India Data Center Rack Market Size and Share

Market Overview

| Study Period | 2025 - 2032 |

|---|---|

| Forecast Data Period | 2026 - 2032 |

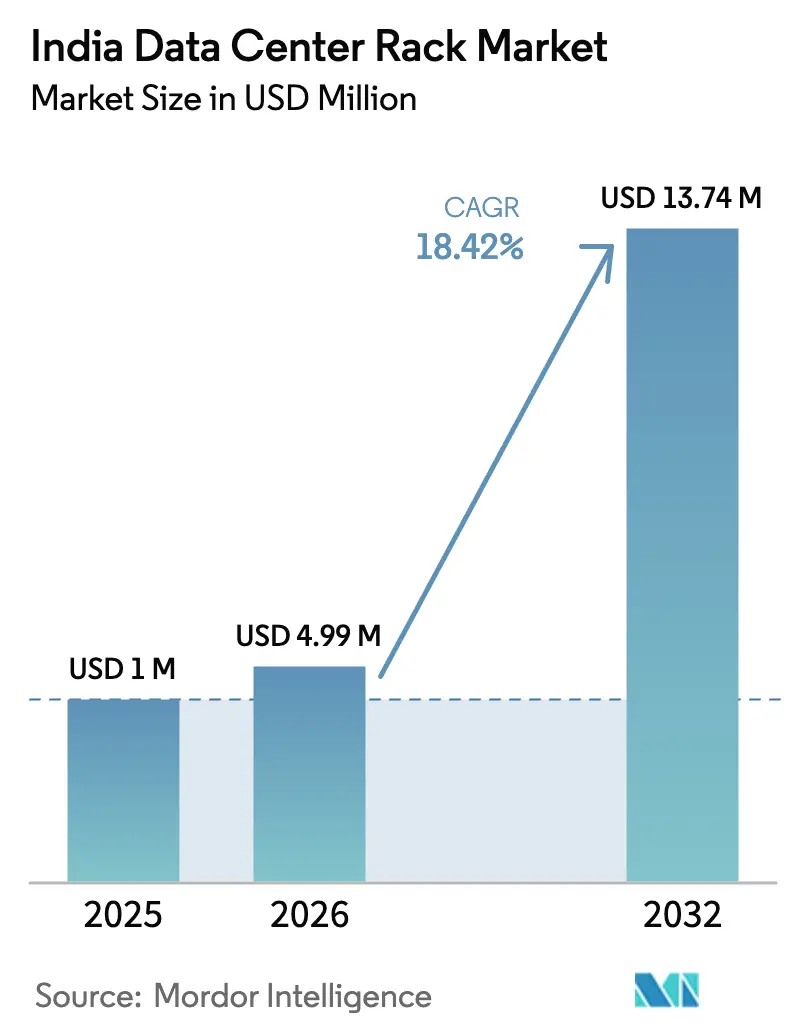

| Base Year Market Size (2025) | USD 1 Million |

| Market Size (2026) | USD 4.99 Million |

| Market Size (2032) | USD 13.74 Million |

| Growth Rate (2026 - 2032) | 18.42% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Data Center Rack Market Analysis by Mordor Intelligence

The India data center rack market size was valued at USD 4.21 million in 2025 and estimated to grow from USD 4.99 million in 2026 to reach USD 13.74 million by 2032, at a CAGR of 18.42% during the forecast period (2026-2032). A surge of hyperscale investments, supportive government policies, and rapid edge-computing roll-outs are combining to push capacity from 1 GW in 2025 toward 17 GW by 2030. Foreign direct investment by Google, AWS, Microsoft, and Colt is translating into fast-tracked build-outs that demand standardized, high-density rack designs. Rising electricity costs are reinforcing the shift toward liquid-cooling-ready rack formats, while domestic value-addition norms under Make in India are tilting procurement toward local manufacturers that can certify 25-45% indigenous content. Meanwhile, edge facilities in Patna, Jaipur, and Kochi are expanding the geographic footprint beyond Mumbai, Chennai, and Hyderabad to support latency-sensitive AI workloads.

Key Report Takeaways

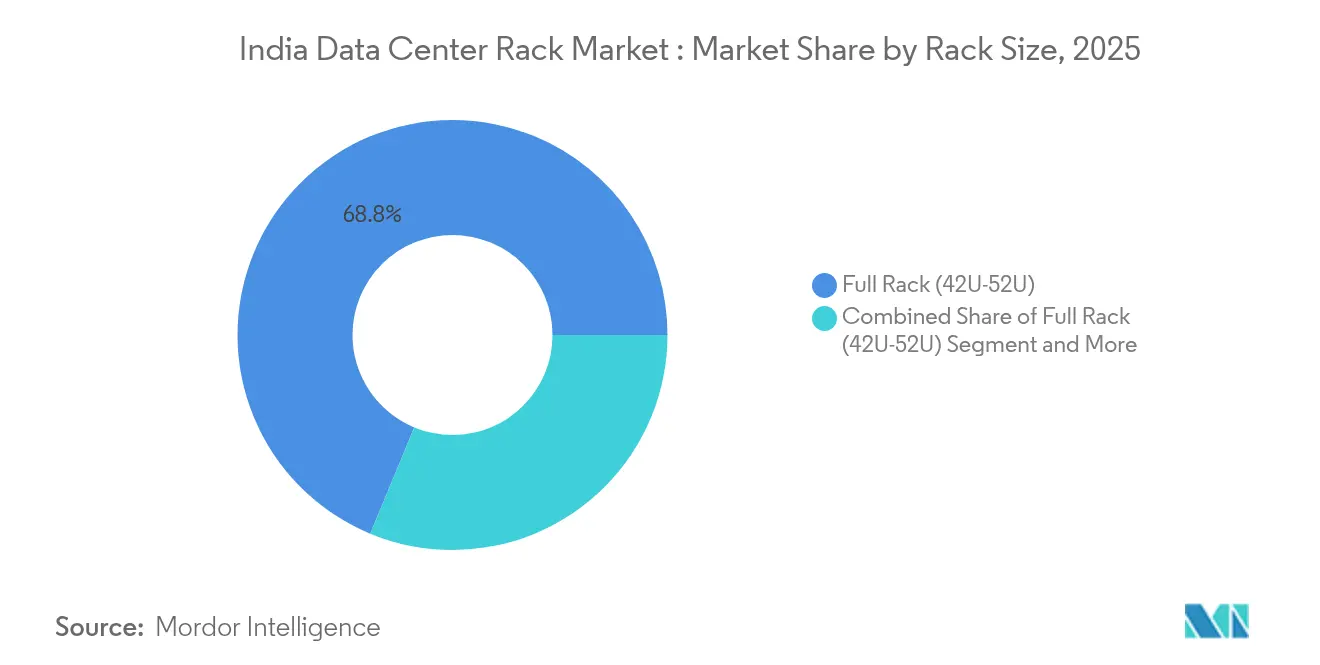

- By rack size, full-rack formats captured 68.75% of India data center rack market share in 2025, while half racks are pacing the field with a 19.02% CAGR through 2032.

- By rack type, enclosed server cabinets commanded 72.35% revenue share in 2025; soundproof racks are forecast to expand at a 20.01% CAGR between 2026-2032.

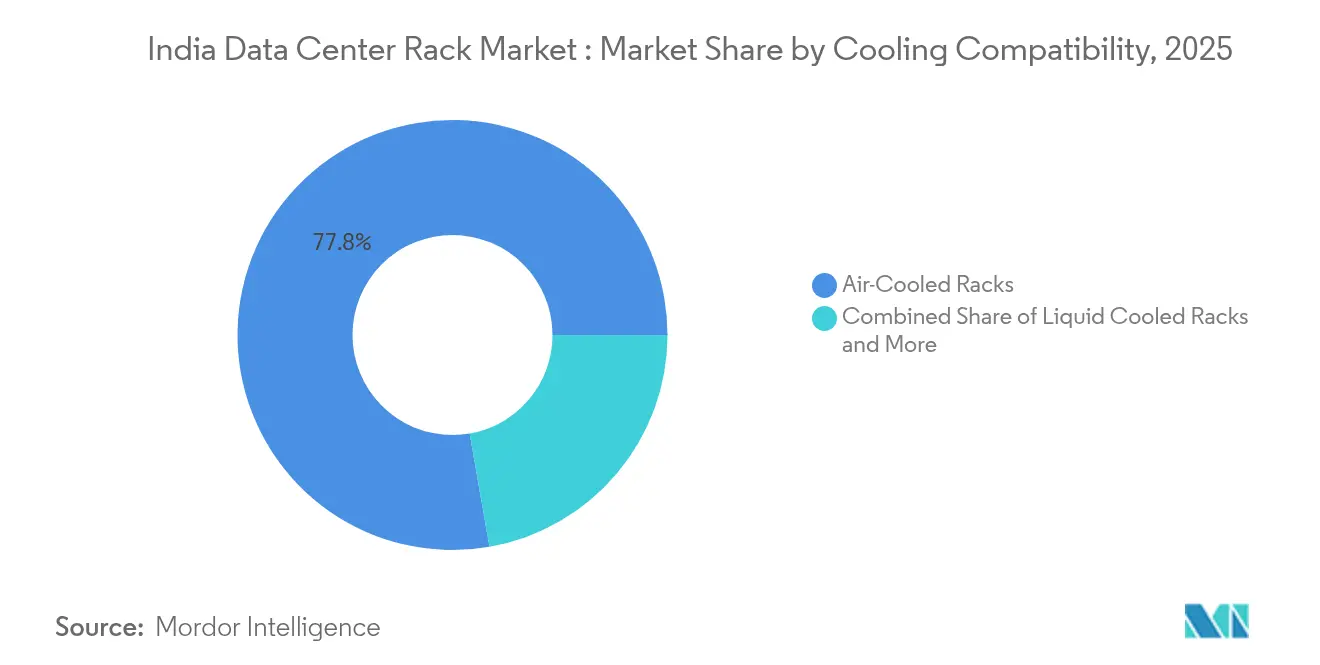

- By cooling compatibility, air-cooled designs held 77.75% of the India data center rack market size in 2025, whereas liquid-cooled models are expected to grow at a 19.34% CAGR to 2032.

- By end user, IT and telecommunication accounted for 39.45% of 2025 spending; healthcare and life sciences is advancing at a 19.56% CAGR through 2032.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple countries and regions, with India being one of the contributors. Our global data center rack market size represents that cumulative total.

India Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing deployment of data-center facilities | +4.2% | Mumbai, Chennai, Hyderabad | Medium term (2-4 years) |

| Growing cloud-computing and hyperscale investments | +3.8% | South dominant, spreading North and West | Long term (≥ 4 years) |

| Government-led digital initiatives | +2.9% | Nationwide, Tier-2/3 focus | Long term (≥ 4 years) |

| Rising demand for colocation and managed hosting | +2.1% | Metros plus emerging cities | Medium term (2-4 years) |

| Edge-computing expansion in Tier-2 and Tier-3 cities | +1.8% | Patna, Jaipur, Kochi, Ahmedabad | Short term (≤ 2 years) |

| Standardization for high-density AI/ML racks | +1.6% | Bangalore, Hyderabad, Pune | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Deployment of Data Center Facilities

India’s build-out wave is anchored by Google’s USD 6 billion Visakhapatnam project and Reliance’s planned 3 GW AI campus in Gujarat.[1]NDTV, “Andhra Pradesh, Google Sign USD 6 Billion Worth Major Data Centre Deal,” ndtv.com Central and state incentives, such as Maharashtra’s USD 20 billion Green Integrated Data Centre Parks, are bundling land, power, and single-window clearances. New guidelines on renewable procurement are prompting developers to embed solar and wind offsets at the design stage. Standard 42U–52U racks that support 15–100 kW loads are therefore becoming the default spec. Domestic rack makers benefit because proximity allows custom fabrication to meet site-specific seismic and thermal codes.

Growing Cloud Computing and Hyperscale Investments

AWS has earmarked USD 12.7 billion through 2030 to roll out AI-ready zones,[2]Business Standard, “Amazon Web Services bets big on India's talent in the global AI race,” business-standard.com while Microsoft, Oracle, and Equinix continue to scale 50-100 MW campuses. Workloads such as generative AI are pushing rack densities to 100 kW, making liquid-cooling readiness mandatory. Hyperscalers prefer uniform rack enclosures that streamline logistics across multi-region footprints. In response, suppliers are integrating quick-connect manifolds and rear-door heat exchangers as factory options. Procurement volumes from just three hyperscale buyers already exceed combined demand from the top fifty enterprises, underscoring their outsized influence on standards.

Government-Led Digital Initiatives

Digital India’s localization mandates require financial-payment and public-sector data to reside onshore, spurring fresh capacity in non-metro zones. MeitY now links procurement preference to racks with 25-45% domestic value addition, nudging integrators toward local welders, powder-coaters, and cable-tray vendors. The forthcoming data-center policy promises fast-track land conversion and dual-feed power at regulated tariffs, de-risking project economics. As a result, certified Indian Standards Organization racks with seismic rating, smoke seals, and biometric bays are gaining traction across state tenders.

Rising Demand for Colocation and Managed Hosting Services

Enterprises are migrating legacy workloads into shared facilities that promise 99.99% uptime without heavy capital outlay. Yotta’s partnership with NVIDIA showcases how colocation providers are pre-installing GPU-dense racks to attract AI clients.[3]Yotta Infrastructure, “Yotta Data Services Collaborates with NVIDIA,” yotta.com BFSI tenants demand acoustic and EMI shielding to comply with RBI norms, raising demand for sound-dampened enclosures. Sustainability is an additional lever; CtrlS targets carbon neutrality by 2030, and Nxtra’s AI-driven SmartSense platform trims non-IT power by 10%.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Availability of cheap and counterfeit racks | -2.4% | Nationwide, notably Tier-2/3 | Short term (≤ 2 years) |

| High upfront CAPEX and compliance costs | -1.9% | Metro zones with strict norms | Medium term (2-4 years) |

| Volatile CRCA steel supply chain | -1.7% | National, with higher impact on domestic manufacturers | Short term (≤ 2 years) |

| Land acquisition and power-provisioning delays | -1.4% | Metropolitan areas and emerging Tier-2/Tier-3 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Cheap and Counterfeit Racks

Price-sensitive buyers sometimes select non-certified enclosures fabricated from thin-gauge steel, heightening fire risk and load failure. Steel cost swings between INR 63 500-68 500 per tonne intensify the temptation to down-spec materials, undermining reliability. Substandard units rarely support the 1 200-kg static loads common in hyperscale deployments. To curb counterfeit imports, customs authorities now mandate BIS traceability codes, but enforcement gaps persist in secondary markets.

High Upfront CAPEX and Compliance Costs

ISO 27001, ISO 14001, and MeitY empanelment together add 12-15% to rack acquisition costs, squeezing margins for small operators. Healthcare deployments must also meet HIPAA-aligned acoustic criteria, pushing buyers toward premium soundproof racks that can cost 35% more than standard cabinets. Power distribution units rated for 100 A per phase and redundant busways raise total build costs further. Smaller carriers often defer upgrades, slowing penetration in underserved districts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: High-Density Full Racks Anchor Core Sites

Full racks claiming 68.75% of 2025 shipments underscore how hyperscalers favor tall, deep frames that optimize floor utilization. The India data center rack market size for full racks is poised to expand at 17.98% CAGR, reflecting uniform deployment templates across new 100 MW campuses. Half racks, though a smaller base, are gaining momentum in edge sites, and their India data center rack market share could reach double digits by 2032 as operators balance space and power constraints. Quarter racks remain niche, serving telecom shelters and retail back-offices where weight limits cap equipment loads.

Second-generation full racks incorporate brush grommets, perforated doors, and BMS-ready sensor arrays, enabling airflow tuning without major retrofits. Half-rack designs now ship with slide-out sections that accept additional U-spaces, protecting initial capex while allowing future scaling.

By Rack Type: Enclosed Cabinets Dominate, Acoustic Designs Surge

Enclosed cabinets captured 72.35% sales because multi-tenant sites require lockable, dust-resistant compartments. The India data center rack market size for enclosed models will rise steadily as BFSI and government workloads move into colocation halls. Open-frame racks thrive in captive hyperscale halls, where perimeter security and structured airflow make doors redundant. Soundproof racks, advancing at a 20.01% CAGR, are entering hospital data rooms and urban micro-edge pods that need to stay within 60 dB noise limits. Wall-mount units hold a minor slice, yet remain relevant for 5G base-band units and branch-office routers.

Manufacturers are embedding composite panels and mass-loaded vinyl in acoustic racks without expanding overall footprint. Compliance with ISO 3744 noise-emission standards is becoming a bid requirement in healthcare tenders, bolstering adoption.

By Cooling Compatibility: Air Leads, Liquid Gains Traction

Air-cooled enclosures still command 77.75% revenue because brownfield sites rely on perimeter CRAC units. However, the India data center rack market size for liquid-cooled cabinets is forecast to triple by 2032 alongside ramping AI adoption. Operators opt for hybrid-ready frames that can start with air and retrofit to cold-plate loops later, safeguarding capex. Early liquid-ready installs report 15-20% PUE improvement once servers switch to direct-chip coolant, offsetting higher upfront costs.

Rack vendors now pre-drill for quick-disconnect fittings and integrate drip-less valves, reducing on-site retro-fit time. Standard 600 mm widths are favored because they leave 200 mm of side clearance in 1 200 mm aisles, simplifying hose management.

By End User: IT and Telecom Leads, Healthcare Ramps Up

IT and telecommunication buyers held 39.45% of 2025 outlay as CSPs and carriers rolled out regional availability zones. The India data center rack market size for healthcare is projected to climb fastest, buoyed by tele-ICU, imaging PACS, and regulatory digitization drives. BFSI continues to expand secure pods that require dual-factor locks and vibration isolation. Media-streaming firms position cache nodes close to population centers, driving quarter-rack demand in mall rooftops and stadium basements.

Specialized needs such as MRI image archiving push healthcare buyers toward sound-damped, EMI-shielded cabinets. Manufacturers supplying antimicrobial powder coats and negative-pressure plinths gain an edge when bidding hospital projects.

By Data Center Type: Hyperscale Growth Reshapes Traditional Models

Colocation facilities dominated the India data center rack market with 66.20% market share in 2025, underlining enterprise preference for shared halls that optimize capital efficiency and operational expertise. Hyperscale/self-built facilities are racing ahead at a 20.25% CAGR through 2032, driven by Google’s USD 6 billion Visakhapatnam campus and AWS’s USD 12.7 billion outlay to 2031. These AI-centric builds require racks engineered for 80-100 kW loads and manifold liquid loops.

Others, comprising enterprise and edge deployments, fill specialized needs where proximity or compliance dictates dedicated halls. CtrlS’s Patna site, valued at INR 400 crore (USD 48.2 million), exemplifies the edge trend that balances cost with reliability. Colocation providers now bundle hybrid offers, mixing shared aisles with dedicated cages, enabling rack suppliers to leverage standardized manufacturing while catering to varied service-level agreements.

Geography Analysis

South India remains the epicenter, contributing over half of active MW capacity and a 65% pipeline toward 2030. Chennai and Bangalore benefit from submarine cable proximity and talent density, while Hyderabad’s tax holidays deepen its allure. Land parcels bundled with green-power wheeling agreements cut project lead time by up to six months, supporting continued dominance.

West India, anchored by Mumbai and Navi Mumbai, retains strategic weight thanks to BFSI workloads and international gateway cables. Maharashtra’s green-park policy offering concessional tariffs for 100% renewable operation is attracting USD 20 billion of planned investments. High land prices encourage taller rack aisles and multi-story data halls, making enclosure strength and seismic compliance critical.

North and East corridors are emerging on the back of state incentives. The Rs 600 crore Northeast facility targets underserved logistics and government workloads. CtrlS’s 60 MW Kolkata campus signals confidence in lower-cost power grids and cooler ambient temperatures that trim cooling bills. Together, these regions diversify risk from coastal weather events and decongest prime metros.

Coverage of the data center rack market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, North America, and Africa, alongside detailed country-level intelligence for Vietnam, Singapore, Germany, United States, South Africa, and Hong Kong, each shaped by local operating conditions.

Competitive Landscape

Hanut India and Rohan Infotech are capitalizing on Make in India preferences by offering 45% local content and rapid customization. Vertiv, Schneider Electric, and Rittal leverage global supply chains to supply rear-door heat exchangers and high-capacity busways demanded by hyperscalers. Sustainability pledges are reshaping purchasing:

Edge deployments in Tier-2/3 towns open white-space for modular, quick-ship racks that fit 2.4 m doors and elevators. Global players partner with local sheet-metal firms to trim freight and import duties, eroding domestic price advantages. Value-added services—factory-integrated PDUs, sensor kits, and lifecycle support—are becoming decisive, pushing pure-play metal-benders to upgrade capabilities or exit.

Looking ahead, consolidation is probable as component inflation rewards scale economies. Vendors able to bundle racks with power, cooling, and DCIM software can anchor long-term managed services revenues, differentiating in an increasingly crowded field.

India Data Center Rack Industry Leaders

Eaton Corporation

Black Box Corporation

Rittal GMBH & Co.KG

Schneider Electric SE

Vertic Group Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Google confirmed a USD 6 billion, 1 GW campus in Visakhapatnam, earmarking USD 2 billion for renewable integration.

- July 2025: AWS reiterated its USD 12.7 billion commitment through 2030 for AI-centric infrastructure across multiple Indian regions.

- November 2024: Colt and RMZ closed a USD 1.7 billion joint venture to develop sustainable data centers nationwide.

- November 2024: Nxtra by Airtel deployed Ecolibrium’s SmartSense AI platform, cutting non-IT power by 10% and boosting staff productivity by 25%.

India Data Center Rack Market Report Scope

A data center rack is a physical enclosure made up of usually steel housing electronic framework. It is designed to house servers, networking and communication devices, cables, and other data center computing peripherals.

The India data center rack market is segmented by rack size (quarter rack, half rack, and full rack) and end-user industry (BFSI, IT, telecom, government, media, and entertainment). The market sizes and forecasts are provided in terms of volume (units) for all the above segments.

| Quarter Rack (9U–22U) |

| Half Rack (23U–27U) |

| Full Rack (42U–52U) |

| Open-Frame Racks |

| Enclosed Server Cabinets |

| Wall-Mount Racks |

| Soundproof / Acoustic Racks |

| Air-Cooled Racks |

| Liquid-Cooled Racks |

| Hybrid Cooling-Ready Racks |

| IT and Telecommunication |

| BFSI |

| Government and Public Sector |

| Media and Entertainment |

| Healthcare and Life Sciences |

| Manufacturing |

| Other End Users |

| Colocation Facilities |

| Hyperscale/ Self-built Facilities |

| Others (Enterprise, Edge among others) |

| By Rack Size | Quarter Rack (9U–22U) |

| Half Rack (23U–27U) | |

| Full Rack (42U–52U) | |

| By Rack Type | Open-Frame Racks |

| Enclosed Server Cabinets | |

| Wall-Mount Racks | |

| Soundproof / Acoustic Racks | |

| By Cooling Compatibility | Air-Cooled Racks |

| Liquid-Cooled Racks | |

| Hybrid Cooling-Ready Racks | |

| By End User Industry | IT and Telecommunication |

| BFSI | |

| Government and Public Sector | |

| Media and Entertainment | |

| Healthcare and Life Sciences | |

| Manufacturing | |

| Other End Users | |

| By Data Center Type | Colocation Facilities |

| Hyperscale/ Self-built Facilities | |

| Others (Enterprise, Edge among others) |

Key Questions Answered in the Report

How big is the India Data Center Rack Market?

The India Data Center Rack Market size is expected to reach USD 4.99 million in 2026 and grow at a CAGR of 18.42% to reach USD 13.74 million by 2032.

What is the current India Data Center Rack Market size?

In 2026, the India Data Center Rack Market size is expected to reach USD 4.99 million.

Who are the key players in India Data Center Rack Market?

Eaton Corporation, Black Box Corporation, Rittal GMBH & Co.KG, Schneider Electric SE and Vertic Group Corp. are the major companies operating in the India Data Center Rack Market.

What years does this India Data Center Rack Market cover, and what was the market size in 2025?

In 2025, the India Data Center Rack Market size was estimated at USD 4.99 million. The report covers the India Data Center Rack Market historical market size for years: 2024. The report also forecasts the India Data Center Rack Market size for years: 2026, 2027, 2028, 2029, 2030, 2031 and 2032.

Page last updated on: