Automotive Engine Piston Rings Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 3.18 Billion |

| Market Size (2031) | USD 3.91 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

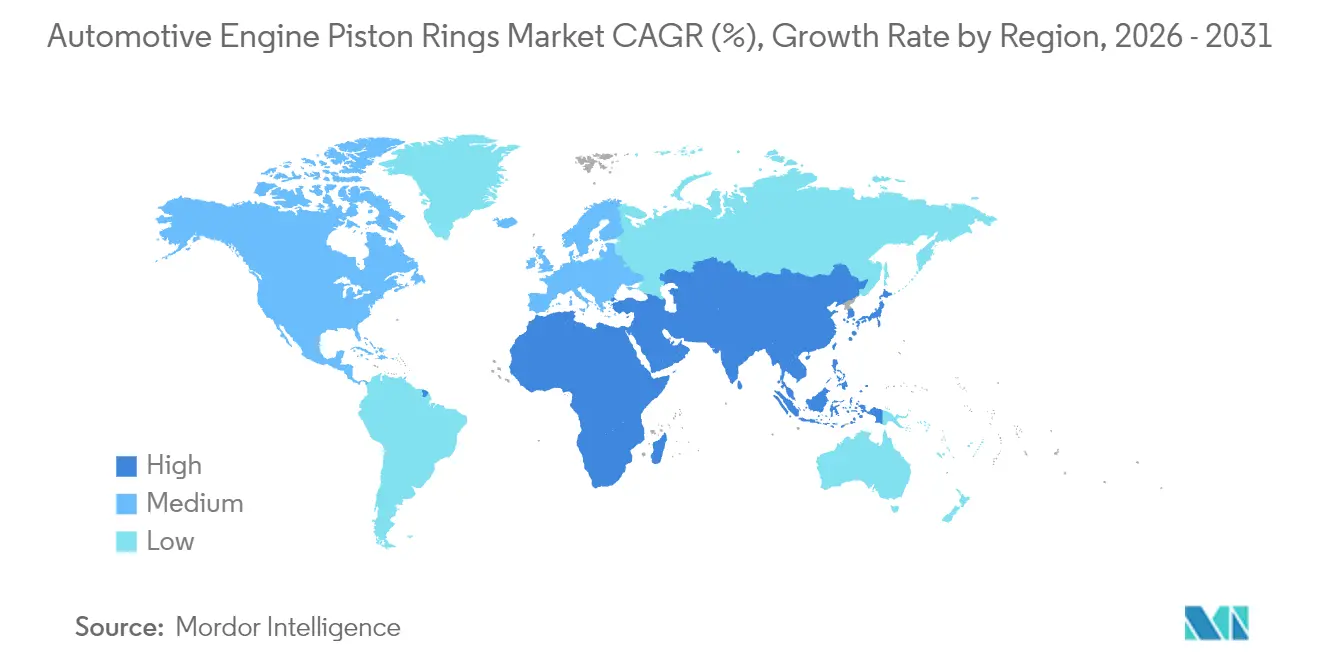

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

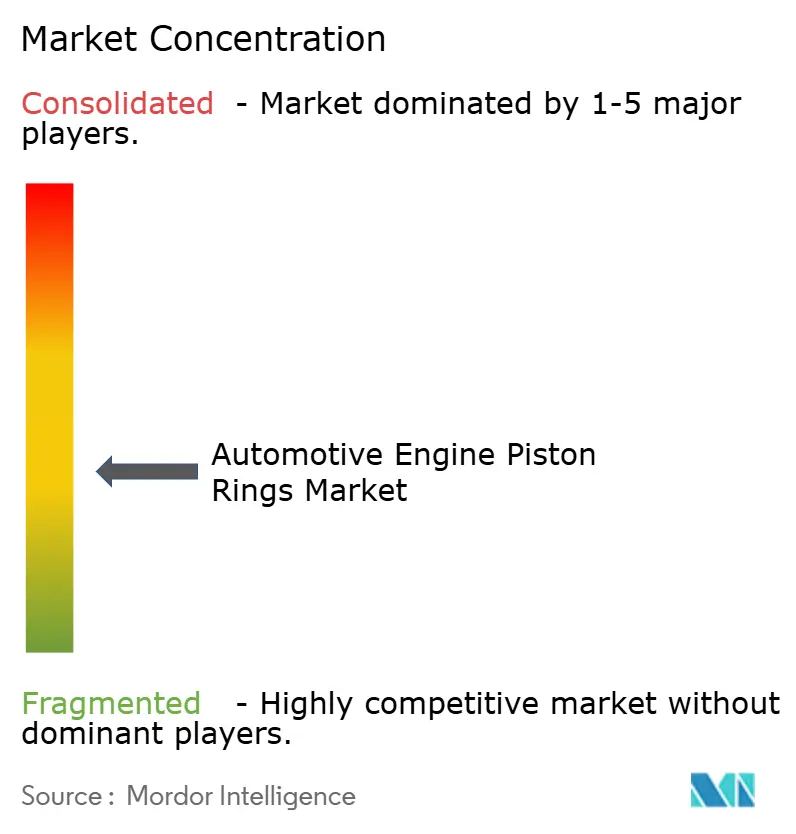

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Engine Piston Rings Market Analysis by Mordor Intelligence

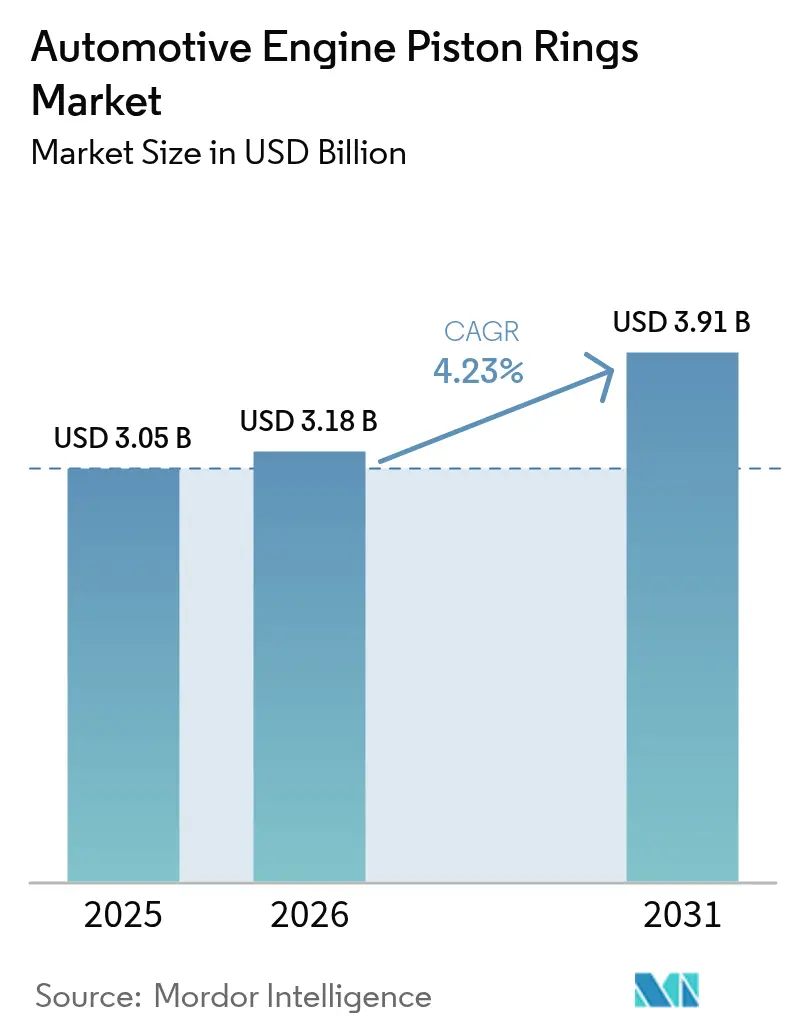

The automotive piston rings market size is expected to grow from USD 3.05 billion in 2025 to USD 3.18 billion in 2026 and is forecast to reach USD 3.91 billion by 2031 at a 4.23% CAGR over 2026-2031. In response to tightening fuel-economy and emissions regulations in Europe, China, and California, automakers are increasingly turning to low-friction rings. These rings help reduce oil consumption to minimal levels. Concurrently, the rising adoption of turbo-gasoline is pushing peak cylinder pressures higher, leading to a heightened demand for stainless and chromium-steel materials. Meanwhile, production of internal combustion engines in India, ASEAN, and Latin America has increased. This growth countered the expansion of battery-electric vehicles in Europe and China, ensuring a stable global volume outlook. While passenger cars held a dominant market share, two-wheelers, spearheaded by Honda's impressive annual output, are set to experience the swiftest growth. This trend is poised to bolster both aftermarket and OEM opportunities throughout South and Southeast Asia. Material substitution is on the rise, with stainless and chromium steel rings projected to expand significantly. This surge is fueled by the demands of turbo engines and hybrid duty cycles, which necessitate high tensile strength and low friction coefficients.

Key Report Takeaways

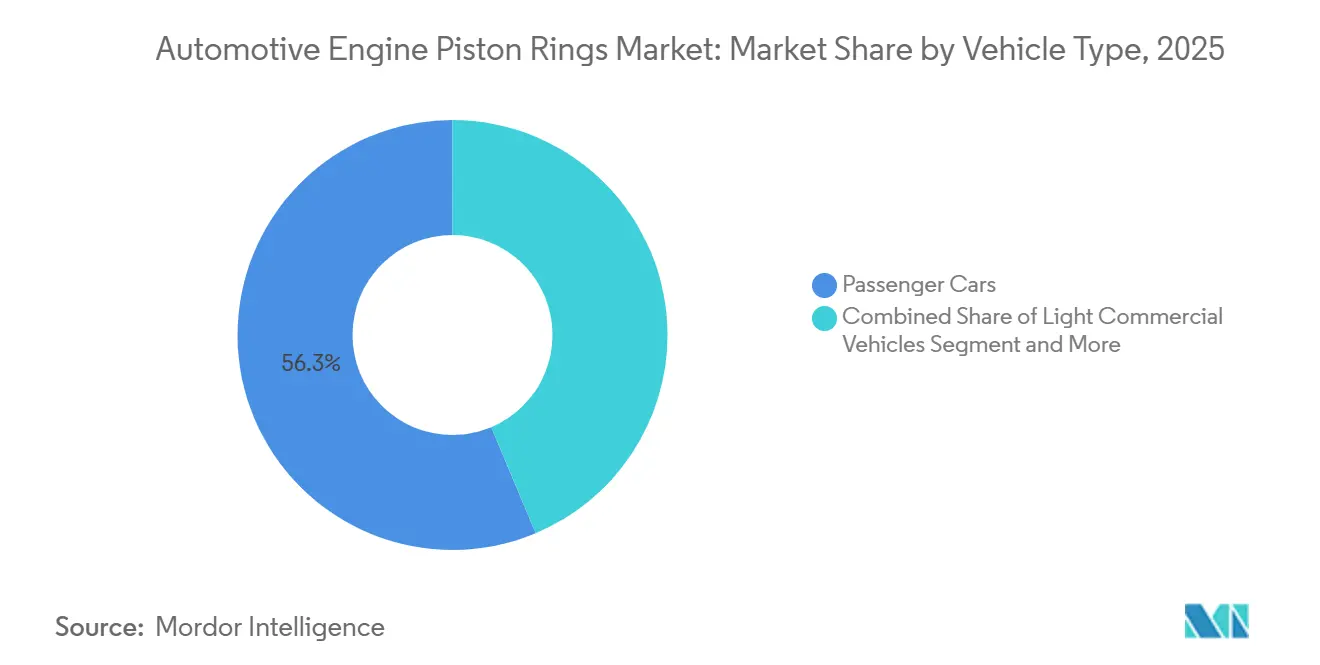

- By vehicle type, passenger cars led with 56.33% of the automotive piston rings market share in 2025, while two-wheelers are forecast to advance at a 7.98% CAGR to 2031.

- By material, gray cast iron retained a 46.62% share in 2025, whereas stainless/chromium steel is projected to grow at an 8.37% CAGR through 2031.

- By ring type, compression rings captured a 59.44% share in 2025; oil-control rings are set to rise at a 7.21% CAGR on tighter Euro 7 particulate norms.

- By coating type, chrome plating held a 35.12% share in 2025, yet DLC & ta-C coatings are poised for a 7.62% CAGR as heavy-duty OEMs target 2-3% fuel-efficiency gains.

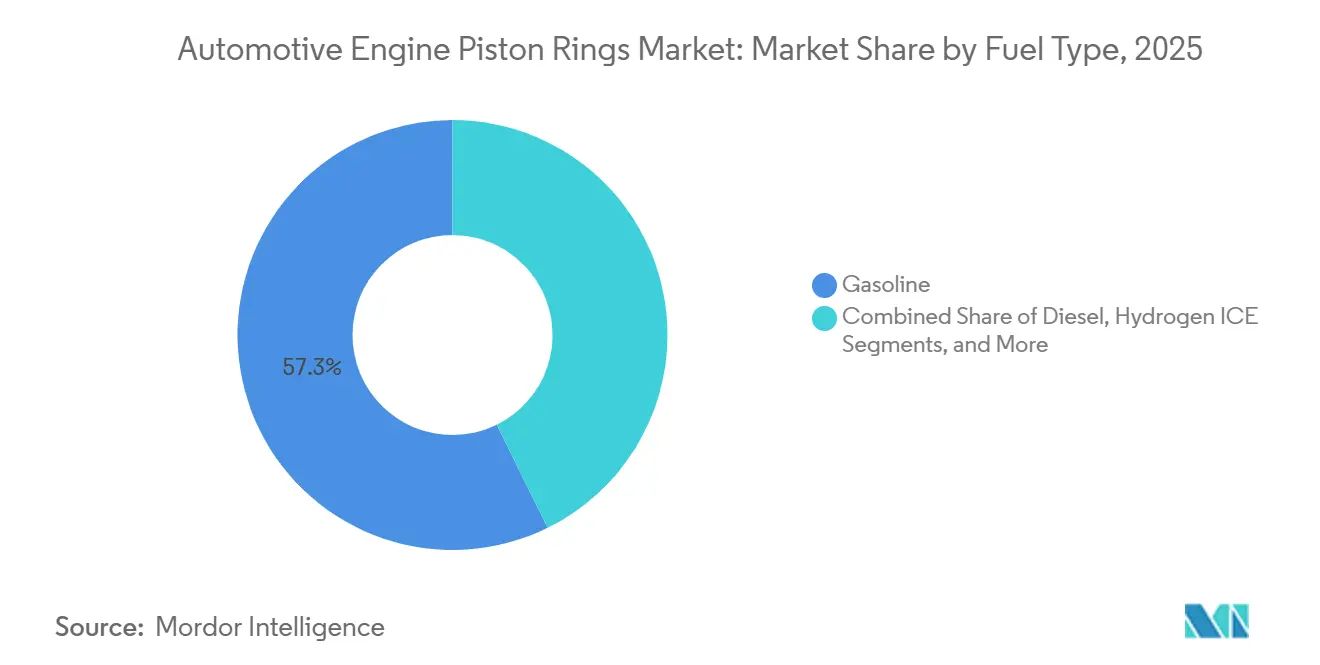

- By fuel type, gasoline engines accounted for 57.31% of the automotive piston ring market in 2025, while hydrogen ICE piston rings are projected to expand at a 7.48% CAGR between 2026 and 2031.

- By channel, the OEM segment commanded 70.12% share in 2025; the aftermarket will climb at a 5.95% CAGR.

- By geography, Asia-Pacific dominated with a 53.22% share in 2025, whereas the Middle East & Africa region is forecast to post the quickest 7.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Engine Piston Rings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict Emissions and Fuel-Economy Regulations | +1.8% | Global, with EU and North America leading | Medium term (2-4 years) |

| Rising ICE Vehicle Production in Emerging Economies | +1.2% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| OEM Shift to Low-Friction, Lightweight Steel Rings | +0.9% | Global, with APAC manufacturing focus | Medium term (2-4 years) |

| Turbo-Gasoline Adoption Demanding Tighter Ring Tolerances | +0.7% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Hydrogen-ICE Pilot Programs Needing Compatible Rings | +0.4% | EU and Japan early adoption, global expansion | Long term (≥ 4 years) |

| Smart Rings with Embedded Wear Sensors | +0.3% | Premium segments in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strict Emissions and Fuel-Economy Regulations Drive Innovation

Euro 7 regulations will limit particulate matter emissions for gasoline vehicles. These rules also mandate that OEMs adopt oil-control rings, ensuring fuel consumption remains below a minimal threshold [1] “Euro 7 Regulatory Package", European Commission, europa.eu. California's Advanced Clean Cars II sets stricter fleet-average CO₂ limits. This creates a crucial period during which all remaining internal combustion engine (ICE) programs must use ultra-low-friction ring sets to achieve significant fuel savings. China's National VI-b regulations introduce real-driving-emissions testing. They impose penalties for excessive oil usage, driving the widespread adoption of three-piece expander oil rings. In India, the upcoming Bharat Stage VII standards will further tighten particulate limits. This move is expected to accelerate the licensing of DLC and ceramic coatings from suppliers in Japan and Germany. Together, these regulations enable premium ISO 6621-certified rings to command higher prices, offsetting potential volume declines from electrification.

Rising ICE Vehicle Production in Emerging Economies Sustains Demand

India experienced significant growth in light vehicle production, while per-capita car ownership remained substantially lower than in the United States[2]“Production Statistics 2025,”, Society of Indian Automobile Manufacturers, siam.in. This indicates a continued structural demand for piston rings. In the ASEAN region, production was driven by Thailand's strong export-oriented automotive hub. Brazil and Mexico also contributed notably to vehicle output, supported by economic recovery and nearshoring incentives. Sub-Saharan Africa's light-vehicle market is expected to expand considerably, underscoring a growing aftermarket for replacement rings that need to be replaced regularly. This additional production helps offset a significant portion of unit losses linked to BEV adoption in OECD countries, reinforcing the market's positive long-term trajectory.

OEM Shift to Low-Friction, Lightweight Steel Rings Transforms Materials

Turbo engines now power a significant portion of global light-duty vehicles. These engines generate cylinder pressures substantially higher than those of naturally aspirated designs. This increase in pressure has led to a shift from gray iron to stainless or chromium-steel rings, offering enhanced durability. Physical-vapor-deposited DLC layers have effectively reduced friction coefficients and extended oil-change intervals. These advancements are critical for European and Japanese hybrids, enabling them to achieve superior fuel efficiency. MAHLE has reported a notable increase in the demand for low-friction rings, reflecting a rapid shift in material preferences. However, in regions like India and Indonesia, adoption remains slower due to higher cost premiums over gray iron, which limits broader market penetration.

Turbo-Gasoline Adoption Demands Tighter Ring Tolerances

China has emerged as a significant manufacturer of turbo-gasoline cars, while Europe has seen a substantial increase in turbo adoption. These trends highlight a growing global demand for rings precision-ground to radial-wall parallelism within tight tolerances. Down-sized turbo units, which routinely operate at high exhaust temperatures, subject rings to extreme peak pressures. This results in significantly higher wear rates compared to naturally aspirated engines, unless the rings are treated with molybdenum spray or ta-C layers. Only a limited number of Tier-1 suppliers possess the precision-machining capabilities required to maintain their competitive advantage. Meanwhile, the adoption of DLC and ta-C coatings continues to expand steadily.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating BEV Penetration | -1.1% | Global, with EU and China leading | Medium term (2-4 years) |

| Volatile Steel and Molybdenum Prices | -0.8% | Global manufacturing regions | Short term (≤ 2 years) |

| Premature Wear Issues with Ultra-Low-Tension Rings | -0.5% | Premium vehicle segments globally | Medium term (2-4 years) |

| Precision-Grinding Talent Shortage | -0.3% | Advanced manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating BEV Penetration Threatens Traditional Demand

Battery-electric vehicle sales have significantly increased, now accounting for a notable share of the global market [3]“Global EV Outlook 2025,”, International Energy Agency, iea.org. This share is expected to grow substantially in the coming years, potentially displacing a large volume of internal combustion engine (ICE) builds annually. China leads with the highest EV share, followed by Europe and California. This transition is eroding the most profitable passenger-car volumes that support Tier-1 margins. Suppliers are adapting to this shift; for instance, Tenneco has divested non-core assets to fund EV-thermal product development, acknowledging that its revenue from traditional products may stabilize in the near future. However, with the global ICE parc still comprising a large number of vehicles and average vehicle ages remaining high in regions such as the United States and Europe, the aftermarket sector provides a buffer against these changes.

Volatile Steel and Molybdenum Prices Compress Margins

Hot-rolled coil prices fluctuated significantly, while molybdenum prices rose sharply before stabilizing. A rise in molybdenum prices increases the ring-set cost, thereby reducing suppliers' gross margins, which are already narrow. Smaller producers in India and China, when faced with these price surges, typically pass on the costs to their customers with a delay. This delay often triggers audits from OEMs, straining engineering resources and slowing down product development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Drive Market Leadership

Passenger cars accounted for 56.33% of the automotive piston ring market in 2025. Yet, the two-wheeler cohort is forecast to post a 7.98% CAGR, as Honda, Hero, and Bajaj maintain high-volume scooter and motorcycle production across Asia. Light commercial vehicles hold a significant market share and are expected to grow steadily. This growth is primarily driven by rising e-commerce delivery demand in regions such as India, Brazil, and Indonesia, where diesel- or CNG-powered engines are preferred for daily routes. Medium and heavy trucks also maintain a notable share, with growth supported by advancements in hydrogen-ICE technology, which require thermally stable, reduced-top-land rings.

Two-wheeler rings are generally manufactured from ductile cast iron with chrome plating to balance cost and durability. However, premium scooters in India are increasingly adopting DLC-coated stainless rings to comply with evolving emission standards. In Europe and Japan, passenger-car OEMs increasingly specify stainless rings with PVD coatings for turbo-gasoline builds, a trend expected to grow as emission regulations tighten further. Light commercial platforms in emerging markets remain cost-sensitive, favoring cast-iron rings, although hybrid vans in the EU are transitioning to low-friction materials. Heavy-truck rings prioritize durability, focusing on extended service intervals. Consequently, molybdenum or ceramic overlays are preferred over friction reduction, sustaining a niche market for companies like Federal-Mogul and MAHLE. This diverse vehicle mix helps stabilize the automotive piston rings market against potential disruptions from the shift toward electrification in the premium car segment.

By Material Type: Gray Cast Iron Maintains Traditional Dominance

Gray cast iron accounted for 46.62% of volume in 2025 due to its USD 2.50-3.00/kg cost and entrenched furnaces in China, India, and Brazil. Stainless/chromium steel accounted for just 10%. Still, it will grow rapidly at an 8.37% CAGR to meet turbo-gasoline engines that run above 180 bar combustion pressure and hybrids that require low thermal expansion. Ductile iron held steady at a significant share, particularly in medium-duty diesels. Here, nodular graphite enhances strength compared to gray iron, allowing for thinner profiles that reduce friction.

Fleet operators note that while stainless rings are more expensive per engine compared to gray iron, the premium is recouped after a certain distance, thanks to fuel savings. However, retail consumers in regions such as India and Indonesia often resist the higher initial cost. The regional divide is evident: countries like Japan and Germany use stainless steel for the majority of their engines, in stark contrast to India and ASEAN, where gray iron remains dominant. Although advanced ceramic or composite rings currently occupy a small niche, developments such as MAHLE's acquisition of a nano-coating firm and Toyota's experiments with silicon nitride in hydrogen vehicles hint at potential growth, especially as hydrogen internal combustion engines (ICE) gain traction.

By Ring Type: Compression Rings Lead Critical Sealing Function

Compression rings led with a 59.44% share in 2025 because every engine requires a robust gas seal and heat path. Oil-control rings post a 7.21% CAGR on Euro 7’s 4.5 mg/km particulate cap that forces OEMs to slash oil consumption to 0.05% of fuel use. Wiper rings held steady, especially in long-haul diesel engines and off-highway machinery, where aggressive scraping is essential to prevent sludge buildup.

New oil-control rings predominantly feature three-piece expander designs, ensuring stable tension over extended distances and curbing lubricant migration, a phenomenon that can lead to catalyst poisoning. The significance of oil-control geometry is heightened in hydrogen internal combustion engines (ICEs), as stray lubricants can pre-ignite fuels with low ignition energy. Recognizing this, Cummins allocates a significant portion of its ring budget to these critical components. Meanwhile, R&D on compression rings is honing in on barrel and taper profiles to shorten the break-in period. In contrast, wiper-ring R&D is progressing at a more measured pace, prioritizing durability and tolerance to debris.

By Coating Technology: Chrome Plating Faces Advanced Alternatives

Chrome plating maintained a 35.12% share in 2025, primarily in the price-sensitive aftermarket, where electroplating lines are already depreciated. DLC and ta-C layers will grow at a 7.62% CAGR, as they drop friction to 0.08 and meet REACH restrictions on hexavalent chrome that take effect after 2025. Molybdenum spray coatings, with a significant market share, are favored for heavy equipment operating over extended intervals. Meanwhile, ceramic and hybrid nano-coats, supported by MAHLE's expanded capacity, account for a smaller share.

Capacity constraints remain a critical issue, as only a few global vendors provide large-scale PVD chambers. This limitation has extended lead times and compelled OEMs to consider chrome as a dual-source option in risk scenarios. The aftermarket is expected to maintain chrome's dominance for older, out-of-warranty vehicles, given its cost advantage over DLC units. However, new ICE platforms emerging in key regions are increasingly adopting DLC or ceramic coatings from the outset, creating a foundation for sustained demand growth.

By Fuel Type: Gasoline Engines Dominate Ring Applications

Gasoline engines accounted for 57.31% of the automotive piston ring market share in 2025, even as the BEV mix rises, since emerging-market growth offsets OECD decline. As urban bans tighten across Europe, diesel's market share is set to decline. However, the impact will be softened by the steadfast demand for commercial vehicles in India and Africa. Meanwhile, alternative gaseous fuels—namely CNG, LPG, and ethanol—are on an upward trajectory, driven by the expansion of India's growing CNG fleet.

Hydrogen ICE will grow at a 7.48% CAGR, with Cummins’ 6.7 L and 15 L engines entering production in 2027 and Toyota showcasing endurance-race prototypes. Hydrogen requires reduced top-land height and tighter oil control to avoid pre-ignition, pushing suppliers toward advanced materials and coatings. While volumes remain niche, the segment garners outsized R&D focus because it preserves familiar ICE manufacturing ecosystems inside a decarbonization narrative.

By Sales Channel: OEM Dominance Reflects Integration Trends

OEM contracts accounted for 70.12% in 2025, yet the aftermarket will expand at a 5.95% CAGR, while OEM growth will slow as ICE fleets in North America and Europe age past 12 years. Online platforms hold a significant share of U.S. aftermarket ring sales. Listings on Amazon and RockAuto enable small garages to bypass traditional distributors.

OEMs are exerting pressure on Tier-1 pricing. For example, Volkswagen has reduced its global supplier list, demanding consistent price reductions from them. As a result, many suppliers are turning to the aftermarket sector to improve margins. In India, independent producers like IP Rings have shifted focus, with a substantial portion of their revenue now coming from replacement demand. They have mitigated lower volumes by offering branded kits at premium prices, which include technical guides and warranties.

Geography Analysis

Asia-Pacific accounted for 53.22% of the target market in 2025; China leads with significant production volumes, followed by India, a key contributor. Thailand's export-focused hub, Indonesia's growing base, and Vietnam's emerging assembly capabilities collectively ensure steady OEM output. Japan's hybrid vehicle production drives demand for stainless and DLC rings, while South Korea's turbo-gasoline units intensify the need for precision machining. Despite the increasing penetration of electric vehicles in China, the remaining internal combustion engine production continues to account for a substantial share of regional piston-ring demand.

Europe holds a notable market share and is expected to grow steadily. Germany, France, and Italy remain prominent producers, with Germany's preference for turbo-gasoline engines boosting stainless steel demand. France and Italy extend the lifecycle of internal combustion engines, primarily for export to regions such as Africa and Latin America. The United Kingdom's focus on hybrid vehicles sustains demand for low-friction rings, while Spain benefits from nearshoring activities in North Africa. Russia's import-substitution initiatives strengthen local supply chains, although sanctions limit access to Western technologies.

North America maintains a significant market share and is projected to continue to grow. The United States dominates vehicle production in the region, with a large proportion of light trucks requiring specialized large-diameter ring sets. Mexico's export-oriented production provides stability for suppliers, while Canada's increasing focus on hybrid vehicles supports market demand. California's electric vehicle adoption is expected to grow under regulatory initiatives, while the extensive fleet of internal combustion engine vehicles nationwide ensures long-term replacement demand.

South America contributes a smaller but growing share to the market. Brazil's flex-fuel vehicles rely on stainless and molybdenum rings to withstand the challenges of ethanol combustion. Argentina's recovering production levels support exports to neighboring countries within the Mercosur bloc. Colombia and Chile are driving demand for durable ductile-iron rings, driven by their mining and agricultural sectors, though economic volatility in the region poses challenges to growth.

The Middle East & Africa are racing ahead at a 7.35% CAGR, as Saudi Arabia focuses on expanding vehicle production capacity, while the UAE transitions to hybrid and CNG taxi fleets. Turkey serves as a vital link between the European and Gulf markets with its automotive production capabilities. Similarly, South Africa plays a key role in meeting the aftermarket demands of sub-Saharan Africa. Although European OEMs are reducing ICE production domestically, oil-revenue-driven industrialization and low motorization rates in these regions indicate significant growth potential.

Competitive Landscape

Top suppliers NPR Riken, Tenneco’s Federal-Mogul, MAHLE, TPR Co., and Shriram Pistons account for a significant share of revenue, indicating moderate market concentration. As BEV penetration reduces car volumes, consolidation efforts are intensifying: Tenneco divested non-core units to strengthen its EV thermal portfolio, MAHLE acquired a ceramic-coating expert to sustain premium margins, and both NPR Riken and TPR optimized their fully integrated casting-to-coating lines, achieving notable reductions in lead times.

Indian producers Shriram Pistons and IP Rings expanded their capacities to meet rising demand from two-wheelers and tractors, strategically positioning themselves as cost-effective exporters to Africa and Latin America. Technology remains the pivotal advantage: suppliers investing in PVD lines are securing turbo and hybrid contracts, while those focused on chrome are facing regulatory challenges in the EU. The introduction of bright rings embedded with magneto-resistive sensors, capable of providing real-time wear data, is emerging as the next competitive frontier. However, patents are secured, a mass-market debut remains elusive, even with field trials validating significant extensions in overhaul intervals.

Automotive Engine Piston Rings Industry Leaders

-

NPR Riken Corporation

-

Tenneco Inc. (Federal-Mogul)

-

MAHLE GmbH

-

TPR Co., Ltd.

-

Shriram Pistons & Rings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Shriram Pistons & Rings Limited (SPRL) had struck a deal to fully acquire Karna Intertech Private Limited (Karna), with the current shareholders pocketing an estimated INR 50 million. The acquisition, scheduled for completion in 2025, highlighted SPRL's dedication to strengthening its operations and enhancing its manufacturing capabilities.

- February 2025: The National Highway Traffic Safety Administration (NHTSA) reports that Kia is recalling 137,256 Seltos and Soul vehicles from the 2021-2023 model years due to a piston ring defect. The recall documentation indicates that a manufacturing deviation by the piston ring supplier could cause cylinder wall surface damage over time.

Global Automotive Engine Piston Rings Market Report Scope

The automotive engine piston rings market report is segmented by vehicle type (passenger cars, medium and heavy commercial vehicles, two-wheelers, and off-highway (construction, agricultural)), material type (grey cast iron, ductile/alloyed cast iron, carbon steel, stainless / chromium steel, and advanced composites & ceramics), ring type (compression rings, wiper/scraper rings, and oil control rings), coating technology (chrome plating, molybdenum / Mo-spray, DLC & ta-c, and ceramic & hybrid nano-coatings), fuel type (gasoline, diesel, alternative fuels (CNG/LPG, biofuels), and hydrogen ice), sales channel (OEM and aftermarket), and geography. The market forecasts are provided in terms of value (USD) and volume (units).

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Two-Wheelers |

| Off-Highway (Construction, Agricultural) |

| Gray Cast Iron |

| Ductile / Alloyed Cast Iron |

| Carbon Steel |

| Stainless / Chromium Steel |

| Advanced Composites & Ceramics |

| Compression Rings |

| Wiper / Scraper Rings |

| Oil Control Rings |

| Chrome Plating |

| Molybdenum / Mo-Spray |

| DLC & ta-C |

| Ceramic & Hybrid Nano-Coatings |

| Gasoline |

| Diesel |

| Alternative Fuels (CNG/LPG, Biofuels) |

| Hydrogen ICE |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Two-Wheelers | ||

| Off-Highway (Construction, Agricultural) | ||

| By Material Type | Gray Cast Iron | |

| Ductile / Alloyed Cast Iron | ||

| Carbon Steel | ||

| Stainless / Chromium Steel | ||

| Advanced Composites & Ceramics | ||

| By Ring Type | Compression Rings | |

| Wiper / Scraper Rings | ||

| Oil Control Rings | ||

| By Coating Technology | Chrome Plating | |

| Molybdenum / Mo-Spray | ||

| DLC & ta-C | ||

| Ceramic & Hybrid Nano-Coatings | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| Alternative Fuels (CNG/LPG, Biofuels) | ||

| Hydrogen ICE | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global demand for automotive piston rings be by 2031?

The automotive piston rings market size is projected to reach USD 3.91 billion by 2031 on a 4.23% CAGR from 2026 to 2031.

Which vehicle class drives the fastest volume growth?

Two-wheelers are expected to post a 7.98% CAGR through 2031 as Asian motorcycle production and rural mobility programs expand.

What materials are gaining share over traditional cast iron?

Stainless and chromium-steel rings are growing at 8.37% CAGR because turbo and hybrid engines need higher strength and lower friction.

Which coatings will replace chrome in new engines

Diamond-like carbon and ta-C coatings are advancing at 7.62% CAGR, meeting both friction and REACH environmental requirements.

Page last updated on: