Autonomous Construction Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.31 Billion |

| Market Size (2030) | USD 9.49 Billion |

| Growth Rate (2025 - 2030) | 12.32% CAGR |

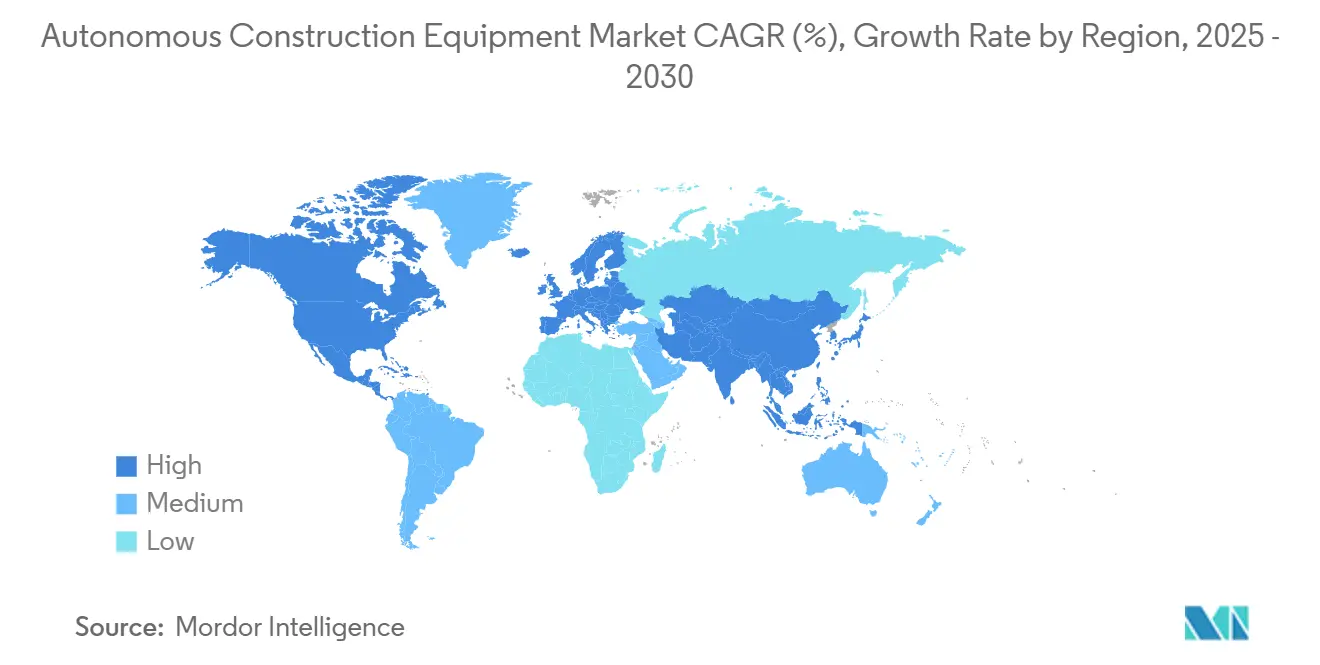

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Autonomous Construction Equipment Market Analysis by Mordor Intelligence

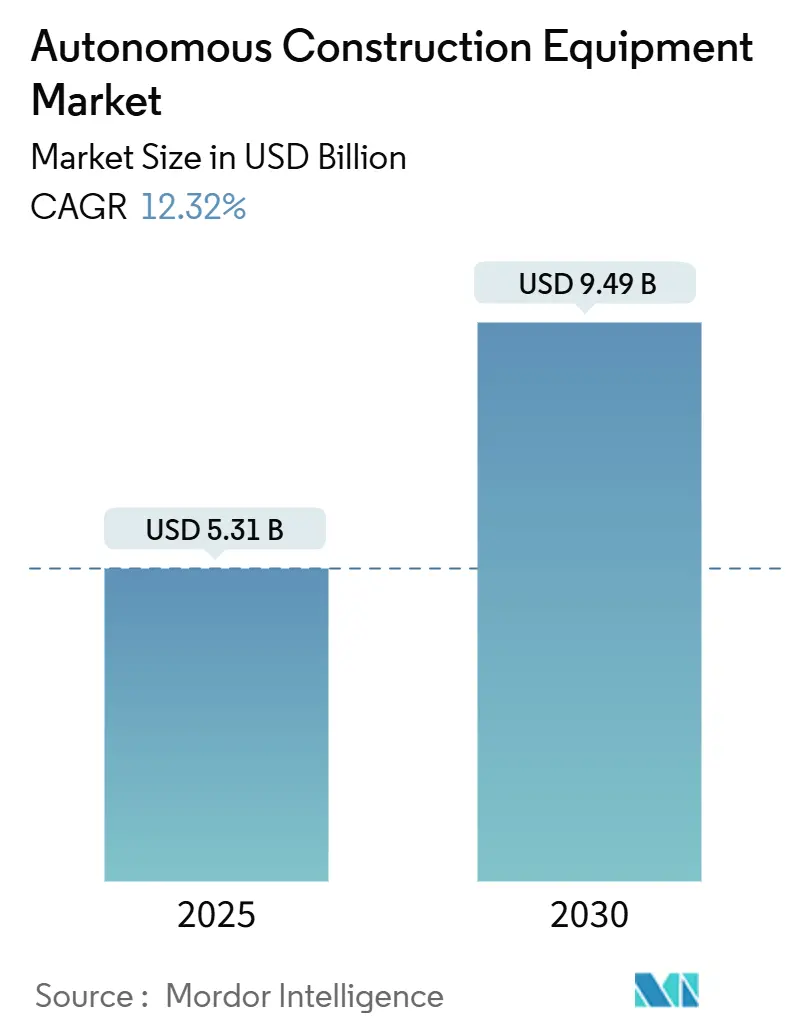

The autonomous construction equipment market size stood at USD 5.31 billion in 2025 and is forecast to climb to USD 9.49 billion by 2030, advancing at a 12.32% CAGR. Robust demand stems from acute skilled-labor shortages, tightening net-zero regulations, and rapid cost declines for key enablers such as sub-USD 70/kWh batteries. Contractors also gain clearer regulatory pathways under ANSI B11 and UL 4600 safety frameworks, which shorten adoption cycles. AI-powered fleet orchestration that raises productivity 25-30% and the growing availability of factory-ready retrofit kits strengthen the economic case for autonomy. New financing models, including technology-inclusive rental contracts, further accelerate deployments across small and mid-sized contractors.[1]Brad Kelechava, "ANSI B11.19-2019: Safeguarding and Machinery Risk Reduction", American National Standards Institute, ansi.org

Key Report Takeaways

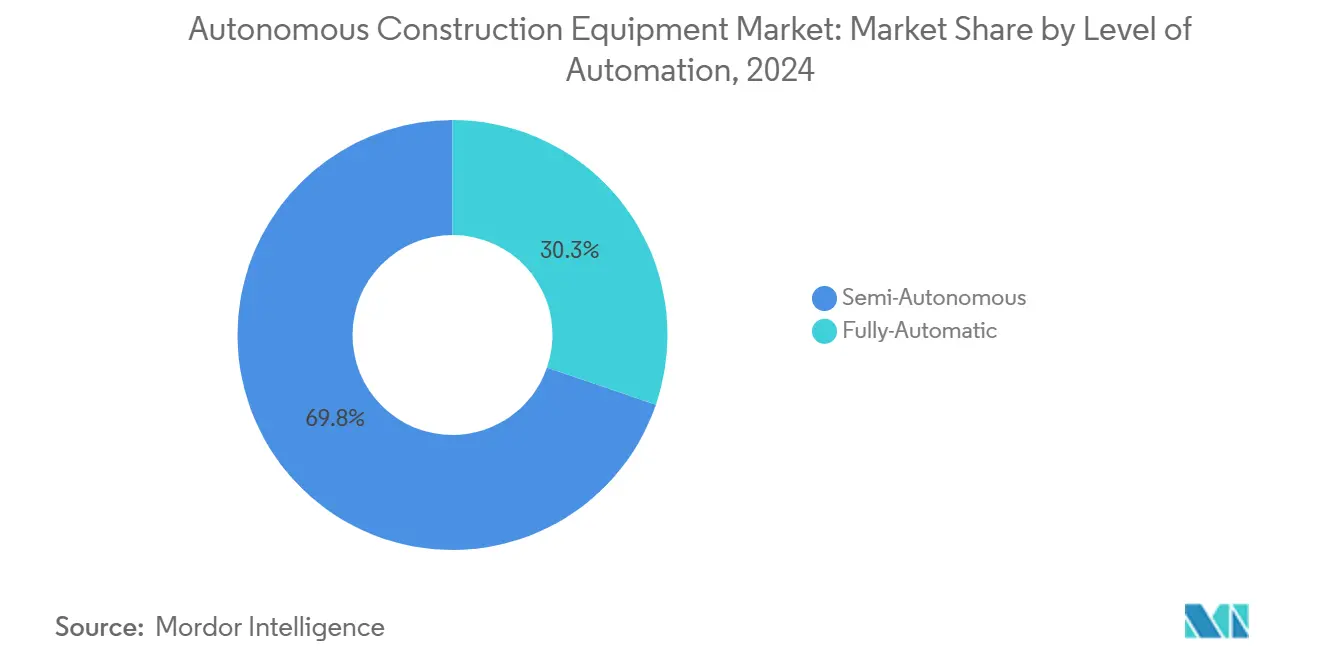

- By level of automation, semi-autonomous systems captured 69.75% of 2024 revenue, while fully autonomous solutions are poised to expand at a 17.83% CAGR to 2030

- By equipment type, earthmoving machinery held 47.18% share in 2024; light and compact tools are set to advance at a 13.42% CAGR through 2030.

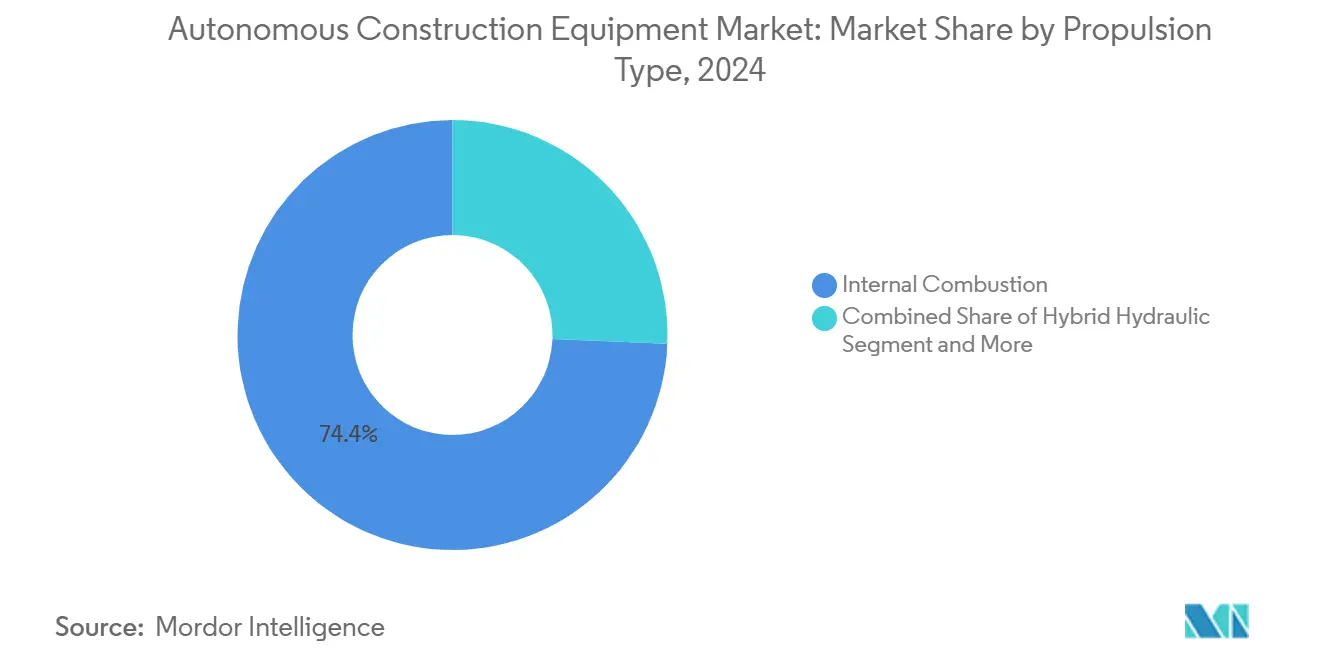

- By propulsion type, internal-combustion equipment preserved 74.36% share, yet battery-electric variants are on track for a 19.26% CAGR.

- By equipment size, heavy equipment above 11 tonnes commanded 53.34% of 2024 sales; compact equipment below 6 tonnes will grow at an 18.95% CAGR.

- By power output, systems rated up to 250 HP are projected to log the fastest expansion at 16.61% CAGR, versus the 250–500 HP segment’s 50.26% share in 2024.

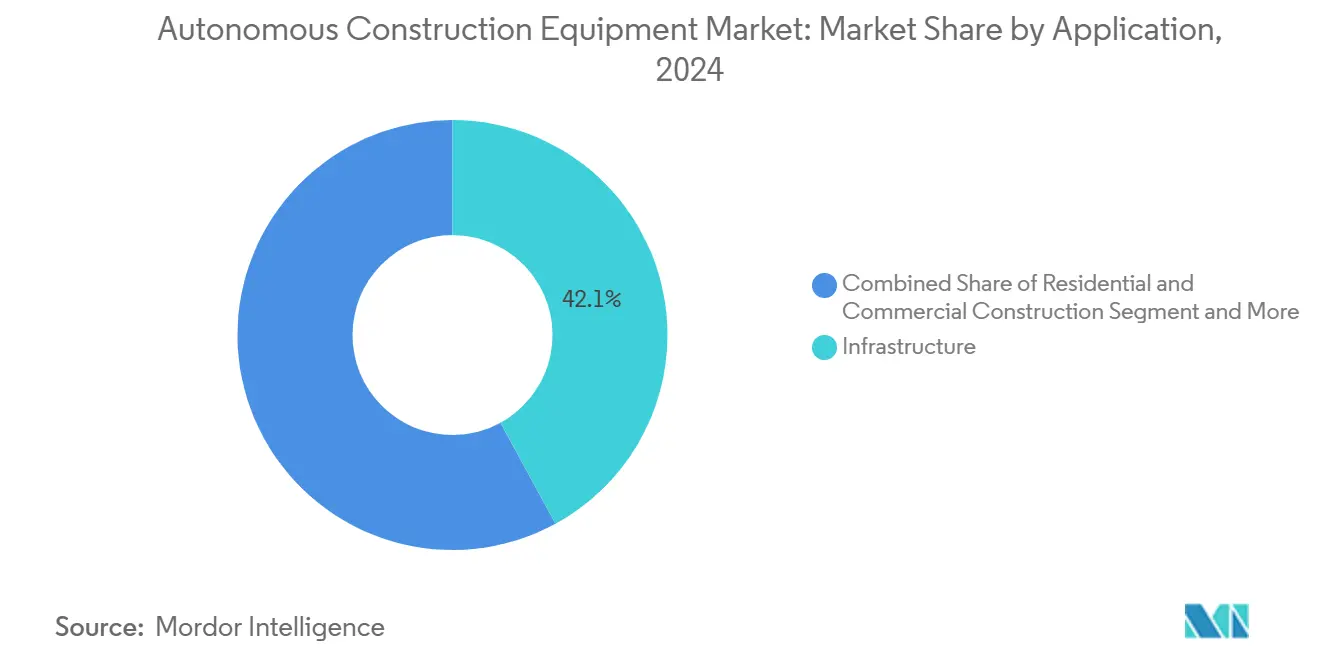

- By Application, infrastructure applications led with 42.05% share; mining and quarrying will register the highest 15.37% CAGR.

- By sales channel, new equipment sales contributed 65.64% of 2024 revenue, while rental channels are expected to post a 17.32% CAGR.

- By geography, Asia-Pacific commanded 45.13% of 2024 revenue, and will outpace all regions with a 12.51% CAGR.

Global Autonomous Construction Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labour-shortage | +2.5% | Global, with acute impact in North America & Europe | Medium term (2-4 years) |

| OEM Retrofit Kits | +1.8% | Global, with early adoption in Asia-Pacific & North America | Short term (≤ 2 years) |

| Rapid Battery-cost Decline | +1.6% | Global, with accelerated deployment in Europe & North America | Medium term (2-4 years) |

| Carbon-linked Project | +1.2% | Europe & Canada, with spillover to Australia & New Zealand | Medium term (2-4 years) |

| AI-enabled Multi-machine Fleet | +0.9% | Global, with early deployment in mining operations | Short term (≤ 2 years) |

| Defence-funded Sensor Fusion | +0.7% | North America & Europe, with technology transfer to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor-shortage Driven ROI Focus on Automation

Construction faces a projected 2.2 million-worker gap by 2026 in North America, elevating unmanned systems from optional upgrades to business-continuity necessities[2] Equipment World Staff, “Machine Control,” Equipment World, equipmentworld.com. Contractors deploying autonomous excavators cut reliance on two to three operators per shift and avoid overtime premiums. Continuous 24/7 operation improves asset utilization and compresses project timelines, enhancing bid competitiveness. Insurance savings accrue as exposure to work-site accidents falls. Compliance with updated ANSI B11 and UL 4600 standards boosts confidence among risk-averse project owners.

OEM Retrofit Kits Slashing Capital Outlay

Retrofit autonomy packages cut implementation costs 40–60% compared with new equipment purchases. Trimble-ready hardware on Liebherr PR 776 dozers illustrates factory-integrated mounting points that preserve warranties and speed field activation. Rental fleets value machine-agnostic 3D control systems that travel across brands, avoiding vendor lock-in. Lower upfront spend hastens technology trials by small contractors. Retrofit pathways also extend the service life of mixed fleets, smoothing the transition toward fully autonomous deployments.

Rapid Battery-cost Decline Enabling Electrification

Average pack prices fell below $100/kWh in 2024 and are projected to continue declining through 2030. Volvo’s EC230 Electric excavator pairs a 450 kWh pack with quick-charge capability and onboard obstacle-classification modules for autonomous operation. Electric drivetrains simplify motion control and reduce maintenance complexity for unmanned systems. Portable 564 kWh site energy storage skids from Liebherr curb infrastructure constraints and encourage off-grid deployments. The combined electrification-autonomy paradigm advances corporate carbon targets alongside productivity aims.

AI-enabled Multi-machine Orchestration

Coordinated fleets of autonomous drills, haulers, and support vehicles have surpassed 1 million meters of automated drilling at reference sites. Optimized task sequencing and collision avoidance raise productivity 25–30% compared with human-directed crews. Algorithms also create predictive-maintenance windows that minimize downtime. Such orchestration gains are especially valuable in mining pits and large infrastructure projects where multi-asset choreography dictates cycle times.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Job-site Topography | -1.4% | Global, with acute challenges in urban & mountainous regions | Short term (≤ 2 years) |

| Unharmonised Safety Regulations | -0.8% | North America & Europe, with spillover regulatory uncertainty globally | Medium term (2-4 years) |

| Data-ownership Disputes | -0.6% | Global, with particular complexity in international EPC projects | Long term (≥ 4 years) |

| High-capacity, Ruggedized Battery Packs Scarcity | -0.4% | Global, with supply chain concentration in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Job-site Topography Limiting GNSS/LiDAR Reliability

Urban reconstruction and multi-level excavations produce obstructed signals that diminish autonomous positioning accuracy. Liebherr’s GPS-independent wheel loader uses 3D environmental sensing to navigate in tunnels where satellite access fails[3]Tom Stone, “Bauma Ones to Watch,” iVT International, ivtinternational.com. Dynamic terrain changes force real-time map updates that tax onboard processing. Defense-grade sensor fusion offers a workaround yet raises system cost, inhibiting widespread use beyond premium projects.

Unharmonized Safety Regulations Across Jurisdictions Delaying Approvals

Regulatory fragmentation across jurisdictions creates compliance complexity that delays autonomous equipment deployment, with varying safety standards between US states and EU member countries requiring multiple certification processes for equipment operating across borders. Fifty individual U.S. state frameworks and diverse EU country rules create duplicative certification loops. While ISO 3691-4 offers overarching guidance, construction-specific clauses remain inconsistently applied. The resulting liability concerns prompt global EPC contractors to postpone autonomous rollouts until clearer rules materialize, slowing near-term uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Level of Automation: Transition From Supervised to Fully Autonomous Operation

Semi-autonomous machines delivered 69.75% of 2024 revenue as contractors favored operator-assisted functions for immediate productivity gains with limited risk. Fully autonomous systems, however, are forecast to capture the fastest 17.83% CAGR as regulatory clarity improves and early pilots prove reliability. Integrated command platforms now let a single supervisor oversee multiple unmanned assets, compressing labor budgets. These gains align with owner demands for shorter schedules and predictable costs.

The fully autonomous cohort benefits from advances in perception sensors and fail-safe architectures that meet ANSI B11 safety requirements. Caterpillar’s MineStar Command demonstrates scalable autonomy migrating from iron-ore mines to aggregates quarries. Early adopters report extended duty cycles and reduced idle fuel burn. Adoption barriers center on upfront integration complexity and the training required for remote supervisors rather than equipment operators.

By Equipment Type: Compact Tools Gain Momentum Against Earthmoving Leaders

Earthmoving equipment retained 47.18% market share in 2024 owing to entrenched autonomous haulage systems and motor graders across mining and highway projects. Compact tools, conversely, will post a 13.42% CAGR as autonomy penetrates skid steers, plate compactors, and material handlers popular on urban and utilities work sites. These smaller assets excel in confined areas where large machinery cannot maneuver, reducing rework and traffic disruption. Expanding model availability from mainstream OEMs keeps upfront prices in check, drawing interest from midsized contractors that lack mega-project budgets.

The autonomous construction equipment market size for compact tools remains modest yet accelerates as retrofit kits become brand-agnostic and easier to finance. Multi-machine site concepts already showcase coordinated tasks among mini-excavators, robotic track loaders, and automated compactors. Broader accessibility rests on streamlined safety certification and dealer support capable of servicing mixed fleets. Increased rental availability further lowers entry barriers by bundling maintenance, software updates, and operator onboarding.

By Propulsion Type: Battery-Electric Innovation Disrupts Combustion Dominance

Internal-combustion engines held 74.36% share in 2024, but battery-electric units are projected to surge at a 19.26% CAGR on the back of emissions mandates and total-cost savings. The autonomous construction equipment market share attributable to battery-electric machines improves yearly as public-private charging infrastructure spreads and batteries hit sub-USD 70/kWh pricing. Electric drivetrains deliver instant torque and precise speed modulation that simplify algorithmic control loops, making them a natural partner for autonomy. Rising diesel costs and corporate decarbonization pledges add financial impetus to conversion programs.

Instant torque enables smoother path-following, while regenerative braking extends runtime and trims maintenance cycles compared with diesel hydraulics. Hydrogen fuel-cell trials progress in heavy wheel loaders where battery mass proves restrictive, though commercialization remains several years away. Hybrid hydraulic systems serve as an interim step, allowing mixed fuel and electric operation during the infrastructure transition. Collectively, these propulsion options widen the technology toolkit available to fleet planners facing varied duty cycles and site constraints.

By Equipment Size: Compact Segments Democratize Autonomy

Heavy machines above 11 tonnes generated 53.34% of 2024 revenue, but compact units under 6 tonnes will expand at an 18.95% CAGR as city projects, landscaping, and rental fleets embrace autonomous assistance. The autonomous construction equipment market size tied to compact classes widens with every new OEM launch, reflecting reduced acquisition costs and simplified transport logistics. Smaller machines impose lower kinetic-energy risks, enabling quicker safety approvals and less extensive geofencing. Contractors value their ability to work beside human crews without large exclusion zones.

Hitachi’s ZE135 electric excavator shows autonomy’s precision in trench cycles where centimeter-level accuracy prevents utility strikes. Heavy classes still dominate high-volume earthmoving because payload scale drives the clearest ROI, particularly in mining and infrastructure megaprojects. Advanced perception suites and remote-diagnostic services keep large autonomous assets productive even in harsh pit conditions. Over time, lessons learned in compact categories feed back into heavy-equipment software, tightening performance gaps.

By Power Output: Sub-250 HP Machines Accelerate Adoption Pathways

The 250–500 HP category controlled 50.26% of 2024 sales, yet units rated below 250 HP will register a 16.61% CAGR as lower power bands align with urban deployment where noise and emissions caps are strict. Autonomous grade-control kits on compact track loaders illustrate this democratization, adding machine guidance to tasks once left to manual skill. Smaller powertrains also enable battery-electric packages without excessive mass, facilitating overnight charging on standard site power. Municipalities stipulate low-noise nighttime work, further favoring lower-HP autonomous assets.

Lower-power platforms feature simplified hydraulics and electronics that reduce integration hours and software complexity. In contrast, the above-500 HP tier remains critical for mining haulage where payload demands require robust power density. High-horsepower units benefit from hydrogen-ready engine prototypes, offering a path to zero-carbon operation without battery swaps. OEM roadmaps suggest cross-pollination of control algorithms between power classes, ensuring consistent user interfaces and fleet-wide orchestration.

By Application: Mining and Quarrying Lead Growth Curve

Infrastructure projects accounted for 42.05% of 2024 demand, reflecting highway and airport expansions that favor fleets of autonomous graders, rollers, and pavers. Mining and quarrying will pace the field at a 15.37% CAGR as operators replicate proven 15% cost savings from unmanned haul-truck fleets. Pit environments yield clearer lines of sight and defined haul paths, allowing faster algorithm validation and regulatory clearance. Meanwhile, oil-and-gas pipeline work and industrial plant construction experiment with autonomous trenching and material staging.

Cost-per-ton improvements, lower accident rates, and continuously optimized haul cycles motivate miners to scale deployments across continents. Residential and commercial builders adopt autonomy more slowly because fragmented sites and shorter project durations dilute ROI, yet compact autonomous tools start to bridge that gap. Specialized tunneling and bridge-inspection robots illustrate emerging niches where autonomy mitigates access hazards. Each application subsegment tailors sensor suites and control logic to local operating conditions and safety rules.

By Sales Channel: Rentals Rise as Risk-sharing Mechanism

New equipment purchases delivered 65.64% of 2024 turnover, but rental activity will climb at a 17.32% CAGR because contractors prefer flexible technology access without depreciation exposure. Rentals bundle maintenance, software updates, and telematics, simplifying lifecycle management for small firms. Rental fleets deploy cloud dashboards that track utilization and automate billing, ensuring transparent ROI metrics. Dealers reconfigure showrooms to market autonomy-ready packages alongside training services.

Used-equipment markets gain relevance when retrofit modules extend operational life and improve residual values. Portable autonomy kits that clip onto hydraulic pilot lines equip older models with grade-following functions, enlarging the addressable base. Subscription pricing for software unlocks recurring revenue streams that offset initial hardware discounts offered by rental houses. As contractors grow comfortable with autonomy, many transition from short-term rentals to long-term lease-purchase agreements that lock in total cost savings.

Geography Analysis

Asia-Pacific dominated the autonomous construction equipment market with 45.13% revenue in 2024, anchored by China’s battery-swap excavators, Japan’s precision sensors, and South Korea’s electronics supply chain. Regional governments finance smart-city and high-speed rail projects that mandate productivity gains and emissions cuts. However, the 12.51% regional CAGR trails the region's pace because adoption saturates quickly in mature sub-sectors. Divergent national standards add compliance overhead and slow pan-regional fleet sharing.

North America’s 12.42% CAGR arises from critical skilled-labor shortages and clearer safety frameworks. U.S. states such as Nevada permit live site testing, accelerating commercialization cycles. Federal infrastructure funding includes carbon-reduction scoring, nudging public contractors toward electric-autonomous packages. Canada’s tender evaluations already award points for zero-operator equipment, making autonomy a differentiator on mega-projects. Supply-chain resilience initiatives also drive local manufacturing of battery packs and sensor modules.

Europe is projected to post a robust CAGR, driven by Green Public Procurement rules that factor whole-life carbon into bid scoring[4]Liesbeth Casier and Ronja Bechauf, “Advancing Green Public Procurement and Low-Carbon Procurement in Europe,” International Institute for Sustainable Development, iisd.org. Nations like the Netherlands use CO₂ Performance Ladder incentives to reward low-emission job sites, pushing contractors to integrate electric-autonomous fleets. Fragmented safety certification across EU states complicates cross-border deployments, but ISO-aligned guidance is tightening. Early electrification pilots in cities such as Eindhoven validate emission-free autonomous diggers on municipal works, setting templates for broader rollouts.

Competitive Landscape

Market concentration remains moderate, creating space for both established OEMs and specialized autonomy providers to compete through different strategic approaches, traditional manufacturers leveraging scale and customer relationships while technology specialists offer retrofit solutions and software platforms. Caterpillar leads by bundling autonomous technology with long-standing dealer support and retrofit kits. Komatsu holds on the strength of autonomous haulage systems and integrated digital platforms. Partnerships flourish as OEMs embed specialist software; Trimble and Liebherr’s factory-ready collaboration exemplifies this hardware-software convergence.

Two strategic archetypes emerge. Full-line manufacturers embed autonomy at the factory and sell integrated fleets with service contracts. Independent technology firms such as Built Robotics pursue retrofit modules that cross brand lines, targeting rental firms and mixed fleets. Competition is also shifting toward data-layer services, with cloud orchestration subscriptions providing recurring revenue and differentiation.

New entrants exploit white-space applications including tunnel excavation, hazardous remediation, and bridge inspection where autonomy mitigates risk. Defense-derived sensor fusion and AI companies court OEMs for co-development deals. Compliance with evolving ISO 3691-4 standards is now a tender prerequisite, steering buyers toward vendors with validated safety processes. As price points fall, regional manufacturers in China and India launch lower-cost autonomous loaders, intensifying price pressure on incumbents.

Autonomous Construction Equipment Industry Leaders

-

Caterpillar Inc.

-

Komatsu Ltd.

-

Deere & Company

-

Volvo Construction Equipment

-

Hitachi Construction Machinery

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Autonomous Solutions Inc. launched ASI Construction with SoftBank, focusing on automating earth-moving fleets.

- April 2025: Hitachi Construction Machinery introduced LANDCROS Connect to integrate mixed-brand fleet data.

- January 2025: John Deere revealed second-generation autonomy kits at CES 2025, combining advanced computer vision and AI for navigation.

- November 2024: Caterpillar demonstrated fully autonomous Cat 777 trucks at Luck Stone’s Bull Run quarry.

Global Autonomous Construction Equipment Market Report Scope

| Semi-Autonomous |

| Fully Autonomous |

| Earthmoving |

| Material Handling |

| Concrete and Road Machinery |

| Light / Compact Tools |

| Internal Combustion |

| Hybrid Hydraulic |

| Battery-Electric |

| Hydrogen Fuel-Cell |

| Heavy (Above 11 t) |

| Medium (6 to 11 t) |

| Compact (Below 6 t) |

| Up to 250 HP |

| 250 to 500 HP |

| Above 500 HP |

| Infrastructure |

| Residential and Commercial Construction |

| Mining and Quarrying |

| Oil and Gas / Pipelines |

| Industrial and Manufacturing |

| New Equipment |

| Rental |

| Used / Refurbished |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Level of Automation | Semi-Autonomous | |

| Fully Autonomous | ||

| By Equipment Type | Earthmoving | |

| Material Handling | ||

| Concrete and Road Machinery | ||

| Light / Compact Tools | ||

| By Propulsion Type | Internal Combustion | |

| Hybrid Hydraulic | ||

| Battery-Electric | ||

| Hydrogen Fuel-Cell | ||

| By Equipment Size | Heavy (Above 11 t) | |

| Medium (6 to 11 t) | ||

| Compact (Below 6 t) | ||

| By Power Output | Up to 250 HP | |

| 250 to 500 HP | ||

| Above 500 HP | ||

| By Application | Infrastructure | |

| Residential and Commercial Construction | ||

| Mining and Quarrying | ||

| Oil and Gas / Pipelines | ||

| Industrial and Manufacturing | ||

| By Sales Channel | New Equipment | |

| Rental | ||

| Used / Refurbished | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast size of the autonomous construction equipment market by 2030?

The market is projected to reach USD 9.49 billion by 2030, advancing at a 12.32% CAGR.

Which region will grow fastest through 2030?

Asia-Pacific is expected to post the highest 12.51% CAGR, driven by labor shortages and supportive regulations.

Which equipment category currently holds the largest revenue share?

Earthmoving machinery led with 47.18% of 2024 revenue.

Which propulsion type is growing most rapidly?

Battery-electric equipment is set to expand at a 19.26% CAGR through 2030.

Why are rental channels gaining traction for autonomous equipment?

Rentals allow contractors to access autonomy without heavy capital outlay, spreading technology risk and supporting a 17.32% CAGR in this channel.

Which application segment is projected to see the fastest adoption?

Mining and quarrying operations are forecast to grow at a 15.37% CAGR owing to proven cost and safety benefits.

Page last updated on: