Laptop Backpacks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

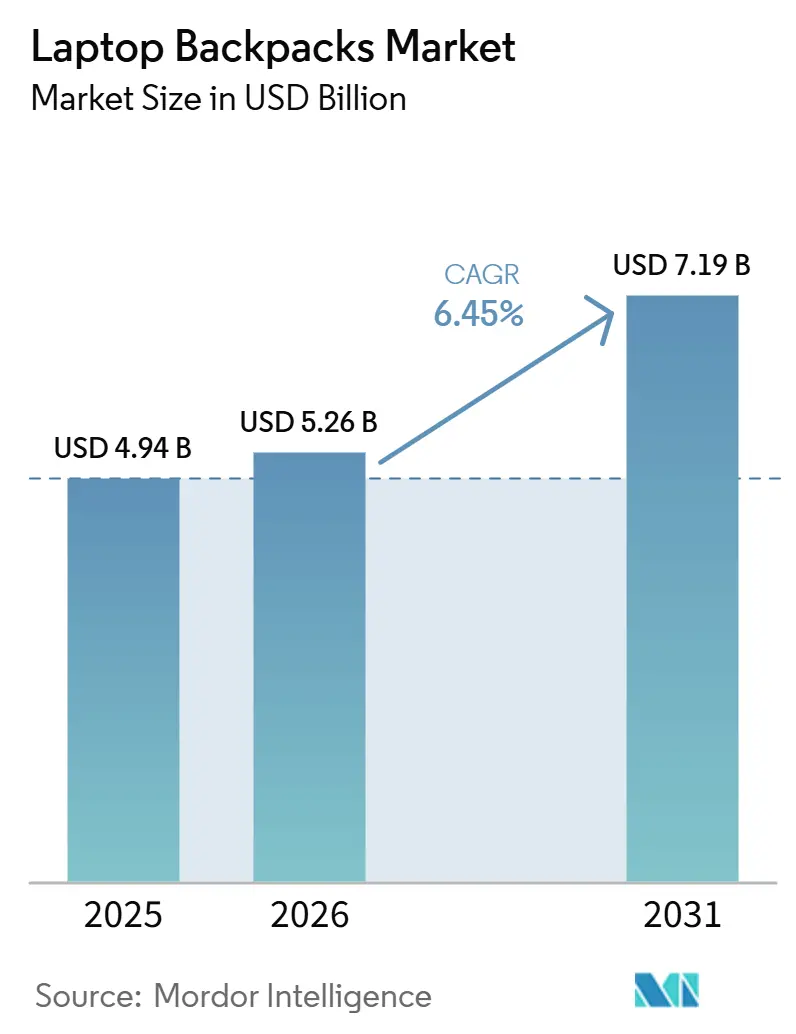

| Market Size (2026) | USD 5.26 Billion |

| Market Size (2031) | USD 7.19 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Laptop Backpacks Market Analysis by Mordor Intelligence

The global laptop backpacks market size is expected to grow from USD 4.94 billion in 2025 to USD 5.26 billion in 2026 and is forecast to reach USD 7.19 billion by 2031 at a 6.45% CAGR over 2026-2031. The global laptop backpacks market is driven by the increasing integration of digital devices into daily life, particularly among students, professionals, and remote workers who require secure and organized solutions for carrying laptops and accessories. The growing demand for mobility and hybrid work models has heightened the need for ergonomic, lightweight, and multifunctional backpacks suitable for commuting and travel. Product innovations, such as anti-theft compartments, USB charging ports, water-resistant materials, and smart storage designs, are enhancing consumer interest. Furthermore, the rising popularity of e-commerce platforms has improved product accessibility and variety. Fashion-conscious consumers are also contributing to demand by seeking aesthetically appealing and customizable designs. Sustainability trends are shaping purchasing decisions, with manufacturers focusing on eco-friendly materials and ethically produced backpacks, thereby supporting market growth.

Key Report Takeaways

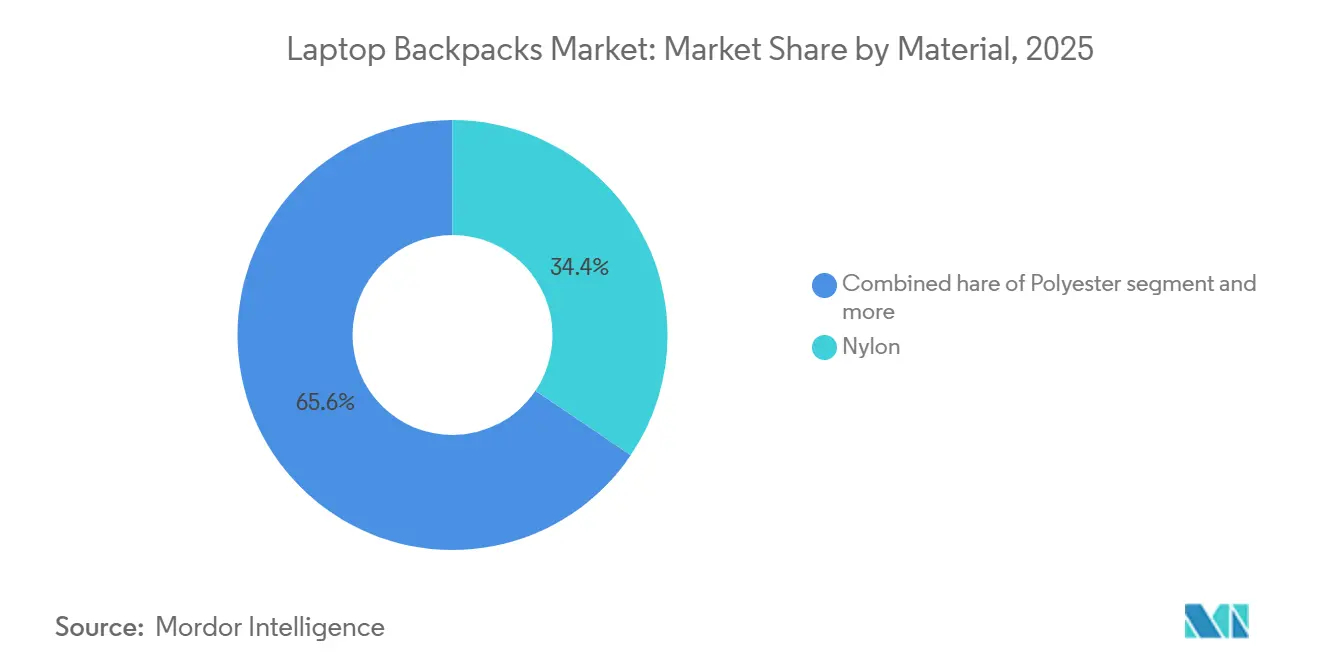

- By material, nylon led with 34.43% of 2025 revenue, while polyester is forecast to post a 6.86% CAGR through 2031.

- By category, the mass tier captured 81.04% share in 2025; however, premium offerings are on track for a 7.19% CAGR.

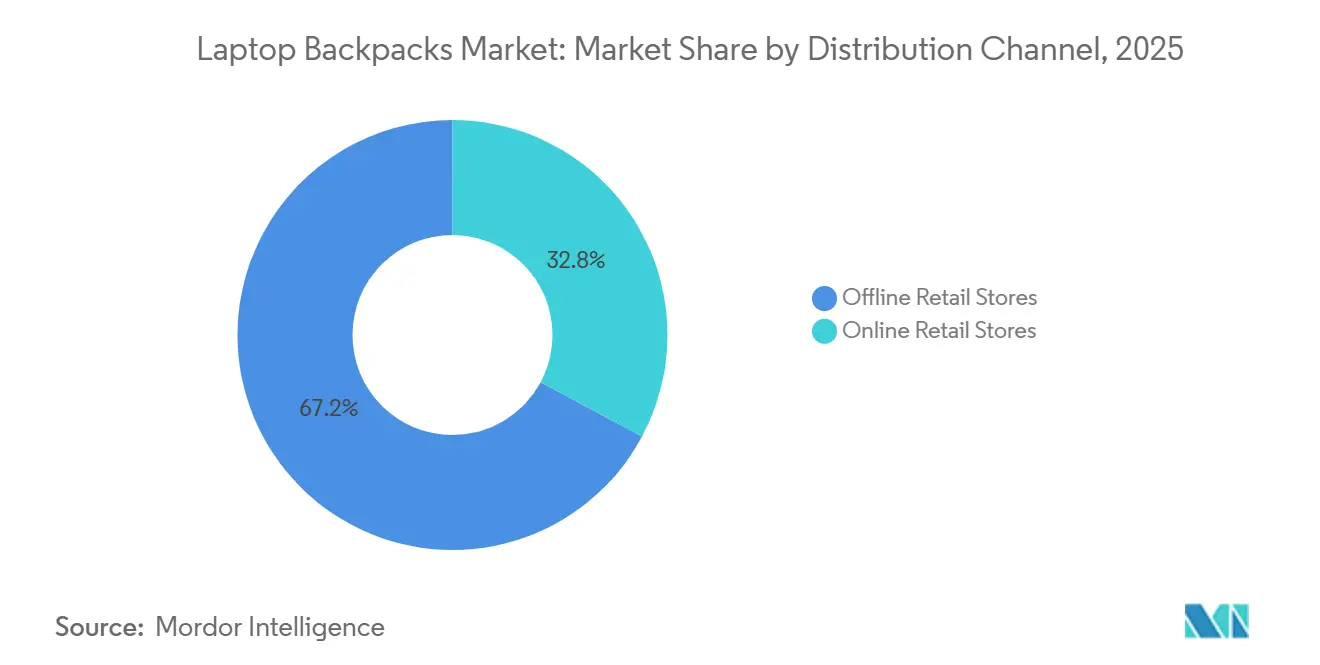

- By distribution channel, offline retail controlled 67.18% of 2025 sales, while online platforms, however, are set to advance at a 7.08% CAGR.

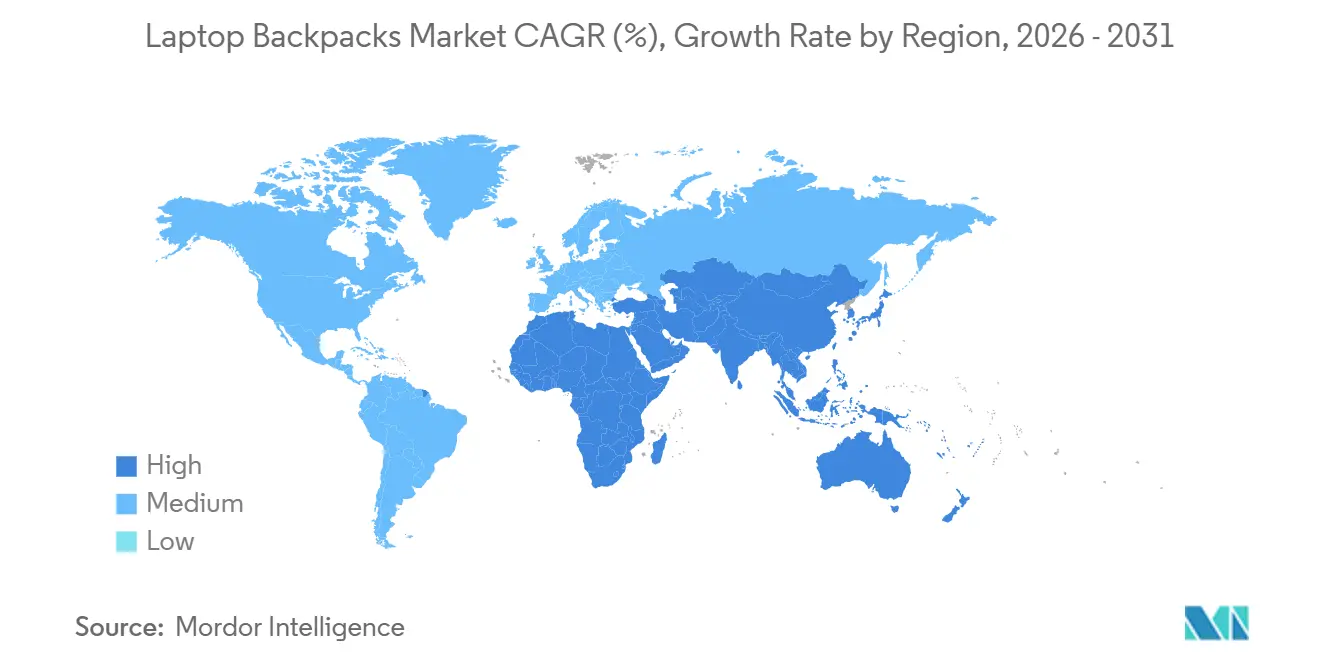

- By geography, North America accounted for 34.57% of 2025 revenue, whereas Asia-Pacific is projected to grow at 6.81% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Laptop Backpacks Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising digitalization and device dependency | +1.4% | Global, with concentration in North America and Asia-Pacific urban centers | Medium term (2-4 years) |

| Expansion of e-learning and digital education | +1.2% | Global, strongest in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Integration of smart features | +0.9% | North America and Europe early adoption, Asia-Pacific volume scale | Short term (≤ 2 years) |

| Rising travel and mobility trends | +1.1% | Global, led by North America and Europe business corridors | Medium term (2-4 years) |

| Sustainability and eco-friendly material adoption | +0.7% | Europe regulatory push, North America corporate procurement | Long term (≥ 4 years) |

| Growth of e-commerce and direct-to-consumer channels | +0.6% | Asia-Pacific infrastructure build-out, North America maturation | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising digitalization and device dependency

Increasing digitalization and reliance on electronic devices are key factors driving the global laptop backpacks market. As individuals depend more on laptops, tablets, and related accessories for work, education, and entertainment, the demand for secure and portable storage solutions has grown. The adoption of digitally enabled lifestyles, supported by remote work, online learning, and flexible office arrangements, has further amplified this need. Laptop backpacks have evolved from basic utility products to essential daily carriers, designed to protect valuable devices while providing convenience and organization. This trend is supported by changing work patterns. According to the U.S. Census Bureau, in 2023, 35% of employed individuals worked from home on workdays, while 73% worked at a physical workplace, reflecting a prevalent hybrid work culture[1]Source: U.S. Bureau of Labor Statistics, "35 percent of employed people did some or all of their work at home on days they worked in 2023," bls.gov. This dual-mode working environment requires frequent transportation of devices, driving demand for durable, functional, and technology-friendly backpacks that cater to modern digital requirements.

Expansion of e-learning and digital education

The growth of e-learning and digital education is a key factor driving the global laptop backpacks market. Students across various age groups increasingly rely on laptops and tablets for virtual classrooms, assignments, and collaborative learning. Educational institutions are adopting digital tools, learning management systems, and online resources as part of their teaching methods, reducing dependence on traditional materials and making electronic devices essential. This transition has led to a heightened demand for backpacks designed to securely carry laptops, chargers, books, and other study essentials in an organized manner. Furthermore, the adoption of hybrid education models, where students alternate between home-based and on-campus learning, has increased the need for frequent device transportation. This has further driven the demand for durable, lightweight, and ergonomically designed laptop backpacks suited for academic purposes.

Integration of smart features

The integration of smart features into laptop backpacks is becoming a significant driver in the global market, as consumers increasingly prefer technologically advanced products that align with their connected lifestyles. Laptop backpacks are transitioning from basic storage solutions to multifunctional products with features such as built-in USB charging ports, RFID-blocking pockets, anti-theft locking systems, and location-tracking capabilities. These enhancements provide added convenience, security, and usability, appealing particularly to tech-savvy professionals, students, and frequent travelers who prioritize device safety and functionality. For instance, on June 1, 2023, Targus launched its Cypress™ Hero Backpack with Find My® Locator, which includes a tracking module compatible with Apple devices, allowing users to locate their belongings using an iPhone, iPad, or Mac. These developments demonstrate how the integration of technology into everyday accessories is reshaping consumer expectations and driving the adoption of smart laptop backpacks globally.

Rising travel and mobility trends

Increasing travel and mobility trends are driving the growth of the global laptop backpacks market, as more individuals engage in frequent business trips, commuting, and leisure travel while carrying essential electronic devices. Professionals, digital nomads, and students seek convenient, compact, and secure solutions to transport laptops and accessories, boosting the demand for versatile backpacks designed for mobility. Key features such as lightweight construction, organized compartments, airport-friendly designs, and enhanced security are becoming important factors influencing purchasing decisions. This trend is further supported by the recovery and expansion of global air travel. According to the International Air Transport Association, total passenger demand increased by 3.8% year-on-year in January 2026[2]Source: International Air Transport Association (IATA), "2026 Begins with 3.8% Air Passenger Demand Growth," iata.org. Moreover, international passenger demand rose by 5.9% and reached record-high load factors[3]Source: International Air Transport Association (IATA), "2026 Begins with 3.8% Air Passenger Demand Growth," iata.org. The growth in passenger traffic highlights increased global movement, directly driving the demand for laptop backpacks that facilitate safe and efficient travel with digital devices.

Restraints Impact Analysis of Laptop Backpacks Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense competition from alternative carrying solutions | -0.8% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Counterfeit and unbranded product proliferation | -0.6% | Asia-Pacific manufacturing hubs, e-commerce platforms globally | Medium term (2-4 years) |

| Compatibility and size limitations | -0.4% | Global, acute in premium gaming and ultra-portable segments | Medium term (2-4 years) |

| Environmental concerns related to synthetic materials | -0.3% | Europe regulatory pressure, North America corporate responsibility | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intense competition from alternative carrying solutions

Intense competition from alternative carrying solutions serves as a significant restraint on the global laptop backpacks market. Consumers have access to a variety of substitutes that fulfill similar functional requirements while catering to diverse design preferences. Alternatives such as laptop messenger bags, briefcases, tote bags, rolling laptop cases, and protective sleeves provide distinct advantages in terms of style, portability, and professional appeal, attracting specific user groups. For example, corporate professionals favor sleek briefcases or messenger bags for formal environments, while travelers might prefer wheeled cases to minimize physical strain. Similarly, minimalist consumers often opt for compact sleeves that can be placed inside other luggage, eliminating the need for dedicated backpacks. This wide range of alternatives reduces the exclusive use of laptop backpacks, intensifies competition based on price and features, and pressures manufacturers to innovate continuously, thereby limiting overall market growth.

Counterfeit and unbranded product proliferation

The widespread availability of counterfeit and unbranded products poses a significant challenge to the global laptop backpacks market. These products undermine brand value, reduce profit margins, and diminish consumer trust. Low-cost imitations, often made with substandard materials and lacking quality assurance, are prevalent in informal retail channels and online marketplaces. This makes it difficult for established brands to compete solely on price. Such products appeal to price-sensitive consumers, particularly in emerging markets, diverting demand from authentic, higher-quality backpacks. Furthermore, counterfeit goods often fail to provide adequate protection for electronic devices, resulting in negative user experiences that can indirectly harm the reputation of the entire category. The presence of these alternatives intensifies competition, restricts pricing power for legitimate manufacturers, and creates ongoing challenges related to intellectual property protection and brand positioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Laptop Backpacks Market Segment Analysis

By Material:

Recycled Polyester Gains on Performance and ComplianceIn 2025, nylon accounted for 34.43% of the global laptop backpacks market, driven by its superior durability, lightweight properties, and high resistance to wear and tear. These characteristics make it particularly suitable for frequent travelers, commuters, and students who require reliable, long-lasting backpacks. Nylon's natural water-resistant properties and ability to endure harsh environmental conditions further enhance its effectiveness in protecting electronic devices, especially in unpredictable weather. Additionally, its premium appearance appeals to professionals seeking a balance of functionality and aesthetics. The material's flexibility allows manufacturers to incorporate advanced design features, such as multiple compartments, ergonomic structures, and reinforced padding, without adding significant weight. The increasing demand for durable, high-performance backpacks in urban mobility and travel-focused lifestyles continues to drive the preference for nylon in the market.

Polyester is projected to grow at a CAGR of 6.86% during 2026-2031, supported by its cost-effectiveness, versatility, and ease of mass production. These attributes make polyester backpacks accessible to a wide range of consumers across various price segments. The material's resistance to shrinking, stretching, and wrinkling ensures consistent shape retention and durability, making it particularly appealing to students and daily commuters. Polyester's adaptability to diverse colors, prints, and textures enables manufacturers to create fashionable and customizable designs that align with changing consumer preferences. Additionally, advancements in recycled polyester production are fostering alignment with sustainability trends, encouraging environmentally conscious consumers to choose eco-friendly backpack options. The combination of affordability, design flexibility, and increased availability through offline and online retail channels continues to drive the global demand for polyester backpacks.

By Category:

Premium Tier ExpandsMass-market products accounted for an 81.04% share in 2025, primarily due to their affordability and widespread accessibility. These products are the preferred choice for students, entry-level professionals, and price-sensitive consumers. They address essential needs by providing basic laptop protection, functional storage, and durable construction at competitive price points. Factors such as rapid urbanization, increasing enrollment in educational institutions, and the growing use of laptops for daily activities are further driving demand in this segment. Additionally, the expansion of e-commerce platforms and organized retail has facilitated access to a wide range of budget-friendly options, enabling consumers to conveniently compare features and prices. Manufacturers in this segment emphasize high-volume production and standardized designs, which help maintain low costs while meeting the functional requirements of a broad consumer base.

Premium offerings are projected to grow at a 7.19% CAGR during 2026-2031, driven by increasing consumer preference for high-quality, feature-rich, and aesthetically refined products that combine functionality with style. Professionals, business travelers, and tech-savvy users are showing a greater willingness to invest in backpacks that offer enhanced durability, superior materials such as ballistic nylon or leather accents, and advanced features like anti-theft systems, smart tracking, USB charging ports, and ergonomic support. Brand reputation, design innovation, and product differentiation significantly influence purchasing decisions in this segment. Furthermore, the rising focus on lifestyle-oriented products and status-driven consumption is boosting demand for premium backpacks that align with personal identity and professional image. Sustainability trends are also playing a role, as many premium brands incorporate eco-friendly materials and ethical production practices, enhancing their appeal among environmentally conscious consumers.

By Distribution Channel:

Offline Retail Holds GroundOffline retail stores accounted for a 67.18% market share in 2025, driven by consumers' preference for physically evaluating products. This allows them to assess factors such as material quality, comfort, size, and storage capacity before purchasing. The ability to try on backpacks and check for ergonomic fit is particularly significant for students, professionals, and travelers who prioritize comfort for daily use. In-store assistance from sales personnel further supports buyers in making informed decisions based on specific needs, such as device size compatibility and usage patterns. Additionally, the presence of exclusive brand outlets, supermarkets, and specialty stores enhances product visibility and builds trust, especially in regions where consumers remain cautious about online purchases. Immediate product availability without delivery delays and the assurance of easy returns or exchanges also contribute to the sustained demand for offline retail channels.

Online platforms are projected to grow at a 7.08% CAGR during 2026-2031, supported by the convenience of anytime, anywhere shopping and access to a wide range of brands, designs, and price points on a single platform. Consumers benefit from detailed product descriptions, customer reviews, and comparison tools, enabling more informed purchasing decisions. Competitive pricing, frequent discounts, and bundled offers further enhance the appeal of online platforms, particularly for price-sensitive buyers. The increasing adoption of smartphones, digital payment systems, and improved logistics infrastructure has made online shopping more accessible and reliable in both urban and semi-urban areas. Additionally, easy return policies and fast delivery options have reduced perceived risks, encouraging more consumers to adopt online channels for purchasing laptop backpacks.

Geography Analysis

North America Laptop Backpacks Market

North America accounted for 34.57% of the 2025 revenue, driven by the widespread use of digital devices, a well-established remote and hybrid work culture, and strong consumer preference for technologically advanced and ergonomic products. A significant base of professionals, students, and frequent travelers depends on laptops for daily activities, sustaining consistent demand for protective and functional backpacks. The region also demonstrates high adoption of premium products, with consumers prioritizing features such as anti-theft designs, USB charging ports, and smart tracking capabilities. Additionally, the presence of leading brands, developed retail infrastructure, and heightened awareness of product quality and sustainability further bolster market growth, as buyers increasingly prefer durable and eco-friendly materials.

APAC Laptop Backpacks Market

The Asia-Pacific region is projected to grow at a CAGR of 6.81% during 2026-2031, driven by a rising student population, increasing adoption of digital education, and a growing number of working professionals in emerging economies. Rapid urbanization and the expansion of middle-class populations are contributing to greater laptop usage for academic and professional purposes. The region’s robust manufacturing base supports cost-effective production, making backpacks more affordable and accessible to diverse income groups. Furthermore, the booming e-commerce sector, combined with widespread smartphone usage, has significantly enhanced product availability and consumer reach. Demand is also supported by a mix of price-sensitive buyers opting for mass-market products and an emerging segment of consumers seeking stylish, branded, and feature-rich backpacks.

EMEA and South America Laptop Backpacks Market

In Europe, South America, and the Middle East & Africa, the laptop backpacks market is influenced by evolving work patterns, increasing digital connectivity, and growing mobility trends. In Europe, demand is driven by a strong emphasis on sustainability and premium product design, with consumers favoring high-quality, environmentally responsible backpacks. In South America, improving access to education and the rising adoption of digital tools are fueling demand for affordable and durable options. Meanwhile, in the Middle East & Africa, expanding urban centers, a growing youth population, and gradual digital transformation are encouraging laptop usage in both educational and professional contexts. Across these regions, the influence of global fashion trends, the expansion of retail networks, and the increasing penetration of online shopping platforms collectively support steady market growth.

Competitive Landscape

The global laptop backpacks market exhibits moderate fragmentation, with competition spanning traditional luggage manufacturers, technology-focused accessory providers, and lifestyle-oriented brands. This competitive environment is supported by relatively low barriers to entry, as production can be outsourced to cost-efficient manufacturing hubs, allowing new entrants to participate without significant capital investment. Additionally, diverse consumer preferences regarding design, functionality, and pricing hinder market consolidation, ensuring that no single segment or product type achieves universal dominance.

Market competition is shaped by varying strategic approaches among participants. Some companies emphasize product durability, extensive retail networks, and established consumer trust, while others focus on compatibility with electronic devices and adapting to changing workplace and academic requirements. The emergence of digitally native brands has further intensified competition by introducing design-focused products and engaging consumers directly through online platforms. This has driven companies to prioritize product differentiation, aesthetic appeal, and user-centric features in an effort to stand out in a market where functional similarities are prevalent.

Innovation in product design and shifting consumer expectations are key areas of emerging competition. Modular backpack concepts, which allow users to customize compartments and accessories, are gaining popularity as they align with personalization trends and sustainability goals by extending product lifecycles. Additionally, the integration of advanced technological features is gradually gaining traction, though adoption remains limited due to concerns over cost, practicality, and regulatory compliance. Furthermore, adherence to ergonomic and safety standards is becoming increasingly significant, particularly in regions with stringent occupational health regulations. This focus on compliance offers manufacturers an opportunity to differentiate their products and strengthen their market position.

Laptop Backpacks Industry Leaders

-

Samsonite International S.A.

-

Targus Corp.

-

Thule Group AB

-

VIP Industries Ltd.

-

Nike Inc.

- *Disclaimer: Major Players sorted in no particular order

Laptop Backpacks Market Companies Covered in this Report

- Samsonite International S.A.

- Targus Corp.

- Thule Group AB

- VIP Industries Ltd (Skybags)

- Nike Inc.

- HP Inc.

- Lenovo Group Ltd.

- Dell Technologies Inc.

- Incase Designs Corp.

- Herschel Supply Co.

- The North Face (VF Corp.)

- ASUStek Computer Inc.

- American Tourister

- SwissGear (Wenger SA)

- Safari Industries (Urban Jungle)

- Osprey Packs Inc.

- BANGE Luggage

- Xiaomi (Mi Business backpacks)

- Fjällräven AB

- ASUS Republic of Gamers (ROG)

Recent Industry Developments in Laptop Backpacks Market

- June 2025: Urban Jungle made its debut in Pune, unveiling its first exclusive store. The store showcases a range of contemporary backpacks tailored for today's urban, on-the-go consumers. These backpacks are designed with a focus on functionality and style, featuring a dedicated laptop compartment to meet the needs of mobile professionals and students.

- May 2025: Tolaccea launched a new Travel Laptop Backpack tailored to meet the changing requirements of modern professionals and frequent travelers. Designed with a focus on practicality, durability, and versatility, the backpack is suitable for daily commutes as well as long-distance travel. It features well-organized compartments, durable materials, and user-focused elements aimed at improving organization, carrying comfort, and convenience. In addition to its role as a standard backpack, it serves as a mobility-focused solution for active and on-the-go lifestyles.

- April 2025: Wenger unveiled its latest offering: a durable backpack boasting a triple-protection laptop compartment and airflow back padding for enhanced comfort during extended use. This eco-friendly product is crafted from recycled PET bottles, aligning with the company's commitment to sustainability.

- February 2025: Targus HeritageLuxe introduced its executive backpack, packed with advanced features such as Blue Shock protection to safeguard devices, USB-C charging for convenience, and interiors made from recycled materials. This product is designed to cater to professionals seeking both functionality and environmental responsibility.

Global Laptop Backpacks Market Report Scope

Segmentation Overview

| Nylon |

| Polyester |

| Others |

| Mass |

| Premium |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East and Africa |

| By Material | Nylon | |

| Polyester | ||

| Others | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Why do premium laptop backpacks outpace mass-market growth?

Enterprise procurement bundles warranty-backed premium backpacks with laptop refreshes, driving a 7.19% CAGR in the premium tier.

How fast will the laptop backpacks market grow through 2031?

It is projected to rise at a 6.45% CAGR from 2026 to 2031, lifting value from USD 5.26 billion in 2026 to USD 7.19 billion by 2031.

Which material segment is gaining most rapidly?

Polyester is the fastest riser, forecast at a 6.86% CAGR owing to regulatory compliance and lighter-weight strength.

Which region offers the strongest future upside?

Asia-Pacific leads with a 6.81% projected CAGR as rising student populations in China and India upgrade to purpose-built models.

Page last updated on: