Sawn Wood Market Size and Share

Sawn Wood Market Analysis by Mordor Intelligence

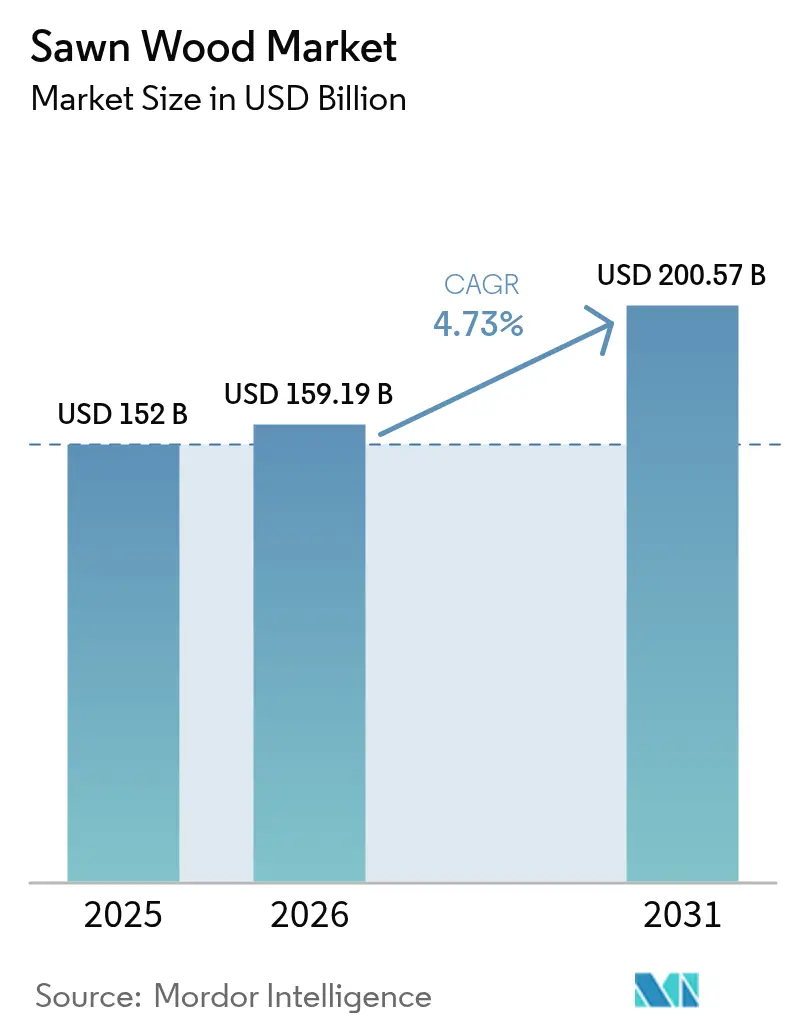

Sawn Wood market size in 2026 is estimated at USD 159.19 billion, growing from 2025 value of USD 152 billion with 2031 projections showing USD 200.57 billion, growing at 4.73% CAGR over 2026-2031.

The moderate expansion reflects an industry that is moving from rapid growth to steady maturation while navigating the twin forces of sustainability mandates and process automation. Rising adoption of certified timber in mass-timber construction, coupled with sustained furniture and interior-décor demand, continues to underpin volume growth even as engineered wood alternatives chip away at some traditional applications. Competitive pressure is intensifying around traceability, with the European Union Deforestation Regulation (EUDR) creating both compliance costs and premium-pricing opportunities for suppliers that can prove origin. At the same time, investments in advanced sawmilling and kiln-drying technology are lifting yields, lowering per-unit emissions, and enabling mills to stay profitable despite labor shortages and evolving regulatory scrutiny. Together, these elements point to a resilient sawnwood market that is gradually rebalancing toward higher-value, lower-carbon product niches.

Key Report Takeaways

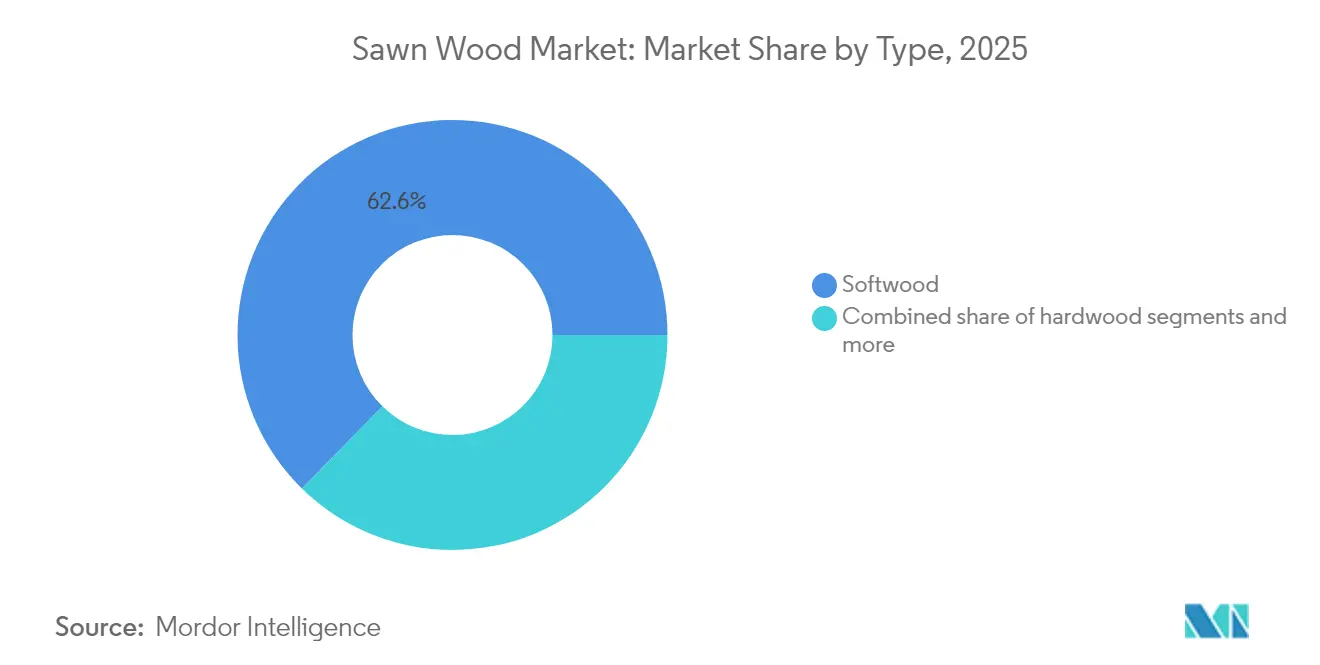

- By type, softwood led with 62.65% of the sawnwood market share in 2025, while hardwood is projected to post the fastest 5.38% CAGR through 2031.

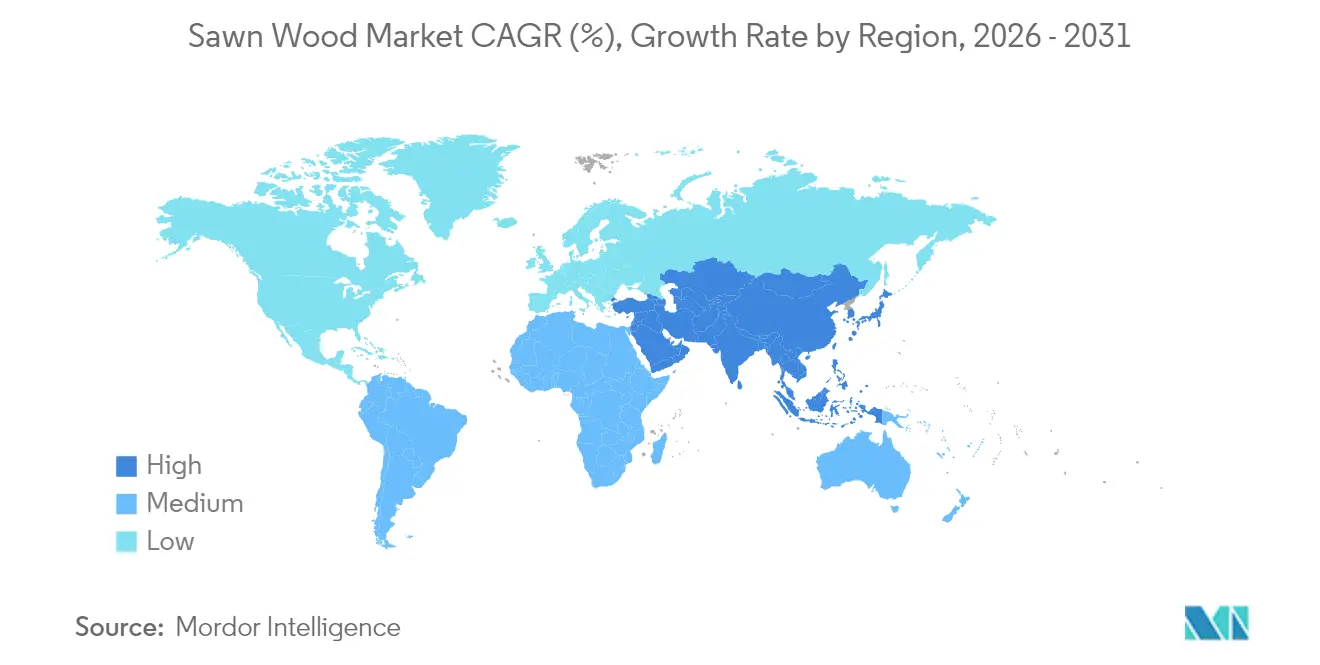

- By geography, Asia-Pacific captured 38.55% of the sawnwood market size in 2025; the Middle East is anticipated to expand at a market-leading 6.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sawn Wood Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging construction activity in emerging economies | +1.0% | Asia-Pacific, Middle East, and South America | Medium term (2-4 years) |

| Booming furniture and interior décor industry | +0.8% | Global, with concentration in Asia-Pacific and North America | Short term (≤ 2 years) |

| Advances in sawmilling and kiln-drying technology | +0.6% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Shift to low-carbon timber buildings | +0.7% | Europe, North America, and Australia | Medium term (2-4 years) |

| Rise of modular off-site mass-timber construction | +0.5% | North America, and Europe | Long term (≥ 4 years) |

| Premium pricing for certified traceable sawn wood | +0.4% | Global, particularly Europe markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging construction activity in emerging economies

Rapid urbanization across India, Indonesia, Vietnam, and select Gulf states is funneling unprecedented capital into housing, road, and public infrastructure projects, driving incremental demand for framing lumber and formwork. India’s annual wood requirement has risen to 63 million m³, with imports covering 33 million m³ as domestic supply lags behind expanding furniture production. Reconstruction programs after Turkey’s 2023 and 2024 earthquakes tripled Russian softwood imports to 292,200 m³, underscoring how rebuilding cycles can spark regional demand spikes. Consumers are also attaching greater weight to provenance; 51% now consider country-of-origin labeling when buying furniture, which is encouraging importers to source certified lumber for downstream value addition. Together, these factors continue to lift the sawnwood market in developing regions even as substitution pressure rises elsewhere.

Booming furniture and interior décor demand

Furniture buyers increasingly equate sustainability credentials with premium quality, and 67% cite responsible sourcing as a decisive purchase factor. Tight rubberwood supply in Malaysia has prompted calls to prioritize domestic processors, illustrating how localized shortages can quickly reconfigure global trade flows. Although U.S. hardwood flooring revenue fell 15% in 2024, oak retained 85% share of sales, validating hardwood’s staying power in the premium tier. Certification schemes such as FSC and PEFC have shifted from value-added features to baseline market-entry requirements for multinational retailers, pushing mid-scale mills to upgrade chain-of-custody systems or risk exclusion[1]Source: PEFC, “When Values add Value: Consumer Preferences for Sustainable Furniture,” furniture.pefc.org.

Advances in sawmilling and kiln-drying technology

Automation is emerging as the critical hedge against rising labor costs and aging workforces. Metsä Fibre’s Rauma plant, built for EUR 260 million (USD 275 million), processes 40 logs per minute using machine-vision grading, boosting recovery rates and lowering downtime. Pilot trials indicate that precise 425-400-400°F kiln schedules minimize defects in southern pine while preserving structural integrity, thereby improving saleable yields[2]Source: iForest, “Drying of Southern Pine Lumber,” iforest.sisef.org. Mills' integrating transportation-management software can now pair traceability data with real-time route optimization, an essential capability given EUDR’s geolocation disclosure rules.

Shift to low-carbon timber buildings

Government climate policies are embedding wood into mainstream building codes. The United Kingdom’s Timber in Construction Roadmap targets 1.5 million new homes built predominantly from sustainable timber by 2035[3]Source: UK Government, “Timber in Construction Roadmap 2025,” gov.uk. In the United States, 2,115 mass-timber projects were completed or underway by March 2024, requiring an estimated 250 million board-feet of softwood annually. Cross-laminated timber (CLT) prices more than doubled to USD 45 per cubic foot between 2016 and 2021 as supply struggled to keep pace, signaling strong price resilience when environmental regulations and design preferences align.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deforestation regulations and sustainability pressures | -0.6% | Global, particularly Europe markets | Short term (≤ 2 years) |

| Logistics bottlenecks and supply-chain disruptions | -0.5% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Substitution by engineered wood composites | -0.4% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Skilled-labor shortages in sawmills | -0.3% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Deforestation regulations and sustainability pressures

The EUDR’s stringent traceability requirement is reshaping trade routes by penalizing opaque supply chains. Smallholder operations in Southeast Asia and Central Africa often lack the resources to generate GPS-verified harvest data, risking exclusion from the EU’s USD 20 billion annual wood-product import market. While established producers such as Finland and Sweden already meet disclosure standards, the compliance gap is widening, accelerating industry consolidation around capital-rich enterprises able to embed blockchain or satellite-imaging tools. The shift has begun to redirect untraceable volumes toward markets with looser rules, exerting a mild drag on global sawnwood market growth in the near term.

Logistics bottlenecks and supply-chain disruptions

Transport fragility continues to create supply shocks. The August 2024 Canadian rail shutdown stranded an estimated USD 277 billion in annual U.S.-Canadian trade, forcing many lumber shippers onto higher-cost truck routes. In Europe, Red Sea rerouting added 30-45 days to transit times for hardwood arriving from Southeast Asia during 2024, inflating landed costs and eroding margins. Sawmills are mitigating risk by diversifying port gateways and contracting additional warehouse space, but higher working capital requirements offset some of the gains from improved technology.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hardening leadership for softwood while hardwood accelerates

Softwood accounted for 62.65% of the sawnwood market share in 2025, energized by U.S. housing starts projected at 1.38 million units for 2025. North America’s expansive forest base ensures a stable supply, and continued adoption of CLT and glulam keeps structural consumption buoyant. The softwood-heavy sawnwood market size for construction framing alone is set to rise 2.78% annually through 2031. Still, cascading substitution risk from engineered panels keeps price growth in check, encouraging mills to leverage higher-yield scanning systems and automated grading to preserve profitability.

Hardwood, meanwhile, is posting a brisk 5.38% CAGR as luxury furniture makers and boutique architects specify premium species for aesthetics and durability. Oak and walnut dominate North American upscale demand, while Asian buyers are turning to certified African mahogany and European beech. As certification becomes table stakes, hardwood producers equipped with transparent chain-of-custody logs command 8-12% price premiums, supporting investment in selective-harvest regimes that sustain long-term fiber availability. The sawnwood market size for certified hardwood could reach USD 90.8 billion by 2031, opening new avenues for value-added finishing and engineered overlays.

Geography Analysis

Asia-Pacific’s 38.55% grip on the global sawnwood market stems from the unmatched breadth of consumption and production. China’s record 110 million m³ domestic output in 2024 trimmed import dependency but left room for high-quality Scandinavian timber in window and door manufacturing. India stands out: wood-product imports climbed over two decades to USD 2.3 billion in 2024 as furniture demand surged alongside rising disposable income. Malaysia’s rubberwood tightness highlights the region’s vulnerability to species-specific supply shocks, prompting calls for export curbs that could reshape trade lanes.

The Middle East is growing as the fastest-growing region at a 6.51% CAGR on the back of large-scale urban developments like Saudi Arabia’s NEOM and the United Arab Emirates’ Sustainable City projects. North America remains the volume engine for softwood exports, yet structural supply constraints persist. Canada still tops global sawnwood exporters at roughly USD 6.5 billion a year despite British Columbia output falling by half since 2019 due to fiber shortages and higher costs. U.S. federal policy now targets greater domestic harvests to reduce wildfire risk and bolster mill utilization, though environmental reviews still slow land-release timelines. Housing demand recovery is projected to lift softwood shipments 2-3% annually through 2027, bringing partial respite to mill communities hit by 2024 shutdowns.

Europe’s market is in flux as EUDR ushers in a compliance-driven premium tier. Sweden and Finland, already steeped in traceability protocols, are positioned to thrive, while Eastern European and Southeast Asian exporters scramble to upgrade due diligence systems. The bloc represents 56.8% of global sawnwood export value and remains a net exporter despite robust internal consumption. Middle Eastern megaprojects are generating fresh pull on European and North American supplies, incentivizing mills to cultivate direct distribution links with Gulf developers.

Recent Industry Developments

- August 2024: Canadian rail shutdown stranded billions in cross-border lumber trade, exposing supply-chain fragility for mills reliant on rail.

- July 2024: Weyerhaeuser agreed to acquire 84,300 acres of Alabama timberland for USD 244 million, targeting USD 12.5 million EBITDA per year over the first decade.

- January 2024: Boise Cascade expanded its Oakdale, Louisiana facility with a USD 75 million investment, increasing veneer production capacity by 30% to reach 400 million square feet annually.

Global Sawn Wood Market Report Scope

Sawn wood refers to wood that has been cut from logs into various shapes and sizes. For the purpose of the study, both coniferous and non-coniferous sawn wood is considered. The sawn wood market is segmented by type (Hard wood and Soft wood) and geography (North America, Europe, Asia-Pacific, South America, and Middle East & Africa). The report includes the production analysis (volume), consumption analysis (value and volume), export analysis (value and volume), import analysis (value and volume), and price trend analysis. The report offers the market size and forecasts in terms of volume in metric tons and value in USD for all the above segments.

| Softwood |

| Hardwood |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Russia |

| Germany | |

| Sweden | |

| Finland | |

| Austria | |

| Asia-Pacific | China |

| India | |

| New Zealand | |

| Australia | |

| Vietnam | |

| Japan | |

| South America | Brazil |

| Argentina | |

| Middle East | Turkey |

| Saudi Arabia | |

| Africa | Egypt |

| Nigeria |

| By Type (Value) | Softwood | |

| Hardwood | ||

| By Geography (Production Analysis in Volume, Consumption Analysis by Volume and Value, Import Analysis by Value and Volume, Export Analysis by Value and Volume, and Price Trend Analysis) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Russia | |

| Germany | ||

| Sweden | ||

| Finland | ||

| Austria | ||

| Asia-Pacific | China | |

| India | ||

| New Zealand | ||

| Australia | ||

| Vietnam | ||

| Japan | ||

| South America | Brazil | |

| Argentina | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| Africa | Egypt | |

| Nigeria | ||

Key Questions Answered in the Report

How large is the global sawnwood market in 2026?

The global sawnwood market size is valued at USD 159.19 billion in 2026.

What is the projected growth rate for sawnwood through 2031?

The market is forecast to expand at a 4.73% CAGR, reaching USD 200.57 billion by 2031.

Which region dominates global sawnwood demand?

Asia-Pacific holds the largest 38.55% share in 2025 thanks to China's vast consumption base.

Which segment is growing faster, softwood or hardwood?

Hardwood is projected to outpace softwood with a 5.38% CAGR through 2031.

How is regulation affecting sawnwood trade with Europe?

The EUDR mandates geolocation traceability for all wood products from December 2025, favoring suppliers with robust certification systems.

What drives the premium for certified sawnwood lumber?

Compliance with traceability standards like FSC and PEFC commands price premiums of USD 25-50 per m³ in EU markets.

Page last updated on: