Driving Simulator Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

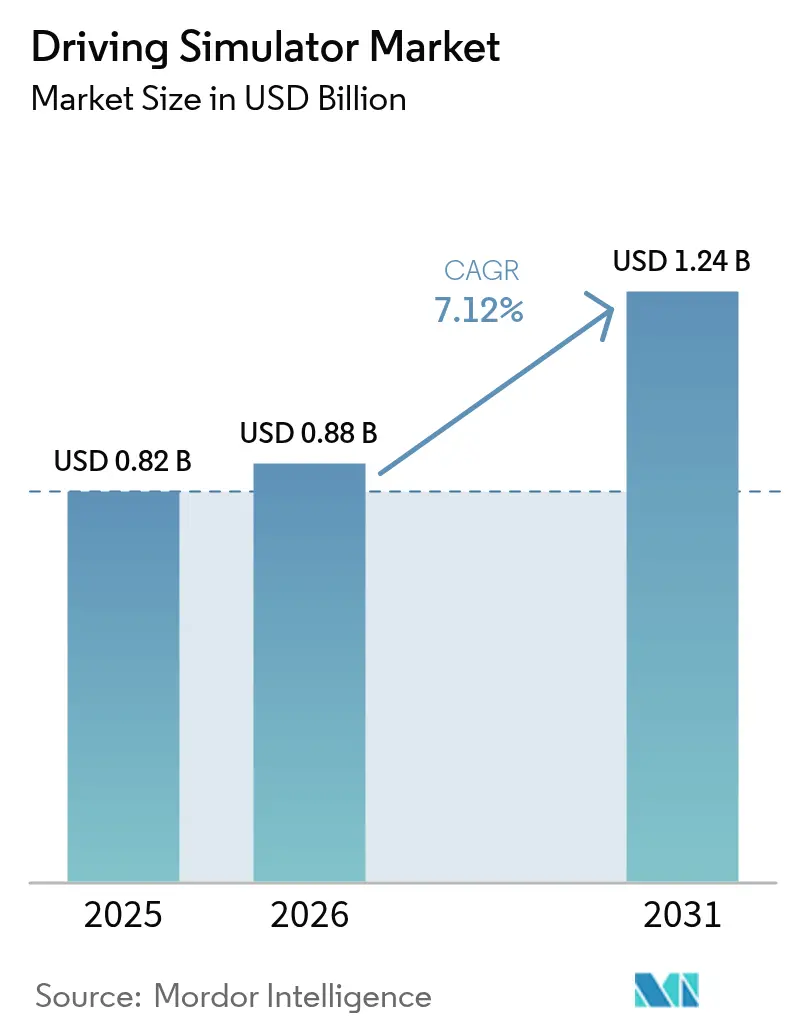

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 1.24 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Driving Simulator Market Analysis by Mordor Intelligence

The driving simulator market size was valued at USD 0.82 billion in 2025 and estimated to grow from USD 0.88 billion in 2026 to reach USD 1.24 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031). This steady rise stems from regulatory pressure for safer driver certification, the need to cut prototype testing costs, and the alignment of autonomous-vehicle roadmaps with virtual validation mandates. Commercial fleets turn to advanced simulators to shorten recruitment cycles, while carmakers channel research budgets toward software-in-the-loop test beds that complement physical tracks. Subscription-based, cloud-hosted platforms broaden access in cost-sensitive regions and nurture new user segments. Europe maintains its lead due to a mature automotive ecosystem, while Asia-Pacific contributes the largest incremental revenue as China and India expand their logistics networks. Competitive advantage now flows to providers that fuse digital twin maps, over-the-air software verification, and hardware-agnostic motion cueing. However, high capital outlays, motion sickness risks, and rising cybersecurity alerts hold back smaller adopters.

Key Report Takeaways

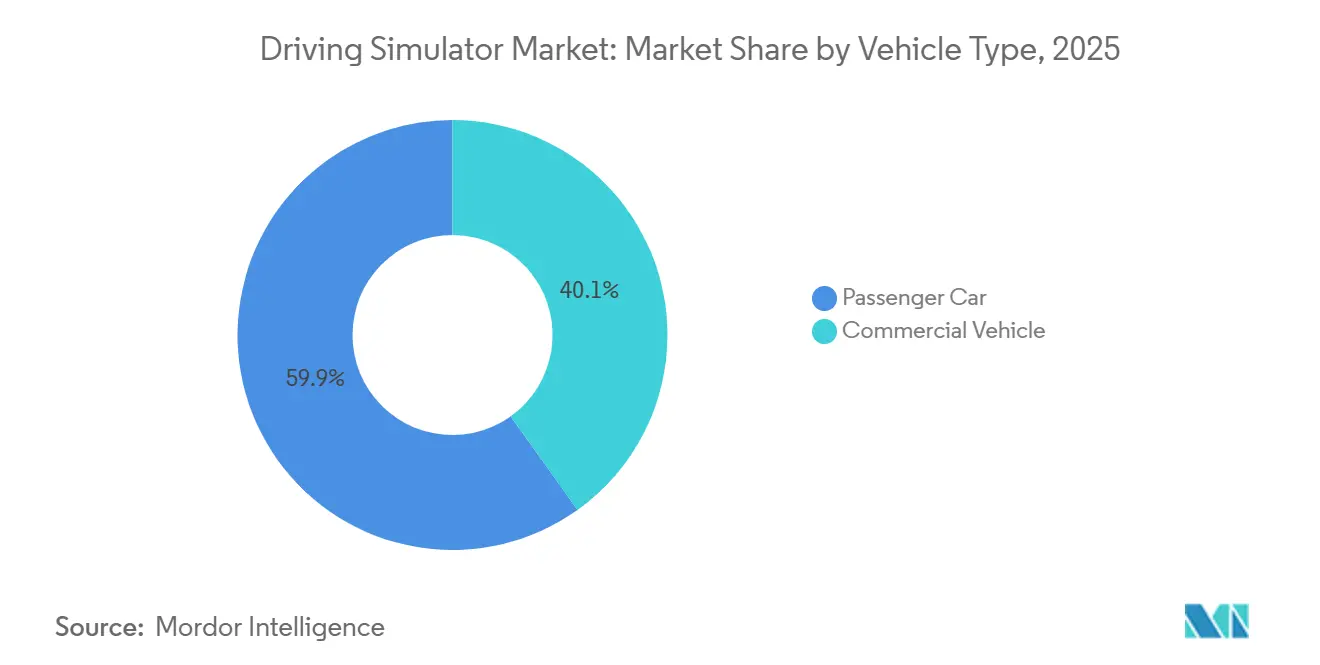

- By vehicle type, passenger cars held 59.88% of the driving simulator market share in 2025, while commercial vehicles are projected to post the fastest 7.14% CAGR through 2031.

- By application type, training accounted for 50.72% of the driving simulator market size in 2025; testing and research are forecast to expand at a 7.21% CAGR to 2031.

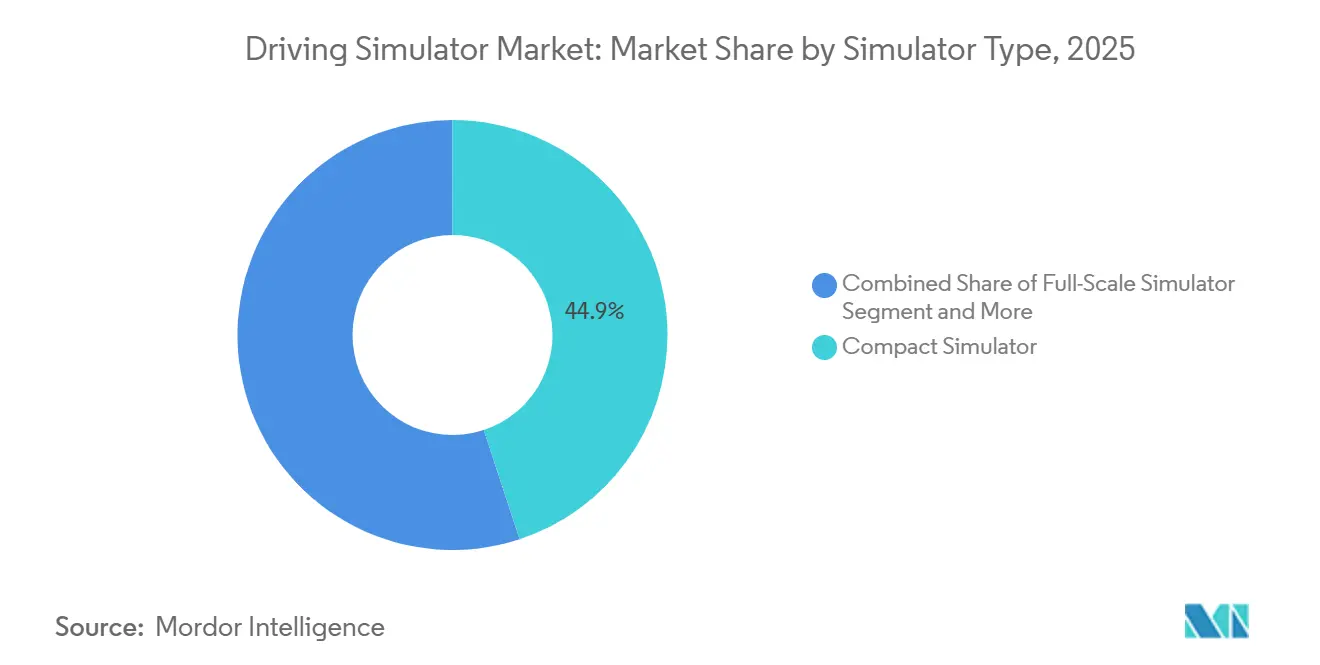

- By simulator type, compact units commanded 44.93% of the driving simulator market share in 2025, yet advanced systems will register the highest 7.29% CAGR over the forecast horizon.

- By end-user, driving schools controlled 30.66% of the driving simulator market size in 2025, while fleet operators are set to deliver a 7.23% CAGR through 2031.

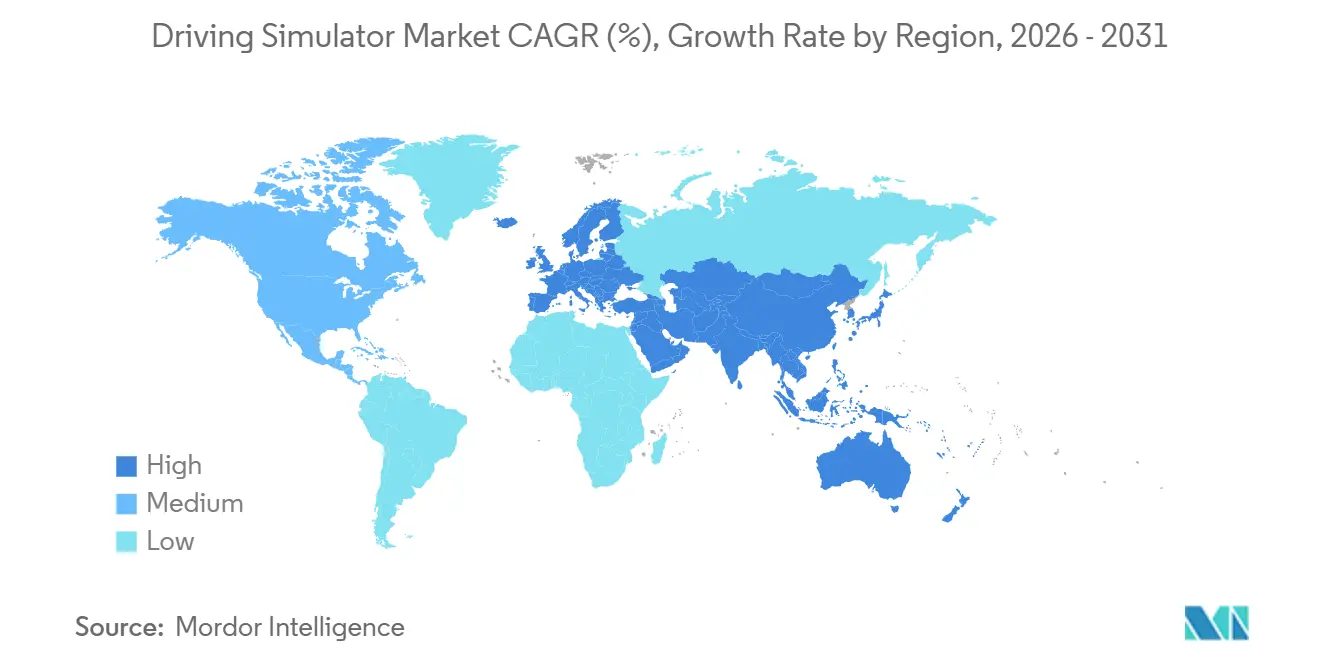

- By geography, Europe led with 36.22% of the driving simulator market share in 2025; Asia-Pacific is advancing at the fastest 7.17% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Driving Simulator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS/AV Validation | +1.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| E-Commerce Boom Raising | +1.5% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Road-Safety Regulations | +1.2% | Global, with early adoption in EU and North America | Long term (≥ 4 years) |

| Cloud "Simulator-As-A-Service" Lowering Capex | +1.1% | Global, faster adoption in emerging markets | Short term (≤ 2 years) |

| Insurance-Linked Premium Discounts | +0.9% | North America and Europe primarily | Medium term (2-4 years) |

| Digital-Twin Integration | +0.8% | Global, led by automotive manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ADAS/AV Validation Needs Surge

Tougher homologation rules now insist on billions of virtual test miles before autonomous functions reach public roads. Euro NCAP and NHTSA protocols released in 2024 pair track runs with simulation, turning high-fidelity rigs into compliance gates[1]“Vehicle Safety Research 2025,” National Highway Traffic Safety Administration, nhtsa.gov. The IEEE forecasts an autonomous-driving simulation niche of over a billion dollars by 2030, underscoring how carmakers rely on digital twins to probe edge cases unreachable on open roads[2]“Simulation Requirements for Autonomous Vehicles,” IEEE Standards Association, ieee.org . Platforms integrating real-world sensor logs with scalable scenario engines let engineers shorten iteration loops and trim prototype fleets. As software updates are delivered over the air, virtual regression testing becomes mandatory, driving steady demand for the driving simulator market. Vendors that wrap scenario libraries, physics engines, and data-fusion interfaces into one stack now win more RFQs from tier-1 suppliers.

E-Commerce Boom Raising Truck-Driver Training Demand

Online retail is pushing parcel volumes higher, straining freight capacity. Carriers such as UPS and Fremont Contract Carriers equip classrooms with motion-based simulators and report reductions in accidents alongside faster rookie onboarding. The Nebraska Trucking Association’s mobile units bring training to remote colleges, easing the rural talent gap. Repeatable hazard scenarios help fleets meet insurance audits and qualify recruits within weeks, boosting uptake. This commercial pull offsets slower growth in consumer driver-ed programs and keeps the driving simulator market momentum above one-tenth in the short term.

Road-Safety Regulations & Driver-Licensing Reforms

Authorities expand simulator-based assessments to address human-error crash rates. Transport Canada researches eye-tracking metrics in simulators to refine vision standards, while several European regulators pilot prescreening modules for older or high-risk drivers[3]“Human Factors in Connected Vehicle Research,” Transport Canada, tc.gc.ca. In the United States, the Federal Motor Carrier Safety Administration limits seat-time substitution yet allows simulators for theory components, creating a hybrid training norm. Such directives turn simulators from optional aids into core public-safety infrastructure. As ISO 26262 references virtual verification, demand from licensing centers, police academies, and medical driving-fit clinics rises, bolstering the driving simulator market.

Digital-Twin Integration For OTA Software Regression

Automakers patch vehicle functions weekly, creating continuous regression cycles. Simulators linked to real-time map updates and fleet telemetry let engineers replay rare incidents under controlled conditions. Vendors offering map-creation toolchains and sensor-behavior authoring gain sticky revenue from subscription updates. As more ECUs move to centralized zonal architectures, virtual E-HIL (electronic hardware-in-the-loop) becomes standard, driving incremental orders for advanced systems in the driving simulator market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex Of Full-Motion Systems | -1.4% | Global, particularly affecting emerging markets | Long term (≥ 4 years) |

| Motion-Sickness and Fidelity Limitations | -0.8% | Global, varies by demographic sensitivity | Medium term (2-4 years) |

| Shortage Of Scenario-Content Developers | -0.7% | Global, concentrated in specialized markets | Medium term (2-4 years) |

| Cyber-Security Risk | -0.6% | Global, heightened in regulated industries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex Of Full-Motion Systems

Eight-axis motion bases, panoramic domes, and purpose-built halls push acquisition costs beyond the reach of many vocational centers. Europe’s Stuttgart Driving Simulator illustrates the real-estate and maintenance footprint such rigs require. Financing hurdles prolong payback periods, especially where tuition fees are regulated. Emerging-market buyers often defer purchases or settle for static cockpits, tempering volume growth for premium hardware in the driving simulator market.

Motion-Sickness & Fidelity Limitations

Visual-vestibular mismatch can trigger nausea, curbing session length and user acceptance. Studies find that static systems induce discomfort in longitudinal events, while dynamic platforms struggle with vertical cue accuracy. Older trainees and novice gamers show higher dropout rates, prompting developers to tune frame rates, field-of-view settings, and cueing algorithms. Progress is steady, yet the perception risk keeps some regulators cautious about full substitution for on-road hours.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Accelerated Adoption

Passenger-car simulators still dominate with 59.88% of the driving simulator market share in 2025, serving both novice driver education and OEM R&D, but growth moderates as consumer licensing boards limit simulator substitution. The divergence in uptake illustrates how logistics digitization reshapes demand patterns for simulators. Commercial vehicles accounted for a smaller share of revenue in 2025, yet their 7.14% CAGR makes them the primary driver of future expansion in the driving simulator market. Fleet managers deploy simulators to cut per-driver training costs, keep rigs on the road, and satisfy stricter hours-of-service audits—Telematics integration further links in-cab behavior with classroom refreshers.

The commercial-vehicle push stimulates the customization of the peripheral services scenario library for hazmat routes, multi-language UI overlays, and remote instructor stations. Vendors leveraging modular cockpits and cloud rendering are penetrating small- and mid-sized transport operators previously priced out. Meanwhile, passenger-car programs focus on human-machine interface testing for next-gen infotainment, a niche that commands higher margins but fewer seats. Suppliers that craft dual-purpose architectures, swappable dashboards, and adaptable software stacks retain cross-segment flexibility in the driving simulator market.

By Application: Testing Surge Outpaces Training Growth

Training held 50.72% of the driving simulator market size in 2025 due to entrenched driver-ed curricula and corporate compliance needs. Yet the 7.21% CAGR logged by testing and research signals a structural pivot. Automakers seeking to shorten release cycles channel budgets toward software-dominated validation, where virtual miles cost less than track miles. Growth also comes from regulatory labs conducting crash-avoidance verification under controlled, repeatable conditions.

Training demand remains resilient, particularly in regions where road congestion and fuel prices make real-world lessons inefficient. Virtual-reality headsets and adaptive AI tutors personalize modules, boosting learner retention. Still, budget-sensitive schools adopt a wait-and-see stance on replacing entire fleets of conventional cars. Providers hedge by offering mixed-use licenses that toggle between test automation scripts and classroom content, increasing seat utilization and diversifying revenue in the driving simulator market.

By Simulator Type: Advanced Systems Capture Premium Growth

Compact rigs led the driving simulator market with 44.93% in 2025, but advanced simulators featuring six-degree-of-freedom motion, ultra-high-resolution wrap-around visuals, and low-latency force feedback will post a 7.29% CAGR to 2031. The rise is linked directly to autonomous-vehicle edge-case validation that demands sub-20-millisecond loop times and centimeter-level road-surface modeling. These features translate into higher selling prices and service contracts, lifting overall value even if unit counts remain modest.

Full-scale platforms occupy a middle tier, targeting driver-licensing agencies that need immersive realism without skyscraper-sized structures. Vendors pitch modular upgrades, add-on motion actuators, or 4K projectors to keep installed bases fresh. Compact simulators still win on portability and price, especially for outreach programs and rural schools, but risk commoditization as white-label kits flood the market. Continuous content updates, rather than hardware specs, emerge as the key differentiator across all simulator types in the driving simulator market.

By End-User: Fleet Operators Emerge as Growth Leaders

Driving schools accounted for 30.66% of the driving simulator market in 2025, reflecting legacy dominance in learner preparation. Their growth plateaus, however, as demographic shifts shrink the pool of teen drivers in several mature economies. Fleet operators, projected at a 7.23% CAGR, seize momentum by embedding simulators into safety, recruitment, and insurance workflows. Subscription models with per-driver analytics appeal to logistics companies chasing thin margins.

Automotive OEMs and tier-1 suppliers represent a high-value but narrower slice, demanding top-end specs and stringent IP protections. University labs and public-sector research bodies play complementary roles, often funded through grants to study human factors in connected-vehicle ecosystems. The diversified buyer mix cushions the driving simulator industry against cyclical swings in any single end-user group.

Geography Analysis

Europe maintained a 36.22% share of the driving simulator market in 2025, driven by its dense network of test circuits, harmonized safety rules, and R&D tax incentives. Carmakers in Germany, France, and Sweden run integrated simulation pipelines that feed regulatory dossiers, ensuring a steady hardware refresh cycle. National transport ministries pilot simulator-based licensing updates, keeping public procurement programs alive even as private budgets fluctuate.

Asia-Pacific, advancing at a 7.17% CAGR, adds the most new seats. China funnels smart-city budgets into autonomous shuttle pilots, while India scales truck-driver academies to plug chronic labor gaps. Cloud-rendered solutions bypass infrastructure bottlenecks, letting institutes deploy laptop-controlled cockpits in temporary classrooms. Japan’s well-established automotive sector focuses on scenario libraries that represent complex urban intersections, reinforcing upstream software demand in the driving simulator market.

North America benefits from structured federal guidelines covering commercial driver qualifications and an early culture of simulator adoption in aviation and defense. Large freight haulers invest in networked fleets of rigs across regional hubs, leveraging centralized content pushes. Latin America and the Middle East remain smaller consumers, yet oil-and-gas convoy operators in the Gulf show rising interest, signaling wider geographic penetration ahead.

Competitive Landscape

Major players in the driving simulator market wield proprietary physics engines, complemented by open-API toolkits, enabling clients to integrate personalized dashboards. In contrast, emerging entrants are gravitating towards browser-based rendering, targeting budget-conscious consumers. Companies boasting ISO 26262 or DO-178C certifications bolster their market position by adhering to stringent safety-centric procurement standards.

Hardware vendors converge with software studios through M&A; recent deals channel R&D toward digital twin asset creation to feed autonomous vehicle pipelines. Strategic partnerships emerge between simulator houses and lidar or radar sensor makers, integrating raw point cloud data for validation tasks. Subscription revenue softens the lumpy nature of capital-equipment sales, prompting legacy OEMs to launch cloud divisions.

Automakers rolling in-house simulators to protect IP and slash vendor dependence also creates competitive tension. Providers respond by offering white-label scenario marketplaces and on-premises render clusters, both of which are managed under service-level agreements. Ecosystem depth, ranging from content authoring to analytics and cyber-security hardening, now defines long-term positioning in the driving simulator industry.

Driving Simulator Industry Leaders

AVSimulation

VI-grade Gmbh

IPG Automotive GmbH

AB Dynamics PLC

FAAC Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Bridgestone commenced full operations of its driver-in-the-loop simulator in Italy. This advanced simulator is designed to enhance vehicle testing and development by providing a controlled environment that simulates real-world driving conditions. The initiative reflects Bridgestone's commitment to leveraging cutting-edge technology to improve performance and safety in the automotive sector.

- May 2024: IPG Automotive expanded its case-study library to cover ADAS and hardware-in-the-loop deployments, underscoring demand for integrated test environments.

Global Driving Simulator Market Report Scope

Driving simulators are used in driver education classes offered by educational institutions and by private firms such as driving schools. In the automotive sector, they are also used to develop and assess new cars and advanced driver assistance systems. They are also used in human factors and medical research to monitor driver behavior, performance, and attention.

The driving simulator market is segmented by vehicle type, Application type, simulator type, and Geography.

Based on the vehicle type, the market is segmented into passenger cars and commercial vehicles. Based on application type, the market is segmented into training, testing, and research. Based on the simulator type, the market is segmented into compact, full-scale, and advanced simulators. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, and the rest of the world.

For each segment, the market sizing and forecast have been done based on the value (USD).

| Passenger Car |

| Commercial Vehicle |

| Training |

| Testing & Research |

| Compact Simulator |

| Full-Scale Simulator |

| Advanced Simulator |

| Driving Schools & Training Centers |

| Automotive OEMs |

| Fleet Operators & Logistics |

| Academic & Research Institutions |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Car | |

| Commercial Vehicle | ||

| By Application | Training | |

| Testing & Research | ||

| By Simulator Type | Compact Simulator | |

| Full-Scale Simulator | ||

| Advanced Simulator | ||

| By End-User | Driving Schools & Training Centers | |

| Automotive OEMs | ||

| Fleet Operators & Logistics | ||

| Academic & Research Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the driving simulator market be by 2031?

The driving simulator market size is projected to reach USD 1.24 billion by 2031, growing at a 7.12% CAGR through the forecast period.

Which vehicle category is expanding fastest in simulator use?

Commercial vehicles are forecast to post a 7.14% CAGR, outpacing passenger applications as fleets scale e-commerce logistics programs.

What region is set to add the most new simulator seats?

Asia-Pacific is the fastest-growing territory at a 7.17% CAGR owing to rapid autonomous-vehicle projects and expanding truck fleets.

Why are insurers interested in simulator-based training?

Underwriters see proof that certified programs reduce crash claims, so they offer premium discounts that improve fleet ROI.

What differentiates advanced simulators from compact models?

Advanced systems provide six-degree-of-freedom motion, ultra-high-resolution visuals, and real-time data fusion, enabling edge-case validation for autonomous features.

What is the biggest barrier for small driving schools?

High capital expenditure for full-motion hardware and ongoing maintenance makes top-tier systems difficult for smaller institutions to afford.

Page last updated on: