B2B SaaS Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.49 Trillion |

| Market Size (2031) | USD 1.58 Trillion |

| Growth Rate (2026 - 2031) | 26.24% CAGR |

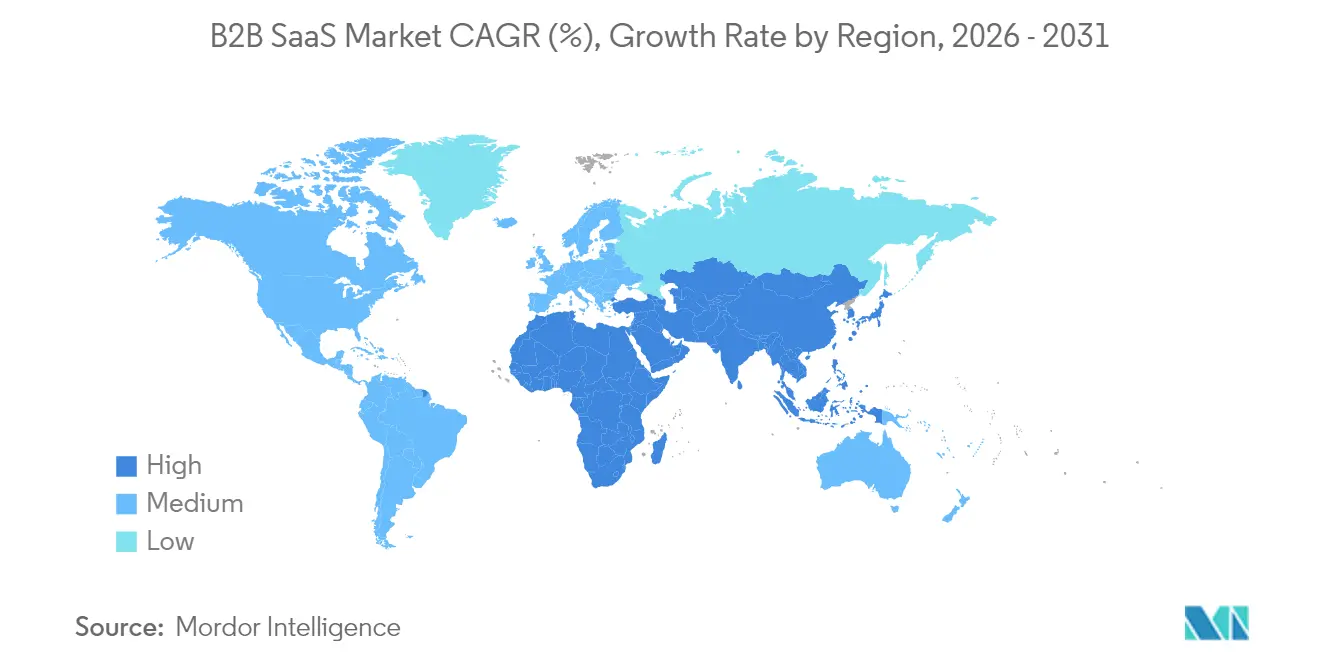

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

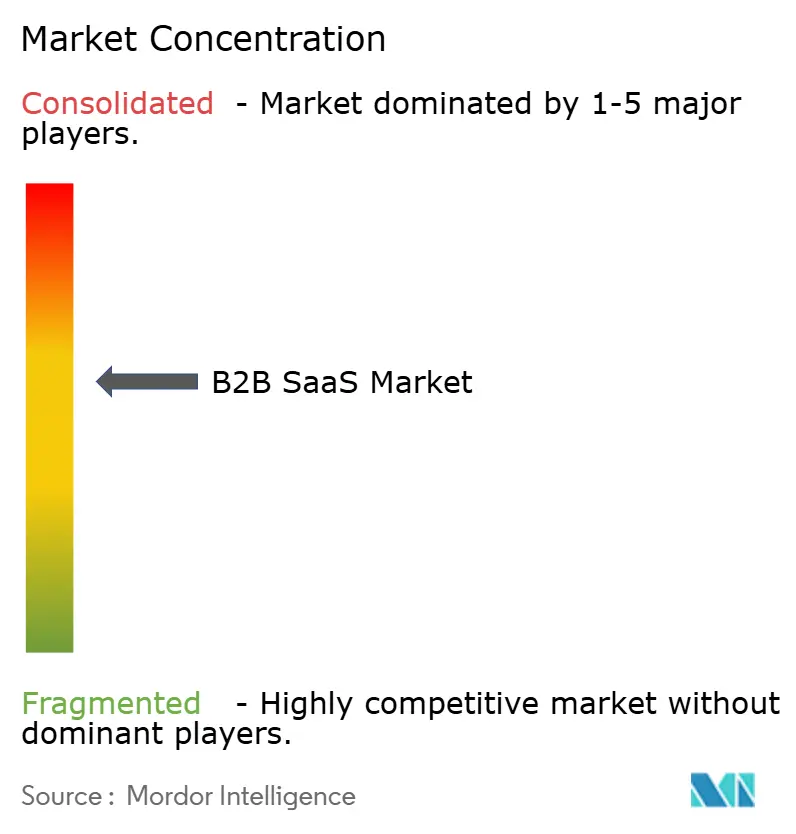

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

B2B SaaS Market Analysis by Mordor Intelligence

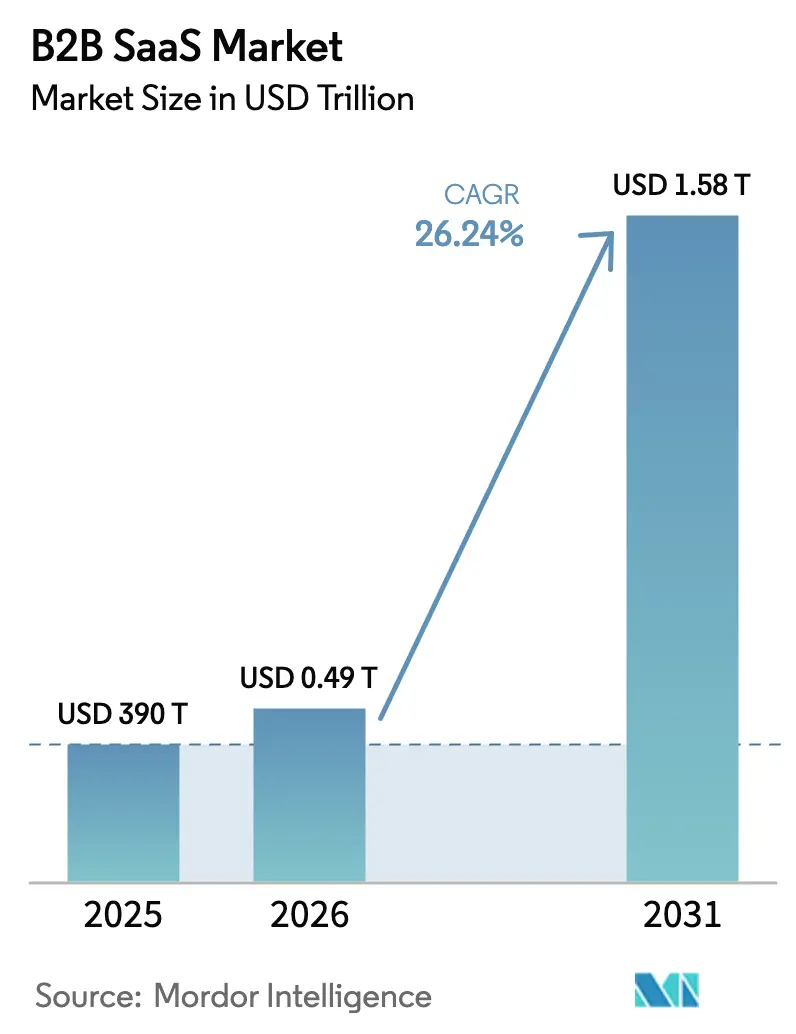

The B2B SaaS market size was valued at USD 390 billion in 2025 and estimated to grow from USD 492.34 billion in 2026 to reach USD 1578.2 billion by 2031, at a CAGR of 26.24% during the forecast period (2026-2031). Surging adoption of generative-AI copilots, cloud-first transformation budgets, and flexible usage-based pricing are steering the shift from perpetual licensing to outcome-driven consumption. Enterprises view autonomous AI agents as a pathway to measurable business impact, while regulators in the European Union and elsewhere channel demand toward compliant cloud solutions. Vertical SaaS specialties, most notably in healthcare, open fresh revenue streams as providers integrate telemedicine workflows with diagnostic AI. Heightened investment activity, illustrated by IBM’s USD 6.4 billion HashiCorp acquisition, underlines the competitive race to embed cloud-native stacks and cross-platform integrations.

Key Report Takeaways

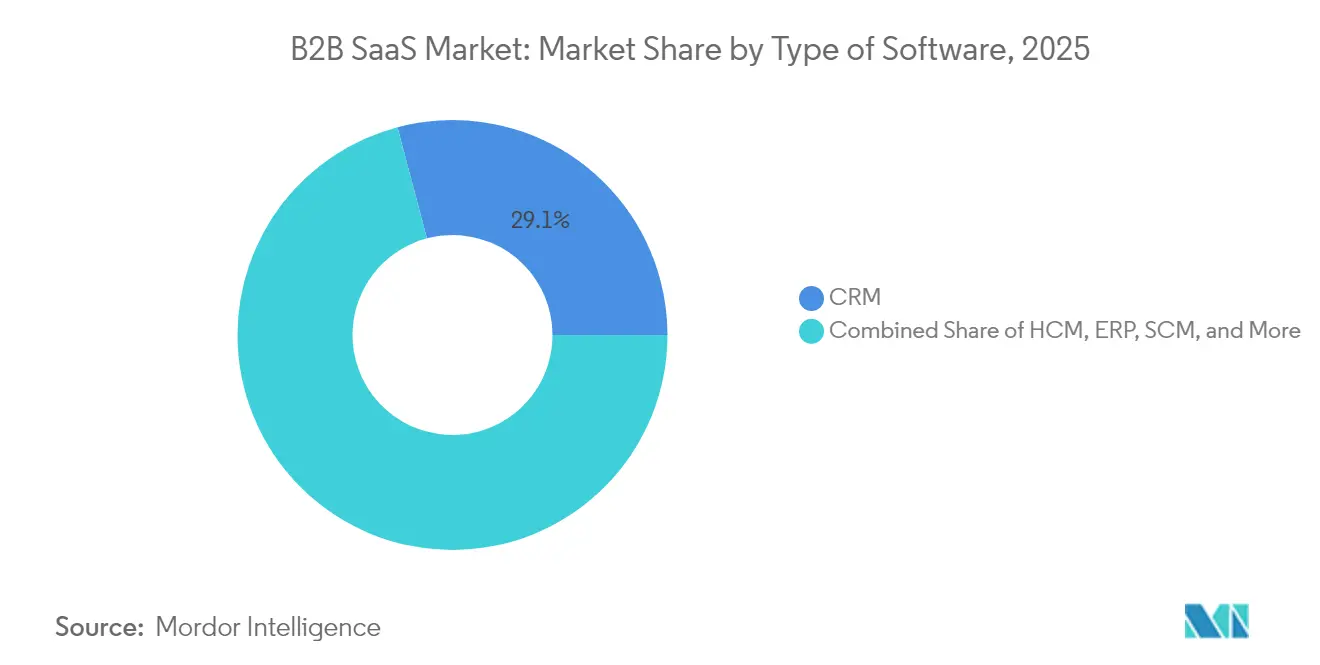

- By type of software, Customer Relationship Management captured 29.12% of the B2B SaaS market share in 2025; Enterprise Resource Planning is expanding at an 17.75% CAGR through 2031.

- By deployment model, the public-cloud segment held 61.85% share of the B2B SaaS market size in 2025, while hybrid-cloud configurations are advancing at a 26.20% CAGR to 2031.

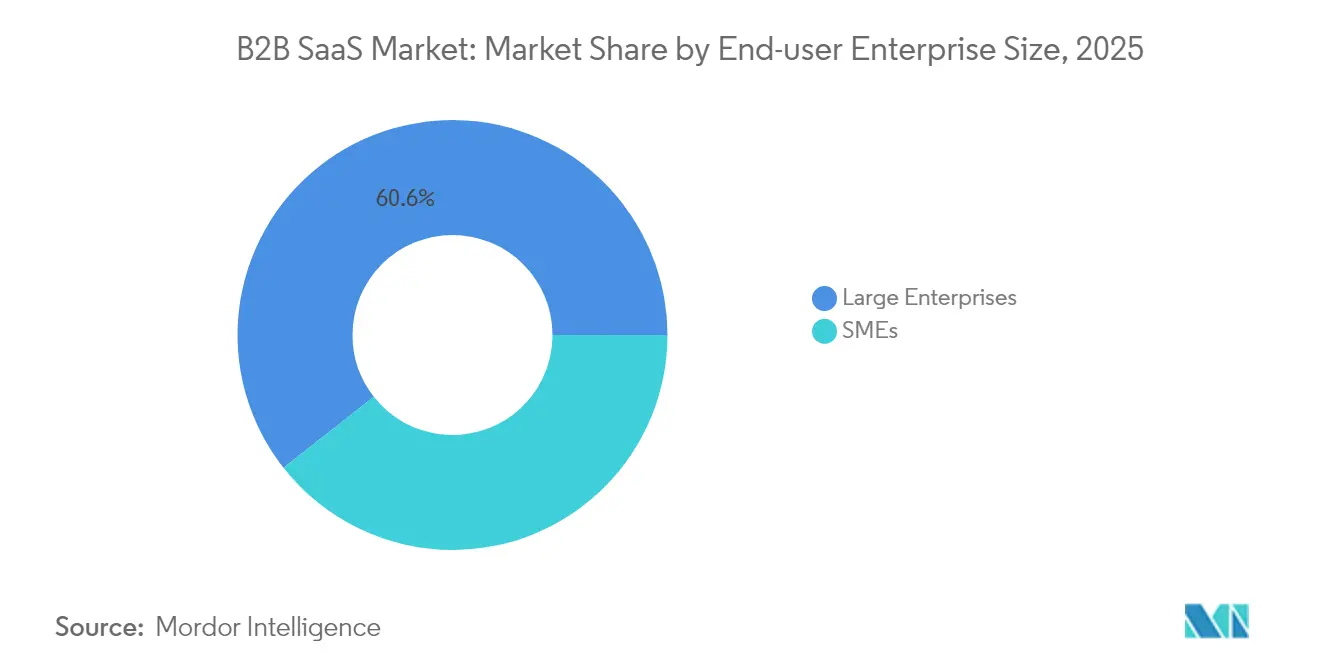

- By end-user enterprise size, large enterprises accounted for 60.60% of the B2B SaaS market in 2025; small and medium enterprises are forecast to rise at a 22.80% CAGR through 2031.

- By end-user industry, Banking, Financial Services, and Insurance led with 24.05% share of the B2B SaaS market in 2025, whereas healthcare is projected to grow at a 29.50% CAGR to 2031.

- By geography, North America retained a 32.85% revenue share in 2025; Asia-Pacific posts the fastest regional CAGR at 24.60% over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global B2B SaaS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first digital-transformation budgets | +8.2% | Global, led by North America and EU | Medium term (2-4 years) |

| Remote-work adoption sustaining SaaS collaboration demand | +5.1% | Global, strong in Asia-Pacific | Short term (≤ 2 years) |

| API-led integrations reducing vendor-lock-in concerns | +4.7% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Generative-AI copilots embedded in vertical SaaS | +6.9% | Global, early focus on North America | Long term (≥ 4 years) |

| Rise of micro-SaaS for niche workflows | +3.2% | Global, traction in developed markets | Long term (≥ 4 years) |

| ESG-driven Green-SaaS preferences | +2.1% | EU leading, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Digital Transformation Budgets

Enterprises continue reallocating capital from hardware refresh cycles toward scalable cloud services that compress innovation timelines and enable rapid product iteration. The United Kingdom’s National Digital Exchange alone is expected to reduce public procurement expenses by USD 1.2 billion each year, reinforcing the economic rationale for software-as-a-service [1]Department for Science, Innovation and Technology, “Transforming Public Procurement through the National Digital Exchange,” gov.uk. CIOs increasingly anchor transformation roadmaps around B2B SaaS platforms because they deliver continuous feature releases rather than multi-year version upgrades. AI and analytics embedded inside these cloud stacks further increase ROI by turning data exhaust into actionable insights.

Generative-AI Copilots Embedded in Vertical SaaS

Context-aware copilots are elevating day-to-day workflows within healthcare, finance, and customer service. Salesforce’s Agentforce enables autonomous ticket resolution, cutting human involvement while safeguarding customer experience. Competitive differentiation now rests on depth of domain expertise woven into each AI model rather than on generic language capabilities. As generative models become commoditized, vendors with vertical knowledge bases and curated data flywheels are positioned to win outsized value capture.

API-Led Integrations Reducing Vendor Lock-In Concerns

Chief technology officers are embracing composable architectures in which discrete best-of-breed applications communicate via standardized APIs. Integration readiness is thus a top selection criterion, forcing vendors to open ecosystems previously guarded by proprietary interfaces. The shift reshapes go-to-market strategies: providers compete on distinct functional excellence rather than broad feature checklists. Seamless data portability also lowers switching costs, stimulating a more dynamic competitive field within the B2B SaaS market.

Remote Work Adoption Sustaining SaaS Collaboration Demand

Hybrid work patterns maintain steady appetite for collaboration suites that fuse messaging, video, file sharing, and workflow automation. A 2025 SMB survey showed 91% of firms using AI-powered analytics reported higher revenue after adopting cloud collaboration tools. Asia-Pacific small and midsize enterprises, buoyed by governmental digitization grants, account for much of the incremental demand. Outcome-driven productivity metrics, surfaced through SaaS dashboards, anchor continued license renewals and net-new seat growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent data-sovereignty and privacy regulations | −4.3% | EU leading with GDPR/NIS2, expanding globally | Medium term (2-4 years) |

| Talent shortage in cloud security and FinOps | −2.8% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Surging generative-AI inference costs compressing margins | −3.1% | Global, affects AI-intensive providers | Short term (≤ 2 years) |

| Heightened vendor-due-diligence in MandA exits | −1.9% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Data Sovereignty and Privacy Regulations

The EU’s NIS2 directive obliges SaaS vendors handling critical infrastructure data to implement strict access controls and incident reporting, increasing compliance overhead and prolonging deal cycles. Enterprises now demand regionally isolated data centers and granular audit logs, favoring local providers already compliant with jurisdiction-specific rules. The US Securities and Exchange Commission’s 2024 cybersecurity disclosure rules add an extra layer of scrutiny for publicly listed customers, amplifying due diligence workloads. These overlapping requirements delay deployments and redirect R&D funds toward regulatory tooling.

Surging Generative-AI Inference Costs Compressing Gross Margins

As user interactions surge, compute-intensive inference workloads inflate cost-of-goods sold for AI-centric SaaS firms. Providers navigate a delicate balance between absorbing costs to defend market share and repricing tiers to preserve profitability. Forward-looking strategies include model distillation, intelligent caching, and hybrid fixed-plus-usage pricing to stabilize margins amid volatile GPU spot pricing. The constraint is most acute for vertical SaaS vendors whose core differentiation hinges on AI embedded deep in industry workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Software: CRM Dominance Meets ERP Innovation

Customer Relationship Management software retained 29.12% of B2B SaaS market share in 2025, reflecting its central role in driving revenue and loyalty programs. Salesforce alone reported USD 34.9 billion in fiscal 2024 revenue, underlining the segment’s scale . In parallel, Enterprise Resource Planning platforms are forecast to register an 17.75% CAGR through 2031, propelled by AI-enabled manufacturing digitization. Underlying market movement signals a convergence toward integrated operating systems where CRM, ERP, and supply-chain modules operate on a common data schema, simplifying analytics and governance.

Second-tier categories such as Human Capital Management and Supply-Chain Management maintain steady expansion as cloud scalability and advanced analytics elevate HR workflows and logistics visibility. The “Others” basket spans cybersecurity, data analytics, and vertical point solutions that collectively contribute to the long-tail growth of the B2B SaaS market. Manufacturing companies, under rising pressure to adopt predictive maintenance and quality analytics, accelerate ERP upgrades to AI-ready editions. Overall vendor roadmaps hint at platform consolidation that can streamline procurement yet preserve best-of-suite choice for specialized functions.

By Deployment Model: Public Cloud Leadership with Hybrid Acceleration

Public-cloud deployments hold 61.85% of the B2B SaaS market in 2025, a position cemented by global hyperscaler ecosystems and pay-as-you-go elasticity. Hybrid-cloud architectures, however, are projected to clock a 26.20% CAGR to 2031 as firms blend regulatory resilience with latency-optimized compute placement. Europe offers the sharpest illustration as GDPR compels physical data residency while organizations still tap public compute for burst workloads.

Private cloud installations remain relevant in tightly regulated sectors such as defense and life sciences, providing maximum configuration control. Hybrid growth also draws momentum from container orchestration advances and edge nodes that extend SaaS functionality closer to end users. Enterprises increasingly orchestrate workload placement through policy engines that weigh data sensitivity, performance targets, and cost envelopes, reinforcing the trajectory toward flexible deployment mixes within the broader B2B SaaS market.

By End-user Enterprise Size: SME Growth Outpaces Large Enterprise Adoption

Large corporations accounted for 60.60% of 2025 spending because multi-suite rollouts across global subsidiaries require deep pockets and mature IT governance. Customized integrations and professional services lift deal sizes, but complexity elongates lifecycles. Small and midsize enterprises, by contrast, are on track for a 22.80% CAGR, buoyed by simplified onboarding, modular pricing, and pre-configured industry templates.

SME decision makers value time-to-value and cash-flow alignment, qualities inherent in subscription licensing and usage-based tiers. Vendors must therefore balance enterprise-grade compliance with turnkey automation to serve both extremes effectively. Platform APIs, marketplace add-ons, and low-code tools are pivotal, enabling SMB customers to extend functionality without hiring specialized developers. This twin-track dynamic anchors future revenue diversification inside the B2B SaaS market.

By End-User Industry: Healthcare Surge Challenges BFSI Leadership

Banking, Financial Services, and Insurance held 24.05% of the B2B SaaS market in 2025, underpinned by relentless digitalization of customer onboarding, fraud prevention, and reporting obligations. RegTech modules embedded inside core banking suites automate compliance checks and real-time transaction monitoring. Healthcare, however, is forecast to grow at a 29.50% CAGR through 2031, fueled by telemedicine normalization, AI-assisted diagnostics, and modernization of electronic health records.

Retail, manufacturing, IT, and telecom also maintain strong cloud trajectories, each solving distinct pain points such as omni-channel personalization or network analytics. Emerging verticals including public sector, education, and energy fall in the “Others” bracket yet represent untapped upside as policy and infrastructure catch up. Vertical penetration patterns affirm that domain depth and regulatory proof points will remain decisive buying criteria in the B2B SaaS market.

Geography Analysis

North America kept 32.85% share of 2025 revenue on the strength of early cloud adoption, venture capital depth, and supportive regulation. Microsoft’s cloud segment posted USD 42 billion in Q3 2025 revenue, illustrating the region’s capacity for large-scale consumption. Federal initiatives such as the US Cloud Smart program further widen public-sector lanes, although increasing cybersecurity mandates introduce additional vendor evaluation hurdles.

Asia-Pacific is racing ahead at a 24.60% CAGR, aided by manufacturing digital agendas, government stimulus, and a vast SME base hungry for cloud productivity. The growth is further propelled by government digital transformation mandates, manufacturing sector modernization, and SME technology adoption that creates vast addressable markets for SaaS solutions across diverse economic conditions and regulatory frameworks.

Europe enjoys steady growth under a complex compliance canopy. The EU AI Act and GDPR position local providers as trusted partners able to maneuver through intricate legal terrain. Latin America, the Middle East, and Africa remain emerging frontiers where improving connectivity and fintech adoption establish foundational demand yet macroeconomic swings temper immediate scale. Vendors tailoring go-to-market motions to localized compliance and language nuances are poised to capture outsized gains in each theatre of the B2B SaaS market.

Competitive Landscape

The competitive field sits at a moderate concentration. Microsoft, Salesforce, and Oracle constitute a formidable core, yet cloud-native challengers erode incumbency by launching vertically specialized modules and AI-infused features. IBM’s USD 6.4 billion HashiCorp purchase shows the premium placed on developer-centric tooling that bridges multi-cloud environments [3]IBM Press Office, “IBM to Acquire HashiCorp for USD 6.4 Billion,” ibm.com. Salesforce’s acquisition of Zoomin adds unstructured content analysis to its ecosystem, pointing to a future where data context is as critical as application breadth.

Pricing strategy is evolving. Roughly 85% of SaaS firms now experiment with consumption-based tiers, aligning revenue with real-time resource utilization. Partnerships and marketplace integrations serve as accelerants, particularly for niche providers that add value through domain-level extensions. White-space opportunities persist in micro-SaaS niches, regional compliance SaaS, and integration platforms that orchestrate unified identity, billing, and observability across the B2B SaaS market.

B2B SaaS Industry Leaders

Adobe Inc.

Microsoft Corporation

Salesforce Inc.

Intuit Inc.

ServiceNow Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Black and White Zebra rebranded its B2B SaaS sales and marketing platform SoftwareSelect to Revleads, signaling a focus on broader revenue-enablement use cases.

- January 2025: Venture capital firm Defiant launched a USD 30 million fund for early-stage B2B SaaS and fintech start-ups across Europe, with a USD 70 million fundraising target.

- January 2025: Blackstone and Vista Equity Partners completed the USD 8.4 billion acquisition of Smartsheet, underlining investor conviction in collaboration SaaS.

- October 2024: Thryv Holdings finalized its USD 80 million buyout of Keap, adding over 100,000 SMB subscriptions and strengthening CRM plus marketing automation capacity.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the business-to-business software-as-a-service market as all subscription-based, multi-tenant applications delivered over public, private, or hybrid clouds that are purchased by enterprises for internal use, including ERP, CRM, HCM, SCM, collaboration, analytics, and other horizontal or vertical suites. According to Mordor Intelligence, revenues from professional services, on-premise licenses, and consumer-focused SaaS are out of scope.

Scope exclusion: consumer-grade personal productivity and gaming SaaS are not covered.

Segmentation Overview

- By Type of Software

- ERP

- CRM

- HCM

- SCM

- Others

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By End-user Enterprise Size

- SMEs

- Large Enterprises

- By End-user Vertical

- BFSI

- Healthcare

- IT and Telecom

- Retail and eCommerce

- Manufacturing

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed product leaders, channel partners, and CIOs across North America, Europe, and key Asia-Pacific growth hubs. Discussions clarified typical seat-based pricing, churn ranges, and emerging Gen-AI surcharge models, insights that filled gaps left by desk research and guided our conversion of reported ARR into addressable market value.

Desk Research

Mordor analysts first compiled publicly available indicators such as OECD ICT expenditure tables, US Bureau of Economic Analysis cloud software spending, Eurostat enterprise cloud adoption surveys, India's MeitY Digital Economy reports, and annual filings of the top twenty listed SaaS vendors. Trade groups such as the Cloud Native Computing Foundation and the Asia Cloud Computing Association offered uptake statistics by sector, while press releases captured landmark funding and M&A deals. Select paid datasets, D&B Hoovers for company financials and Dow Jones Factiva for deal momentum, helped validate revenue splits and regional footprints. The sources cited above are illustrative; many additional references informed data collection and cross-checks.

Market-Sizing & Forecasting

A calibrated top-down model starts with national enterprise software outlays, which are then filtered through SaaS penetration ratios, average subscription price trends, and vertical adoption curves. Bottom-up spot checks, supplier roll-ups and sampled ARR-per-seat times active seats, serve as guardrails before totals are finalized. Variables such as internet bandwidth cost, remote-work intensity, data-sovereignty regulation count, venture funding flows, and median customer churn directly influence CAGR assumptions. Multivariate regression linked these drivers to historical revenue growth, while scenario analysis adjusted for currency shifts and AI workload inflation. Data voids, for example in private vendor ARR, were bridged using ratio estimates derived from comparable public peers and confirmed during expert calls.

Data Validation & Update Cycle

Outputs pass a two-stage peer review, anomaly flags trigger source rechecks, and variances beyond five percentage points prompt fresh interviews. Reports refresh annually; material events like major platform pricing changes lead to interim updates. A final analyst walk-through occurs just before client release, ensuring users receive the latest vetted view.

Why Mordor's B2B Saas Baseline Earns Stakeholder Trust

Published estimates often vary because each firm picks its own software categories, pricing assumptions, and currency treatment, which pushes headline numbers apart before any forecasting even begins.

Key gap drivers may include counting professional services revenue, applying flat global ASPs that ignore wide regional discounts, or projecting CAGRs without reconciling churn and upsell dynamics that our analysts track quarterly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 390 B (2025) | Mordor Intelligence | - |

| USD 328 B (2024) | Global Consultancy A | Excludes hybrid-cloud deployments and converts local revenues at fixed 2022 FX rates |

| USD 384 B (2024) | Industry Journal B | Adds implementation services and uses vendor-reported bookings rather than recognized ARR |

| USD 393 B (2024) | Regional Consultancy C | Applies single ASP across regions, overlooks tier-based pricing and freemium upgrades |

The comparison shows that once differing scopes and pricing logic are stripped away, Mordor's balanced approach, anchored to verifiable ARR, region-specific price ladders, and annually refreshed penetration ratios, delivers the most transparent, repeatable baseline for planners who need dependable numbers.

Key Questions Answered in the Report

What is the current size of the B2B SaaS market?

The B2B SaaS market stands at USD 0.49 trillion in 2026.

How fast is the B2B SaaS market expected to grow?

It is projected to expand at a 26.24% CAGR, reaching USD 1.58 trillion by 2031.

Which software segment holds the largest share today?

Customer Relationship Management accounts for 29.12% of B2B SaaS market share.

Why is hybrid-cloud deployment growing so quickly?

Enterprises need to balance regulatory compliance, latency, and cost, driving a 26.20% CAGR for hybrid configurations.

Which region shows the fastest growth?

Asia-Pacific is forecast to grow at 24.60% CAGR as government digital programs and SME adoption accelerate.

What is the main challenge facing AI-driven SaaS vendors?

Rising generative-AI inference costs are squeezing gross margins, forcing optimization of models and pricing.

Page last updated on: