Automotive Piston Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

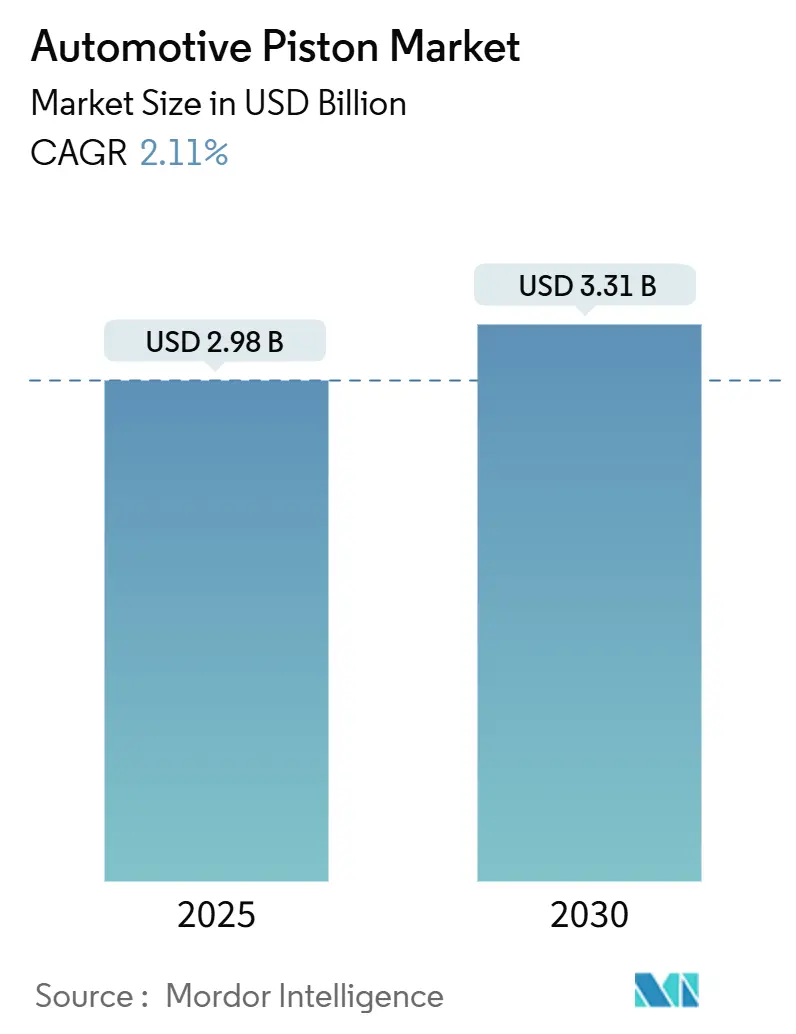

| Market Size (2025) | USD 2.98 Billion |

| Market Size (2030) | USD 3.31 Billion |

| Growth Rate (2025 - 2030) | 2.11% CAGR |

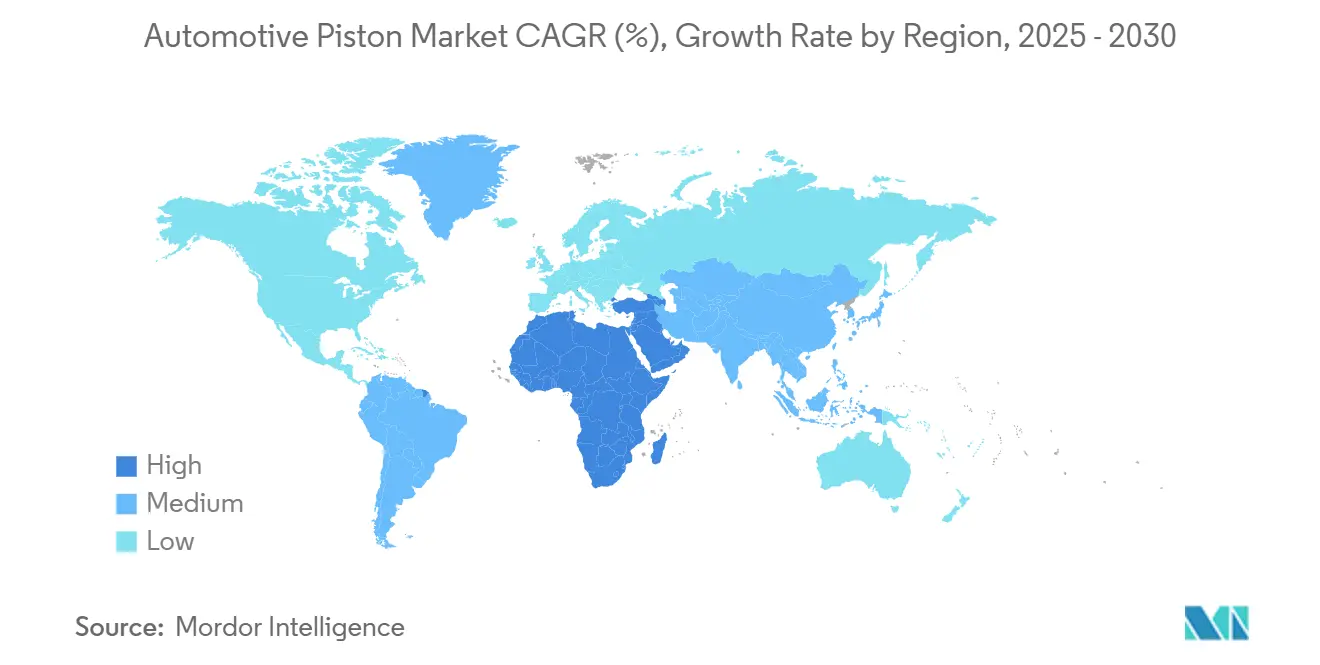

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

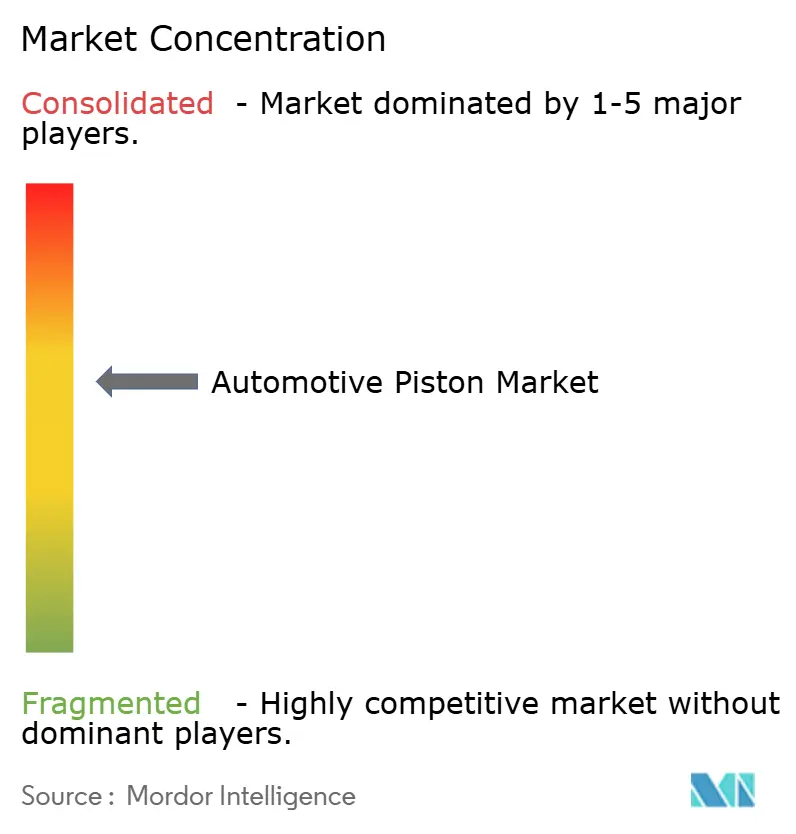

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Piston Market Analysis by Mordor Intelligence

The automotive piston market size reached USD 2.98 billion in 2025 and is forecast to expand at a 2.11% CAGR, pushing value to USD 3.31 billion by 2030. Growth rests on a delicate balance between enduring internal-combustion demand in emerging economies and mounting electrification mandates in developed regions. Manufacturers are sharpening focus on lightweight alloys, advanced coatings, and 3-D-printed geometries that improve heat management and fuel efficiency while satisfying stricter Euro 7 durability thresholds. At the same time, a steadily aging global vehicle parc is widening the revenue base for replacement pistons, rings, and pins, especially in markets where service intervals are lengthening and fuel quality varies widely. The supply landscape remains moderately consolidated, but capital infusions into hydrogen-ICE, hybrid, and coating R&D signal long-term confidence in the technology’s residual value.

Key Report Takeaways

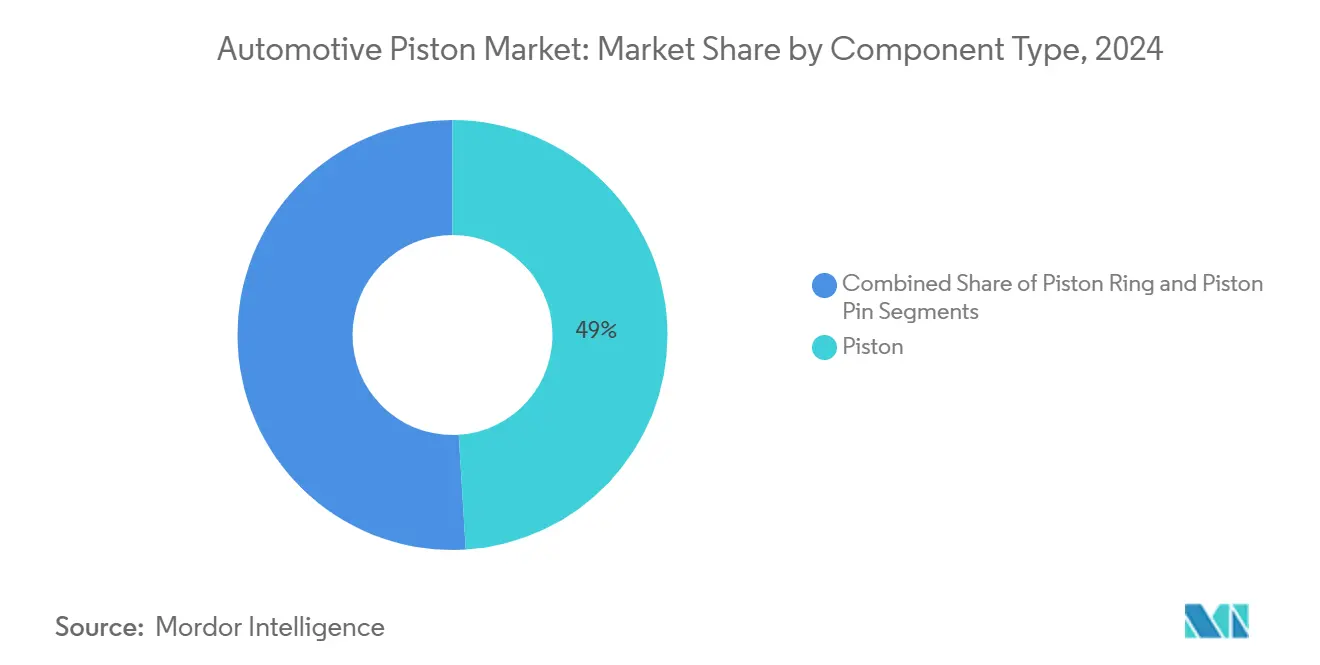

- By component type, pistons held 49.02% of the automotive piston market share in 2024, while piston pins are projected to post the fastest 3.79% CAGR through 2030.

- By coating type, thermal barrier coatings led with 40.34% of the automotive piston market share in 2024, whereas dry-film lubrication coatings are expected to accelerate at a 3.25% CAGR to 2030.

- By vehicle type, passenger cars captured 64.55% of the automotive piston market share in 2024, yet commercial vehicles are forecasted to rise at a 2.63% CAGR between 2025 and 2030.

- By material type, aluminum accounted for 72.92% of the automotive piston market share in 2024, while steel pistons are anticipated to grow at a 2.41% CAGR through 2030.

- By geography, Asia-Pacific dominated with a 47.71% of the automotive piston market share in 2024, and the Middle East and Africa are poised to record the highest 2.49% CAGR through 2030.

Global Automotive Piston Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continued ICE Vehicle Demand | +1.2% | Asia-Pacific, South America, Middle East and Africa | Medium term (2-4 years) |

| Lightweight Al and Coated Pistons | +0.9% | Global, with early gains in Europe, North America | Short term (≤ 2 years) |

| Growing Vehicle Parc | +0.8% | Global, spill-over to mature markets | Long term (≥ 4 years) |

| Hydrogen ICE Prototypes | +0.7% | Europe, Japan, select North America programs | Long term (≥ 4 years) |

| Low-Friction Skirt Coatings | +0.6% | North America and EU, APAC core | Medium term (2-4 years) |

| 3-D Printed Custom Pistons | +0.4% | Global, with early gains in motorsport, premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Continued ICE Demand in Emerging Markets

Rapid motorization in India, Brazil, and Southeast Asia keeps internal-combustion programs central to OEM capacity planning. India's passenger-vehicle dispatches continued to climb in 2024 despite higher electrification rhetoric. Consumer purchasing-power realities, infrastructure gaps, and bio-fuel compatibility reinforce short- to mid-term reliance on gasoline and flex-fuel powertrains. Suppliers therefore prioritize scalable piston designs that meet Euro 7 thermal loads yet remain cost-competitive for value-oriented segments. This demand cushion offers vital volume stability as Western ICE output plateaus.

Stringent Emissions Pushing Lightweight Aluminum and Coated Pistons

Euro 7 extends durability requirements to 160,000 km and tightens particulate limits, compelling OEMs to adopt lighter alloys and ceramic crowns that hold peak temperatures in check. Yttria-stabilized zirconia coatings can drop piston-crown temperature significantly while lifting part-load brake-thermal efficiency. Nano-crystalline bore coatings and DLC-based skirt films further reduce friction, enabling lower-viscosity oils without seizure risk. Suppliers are racing to industrialize multi-layer barrier stacks that meet both thermal-fatigue and recyclability targets. Early adopters gain emission-credit headroom and warranty cost relief.

Growing Vehicle Parc Driving Aftermarket Piston Replacement

Global vehicle average fleet age tops 12 years in North America and Western Europe. Extended oil-change intervals, ethanol blends, and poorer fuel filtration in developing regions accelerate ring and skirt wear, sustaining a healthy replacement cadence. E-commerce parts portals and telematics-driven maintenance alerts are streamlining demand capture for remanufactured and OE-equivalent pistons. Cast-iron rings continue to dominate heavy-duty applications, yet coated steel rings are gaining share where low-ash lubricants prevail. Combined, these trends underpin a multi-year aftermarket revenue tail even as OE volumes level off.

Hydrogen-ICE Prototypes Need High-Temperature Steel Pistons

Automakers are piloting hydrogen direct-injection engines that operate at combustion temperatures exceeding those of standard gasoline units. Steel pistons with optimized cooling galleries provide the required thermal mass and dimensional stability, tolerating peak in-cylinder pressures above 200 bar. Additive-manufactured steel crowns paired with aluminum skirts balance inertia with heat resistance, a design now moving from laboratory cells to limited-series trucks and sports cars. A growing pipeline of commercial-vehicle pilots in Europe and Japan is creating niche but technologically influential demand. For piston vendors, early mastery of hydrogen-specific metallurgy and coatings offers a strategic hedge against pure EV dominance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating EV Penetration | -1.5% | Europe, China, select North America markets | Medium term (2-4 years) |

| Engine Downsizing | -1.1% | Global, with concentration in developed markets | Short term (≤ 2 years) |

| Cylinder-Deactivation | -0.8% | North America and EU, expanding to Asia | Medium term (2-4 years) |

| OEM Cap-Ex | -0.6% | Global OEM strategies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating EV Penetration Cannibalizes ICE Volumes

Battery-electric vehicles account for a significant market share in new-car sales in Europe and China during 2024, translating into fewer piston sets ordered per assembly line. Oil-demand displacement tops 1 million barrels per day, and regulatory incentives are tilting future capital spending toward gigafactories rather than foundries. Nevertheless, wavering consumer subsidies and raw-material price spikes have injected volatility into EV adoption curves, creating planning uncertainty for piston makers. Suppliers diversify into thermal-management plates, e-axle housings, and hydrogen-ICE prototypes to offset looming ICE attrition. The timing mismatch between EV penetration and fleet turnover still grants a medium-term buffer, but boardrooms are recalibrating investment horizons.

Engine Downsizing Reduces Piston Count per Vehicle

OEMs are replacing six- and eight-cylinder blocks with turbocharged three- and four-cylinder units to meet CO₂ targets, slashing the number of pistons required per vehicle. Although each remaining piston faces higher specific loads, overall unit demand drops, pressuring volume-dependent foundries. Downsizing also aligns with cylinder-deactivation strategies that further lower operational duty cycles, shortening aftermarket replacement frequency. Design complexity rises: skirt asymmetry, reinforced pin bosses, and DLC coatings must counter elevated blow-by risks and peak pressures. Vendors that offer finite-element-validated, high-temperature alloys secure a competitive advantage, while legacy grey-iron lines risk obsolescence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Demand Concentrated in Pistons; Pins Outpace on Growth

The automotive piston market size attributed to pistons stood at 49.02% revenue in 2024, reflecting their critical combustion-chamber role. OEM programs emphasize topology-optimized, 3-D printed piston crowns that deliver up to 20% weight savings and integrated cooling, tightening tolerances to comply with Euro 7 heat-flux limits. Aftermarket demand remains resilient for cast pistons and rings, especially in high-mileage vehicles requiring durable metallurgy.

Piston pins are the fastest-growing component, with a 3.79% CAGR to 2030, driven by diamond-like carbon coatings that cut friction coefficients to around 0.1 while permitting bearing-bush elimination. PVD processes raise operating-temperature ceilings to 450 °C, supporting engine downsizing trends. Piston rings continue to leverage robust replacement cycles, with low-viscosity oil compatibility prompting refined surface finishes. Co-development initiatives between piston manufacturers and ring specialists target optimal tribological pairings that extend service life.

By Coating Type: Thermal Barriers Anchor Revenue; Dry Films Surge

Thermal barrier coatings secured 40.34% of the automotive piston market size in 2024 revenue, owing to widespread deployment of yttria-stabilized zirconia layers that boost part-load efficiency and mitigate thermal fatigue. Suspension-plasma-sprayed gadolinium zirconate barriers lower heat losses and increase indicated efficiency[1]“Suspension Plasma Sprayed Thermal Barrier Coatings for Light Duty Diesel Engines,” Journal of Thermal Spray Technology, link.springer.com. OEM adoption of multi-layer systems integrating ceramic and metallic intermediates is rising to withstand peak in-cylinder pressures.

Dry-film lubrication is projected to expand at a 3.25% CAGR, supported by skirt-coating demand in low-viscosity-oil engines seeking fuel-economy credits. Early-generation molybdenum-graphite blends are giving way to nano-composite dispersions that halve wear rates. Oil-shedding coatings sustain niche uptake in commercial vehicles, where oil-consumption control over long drain intervals remains a priority. ISO 14001 programs spur greener coating chemistries and closed-loop spray systems.

By Vehicle Type: Passenger Cars Retain Scale; Commercial Applications Accelerate

Passenger cars captured 64.55% of the automotive piston market size in 2024, anchored by compact and midsize models produced in Asia-Pacific. Hybrid architectures still leverage conventional pistons during combustion phases, softening the impact of battery-electric substitution. Automakers co-engineer aluminum crowns and low-friction skirt films to balance fuel-economy targets with warranty durability, while aftermarket rings cater to older sedans where oil consumption rises with mileage. Digital service platforms predicting piston wear from telematics data are gaining fleet traction, enabling proactive maintenance and cross-selling upgraded parts.

Commercial-vehicle demand will outpace passenger-car growth at a 2.63% CAGR through 2030, as infrastructure spending and e-commerce logistics widen haulage fleets. Heavy-duty diesels require pistons that tolerate brake mean-effective pressures above 25 bar, driving adoption of steel crowns and dual-material assemblies. Regional emission regimes, EPA Phase 3 in the United States and pending Euro VII in Europe, push fleets toward cleaner combustion but still depend on ICE technology for range and payload. Component suppliers that can validate pistons for renewable-diesel and hydrogen blends stand to gain from public-sector procurement and early decarbonization pilots. Retrofit kits offering thermally robust crowns and low-ash ring packs are emerging as a commercial-fleet budget alternative to full power-unit replacement.

By Material Type: Aluminum Dominates; Steel Gains Strategic Traction

Aluminum accounted for 72.92% of the automotive piston market size in 2024, as it remains the default choice for light-vehicle pistons owing to its superior thermal conductivity and casting efficiency. Advanced 2000-series alloys, reinforced with trace copper and silicon, realize yield strengths above 420 MPa, enabling thinner crowns and reduced reciprocating mass. High-pressure-die-cast processes now incorporate vacuum assists and real-time X-ray inspection to cut porosity, a critical enabler of Euro 7 life-cycle targets. Sustainability is improving through closed-loop recycling: foundries feed secondary aluminum content while meeting IATF 16949 cleanliness metrics. These gains dovetail with OEM carbon-neutral pledges, reinforcing aluminum’s near-term dominance.

Steel pistons, growing at a 2.41% CAGR, are carving out growth niches in heavy-duty diesel, performance gasoline, and hydrogen-ICE segments where combustion temperatures surpass aluminum fatigue thresholds. Additive manufacturing allows topology-optimized galleries that trim mass while containing peak crown temperatures. Dual-metal approaches, steel crowns friction-welded to aluminum skirts, merge thermal endurance with inertia advantages, and several European truck platforms are moving the architecture into series production. Material scientists are experimenting with martensitic micro-alloying and nano-oxide dispersions to push thermal-fatigue resistance further. Long term, steel’s share will hinge on cost-downs in powder-bed fusion and the scalability of bimetal joining techniques validated under Euro VII cycles.

Geography Analysis

Asia-Pacific commanded 47.71% of the automotive piston market share in 2024, underpinned by China, India, and Japan’s capacity. India’s two-wheeler share drives high-volume demand for small-bore aluminum pistons[2]“India’s Automobile Industry: Growth & Trends,” India Brand Equity Foundation, ibef.org. Deep supply chains, competitive labor costs, and proximity to fast-growing domestic markets anchor the region’s leadership. China’s piston-ring aftermarket growth reflects a vast vehicle parc with rising replacement intervals, while Japan’s hybrid focus sustains aluminum-skirt adoption.

The Middle East and Africa will post the highest 2.49% CAGR through 2030. Infrastructure spending, population growth, and diversification programs raise vehicle penetration and boost commercial transportation needs. Harsh climates necessitate premium coatings capable of handling extreme temperatures and abrasive dust, elevating average selling prices. Import-heavy markets in the Gulf cooperate with local assembly initiatives, creating opportunities for regional machining hubs and logistic partnerships.

North America and Europe exhibit a subdued growth as electrification tempers new ICE builds. Nonetheless, sizeable legacy fleets and robust commercial-vehicle segments ensure predictable aftermarket volumes. U.S. Class-8 truck cycles favor steel-crown pistons for high thermal loads, and Canada’s cold-weather conditions sustain demand for low-expansion alloys. Latin America remains resilient, with Mexico exporting majority of its production. Ethanol-compatible pistons and flexible-fuel designs support differentiated material mixes across the region.

Competitive Landscape

The automotive piston market exhibits moderate concentration, indicating substantial opportunities for consolidation as the industry navigates electrification pressures while maintaining ICE expertise. Leading companies combine vertical integration with advanced manufacturing to defend their share. For example, one top player introduced 3-D printed aluminum pistons that lower weight by about 10% and unlock 30 horsepower gains through internal cooling features. Another leading supplier secured investment capital to accelerate product diversification into clean-air and conventional powertrain lines.

Portfolio realignment continues as firms shed non-core assets and reinforce technology gaps. A prominent European producer divested small-bore piston production to focus on large-bore and defense applications. Regional acquisition moves, such as a South Asian specialist’s purchase of a precision-molding company, aim to secure critical tooling and protect proprietary designs. White-space growth lies in hydrogen-ICE, DLC-coated pins, and emerging-market aftermarket channels, where established brands can leverage distribution depth and technical know-how.

Collaborative R&D with engine OEMs intensifies around Euro 7 and EPA Phase 3 compliance. Material science advances, dual-metal assemblies, nano-composite skirts, and hybrid lubrication coatings, are progressing from prototype to series production. Quality frameworks such as IATF 16949 and ISO 9001 remain gating requirements for Tier-1 awards, while sustainability metrics enter sourcing scorecards. Overall, strategic emphasis rests on balancing ICE profitability with staged electrification participation.

Automotive Piston Industry Leaders

Mahle GmbH

Tenneco Inc.

Rheinmetall AG

Aisin Corporation

Shriram Pistons and Rings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Danfoss Power Solutions introduced the MP1T axial-piston tandem pump aimed at higher rotating efficiency and compact installation.

- March 2025: Ferrari filed a patent for V12 slotted pistons rotated 90° to the crankshaft, enabling a more compact combustion chamber.

- January 2025: Piston Automotive expanded its Detroit facility to produce hydrogen fuel-cell assemblies, aided by a USD 1.5 million state grant.

- December 2024: Shriram Pistons & Rings acquired TGPEL Precision Engineering to strengthen high-precision molding capabilities for diversified applications.

Global Automotive Piston Market Report Scope

| Piston |

| Piston Ring |

| Piston Pin |

| Oil Shedding |

| Dry Film Lubrication |

| Thermal Barrier |

| Passenger Cars |

| Commercial Vehicles |

| Aluminum |

| Steel |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Component Type | Piston | |

| Piston Ring | ||

| Piston Pin | ||

| By Coating Type | Oil Shedding | |

| Dry Film Lubrication | ||

| Thermal Barrier | ||

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Material Type | Aluminum | |

| Steel | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the automotive piston market?

The market was valued at USD 2.98 billion in 2025.

How fast is the automotive piston market expected to grow?

The market is projected to register a 2.11% CAGR from 2025 to 2030.

Which region holds the largest share of global piston demand?

Asia-Pacific accounted for 47.71% of global revenue in 2024.

Which coating technology is growing the quickest?

Dry-film lubrication coatings are forecast to rise at a 3.25% CAGR through 2030.

Which material is gaining momentum against aluminum pistons?

Steel pistons are the fastest-growing material segment, advancing at a 2.41% CAGR.

Page last updated on: