Market Overview

| Study Period | 2021 - 2031 |

|---|---|

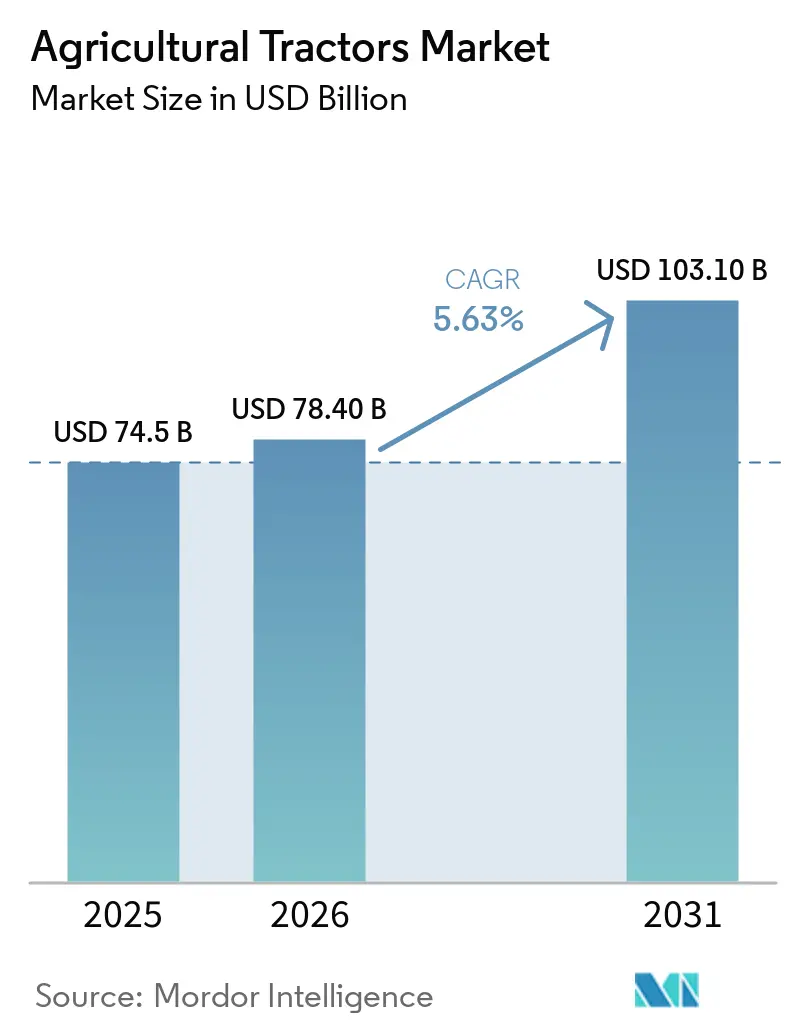

| Market Size (2026) | USD 78.40 Billion |

| Market Size (2031) | USD 103.10 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

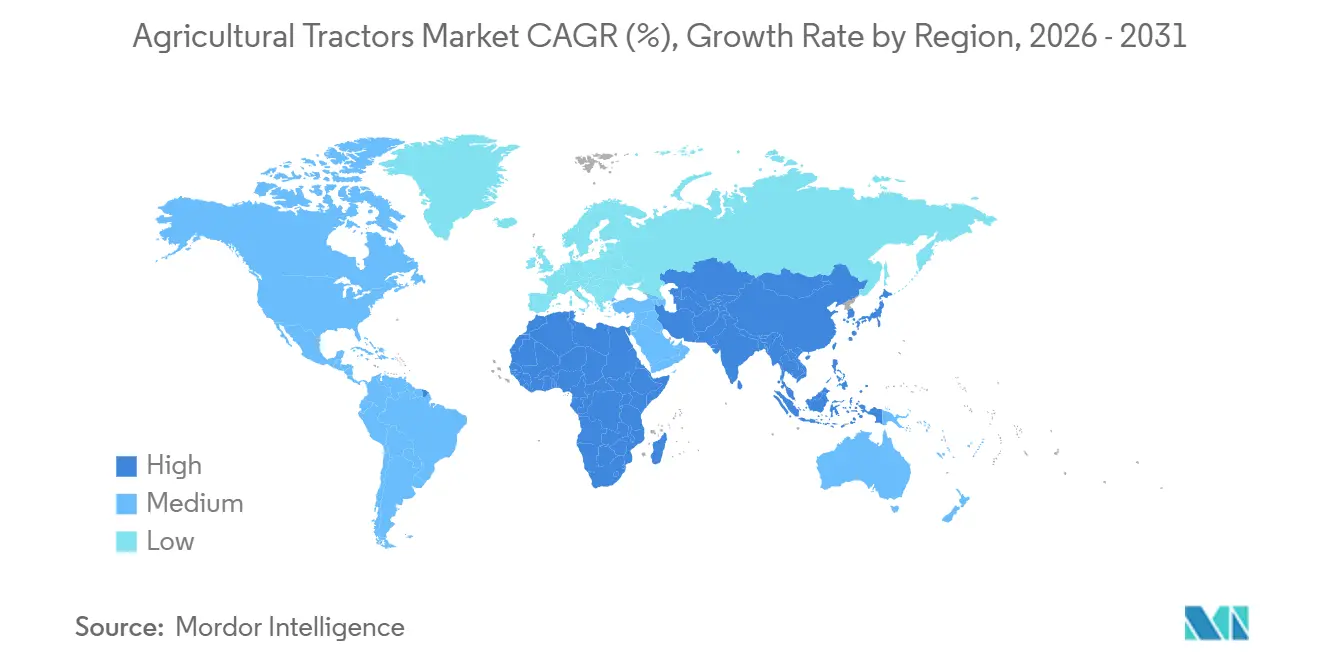

| Fastest Growing Market | Africa |

| Largest Market | Asia-Pacific |

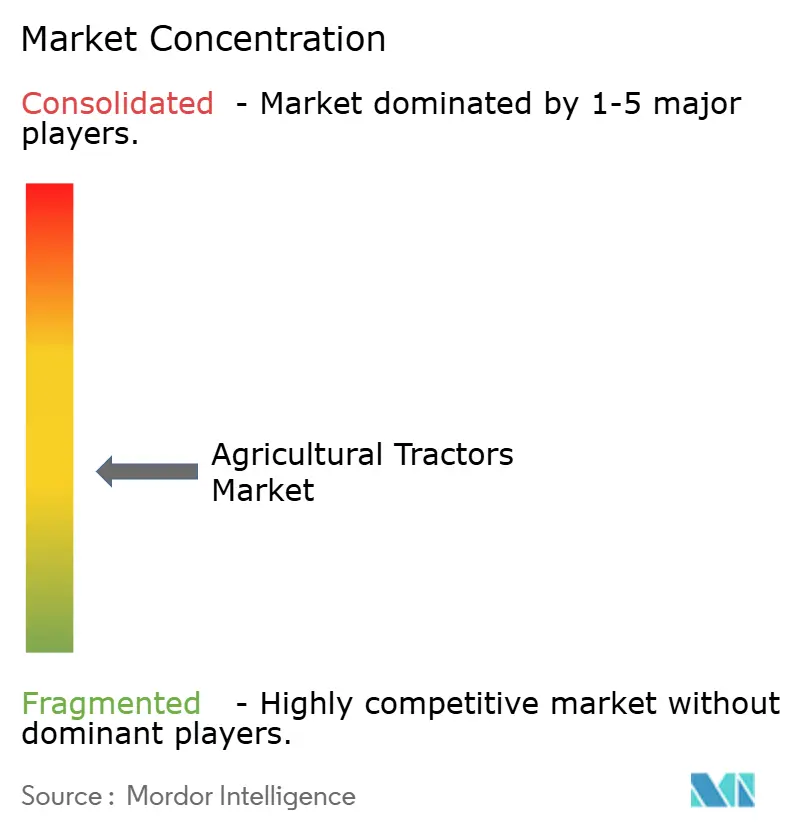

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Tractors Market Analysis by Mordor Intelligence

The agricultural tractors market size is anticipated to increase from USD 74.5 billion in 2025 to USD 78.40 billion in 2026 and reach USD 103.10 billion by 2031, growing at a CAGR of 5.63% over 2026-2031. This growth is primarily attributed to the expansion of cultivated areas in regions such as Africa and South Asia, a stronger replacement cycle in North America and Western Europe driven by stricter emissions regulations, and increased investments in precision guidance and autonomy-ready platforms. The market exhibits uneven regional demand, with robust volume growth in India contrasting with weaker short-term conditions in parts of Western Europe. Competition in the market is increasingly focused on connected machines that integrate guidance capabilities, retrofit modules, and support for farm data workflows, in addition to delivering core field performance. In response, leading manufacturers are updating product portfolios, forming partnerships in precision technology, and expanding manufacturing operations in cost-effective locations. However, market growth is constrained by higher acquisition costs, tighter machinery financing conditions, and rising expenses related to emissions-compliant diesel systems.

Key Report Takeaways

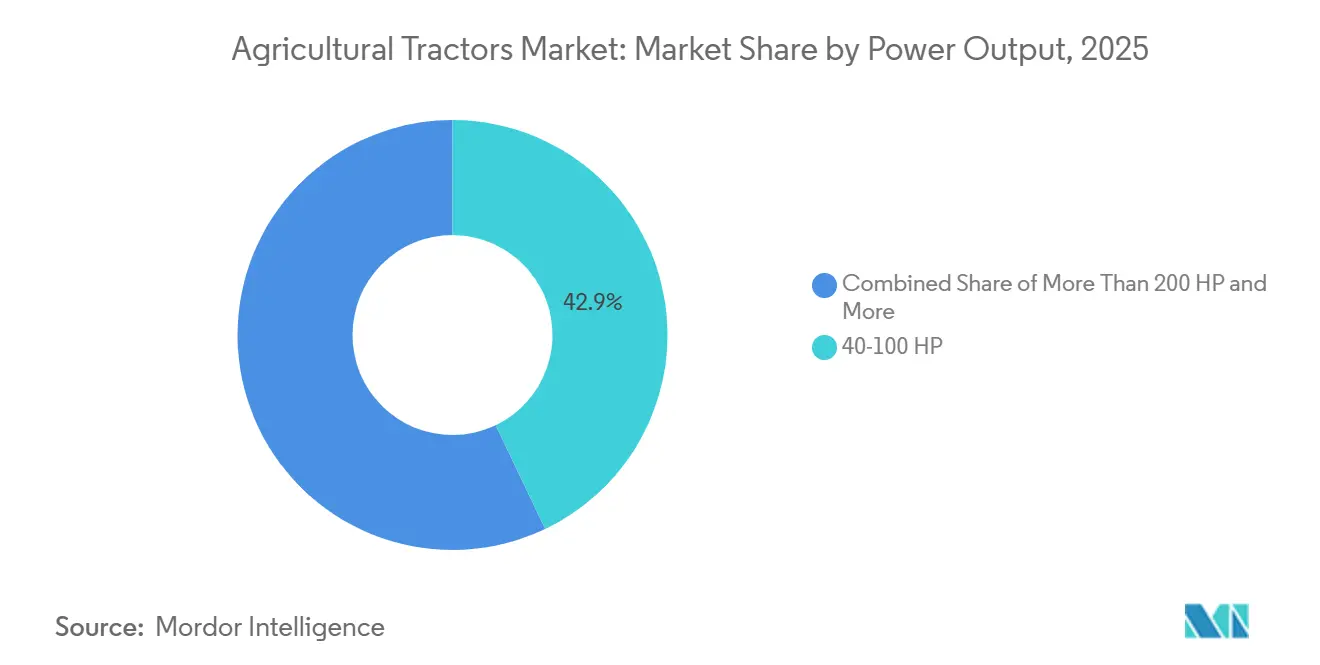

- By power output, the 40-100 HP segment led with the largest 42.9% of the agricultural tractors market share in 2025, while the agricultural tractors market size for the more than 200 HP segment is forecast to grow at the fastest 7.5% CAGR from 2026 to 2031.

- By drive type, the agricultural tractors market share for 2-wheel drive held the largest 71.8% in 2025, while the agricultural tractors market size for the 4-wheel drive is projected to expand at the fastest 7.6% CAGR from 2026 to 2031.

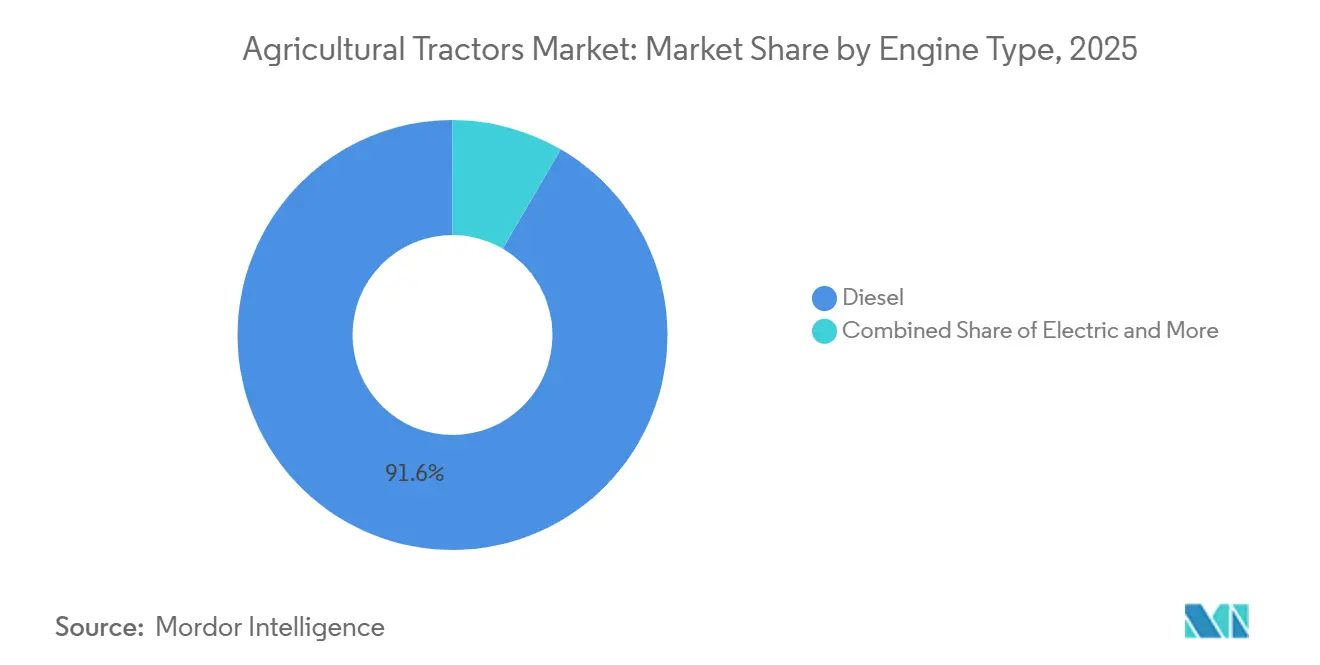

- By engine type, the agricultural tractors market share for diesel accounted for the largest 91.6% in 2025, while the agricultural tractors market size for electric is projected to grow at the fastest 18.6% CAGR from 2026 to 2031.

- By tractor type, the agricultural tractors market share for utility tractors accounted for the largest 46.5% in 2025, while the agricultural tractors market size for autonomous tractors is forecast to advance at the fastest 29.5% CAGR from 2026 to 2031.

- By geography, the agricultural tractors market share for Asia-Pacific held the largest 38.6% in 2025, while the agricultural tractors market size for Africa is projected to grow at the fastest 7.6% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agricultural Tractors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government mechanization subsidy continuity | +1.1% | Global, with peak intensity in South Asia, Sub-Saharan Africa, and Eastern Europe | Medium term (2-4 years) |

| Precision agriculture integration across installed fleets | +0.9% | North America, Western Europe, large-farm segments in Brazil and Australia | Medium term (2-4 years) |

| Replacement demand for an aging tractor fleet | +0.8% | North America and Western Europe | Short term (≤ 2 years) |

| High-horsepower and 4-wheel drive adoption on large farms | +0.7% | North America, Brazil, Eastern Europe, and Australia | Medium term (2-4 years) |

| Retrofit-first autonomy and guidance upgrades | +0.5% | North America, Western Europe, and large commercial farm segments globally | Long term (≥ 4 years) |

| Specialty-crop electrification in orchards, vineyards, and greenhouses | +0.3% | Western Europe, California, New Zealand, and select Asia-Pacific specialty crop zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Mechanization Subsidy Continuity

Government-supported mechanization programs continue to play a significant role in sustaining demand for the agricultural tractors market in regions such as India, Sub-Saharan Africa, and Southeast Asia. In India, subsidies provided under the Sub-Mission on Agricultural Mechanization remain a key factor in ensuring tractors are accessible in districts with lower levels of mechanization. In Nigeria, a structured mechanization rollout in 2025 introduced 2,000 heavy-capacity tractors through mechanization service providers under a lease-to-own model, reflecting a more organized procurement strategy compared to direct public ownership. This shift influences how manufacturers approach the agricultural tractors market, as fleet intermediaries require large-scale financing, service planning, and parts support. Additionally, China’s 75.5% mechanization rate for crop planting, harvesting, and processing by 2025 serves as a benchmark for neighboring countries aiming to accelerate agricultural modernization [1]Source: United Nations Office for South-South Cooperation (UNOSSC), “UNOSSC and FAO Conclude Capacity-Building Series on Agricultural Mechanization for Inclusive Development,” unsouthsouth.org.

Precision Agriculture Integration Across Installed Fleets

Precision agriculture adoption is advancing more rapidly across existing equipment fleets than new tractor sales alone indicate. This trend is significant for the agricultural tractors market, as digital capabilities are increasingly being integrated through upgrades. The economic benefits are becoming more evident, with the Association of Equipment Manufacturers and Kearney estimating that current precision agriculture adoption has increased annual crop production in the United States by 5% and reduced fuel consumption by 147 million gallons annually in 2025 [2]Source: Association of Equipment Manufacturers (AEM), “The Benefits of Precision Ag in the United States – Final Report,” aem.org. This is driving demand for retrofitting, as mixed-brand farm operators seek unified guidance and data tools without waiting for a complete equipment replacement cycle. Consequently, the agricultural tractors market is favoring manufacturers and technology providers capable of supporting the existing equipment base, rather than relying solely on new equipment sales.

High-Horsepower and 4-Wheel Drive Adoption on Large Farms

Large grain and oilseed farms are driving the agricultural tractors market toward higher horsepower and stronger traction platforms due to the need for increased machine productivity within narrow fieldwork windows. Deere and Company, in February 2026, launched redesigned 8R and 8RX tractors, offering 440 HP, 490 HP, and 540 HP, highlighting how major manufacturers are catering to operators aiming to plant up to 1,200 acres in a single day. Similarly, Case IH introduced the Steiger 785 Quadtrac with 853 peak horsepower in 2025, addressing the requirements of the most demanding drawbar applications. However, the rising costs associated with larger engines, which require advanced aftertreatment systems, are becoming a significant consideration as platform prices increase with horsepower. Despite these cost challenges, the agricultural tractors market continues to witness growing interest in 4-wheel drive models, as larger farms benefit from improved traction, wider implements, and faster daily field coverage.

Retrofit-First Autonomy and Guidance Upgrades

Autonomy is being introduced into the agricultural tractors market primarily through upgrades and retrofit systems rather than solely through the purchase of new autonomous machines. In 2024, AGCO Corporation advanced its precision agriculture strategy by establishing PTx Trimble, enabling support for mixed fleets with brand-agnostic guidance and retrofit technologies, thereby expanding the addressable installed base. In 2026, Kubota Corporation launched its autonomous solution for the M5 Narrow tractor, developed in collaboration with Agtonomy and deployed at Treasury Wine Estates Limited. This demonstrated the integration of autonomous operations into specialty crop applications, such as mowing and under-vine cultivation, transitioning into regular field use. This trend is significant as most farms are not yet prepared to invest in entirely new autonomous fleets but are open to incremental improvements that offer labor savings and enhanced machine utilization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition cost and tighter machinery financing | -0.8% | Global, most acute in North America, Western Europe, and larger farm operations in Brazil | Short term (≤ 2 years) |

| Emissions-compliant diesel powertrain cost inflation | -0.5% | India, Europe, China, and North America, markets with active Tier 4 and Stage V equivalent mandates | Medium term (2-4 years) |

| Weak farm cash flows and seasonal credit access gaps | -0.6% | Brazil, North America, and Western Europe, where commodity price softness has been most pronounced | Short term (≤ 2 years) |

| Dealer and service-readiness gap for electric and autonomous models | -0.4% | Global, with greatest gap in Sub-Saharan Africa, Southeast Asia, and secondary markets in South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Acquisition Cost and Tighter Machinery Financing

Higher borrowing costs and tighter credit conditions are delaying purchase decisions in the US agricultural tractor market, particularly for high-value machinery categories. In the United States high-horsepower segment, retail values for tractors above 425 HP decreased by 3.2% year-over-year in 2025, while auction values declined by 6.7%. This reflects weaker buyer sentiment and the financial strain caused by elevated dealer carrying costs. The impact varies across farm sizes, with large-scale operators taking advantage of opportunities in the used-equipment market, while smaller farms face greater financing challenges and delayed replacement cycles. Consequently, the agricultural tractors market is becoming increasingly polarized, with stronger demand for advanced premium machinery and weaker demand for entry-level and utility tractor models in more price-sensitive farming segments.

Emissions-Compliant Diesel Powertrain Cost Inflation

Emissions-compliant diesel powertrains are driving up manufacturing and ownership costs in the agricultural tractors market, particularly in regions enforcing stricter nonroad engine regulations. According to the Association of Equipment Manufacturers (AEM), India’s planned transition to TREM V emission standards in April 2026 will necessitate advanced after-treatment technologies and upgraded engine systems, even for lower-horsepower tractors. This shift is projected to increase costs in a segment traditionally characterized by price-sensitive demand. Additionally, the AEM notes that China has already implemented CN Stage IV standards, while the European Union is anticipated to further tighten nonroad diesel emission regulations over the next decade. This fragmented regulatory environment is resulting in uneven compliance cost structures across regions, complicating global platform standardization and product planning for tractor manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Output: Mid-Range Dominance Masks a High-HP Shift

The agricultural tractors market share for the 40-100 HP segment led with the largest 42.9% in 2025. This segment remains dominant due to its suitability for mixed farming, haulage, tillage, and utility operations in emerging agricultural economies. Mid-range tractors are widely adopted in regions such as Asia-Pacific, South America, and parts of Africa, where farms require a balance of fuel efficiency and implement compatibility. Smaller farms favor these tractors for their operational flexibility and lower ownership costs compared to high-horsepower models. The stability in demand for this segment highlights the continued reliance on versatile, utility-focused farm mechanization.

The agricultural tractors market size for the more than 200 HP segment is forecast to grow at the fastest 7.5% CAGR from 2026 to 203. This growth is driven by increasing farm consolidation and the rising need for large-scale field productivity in regions such as North America, Brazil, and Eastern Europe. Large commercial operators are adopting higher horsepower equipment to enhance field coverage and reduce seasonal operating time. Premium manufacturers are focusing on developing advanced row-crop and high-capacity tractor platforms equipped with precision farming systems. However, mid-range tractors continue to form the structural volume base in developing agricultural economies worldwide.

By Drive Type: 4-Wheel Drive Gaining Ground on Productivity Arguments

2-wheel drive tractors accounted for the largest 71.8% of the agricultural tractors market share in 2025. These tractors maintain their dominance due to lower upfront costs, simpler maintenance requirements, and their suitability for light tillage, transport, and row-crop farming activities. They are widely preferred in regions such as India, Southeast Asia, and parts of Africa, where small and medium-sized farms prioritize affordability and operational simplicity. Additionally, the segment benefits from extensive dealer networks and lower fuel consumption in lower-horsepower applications. This combination ensures that 2-wheel drive tractors remain the preferred choice for cost-sensitive agricultural operations in several developing economies.

The agricultural tractors market size for the 4-wheel drive tractor segment is projected to grow at the fastest CAGR of 7.6% from 2026 to 2031. The adoption of higher-traction tractor systems is increasing in regions such as North America, Brazil, and Eastern Europe, driven by expanding farm sizes and the need for wider implement usage. Large commercial farms favor 4-wheel drive configurations for their ability to enhance drawbar pull, reduce wheel slippage, and support heavy-duty field operations. Manufacturers are also broadening their premium tractor portfolios with advanced hydraulic systems and precision farming technologies tailored for large-scale farming. The growth in this segment reflects rising productivity demands rather than a complete shift away from traditional 2-wheel drive platforms in global agricultural markets.

By Engine Type: Diesel's Stronghold Confronts Electric Disruption

Diesel tractors accounted for the largest 91.6% of the agricultural tractors market share in 2025. Their dominance is attributed to proven reliability, high torque output, and an established refueling infrastructure in major agricultural economies. The accessibility of service and strong field performance further reinforce the central role of diesel systems in commercial farming operations across both developed and developing regions. While hybrid systems are limited to specific heavy-duty applications requiring extended operating ranges, diesel platforms face increasing complexity and ownership costs due to evolving emission regulations. However, diesel engines continue to hold a strong position as alternative technologies encounter challenges related to infrastructure and affordability in several agricultural markets.

The agricultural tractors market share for the electric segment is projected to grow at the fastest CAGR of 18.6% from 2026 to 2031. Their adoption is gradually increasing, driven by specialty farming applications, government-supported electrification initiatives, and the integration of precision agriculture. Early opportunities are strongest in orchard, vineyard, and compact utility operations, which typically involve predictable duty cycles and shorter field ranges. Manufacturers are also integrating electrification with autonomous technologies and digital fleet management systems to enhance operational efficiency.

By Tractor Type: Autonomy Redefines the Premium Segment While Utility Anchors the Base

Utility tractors captured the largest 46.5% share in 2025. Their dominance is attributed to their versatility in applications such as tillage, transportation, field preparation, and power take-off operations. These tractors are widely adopted by small and medium-sized farms due to their ability to support multiple farming activities while offering lower ownership complexity compared to specialized premium equipment. While row-crop tractors cater to large-scale grain farming operations and orchard and vineyard tractors serve niche specialty-crop needs, utility tractors maintain strong demand across both developed and developing agricultural economies.

Autonomous tractors are forecast to advance at the fastest 29.5% CAGR from 2026 to 2031. This growth is driven by increasing labor shortages, the adoption of precision farming practices, and the need for greater operational efficiency in commercial agriculture. Autonomous systems are initially gaining traction in controlled farming environments, such as orchards and vineyards, where repetitive field patterns enhance deployment feasibility. Manufacturers are integrating advanced software platforms, remote monitoring capabilities, and machine automation with traditional tractor hardware.

Geography Analysis

Asia-Pacific held the largest 38.6% agricultural tractors market share in 2025, supported by strong mechanization demand across India and China. India remained one of the leading tractor-consuming countries globally, primarily due to the widespread adoption of utility tractors on small and medium-sized farms. China continued to enhance agricultural mechanization through increased adoption of advanced farming equipment and the expansion of domestic manufacturing capabilities. Japan and South Korea sustained demand for compact, precision-oriented tractors tailored for specialized agricultural operations. The region benefits from government-backed mechanization programs, improved rural equipment financing access, and growing local manufacturing capacity, which supports cost-effective tractor production and exports to neighboring agricultural economies worldwide.

Africa is projected to grow at the fastest 7.6% CAGR from 2026 to 2031 due to rising mechanization investments and expanding organized procurement programs. Governments in countries such as Nigeria, Ghana, Kenya, and Tanzania are increasing support for farm mechanization through tractor financing initiatives and public-private agricultural modernization programs. The region is transitioning from fragmented equipment purchases to structured distribution and service-provider models, enhancing long-term equipment accessibility. Global manufacturers are also strengthening dealer networks and distribution partnerships to improve market penetration in the region. Growth is particularly robust in countries with expanding commercial farming activities and a heightened policy focus on food security and agricultural productivity improvements.

North America and Europe experienced varied demand trends in 2025 and early 2026, driven by higher interest rates and fluctuating farm profitability, which impacted equipment purchasing decisions. Despite these challenges, replacement demand and the need for ongoing mechanization supported specific markets. According to the Association of Equipment Manufacturers (AEM), total Canadian agricultural tractor sales increased by 1.6% year-to-date as of June 2025, while sales of 4-wheel-drive tractors grew by 24.7%, indicating sustained investment in high-power farm machinery and large-scale agricultural operations [3]Source: Association of Equipment Manufacturers (AEM), “Canadian Agricultural Tractor Sales Rise Slightly in June 2025 as US Sales Continue to Drop,” newsroom.aem.org. In contrast, several Western European markets saw weaker registrations before demand gradually stabilized.

Competitive Landscape

The market remains moderately fragmented among global manufacturers, including Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and Mahindra & Mahindra Limited. These companies maintain their competitive edge through extensive dealer networks, integration of precision agriculture technologies, and diversified product portfolios spanning various horsepower categories. Global competition is increasingly shifting focus from mechanical performance to digital connectivity, telematics, and software-enabled fleet management capabilities. Meanwhile, regional manufacturers in China, India, and Eastern Europe are aggressively expanding in value-oriented segments, where affordability and localized manufacturing are key purchasing priorities for farmers.

Manufacturers are increasingly integrating hardware, precision technology, and distribution expansion into cohesive growth strategies. In 2026, Mahindra & Mahindra Limited announced plans for a large integrated tractor and automotive manufacturing facility in Nagpur to bolster long-term production capacity. Companies are also strengthening distribution partnerships in emerging agricultural economies to improve dealer access and after-sales support. These developments highlight the growing importance of technology ecosystems, software integration, and regional channel expansion alongside traditional tractor manufacturing capabilities.

Competitive opportunities are strongest in affordable precision farming systems, digital services tailored to smallholders, and infrastructure supporting autonomous equipment. Dealer consolidation is accelerating in developed markets as advanced tractors increasingly require specialized software diagnostics and connected fleet servicing capabilities. In 2025, AGCO Corporation finalized a settlement with Tractors and Farm Equipment Limited (Amalgamations Group) regarding brand use in India, Nepal, and Bhutan, refining its regional positioning strategy. Competition is increasingly centered on digital capabilities, aftermarket service execution, and regional distribution strength, rather than solely on engine performance and hardware reliability.

Agricultural Tractors Industry Leaders

Deere & Company

CNH Industrial N.V.

Kubota Corporation

AGCO Corporation

Mahindra & Mahindra Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Deere and Company introduced six new 8R and 8RX tractors with power ratings of 440 HP, 490 HP, and 540 HP. These tractors are equipped with the JD14 engine, autonomy-ready hardware, a G5Plus display featuring AutoTrac Turn Automation and AutoPath, and an Electric Variable Transmission. They are designed to support single-plug power offboarding to planters, enabling a planting capacity of up to 1,200 acres per day.

- February 2026: Mahindra and Mahindra Limited announced plans for an INR 15,000 crore (USD 1.75 billion) integrated auto and tractor manufacturing facility in Nagpur, Maharashtra. The facility will cover 1,500 acres and is designed with an annual production capacity exceeding 100,000 tractors. This initiative aims to strengthen the company's domestic market leadership and support export market expansion.

- January 2026: Kubota Corporation introduced a commercialized autonomous solution for its 105.7 HP M5 Narrow tractor at the Consumer Electronics Show (CES) 2026. Developed in collaboration with Agtonomy, this solution is designed for specialty crop applications such as mowing and under-vine cultivation. Treasury Wine Estates has deployed four units in North Napa Valley, with one operator managing three machines simultaneously.

Global Agricultural Tractors Market Report Scope

A tractor is a farm vehicle that is used to pull farm machinery and provide the energy needed for the machinery to work. It helps to reduce the time required by farming operations and makes it easy. For this report, tractors used in agricultural operations in farming have been considered. The agricultural tractors market report is segmented by power output (less than 40 HP, 40-100 HP, 101-200 HP, and more than 200 HP), by drive type (2-wheel drive and 4-wheel drive), by engine type (diesel, electric, and hybrid), by tractor type (utility, row-crop, orchard and vineyard, and autonomous), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

By Power Output

| Less than 40 HP |

| 40-100 HP |

| 101-200 HP |

| More than 200 HP |

By Drive Type

| 2-Wheel Drive |

| 4-Wheel Drive |

By Engine Type

| Diesel |

| Electric |

| Hybrid |

By Tractor Type

| Utility |

| Row-Crop |

| Orchard and Vineyard |

| Autonomous |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| United Kingdom | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Power Output | Less than 40 HP | |

| 40-100 HP | ||

| 101-200 HP | ||

| More than 200 HP | ||

| By Drive Type | 2-Wheel Drive | |

| 4-Wheel Drive | ||

| By Engine Type | Diesel | |

| Electric | ||

| Hybrid | ||

| By Tractor Type | Utility | |

| Row-Crop | ||

| Orchard and Vineyard | ||

| Autonomous | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| United Kingdom | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the agricultural tractors market by 2031?

The agricultural tractors market is forecast to reach USD 103.1 billion by 2031.

Which region leads global demand for agricultural tractors?

Asia-Pacific accounted for the largest 38.6% market share in 2025.

Which horsepower range is most important in tractor demand today?

The 40-100 HP segment led with the largest 42.9% market share in 2025.

What is driving growth rate in autonomous tractors?

Autonomous tractors are forecast to grow at the fastest 29.5% CAGR from 2026 to 2031.

Page last updated on: