Automotive Engine Valve Market Size and Share

Market Overview

| Study Period | 2024 - 2030 |

|---|---|

| Market Size (2025) | USD 5.81 Billion |

| Market Size (2030) | USD 6.08 Billion |

| Growth Rate (2025 - 2030) | 0.91% CAGR |

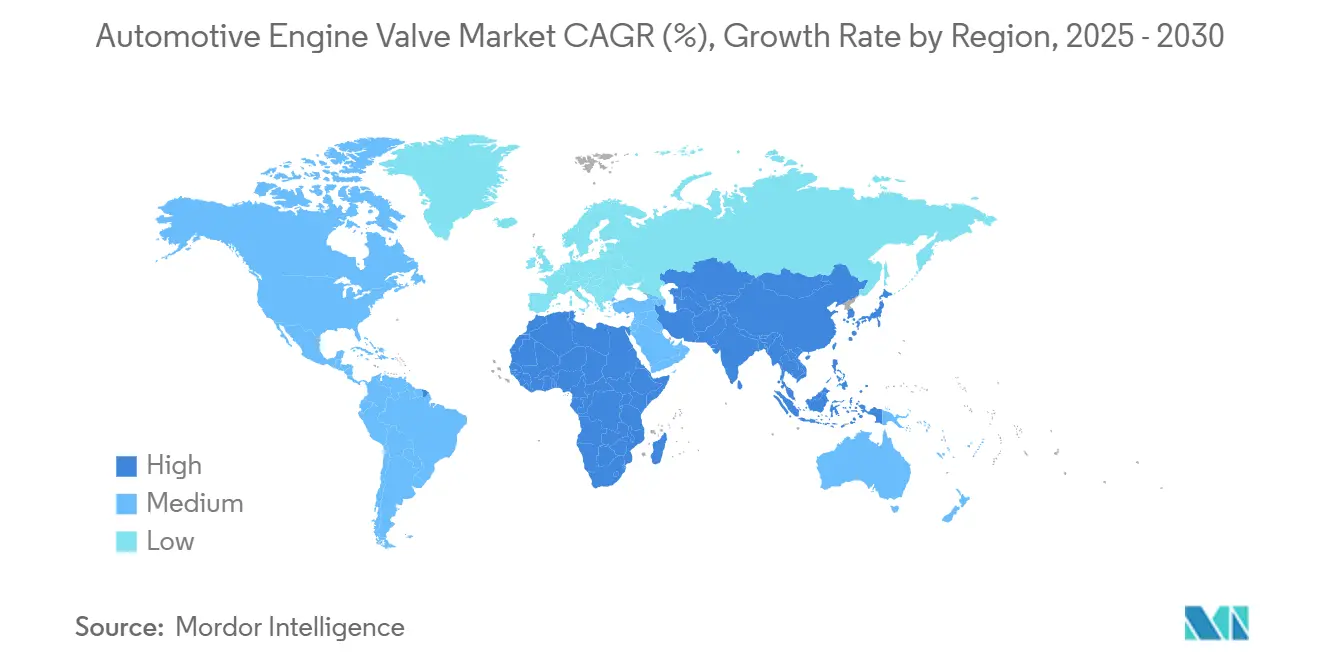

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

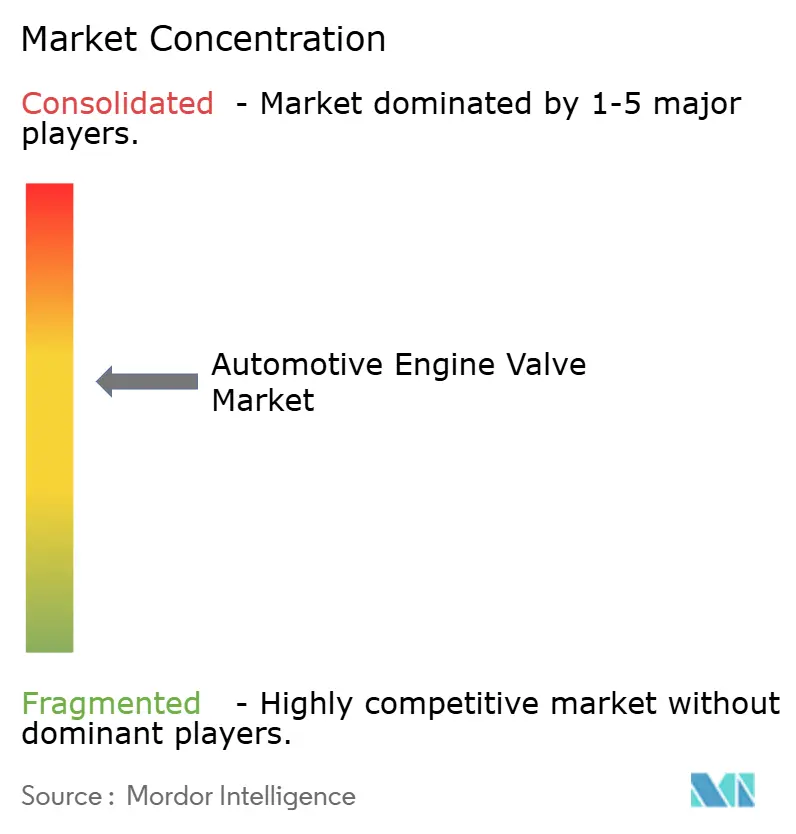

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Engine Valve Market Analysis by Mordor Intelligence

The automotive engine valve market size reached USD 5.81 billion in 2025 and, on a modest 0.91% CAGR, is forecast to reach USD 6.08 billion by 2030, highlighting a maturing landscape even as hollow-stem innovation and smart valve electronics extend the life of internal-combustion components within hybrid powertrains. Hollow valves, titanium alloys, and sensor-enabled designs are helping original-equipment suppliers defend relevance against rising electrification, while regional micro-machining and near-sourcing strategies build supply-chain resilience in Asia-Pacific and Mexico. Meanwhile, aftermarket distributors see fresh opportunities as aging fleets in emerging markets demand replacement parts, offsetting OEM volume deceleration linked to battery-electric penetration. Overall, the automotive engine valve market continues to pivot toward premium materials, digital monitoring, and sustainability-driven recyclability mandates, even as top-line growth remains subdued.

Key Report Takeaways

- By valve type, mono-metallic products retained 59.15% of the automotive engine valve market share in 2024, whereas hollow variants are forecast to expand at a 1.25% CAGR through 2030.

- By function, intake valves led the automotive engine valve market with a 64.21% share in 2024; exhaust valves are projected to rise at a 2.08% CAGR by 2030.

- By material, steel commanded 61.46% of the automotive engine valve market share in 2024, while titanium is expected to grow at a 4.03% CAGR through 2030.

- By vehicle type, passenger cars comprised 52.33% of the automotive engine valve market share in 2024; medium and heavy commercial vehicles will post the fastest 4.66% CAGR to 2030.

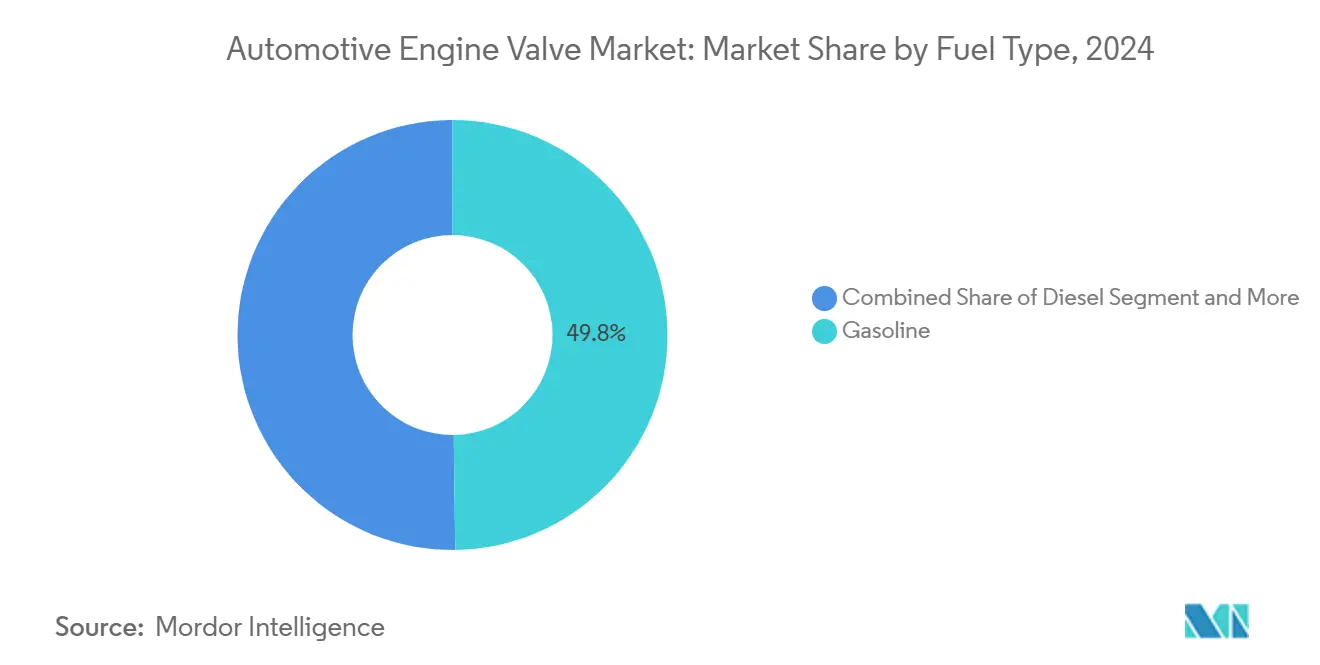

- By fuel type, gasoline held a 49.75% of the automotive engine valve market share in 2024, whereas CNG/LPG applications will accelerate at a 3.14% CAGR over the same period.

- By distribution channel, OEMs accounted for 73.44% of the automotive engine valve market share in 2024, yet the aftermarket will advance at a 3.74% CAGR to 2030.

- By geography, Regionally, Asia-Pacific dominated with a 44.26% of the automotive engine valve market share in 2024 and is expected to log the quickest 2.66% CAGR through 2030.

Global Automotive Engine Valve Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Rising Vehicle Production | +0.3% | APAC core, MEA spill-over | Medium term (2-4 years) |

| Regulations Drive Emission, Fuel-Efficiency | +0.2% | Global, EU, and North America lead | Long term (≥ 4 years) |

| Engine Downsizing and Turbocharging | +0.2% | North America and the EU, expanding APAC | Medium term (2-4 years) |

| Expansion Of CNG/LPG Fleets | +0.1% | India, China, the Middle East | Long term (≥ 4 years) |

| Regional Micro-Machining and Near-Sourcing | +0.1% | APAC manufacturing hubs | Short term (≤ 2 years) |

| Smart Valves Use Predictive Maintenance | +0.1% | North America and EU early; APAC scale | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Vehicle Production

China produced approximately 31.28 million vehicles in 2024, and growing premium-segment output is increasing valve content per vehicle, particularly hollow-stem designs that dissipate turbocharged heat more effectively. Southeast-Asian and Mexican assembly hubs compound demand as OEMs favor localized sourcing to manage logistics risk. Collectively, these patterns support incremental growth for the automotive engine valve market even in the face of electrification.

Stringent Emission and Fuel-Efficiency Regulations

Euro 7 and aligned North American rules force nickel-based and advanced stainless-steel alloys that survive high exhaust temperatures while guaranteeing million-mile durability cycles. Suppliers such as Federal-Mogul answer with ECMS-2512NbN austenitic steel, maintaining compliance at lower cost than super-alloys. Tighter real-world testing widens the opportunity for variable-valve-timing hardware that boosts efficiency.

Engine Downsizing and Turbocharging Trends

Smaller displacement paired with higher boost has reignited demand for lightweight titanium valves in premium performance cars. Hollow-stem designs integrate with variable cam systems such as Schaeffler’s iFlexAir, which is reported to cut diesel CO₂ by 5% and hydrogen combustion fuel use by 6%. The integration of electro-hydraulic actuation transforms valves from passive to smart energy-management nodes.

CNG/LPG Fleet Expansion in Asia and MEA

Indian CNG vehicle sales reported a 33% year-over-year increase in H12024, and China’s growing penetration of LNG trucks in heavy-duty segments demands corrosion-resistant seat coatings and gas-tight faces. This alternative-fuel agenda underscores why the automotive engine valve market continues to innovate around exotic metallurgy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Powertrain Electrification | -0.2% | Global, EU, and China lead | Long term (≥ 4 years) |

| Titanium, Nickel Price Volatility | -0.2% | Global, concentrated mining | Medium term (2-4 years) |

| Counterfeit Aftermarket Valves | -0.1% | Emerging markets | Short term (≤ 2 years) |

| Bimetallic Valve Recycling Compliance | -0.1% | EU lead; developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Power-Train Electrification

While BEV adoption removes the need for valves, hybrids keep demand alive via dual-power architectures; BorgWarner’s strategy balances conventional turbocharger contracts through 2028 alongside EV growth investments [1]“BorgWarner 2025 Strategy Update,” BorgWarner, borgwarner.com. Region-specific electrification rates encourage portfolio segmentation to preserve revenue streams for the automotive engine valve market.

Titanium and Nickel Alloy Price Volatility

In recent years, titanium prices have experienced a notable increase, with expectations of continued growth in the coming years, putting pressure on margins for suppliers of high-performance valves. Nickel swings add uncertainty, compelling contingency sourcing and alloy substitution strategies that still meet endurance targets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Valve Type: Hollow Innovation Drives Premium Shift

The automotive engine valve market measured mono-metallic leadership at 59.15% in 2024, while hollow-stem alternatives are tracking a 1.25% CAGR that will nudge the market toward higher average selling prices. Small internal cavities dissipate exhaust heat and shed grams, critical for downsized turbocharged blocks where every degree of thermal margin matters.

Cross-wedge rolling and precision forging are bringing cost parity closer to mainstream thresholds. Ferrea’s hollow-stem steel and Mitsubishi Heavy Industries’ hollow-head variants in Nissan GT-R powertrains validate commercial feasibility. As regional micro-machining spreads, hollow valves will reach mid-range vehicles, elevating functional sophistication without drastic price spikes.

By Function Type: Exhaust Valve Innovation Accelerates

Intake valves held a 64.21% share of the automotive engine valve market in 2024, reflecting higher unit counts and more frequent service intervals. Exhaust counterparts, however, are racing forward at a 2.08% CAGR as peak gas temperatures exceed 950 °C in modern turbo engines. The automotive engine valve market benefits from nickel-enriched steel like ECMS-Ni36, which balances oxidation resistance and cost for commercial diesels.

Weight-critical sports cars lean on titanium exhaust valves to counter high-rpm inertia, while variable valve timing widens duty cycles and fosters precision emissions control. In commercial fleets, exhaust gas recirculation valves ordered by Rheinmetall for a 2026-2031 contract reveal how durability wins OEM favor [2]“Rheinmetall Wins Large-Scale EGR Valve Order,” Rheinmetall, rheinmetall.com.

By Material Type: Titanium Gains Performance Traction

Steel dominates with 61.46% of 2024 revenue, yet titanium’s 4.03% CAGR signals a migration to lightweight, high-temperature materials that raise the automotive engine valve market value proposition. Grade 23 Ti-6Al-4V ELI delivers twice the strength-to-weight of steel and resists oxidation to 800 °C, appealing to premium gasoline and track-day applications.

Additive manufacturing facilitates complex internal cooling channels, minimizing waste and trimming costs. Katech sells titanium valves for GM LT engines at USD 224.99 each, proving end-buyers will pay for measurable performance gains [3]“Titanium Valves for GM LT,” Katech Engines, katechperformance.com . Nickel alloys remain niche but indispensable for marine diesels and off-road heavy equipment facing continuous 1,000 °C exhaust streams.

By Vehicle Type: Commercial Vehicles Drive Growth

Passenger cars dominated the automotive engine valve market with 52.33% of its revenue in 2024, yet medium and heavy trucks will outpace at 4.66% CAGR, buoyed by logistics expansion and stricter NOx rules in China, India, and the EU. The automotive engine valve market responds with steel-titanium hybrids that preserve cost while raising the thermal ceiling.

Extended duty cycles mean more frequent replacement, boosting aftermarket pull. Federal-Mogul targets 10–16 liter blocks above 500 hp, spotlighting how durability counts when engines idle for hours in congested ports or construction sites. Light commercial vans sit between cost pressure and uptime demand, prompting mixed-metal choices.

By Fuel Type: Alternative Fuels Create Specialization

Gasoline still controlled the automotive engine valve market with a 49.75% share in 2024, but CNG/LPG valve sets will climb 3.14% CAGR, driving the market toward corrosion-resistant seat metals. India’s fleet volume and China’s LNG truck mix drive engineering around embrittlement and gas leakage safety.

Hydrogen internal-combustion pilots, enabled by Schaeffler’s 50-bar injection, need coatings that tolerate H₂ embrittlement. Diesel remains vital in off-highway and long-haul classes, though low-carbon regulations intensify exhaust after-treatment complexity, indirectly elevating valve durability needs.

By Distribution Channel: Aftermarket Opportunities Expand

OEM pipelines captured 73.44% of the automotive engine valve market in 2024 invoices, given stringent homologation demands, yet aging fleets push the aftermarket to a 3.74% CAGR. The automotive engine valve market sees e-commerce portals simplifying rural access to branded replacements and telematics alerts synchronizing parts procurement.

Counterfeit avoidance spurs QR-code serialization and blockchain manifests, differentiating legitimate brands. Consolidators merging distribution and remanufacturing secure economies of scale, while small importers face rising compliance costs under recycled-content mandates.

Geography Analysis

Asia-Pacific led the automotive engine valve market with a 44.26% slice in 2024 and a 2.66% CAGR outlook through 2030. China’s vehicle output anchors volume, whereas India’s CNG surge ensures niche product strength. Regional micro-machining hubs in Thailand and Indonesia foster hollow-stem scale-up while cutting shipping risk.

North America preserves premium leadership via titanium and IoT-enabled smart valves. BorgWarner extended turbocharger supply contracts with U.S. OEMs into 2028, underscoring ICE relevancy despite battery uptake. Mexico’s near-shoring drives midsized-vehicle assembly, supporting regional valve sourcing. Europe pairs stringent Euro 7 limits with circular-economy recycling rules. Supply contracts like Rheinmetall’s six-year EGR valve deal illustrate stable demand for emission-control hardware that meets durability and recyclability quotas. Western OEMs pilot blockchain traceability to certify alloy provenance for decarbonization accounting.

Middle East & Africa expand slowly from a small base, aided by price-sensitive LPG taxis and LNG heavy trucks. Limited component supply chains encourage imports and open doors for localized machining if policy incentives materialize. Oil-industry valve metallurgy in Saudi Arabia can transfer know-how to the automotive fields, bolstering regional self-reliance prospects over the decade.

Competitive Landscape

Competitive intensity is moderate; the top suppliers are Eaton, Mahle, BorgWarner, Federal-Mogul, and Rheinmetall. They emphasize alloy design, surface treatments, and electromechanical actuation instead of price wars. Eaton’s sodium-filled hollow valves elevate heat conductivity, while Mahle invests in e-valve launches for camless concept cars.

Patent filings around camless rotary valve trains from LSP Innovation Automotive Solutions signal disruptive potential. LSP’s RVT eliminates camshafts, using electric-motor actuation to vary lift continuously, promising significant fuel savings and near-zero pumping losses. Smaller Asian entrants deploy incremental cost advantages, relying on regional micro-machining to secure tier-2 OEM contracts.

Strategic mergers surface: Mahle acquired Kokusan Denki’s valvetrain sensor business in 2024, aligning with predictive-maintenance ambitions. BorgWarner partners with semiconductor firms to embed pressure sensors in stainless-steel valve heads, pursuing data-rich service models. Meanwhile, counterfeit mitigation pushes market leaders toward digital watermarking and cloud-hosted authentication to safeguard brand equity.

Automotive Engine Valve Industry Leaders

Eaton Corporation

Mahle GmbH

BorgWarner Inc.

Fuji Oozx Inc.

Federal-Mogul (Tenneco)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Rheinmetall confirmed full-scale exhaust-gas-recirculation valve production from January 2026 under a six-year OEM contract, plus an added 15-year spare-parts supply window.

- August 2024: The U.S. NHTSA disclosed a Ford recall of 90,736 vehicles featuring 2.7 L and 3.0 L Nano EcoBoost engines because intake valves risk fracture during operation.

Global Automotive Engine Valve Market Report Scope

| Mono-metallic Valves |

| Bi-metallic Valves |

| Hollow Valves |

| Intake Valves |

| Exhaust Valves |

| Steel |

| Titanium |

| Nickel-based Alloys |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

| Buses and Coaches |

| Gasoline |

| Diesel |

| CNG/LPG |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East & Africa |

| By Valve Type | Mono-metallic Valves | |

| Bi-metallic Valves | ||

| Hollow Valves | ||

| By Function Type | Intake Valves | |

| Exhaust Valves | ||

| By Material Type | Steel | |

| Titanium | ||

| Nickel-based Alloys | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (MHCVs) | ||

| Buses and Coaches | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| CNG/LPG | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the automotive engine valve market size in 2025?

The market stands at USD 5.81 billion in 2025 and is projected to reach USD 6.08 billion by 2030.

Which material segment is growing fastest?

Titanium valves are expanding at a 4.03% CAGR due to superior strength-to-weight performance in turbocharged engines.

How big is Asia-Pacific’s share of global demand?

Asia-Pacific held 44.26% of 2024 revenue and will log the quickest 2.66% CAGR through 2030.

What is driving aftermarket growth?

An aging global fleet combined with longer service lifecycles is pushing the aftermarket channel toward a 3.74% CAGR to 2030.

Page last updated on: