location | On-Site (Branch) ATMs | |

| Off-Site / Retail ATMs | ||

| Other (White-Label,Drive-Through ATMs) | ||

| By End-User | Retail Banking Customers | |

| Corporate Customers | ||

| Under-banked Population | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the cardless ATM market?

The cardless ATM market is valued at USD 4.58 billion in 2026 and is forecast to reach USD 8.39 billion by 2031.

Which technology leads the cardless ATM space today?

NFC currently dominates, representing 41.95% of global 2025 revenue, although biometrics is the fastest-growing segment.

Why is Asia-Pacific the fastest-growing region?

Smartphone-first consumer habits, supportive regulations such as India’s UPI-ATM framework, and rapid bank-fintech partnerships drive a 14.02% regional CAGR through 2031.

How do banks benefit financially from cardless ATMs?

Eliminating plastic card issuance, lowering fraud remediation, and collaborating with white-label operators reduce operating costs while enhancing customer experience.

Page last updated on: