Balsa Wood Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

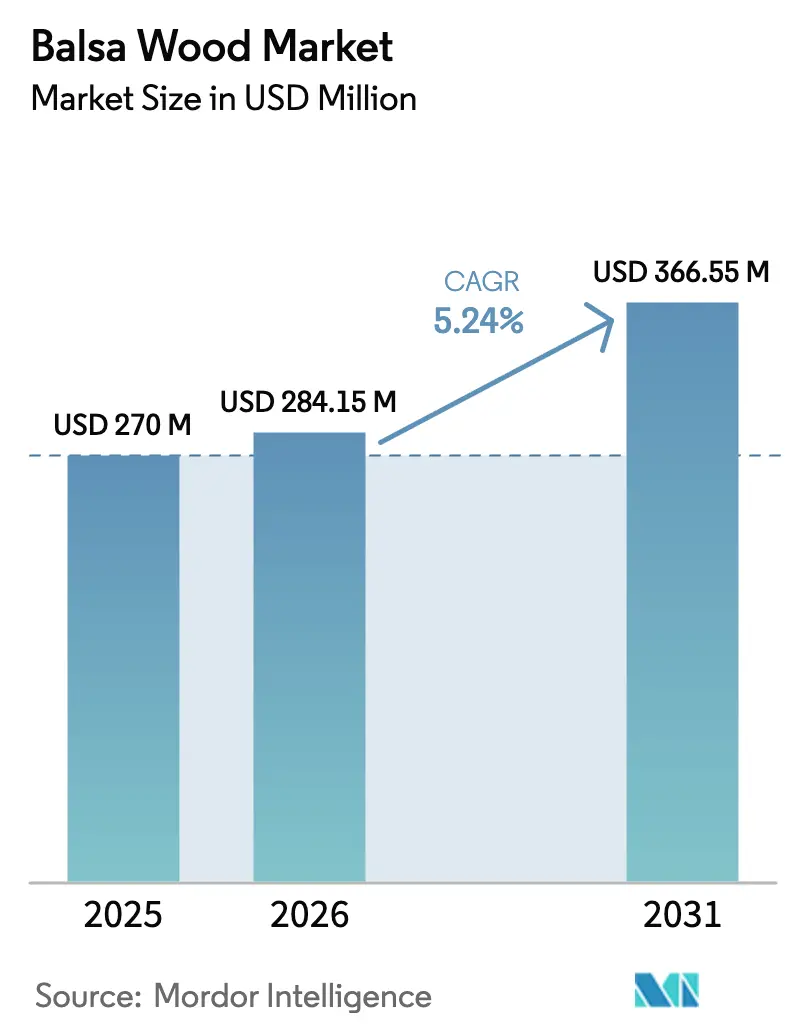

| Market Size (2026) | USD 284.15 Million |

| Market Size (2031) | USD 366.55 Million |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Balsa Wood Market Analysis by Mordor Intelligence

The balsa wood market size was valued at USD 270 million in 2025 and estimated to grow from USD 284.15 million in 2026 to reach USD 366.55 million by 2031, at a CAGR of 5.24% during the forecast period (2026-2031). Expansion in wind-energy blade cores, high-performance marine panels, and weight-sensitive aerospace structures supports this steady trajectory, while end-product manufacturers increasingly favor traceable, Forest Stewardship Council (FSC) certified supply. Ecuador supplies 68% of global output, giving the country outsized influence on both price and availability. The country’s plantation owners, therefore, wield a pivotal role in de-risking supply for downstream customers. As civil aviation electrifies and prototype eVTOL aircraft accelerate, demand for ultra-light structural inserts further complements bulk consumption in renewable energy.

Key Report Takeaways

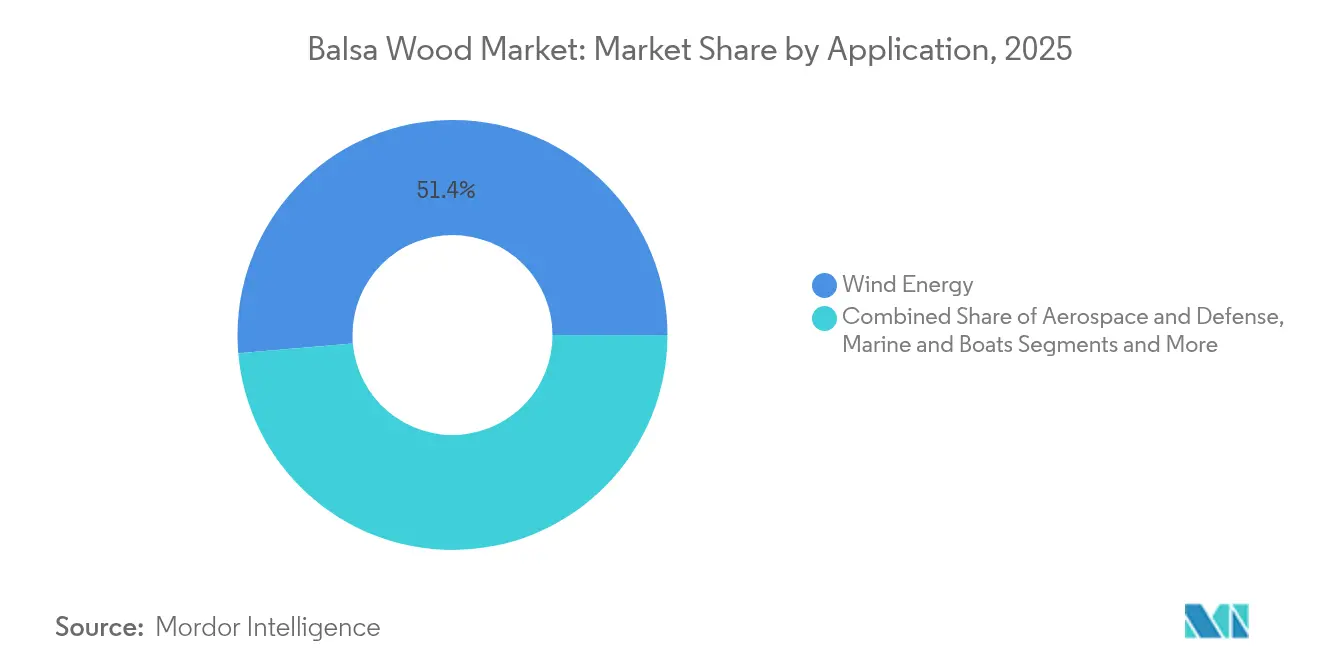

- By application, wind energy led with 51.35% of the balsa wood market share in 2025; offshore wind cores are forecast to expand at an 8.08% CAGR by 2031.

- By density grade, Grade A captured a 42.60% share of the balsa wood market size in 2025 and is projected to rise at a 6.31% CAGR.

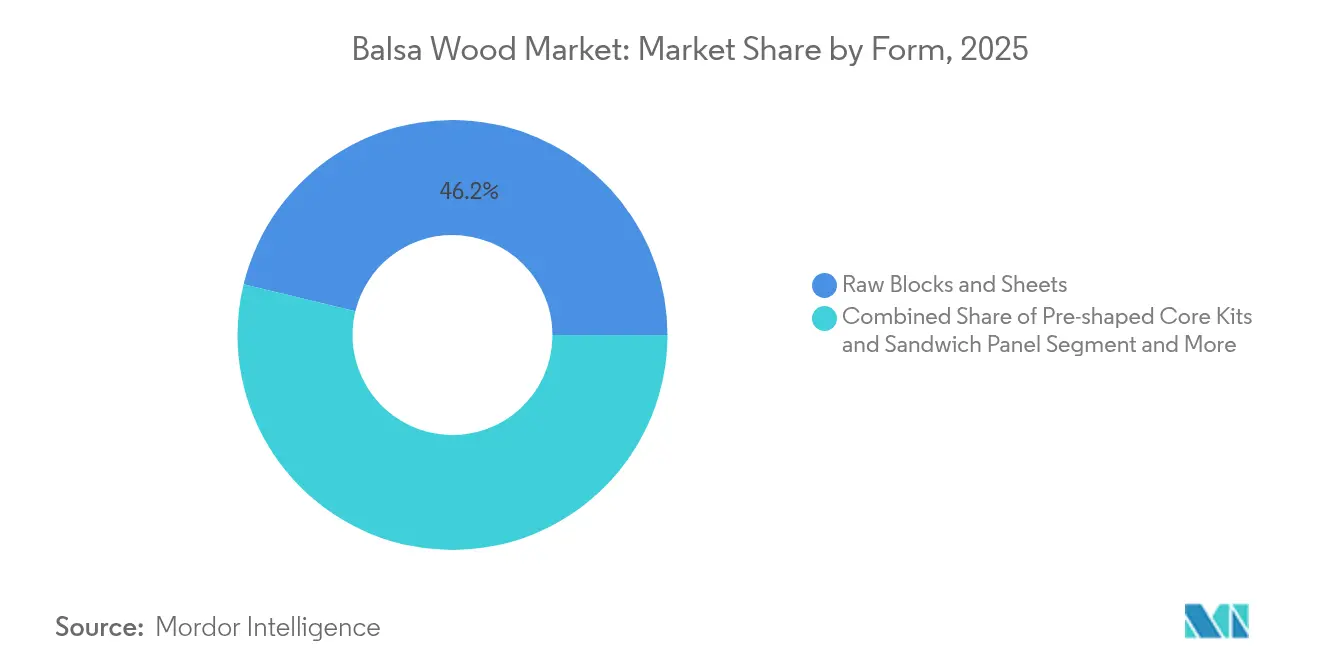

- By form, raw blocks and sheets held 46.20% revenue share in 2025, while pre-shaped kits are set to grow at a 7.14% CAGR through 2031.

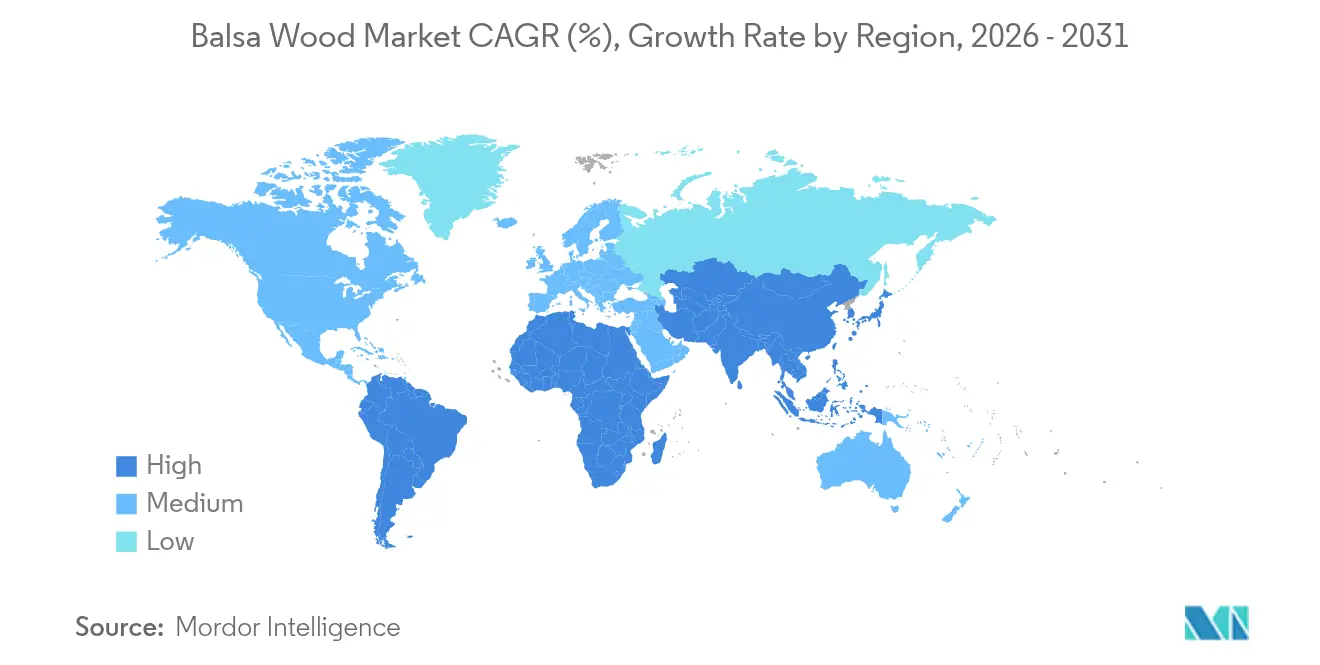

- By geography, Asia-Pacific accounted for 38.95% of global demand in 2025; South America is the fastest-growing region at 7.05% CAGR.

- The market shows significant consolidation, with 3A Composites, Gurit, and DIAB holding around 45.40% shares of the global market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Balsa Wood Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global wind-turbine blade demand for lightweight cores | +1.8% | Global, with concentration in China, Europe, and North America | Long term (≥ 4 years) |

| Growing adoption of lightweight composites in the space sector | +0.9% | North America and the Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Rising use of balsa sandwich panels in global marine and yacht construction | +0.7% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Sustainability push toward bio-based, recyclable core materials across industries | +1.2% | Global, led by Europe regulations | Long term (≥ 4 years) |

| Rapid eVTOL aircraft prototyping requiring ultra-light interior structures | +0.4% | North America, Europe, select Asia-Pacific markets | Short term (≤ 2 years) |

| Circular economy is driving the need for high-grade virgin balsa | +0.3% | EU primarily, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging global wind-turbine blade demand for lightweight cores

Wind turbine makers now specify balsa for blades exceeding 15 MW because PET foams can lose rigidity under dynamic marine loading. End-grain orientation delivers optimum shear strength, especially near blade roots where stress peaks. Pre-shaped kits have cut labor hours by up to 30% at large Chinese blade plants, supporting continued uptake despite foam price advantages. These tailwinds solidify wind energy as the anchor segment for the long-run offtake.

Growing adoption of lightweight composites in space sectors

Satellite makers favor balsa cores for payload platforms because every kilogram saved reduces launch expenses. Natural damping mitigates vibration, shielding delicate electronics through ascent profiles. Emerging eVTOL aircraft prototypes use balsa sandwich floors to extend battery-powered flight range, underscoring near-term aerospace opportunities. Advanced curing techniques now match stringent outgassing and flammability standards, allowing balsa to compete head-to-head with Nomex honeycomb on cost.

Rising use of balsa sandwich panels in global marine and yacht construction

Premium yacht builders in Europe increasingly request FSC-certified panels to align with eco-conscious customer preferences. Vacuum-infusion manufacturing leverages balsa’s uniform cell structure for high laminate quality, while new hydrophobic coatings curb moisture ingress, extending service life. As recreational craft lengths trend upward, designers specify thicker cores for stiffness, boosting volumetric demand across pleasure and commercial marine platforms.

Sustainability push toward bio-based, recyclable core materials across industries

EU regulations that favor renewable, traceable materials spur OEMs to switch from petroleum foams to wood-based cores. Vattenfall’s pledge for 100% circular composite flows by 2030 illustrates top-down pressure on the supply chain[1]Source: Vattenfall AB, “Towards Circular Wind Turbines,” vattenfall.com. Fraunhofer pilot projects now reclaim end-of-life turbine blades, isolate balsa, and reincorporate the fibers into new panels, broadening the resource loop. Carbon sequestration during balsa growth further strengthens the material’s green proposition as companies tally Scope 3 emissions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply instability from climate impacts | -0.8% | Ecuador, Peru, Papua New Guinea | Medium term (2-4 years) |

| Intensifying cost competition from PET/PVC/recycled foam core alternatives | -1.1% | Global, strongest in price-sensitive markets | Short term (≤ 2 years) |

| Stricter global fumigation and phytosanitary rules are increasing export logistics costs | -0.4% | Global trade routes, particularly from Ecuador to Asia | Short term (≤ 2 years) |

| New turbine blade designs are reducing balsa intensity per MW | -0.6% | Global wind markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply instability from climate impacts

Irregular rainfall has reduced Ecuadorean plantation yields, altering density profiles and forcing spot-market surges. Illegal logging in Peru compounds risk, drawing scrutiny from European and North American importers that now mandate chain-of-custody certification. Tighter fumigation rules lengthen customs clearance, raising freight costs on the principal Ecuador-Asia route and affecting working capital cycles. Producers consequently diversify acreage into Colombia and Bougainville to smooth shipment schedules.

Intensifying cost competition from PET/PVC/recycled foam core alternatives

PET foams captured over half of wind-blade core volumes by 2023 due to stable pricing and ease of digital machining. Recycled PET variants deliver sustainability claims comparable to balsa, narrowing the environmental gap. Major blade builder LM Wind Power’s pivot to PET illustrates OEM priorities around predictable supply and process commonality. To retain share, balsa suppliers highlight superior fatigue performance and fire resistance in critical sections while co-developing hybrid wood-foam solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Wind Energy Dominates Core Demand

Wind energy currently accounts for 51.35% of the balsa wood market, cementing the segment’s role as the primary demand engine. Offshore installations represent the fastest-growing slice with an 8.08% CAGR outlook, reflecting both longer blade designs and harsher oceanic load profiles. Aerospace and defense remain the second-largest consumer block, emphasizing mass-saving opportunities in satellite panels and eVTOL cabin structures. Marine construction, particularly performance yachts, sustains a niche yet premium demand that values buoyancy and moisture resistance.

Wind sector dominance also locks in long asset-life contracts, as turbines remain operational for 20–25 years, ensuring predictable offtake. In aerospace, advanced certification is enabling wider substitution for synthetic honeycombs, helping the balsa wood market penetrate space launch systems.

By Density Grade: Grade A Leads Premium Applications

Grade A captured a 42.60% share of the balsa wood market size in 2025 and is projected to rise at a 6.31% CAGR, underpinned by specification in blade root sections and missile airframes where high stiffness-to-weight metrics are indispensable. Its share of the balsa wood market size is forecast to rise alongside offshore turbine proliferation. Grade B stocks serve cost-sensitive components within the same industries, delivering moderate mechanical properties at lower price points. Grade C is common in decking and rail-car floors that require extra impact tolerance.

Precision silviculture and computerized kiln drying now yield tighter density tolerances, reducing downstream scrap and resin uptake. Micro-sanded Grade A panels lessen adhesive demand by nearly 15%, a saving that offsets higher raw-wood pricing. As engineers integrate density-graded cores tailored to localized stress maps, value migrates toward suppliers able to deliver consistent, certified quality.

By Form: Pre-shaped Solutions Drive Manufacturing Efficiency

Raw blocks and sheets still represent 46.20% of 2025 sales because many small and mid-size fabricators retain in-house cutting capability. Yet pre-shaped kits are advancing at a 7.14% CAGR, capturing share as blade and hull builders automate lay-ups to cut takt time. The balsa wood market share for precision core kits reached 22.60% in 2025 and is on course to approach 29.80% by 2031. Sandwich panels with integrated finishing skins draw interest from modular builders pursuing plug-and-play components that minimize onsite labor.

Schweiter Technologies’ USD 80.3 million purchase of JMB Wind Engineering underscores strategic intent to capture this high-growth niche. End-grain formats continue to serve highly loaded structures by optimizing fiber orientation for shear, a property especially valuable in helicopter rotor blades and racing-yacht keels.

Geography Analysis

Asia-Pacific commanded 38.95% of the global balsa wood market demand in 2025, thanks largely to China’s leadership in turbine output and its importation of 50% of worldwide balsa volumes. Initiatives in Yunnan province aim to supply 10% of domestic needs by 2024, hedging against overseas disruption. India’s National Aerospace Program elevates local composite consumption, while Vietnam and Indonesia scale trimming and lamination lines to feed regional export chains. Overall, the balsa wood market size for Asia-Pacific is projected to grow at 5.48% annually through 2031.

South America is the fastest-expanding region at a 7.05% CAGR, underpinned by Ecuador’s 68% share of global output and record forestry exports of USD 650 million in 2024, of which balsa contributed 33.5%. Peru’s meteoric rise from negligible volumes to 40,000 m³ deliveries in two years diversifies supply but raises regulatory flags amid reports of illegal felling. Colombia and Brazil invest in plantation acreage and kiln capacity, bolstering regional footprints that directly feed Asian blade factories.

North America and Europe remain mature but value-intensive outlets emphasizing FSC certification and closed-loop recycling. United States import volumes increased 26% in 2024 as wind-repowering projects accelerated. The EU’s Green Deal continues to tighten traceability and carbon accounting, creating defensive moats for suppliers with audited plantations. Middle-East and African markets collectively stay small but poised to grow alongside nascent wind corridors in Egypt, Saudi Arabia, and South Africa.

Competitive Landscape

The industry shows moderate concentration; the top three providers—3A Composites, Gurit, and DIAB—control an estimated 46% of balsa wood market revenue in 2024. Their plantation ownership secures fiber feedstock, while integrated mills and CNC finishing lines unlock cost savings and fast delivery. Each holds FSC chain-of-custody certification, a requirement for many European bids. Gurit’s multi-market shift reduced its historical reliance on wind to 63% of sales in 2024, expanding its presence in the marine and industrial segments.

Strategic mergers continue: Schweiter Technologies absorbed JMB Wind Engineering to cement leadership in pre-shaped kits, while DIAB has formed a joint venture in Indonesia to shorten lead times to Chinese blade plants. Technological differentiation centers on vacuum-resin infusion compatibility, digital quality inspection, and surface-treatment chemistries that block moisture. Smaller niche competitors, such as CoreLite, thrive by supplying specialty grades, whereas new entrants face long certification cycles and the challenge of financing 4–6-year plantation rotations.

Foam producers exert pricing pressure, prompting wood suppliers to showcase lifecycle emissions advantages and to co-engineer hybrid PET-balsa stacks that marry consistency with natural damping. Recycle-ready formulations position incumbents for future regulatory mandates on blade materials. Over time, market power is expected to consolidate further around players that command both forestry assets and automated fabrication capacity.

Balsa Wood Industry Leaders

Schweiter Technologies AG (3A Composites)

Gurit Services AG

Diab Group AB (Ratos AB)

CoreLite

Auszac Pty Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Gurit posted CHF 431.7 million net sales for 2024, rolling out a multi-market diversification plan Gurit.

- December 2024: MDPI research compared balsa to Rohacell and Nomex, confirming the superior mechanical performance of MDPI.

- November 2024: Researchers at Empa's Cellulose and Wood Materials laboratory in Switzerland have developed luminous wood, a glow-in-the-dark balsa wood composite for technical applications, designer furniture, and jewelry.

- July 2024: Bougainville, Papua New Guinea, completed its first commercial balsa wood shipment, expanding the geographic diversity of global balsa supply under the oversight of the Autonomous Bougainville Government (ABG).

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the global balsa wood market as the value of all newly harvested and industrially processed Ochroma pyramidale wood raw blocks, end-grain sheets, pre-shaped core kits, and engineered sandwich panels sold for structural, buoyancy, and craft applications across wind energy blades, marine panels, aerospace interiors, construction insulation, and hobby models.

Scope Exclusion: Furniture grade hardwoods, foam, honeycomb, or other non-balsa core materials fall outside our scope.

Segmentation Overview

- By Application

- Wind Energy

- Aerospace and Defense

- Marine and Boats

- Construction and Insulation

- DIY Models, Crafts, and Packaging

- By Density Grade

- Grade A

- Grade B

- Grade C

- By Form

- Raw Blocks and Sheets

- End-Grain Balsa

- Pre-shaped Core Kits and Sandwich Panels

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Ecuador

- Peru

- Brazil

- Rest of South America

- Europe

- Germany

- Spain

- United Kingdom

- Russia

- France

- Rest of Europe

- Asia-Pacific

- China

- India

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Phone interviews and online surveys with plantation owners in Ecuador, composite panel fabricators in China, turbine OEM buyers in Denmark, and marine design houses in the United States validate harvest yields, waste factors, grade mix, and seasonality. Procurement managers and regional distributors supply ASP corridors and confirm substitution trends toward PVC foam in low-load sections.

Desk Research

Our analysts begin with customs-coded trade flows from UN Comtrade, FAO forestry statistics, and shipping manifests scraped via Volza, then enrich the tonnage picture with production data from Ecuador's Ministry of Agriculture and Asia Pacific lumber associations. Industry journals such as Renewable Energy World and MarineLink help trace demand inflections, while audited company filings accessed through D&B Hoovers and news archives on Dow Jones Factiva ground revenue splits. Patent families sourced on Questel reveal density grade innovation pipelines. The sources cited above are illustrative; many additional open datasets and publications inform the desk review.

An internal knowledge base of prior Mordor studies (wind turbine blades, lightweight composites) is cross-queried to benchmark utilization factors, and price series are compared with CME balsa futures (where available) to set average selling price (ASP) bands.

Market-Sizing & Forecasting

A top-down production plus trade rebuild converts cubic meter harvests to revenue using region-specific ASPs, which are then corroborated with selective bottom-up roll-ups of core kit manufacturers' output. Key variables like offshore wind turbine installations, average blade length, Ecuadorian log export quotas, share of Grade A in aerospace panels, and China's import tariff dynamics feed a multivariate regression that projects demand. Gap pockets in bottom-up estimates are bridged with modeled utilization rates and triangulated against primary insights.

Data Validation & Update Cycle

Before sign-off, outputs pass anomaly checks, senior analyst peer review, and variance testing against independent price and volume indicators. Reports refresh annually, and material events (for example, a sudden export ban) trigger interim revisions; a final validation sweep occurs just prior to client delivery.

Why Mordor's Balsa Wood Baseline Commands Reliability

Published numbers differ because firms vary scope, refresh cadence, and price normalizations. Mordor's disciplined inclusion of craft and packaging demand, explicit ASP by density grade, and annual trade recalibration produces a broader yet traceable baseline that decision makers can rely on.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 270 million (2025) | Mordor Intelligence | - |

| USD 171 million (2024) | Regional Consultancy A | Omits craft and packaging, relies mainly on export data, no grade level ASP adjustments |

| USD 181 million (2025) | Global Consultancy B | Uses constant ASP, narrower end use list, biennial model refresh |

In sum, the larger 2025 baseline from Mordor stems from our wider demand lens and yearly data updates, providing a balanced, transparent figure anchored to clearly documented variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the balsa wood market?

The market is valued at USD 284.15 million in 2026 and is forecast to reach USD 366.55 million by 2031.

Which application uses the most balsa wood?

Wind-energy blade manufacturing dominates with 51.35% of 2025 demand.

Why is Grade A balsa preferred in offshore turbines?

Its 100–150 kg/m³ density provides the highest strength-to-weight ratio, crucial for large blades facing marine fatigue loads.

Which region supplies most of the world’s balsa?

Ecuador delivers 68% of global output and remains the pivotal export hub.

How are foam alternatives affecting the market?

PET foams have captured over half of blade core volumes in cost-sensitive segments, compelling wood suppliers to emphasize sustainability and hybrid solutions.

What growth rate is projected for pre-shaped balsa core kits?

Pre-shaped kits are projected to advance at a 7.14% CAGR through 2031, driven by manufacturing efficiency gains.

Page last updated on: