Bamboos Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 69.38 Billion |

| Market Size (2031) | USD 91.89 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bamboos Market Analysis by Mordor Intelligence

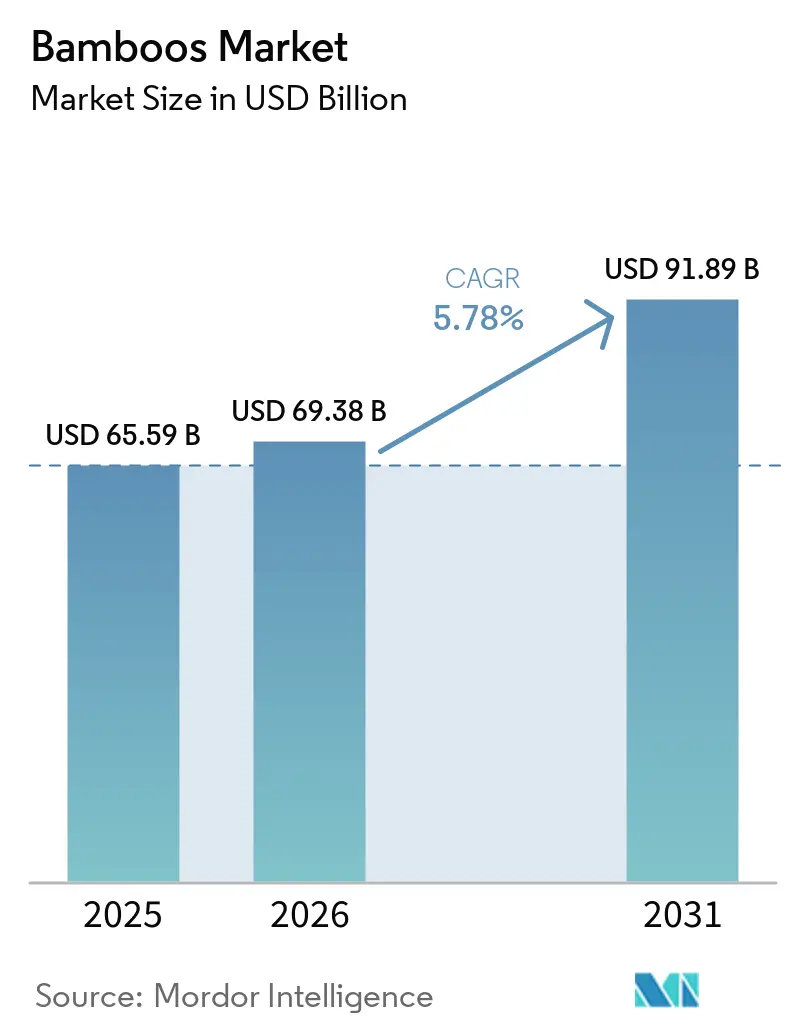

The bamboos market size was valued at USD 65.59 billion in 2025 and is projected to grow from USD 69.38 billion in 2026 to USD 91.89 billion by 2031, registering a CAGR of 5.78% from 2026 to 2031. Growth in the bamboos market is driven by stricter plastic reduction policies, increased interest in low-carbon building materials, and ongoing investments in bamboo fiber processing. Supply is not a significant challenge in the bamboo market, as there is an adequate supply available. The primary challenge lies in converting the abundant raw material into finished products that meet certification, traceability, and consistency standards required by stringent import regulations in Europe and North America. Additionally, the market is becoming more selective, as strong carbon performance enhances plantation economics, while limited Forest Stewardship Council certification continues to distinguish larger compliant suppliers from smaller exporters.

Key Report Takeaways

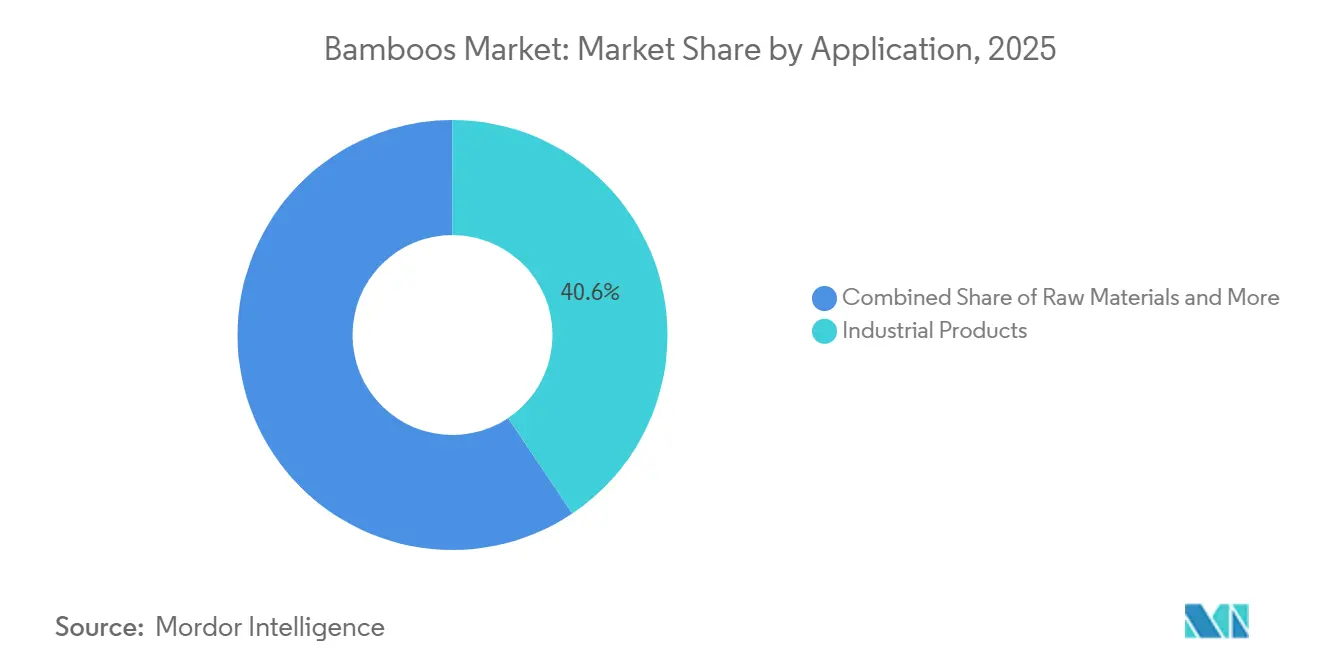

- By application, the bamboos market share for the industrial products segment held the largest 40.6% in 2025, and the bamboos market size for this segment is projected to grow at the fastest 5.5% CAGR from 2026 to 2031.

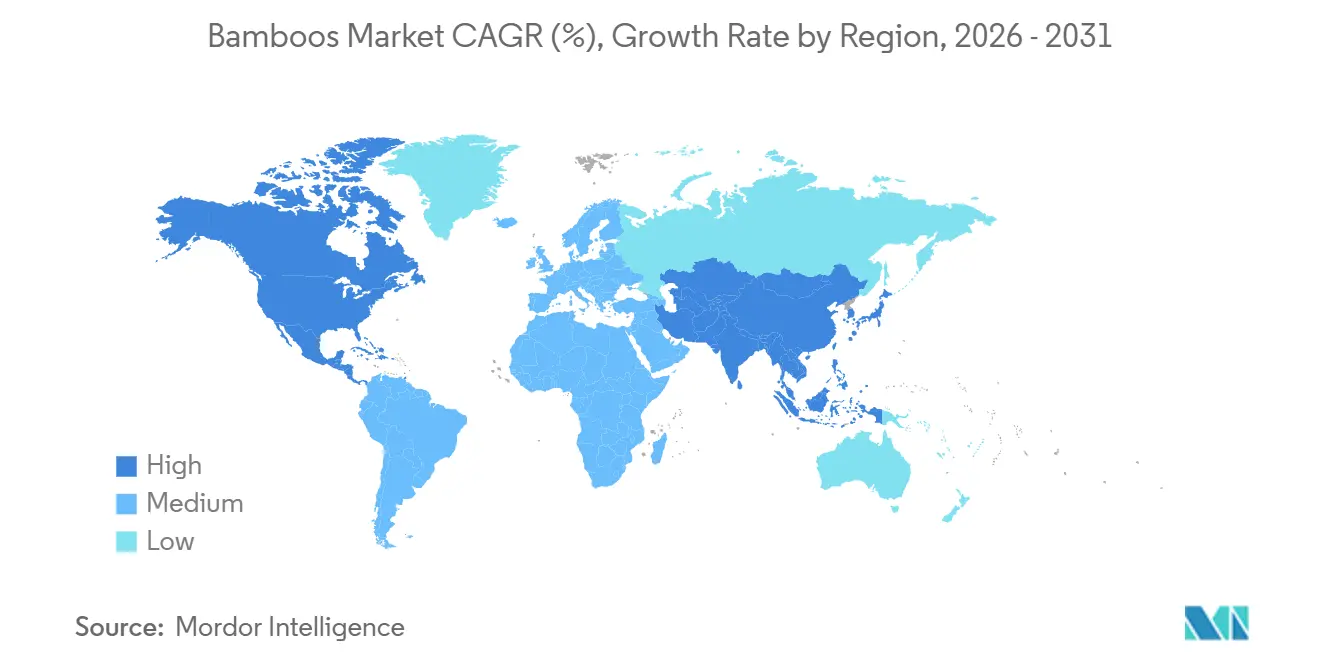

- By geography, the bamboos market share for Asia-Pacific accounted for the largest 79% in 2025, while the bamboos market size for North America is projected to grow at the fastest 6.2% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bamboos Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic substitution mandates boosting bamboo packaging demand | +1.2% | Global, concentrated in Europe, North America, and East Asia | Short term (≤ 2 years) |

| Engineered bamboo adoption in green construction projects | +1.0% | Global, with early leadership in Asia-Pacific, Europe, and North America | Medium term (2-4 years) |

| Furniture sector shifting toward low-carbon bamboo materials | +0.6% | Asia-Pacific core, with spillover into Europe and North America | Medium term (2-4 years) |

| Rising bamboo fiber demand across industrial applications | +0.8% | Asia-Pacific core, with growth in Europe and North America | Medium term (2-4 years) |

| Bamboo-for-plastic policies increasing industrial bamboo demand | +1.1% | China as the primary driver, with relevance across International Bamboo and Rattan Organization member countries | Short term (≤ 2 years) |

| Carbon monetization improving bamboo plantation project economics | +0.5% | Africa, South America, and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic Substitution Mandates Boosting Bamboo Packaging Demand

Plastic substitution initiatives are driving growth in the bamboo market by promoting the adoption of bamboo-based alternatives in packaging and industrial applications. According to the Press Information Bureau of India, as of 2025, India possesses the largest bamboo-growing area globally, covering 13.96 million hectares. It is also the second-richest country in bamboo diversity after China, with 136 species, including 125 indigenous and 11 exotic species. This extensive raw material base is bolstering bamboo processing industries and facilitating the production of sustainable bamboo products as substitutes for plastic-based materials.

Engineered Bamboo Adoption in Green Construction Projects

The adoption of engineered bamboo in green construction projects is driving growth in the bamboos market, as architects and developers increasingly prioritize low-carbon structural materials for sustainable building applications. In February 2026, Guadua Bamboo S.A.S. completed a 28-meter structural bamboo tower in Belgium, showcasing the commercial feasibility of engineered bamboo in modern construction[1]Source: Guadua Bamboo S.A.S., “Bamboo Tower in Belgium,” guaduabamboo.com. This project enhanced the visibility of bamboo-based structural systems among architects, engineers, and public infrastructure buyers, while boosting demand for certified, specification-grade bamboo materials with verified structural performance and sustainable sourcing credentials.

Bamboo-for-Plastic Policies Increasing Industrial Bamboo Demand

Bamboo-for-plastic policies are driving growth in the bamboos market as governments increasingly advocate for bamboo-based industrial materials to reduce reliance on single-use plastics and carbon-intensive products. The National Forestry and Grassland Administration of China reported that the “Replace Plastic with Bamboo” initiative was officially included in China’s 15th Five-Year Plan for 2026 to 2030 in March 2026[2]Source: National Forestry and Grassland Administration of China, “Replace Plastic with Bamboo Initiative Included in 15th Five-Year Plan,” forestry.gov.cn. This inclusion reinforces long-term policy support for bamboo industrialization. The initiative is fostering investment in bamboo-based packaging, automotive components, consumer products, and industrial materials, while promoting the development of large-scale bamboo processing and export-oriented manufacturing capabilities.

Carbon Monetization Improving Bamboo Plantation Project Economics

Carbon monetization is driving growth in the bamboos market as bamboo plantations increasingly generate value through carbon sequestration alongside fiber and processed material sales. A study conducted in 2025 by researchers from Zhejiang Aand F University, published in Advances in bamboo science, revealed that Moso bamboo forests can sequester over 40 metric tons of carbon dioxide per hectare annually. This significant carbon capture potential is enhancing the economic feasibility of bamboo plantation projects and promoting investment in sustainable forestry and carbon-credit-linked bamboo cultivation across Asia, Africa, and South America.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented feedstock supply and inconsistent grading standards | -0.8% | Global, most acute in India, Southeast Asia, and Africa | Medium term (2-4 years) |

| Processing capacity concentrated within limited producer countries | -0.6% | Non-producer markets including North America, Europe, the Middle East, and Africa | Long term (≥ 4 years) |

| Competition from plastics and alternative composite materials | -0.5% | Global, with stronger pressure in price-sensitive markets across Asia-Pacific and the Middle East | Short term (≤ 2 years) |

| Scrutiny over textile certification and traceability compliance | -0.4% | Europe, North America, and Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Feedstock Supply and Inconsistent Grading Standards

Fragmented feedstock supply and inconsistent grading standards are hindering growth in the bamboos market, as variability in bamboo quality reduces processing efficiency and complicates standardized manufacturing. A 2025 study by researchers from the University of Pittsburgh, published in npj Materials Sustainability, revealed that designed stresses in full-culm bamboo structures often remain below 20% of the actual material strength after accounting for safety and exposure factors. Variations in culm size, wall thickness, and structural consistency contribute to increased processing waste and limit the broader industrial use of bamboo in engineered construction and export-oriented manufacturing applications.

Scrutiny over Textile Certification and Traceability Compliance

Increased scrutiny over textile certification and traceability compliance is constraining growth in the bamboo market, as exporters encounter rising demands for sourcing transparency, sustainability verification, and product traceability. A 2024 academic paper published in the journal Advances in Bamboo Science reported that only 48 valid Forest Stewardship Council (FSC) bamboo forest management certificates existed globally, compared to 3,237 chain-of-custody certificates. This disparity underscores the limited availability of fully certified bamboo forests, posing compliance challenges for textile and fiber suppliers seeking to participate in premium retail and export programs in Europe and North America.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Industrial Demand Anchors Market Value

The bamboos market share for the industrial products segment accounted for the largest 40.6% in 2025, and the bamboos market size for this segment is forecasted to expand at the fastest 5.5% CAGR from 2026 to 2031. Industrial applications continue expanding across engineered panels, bamboo fiber materials, composite products, packaging formats, and construction-related intermediates that compete with wood and petroleum-based materials. Demand is also increasing for specification-grade bamboo products that support sustainability goals and lower-carbon procurement strategies. Growth in processing technology, industrial treatment capability, and export-focused manufacturing continues to strengthen the commercial role of industrial bamboo applications across construction, packaging, transportation, and consumer goods sectors.

Furniture and related consumer applications remain important across the bamboo industry because bamboo products increasingly align with demand for sustainable home furnishing and interior products. Bamboo furniture benefits from lower weight, natural aesthetics, and renewable sourcing advantages compared to traditional hardwood products. Bamboo shoots also maintain stable demand within processed food categories across Asia-Pacific markets. Emerging applications including bamboo textiles, bamboo-wound composite pipes, activated carbon, and biochar continue attracting commercial interest because they support diversification beyond traditional construction and handicraft uses. The expanding application mix is strengthening long-term industry resilience while creating additional opportunities for higher-margin processed bamboo product development globally.

Geography Analysis

The bamboos market share for the Asia-Pacific held the largest 79% in 2025. China remains the leading producer of bamboo globally, driven by its extensive bamboo forest resources, well-developed processing infrastructure, and government policies promoting bamboo as a substitute for plastics and wood materials. According to Xinhua News Agency, the output of China's bamboo industry surpassed CNY 520 billion (USD 71.7 billion) in January 2026, supported by nearly 8 million hectares of bamboo forests. Additionally, the region benefits from cost-effective manufacturing capabilities and robust export infrastructure in countries such as China, Vietnam, Indonesia, and India, further solidifying the Asia-Pacific's role in global bamboo processing and supply chains.

The bamboos market size for North America is forecasted to grow at the fastest 6.2% CAGR from 2026 to 2031. Increasing demand for sustainable construction materials, bio-based packaging, engineered flooring, and low-carbon interior products is driving the adoption of bamboo across residential and commercial sectors. Importers and distributors are expanding their offerings of specification-grade bamboo products for architects, retailers, and infrastructure projects. Consumers are also showing a growing preference for renewable and certified materials in furniture and home improvement categories. Furthermore, stricter environmental regulations and rising interest in alternatives to tropical hardwood products are supporting the broader commercial use of processed bamboo materials in the North American market.

Europe remains a significant export destination as buyers increasingly emphasize certified sourcing, traceability, and sustainable construction materials. According to MOSO International B.V., bamboo flooring gained a pricing advantage in 2025 when European Union anti-dumping measures on multilayered wood flooring from China excluded bamboo flooring products[3]MOSO International B.V., “MOSO Bamboo Flooring Does Not Fall Under the Anti-Dumping Measures,” moso-bamboo.com. This regulatory development enhanced commercial opportunities for bamboo-based flooring and interior materials in European construction and renovation markets. Demand in the region continues to grow across applications such as flooring, furniture, hospitality interiors, and sustainable building projects, driven by stricter environmental procurement standards and a rising preference for renewable, low-carbon construction materials.

Competitive Landscape

The bamboos market remains fragmented, with major companies such as MOSO International B.V., Dasso Industrial Group Co., Ltd., Bamboo Australia Pty Ltd, Shanghai Tenbro Bamboo Textile Co., Ltd., and Smith & Fong Company. However, large-scale processing capacity and certified sourcing capabilities are concentrated among a smaller group of vertically integrated manufacturers. Competition increasingly hinges on factors such as plantation access, industrial treatment capabilities, technical testing, export compliance, and long-term supply reliability, rather than solely on raw bamboo availability. Companies are enhancing their market positions through certified forestry operations, premium engineered bamboo products, and export-oriented manufacturing platforms catering to the construction, packaging, and interior furnishing industries. Buyers are showing a growing preference for suppliers capable of delivering specification-grade bamboo products, supported by traceability, sustainability documentation, and consistent industrial processing standards across international markets and regulated procurement environments.

Brand positioning, processing technology, and supply chain integration are becoming critical competitive differentiators in the bamboo industry. Manufacturers are increasingly investing in engineered bamboo, bamboo composites, and industrial material processing to strengthen their presence in higher-value construction and infrastructure applications. Export-oriented suppliers are expanding partnerships with distributors, architects, and commercial developers to enhance access to premium retail and specification-grade building channels. Product innovation focusing on durability, treatment quality, and certified sustainability performance is gaining importance as buyers prioritize renewable materials with transparent sourcing. Additionally, the industry benefits from stronger government support for bamboo industrialization and sustainable manufacturing initiatives on a global scale.

Long-term supply partnerships and certified processing capacities are gaining significance within international bamboo trade networks. The growing demand for specification-grade bamboo materials in construction, flooring, decking, and interior furnishing applications is driving manufacturers to enhance vertically integrated sourcing and export distribution capabilities. In November 2025, Fiberplast Group chose Dasso Industrial Group Co., Ltd. as its preferred bamboo supplier for the Benelux region. This partnership enhances Dasso’s access to European buyers and highlights the significance of certified supply partnerships in the global bamboo trade. Buyers increasingly prefer suppliers that can provide specification-grade bamboo products, along with traceability, sustainability documentation, and adherence to consistent industrial processing standards across international markets and regulated procurement environments.

Bamboos Industry Leaders

MOSO International B.V.

Dasso Industrial Group Co., Ltd.

Bamboo Australia Pty Ltd

Shanghai Tenbro Bamboo Textile Co., Ltd.

Smith & Fong Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Guadua Bamboo S.A.S. completed the 28-meter Guadua Bamboo Tower at Planckendael Zoo in Belgium, Europe’s largest structural bamboo building. The project used 10,260 meters of certified Guadua poles from its Valle del Cauca, Colombia facility and established a structural certification methodology for full-culm bamboo in Europe in collaboration with Ghent University and de Noordboom.

- August 2025: Moso International B.V. highlighted that its bamboo flooring products are exempt from the European Union's anti-dumping measures on multilayered wood flooring imports from China, enhancing its competitive position in the European sustainable flooring market.

- February 2025: The Tripura government has launched a five-year plan to expand bamboo cultivation for industrial applications, targeting an increase to 45,000 hectares. This initiative seeks to position the state as a leading supplier of bamboo products in India.

Global Bamboos Market Report Scope

Bamboo is a fast-growing woody grass extensively utilized as a renewable raw material in construction, furniture, flooring, textiles, paper, packaging, handicrafts, and food products. It is recognized for its rapid growth, high strength-to-weight ratio, carbon sequestration properties, and sustainability advantages, positioning it as a significant alternative to wood, plastic, and other traditional industrial materials. The bamboos market report is segmented by application (raw materials, industrial products, furniture, shoots, and other applications) and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Raw Materials |

| Industrial Products |

| Furniture |

| Shoots |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Indonesia | |

| Vietnam | |

| Philippines | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | Ethiopia |

| Ghana | |

| South Africa | |

| Rest of Africa |

| By Application | Raw Materials | |

| Industrial Products | ||

| Furniture | ||

| Shoots | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Indonesia | ||

| Vietnam | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Ethiopia | |

| Ghana | ||

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the outlook for bamboo products through 2031?

The bamboos market is projected to rise from USD 69.38 billion in 2026 to USD 91.89 billion by 2031.

Which application area leads global demand today?

Industrial Products lead with the largest 40.6% of demand in 2025.

Why does Asia-Pacific dominate global revenue?

Asia-Pacific hold the largest 79% of global value in 2025 because China combines bamboo forest resources, policy support, and dense processing infrastructure. The region also benefits from expanding clusters in countries such as Vietnam, India, and Indonesia.

What are the main risks for suppliers and exporters?

The biggest risks are uneven feedstock quality, limited grading standards, and stricter textile traceability requirements. These issues raise processing waste, slow product approval, and make compliance more expensive for smaller exporters.

Page last updated on: