Automotive Piston Pin Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 32.52 Billion |

| Market Size (2031) | USD 39.17 Billion |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Piston Pin Market Analysis by Mordor Intelligence

The automotive piston pin market is projected to reach USD 31.33 billion in 2025, USD 32.52 billion in 2026, and USD 39.17 billion by 2031, growing at a CAGR of 3.79%. Sustained production of internal-combustion vehicles in emerging economies, premiumization of passenger vehicles, and robust aftermarket demand underpin the steady expansion of the automotive piston pin market. Lightweighting initiatives are accelerating the shift toward aluminum and titanium variants, while hybrid powertrains and alternative-fuel engines preserve the relevance of high-performance steel designs. Competitive intensity remains moderate, as precision-manufacturing barriers restrict new entrants, yet capital investment continues in advanced coating and forging technologies that raise average selling prices and support margins. South America, led by Brazil, offers the fastest regional growth as local manufacturing scales to meet regional trade opportunities.

Key Report Takeaways

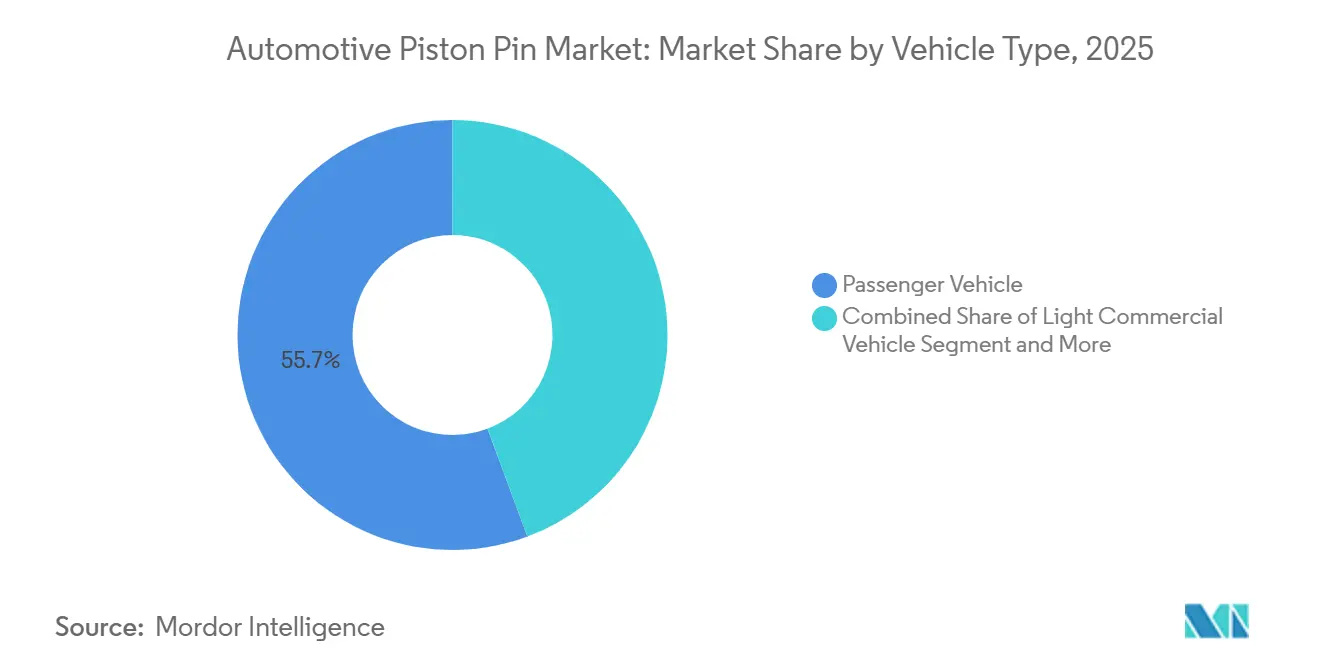

- By vehicle type, passenger vehicles led 55.68% of the automotive piston pin market share in 2025; the light commercial vehicle segment is projected to expand at a 5.05% CAGR through 2031.

- By fuel type, gasoline engines captured 48.59% of the automotive piston pin market share in 2025, while alternative fuel applications are advancing at a 6.44% CAGR through 2031.

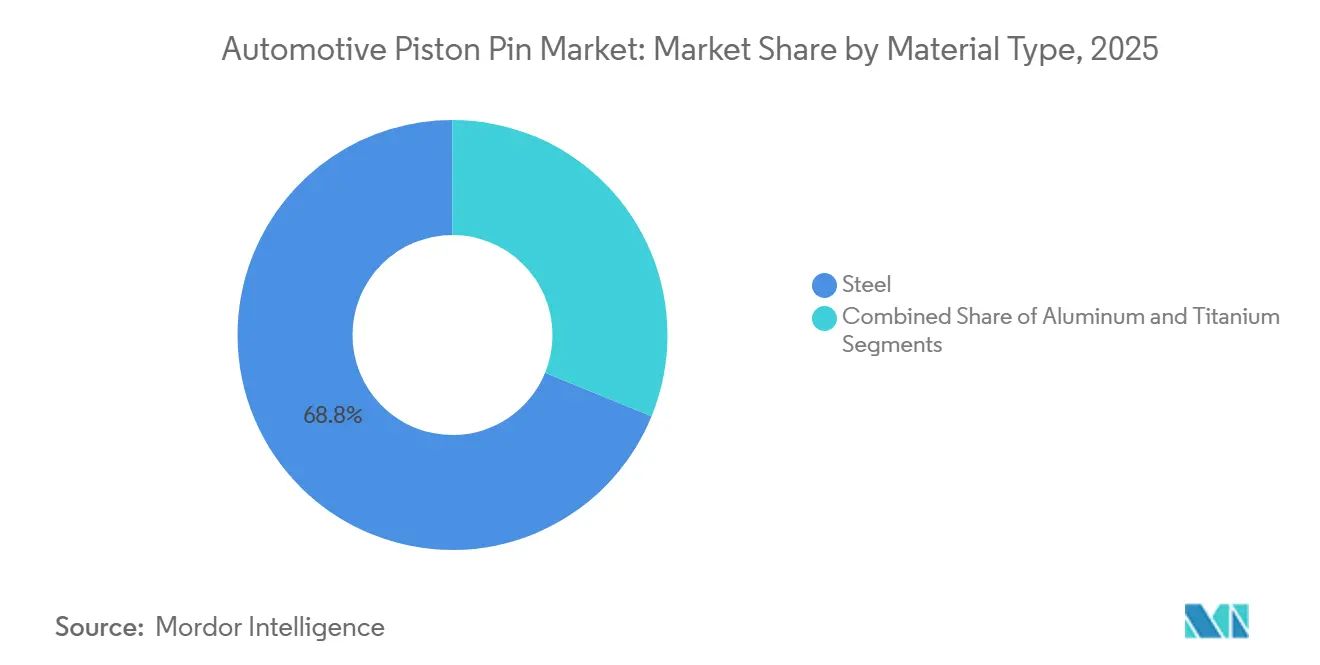

- By material type, steel maintained a 68.84% share of the automotive piston pin market in 2025, while aluminum is poised to grow at a 5.26% CAGR through 2031.

- By sales channel, OEM supply commanded 92.12% of the automotive piston pin market share in 2025; the aftermarket segment is climbing at a 4.47% CAGR through 2031.

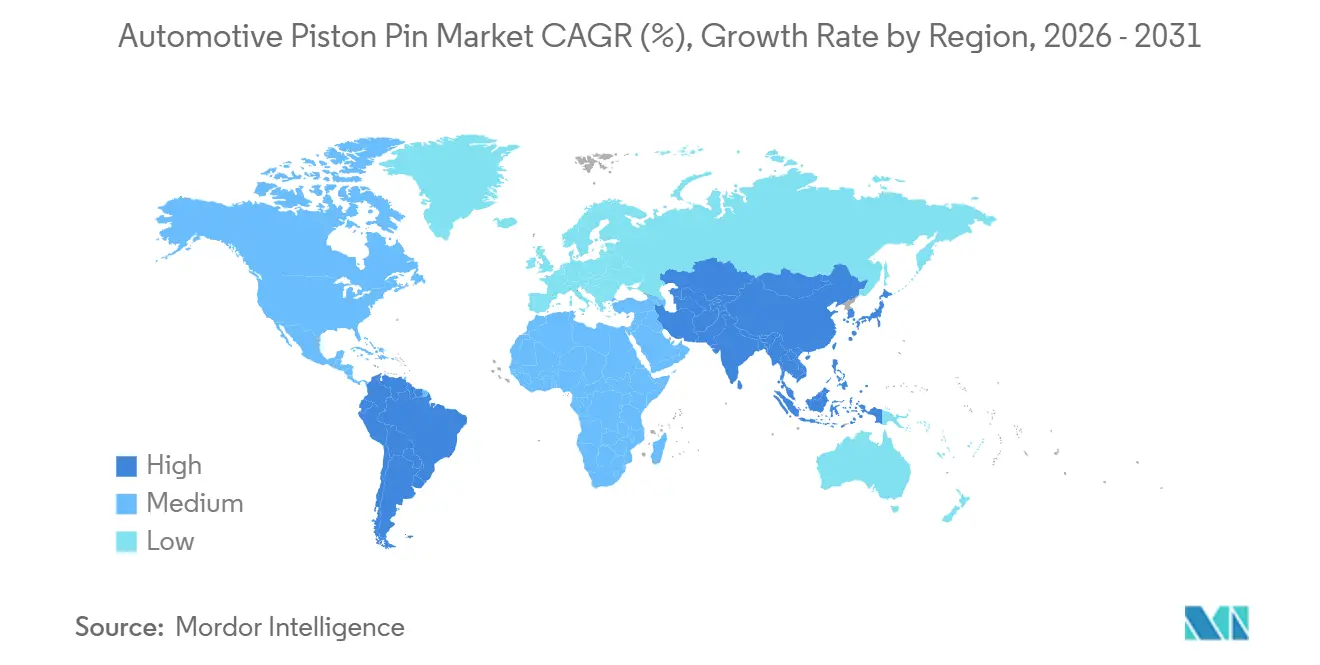

- By geography, Asia-Pacific dominated with 45.56% of the automotive piston pin market share in 2025, whereas South America is projected to record the highest regional CAGR at 4.08% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Piston Pin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Passenger-Vehicle Output Surge | +1.2% | Global, with Asia Pacific and North America leading | Medium term (2-4 years) |

| Sustained ICE Vehicle Production | +0.9% | Asia Pacific core, spill-over to South America and Middle East and Africa | Long term (≥ 4 years) |

| Alt-Fuel ICE Fleets | +0.7% | Global, with early gains in Europe and Asia Pacific | Medium term (2-4 years) |

| High-Performance Engine Demand | +0.6% | North America and Europe, expanding to Asia Pacific | Short term (≤ 2 years) |

| DLC/PVD Coatings | +0.4% | Global, led by premium OEMs | Long term (≥ 4 years) |

| Hybrid ICE Upgrades | +0.3% | North America, Europe, and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

SUV-Led Surge in Passenger-Vehicle Output

Global SUV demand continues to drive increases in engine displacement and cylinder counts, directly increasing the required piston pin volumes. India’s SUV registrations grew at double-digit rates between 2020 and 2024, reinforcing the dominant contribution of passenger vehicles to the automotive piston pin market[1]“Revolutionizing Mobility: The Make in India Auto Story,” Press Information Bureau, PIB, pib.gov.in. Large-format turbocharged engines specified for premium SUVs demand advanced steel alloys and DLC coatings, raising per-vehicle content value. Suppliers that offer precise forging and coating capabilities secure long-term OEM platforms, as SUVs anchor automakers' profitability worldwide. Rising SUV penetration across APAC and North America, therefore, magnifies volume and value growth outlooks for piston pin manufacturers.

Sustained ICE Vehicle Production in Emerging Economies

Infrastructure and cost realities keep traditional powertrains prevalent across India, Southeast Asia, and South America, safeguarding baseline demand in the automotive piston pin market. India’s component sector projects high-single-digit growth in 2025-26, with engine parts accounting for over one-quarter of the OEM bill of materials. Domestic value-addition mandates encourage investment in local forging and machining, reducing reliance on imports and broadening supplier participation. Agricultural machinery and commercial vehicles bolster volumes as these applications favor diesel reliability over early electrification. Consequently, ICE-centric growth trajectories in developing regions offset volume losses anticipated in mature markets.

Growth in CNG/LNG And Other Alt-Fuel ICE Fleets

Fleet operators targeting fuel cost savings and emissions reductions are accelerating the adoption of CNG and LNG trucks and buses. These engines operate under higher peak pressures, prompting premium piston pin specifications with tighter tolerances and enhanced surface treatments. Global alternative-fuel applications are forecast to grow significantly, sustaining a differentiated, higher-margin niche within the automotive piston pin market. Hydrogen ICE programs, exemplified by PHINIA’s development work, foreshadow future demand for novel materials and coatings that withstand the unique combustion characteristics of hydrogen [2]“PHINIA’s Alternative Fuel Innovations Take Center Stage at the 2025 Vienna Motor Symposium,” PHINIA Inc., phinia.com. Suppliers investing early in alt-fuel expertise stand to capture outsized value as regulatory support and fleet economics coalesce.

Lightweight, High-Performance Engine Demand

Engine downsizing paired with turbocharging necessitates piston pins that reduce reciprocating mass while withstanding elevated mechanical loads. Advanced aluminum-silicon alloys and titanium rods are growing in use, driving demand for lightweight materials in the automotive piston pin market. Precision forging, vacuum heat treatment, and nanostructured coatings enhance fatigue resistance and dimensional stability. Performance-oriented segments, including premium compact cars and motorcycles, show early adoption, but mainstream models follow as cost curves recede. The resulting shift in the material mix increases average revenue per unit despite slower absolute volume growth in downsized engines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BEV Adoption | -1.8% | Global, led by China and EU | Long term (≥ 4 years) |

| Engine Downsizing | -0.8% | Global, with EU and Japan leading | Medium term (2-4 years) |

| OEM Vertical Integration | -0.5% | APAC core, expanding globally | Long term (≥ 4 years) |

| Patent-Protected H₂ ICE Pin Designs | -0.2% | EU and Japan, limited global impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating BEV Adoption

Battery-electric vehicles eliminate internal-combustion systems entirely, eliminating piston-pin use and posing the sharpest structural threat to long-range demand. China’s electric-car share more than doubled to light-vehicle output in 2024, a trajectory reinforced by purchase incentives and localized cell manufacturing. Europe mirrors this trend through stringent CO₂ targets and expanding charging networks. Suppliers must diversify toward alt-fuel, hybrid, or non-powertrain components to hedge volume erosion. Nonetheless, legacy vehicle fleets and hybridization pathways defer the restraint’s full impact to the latter half of the decade, allowing managed capacity transitions.

Engine Downsizing

Three-cylinder turbocharged units replace larger four-cylinder engines, cutting piston pin counts by over 20% per vehicle. Regulatory pressure for lower emissions is hastening downsizing across Europe and Japan, while cost-sensitive markets lag in adoption. Component makers mitigate the restraint by raising unit value through advanced alloys and coatings that endure higher specific combustion loads. However, aggregate volume declines persist, especially in small-car segments where electrification uptake combines with cylinder reduction. Suppliers in high-volume, entry-level programs face steeper adjustments than those servicing premium or commercial applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Dominance, Tractor Upswing

Passenger cars accounted for 55.68% of the automotive piston pin market revenue in 2025, reflecting sustained global light-vehicle assembly output. The automotive piston pin market size for passenger vehicles continues to rise as premium SUVs require larger-bore engines and multiple turbochargers, which heighten durability requirements. OEM modular platform strategies further cement long-term sourcing partnerships, favoring suppliers with global footprints and strict quality management systems. Meanwhile, aftermarket volumes grow steadily because aging passenger-vehicle fleets extend maintenance cycles in mature economies.

The light commercial vehicle segment is on track for the fastest 5.05% CAGR through 2031 as last-mile logistics and rural transport grow in India, Southeast Asia, and Latin America. Light commercial vehicles (LCVs) equipped with compact diesel and CNG engines play a crucial role. The frequent stop-start cycles and varying payloads put added strain on engine components, such as piston pins and bearings, leading to heightened wear. This phenomenon fuels a consistent demand in the aftermarket, particularly in tier-2 and tier-3 service hubs. Suppliers boasting nimble distribution networks collaborating with OEMs are co-developing wear-resistant alloys. These innovations are designed to withstand the challenges of urban congestion and thermal cycling.

By Fuel Type: Gasoline Holds Lead, Alternative Fuels Accelerat

Gasoline architectures accounted for 48.59% of the automotive piston pin market share in 2025, owing to entrenched fueling infrastructure and consumer familiarity. The segment’s moderate expansion benefits from ongoing hybridization that retains combustion elements, sustaining piston pin use even as electric drive integrates. Simultaneously, diesel remains indispensable in freight and off-highway equipment, though its share edges lower under regulatory scrutiny.

Alternative fuels post the highest CAGR at 6.44%, propelled by policy incentives and fleet economics. The automotive piston pin market size for CNG and LNG engines is growing rapidly as commercial operators pursue lower fuel costs and emissions targets—specialized pin geometries with superior thermal stability command premium prices, lifting revenue per unit. Hydrogen ICE prototypes under development with PHINIA and other tier-ones signal future high-margin sub-markets that will diversify the traditional fuel-mix landscape.

By Material Type: Steel Endures, Aluminum–Titanium Advance

Steel accounted for 68.84% of the automotive piston pin market revenue in 2025, underpinned by cost efficiency and mature supply chains. Continuous metallurgical innovation, including vanadium micro-alloying and bainitic quenching, enhances strength-to-weight ratios, enabling steel to compete in moderate lightweighting programs. Correspondingly, “automotive piston pin market size” gains tied to steel remain resilient, especially in cost-sensitive vehicle categories.

The aluminum segment is anticipated to grow at a 5.26% CAGR as OEMs target aggressive mass-reduction goals. While raw material costs are higher, lifecycle fuel savings and performance benefits justify adoption in turbocharged engines and premium motorcycles. Emerging nanostructured DLC coatings narrow wear gaps relative to hardened steel, boosting confidence among powertrain engineers. Therefore, the aluminum–titanium share of the automotive piston pin market is projected to climb steadily within hybrid and performance-oriented segments.

By Sales Channel: OEM Supremacy, Aftermarket Momentum

OEM channels accounted for 92.12% of automotive piston pin market shipments in 2025, reflecting automakers’ preference for tight quality oversight and synchronized logistics. Long-term contracts create predictable demand that underpins capacity investment, yet price competition remains intense. Platform lifecycle extensions stabilize OEM volumes, even as engine families evolve toward hybrid integration. The aftermarket delivers a faster 4.47% CAGR through 2031 as average global vehicle age rises beyond 12.5 years.

The automotive piston pin market is linked to the expansion of the replacement business, particularly in Latin America and Eastern Europe, where vehicle lifespans stretch. Independent repair networks and engine remanufacturers demand competitive pricing but value quick availability, giving an advantage to regionally warehoused suppliers. Digital cataloging and e-commerce ordering streamline access, expanding the addressable customer base beyond traditional distributor channels.

Geography Analysis

Asia-Pacific retained 45.56% of the automotive piston pin market revenue in 2025, anchored by China’s expansive supply chain and India’s fast-growing component sector. Regional governments bolster localization through tax incentives and infrastructure development, prompting global tier-ones to expand their forging and coating facilities near assembly plants. Aftermarket demand remains vibrant as fleet sizes surge and repair culture favors replacement over retirement.

South America posts the highest CAGR at 4.08% through 2031, owing to Brazil’s revitalized automotive output and regional trade that channels components to North American and European OEMs. Agricultural mechanization across Brazil and Argentina drives consumption of tractor engine parts, while freight expansion increases demand for medium- and heavy-duty commercial vehicle pins.

North America and Europe hold a sizeable share, yet grow modestly, as electrification weighs on ICE volumes. Nevertheless, premium vehicle programs and performance aftermarket segments preserve niche growth opportunities. Advanced manufacturing hubs in Germany and the United States specialize in high-precision, lightweight piston pins that serve global export markets. Hybrid powertrain prevalence across North America mitigates outright declines by maintaining smaller-displacement ICE components within broader electrified architectures.

The Middle East and Africa exhibit stable, low-single-digit expansion, driven by infrastructure projects and demand for replacement parts for aging commercial fleets. Localized engine-rebuilding ecosystems provide recurring aftermarket opportunities for piston pin suppliers, offering rugged, diesel-oriented designs suitable for harsh operating environments. Government diversification agendas in Gulf states also invest in regional automotive clusters, laying the groundwork for a gradual shift from completely built-up imports to localized part production.

Competitive Landscape

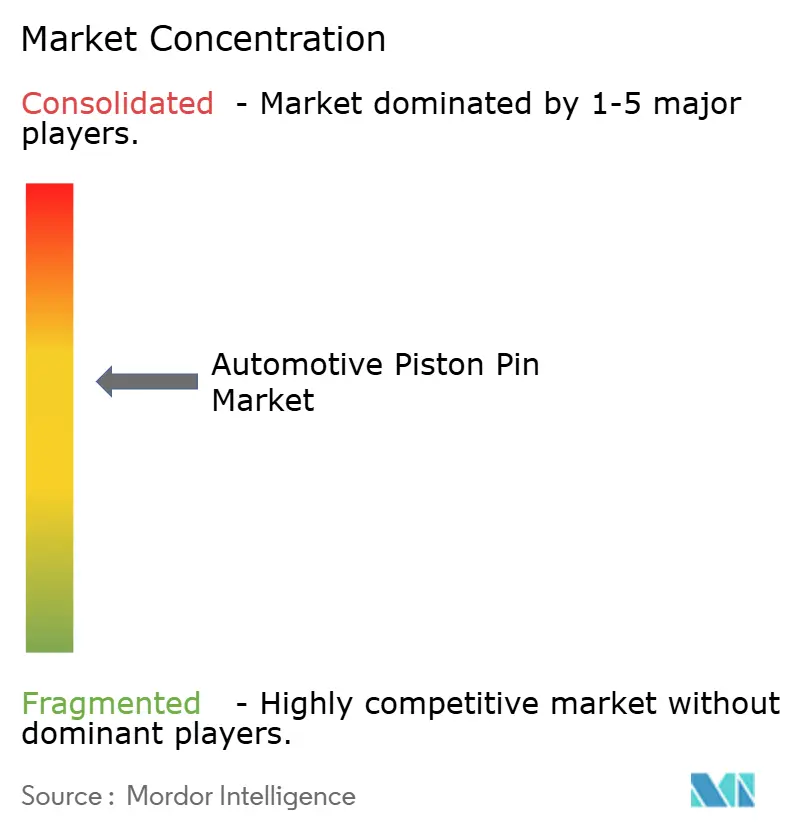

The automotive piston pin market exhibits moderate concentration, reflecting technical barriers to precision manufacturing and capital-intensive production requirements that limit new-entrant threats while creating opportunities for consolidation among existing players. These leaders leverage global production footprints, advanced toolsets, and co-development programs with OEMs to anchor supply contracts. Vertical integration across forging, machining, and coating streamlines cost structures and quality assurance.

Strategic investments prioritize diamond-like carbon (DLC) and physical vapor deposition (PVD) technologies that extend life under turbocharged and alternative-fuel conditions. Schaeffler’s recent alignment with drivetrain specialist Vitesco fortifies its materials science capabilities and expands access to hybrid powertrain programs. Simultaneously, suppliers are expanding regional capacity in Brazil, India, and Southeast Asia to meet localization mandates and hedge against logistical risks.

Disruptive entrants target lightweight titanium applications and hydrogen ICE programs, niches where incumbent economies of scale offer less advantage. OEM in-house machining expansion presents a dual threat and collaboration avenue: while reducing open-market volumes, it creates demand for equipment, tooling, and semi-finished blanks. As a result, successful suppliers provide flexible manufacturing solutions alongside finished components, embedding themselves deeper within customer value chains. Intellectual-property portfolios around coatings and micro-alloy formulations further differentiate competitors as price pressures intensify.

Automotive Piston Pin Industry Leaders

MAHLE GmbH

Tenneco Inc.

Aisin Corporation

Rheinmetall AG

Shriram Pistons and Rings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: MAN Truck & Bus selected MAHLE to supply piston pins and other components for the hydrogen-fueled MAN hTGX heavy-duty engine program.

- October 2024: JE Pistons released 9310 DLC-coated wrist pins, broadening its coated pin lineup for mid-power engines.

Global Automotive Piston Pin Market Report Scope

The automotive piston pin market is segmented into vehicle type, fuel type, material type, sales channel, and geography. By vehicle type, the market is segmented into passenger vehicle, light commercial vehicle, and medium and heavy commercial vehicle. By fuel type, the market is segmented into diesel, gasoline, and alternative fuel. By material type, the market is segmented into steel, aluminum, and titanium. By sales channel, the market is segmented into OEM and aftermarket. By geography, the market is segmented into North America, South America, Europe, Asia Pacific, and the Middle East and Africa.

The market size is provided both in terms of value in USD and volume in units.

| Passenger Vehicle |

| Light Commercial Vehicle |

| Medium and Heavy Commercial Vehicle |

| Diesel |

| Gasoline |

| Alternative Fuel |

| Steel |

| Aluminum |

| Titanium |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Vehicle Type | Passenger Vehicle | |

| Light Commercial Vehicle | ||

| Medium and Heavy Commercial Vehicle | ||

| By Fuel Type | Diesel | |

| Gasoline | ||

| Alternative Fuel | ||

| By Material Type | Steel | |

| Aluminum | ||

| Titanium | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is global demand for piston pins today?

The automotive piston pin market size reached USD 32.52 billion in 2026 and is projected to hit USD 39.17 billion by 2031.

Which vehicle category uses the most piston pins?

Passenger cars dominate with 55.68% share in 2025 because of high production volumes and the rise of multi-cylinder SUVs.

Which material is gaining fastest adoption?

Aluminum piston pins are growing at 5.26% CAGR due to lightweighting priorities in turbocharged engines.

Where is regional growth strongest?

South America leads with a 4.08% CAGR through 2031, powered by Brazil’s manufacturing expansion and agricultural equipment demand.

How will battery-electric vehicles affect the sector?

BEV adoption removes internal-combustion components, subtracting 1.8 percentage points from forecast CAGR, but hybrids and alternative-fuel engines temper long-term volume loss.

Page last updated on: