Automotive Tow Bars Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

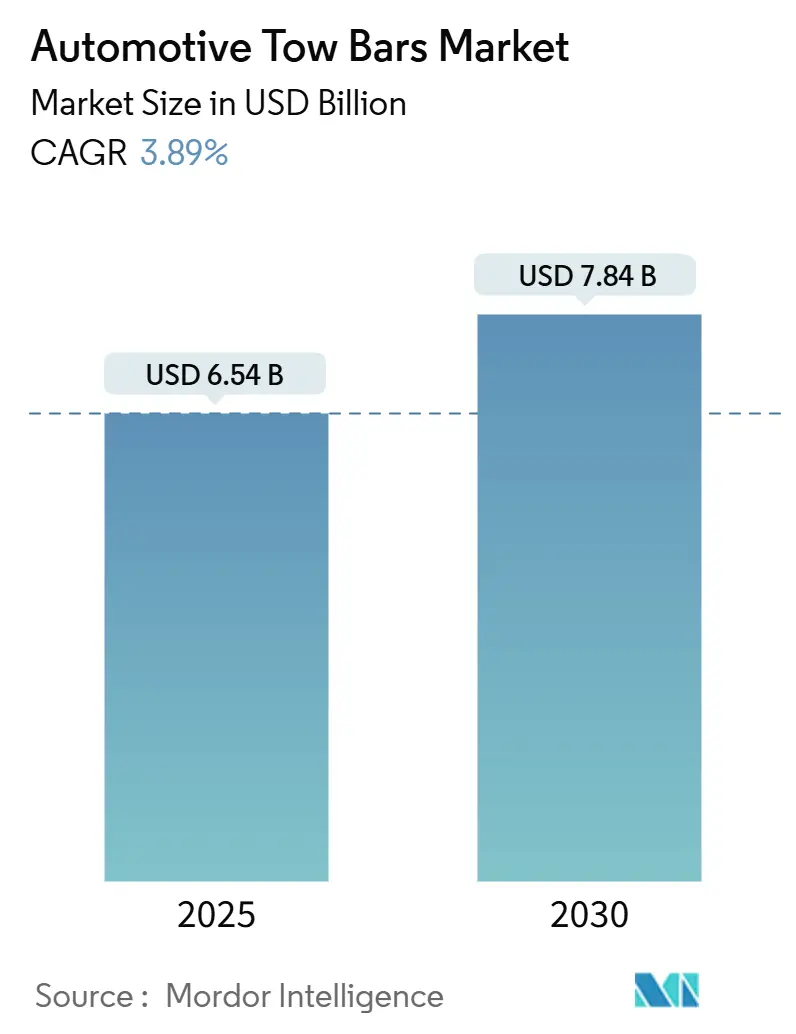

| Market Size (2025) | USD 6.54 Billion |

| Market Size (2030) | USD 7.84 Billion |

| Growth Rate (2025 - 2030) | 3.89% CAGR |

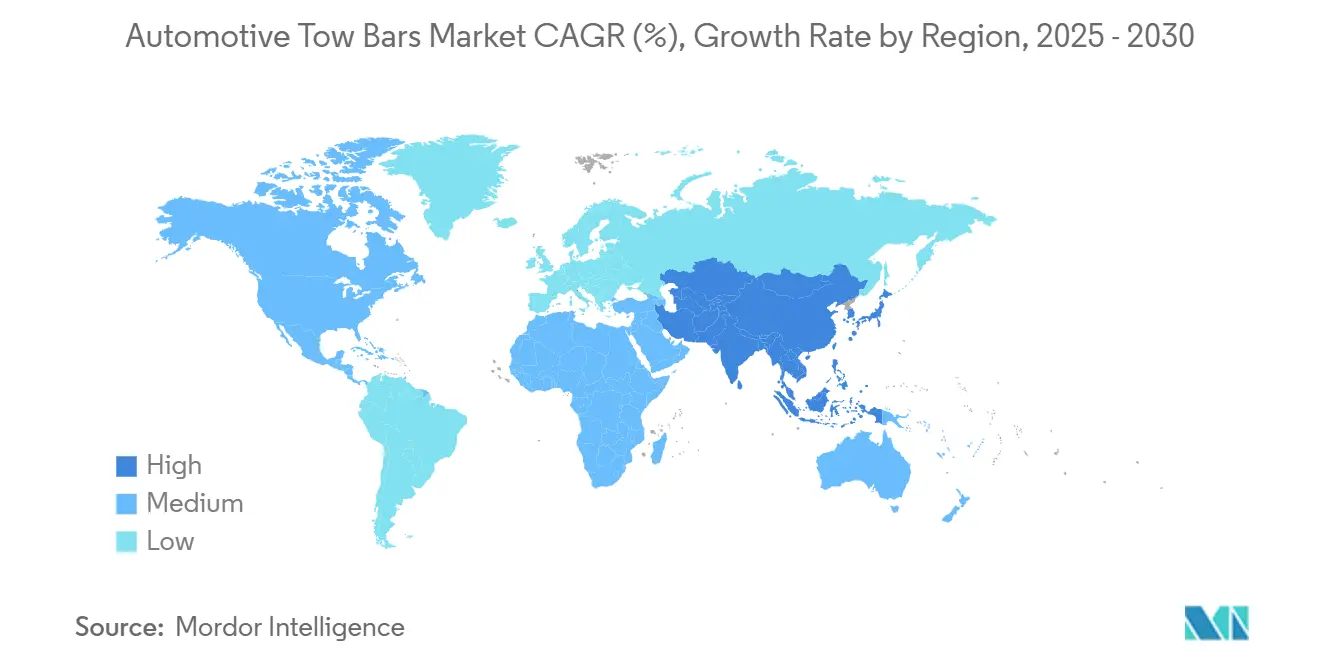

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Tow Bars Market Analysis by Mordor Intelligence

The automotive tow bars market size stands at USD 6.54 billion in 2025 and is forecast to reach USD 7.84 billion by 2030, advancing at a 3.89% CAGR. This moderate expansion reflects a sector moving from early growth into disciplined product innovation as vehicle architectures, safety mandates, and electrification each raise the technical bar for towing hardware. Recreational vehicle tourism, growing SUV penetration, and tightening regional certification rules reinforce demand, while rising electric-vehicle (EV) sales push manufacturers to engineer lighter, aerodynamically efficient modules that protect driving range.

Key Report Takeaways

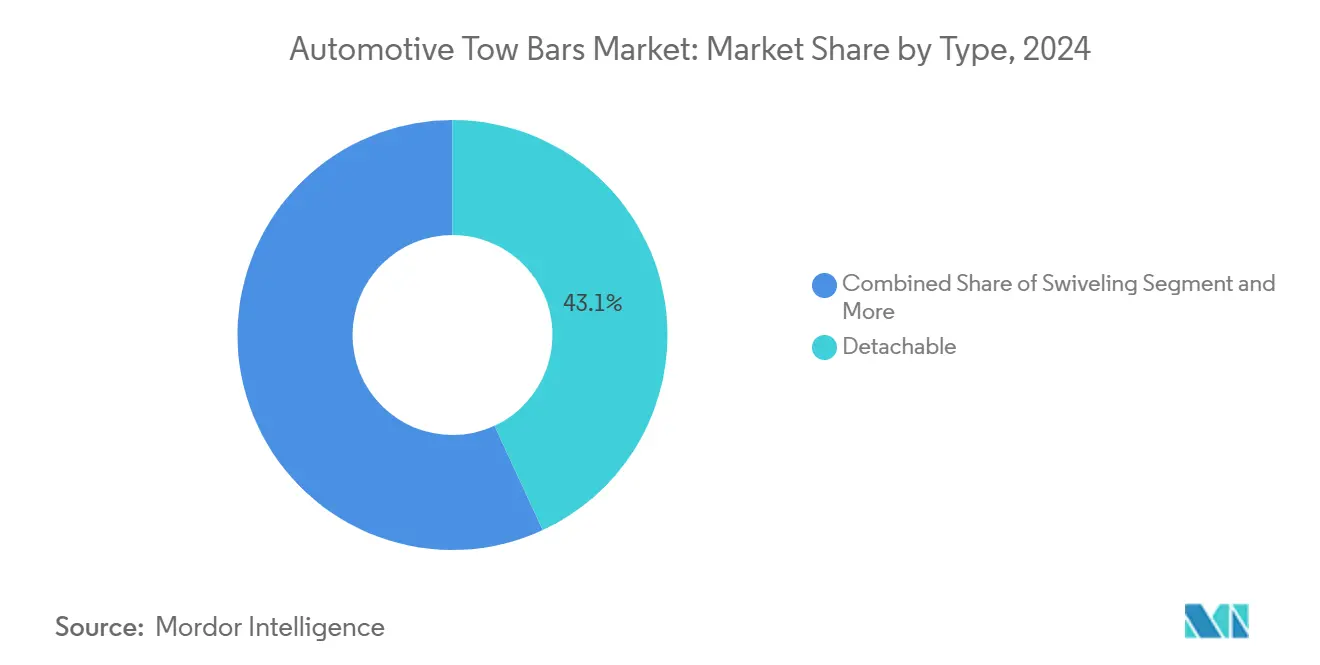

- By type, detachable systems led with 43.12% of automotive tow bars market share in 2024; Swiveling post the fastest 10.21% CAGR through 2030.

- By vehicle type, passenger vehicles accounted for 70.05% of the automotive tow bars market size in 2024, while electric passenger applications show the highest 8.39% CAGR to 2030.

- By sales channel, OEM integration captured 55.08% share of the automotive tow bars market in 2024 and is growing at a 6.02% CAGR to 2030.

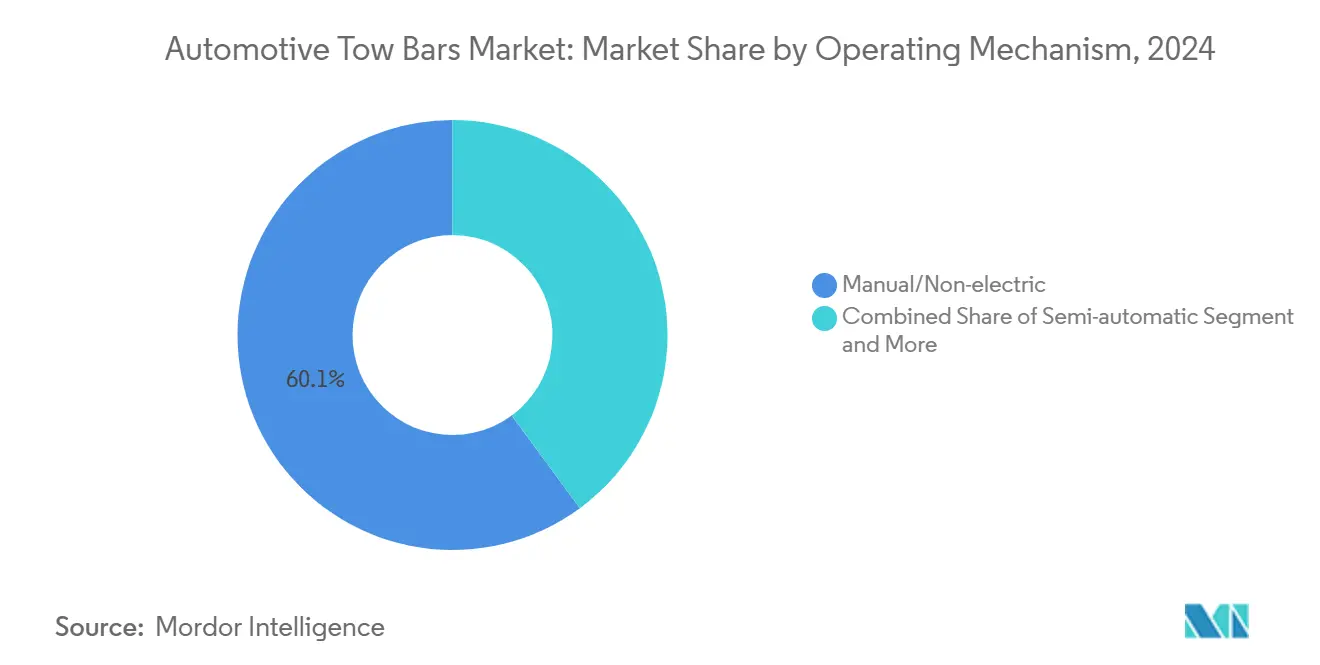

- By operating mechanism, manual/non-electric systems retained 60.14% share in 2024, yet fully-electric retractables expand at a 10.18% CAGR through 2030.

- By geography, North America held 36.12% revenue share in 2024; Asia-Pacific records the quickest 7.04% CAGR through 2030.

Global Automotive Tow Bars Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global SUV and Pickup Sales Growth | +0.9% | North America and Asia-Pacific Core, Global Spill-over | Short Term (≤ 2 Years) |

| Recreational Vehicle Ownership and Caravan Tourism | +0.8% | North America, Europe, Spill-over to Asia-Pacific | Medium Term (2-4 Years) |

| OEM Adoption of Lightweight, Crash-Tested EV Modules | +0.7% | Europe and North America Lead, Global Follow-on | Medium Term (2-4 Years) |

| Stricter Regulations Mandating Certified Solutions | +0.5% | Europe and North America, Expanding to Asia-Pacific | Long Term (≥ 4 Years) |

| Peer-to-Peer Trailer-Sharing Platform Expansion | +0.4% | North America Core, Emerging in Europe and Asia-Pacific | Medium Term (2-4 Years) |

| Luxury-Segment Shift to Fully-Electric Retractables | +0.3% | North America and Europe Luxury Clusters | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Growth in Recreational Vehicle (RV) Ownership and Caravan Tourism

The recreational vehicle sector's robust expansion creates cascading demand for sophisticated towing solutions as manufacturers pivot toward integrated mobility ecosystems. This surge coincides with demographic shifts as millennials enter peak earning years and prioritize experiential travel over traditional hospitality, creating sustained demand for vehicle-trailer combinations that require certified towing hardware. The trend extends beyond leisure applications as commercial fleet operators adopt trailer-based logistics solutions to optimize last-mile delivery costs, particularly in e-commerce fulfillment networks where modular capacity adjustments prove economically advantageous. Mobile towbar fitting services have emerged to serve this expanding customer base, with companies like Adelaide On-Site and Towbar Express UK reporting 40% year-over-year growth in 2024 as consumers seek convenient installation solutions.

Surge in Global SUV and Pickup Sales Supporting Higher Factory-Fitted Towing Capability

SUV and pickup truck proliferation fundamentally alters automotive tow bars market dynamics as these platforms arrive factory-equipped with enhanced towing provisions that drive aftermarket upgrade demand. Global manufacturers like Ford, GM, and Toyota are integrating advanced towing packages that include smart trailer backup assist and load monitoring systems. The strategic shift toward body-on-frame construction in premium SUVs enables higher towing capacities that previously required commercial vehicle platforms, expanding the addressable market for heavy-duty towbar systems rated above 3,500 kg. Chinese dual-cab utilities entering Australian markets exemplify this trend, arriving with 3,500 kg towing capacity as standard equipment that necessitates compatible aftermarket accessories. Fleet electrification adds complexity as electric SUVs like BMW iX (2,500 kg capacity) and Rivian R1S (7,700 lbs capacity) require specialized electrical integration for trailer brake controllers and regenerative braking coordination. This convergence of higher towing capacities and electrification drives demand for intelligent towbar systems that communicate with vehicle control modules to optimize energy management during towing operations.

Stricter Regional Regulations Mandating Certified Towing Solutions

Regulatory tightening across major automotive markets transforms towbar compliance requirements from voluntary guidelines to mandatory certification pathways that reshape competitive dynamics. The European Union's ECE R55 regulation superseded EC94/20 in 2012, introducing secondary coupling tests and administrative requirements that elevated barriers for non-certified manufacturers[1]"Approval & Traceability," Tow Trust, tow-trust.co.uk.. Australia's Vehicle Standards Bulletin 1 (Revision 6) mandates specific static test loads—longitudinal tension/compression at 1.5 × ATM × 9.81 N and transverse thrust at 0.5 × ATM × 9.81 N—creating technical hurdles for aftermarket suppliers lacking testing facilities[2]"Vehicle Standards Bulletin 1 (Revision 6) – Trailers with an aggregate trailer mass of 4.5 tonnes or less," Department of Infrastructure, Transport, Regional Development, Communications and the Arts, www.infrastructure.gov.au.. New Zealand's LVVTA framework explicitly exempts towbars from Low Volume Vehicle certification, provided structural integrity remains uncompromised, creating competitive advantages for manufacturers offering bolt-on solutions that avoid welding requirements. Transport Canada's National Safety Mark authorization process requires comprehensive documentation, including technical drawings, test reports, and component specifications, effectively consolidating market share among established players with regulatory expertise. These evolving standards create a two-tier market structure where certified manufacturers command premium pricing while non-compliant products face market exclusion.

OEM Integration of Lightweight, Crash-Tested Towbar Modules in New EV Platforms

Electric vehicle architecture integration presents both opportunity and complexity as automakers redesign chassis structures to accommodate battery packs while maintaining towing functionality. BMW's integration of towbar provisions in iX and i5 platforms demonstrates how manufacturers balance aerodynamic efficiency with utility requirements, achieving towing capacities of 2,500 kg and 1,500-2,000 kg, respectively, through aluminum construction and optimized mounting geometries. Tesla's approach with Model X (5,000 lbs capacity) showcases software-hardware integration where towing mode automatically adjusts regenerative braking, suspension settings, and range calculations to compensate for trailer loads. The challenge intensifies as battery placement constrains traditional mounting points, forcing towbar manufacturers to develop vehicle-specific solutions that distribute loads across reinforced chassis members. Crash testing requirements add complexity as towbar integration must not compromise occupant protection or structural integrity during impact scenarios, driving collaboration between OEMs and specialized suppliers. This technical evolution favors manufacturers with engineering capabilities to develop integrated solutions rather than universal aftermarket products, potentially consolidating market share among technology-forward companies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Professional Installation and Homologation Costs | −0.6% | Europe and Other Developed Markets, Global | Short Term (≤ 2 Years) |

| Battery-Range Penalty of Towed Loads Reducing EV Owner Uptake | −0.5% | Europe and North America Lead, Global EV Markets | Medium Term (2-4 Years) |

| Battery-Range Penalty When EVs Tow | −0.4% | Europe and North America Lead, Global EV Markets | Medium Term (2-4 Years) |

| Proliferation of Counterfeit Low-Grade Towbars in Emerging Markets Eroding Consumer Trust | −0.3% | Asia-Pacific and Latin America, Emerging Markets | Medium Term (2-4 Years) |

| Source: Mordor Intelligence | |||

High Professional-Installation and Homologation Costs

Installation and certification expenses create significant market friction as professional fitting costs range from USD 300 to 1,000, while homologation processes add regulatory complexity that deters smaller manufacturers. Australian market data indicates total towbar costs spanning USD 300 to 2,000, including equipment and installation, with premium electric retractable systems commanding higher margins but requiring specialized technician training. California's Air Resources Board certification fees compound these challenges, with aftermarket parts applications costing USD 2,000 for standard businesses and USD 500 for small enterprises, creating barriers for market entry. The technical complexity of modern vehicle integration—particularly with ADAS systems and electronic stability control—necessitates dealer-level diagnostic equipment for proper calibration, limiting DIY installation options. Mobile fitting services partially address cost concerns but face scalability constraints in rural markets where travel distances inflate service charges. This cost structure bifurcates demand between price-sensitive consumers who defer purchases and premium buyers willing to pay for convenience and warranty coverage.

Battery-Range Penalty of Towed Loads Reducing EV Owner Uptake

Electric vehicle towing applications face fundamental physics constraints as trailer loads can reduce driving range by up to 50%, creating adoption barriers that limit market expansion in the growing EV segment. Comprehensive towing guides indicate range penalties vary significantly by vehicle design, with aerodynamic trailers causing less impact than high-profile cargo loads, yet even optimized configurations typically reduce range by 25-30% under highway conditions. This limitation proves particularly acute for long-distance recreational towing, where charging infrastructure gaps compound range anxiety, effectively limiting EV towing to short-haul applications or routes with dense charging networks. Retrofit towbar costs for EVs range from EUR 450 to 1,150, representing a higher investment relative to ICE vehicles due to specialized electrical integration requirements for regenerative braking coordination and battery thermal management. The market response includes development of smart towing systems that optimize energy consumption through predictive algorithms and trailer-integrated solar panels, yet these solutions remain nascent and expensive. Consumer behavior studies suggest EV owners prioritize efficiency over utility, creating preference shifts toward lightweight trailers and reduced towing frequency that constrain overall market growth in the electrified segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Swiveling Drive Premium Transformation

Detachable towbar systems command 43.12% market share in 2024, reflecting consumer preference for aesthetic integration and theft deterrence capabilities that traditional fixed systems cannot provide. The Swiveling are poised to grow at 10.21% CAGR through 2030, driven by luxury vehicle integration and technological advancement in motor control systems that enable one-touch operation. Fixed towbars maintain cost advantages in commercial applications where durability outweighs convenience, while detachable variants serve urban consumers requiring occasional towing without permanent vehicle modification. Swiveling designs address niche applications in recreational vehicle markets where maneuverability constraints demand articulated coupling solutions.

General Motors' patent filing for drone-assisted towing systems (US 12,312,107 B2) exemplifies the technological trajectory toward automated coupling and monitoring capabilities that transform traditional towbar functionality. The innovation pipeline includes smart materials integration and IoT connectivity that enable predictive maintenance alerts and load monitoring through smartphone applications. Roadmaster's Nighthawk introduction as the world's first illuminated towbar with embedded LED lights demonstrates how manufacturers differentiate through safety-focused innovation, commanding premium pricing in the 8,000 lb capacity segment. This technological evolution favors manufacturers with R&D capabilities to develop integrated electronics while challenging traditional mechanical specialists to adapt or cede market share.

By Vehicle Type: Electrification Reshapes Passenger Dominance

Passenger vehicles maintain 70.05% market share in 2024, yet electric passenger vehicle applications grow at 8.39% CAGR as manufacturers address range optimization challenges through aerodynamic towbar designs and intelligent power management systems. Commercial vehicle adoption remains constrained by regulatory complexity and higher certification costs, though fleet electrification initiatives create opportunities for specialized heavy-duty towing solutions. The passenger vehicle dominance reflects broader automotive trends toward SUV and crossover platforms that arrive with enhanced towing provisions as standard equipment.

Electric vehicle integration presents both opportunity and challenge as manufacturers like BMW demonstrate with iX (2,500 kg capacity) and i5 (1,500 to 2,000 kg capacity) platforms that balance aerodynamic efficiency with utility requirements through aluminum construction and optimized mounting geometries. Tesla's Model X approach showcases software-hardware integration where towing mode automatically adjusts vehicle systems to compensate for trailer loads, creating competitive advantages for OEMs with advanced control algorithms. The commercial vehicle segment faces transformation as fleet operators evaluate total cost of ownership implications for electric trucks with towing capability, particularly in last-mile delivery applications where trailer modularity optimizes capacity utilization. Regulatory frameworks like Transport Canada's National Safety Mark requirements create barriers for aftermarket suppliers while favoring OEM-integrated solutions that meet certification standards during vehicle homologation.

By Sales Channel: OEM Integration Accelerates

OEM channels capture 55.08% market share in 2024 with sustained 6.02% growth, reflecting automakers' strategic shift toward factory-fitted solutions that bypass aftermarket installation complexities and liability concerns. This trend accelerates as vehicle architectures become more integrated and electronic systems require specialized calibration that exceeds typical aftermarket installer capabilities. Aftermarket channels maintain relevance in retrofit applications and specialized towing requirements that OEM offerings cannot address, particularly in commercial vehicle modifications and recreational vehicle accessories.

The OEM integration trend reflects broader automotive industry consolidation as manufacturers seek to control customer experience and capture aftermarket revenue streams traditionally dominated by independent suppliers. Genuine Parts Company's automotive segment performance—USD 3.665 billion sales in Q1 2025 with 2.5% year-over-year growth—demonstrates aftermarket channel resilience despite OEM encroachment, supported by extensive distribution networks spanning 10,700 locations globally. The channel dynamics create opportunities for manufacturers capable of serving both OEM integration requirements and aftermarket retrofit demand, while challenging single-channel specialists to expand their go-to-market strategies. Mobile installation services emerge as a hybrid model that combines aftermarket flexibility with professional installation quality, addressing consumer convenience preferences while maintaining competitive pricing relative to dealer services.

By Operating Mechanism: Automation Commands Premium Pricing

Manual/non-electric systems retain 60.14% market share in 2024, demonstrating cost-conscious consumer preferences and commercial vehicle requirements for mechanical reliability over electronic convenience. Fully-electric retractable mechanisms advance at 10.18% CAGR, concentrated in luxury vehicle applications where convenience and aesthetic integration justify premium pricing. Semi-automatic variants occupy a middle ground, offering enhanced functionality without the complexity and cost of fully-automated systems.

The operating mechanism segmentation reflects broader automotive trends toward electrification and automation, with manufacturers like ORIS developing E3 electric retractable systems that integrate with vehicle control modules for seamless operation. Pebble Flow's Magic Hitch system demonstrates the technological frontier with automated hitching capabilities controlled via smartphone applications, representing the convergence of towbar functionality with connected vehicle ecosystems. The market bifurcation between manual and electric systems creates distinct value propositions—mechanical reliability and cost efficiency versus convenience and integration—that serve different customer segments and use cases. Dexter Group's Tow Assist system exemplifies the evolution toward intelligent towing solutions that incorporate ABS, sway mitigation, and odometer functionality, transforming towbars from passive hardware into active safety systems. This technological progression favors manufacturers with electronics capabilities while creating opportunities for software-focused companies to enter the market through partnership strategies.

Manual/non-electric systems maintain 60.14% market share in 2024, reflecting cost sensitivity and commercial vehicle preferences for mechanical reliability over electronic complexity. Semi-automatic variants bridge the gap between cost and convenience, offering enhanced functionality without full automation complexity. Fully-electric retractable towbars achieve 10.18% CAGR growth through 2030, led by luxury vehicle integration and consumer preference for convenience features that eliminate manual handling requirements.

Ford's Pro Trailer Backup Assist and Smart Trailer Tow Connector integration exemplifies how manufacturers embed towbar functionality within broader vehicle control systems, creating competitive moats through proprietary software algorithms. GMC's Smart Trailer Towing system with myGMC app integration demonstrates the evolution toward connected towing solutions that provide tire monitoring, maintenance reminders, and load optimization recommendations. The technological trajectory toward IoT connectivity and predictive analytics transforms towbars from passive hardware into active vehicle systems that enhance safety and user experience. This evolution favors manufacturers with software development capabilities while creating partnership opportunities between traditional hardware suppliers and technology companies seeking automotive market entry.

Geography Analysis

North America leads with 36.12% market share in 2024, driven by recreational vehicle culture, pickup truck prevalence, and established trailer-sharing economies that create sustained demand for both OEM and aftermarket towing solutions. The region's regulatory framework, anchored by NHTSA standards and state-level requirements, provides stability for manufacturers while creating barriers for non-compliant products. Canada's National Safety Mark authorization process exemplifies the regulatory rigor that consolidates market share among established players with certification expertise, while cross-border trade dynamics influence supply chain strategies for manufacturers serving both US and Canadian markets.

Asia-Pacific emerges as the fastest-growing region with 7.04% CAGR through 2030, propelled by expanding SUV adoption, infrastructure development, and emerging peer-to-peer trailer sharing platforms that mirror North American market evolution. China's automotive standards development and dual-cab utility exports to Australia demonstrate the region's growing influence in global towbar design requirements, while India's rising consumer demand creates opportunities for cost-effective towing solutions. The region's growth trajectory reflects broader economic development patterns where increased disposable income drives recreational vehicle adoption and commercial trailer utilization for logistics optimization.

Europe maintains steady growth despite mature market characteristics, supported by stringent ECE R55 regulations that favor certified manufacturers and create barriers for counterfeit products. The region's emphasis on environmental regulations drives innovation in lightweight materials and aerodynamic designs that minimize fuel consumption penalties during towing operations. Brexit implications continue to influence supply chain strategies as manufacturers navigate changing trade relationships and regulatory frameworks between UK and EU markets. The European market's sophistication in electric vehicle adoption creates demand for specialized EV-compatible towing solutions that address range optimization and battery thermal management challenges, positioning the region as a technology development hub for next-generation towing systems.

Competitive Landscape

The automotive tow bars market exhibits moderate fragmentation with established players like Horizon Global Corporation, Bosal International, and Westfalia-Automotive competing against specialized manufacturers focused on electric retractable systems and EV-compatible designs. Market concentration trends toward consolidation as regulatory compliance costs and R&D requirements favor larger manufacturers with resources to navigate certification processes and develop integrated solutions for modern vehicle platforms.

White-space opportunities emerge in smart towing systems that integrate IoT connectivity, predictive maintenance, and autonomous vehicle compatibility, creating entry points for technology-focused companies willing to partner with traditional hardware manufacturers. Strategic patterns reveal bifurcation between cost-focused suppliers serving commercial and aftermarket segments versus premium manufacturers targeting OEM integration and luxury vehicle applications.

The competitive intensity escalates as counterfeit products from China capture market share in emerging economies, with the European Union Intellectual Property Office reporting 94% of seized counterfeit automotive parts originating from Chinese manufacturers in 2024. Technology deployment becomes a key differentiator as companies like General Motors file patents for drone-assisted towing systems (US 12,312,107 B2) while traditional manufacturers invest in electric retractable mechanisms and smart coupling solutions. ECE R55 regulatory compliance creates barriers for smaller manufacturers while favoring established players with certification expertise and testing capabilities, potentially accelerating market consolidation through acquisition of non-compliant suppliers seeking regulatory pathway access.

Automotive Tow Bars Industry Leaders

-

Horizon Global Corporation

-

Bosal International N.V.

-

Brink Group B.V.

-

CURT Manufacturing LLC

-

Westfalia-Automotive GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Lippert Components acquired RVibrake, a manufacturer of flat tow brake systems, expanding its portfolio of RV-related towing solutions and strengthening market position in the recreational vehicle segment. The acquisition provides Lippert with specialized braking technology for flat-towed vehicles, addressing a niche but growing market segment driven by motorhome tourism expansion.

- November 2024: Thule Group completed the acquisition of Quad Lock for SEK 3.6 billion (USD 337 million), expanding its vehicle accessory offerings and direct-to-consumer capabilities. While not directly towbar-related, this acquisition demonstrates consolidation trends in the broader automotive accessories market and Thule's strategy to diversify beyond traditional roof-mounted solutions.

Global Automotive Tow Bars Market Report Scope

| Fixed |

| Detachable |

| Swiveling |

| Others |

| Passenger Vehicle |

| Commercial Vehicle |

| OEM |

| Aftermarket |

| Manual/Non-electric |

| Semi-automatic |

| Fully-electric Retractable |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Fixed | |

| Detachable | ||

| Swiveling | ||

| Others | ||

| By Vehicle Type | Passenger Vehicle | |

| Commercial Vehicle | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Operating Mechanism | Manual/Non-electric | |

| Semi-automatic | ||

| Fully-electric Retractable | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Which vehicle category dominates tow-bar demand?

Passenger cars, especially SUVs and crossovers, account for 70.05% of 2024 revenue, though electric-passenger applications are the fastest rising.

Why are fully-electric retractable hitches gaining popularity?

Luxury SUVs favor them for seamless aesthetics, one-touch convenience, and integration with driver-assist electronics, driving a 10.21% CAGR through 2030.

What limits tow-bar adoption on electric vehicles?

Towing can cut EV range by up to 30–50%, and installation requires specialized regenerative-brake-compatible controls, raising cost and complexity.

Which region is growing the fastest?

Asia-Pacific leads with a 7.04% CAGR thanks to rising SUV ownership, trailer-sharing apps, and infrastructure build-out.

How are regulations shaping the market?

Standards such as Europe’s ECE R55 and Canada’s National Safety Mark demand certified products, elevating barriers to entry but improving safety and compliance.

Page last updated on: