Aviation Cloud Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

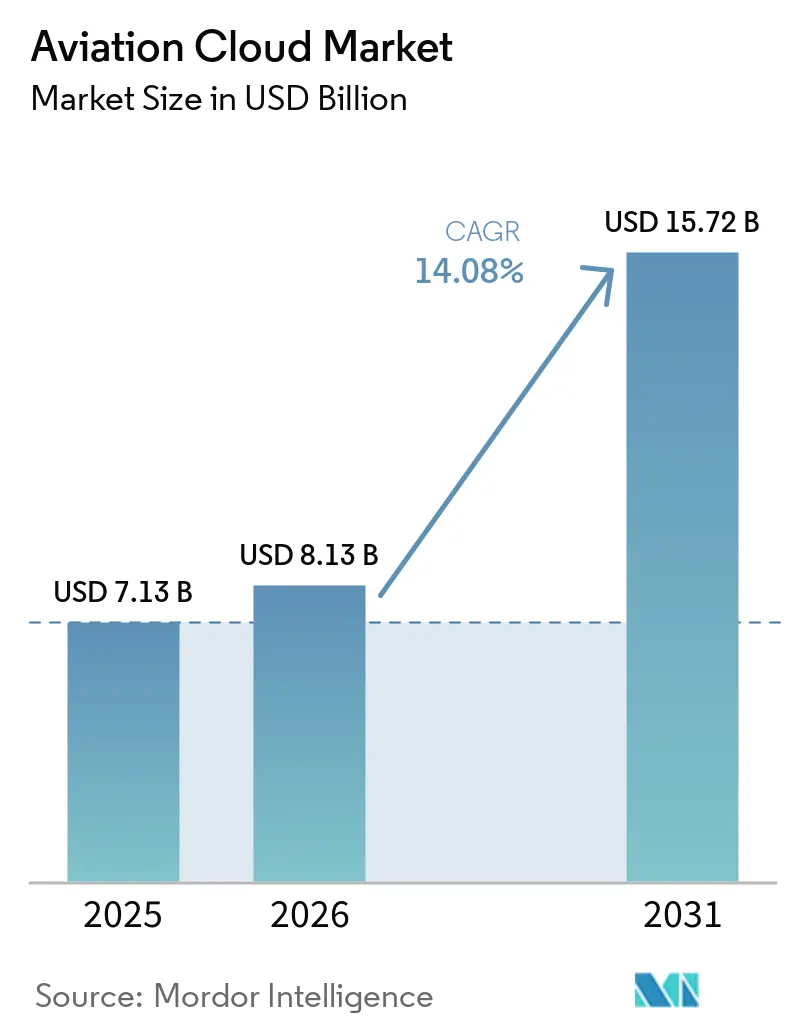

| Market Size (2026) | USD 8.13 Billion |

| Market Size (2031) | USD 15.72 Billion |

| Growth Rate (2026 - 2031) | 14.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aviation Cloud Market Analysis by Mordor Intelligence

The aviation cloud market size is expected to grow from USD 7.13 billion in 2025 to USD 8.13 billion in 2026 and is forecast to reach USD 15.72 billion by 2031 at a 14.08% CAGR over 2026-2031. Rapid workload migration from on-premise data centers to hyperscale regions is improving real-time analytics, elastic scalability, and multi-tenant economics that legacy airline systems cannot deliver. Capital reallocation toward cloud platforms intensified after global airline and airport IT spending reached USD 50.8 billion in 2025, with the aviation cloud market absorbing the fastest-growing share of those budgets. Hybrid architectures are surging as carriers comply with data-residency laws while tapping hyperscaler capacity, and platform services are enabling airlines to build proprietary analytics without managing base infrastructure. Competitive dynamics remain fluid as hyperscalers race to secure aviation-specific compliance certifications, while niche vendors use serverless microservices to undercut legacy enterprise-resource-planning software.

Key Report Takeaways

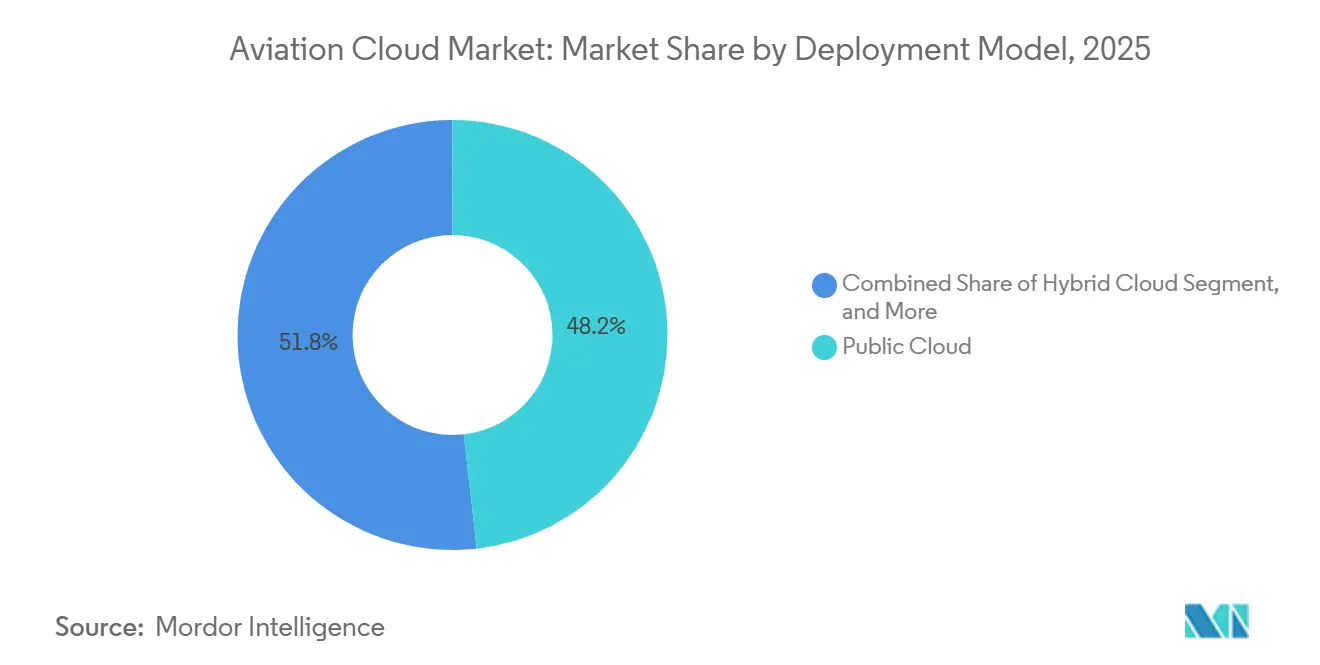

- By deployment model, public cloud led with 48.2% of the aviation cloud market share in 2025, while hybrid cloud posted the highest projected 16.9% CAGR through 2031.

- By service model, software-as-a-service captured 41.5% of the aviation cloud market revenue in 2025, and platform-as-a-service is forecast to expand at a 15.7% CAGR through 2031.

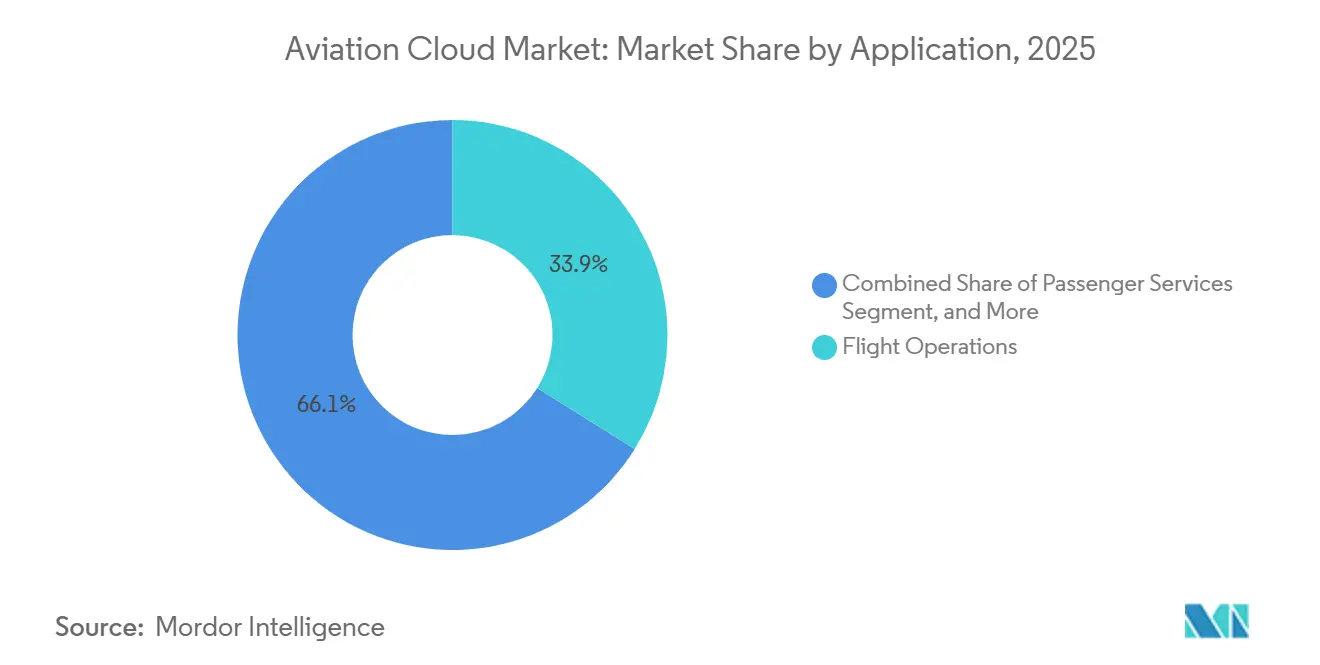

- By application, flight operations accounted for 33.9% of the aviation cloud market size in 2025, and maintenance, repair, and overhaul is advancing at a 16.1% CAGR through 2031.

- By end user, airlines held 63.7% of the aviation cloud market share in 2025, while MRO providers are projected to grow at 15.4% CAGR between 2026 and 2031.

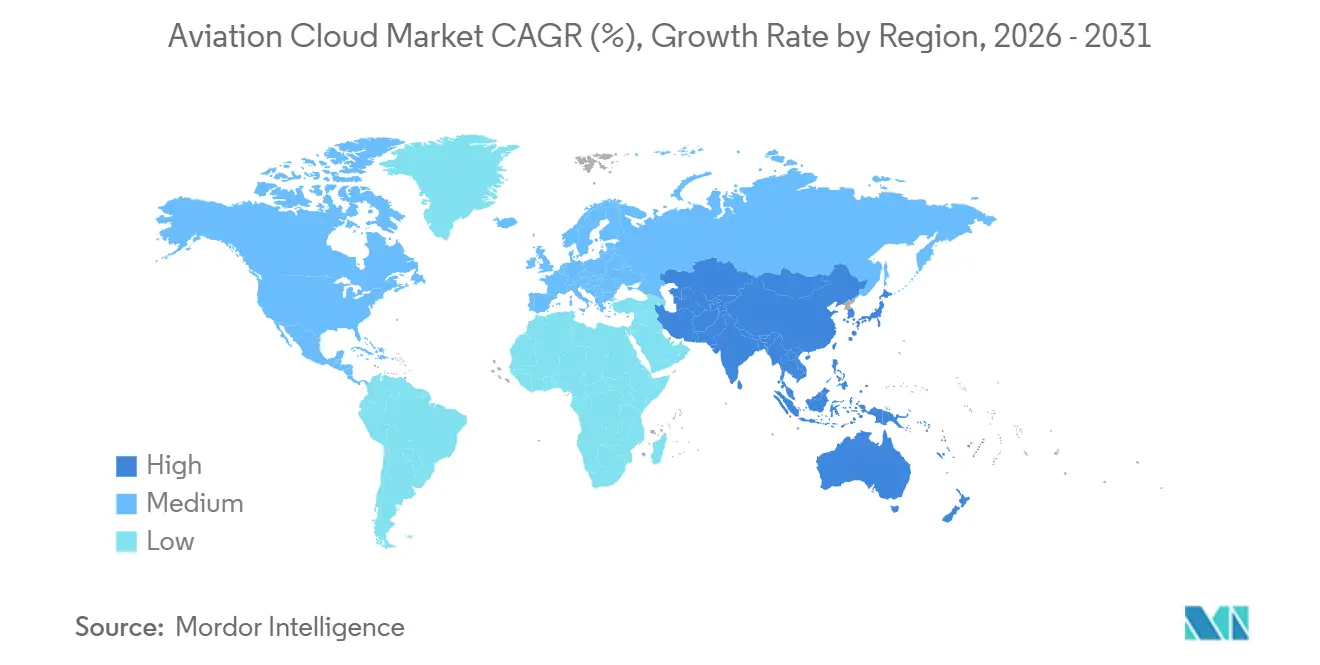

- By geography, North America commanded 36.3% revenue share of the aviation cloud market in 2025, and Asia-Pacific is expected to register the fastest 15.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aviation Cloud Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive Growth in Airline Digital-Transformation Budgets | +3.20% | Global, strongest in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising Demand for Real-Time Flight-Data Analytics | +2.80% | Global, early in North America and Europe, quick uptake in Asia-Pacific | Short term (≤ 2 years) |

| Cloud Cost-Optimization Over Legacy Airline IT | +2.40% | Global, led by North America and Europe | Medium term (2-4 years) |

| IaaS Expansion by Hyperscalers into Tier-2 Airports | +1.90% | Asia-Pacific core, spill-over to Middle East and South America | Long term (≥ 4 years) |

| Sovereign-Cloud Mandates for Aviation Data | +1.60% | Europe, Middle East, Asia-Pacific | Medium term (2-4 years) |

| Satellite-Edge Fusion for Oceanic Route Coverage | +1.30% | Global, priority on transoceanic routes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth in Airline Digital-Transformation Budgets

Airlines are diverting capital from new-aircraft programs to cloud platforms that accelerate passenger experience innovation and operational resilience. The shift is visible in SITA’s USD 50.8 billion 2025 IT-spend figure, where cloud migration rose faster than any other category.[1]SITA, “Air Transport IT Insights 2025,” sita.aero Examples include Virgin Atlantic’s 2026 launch of satellite-enabled streaming that relies on cloud back-ends for real-time loyalty updates, while several low-cost carriers in Southeast Asia run entirely serverless reservation stacks.[2]Virgin Atlantic, “Starlink In-Flight Connectivity Launch,” virgin-atlantic.com Payback periods have shortened as carriers retire lease-heavy data centers and trim IT headcount, making the aviation cloud market a core pillar of airline digital strategy.

Rising Demand for Real-Time Flight-Data Analytics

Event-driven platforms now process turbulence reports, health-monitoring telemetry, and radar plots within seconds, unlocking fuel and maintenance savings. Lufthansa’s Turbulence Aware deployment and JetBlue’s predictive-maintenance tie-in to Airbus Skywise both converted raw sensor feeds into sub-second operational decisions in 2025.[3]Lufthansa, “IATA Turbulence Aware Partnership,” lufthansa.com EUROCONTROL’s 2025 proof-of-concept extended the model to air navigation service providers, indicating that real-time processing is becoming mandatory across the aviation cloud industry.

Cloud Cost-Optimization Over Legacy Airline IT

Hybrid environments have shown double-digit annual savings once carriers price energy, lease, and depreciation costs into baseline comparisons. Delta Air Lines trimmed infrastructure outlays by 18% after moving revenue management to a mixed architecture in 2025, and Saber’s multi-cloud play with Google Cloud and Oracle offers consumption pricing that eliminates large upfront licenses for smaller carriers.[4]Delta Air Lines, “Hybrid Cloud Architecture Migration,” delta.com Careful design is still critical, because unchecked data-egress fees or cross-region transfers can dilute projected savings.

IaaS Expansion by Hyperscalers into Tier-2 Airports

Edge compute points placed inside secondary terminals now support queue monitoring, biometric boarding, and baggage tracking with sub-50 millisecond latency. Deployments in Mexico’s Monterrey and Guadalajara airports during 2026 reduced security wait times by more than one-fifth, demonstrating tangible passenger benefits. Asia-Pacific governments are fueling similar rollouts as they expand airports in medium-sized cities, integrating India’s Digi Yatra biometric framework that rests entirely on aviation cloud market infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Sovereignty and Data-Residency Compliance Costs | -1.40% | Europe, Middle East, Asia-Pacific, emerging in South America | Medium term (2-4 years) |

| Skill Shortages in Aviation-Grade Cloud DevSecOps | -1.10% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Volatile Jet-Fuel Economics Delaying IT Refresh | -0.80% | Global, heavier on low-cost and emerging-market airlines | Short term (≤ 2 years) |

| Stratospheric Spectrum-Sharing Uncertainty | -0.50% | Global, affects satellite connectivity plans | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Sovereignty and Data-Residency Compliance Costs

Fragmented laws force carriers to replicate infrastructure across multiple jurisdictions, lifting capital needs 15-25% above single-region setups. The European Union’s 2025 framework requires in-country processing of passenger name records, while Qatar Airways chose a private-cloud model in 2026 to satisfy national mandates. Comparable constraints in China and India compel airlines to maintain separate data lakes and audit chains, challenging uniform governance across global networks.

Skill Shortages in Aviation-Grade Cloud DevSecOps

Few engineers understand Kubernetes orchestration and zero-trust networking while also navigating DO-178C traceability rules. Lufthansa Systems reported six-month schedule overruns in 2025 because of the dual-skill deficit. As hyperscalers release serverless, confidential computing, and AI services, configuration complexity continues to rise, widening the talent gap and slowing workload migration in the aviation cloud market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Architectures Balance Sovereignty and Scale

Hybrid cloud is slated to grow 16.9% annually to 2031, reflecting airline demand for sovereign data control without forgoing hyperscaler elasticity. Delta Air Lines stores passenger information on private nodes while training demand-forecasting models on public GPUs, illustrating the two-tier pattern driving the aviation cloud market. Public deployments remain preferred for multi-tenant SaaS, such as reservations or crew scheduling, while private cloud lingers among flag carriers bound by explicit state directives. Community clouds, though small, enable regional alliances to share slots and maintenance data under joint governance, avoiding unilateral exposure.

Forward-looking deployments now interconnect private instances with edge zones inside airports to minimize latency for passenger flow, baggage tracking, and biometric boarding. The structure allows airlines to manage compliance for sensitive flight plans locally while executing high-volume analytics jobs in burstable public clusters. As regulators clarify cloud audit standards, carriers are expected to refine workload-placement policies rather than abandon the hybrid model that will anchor future growth of the aviation cloud market.

By Service Model: Platform Layers Unlock Proprietary Analytics

Platform-as-a-service should log the fastest 15.7% CAGR because it offers managed data lakes and event-streaming engines that eliminate the undifferentiated heavy lifting. Airbus Skywise, serving 200 airlines by 2025, lets carriers inject flight, maintenance, and weather feeds into a shared lake, then run custom reliability models without provisioning servers. SaaS still accounts for 41.5% of 2025 revenue, driven by passenger service, departure control, and revenue management suites migrated from mainframes to multi-tenant clouds. Infrastructure as a service underlies both layers, as airlines provision compute when lifting monolithic code for gradual refactoring.

Function-as-a-service, while niche, is emerging for discrete triggers such as automatic fare changes when competitors cut prices or auto-rebook logic during weather disruptions. This pay-per-execution model avoids idle resources, making it attractive for irregular operations. The cumulative effect of these service models underpins the expansion of the aviation cloud market, as carriers match technical tasks with the most cost-efficient abstraction layer.

By Application: MRO Digitalization Outpaces Flight Operations

Maintenance, repair, and overhaul workloads are forecast to expand 16.1% through 2031, as illustrated by Thai Airways moving its planning suite to the cloud and cutting downtime 12%. Digital records, blockchain parts tracking, and predictive algorithms require scalable ingestion from aircraft health-monitoring units, reinforcing cloud dependence. Flight operations remain the largest slice, accounting for 33.9% of revenue in 2025, covering dispatch, crew scheduling, and flight planning, where sub-second weather ingestion shapes tactical reroutes.

Passenger-service platforms integrate biometric identity, mobile check-in, and baggage APIs so travelers switch channels without re-entering data. Airport operations leverage real-time coordination among airlines, handlers, and customs to improve on-time performance. Crew optimization engines factor regulatory rest rules and preferences, while cargo, fuel, and sustainability modules complete the application stack, each benefiting from low-latency cloud data exchange inside the aviation cloud industry.

By End User: MRO Providers Accelerate Cloud Adoption

MRO providers are projected to grow spending at a 15.4% CAGR as they digitize processes to compete with OEM-aligned service networks. IFS’s 2026 roll-out at Albatechnics cut quotation cycle times 35%, proving bottom-line impact. Airlines still dominate 63.7% of the 2025 value, modernizing reservations, loyalty, and operational control across hybrid footprints. Airports deploy biometric boarding, queue prediction, and resource management that rely on shared clouds connecting airlines, security, and immigration.

Air navigation service providers migrate surveillance fusion and decision-support to managed platforms consistent with CANSO’s 2035 digital vision, while OEMs stream health-monitoring data to centralized analytics that feed design improvements. Regulators analyze safety reports using machine learning to flag emerging hazards sooner. Ground handlers and freight forwarders integrate via open APIs, demonstrating how every actor in the aviation cloud market taps scalable infrastructure for situational awareness and operational efficiency.

Geography Analysis

North America, which accounted for 36.3% of 2025 revenue, benefits from early FAA endorsement of cloud-native air-traffic systems and multi-year airline migration programs. Delta, United, and American leverage hybrid blueprints that maintain on-premise failover while scaling compute for holiday peaks. Canada’s NAV CANADA likewise shifted flight-data processing to a hybrid Azure stack, illustrating regulator confidence in controlled public platforms. Mexico’s airport operators adopted queue analytics SaaS, signaling regional spill-over.

Asia-Pacific is expected to post a 15.1% CAGR through 2031 and drive the largest absolute gain in the aviation cloud market size. India’s Digi Yatra and China’s mandate that all new airports embed cloud resource systems accelerate adoption even at tier-3 facilities. Airlines in Indonesia, Japan, and Australia migrate maintenance, inventory, and passenger-experience workloads to the cloud, often skipping legacy data centers entirely. Satellite-enabled connectivity on Singapore Airlines’ intercontinental routes demonstrates growing demand for cloud-hosted streaming and loyalty apps.

Europe’s trajectory is shaped by the 2025 Cloud Sovereignty Framework, which requires passenger records to remain within member states. The rule steers carriers toward private or community clouds and stimulates local infrastructure builds. Middle East airlines such as Qatar Airways prefer private deployments inside national borders yet still integrate with global distribution systems. South America shows mixed adoption, with Brazil and Chile modernizing airport operations through cloud platforms that cut turnaround times and enhance resource allocation.

Competitive Landscape

Hyperscalers Amazon Web Services, Microsoft Azure, and Google Cloud anchor foundational capacity in the aviation cloud market. However, SITA, Amadeus, and Saber dominate aviation-domain SaaS workloads, leading to moderate fragmentation within the market. Strategic alliances are increasingly blurring traditional boundaries. For instance, Saber’s 2025 partnership with Google Cloud and Oracle introduces consumption-based billing models tailored for smaller carriers, enhancing accessibility. Similarly, SITA’s multi-cloud strategy customizes regional solutions to address data sovereignty concerns. Meanwhile, niche innovators are leveraging serverless functions to address specific challenges, such as crew pairing optimization or dynamic ancillary services, at reduced costs. These innovators are capitalizing on gaps left by legacy ERP suppliers, carving out opportunities in the market.

Systems integrators such as Accenture, Capgemini, and Tata Consultancy Services are monetizing their expertise by offering managed services that integrate security, compliance, and workload placement. These integrators are increasingly focusing on regulatory credentials, such as ISO 27001 and IATA Operational Safety Audit, which are becoming critical factors in securing contracts. Vendors that invest early in obtaining these certifications are gaining a competitive edge. Additionally, the depth of service portfolios, the deployment of edge-compute nodes within airports, and the use of confidential-computing enclaves for safety-critical code are emerging as key differentiators. These factors are expected to significantly influence market share dynamics in the aviation cloud sector.

Looking ahead, the aviation cloud market is poised for further evolution as vendors explore advanced technologies to enhance their offerings. The integration of artificial intelligence and machine learning into cloud solutions is anticipated to drive innovation, enabling predictive maintenance and real-time decision-making. Furthermore, the adoption of hybrid cloud models is likely to increase, allowing airlines to balance cost efficiency with operational flexibility. As competition intensifies, the ability to deliver scalable, secure, and compliant solutions will remain paramount. Vendors that can effectively address these demands while fostering strategic partnerships and maintaining a focus on innovation are expected to emerge as leaders in this dynamic market.

Aviation Cloud Industry Leaders

Amazon Web Services Inc.

Microsoft Corporation

Google LLC

International Business Machines Corporation (IBM)

SITA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Aeropuerto Internacional de la Ciudad de México activated its cloud-based Sistema Integral de Gestión Aeroportuaria across both terminals, cutting the average turnaround 15% during peak departures.

- March 2026: GE Aerospace and NAVBLUE signed a memorandum to co-develop a cloud flight-operations platform combining engine health data with performance optimization tools.

- March 2026: AERODOM rolled out a cloud airport-operations suite at six Dominican Republic airports, lowering average turnaround 18%.

- March 2026: Veryon integrated its maintenance-tracking cloud with Airbus Helicopters’ fleet system, automating airworthiness compliance for rotorcraft operators.

Global Aviation Cloud Market Report Scope

The Aviation Cloud Market Report is Segmented by Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud, and Community Cloud), Service Model ( Infrastructure as a Service (IaaS), Platform as a Service (PaaS), Software as a Service (SaaS), Function as a Service (FaaS)), Application (Flight Operations, Passenger Services, Airport Operations, Maintenance Repair and Overhaul (MRO), Crew and Workforce Management, Other Applications, End User (Airlines, Airports, MRO Providers, Air Navigation Service Providers (ANSPs), Aircraft OEMs and Integrators, Aviation Regulators,and Other End-users), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Community Cloud |

| Infrastructure as a Service (IaaS) |

| Platform as a Service (PaaS) |

| Software as a Service (SaaS) |

| Function as a Service (FaaS) |

| Flight Operations |

| Passenger Services |

| Airport Operations |

| Maintenance Repair and Overhaul (MRO) |

| Crew and Workforce Management |

| Other Applications |

| Airlines |

| Airports |

| MRO Providers |

| Air Navigation Service Providers (ANSP) |

| Aircraft OEMs and Integrators |

| Aviation Regulators |

| Other End Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Turkey | ||

| Saudi Arabia | ||

| Israel | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| Community Cloud | |||

| By Service Model | Infrastructure as a Service (IaaS) | ||

| Platform as a Service (PaaS) | |||

| Software as a Service (SaaS) | |||

| Function as a Service (FaaS) | |||

| By Application | Flight Operations | ||

| Passenger Services | |||

| Airport Operations | |||

| Maintenance Repair and Overhaul (MRO) | |||

| Crew and Workforce Management | |||

| Other Applications | |||

| By End User | Airlines | ||

| Airports | |||

| MRO Providers | |||

| Air Navigation Service Providers (ANSP) | |||

| Aircraft OEMs and Integrators | |||

| Aviation Regulators | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Turkey | |||

| Saudi Arabia | |||

| Israel | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the aviation cloud market?

The aviation cloud market size stood at USD 8.13 billion in 2026 and is projected to reach USD 15.72 billion by 2031, according to Mordor Intelligence.

Which region is expected to grow fastest in aviation cloud adoption?

Asia-Pacific is forecast to expand at a 15.1% CAGR to 2031, driven by new airport construction and digital processing mandates.

Which deployment model is gaining momentum?

Hybrid cloud is rising the quickest, with a 16.9% CAGR expected as airlines balance sovereignty and scalability requirements.

Who are the major players in aviation cloud services?

Amazon Web Services, Microsoft Azure, Google Cloud, SITA, Amadeus, and Sabre dominate, with integrators such as Accenture and Capgemini providing migration support.

Which application area offers the highest growth potential?

Maintenance repair and overhaul workloads are set to grow at 16.1% through 2031 because digitized records and predictive analytics demand scalable cloud capacity.

What challenges could slow market expansion?

Stringent data-residency laws and shortages of engineers versed in both cloud security and aviation safety standards represent the most immediate brakes on adoption.

Page last updated on: