South Africa Data Center Server Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

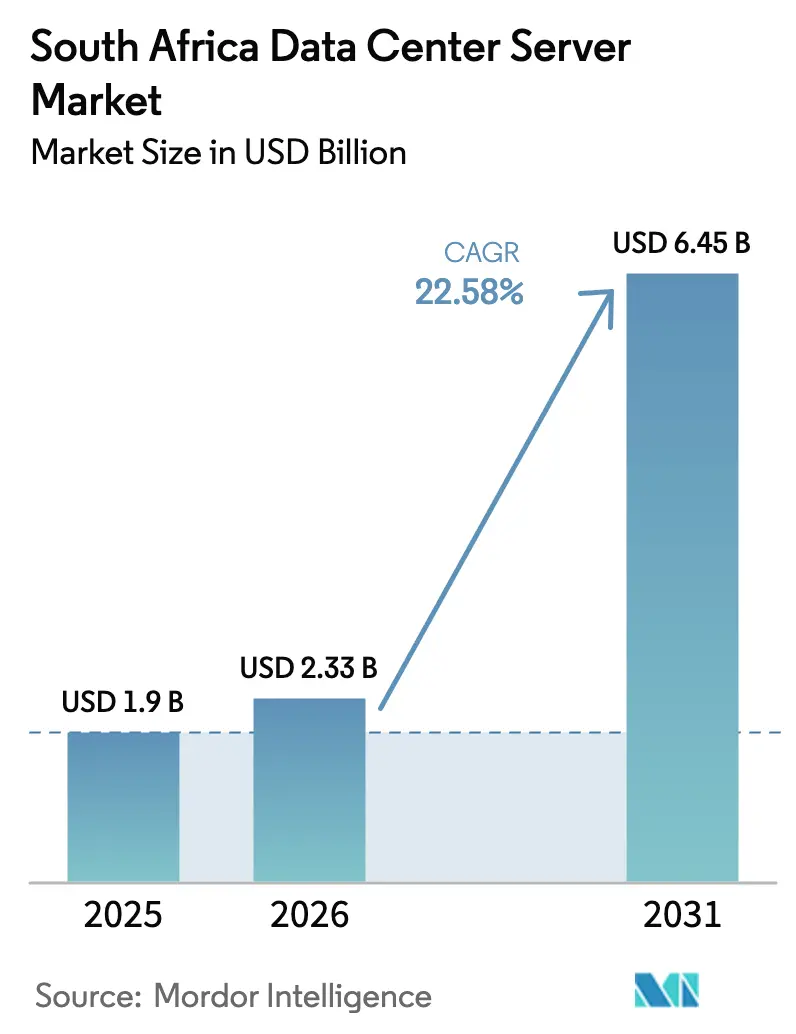

| Base Year Market Size (2025) | USD 1.9 Billion |

| Market Size (2026) | USD 2.33 Billion |

| Market Size (2031) | USD 6.45 Billion |

| Growth Rate (2026 - 2031) | 22.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Data Center Server Market Analysis by Mordor Intelligence

The South Africa data center server market size is expected to grow from USD 1.9 billion in 2025 to USD 2.33 billion in 2026 and is forecast to reach USD 6.45 billion by 2031 at 22.58% CAGR over 2026-2031. Expansion is underpinned by local data-sovereignty rules, accelerated cloud migration, and rising artificial-intelligence workloads that collectively re-shape server procurement patterns. Hyperscalers choose Johannesburg as their continental gateway, a decision reinforced by NAPAfrica Internet Exchange surpassing 5 Tbps of peak traffic in 2025. At the same time, Protection of Personal Information Act mandates and local content-hosting rules sustain on-premises capacity investments even as enterprises embrace hybrid cloud. Intensifying power constraints make renewable power purchase agreements a competitive differentiator, while one-year GPU refresh cycles are shortening hardware life spans and lifting replacement demand.

Key Report Takeaways

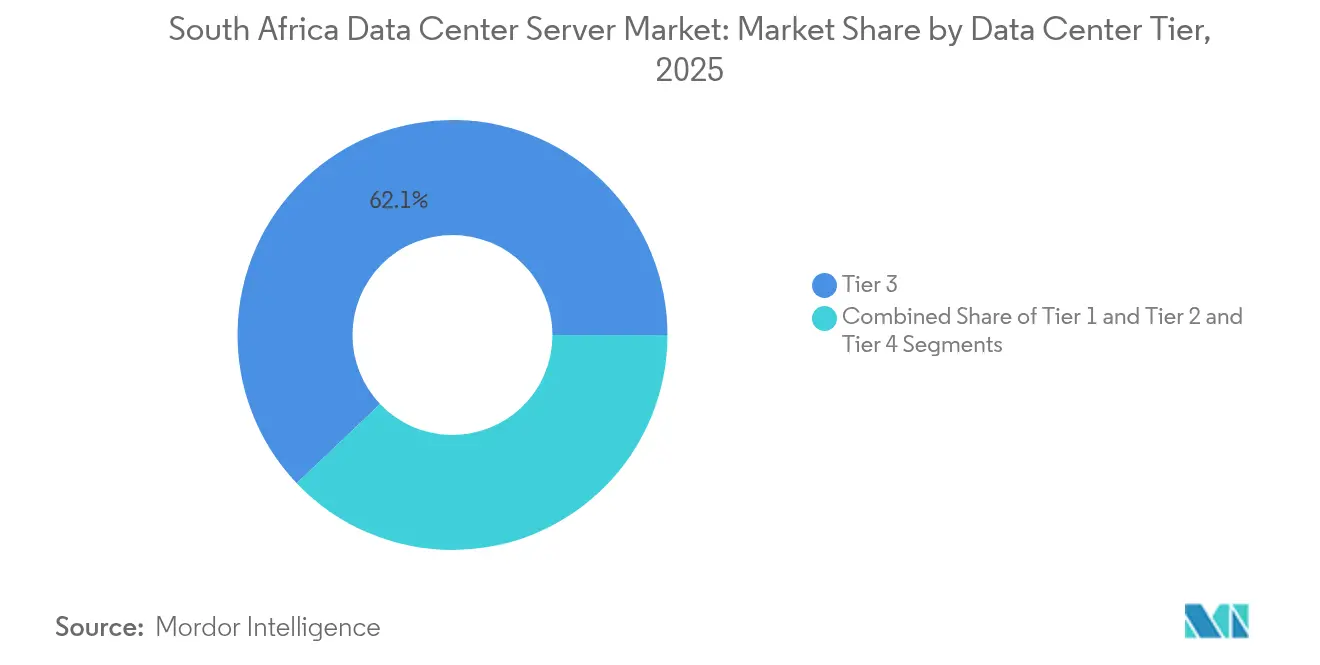

- By data-center tier, Tier 3 facilities led with 62.10% revenue share in 2025; Tier 4 is projected to expand at a 24.62% CAGR through 2031.

- By form factor, half-height blades held 54.60% of the South Africa data center server market share in 2025, whereas quarter-height micro-blades are on track to grow at 25.07% CAGR to 2031.

- By workload, virtualization and private cloud accounted for 38.70% of 2025 deployments, while AI/ML workloads are set to grow at 26.22% CAGR.

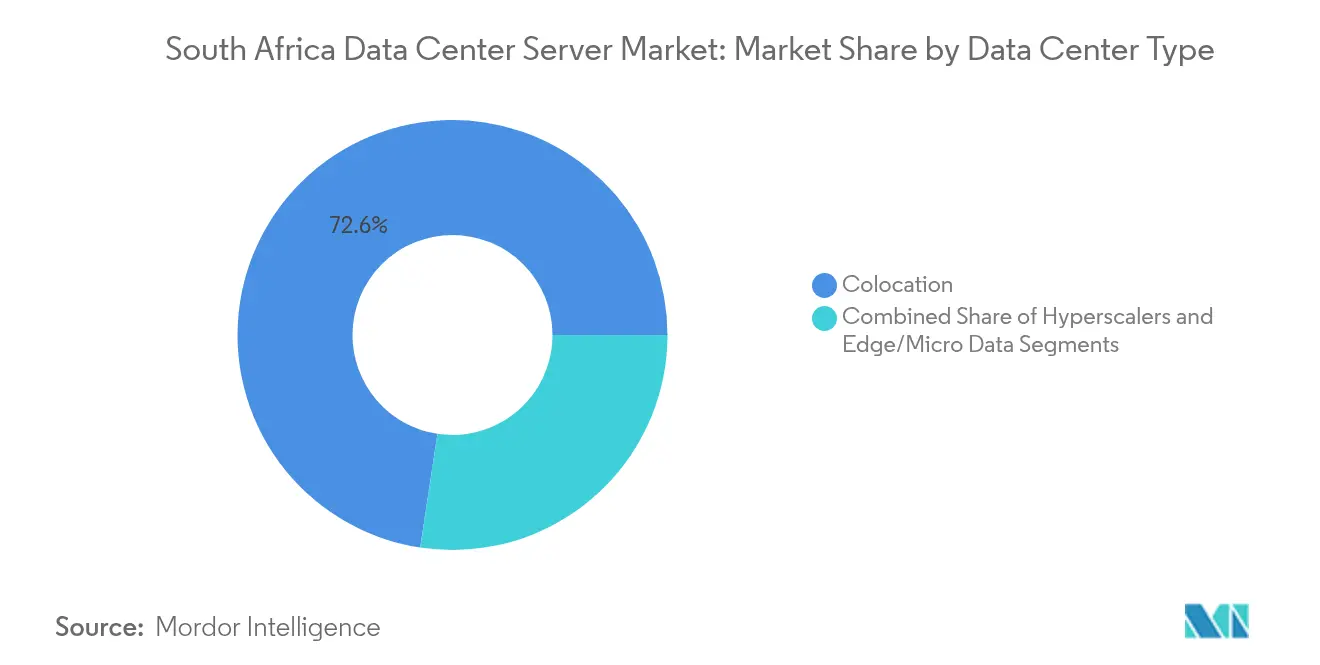

- By data-center type, colocation commanded 72.60% share of the South Africa data center server market size in 2025; hyperscaler facilities will post a 27.05% CAGR to 2031.

- By end-use industry, IT and telecoms led with 30.70% revenue share in 2025, but manufacturing workloads are projected to enlarge at 27.68% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Viewed independently, South africa offers depth on local conditions but not full coverage of the overall global system. Mordor Intelligence's coverage on the data center server market brings the wider geographic picture into focus.

South Africa Data Center Server Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated cloud-first strategies | +4.2% | Johannesburg, Cape Town, national | Medium term (2-4 years) |

| Surge in AI/ML and edge workloads | +5.8% | National, led by finance and telecoms | Short term (≤ 2 years) |

| Rapid fibre roll-outs by Telkom, DFA, MTN | +3.1% | Metropolitan corridors | Medium term (2-4 years) |

| Sub-1 ms cross-connect demand at new IXs | +2.3% | Johannesburg | Short term (≤ 2 years) |

| Local content-hosting mandates | +3.7% | National | Long term (≥ 4 years) |

| Eskom green-tariff pilot for PPA adoption | +2.9% | Renewable-energy zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Cloud-First Strategies Among Enterprises

A national pivot toward public-cloud adoption sees the domestic cloud services market tripling to ZAR 113 billion by 2028, compelling enterprises to redesign server estates around hybrid and multi-cloud architectures. Google Cloud’s Johannesburg region, preferred by 43% of local businesses, anchors demand for servers that marry local data residency with hyperscale performance. Financial institutions lead the shift, migrating core workloads yet retaining compliant, high-density blades for sensitive data. The National Data and Cloud Policy solidifies this dual-footprint model, sustaining local capacity even as off-premises usage grows.[1]Government of South Africa, “National Data and Cloud Policy,” gov.za Vendors that integrate seamless cloud interconnects, on-premises compliance features, and GPU readiness capture a disproportionate share in the South Africa data center server market.

Surge in AI/ML and Edge Workloads Requiring High-Density Servers

AI workloads accelerate GPU adoption and push power densities above 25 kW per rack, driving a redesign of cooling regimes.[2]International Energy Agency, “Electricity 2025,” iea.org Dell, Lenovo, and Supermicro now refresh GPU nodes annually to align with Nvidia’s release cadence. Healthcare illustrates this pivot: the National Health Laboratory Service roadmap calls for AI-enabled diagnostics that depend on local, high-density compute clusters.[3]National Health Laboratory Service, “Strategic Plan 2025-2030,” nhls.ac.za Simultaneously, manufacturing and telecom operators deploy edge servers to process sensor data in real time, reducing backhaul latency. These workloads amplify the South Africa data center server market’s appetite for liquid-cooled micro-blade platforms that pack maximum GPU horsepower into constrained footprints.

Rapid Fibre-to-the-Data-Centre Roll-outs by Telkom, DFA and MTN

More than 165,000 km of Telkom fibre and multi-billion-rand builds by Dark Fibre Africa and MTN shorten latency and widen access to carrier-neutral facilities. As prices fall, enterprises distribute disaster-recovery nodes between Johannesburg and Cape Town, expanding addressable server demand. Residential fibre, led by Vumatel’s 1.9 million-home footprint, fuels edge-content caching near consumers. SA Connect targets nationwide broadband coverage, opening rural markets to micro data-centres and edge servers. Robust backhaul is therefore a structural enabler of the South Africa data center server market’s long-term growth.

Local Content-Hosting Mandates in POPIA and Film and Publication Board Act

POPIA requires that personal data be processed on South African soil, locking in local compute needs for banks, healthcare providers, and media firms. Streaming platforms must store copies of licensed content locally, spurring demand for high-capacity storage arrays. Healthcare providers adopt in-country AI platforms to comply with stringent patient-data rules. By compelling on-shore processing, these statutes guarantee a persistent expansion path for the South Africa data center server market, even as global cloud offerings mature.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating construction CapEx on metal price spikes | -2.8% | Nationwide | Short term (≤ 2 years) |

| Chronic grid-power instability and diesel reliance | -3.4% | Industrial zones | Medium term (2-4 years) |

| Import duties of 5%–15% on fully-assembled servers | -1.9% | Ports and free-trade zones | Short term (≤ 2 years) |

| Skills shortage limiting Industry 4.0 implementation | -1.6% | Manufacturing clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Construction CapEx Amid Steel, Copper and Lithium Price Spikes

Raw-material volatility inflates shell-and-core costs, delaying commissioning cycles and reducing free cash for server refreshes. Copper price surges strain electrical and cooling budgets, while lithium costs lift battery-UPS expenditure. Operators counter this pressure with modular builds and off-site prefabrication, yet up-front capital intensity still tempers the South Africa data center server market’s tempo. Larger incumbents leverage scale purchasing, widening the gap over smaller entrants.

Chronic Grid-Power Instability Driving Costly Diesel Backup

Despite a slowdown in rotational power cuts, Eskom’s tariff reform and supply constraints elevate operating costs. Data-centre operators maintain diesel gensets and battery strings, pushing energy overheads to 65% of operational spend during peak outages. Teraco and others sign long-term wind-and-solar PPAs to hedge, but capital outlays delay ROI. Power insecurity therefore caps expansion velocity across the South Africa data center server market and accelerates demand for energy-efficient servers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data-Center Tier: Mission-Critical Infrastructure Drives Tier 4 Growth

Tier 3 facilities held 62.10% of 2025 revenue, giving them leadership within the South Africa data center server market. Banks, insurers, and public-sector agencies trust Tier 3 for a balance of uptime and cost. Tier 4 supply, although only a fraction today, will post a 24.62% CAGR to 2031 as hyperscalers standardize on fault-tolerant architecture. This shift raises the South Africa data center server market size for advanced power distribution, redundant feeds, and liquid-cooling systems. POPIA and the National Data and Cloud Policy further tilt decisions toward higher tiers that guarantee compliance.

Mission-critical workloads such as digital payments require 99.995% availability, prompting migration to Tier 4 halls in Johannesburg. Multinational cloud providers replicate global design templates that specify concurrent maintainability, elevating local engineering standards. Tier 1 and Tier 2 remain cost-effective for edge nodes where latency trumps redundancy. Overall, premium-tier take-up boosts demand for high-density, hot-swappable blades and GPU shelves across the South Africa data center server market.

By Form Factor: Micro-Blades Emerge as Edge Computing Catalyst

Half-height blades secured 54.60% revenue in 2025, reflecting a legacy of enterprise virtualization. Edge deployments, however, elevate quarter-height and micro-blades, which will expand at 25.07% CAGR. Telecommunications operators place micro-blades in 5G base-station shelters, reducing backhaul and enabling real-time analytics. Manufacturing plants adopt ruggedized variants to facilitate predictive maintenance. Liquid-cooling solutions launching in 2025 unlock rack densities above 70 kW, a milestone that enlarges the South Africa data center server market size for compact form factors.

Space-constrained colocation cages in Cape Town also adopt micro-blades to optimise rack revenue. Full-height blades remain relevant for research and rendering workloads that need maximum memory channels. Vendors that align design roadmaps with one-year GPU cadences seize opportunity, as enterprises refresh earlier to secure AI horsepower.

By Application/Workload: AI/ML Acceleration Reshapes Computing Demands

Virtualization and private cloud kept a 38.70% slice of 2025 consumption, anchoring steady revenue for conventional x86 nodes. Yet AI/ML training racks will grow at 26.22% CAGR to 2031, powered by finance, healthcare, and mining analytics. GPU scarcity raises lead times, hence hyperscalers reserve allocations a year ahead. High-performance computing remains essential for weather research and seismic exploration, maintaining a smaller but stable footprint in the South Africa data center server market.

Edge and IoT gateways proliferate, processing telemetry in milliseconds and feeding centralized clusters for deeper inference. Regulatory pressures confine sensitive patient and transaction data to in-country AI clusters, reinforcing local demand. Consequently, purpose-built GPU servers enlarge the South Africa data center server market share for accelerated computing platforms.

By Data-Center Type: Hyperscalers Drive Infrastructure Modernisation

Colocation dominated with 72.60% share in 2025 as enterprises outsourced real estate and operations. Google, Microsoft, and AWS now localize capacity, lifting hyperscaler CAGR to 27.05%. Their arrival scales the South Africa data center server market through bulk purchasing, 100 MW campuses, and subsea cable anchoring. Enterprise data-centres, while declining in proportion, still upgrade internal nodes for compliance and latency-sensitive systems.

Edge micro-datacentres multiply across retail malls and mining sites, where sub-10 ms latency boosts application performance. These compact sites rely on micro-blades and fan-less designs, carving a new layer in the South Africa data center server industry. Vendors that preload infrastructure for hyperscaler specifications secure predictable multi-year demand streams.

By End-Use Industry: Manufacturing Digitisation Accelerates Despite Readiness Gaps

IT and telecoms retained 30.70% revenue in 2025, owing to network-function virtualisation and cloud hosting. Manufacturing, though less mature, will scale server demand at 27.68% CAGR, led by automotive and mining. These sectors deploy IoT sensors and AI inspection systems that require rugged edge nodes, enlarging the South Africa data center server market size for industrial-grade gear. BFSI sustains investment in encryption-capable blades to satisfy financial regulators, while healthcare adopts GPU clusters for imaging diagnostics and electronic records.

Skills shortages and capex constraints hamper many small factories. Import-duty regimes favour local assembly, encouraging OEMs to partner with contract manufacturers. Government grants under the Industrial Policy Action Plan provide funding for pilot smart-factory projects, indirectly supporting server uptake. As Industry 4.0 adoption widens, cross-sector diversification stabilises revenue across the South Africa data center server market.

Geography Analysis

Johannesburg and Cape Town account for an estimated 78% of installed racks, driven by dense fibre backbones, subsea cable landings, and skilled labour. Johannesburg’s interconnection ecosystem grew rapidly after NAPAfrica crossed the 5 Tbps threshold, supporting low-latency east-west traffic flows. Cape Town benefits from renewable-energy corridors that mitigate grid risk and from WACS and Equiano cable gateways connecting to Europe, which diversify supply inside the South Africa data center server market.

Beyond the metros, Durban and Port Elizabeth attract disaster-recovery nodes and content caches that serve coastal populations. DFA’s 16 million-rand build-out in Secunda links petrochemical and mining operations to core clouds, unlocking new edge opportunities. SA Connect’s rural broadband agenda will push micro-data-centre rollouts into Northern Cape solar hubs, where abundant sun supports off-grid server clusters.

South Africa further positions itself as a regional hub for the Southern African Development Community members. Cross-border enterprises shift workloads to Johannesburg to leverage mature peering, while content-delivery networks store popular media closer to Zambia, Botswana, and Mozambique audiences. Consequently, geographic diversification balances risk and sustains expansion across the South Africa data center server market.

Mordor Intelligence evaluates the data center server market across all key regional markets, including Africa, Asia, and Middle East, with deeper country-level insights covering Nigeria, Philippines, Saudi Arabia, Singapore, Japan, and Germany.

Competitive Landscape

Competition remains moderate as no vendor exceeds a 15% revenue slice, yet technological churn intensifies. Dell, Lenovo, HPE, and Supermicro pivot to annual GPU cycles, eroding advantages of slower-moving rivals. Liquid cooling emerges as a differentiation lever: Supermicro plans to equip 15% of new halls with direct-chip liquid loops, reducing rack PUE to 1.1. Local assemblers exploit 5%–15% import tariffs to offer POPIA-compliant systems at lower landed cost, attracting state-owned enterprises and mid-tier banks.

Huawei courts municipal cloud and smart-city contracts, bundling servers with networking and surveillance suites. HPE emphasises GreenLake Private Cloud AI, bundling consumption-based pricing that resonates with CFOs seeking opex models. Suppliers providing holistic power-usage analytics and compliance dashboards gain traction inside the South Africa data center server market because operators must justify energy spend to boards and regulators.

White-space opportunities cluster around edge infrastructure for mining and agro-processing, where rugged servers encounter little incumbent presence. Channel partners with engineering services for industrial environments enjoy higher margins. Overall, hardware vendors that translate global product roadmaps into locally compliant, power-efficient bundles capture leadership.

South Africa Data Center Server Industry Leaders

Dell Inc.

Hewlett Packard Enterprise

Lenovo Group Limited

Huawei Technologies Co., Ltd.

International Business Machines Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Google launched its first African cloud region in Johannesburg with ZAR 2.5 billion investment, catalysing regional server demand.

- March 2025: NAPAfrica Internet Exchange surpassed 5 Tbps peak traffic, reinforcing Johannesburg as Africa’s largest IX.

- March 2025: Eskom adopted NERSA-approved FY 2026 tariffs effective April 1, altering electricity cost structures for data-centre operators.

- May 2025: Kaseya enabled local Microsoft 365 backup in South Africa, expanding compliant cloud options.

- April 2025: Microsoft unveiled a USD 1.4 billion data-centre park that will serve AI workloads across Africa.

- March 2024: NetActuate expanded its Johannesburg facility to boost capacity and interconnects.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Africa data-center server market as all new, factory-built rack, blade, and tower servers that are installed inside carrier-neutral colocation sites, cloud, or enterprise data centers located within the country. Revenue is tracked at ex-factory average selling price (ASP) and excludes any value-added services.

Scope Exclusion: Used or refurbished servers and hyperscale build-to-suit imports that never clear South African customs are not counted.

Segmentation Overview

- By Data-Center Tier

- Tier 1 and 2

- Tier 3

- Tier 4

- By Form Factor

- Half-height Blades

- Full-height Blades

- Quarter-height / Micro-blades

- By Application / Workload

- Virtualisation and Private Cloud

- High-Performance Computing (HPC)

- Artificial Intelligence/Machine Learning and Data Analytics

- Storage-centric

- Edge / IoT Gateways

- By Data Center Type

- Hyperscalers/Cloud Service Provider

- Colocation Facilities

- Enterprise and Edge

- By End-use Industry

- BFSI

- IT and Telecom

- Healthcare and Life-Sciences

- Manufacturing and Industry 4.0

- Energy and Utilities

- Government and Defence

Detailed Research Methodology and Data Validation

Primary Research

Telephone interviews with data-center operators, server distributors, and senior infrastructure officers across Gauteng, Western Cape, and KwaZulu-Natal helped us validate shipment splits, typical ASP movement, and utilization ramps. Follow-up surveys with global OEM channel teams closed remaining gaps on blade versus rack mix.

Desk Research

We first mapped the national demand pool through freely available sources such as Statistics South Africa's ICT supply-and-use tables, SARS import codes 8471/8473, the Independent Communications Authority of South Africa's annual ICT indicators, and the South African Reserve Bank's quarterly exchange data. Trade association notes (e.g., FTTH Council Africa) and peer-reviewed papers on edge compute density fleshed out regional deployment patterns. When company-level splits were required, D&B Hoovers and Dow Jones Factiva provided financials and deal news. Local press releases on new facilities, tender portals that publish rack counts, and patent filings extracted via Questel helped us cross-check claimed capacities and refresh assumptions. This list is illustrative only; many other public and subscription sources were tapped for verification and clarification.

Market-Sizing & Forecasting

A top-down build tied national IT load (MW) to standard rack densities, which was then multiplied by verified rack counts to derive unit demand, followed by ASP application. Select bottom-up checks, supplier sales roll-ups, and channel sell-through audits tempered the totals. Key model inputs include rack density migration, enterprise cloud penetration, 5G subscriber growth, import duty shifts, and average blade ASP trends. Multivariate regression, informed by primary-research consensus on these variables, drives the 2025-2030 forecast. Where bottom-up estimates were sparse, weighted interpolation from adjoining quarters kept variance below 3 %.

Data Validation & Update Cycle

Outputs pass three analyst reviews, after which anomalies trigger re-engagement with interviewees. Models refresh every twelve months, with interim updates issued when material events, such as a >20 MW campus announcement, occur.

Why Our South Africa Data Center Server Baseline Stands Up to Scrutiny

Published numbers often diverge because firms choose different form-factor mixes, treat imported hyperscale gear unevenly, or refresh models on dissimilar cadences.

Key gap drivers include narrower hardware-only scopes, single-source ASP assumptions, or currency conversions frozen at announcement date. Mordor Intelligence updates variables quarterly and applies both capacity and price bridges, which keeps our 2025 baseline balanced and transparent.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.9 B (2025) | Mordor Intelligence | - |

| USD 1.93 B (2024) | Global Consultancy A | Treats installation services as product revenue, inflation not rebased |

| USD 0.25 B (2023) | Regional Consultancy B | Counts only rack servers in enterprise sites, excludes cloud and blade units |

These comparisons show that once scope, ASP cadence, and deployment channels are normalized, our baseline offers decision-makers a dependable, repeatable view of South Africa's fast-growing data-center server opportunity.

Key Questions Answered in the Report

What is the current value of the South Africa data center server market?

The market stands at USD 2.33 billion in 2026 and is projected to reach USD 6.45 billion by 2031.

Which server form factor is growing fastest?

Quarter-height micro-blades lead with a 25.07% CAGR thanks to edge computing needs.

Why are Tier 4 data-centres expanding quickly?

Financial-services and hyperscale operators demand 99.995% uptime to meet regulatory and service-level commitments, boosting Tier 4 at 24.62% CAGR.

How does Eskom’s power situation affect data-centres?

Grid instability raises diesel and energy costs, trimming market CAGR by an estimated 3.4%.

Which workload category will dominate future server demand?

AI and machine-learning workloads are forecast to grow at 26.22% CAGR, surpassing traditional virtualization.

What geographic areas in South Africa host most server capacity?

Johannesburg and Cape Town together host roughly three-quarters of installed racks due to mature fibre backbones and interconnection hubs.

Page last updated on: