Autonomous Driving Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

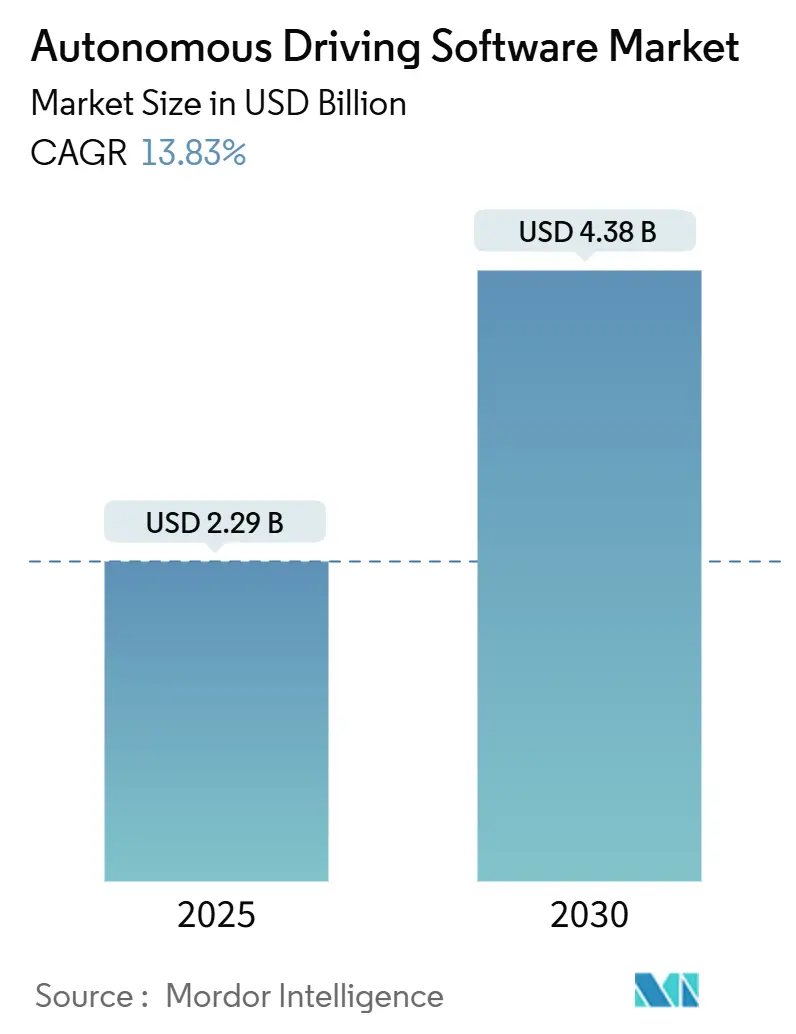

| Market Size (2025) | USD 2.29 Billion |

| Market Size (2030) | USD 4.38 Billion |

| Growth Rate (2025 - 2030) | 13.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autonomous Driving Software Market Analysis by Mordor Intelligence

The autonomous driving software market size is USD 2.29 billion in 2025 and is projected to reach USD 4.38 billion by 2030, tracking a 13.83% CAGR during the forecast period (2025-2030). Demand is spurred by mandatory advanced driver-assistance regulations, a rapid fall in sensor and compute costs, and original-equipment-manufacturer pivots to software-defined vehicles. Platform ecosystems have overtaken hardware differentiation, so value now concentrates in perception, prediction, and decision-making code. Asia-Pacific leads revenue and volume thanks to China’s policy push, while Europe and the United States supply key validation and safety frameworks. Competitive momentum favors firms able to integrate hardware acceleration with cloud-native development, shortening iteration cycles and unlocking recurring revenue through over-the-air updates.

Key Report Takeaways

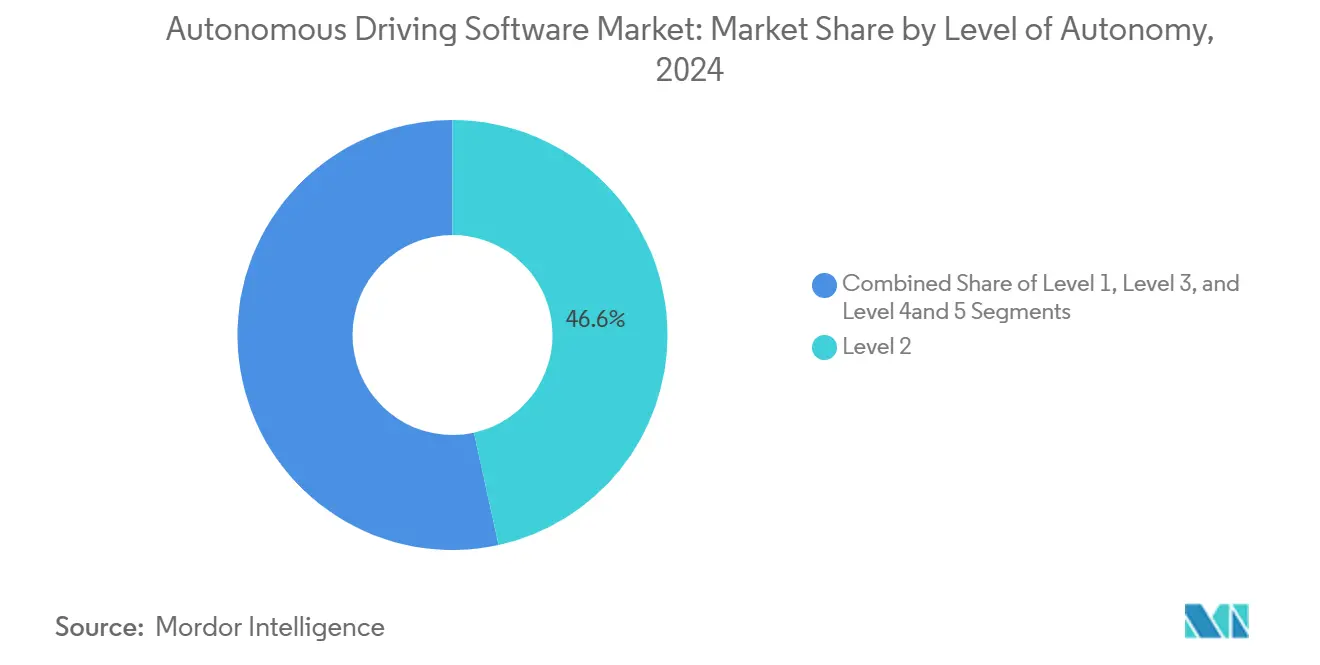

- By level of autonomy, Level 2 software held 46.57% of the autonomous driving software market share in 2024; Level 4 and 5 solutions are expected to expand at a 17.35% CAGR during the forecast period (2025-2030).

- By propulsion type, internal combustion platforms accounted for a 62.77% share of the autonomous driving software market in 2024. In contrast, electric vehicles are expected to register the fastest 18.13% CAGR during the forecast period (2025-2030).

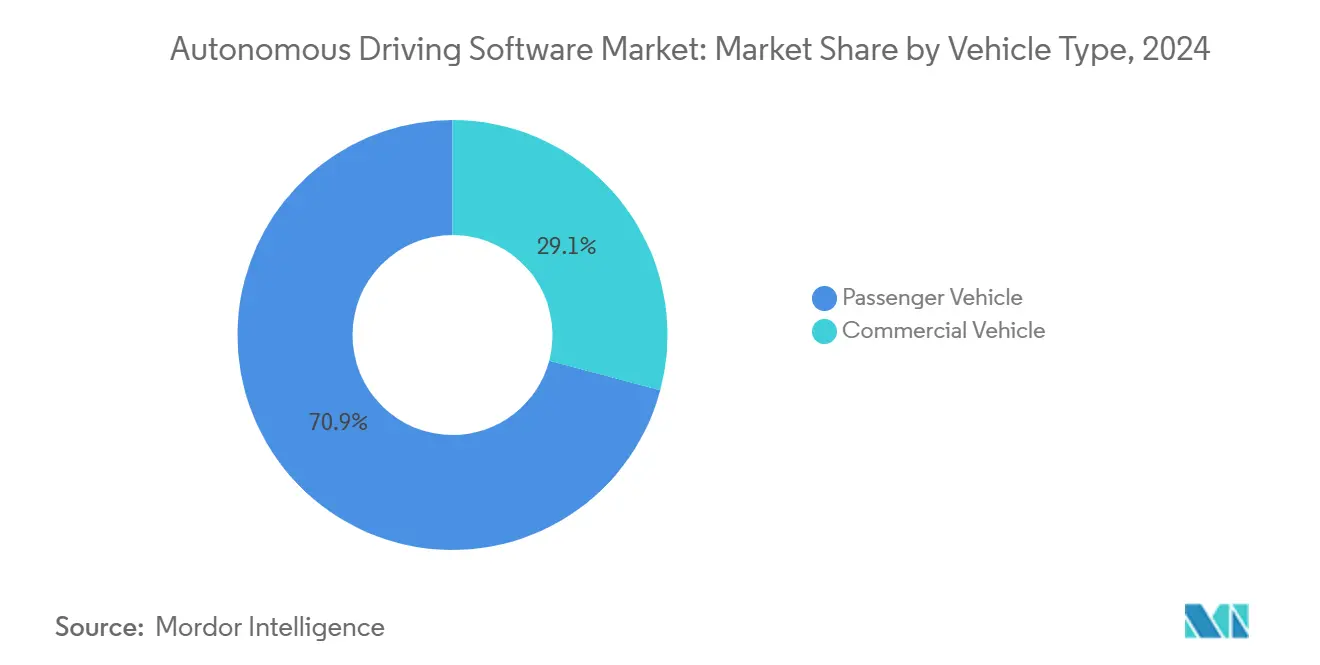

- By vehicle type, passenger cars led the autonomous driving software market with a 70.86% share in 2024; commercial vehicles are expected to grow at a 16.11% CAGR during the forecast period (2025-2030).

- By software type, perception and planning captured a 38.47% share of the autonomous driving software market in 2024, while chauffeur software is projected to rise at a 15.81% CAGR during the forecast period (2025-2030).

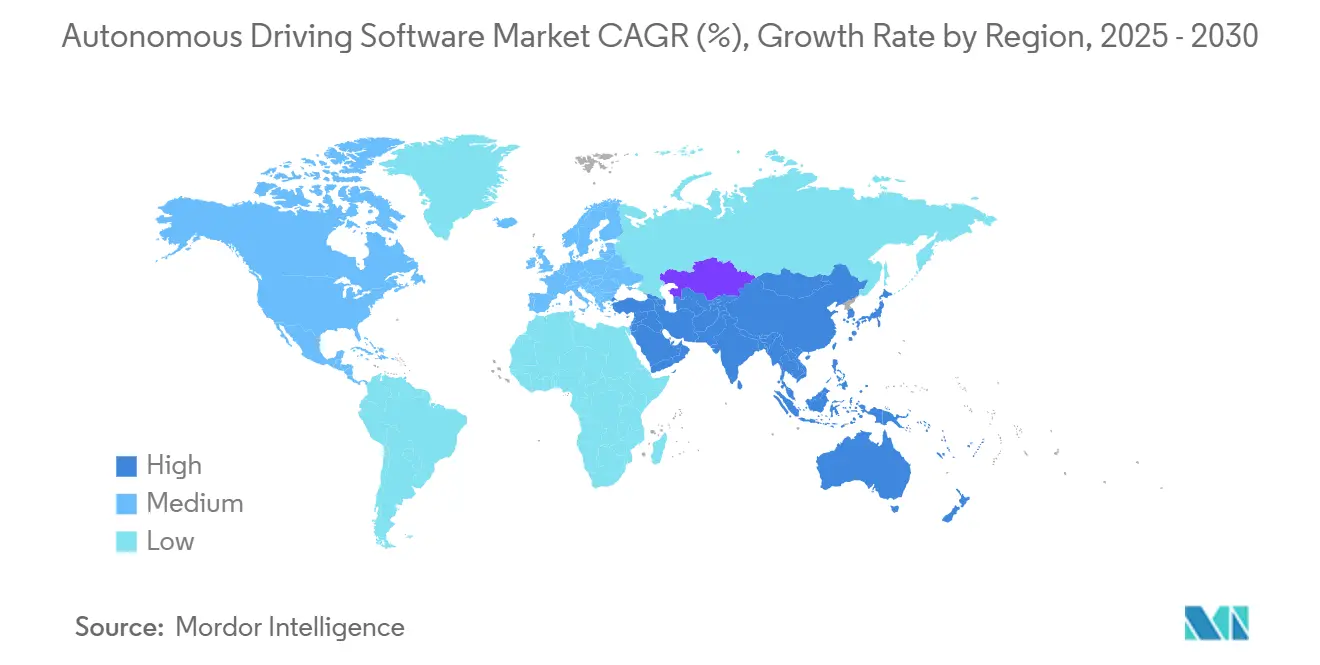

- By geography, the Asia-Pacific captured a 34.42% share of the autonomous driving software market in 2024 and is projected to grow at a 13.99% CAGR during the forecast period (2025-2030).

Global Autonomous Driving Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM Pivot to SDVs | +1.6% | Global, with North America & Europe leading adoption | Medium term (2-4 years) |

| Expanding ADAS Mandates | +1.4% | Europe, China, selective U.S. states | Short term (≤ 2 years) |

| LiDAR and Compute-Unit Costs Decline | +1.3% | Global, with APAC manufacturing advantages | Medium term (2-4 years) |

| Advanced Traffic-Management | +1.1% | Urban centers in North America, China, select European cities | Long term (≥ 4 years) |

| Cloud-Native Simulation | +0.9% | Global, concentrated in major automotive R&D hubs | Short term (≤ 2 years) |

| HD-Map-Free Perception Stacks | +0.8% | China primarily, with spillover to APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

OEM Pivot To Software-Defined Vehicles

Global automakers are reorganizing around over-the-air feature delivery and subscription revenue. General Motors finalized full ownership of Cruise, while Volkswagen aligned with a ride-hailing platform to accelerate robotaxi rollout. Tesla gained significantly from its Full Self-Driving package in 2024, proving out monetization at scale. As per the company, the software's latest version boasts "enhanced data and training compute, a fivefold boost in parameter count, and various architectural enhancements"[1]Haley Cawthon, “Tesla Q3 profits boosted by rising Full Self-Driving revenue” TechTarget, Inc., automotivedive.com. Partnerships with public cloud providers support continuous integration pipelines, allowing weekly software releases that iterate perception and planning algorithms faster than traditional model-year cycles. Competitive pressure is therefore shifting capital expenditure from mechanical engineering toward data pipelines, synthetic-simulation tooling, and safety-case automation.

Expanding ADAS Mandates In Europe, China And U.S.

The European Union’s General Safety Regulation now requires emergency braking and lane-keeping on every new vehicle, effectively guaranteeing baseline demand for perception software[2]“Implementation of the General Safety Regulation,” European Commission, ec.europa.eu. China’s C-NCAP 2024 protocol applies similar pressure by tying five-star ratings to comprehensive driver-assist suites. In the United States, a mix of state-level testing programs and NHTSA safety guidelines supplies a federal framework that supports commercial pilots while maintaining consumer protection. The harmonization of core ADAS functions establishes a stepping-stone toward higher autonomy because suppliers can amortize R&D across multiple geographic programs, shaving cost per vehicle and accelerating feature road-maps.

Rapid Decline In LiDAR And Compute-Unit Costs Post-2025

Automotive LiDAR makers forecast significant cost compression during 2025, mirrored by a robust reduction in high-performance computing modules between 2023 and 2024. Volume manufacturing shifts sensing hardware from premium models into mid-segment vehicles. Total sensor-compute bills that were previously high have dropped significantly, unlocking new addressable segments. As pricing drops, tier-one suppliers bundle multi-sensor suites with turnkey perception software, further reducing OEM integration friction and pulling forward autonomous driving feature adoption schedules.

Advanced Traffic-Management Pilots Enabling L4 Geo-Fenced Robo-Taxis

Waymo has achieved significant autonomous driving milestones across the United States cities, demonstrating the commercial viability of chauffeur-class software within geo-fenced environments. Urban partnerships integrate vehicle routing with municipal traffic-signal infrastructure, shrinking pick-up times and elevating fleet utilization. Similar models unfold in Beijing and Shanghai, where dedicated robotaxi zones supply dense operational data that closes simulation-to-reality gaps. The resulting feedback loop lifts investor confidence and frees capital for expansion into freight corridors and suburban feeder routes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Functional-Safety Talent Scarcity | -1.4% | Global, particularly acute in North America and Europe | Long term (≥ 4 years) |

| Fragmented Regulatory Approvals | -1.2% | United States primarily, with spillover effects globally | Medium term (2-4 years) |

| Thermal-Management Limits in EVs | -0.9% | Global, with particular challenges in hot climate regions | Short term (≤ 2 years) |

| Cyber-Security for OTA | -0.7% | Global, with varying regulatory frameworks by region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity Of Functional-Safety Talent For ISO 26262 And SOTIF

Industry demand for engineers qualified under ISO 26262 and SOTIF outstrips supply. Certification combines deep automotive safety know-how with machine-learning validation skills, a profile cultivated over multiple years of project experience. Leading suppliers report open positions unfilled for up to one year, stretching project timelines and raising salary costs. University programs are expanding, yet the talent gap will persist through the decade. Limited staffing slows safety-case preparation, which in turn delays regulatory clearance for Level 3-plus functions.

Fragmented Regulatory Approval Across U.S. States

The United States states possess individual autonomous-vehicle statutes, each with unique permitting, insurance, and reporting rules. Developers must maintain separate compliance tool-kits, elevating overhead and complicating multi-state fleet logistics. Although NHTSA sets baseline safety expectations, the absence of a harmonized national law stalls nationwide commercial rollouts, especially for freight carriers that cross multiple jurisdictions. The resulting uncertainty dampens capital investment and elongates commercialization timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Level Of Autonomy: Level 2 Scale And Level 4 / 5 Momentum

Level 2 holds a 46.57% share in 2024 within the autonomous driving software market, anchored by adaptive cruise control and lane-centering functions rolled out across high-volume passenger platforms. Revenue flows from subscription packages that unlock enhanced driving convenience, creating steady cash flows while accustoming drivers to supervised automation features. Mandates in Europe and China force OEMs to embed these capabilities as standard equipment, ensuring baseline volume and predictable integration road maps.

Higher-autonomy Level 4 and 5 software records a 17.35% CAGR during the forecast period (2025-2030), as commercial robotaxi and hub-to-hub freight services scale beyond pilot volume. Geo-fenced operating domains, combined with remote-assistance safety protocols, allow revenue operations without an in-vehicle driver. Regulatory pathways remain stringent, yet successful safety-case filings in select cities signal accelerating approvals. Investment funnels toward perception redundancy, behavioral prediction fidelity, and real-time fail-over mechanisms that meet functional safety targets.

By Propulsion Type: Electric-Vehicle Integration Advantages

Internal-combustion platforms command a 62.77% share of the autonomous driving software market size in 2024 because legacy fleet architectures continue to dominate global sales. Hybrid systems face power management complexity that complicates autonomous driving software implementation. OEMs retrofit ADAS features via distributed electronic-control units, but thermal envelopes and 12-volt wiring constrain compute scalability. Software upgrades, therefore, face physical bottlenecks, limiting roadmap agility.

Electric vehicles advance at an 18.13% CAGR during the forecast period (2025-2030), leveraging high-voltage electrics and centralized compute to accommodate multi-sensor arrays and GPU-class processors. Cooling loops originally designed for battery packs now dissipate AI workload heat, solving a critical thermal hurdle. Over-the-air firmware orchestrates battery management and autonomous functions through a unified software stack, supporting continuous feature extension and heightening customer lifetime value.

By Vehicle Type: Commercial Fleets Lead Uptake Economics

Passenger cars generate a 70.86% share of the autonomous driving software market's 2024 revenue, supported by consumer demand for safety and convenience. Volume guarantees economies of scale for camera modules, radar, and domain controllers, thus pulling down unit cost curves that benefit the entire ecosystem. Marketing narratives reposition autonomy as a safety feature rather than a premium gadget, widening mass-market acceptance.

Commercial vehicles, however, post the fastest 16.11% CAGR during the forecast period (2025-2030), because automation sharply reduces driver wage exposure and improves asset utilization. Long-haul routes exhibit stable traffic patterns, enabling efficient perception model training and high miles-per-vehicle metrics. Fleet managers invest in tele-operations centers and predictive-maintenance analytics that slot directly into existing logistics software, simplifying operational change management

By Software Type: Perception Foundation And Chauffeur Growth

Perception and planning retain a 38.47% share of the autonomous driving software market size in 2024, functioning as the indispensable layer that converts raw sensor input into actionable world models. Continuous improvements in computer-vision networks and LiDAR-fusion algorithms lift detection range and classification accuracy, enhancing safety margins and enabling higher-speed operation. Cost-effective SoCs bundled with optimized neural-network accelerators push inference latency below 10 milliseconds, fulfilling stringent reaction-time requirements.

Chauffeur software posts a 15.81% CAGR during the forecast period (2025-2030), as end-to-end stacks combine perception, prediction, and control into cohesive decision engines capable of handling unstructured urban scenarios. Real-world miles harvested from commercial robotaxi fleets feed reinforcement-learning pipelines, improving long-tail competence. Remote-assistance modules and operational-design-domain monitoring guarantee fail-safe fallback, a prerequisite for regulatory approval of unsupervised driving.

Geography Analysis

Asia-Pacific leads with 34.42% share of the autonomous driving software market in 2024 and projects a 13.99% CAGR during the forecast period (2025-2030). Policy makers in China authorize large-scale pilot zones that cover mixed traffic, night conditions, and adverse weather. Domestic technology champions secure preferential access to public road test mileage, amassing proprietary datasets that differentiate perception models. Japan targets autonomous shuttles for rural mobility, while South Korea integrates 5G cellular-vehicle-to-everything backbones that enhance situational awareness. Manufacturing scale in the region compresses hardware cost and speeds global diffusion of next-generation sensor stacks.

North America ranks second and tracks a 12.76% CAGR during the forecast period (2025-2030). Silicon Valley start-ups harness abundant venture capital to explore diverse autonomy niches, ranging from sidewalk robots to autonomous middle-mile logistics. Regulatory sandboxes in California and Arizona permit public-road passenger service and ride-hailing integrations that validate commercial economics. Canada supplements the ecosystem with cold-weather testing corridors, diversifying data coverage and stress-testing perception stacks under snow and ice.

Europe maintains a coordinated regulatory environment and posts a 12.27% CAGR during the forecast period (2025-2030). The General Safety Regulation requires uniform ADAS deployment, so suppliers can amortize development across the region’s large passenger-car base. Germany’s tier-one supplier cluster provides hardware-software integration expertise, while Scandinavian countries experiment with autonomous public-transit pilots that feed operational insights back to the broader market. Harmonized privacy laws clarify data-handling obligations, smoothing cross-border fleet operations.

Competitive Landscape

Market concentration remains moderate, leaving room for specialized entrants. NVIDIA packages high-performance compute with reference perception stacks and a simulation suite, enabling OEMs to accelerate development without full vertical integration. Mobileye leverages economies of scale from millions of EyeQ chips, offering a clear upgrade path from Level 2 to Level 4 on the same hardware footprint. Waymo adopts a vertically integrated approach that controls everything from proprietary sensors to service-delivery apps, prioritizing safety validation through high-mileage real-world operation.

Technology differentiation now hinges on data assets and software-tool-chain maturity. Companies that command petabyte-scale driving logs can iterate neural-network parameters rapidly, improving generalization to new geographies. Safety-case automation, including formal verification of planner logic and synthetic-scenario-based fault injection, emerges as a new battleground. Suppliers able to document ISO 26262 compliance at the code-artifact level win preferred-vendor status among risk-averse OEMs.

Strategic alliances are multiplying. Cloud providers pair edge-compute orchestration with scalable simulation back-ends, while automakers seek shared investment structures that distribute R&D burden across partners. Mergers and acquisitions target niche capabilities such as high-efficiency perception accelerators and end-to-end tool-chain traceability. Patent filings rose around 40% in 2024, reflecting rising competition to secure algorithmic IP before mass commercialization.

Autonomous Driving Software Industry Leaders

NVIDIA Corporation

Mobileye (Intel)

Waymo LLC

Tesla, Inc.

Baidu Apollo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Nissan began public demonstrations of next-generation ProPILOT advanced driver-assist technology, integrating Wayve AI software with proprietary LiDAR-based ground-truth perception.

- September 2025: Qualcomm and BMW unveiled Snapdragon Ride Pilot, an automated-driving system built on co-developed Snapdragon Ride silicon and software.

- September 2025: NVIDIA disclosed intent to invest USD 500 million in Wayve, accelerating embodied-AI research for autonomous vehicles.

- February 2025: General Motors completed a USD 1.35 billion buy-out of Cruise, consolidating ownership ahead of expanded robotaxi launches.

Global Autonomous Driving Software Market Report Scope

| Level 1 |

| Level 2 |

| Level 3 |

| Level 4 and 5 |

| Internal Combustion Engine |

| Electric |

| Passenger Vehicle |

| Commercial Vehicle |

| Perception and Planning Software |

| Chauffeur Software |

| Interior Sensing Software |

| Supervision / Monitoring Software |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Level of Autonomy | Level 1 | |

| Level 2 | ||

| Level 3 | ||

| Level 4 and 5 | ||

| By Propulsion Type | Internal Combustion Engine | |

| Electric | ||

| By Vehicle Type | Passenger Vehicle | |

| Commercial Vehicle | ||

| By Software Type | Perception and Planning Software | |

| Chauffeur Software | ||

| Interior Sensing Software | ||

| Supervision / Monitoring Software | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What revenue does the autonomous driving software market generate in 2025?

The market generates USD 2.29 billion in 2025 and is on track to reach USD 4.38 billion by 2030.

Which region leads adoption of autonomous driving software?

Asia-Pacific holds 34% share in 2024, driven by supportive policy in China and rapid manufacturing scale-up.

Which autonomy level holds the largest commercial share?

Level 2 driver-assistance software leads with 46% share in 2024 thanks to regulatory mandates and mass-market passenger-car rollouts.

Why are electric vehicles important to autonomous software growth?

Electric-vehicle architectures supply centralized compute power and thermal capacity that simplify integration of high-performance autonomous stacks.

Which vehicle segment is expanding fastest?

Commercial vehicles post the fastest 16.11% CAGR because autonomous freight and delivery applications offer clear cost savings for fleet operators.

Page last updated on: