Wood Pulp Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

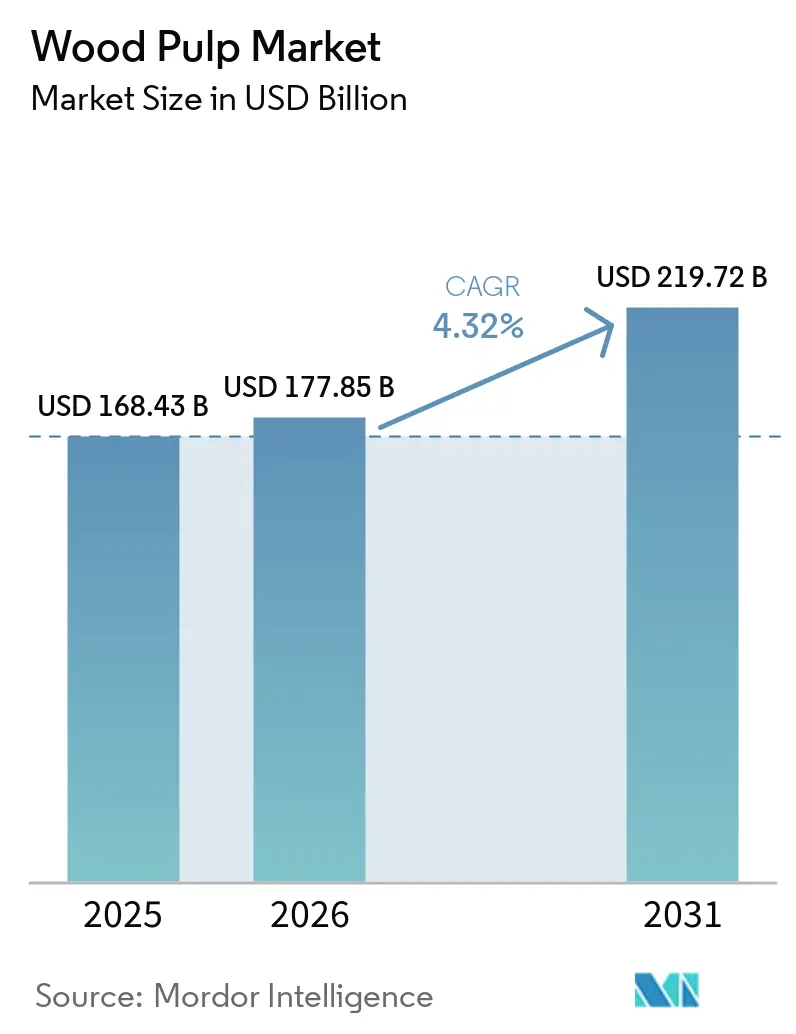

| Market Size (2026) | USD 177.85 Billion |

| Market Size (2031) | USD 219.72 Billion |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wood Pulp Market Analysis by Mordor Intelligence

The wood pulp market size was valued at USD 168.4 billion in 2025 and is estimated to grow from USD 177.9 billion in 2026 to reach USD 219.7 billion by 2031, at a CAGR of 4.3% during the forecast period (2026-2031). The wood pulp market, driven by packaging converters and tissue manufacturers, maintains a stable demand base across daily-use paper and fiber applications. Near-term pricing is shaped by supply adjustments, such as Suzano S.A.'s 3.5% production cut through mid-2026, and delays in Indonesian capacity, which have supported price recovery in China. The market's resilience lies in the diverse cycles of corrugated containerboard, tissue, specialty grades, and dissolving pulp, which absorb oversupply during new capacity additions. Regulatory changes, including stricter plastic packaging rules, higher recycled-content targets, and enhanced traceability requirements, are shifting global procurement priorities, increasing the value of certified fiber supply chains. Producers with plantation access, efficient recovery cycles, and diversified revenue from lignin and biomaterials are better positioned to sustain margins. These interconnected factors highlight the market's adaptability and its ability to balance supply and demand dynamics as it navigates a mid-cycle phase.

Key Report Takeaways

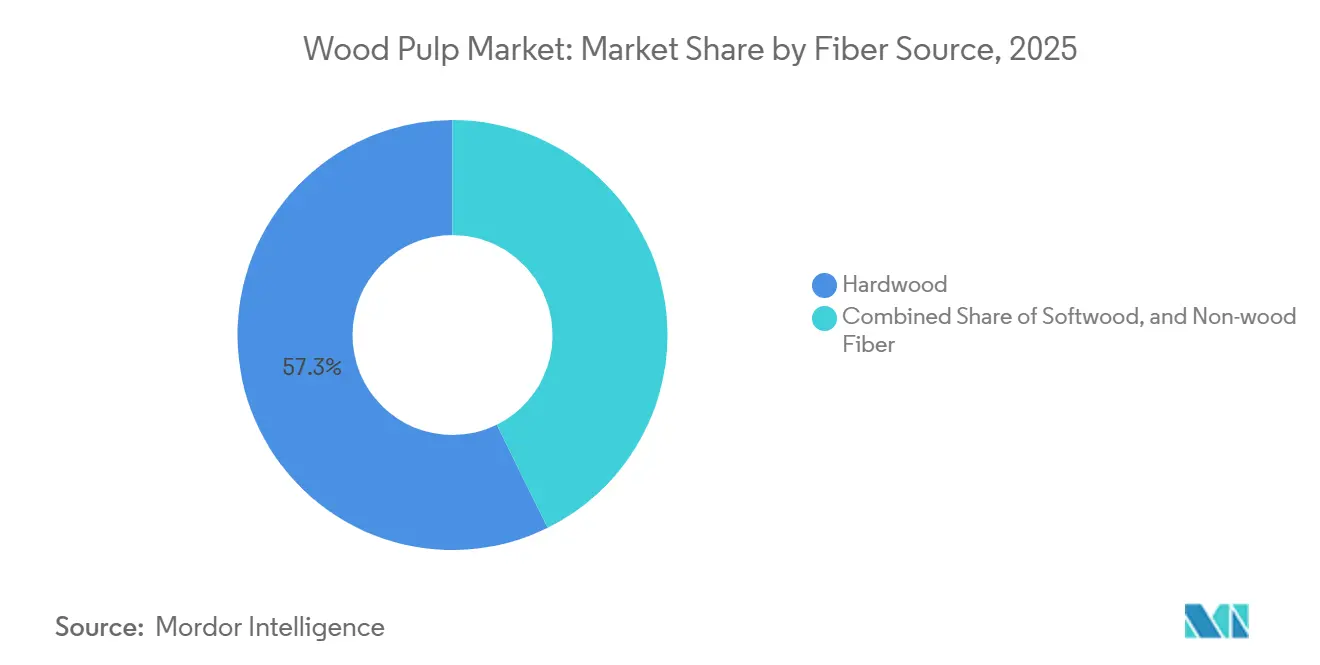

- By fiber source, Hardwood was the largest segment, accounting for 57.3% of the wood pulp market share in 2025, while Non-wood Fibers were the fastest-growing segment, projected to expand at a 5.8% CAGR during 2026-2031.

- By end-use industry, Packaging and Cartonboard held 46.2% of the wood pulp market share in 2025, while Tissue and Hygiene was the fastest segment at a 5.9% CAGR during 2026-2031.

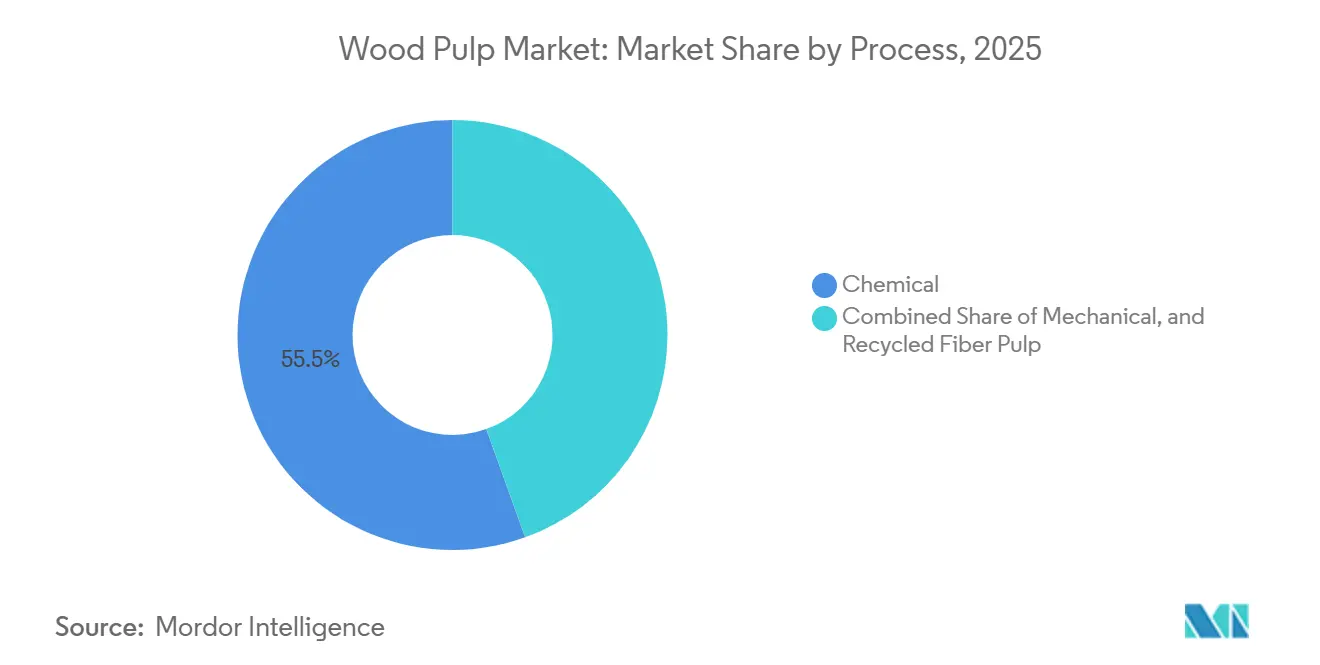

- By process, Chemical pulping accounted for 55.5% of the wood pulp market size in 2025, while Recycled Fiber Pulp was the fastest segment at a 6.2% CAGR during 2026-2031.

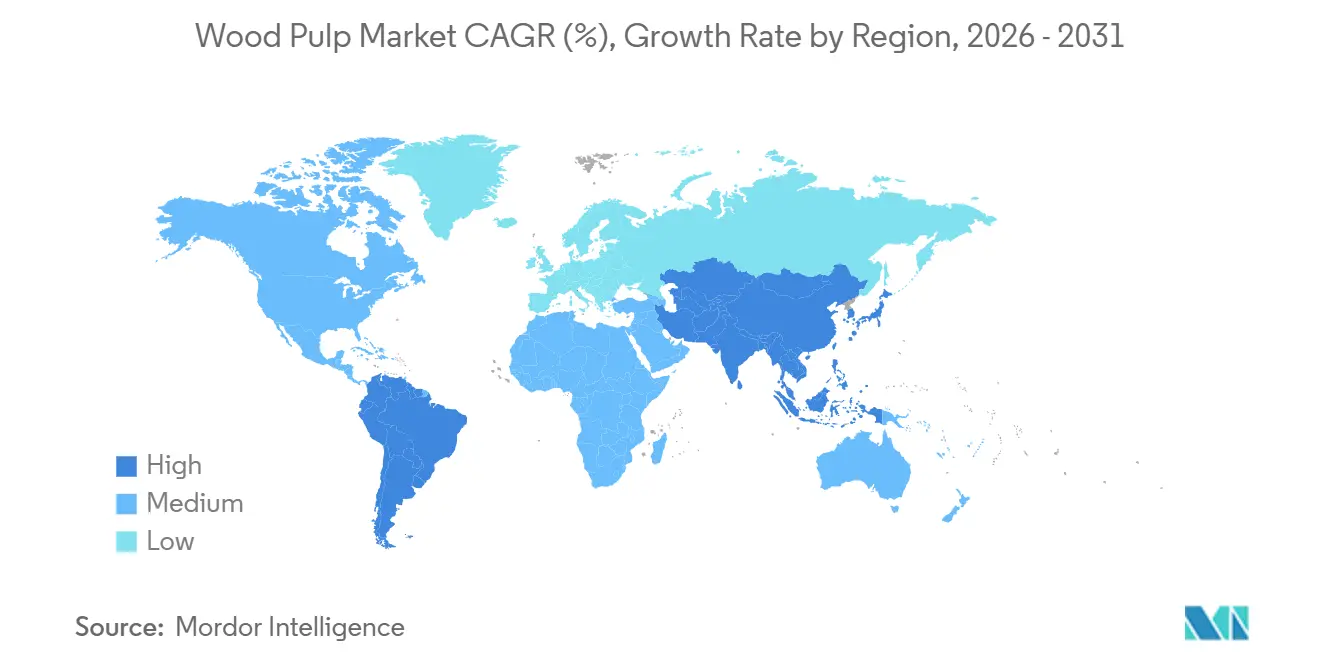

- By geography, Asia-Pacific accounted for 42.6% of the wood pulp market share in 2025 and was also the fastest-growing regional segment, with a 5.4% CAGR during 2026-2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wood Pulp Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce-Led Corrugated Packaging Demand | +0.9% | Global, with the strongest pull in North America, the Asia-Pacific core, and Europe | Short term (≤ 2 years) |

| Tissue and Hygiene Demand Expansion in Emerging Markets | +0.7% | Asia-Pacific core, with spillover into the Middle East and Africa | Medium term (2-4 years) |

| Plastic-to-Fiber Substitution from Packaging Regulation | +0.6% | North America and Europe, with a gradual spread into the Asia-Pacific and South America | Medium term (2-4 years) |

| Low-Cost Hardwood Kraft Capacity Ramp-Up in South America and Asia-Pacific | +0.5% | South America and Asia-Pacific, with export effects on global trade flows | Medium term (2-4 years) |

| Biorefinery Co-product Monetization and Carbon-Value Capture | +0.3% | Europe, South America, and North America | Long term (≥ 4 years) |

| Artificial Intelligence, Digital Twins, and Enzyme-Assisted Process Optimization | +0.2% | Global, with early adoption in Finland, Sweden, Uruguay, Brazil, and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce-led corrugated packaging demand

The wood pulp market is directly influenced by parcel growth, as corrugated packaging remains a key fiber-consuming application in global trade and direct-to-consumer delivery. Packaging Corp. of America reported an 11.1% year-over-year increase in corrugated packaging shipments during Q3 2024, reflecting high containerboard system utilization despite elevated recovered fiber costs. In China, machine-made paper and paperboard output totaled 106.659 million metric tons from January to August 2025, underscoring sustained demand even amid concerns about domestic overcapacity. To meet the evolving needs of fulfillment centers, buyers are prioritizing stronger corrugating grades for higher compression performance at reduced package weights, enhancing the value of premium kraft pulp. Simultaneously, molded fiber packaging is gaining traction as a sustainable alternative to single-use plastics, further driving demand for wood pulp across diverse consumer categories. Together, these trends highlight the growing reliance on advanced packaging solutions to support e-commerce and global trade.

Tissue and hygiene demand expansion in emerging markets

The wood pulp market is driven by growing tissue and hygiene demand in regions with per-capita usage significantly below global averages. In India, tissue paper production capacity, at 238,000–248,000 metric tons per year in 2024, is projected to reach 417,000 metric tons per year by early 2026, while per-capita consumption remains under 0.5 kilograms compared to the global average of 5 kilograms. Similarly, Japan’s tissue segment, with a per-capita consumption of 21.5 kilograms in 2024, continues to rely on imports due to cost advantages of supply from Indonesia and China over local production. Rising urbanization, sanitation investments, and disposable income growth in South Asia and parts of Africa further bolster demand for tissue and absorbent hygiene products, which are still developing from a low base. This expanding demand underscores the preference for short-fiber hardwood grades, valued for their softness, absorbency, and cost efficiency, aligning with the needs of both premium and mass-market products.

Plastic-to-fiber substitution from packaging regulation

The wood pulp market is gaining momentum as regulators and brand owners increasingly shift away from plastics in transport packaging, food service, and protective inserts. The European Union Deforestation Regulation, effective December 30, 2026, for large and medium operators, supports the adoption of fiber-based packaging and simplifies compliance for producers with certified, geolocated supply chains[1]Source: Programme for the Endorsement of Forest Certification, “EUDR Further Delay And Amendments Formally Agreed,” PEFC UK, pefc.co.uk. Complementing this, extended producer responsibility rules and plastic restrictions in Europe and North America are driving investments in fiber-intensive solutions such as corrugated dunnage, food-service board, and molded fiber products. Certification systems such as the Forest Stewardship Council and the Program for the Endorsement of Forest Certification are becoming critical in ensuring low-risk fiber sourcing, paving the way for a more sustainable and compliant supply chain. Together, these regulatory and market shifts are accelerating the transition to fiber-based packaging solutions.

Artificial intelligence, digital twins, and enzyme-assisted process optimization

The wood pulp market is advancing through digital controls, predictive optimization, and reduced-chemical processing, driving cost efficiency and yield improvements. For instance, Metsä Fiber’s Rauma pulp mill implemented Valmet’s Mill-Wide Optimization system in 2024, achieving a 5.2% increase in production over eight months, including two record production months. Complementing this, digital twins in recovery boilers have reduced heat loss by 5% and nitrogen oxide emissions by over 10%, enhancing uptime and minimizing energy waste[2]Source: “Digital Twinning to Advance Effluent Water Treatment for Pulp and Paper Mills, A Data-Driven Approach for Process Optimization,” PubMed, pubmed.ncbi.nlm.nih.gov . Furthermore, enzyme-assisted bleaching, such as xylanase pretreatment of eucalyptus kraft pulps, has reduced chlorine dioxide demand by up to 30% and bleaching effluent loads by 20% to 28%. Together, these innovations underscore the market's shift towards more efficient, sustainable, and optimized production processes.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pulpwood, Energy, and Freight Cost Volatility | -0.7% | Global, with the highest pressure in North America and Northern Europe | Short term (≤ 2 years) |

| Tightening Wastewater, Air Emissions, and Bleaching Compliance | -0.5% | Europe, North America, and Chile | Medium term (2-4 years) |

| Fiber Traceability and Deforestation Due-Diligence Compliance Burden | -0.4% | European Union-facing supply chains, especially Brazil and Indonesia | Medium term (2-4 years) |

| China-Led Capacity Overhang and Tariff-Driven Trade Diversion | -0.6% | Global, with a concentration in Asia-Pacific and export-oriented South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening wastewater, air emissions, and bleaching compliance

Environmental compliance is becoming increasingly costly for wood pulp producers as governments enforce stricter regulations on industrial emissions and wastewater management. Upgrading aging production facilities to meet these evolving environmental standards often diverts capital from capacity expansion and operational improvements, particularly for older mills. This issue is notably pronounced in Europe, where regulatory demands are intensifying. The European Commission's revised Industrial Emissions Directive (EU) 2024/1785, which came into effect in August 2024, imposes more stringent environmental performance requirements on industrial facilities[3]Source: European Parliament and Council of the European Union, “Directive (EU) 2024/1785 on Industrial Emissions,” July 2024, eur-lex.europa.eu.. Adhering to these updated standards is anticipated to necessitate additional investments in emissions control, wastewater treatment, and monitoring systems, thereby creating cost pressures that could limit growth and profitability within the wood pulp industry.

Fiber traceability and deforestation due diligence compliance burden

The European Union Deforestation Regulation, effective December 30, 2026, imposes strict requirements for geolocated harvest data, risk assessments, and Due Diligence Statements through the TRACES system, significantly increasing compliance costs for the wood pulp market. Non-compliance risks fines of up to 4% of annual EU-wide turnover and market access suspension, pressuring mills to adopt robust traceability systems. With over 6 million metric tons of market pulp imported annually from Brazil, North America, and Chile, as per the Confederation of European Paper Industries, global supply chains must adapt to meet these demands. While large producers may absorb these costs as market access investments, smaller converters relying on spot markets face rising procurement costs and supplier consolidation. The exemption for recovered-fiber products further drives the shift toward deinked pulp and old corrugated containers, underscoring the need for strategic adjustments to remain competitive under evolving regulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Source: Eucalyptus Consolidates Short-fiber Cost Leadership

Hardwood dominated the wood pulp market with a 57.3% share in 2025, driven by the cost efficiency of bleached eucalyptus kraft grades used in tissue, fine paper, and folding carton applications. Bleached hardwood kraft pulp remains the primary volume grade, while dissolving hardwood pulp is gaining traction as producers shift paper-grade capacity toward higher-value textile applications. Suzano S.A. estimated that up to 700,000 metric tons of tissue demand could transition annually from long fiber to short fiber in 2025, as eucalyptus demonstrated superior softness and absorption. Despite this shift, softwood remains critical for corrugated liner and specialty packaging due to its tensile strength, though cost pressures in Europe and Canada are limiting its supply flexibility.

Non-wood fibers are emerging as the fastest-growing segment, with a projected CAGR of 5.8% for 2026-2031, reflecting diversification in furnish options. In China, bamboo pulp projects in provinces such as Guizhou and Sichuan are expanding to support the production of tissue and specialty paper. Taison Group is developing a 600,000 metric ton per year integrated tissue paper and bamboo pulp project in Guizhou Province, reflecting increased investment in non-wood fiber supply chains. In India and Southeast Asia, agricultural residue pulp derived from bagasse and straw is gaining prominence as collection and processing systems improve. Although non-wood fibers currently represent a smaller portion of global pulp production compared to hardwood and softwood, they are increasingly being utilized to address raw material constraints and promote localized, sustainable fiber sourcing within the wood pulp market.

By End-use Industry: Packaging Anchors Volume While Tissue Accelerates

Packaging and Cartonboard, holding a 46.2% share in 2025, remains the largest end-use segment in the wood pulp market, driven by its integral role in merchandise trade, e-commerce fulfillment, and the corrugated value chain. Corrugated linerboard and medium dominate applications, supported by a 2.4 million metric ton annual increase in recycled containerboard capacity in North America between 2023 and 2025. Folding cartons and boxboard are also gaining traction as sustainability goals push brand owners to reduce plastic usage. Molded fiber packaging, growing faster than the broader packaging segment, benefits from U.S. trade actions in 2026 that redirected procurement from Chinese imports to domestic pulp-based alternatives.

Meanwhile, the Tissue and Hygiene segment is the fastest-growing category, projected to expand at a 5.9% CAGR during 2026-2031. This growth is fueled by rising demand for feminine hygiene and adult incontinence products in mature markets, alongside increasing adoption of bath tissue in emerging economies. The Specialty and Dissolving Pulp sub-segment complements this trend, as producers shift paper-grade capacity toward textile-grade dissolving pulp for viscose staple fiber. Premium pricing for filter papers, electrical papers, and cellulose derivatives underscores the importance of precise pulp properties over volume. As printing and writing applications contract, exemplified by UPM-Kymmene Oyj’s 2025 closure of the Ettringen paper mill in Germany, the market is clearly transitioning from legacy demand areas to higher-growth, sustainability-driven applications.

By Process: Kraft Maintains Dominance with Recycled Fiber Gaining Structural Ground

Chemical pulping, which accounted for 55.5% of the wood pulp market size in 2025, remains the leading process due to its adoption in major projects such as Celulosa Arauco y Constitución S.A.’s Sucuriú mill, leveraging advanced Valmet DNAe control systems. The Kraft process’s ability to integrate recovery and chemical loops for lignin extraction ensures additional biorefinery income, a clear advantage over mechanical and sulfite systems. While sulfite pulping serves niche applications requiring high alpha-cellulose purity, its relevance is declining, and mechanical pulping faces limited growth due to falling graphic paper demand.

Recycled fiber pulp, projected to grow at a 6.2% CAGR during 2026-2031, is reshaping the market by meeting regulatory requirements and recycled-content targets, while increasing packaging demand. North America’s 8.2% rise in old, corrugated container consumption in early 2024, driven by new recycled containerboard capacities, highlights the growing role of recycled furnish. The European Union Deforestation Regulation further accelerates this trend by exempting recovered-fiber products from due diligence requirements, encouraging their adoption. However, recycled fiber complements rather than replaces virgin fiber, as chemical pulp remains critical for strength, hygiene, and specialty applications. Together, these trends point to a balanced furnish mix, with Kraft maintaining dominance while recycled fiber gains structural importance.

Geography Analysis

The Asia-Pacific region holds the largest share of the wood pulp market, accounting for 42.5% in 2025. It is also projected to be the fastest-growing market, with a CAGR of 5.4% from 2026 to 2031. China’s production of 106.659 million metric tons of machine-made paper and paperboard during the first eight months of 2025, along with the approval of new projects in 2026, emphasizes its market leadership. Additionally, India’s rapid growth in tissue production and Japan’s stable demand of 8.4 million metric tons in 2024, primarily driven by hygiene and packaging grades, further illustrate the region’s expanding significance in the market.

North America, while mature, remains strategically relevant with demand concentrated on packaging, tissue, and fluff pulp. Despite a 6 million metric ton capacity reduction in 2025 due to rationalization in a high-cost environment, investments such as Georgia-Pacific LLC’s USD 800 million upgrade to its Alabama River Cellulose mill, targeting nearly 1 million metric tons by 2027, signal confidence in long-term demand. Canada faces cost pressures from reduced residual chip supply, while Europe adapts through specialty grades and biomaterials. Stora Enso Oyj’s Oulu mill conversion to 750,000 metric tons of packaging board exemplifies Europe’s shift away from graphic paper.

South America remains a critical supply hub, with Brazil producing 25.5 million metric tons of pulp in 2024. Russia’s constrained role due to sanctions has redirected pulp flows from Europe to Asia. In the Middle East, Saudi Arabia's Middle East Paper Company (MEPCO) is expanding its production capacity by constructing a new paper mill. This facility is projected to double the annual paper production capacity from 450,000 metric tons to 900,000 metric tons upon completion, while Turkey emerges as a growing tissue supplier. Africa’s rising hygiene awareness, urbanization, and sanitation programs drive long-term demand potential. Together, these regional shifts underline the interconnected evolution of the global wood pulp market, shaped by supply chain adjustments and changing consumption patterns.

Competitive Landscape

In 2025, the wood pulp market was moderately concentrated, with major players including Suzano S.A., Global Cellulose Fibers, Mercer International Inc., Stora Enso Oyj, and UPM-Kymmene Oyj holding a significant share, while the rest was fragmented among regional suppliers, Chinese state-backed mills, and integrated paper producers. Suzano S.A. focused on capital discipline and optimizing the Ribas do Rio Pardo mill, while Celulosa Arauco y Constitución S.A. invested USD 4.6 billion in the Sucuriú project to strengthen its global short-fiber market position by 2027. UPM-Kymmene Oyj emphasized decarbonization and biochemicals, Metsä Fiber improved yield and energy efficiency at its Finnish mills, and Sappi Limited prioritized cost discipline under its Thrive program to address weak dissolving wood pulp prices.

Producers are increasingly diversifying beyond commodity pulp into specialty biomaterials, lignin derivatives, and lower-carbon absorbent grades. Kraft lignin for battery anodes, specialty chemicals, and biofuel feedstocks is emerging as a key growth area, driven by existing recovery infrastructure in large Kraft mills. Suzano S.A. expanded its Limeira facility in 2025, boosting eucalyptus-based fluff pulp capacity to 440,000 metric tons annually for hygiene applications. Meanwhile, Chinese players such as Huatai Group are disrupting the market with integrated projects, such as the USD 2.3 billion Guangxi initiative, which combines forest resources, dissolving pulp, and industrial paper production. Producers aligning certified fiber with traceability systems by December 30, 2026, are projected to secure a competitive edge in Europe, where sustainability is increasingly prioritized.

Technology is driving the market transformation, with producers leveraging innovation to enhance competitiveness. Celulosa Arauco y Constitución S.A.’s autonomous operations at the Sucuriú mill highlight the integration of digital systems in new facilities. Mercer International Inc. is combining cost-saving measures with carbon capture projects, while Stora Enso Oyj and UPM-Kymmene Oyj are shifting investments from low-growth graphic paper assets to packaging, renewable materials, and biobased chemicals. The market is evolving from a focus on scale and cost efficiency to a race for sustainability, specialty products, and higher-value co-products, positioning producers for long-term growth and competitive advantage.

Wood Pulp Industry Leaders

Suzano S.A.

Global Cellulose Fibers

Mercer International Inc.

Stora Enso Oyj

UPM-Kymmene Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: UPM-Kymmene Oyj's Board approved a demerger plan to separate its Plywood business into a new, separately listed company, concentrating the group portfolio on pulp, specialty papers, decarbonization solutions, and renewable functional fillers, as part of a broader move toward higher-growth and higher-margin product segments.

- April 2026: Celulosa Arauco y Constitución S.A. announced that the Sucuriú Project in Brazil has completed its first year of site operations, exceeding 3.5 million work hours while progressing with construction activities. The project is on schedule for startup in the second half of 2027 and is among the largest pulp mill investments currently under development.

- April 2026: The European Commission initiated a Phase II investigation into the proposed 50/50 graphic paper joint venture between UPM-Kymmene Oyj and Sappi Limited, after Phase I raised unresolved competition concerns. Both companies confirmed continued engagement and target definitive agreements before year-end 2026, pending regulatory clearance in the European Union, United States, and China.

- March 2026: South American pulp project announcements aggregated potential investments of up to BRL 109 billion (USD 21.8 billion) across Brazil, Chile, and Paraguay through 2030, including Empresas CMPC S.A.'s Natureza project, Bracell's planned Bataguassu mill, and Eldorado Brasil's proposed second line in Três Lagoas, reinforcing South America's position as the globally dominant destination for market pulp greenfield investment.

Global Wood Pulp Market Report Scope

Wood pulp is produced by mechanically or chemically breaking down wood fibers into pulp. It is then processed into paper using chemical compounds such as caustic soda. The Wood Pulp Market Report is Segmented by Fiber Source (Hardwood, Softwood, and Non-Wood Fibers), by End-Use Industry (Packaging and Cartonboard, Tissue and Hygiene, Printing and Writing, and Specialty and Dissolving Pulp), by Process (Chemical, Mechanical, and Recycled Fiber Pulp), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardwood | Bleached Hardwood Kraft Pulp |

| Unbleached Hardwood Kraft Pulp | |

| Dissolving Hardwood Pulp | |

| Softwood | Bleached Softwood Kraft Pulp |

| Unbleached Softwood Kraft Pulp | |

| Fluff Pulp | |

| Non-wood Fibers | Bamboo Pulp |

| Bagasse Pulp | |

| Agricultural Residue Pulp |

| Packaging and Cartonboard | Corrugated Linerboard and Medium |

| Folding Cartons and Boxboard | |

| Molded Fiber Packaging | |

| Tissue and Hygiene | Bath Tissue |

| Paper Towels | |

| Facial Tissue and Napkins | |

| Feminine Hygiene and Adult Incontinence | |

| Printing and Writing | Uncoated Freesheet |

| Coated Paper | |

| Newsprint and Groundwood Grades | |

| Specialty and Dissolving Pulp | Textile-grade Dissolving Pulp |

| Filter and Electrical Papers | |

| Cellulose Derivatives and Specialty Applications |

| Chemical | Kraft |

| Sulfite | |

| Mechanical | Thermomechanical Pulp |

| Chemi-thermomechanical Pulp | |

| Groundwood Pulp | |

| Recycled Fiber Pulp | Deinked Pulp |

| Old Corrugated Container Pulp |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| Finland | |

| Sweden | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Indonesia | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Chile | |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Fiber Source | Hardwood | Bleached Hardwood Kraft Pulp |

| Unbleached Hardwood Kraft Pulp | ||

| Dissolving Hardwood Pulp | ||

| Softwood | Bleached Softwood Kraft Pulp | |

| Unbleached Softwood Kraft Pulp | ||

| Fluff Pulp | ||

| Non-wood Fibers | Bamboo Pulp | |

| Bagasse Pulp | ||

| Agricultural Residue Pulp | ||

| By End-use Industry | Packaging and Cartonboard | Corrugated Linerboard and Medium |

| Folding Cartons and Boxboard | ||

| Molded Fiber Packaging | ||

| Tissue and Hygiene | Bath Tissue | |

| Paper Towels | ||

| Facial Tissue and Napkins | ||

| Feminine Hygiene and Adult Incontinence | ||

| Printing and Writing | Uncoated Freesheet | |

| Coated Paper | ||

| Newsprint and Groundwood Grades | ||

| Specialty and Dissolving Pulp | Textile-grade Dissolving Pulp | |

| Filter and Electrical Papers | ||

| Cellulose Derivatives and Specialty Applications | ||

| By Process | Chemical | Kraft |

| Sulfite | ||

| Mechanical | Thermomechanical Pulp | |

| Chemi-thermomechanical Pulp | ||

| Groundwood Pulp | ||

| Recycled Fiber Pulp | Deinked Pulp | |

| Old Corrugated Container Pulp | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| Finland | ||

| Sweden | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Indonesia | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 outlook for wood pulp demand?

The 2026 outlook remains positive, with the wood pulp market projected to rise from USD 177.9 billion in 2026 to USD 219.7 billion by 2031 at a 4.3% CAGR during 2026-2031, supported by packaging, tissue, and specialty applications.

Which fiber source leads global consumption?

Hardwood was the largest fiber source with a 57.3% share in 2025, led by eucalyptus-based bleached kraft grades used across tissue, fine paper, and cartons.

Which end use is growing the fastest through 2031?

Tissue and Hygiene is the fastest end-use segment, projected to expand at a 5.9% CAGR during 2026-2031 as hygiene penetration rises in emerging economies and aging populations support demand in mature markets.

Why is Asia-Pacific so important in this space?

Asia-Pacific accounted for 42.6% of global demand in 2025 and is also the fastest-growing regional segment, with a 5.4% CAGR during 2026-2031, as China, India, Indonesia, and Japan all support large packaging, tissue, and specialty pulp consumption bases.

What are the main risks for producers in 2026?

The main risks are fiber and energy cost inflation, stricter environmental and traceability compliance, and China-led capacity overhang that continues to limit price recovery across grades.

Page last updated on: