SaaS CRM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

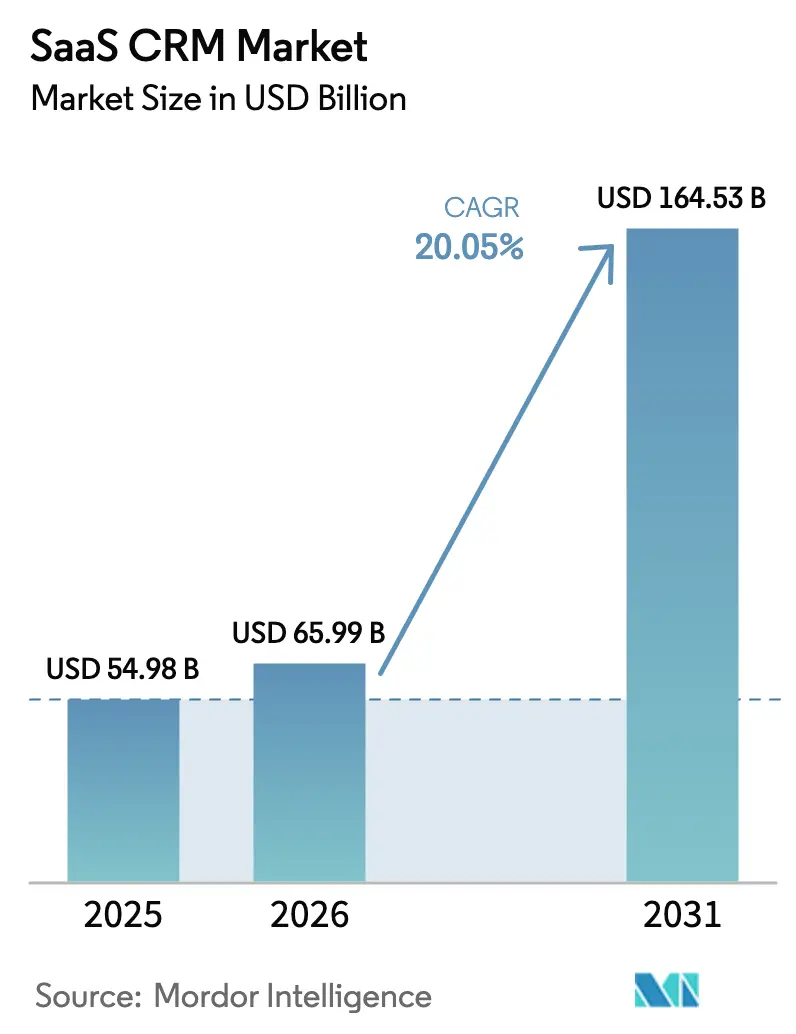

| Market Size (2026) | USD 65.99 Billion |

| Market Size (2031) | USD 164.53 Billion |

| Growth Rate (2026 - 2031) | 20.05% CAGR |

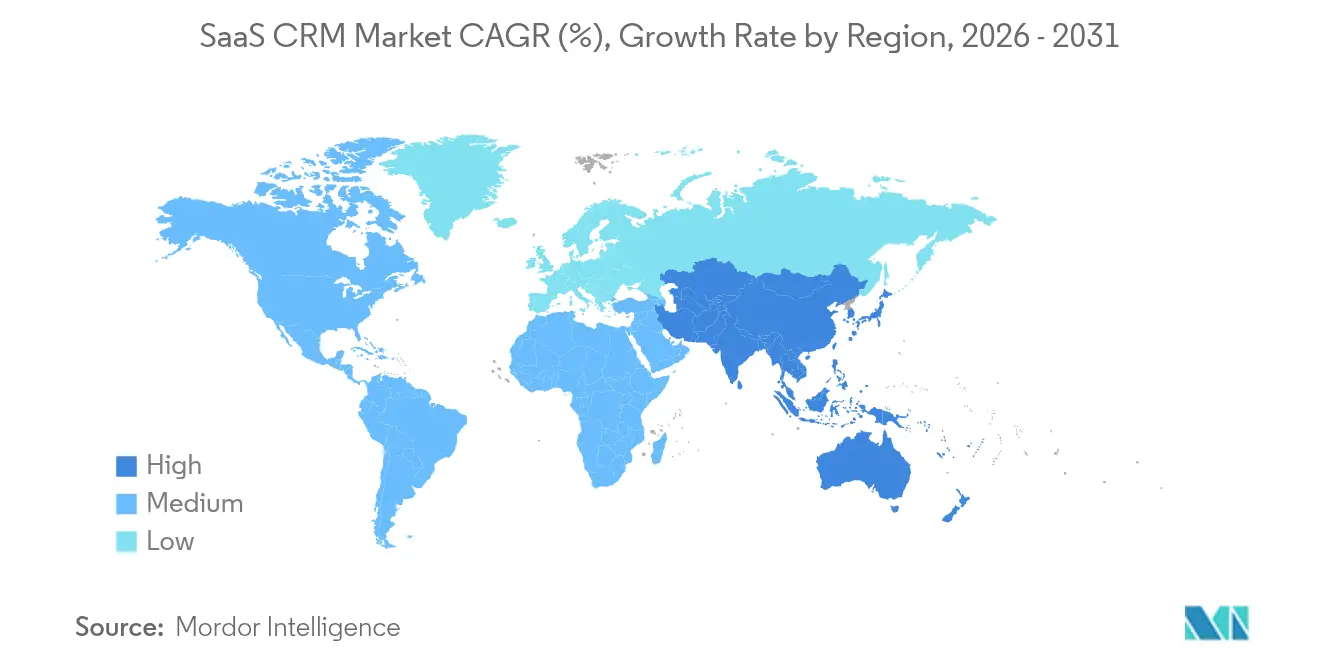

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

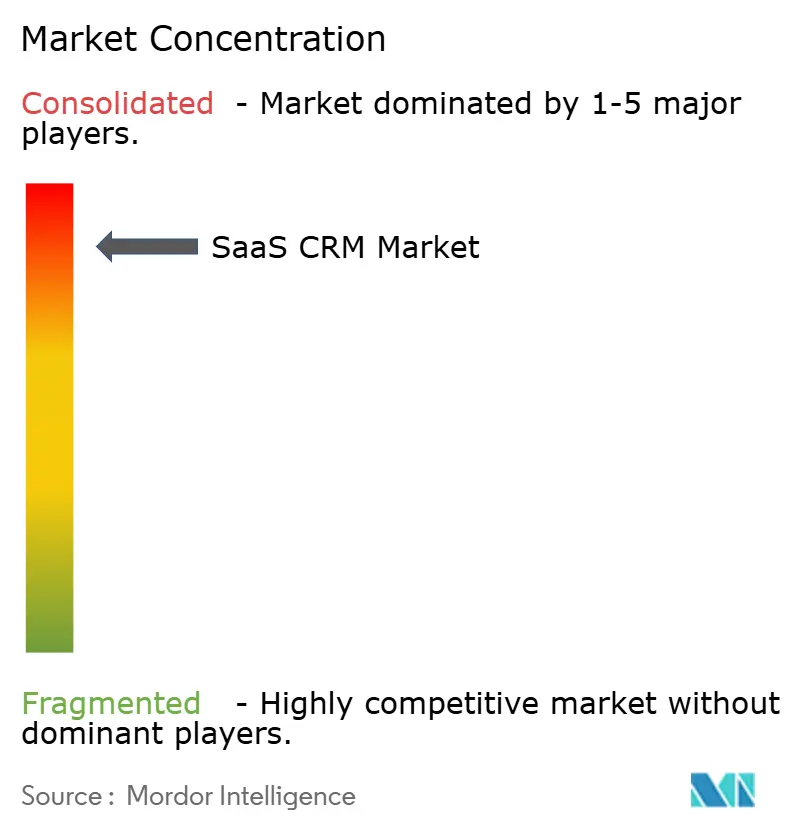

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

SaaS CRM Market Analysis by Mordor Intelligence

The SaaS CRM market size is expected to grow from USD 54.98 billion in 2025 to USD 65.99 billion in 2026 and is forecast to reach USD 164.53 billion by 2031 at 20.05% CAGR over 2026-2031. This rapid rise stems from the decisive migration away from on-premises systems toward cloud-native platforms that embed artificial intelligence, usage-based pricing, and mobile-first architectures. Enterprises adopting AI-infused CRM record markedly higher revenue growth than peers that rely on manual workflows, underscoring the technology’s tangible productivity benefits [salesforce.com]. Large enterprises presently anchor demand, yet small and mid-sized firms now move fastest as freemium and low-cost tiers eliminate historical barriers. Public-cloud, multi-tenant deployments still dominate, but hybrid and vertical-cloud models gain ground as regulated industries balance data control with modern functionality. Regionally, North America retains leadership on account of mature digital ecosystems, while Asia-Pacific supplies the highest growth as businesses leapfrog legacy stages and adopt cloud solutions from inception. [1]Salesforce, “Salesforce Report: Sales Teams Using AI 1.3x More Likely to See Revenue Increase,” salesforce.com

Key Report Takeaways

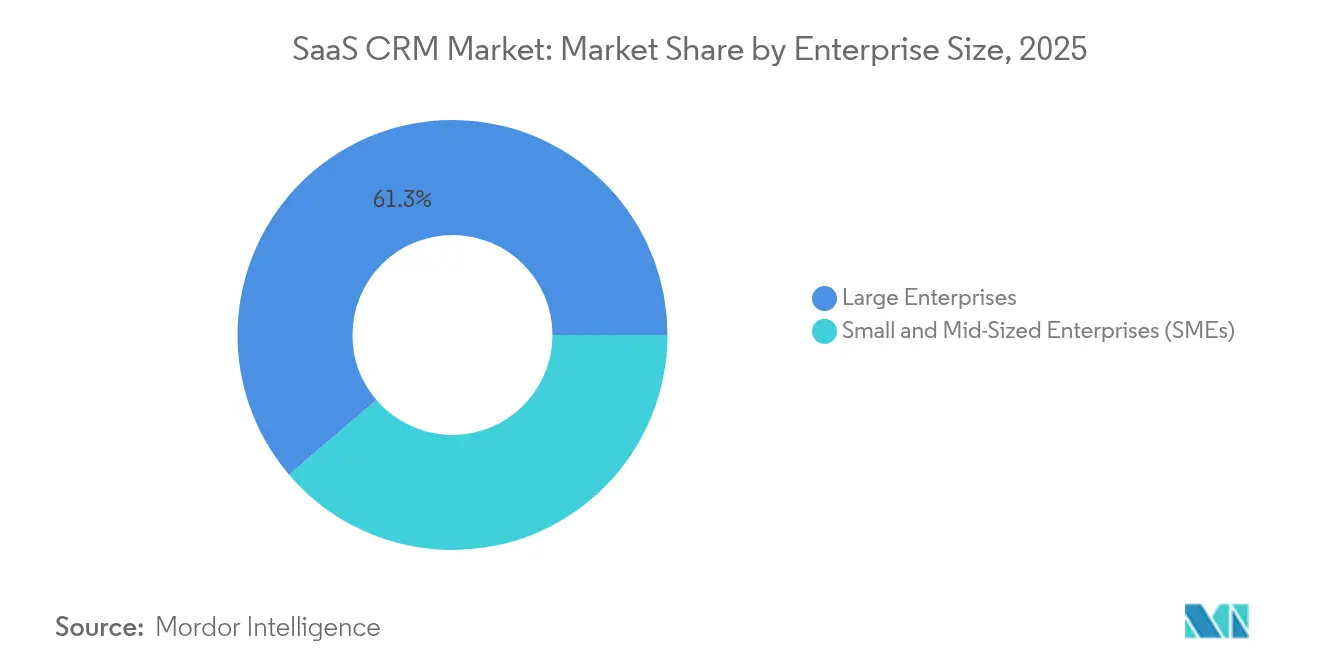

- By enterprise size, large enterprises controlled 61.25% of SaaS CRM market share in 2025, whereas SMEs are set to expand at a 24.9% CAGR to 2031.

- By deployment, public-cloud multi-tenant solutions held 70.20% of the SaaS CRM market share in 2025; hybrid and industry-cloud deployments expect the fastest 27.6% CAGR through 2031.

- By functional module, sales automation led with a 36.20% revenue share in 2025, while AI-driven service bots are projected to advance at a 31.2% CAGR by 2031.

- By geography, North America contributed 44.60% of the SaaS CRM market size in 2025, yet Asia-Pacific is anticipated to register a 23.1% CAGR to 2031.

- Salesforce recorded USD 34.9 billion revenue in fiscal 2024 and Microsoft Dynamics products posted 19% growth, illustrating ongoing scale advantages among top vendors.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global SaaS CRM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid AI infusion into sales-force automation | 4.20% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| SME cloud-first adoption, esp. <1,000 FTE firms | 3.80% | Global, strongest in Asia-Pacific & emerging markets | Short term (≤ 2 years) |

| Mobile-first/anywhere-service workforce | 2.90% | Global, accelerated in remote-work regions | Short term (≤ 2 years) |

| Usage-based ("seatless") pricing disrupting ARPU | 3.10% | North America & EU leading, expanding globally | Medium term (2-4 years) |

| EU–U.S. Data Privacy Framework easing cross-border roll-outs | 1.70% | EU & North America, spillover to APAC | Long term (≥ 4 years) |

| Embedded CRM inside vertical SaaS (construction, prop-tech) | 2.40% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid AI infusion into sales-force automation

AI shifts CRM from passive record-keeping to predictive engines that autonomously qualify leads, compose proposals, and initiate follow-ups. Platforms such as Agentforce now deploy AI agents that operate across Customer 360 and Google Workspace, handling end-to-end tasks without human oversight. Microsoft’s orchestration layer follows a similar agentic path, positioning AI as the primary interface and pushing traditional modules into the background. Organizations using AI-centric CRM are 1.3 times likelier to improve revenue, and 81% of sales teams already employ at least one AI feature. This capability materially elevates pipeline velocity and cross-sell accuracy, directly boosting the SaaS CRM market’s growth outlook.

SME cloud-first adoption, especially ≤1,000 FTE firms

Smaller companies pursue cloud-native CRM to bypass hardware costs and complex maintenance. The US SME segment alone is forecast at USD 11.7 – 13.2 billion by 2029, driven by freemium models such as Bitrix24 that reported roughly 10 million active users. These firms value rapid deployment over exhaustive customization, accelerating market penetration. The shift reflects broader digital-transformation patterns in which SMEs leapfrog legacy technologies, catalysing incremental demand within the SaaS CRM market. [2]Virtasant, “Microsoft vs Salesforce: The Feud Shaping AI in CRM,” virtasant.com

Mobile-first/anywhere-service workforce

Remote work legitimized mobile usage as the default CRM interface. Responsive designs and offline synchronization are now table stakes as field sellers require on-the-go access to customer data. Social-commerce channels also feed directly into CRM pipelines, forcing vendors to capture interactions across LinkedIn, X, and niche communities. The architectural transition underpins rising license counts and makes the SaaS CRM market more resilient to location-based disruptions.

Usage-based (“seatless”) pricing disrupting ARPU

Three in five SaaS providers already bill on consumption rather than per-seat access, and enterprise buyers increasingly demand alignment between cost and realized value. Vendors migrating to usage-based models report 9% higher net revenue retention. This change redefines sales compensation plans, spurs investment in granular usage tracking, and invites new entrants that compete on transparent economics—together enlarging the SaaS CRM market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High switching & integration cost for legacy on-prem | -2.30% | Global, strongest impact in established markets | Medium term (2-4 years) |

| Persistent security & data-sovereignty concerns | -1.80% | EU & regulated industries globally | Long term (≥ 4 years) |

| Looming 'shadow-AI' compliance fines (EU AI Act) | -1.90% | EU primary, spillover to global operations | Short term (≤ 2 years) |

| Rising hyperscaler platform tax squeezing ISV margins | -1.40% | Global, affecting all cloud-dependent vendors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Switching & Integration Cost for Legacy On-Prem

Enterprises that customized on-prem systems face 12- to 18-month migrations and dual-run expenses. Budget strain is significant in mid-market firms, and regulated sectors must maintain audit trails throughout transition, amplifying professional-services costs.Financial, health, and public-sector institutions must meet varied jurisdictional rules, often enforcing local data storage. The EU AI Act’s shadow-AI provisions promise meaningful fines for unregulated algorithms, tempering aggressive AI rollouts. HIPAA compliance further narrows vendor choices for healthcare buyers.

Persistent Security & Data-Sovereignty Concerns

Financial, health, and public-sector institutions must meet varied jurisdictional rules, often enforcing local data storage. The EU AI Act’s shadow-AI provisions promise meaningful fines for unregulated algorithms, tempering aggressive AI rollouts. HIPAA compliance further narrows vendor choices for healthcare buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enterprise Size: SMEs Drive Adoption Velocity

Large enterprises maintained 61.25% of SaaS CRM market share in 2025, benefiting from deeply integrated suites that span multiple business units. SMEs, however, are pacing at a 24.9% CAGR and are set to narrow the gap sharply by 2031. The SaaS CRM market size tied to SMEs is projected to swell as freemium and low-cost tiers drop entry barriers for companies with <1,000 employees. Free packages convert to paid tiers once workflow complexity rises, boosting vendor lifetime value.

Adoption patterns diverge by organizational complexity. Large firms favour platforms offering robust customization, data-governance controls, and global support, whereas SMEs prioritize quick deployment and intuitive UIs that minimize training. Mid-market organizations straddle these needs, creating space for flexible bundles. Vendors now segment go-to-market strategy accordingly, a trend expected to keep the SaaS CRM market in dynamic equilibrium.

By Deployment Type: Hybrid Solutions Gain Momentum

Public-cloud multi-tenant offerings controlled 70.20% revenue in 2025, owing to cost efficiency and elastic scale. Nevertheless, hybrid and industry-cloud deployments will rise at a 27.6% CAGR, lifting their share of the SaaS CRM market size through 2031. Highly regulated buyers in finance and healthcare retain sensitive records on-prem while pushing analytics into the cloud.

This dual-stack approach supports stringent compliance without forfeiting AI engines. Industry-clouds bundle sector-specific workflows and certifications, accelerating time-to-value. Providers that package modular deployments appeal to firms juggling varied data-sensitivity levels across regions.

By Functional Module: AI Service Bots Create a New Category

Sales automation held a 36.20% revenue lead in 2025, but AI-driven service bots are on course for a 31.2% CAGR—the fastest among modules. Their autonomy in handling routine tickets reduces human labour and bolsters customer satisfaction, allowing enterprises to redeploy staff toward high-value tasks.

The functional stack is converging. Sales insights now power marketing lead scores, while historical service logs inform predictive cross-sell. Salesforce’s release of Agentforce 2.0 exemplifies the consolidation of these capabilities into a single AI-rich layer. This convergence raises attach rates and expands the addressable SaaS CRM market.

By End-User Industry: Healthcare Accelerates Transformation

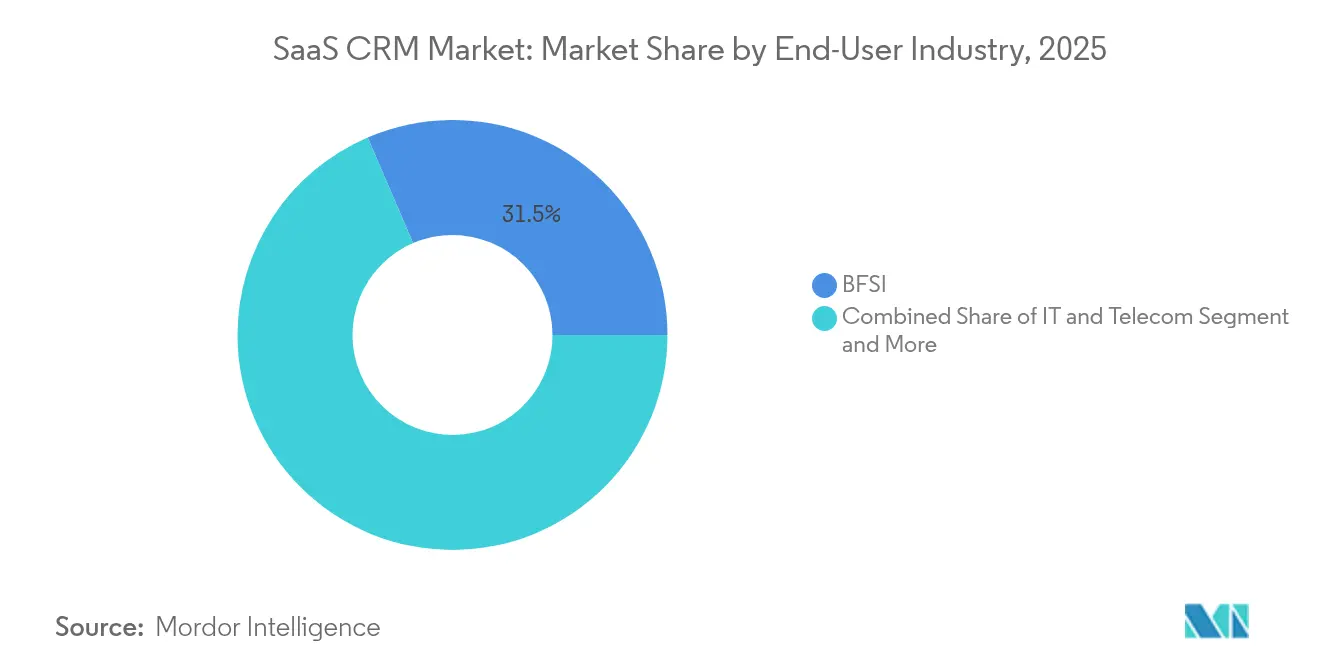

Financial services sustained an 31.45% revenue share in 2025, yet healthcare is slated to grow fastest at 26.1% CAGR. Hospitals and insurers seek unified patient engagement and HIPAA-compliant data handling, pushing specialized vendors to integrate telehealth and care-coordination features.

Industry demands vary banks need exhaustive audit trails, manufacturers favour supply-chain integration, and retailers chase omnichannel personalization. A one-size platform rarely suffices, so vendors build vertical templates to capture incremental SaaS CRM market demand.

By Pricing Tier: Low-Cost Disruption Under USD 25/User/Month

The USD 25–80 tier represented 48.40% revenue in 2025. Still, the sub-USD 25 bracket will climb at 22.8% CAGR as pay-as-you-go plans and AI automation drive down marginal costs. Vendors that master usage metering can profitably serve value-conscious SMEs while expanding wallet share as customers scale.

Per-seat pricing now competes with metrics such as API calls, records processed, or AI tasks executed. Transparency improves retention and unlocks customer segments historically priced out of the SaaS CRM market.

Geography Analysis

North America contributed 44.60% of the SaaS CRM market size in 2025, benefiting from dense cloud infrastructure and high digital-maturity levels among Fortune 500 firms. Vendor R&D hubs in California, Washington, and Texas catalyse rapid feature cycles, and enterprises routinely pilot emerging capabilities such as autonomous AI agents. Elevated user sophistication sustains license expansion even as penetration crests.

Asia-Pacific will outpace all regions at a 23.1% CAGR through 2031. Businesses in India, China, and Southeast Asia bypass legacy installations, adopting cloud CRM from day one. Government e-invoicing and digital-commerce mandates further lift adoption. This leapfrog behaviour adds meaningful volume to the SaaS CRM market, prompting global vendors to localize language support and compliance features.

Europe advances steadily under GDPR and sectoral regulations that motivate either localized data centers or hybrid deployments. The EU-US Data Privacy Framework streamlines cross-border transfers, enabling multinationals to standardize stacks without regulatory risk. Middle East, Africa, and South America present green-field prospects; infrastructure rollouts and improving broadband open room for pilot deployments that convert into multi-year contracts.

Competitive Landscape

The SaaS CRM market is moderately consolidated. Salesforce leads with roughly 202,600 customers and USD 34.9 billion in fiscal 2024 revenue, sustained by an expanding AI feature set in the Einstein 1 Platform. Microsoft leverages seamless tie-ins with Microsoft 365 to post 24% Dynamics 365 growth, using Copilot agents to reposition the interface around natural-language workflows. Oracle, SAP, and HubSpot maintain solid footholds through database heritage, ERP adjacency, and inbound-marketing strengths.

Competitive focus has pivoted from checkbox features to AI differentiation and flexible pricing. Consumption-based contracts appeal to finance chiefs seeking cost-to-value parity; this pressures incumbents to revamp billing engines while favouring startups architected for granular metering. Vertical SaaS players embed native CRM logic (e.g., in construction or prop-tech), absorbing functions once outsourced to horizontal platforms.

M&A remains active. Salesforce’s agreement to acquire Informatica for USD 8 billion amplifies its data-management stack and underscores the strategic premium on unified customer graphs. Creatio’s USD 1.2 billion valuation spotlights demand for no-code deployment, whereas Bitrix24’s 10 million-user freemium base illustrates the potency of funnel-wide monetization. The collective top five vendors held an estimated 62% 2024 revenue share, leaving meaningful white space for niche innovators. [4]Microsoft, “Microsoft 2024 Annual Report,” microsoft.com

SaaS CRM Industry Leaders

-

Salesforce, Inc.

-

Microsoft Corporation (Dynamics 365)

-

Oracle Corporation (Fusion / NetSuite CX)

-

HubSpot, Inc.

-

SAP SE (CX / C4 HANA)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Salesforce signed a definitive agreement to acquire Informatica for USD 8 billion, strengthening its data-management depth and AI roadmap.

- May 2025: Salesforce unveiled a Life Sciences Partner Network to accelerate digital-labour programs in healthcare.

- February 2025: Salesforce and Google expanded collaboration by integrating Gemini models into Agentforce, broadening AI choice for customers.

- January 2025: Salesforce launched Agentforce for Retail and Retail Cloud with modern POS to unify online and in-store data.

Global SaaS CRM Market Report Scope

SaaS CRM is cloud-hosted software that provides continuous access to CRM features and assistance without requiring investment in setup and upkeep. SaaS CRM enhances customer relationships, streamlines marketing, sales, and customer service processes, and adds a personal touch to interactions.

The SaaS CRM market is segmented by enterprise size (large enterprises, SMEs), end-user (IT & telecom, BFSI, healthcare, manufacturing , retail, other end users), geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| Large Enterprises |

| Small and Mid-Sized Enterprises (SMEs) |

| Public-Cloud Multi-Tenant |

| Private-Cloud / Single Tenant |

| Hybrid / Industry-Cloud |

| Sales Automation |

| Marketing Automation |

| Customer Service & Support |

| Commerce / CPQ |

| BFSI |

| IT and Telecom |

| Healthcare |

| Manufacturing |

| Retail and E-Commerce |

| Others (Education, Public-Sector, etc.) |

| Less than USD 25 / User / Mo. |

| USD 25-80 / User / Mo. |

| greater than USD 80 / User / Mo. |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Enterprise Size | Large Enterprises | |

| Small and Mid-Sized Enterprises (SMEs) | ||

| By Deployment Type | Public-Cloud Multi-Tenant | |

| Private-Cloud / Single Tenant | ||

| Hybrid / Industry-Cloud | ||

| By Functional Module | Sales Automation | |

| Marketing Automation | ||

| Customer Service & Support | ||

| Commerce / CPQ | ||

| By End-User Industry | BFSI | |

| IT and Telecom | ||

| Healthcare | ||

| Manufacturing | ||

| Retail and E-Commerce | ||

| Others (Education, Public-Sector, etc.) | ||

| By Pricing Tier | Less than USD 25 / User / Mo. | |

| USD 25-80 / User / Mo. | ||

| greater than USD 80 / User / Mo. | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the SaaS CRM market?

The SaaS CRM market generated USD 65.99 billion in 2026 and is forecast to reach USD 164.53 billion by 2031 at a 20.05% CAGR.

Which region is growing fastest for SaaS CRM adoption?

Asia-Pacific is projected to post a 23.1% CAGR to 2031, the highest among all regions, as businesses adopt cloud solutions from inception.

Why are AI-driven service bots important for CRM platforms?

They automate routine interactions, lower service costs, and are expected to grow at a 31.2% CAGR, the quickest among functional modules, thereby expanding platform value.

How are pricing models changing in the SaaS CRM industry?

Vendors are shifting from per-seat licenses to usage-based billing, which improves net revenue retention and aligns cost with value delivered.

What restrains some companies from migrating to cloud CRM?

High switching costs, integration complexity, and data-sovereignty regulations can extend migration timelines and increase total ownership cost.

Which enterprise size segment grows fastest in SaaS CRM?

Small and mid-sized enterprises are expanding at a 24.9% CAGR due to cloud-first strategies and low-cost entry tiers that remove historical barriers.

Page last updated on: