Automotive Valves Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 27.73 Billion |

| Market Size (2031) | USD 29.17 Billion |

| Growth Rate (2026 - 2031) | 1.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Valves Market Analysis by Mordor Intelligence

The Automotive Valves market size is expected to grow from USD 27.45 billion in 2025 to USD 27.73 billion in 2026 and is forecast to reach USD 29.17 billion by 2031 at 1.02% CAGR over 2026-2031. Demand holds steady because internal-combustion engines (ICEs) remain dominant in commercial fleets, while battery-electric and hybrid models add new thermal-management circuits that require precision valves. Turbo-penetration, Euro 7 and EPA 29 emissions mandates, and over-the-air (OTA) diagnostics accelerate the shift toward smart, heat-resistant components.

Key Report Takeaways

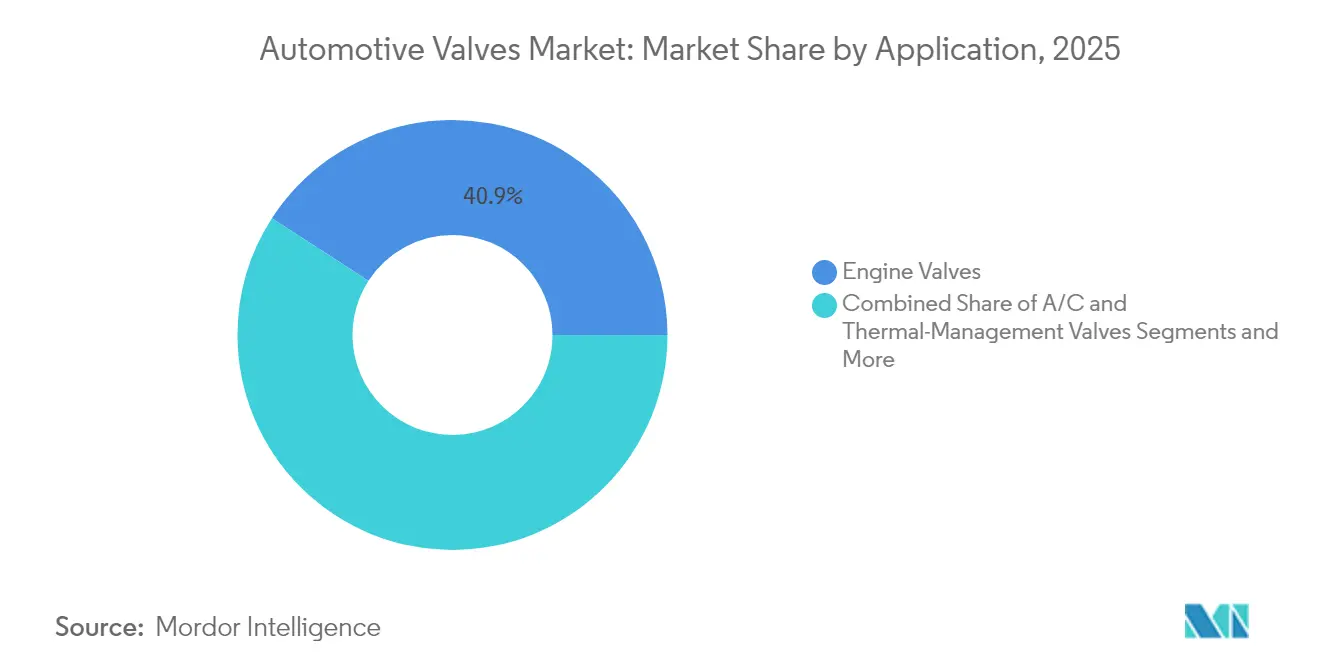

- By application, engine valves led with 40.87% revenue share of the automotive valves market in 2025, while electric coolant valves are projected to grow at 6.82% CAGR to 2031.

- By vehicle type, passenger cars held 71.12% of the automotive valves market share in 2025; medium and heavy commercial vehicles recorded the fastest CAGR at 2.06% through 2031.

- By function, hydraulic valves accounted for 43.12% share of the automotive valves market size in 2025, and electric/solenoid valves are advancing at 1.69% CAGR to 2031.

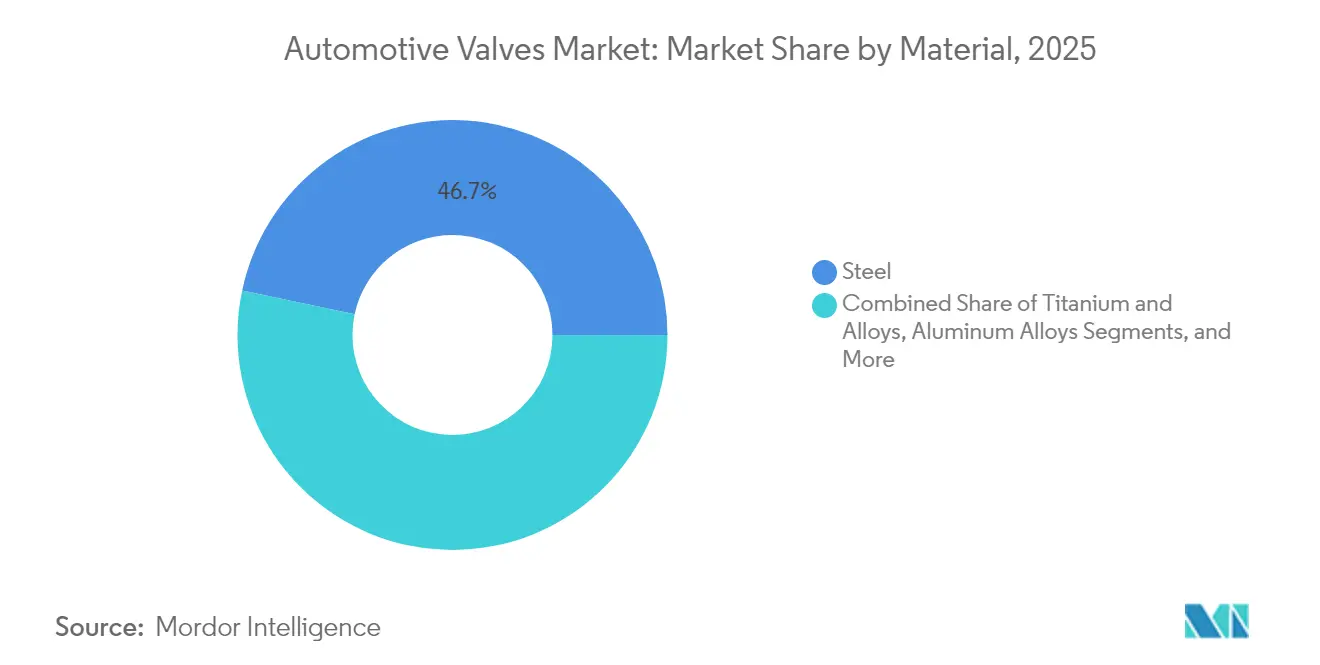

- By material, steel represented 46.68% share of the automotive valves market size in 2025; titanium and alloy valves expand at 1.52% CAGR through 2031.

- By propulsion type, internal combustion engine represented 77.62% share of the automotive valves market size in 2025; hybrid powertrains (HEV/PHEV) expand at 1.78% CAGR through 2031.

- By sales channel, the OEM channel accounted for 75.74% of the automotive valves market share in 2025, while the aftermarket is projected to expand at a 1.31% CAGR through 2031.

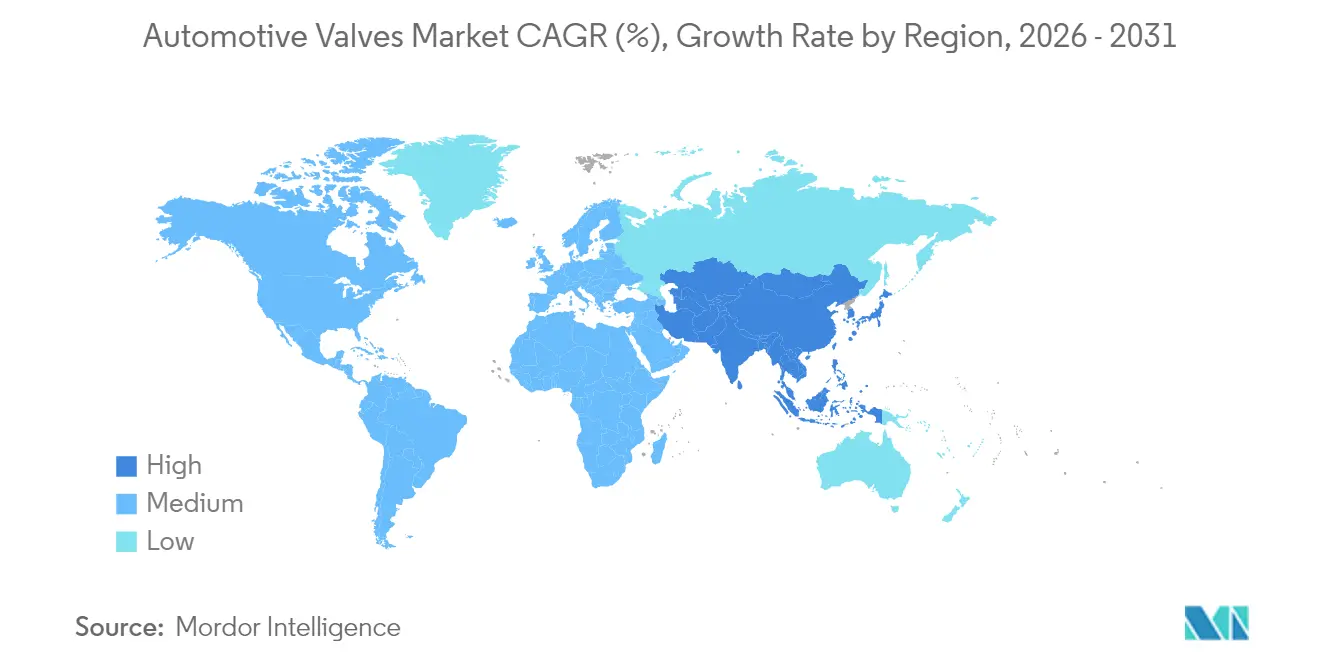

- By geography, Asia–Pacific commanded 52.01% revenue share in 2025, while the same region posts a 3.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Valves Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrified Thermal-management Architecture Boom | +0.25% | Global, led by China and Europe | Long term (≥ 4 years) |

| ICE Downsizing and Turbo-penetration | +0.20% | Global, strongest in Europe and China | Medium term (2-4 years) |

| Tightening Euro 7/EPA 29 norms | +0.15% | Europe and North America, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Smart valves with OTA Diagnostics | +0.12% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Hydrogen-ICE Pilots in CV Segment | +0.08% | Europe and North America, trials in Japan | Long term (≥ 4 years) |

| Localization Mandates in India and Indonesia | +0.06% | Asia-Pacific core, India and Indonesia focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Electrified Thermal-management Architecture Boom

Battery electric and hybrid vehicles require sophisticated thermal management systems that create entirely new valve applications beyond traditional ICE cooling circuits. Electric coolant valves emerge as the fastest-growing segment at 7.25% CAGR, driven by the need to manage battery pack temperatures, power electronics cooling, and cabin heating without engine waste heat. Rheinmetall's advanced coolant valve portfolio demonstrates the technical complexity required, featuring demand-based control and low flow resistance designs optimized for hybrid and electric vehicle applications. The integration of multiple cooling circuits in EVs battery, motor, power electronics, and cabin requires precise valve coordination that traditional ICE systems never demanded. Sanhua Automotive's specialization in thermal expansion valves, electric expansion valves, and refrigerant solenoid valves illustrates the market's evolution toward integrated thermal solutions

ICE Downsizing and Turbo-penetration

Smaller displacement engines dominate new passenger-car programs in Europe and China, and turbochargers heighten operating temperatures. Premium titanium alloys resist these thermal loads and enable tighter valve-timing windows that help manufacturers comply with Euro 7 and EPA 29. Cummins introduced a hydrogen-ICE turbocharger in April 2025 that illustrates how boosting technology migrates to alternative fuels, blending conventional valve know-how with new combustion demands, and lifting average unit prices across the automotive valves market.

Tightening Euro 7/EPA 29 norms

Starting November 2026, Euro 7 extends regulatory durability to 8 years/160,000 km and mandates onboard monitoring. Exhaust-gas-recirculation (EGR) valves must now survive longer exposure to corrosive gases, prompting OEMs to specify stainless steels with high chromium content and invest in variable valve-timing (VVT) systems that cut nitrogen-oxide peaks X. North America’s heavy-duty EPA 29 standard mirrors these targets for the 2027 model year, so suppliers that engineer cross-regional platforms gain scale advantages.[1]"International Council on Clean Transportation", Automotive Industry Trend, theicct.org.

Smart Valves with OTA Diagnostics

Sensors, near-field communication chips, and dual-core microcontrollers turn valves into data nodes. Parker Hannifin’s DFplus Generation IV proportional valve logs cycle counts and sends alerts to the vehicle gateway, which can push firmware updates to recalibrate flow curves, reducing unexpected downtime for fleet operators. Smart valve adoption accelerates in premium segments first, then cascades to volume applications as costs decline and regulatory requirements for emissions monitoring intensify. The convergence of mechanical precision and digital intelligence creates differentiation opportunities for suppliers capable of integrating both domains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China Export-rebate Cuts on Pneumatic Sub-assemblies | –0.30% | China exports, global supply chains | Short term (≤ 2 years) |

| ICE-plant Repurposing in Europe 2027-30 | –0.15% | Europe, spill-over to North America | Medium term (2-4 years) |

| Nickel and Titanium Price Super-cycle | –0.10% | Global supply chains | Medium term (2-4 years) |

| BEV Electronics Replacing Multiple Valve Sets | –0.08% | Global, strongest in China & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nickel and Titanium Price Super-cycle

Material cost inflation creates significant margin pressure for valve manufacturers, particularly those utilizing premium alloys in high-performance applications. Titanium and alloy valves, despite representing the fastest-growing material segment at 5.55% CAGR, face cost headwinds that may limit adoption in price-sensitive applications. The automotive industry's increasing reliance on advanced materials for lightweighting and performance enhancement coincides with supply chain constraints and geopolitical tensions affecting raw material availability. U.S. countervailing duties on aluminum extrusions from China, including automotive components, exemplify how trade policies compound material cost pressures.[2]“The Daily Journal of the United States Government”, Federal Register, www.federalregister.gov.

BEV Electronics Replacing Multiple Valve Sets

Battery-electric vehicles eliminate fuel, EGR, and crankcase-ventilation valves, cutting lifetime part demand even as they add thermal-management circuits. With BEVs projected to reach 56% of new light-duty sales by 2032, many traditional valve lines face volume declines, challenging Tier 2 suppliers to redeploy tooling or exit the automotive valves market. While BEVs create new opportunities in thermal management valves, the volume and value potential cannot fully offset the loss of high-volume ICE applications like intake and exhaust valves. The timing of this transition varies by region, with China leading BEV adoption and Europe following aggressive electrification mandates, while North America and emerging markets maintain ICE dominance longer. Suppliers must navigate this transition carefully, balancing continued ICE investment with BEV capability development to avoid stranded assets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Engine Valves Hold Scale While Coolant Valves Accelerate

Engine valves generated the largest revenue slice in 2025, equal to 40.87% of the automotive valves market. Turbocharged downsized engines, cylinder-deactivation strategies, and VVT upgrades keep intake and exhaust valves critical, yet electric coolant valves deliver a 6.82% CAGR because every hybrid or BEV needs multi-loop thermal control. End-users now pay premiums for wear-resistant face coatings and sodium-filled stems that mitigate hot-spot formation under turbo boost.

Digital twins simulate flow across motor, battery, and cabin loops. This integration forces coolant valve makers to embed temperature and pressure sensors, adding electronics content per unit. Conversely, demand for fuel-injection valves softens in BEVs but persists in plug-in hybrids and emerging hydrogen-ICE programs. The re-mix of combustion and electric requirements expands lifetime value per vehicle even as overall unit volumes migrate.

By Vehicle Type: Commercial Fleets Sustain Growth

Passenger cars represented 71.12% of the automotive valves market revenue in 2025, yet medium and heavy commercial vehicles locked in the highest 2.06% CAGR. Long-haul trucking retains diesel and hydrogen-ICE routes that use robust valve chemistries and longer duty-cycle designs. Hydrogen pilot fleets from MAN and Cummins demand modified seats and stem coatings to accommodate higher water content and combustion variability. Commercial duty cycles require extended service intervals, sometimes 40,000 operating hours, so fleet operators prioritize predictive diagnostics embedded in valve firmware.

Urban bus and delivery fleets electrify fastest, but heavy tractors and construction machinery rely on ICE optimization, prolonging demand for turbo waste-gate valves, EGR, and after-treatment actuators. Passenger-car architectures converge on small-displacement hybrids, cutting high-flow valve counts yet adding electronic coolant modules that offset some volume losses .

By Function: Electric Solenoids Outpace Hydraulic Mainstays

Hydraulic valves retained 43.12% revenue share in 2025 and populate brake boosters, steering racks, and transmission control units. Electric and solenoid valves jump 1.69% CAGR because OTA-enabled intelligence, duty-cycle monitoring, and linear positioning accuracy appeal to OEMs shifting toward software-defined vehicles. Dual-coil, direct-acting solenoids now handle rapid switching in integrated thermal-management modules, replacing multiple mechanical valves and reducing leak paths.

Hybrid actuation blends electro-hydraulic principles to minimize energy draw and meet cybersecurity rules. The function spectrum thus blurs, but electronically commutated solenoids capture outsized value in advanced powertrains and elevate average selling prices in the automotive valves market.

By Material: Steel Is Ubiquitous, Premium Alloys Gain Share

Cost-efficient steel controlled 46.68% of the automotive valves market revenue in 2025. Alloyed steels remain the default for intake and exhaust duties, yet titanium and nickel-based alloys notch a 1.52% CAGR thanks to turbo-era heat loads and mass-reduction targets. Lightweight multiphase steels offer middle-ground solutions for valves that balance price and performance, while ceramics emerge for select high-abrasion duties. Trade-driven price volatility encourages OEMs to dual-source raw materials and explore additive-manufacturing routes for near-net-shape valve heads.

Recyclability and lifecycle carbon metrics influence material choice. Closed-loop steel scrap programs help OEMs meet ESG targets, while titanium recycling remains nascent, limiting widespread use outside premium segments.

By Propulsion: Hybrid Complexity Drives Premium Demand

Internal combustion engine applications dominate the automotive valves market with approximately 77.62% share in 2025, reflecting the continued prevalence of traditional powertrains across global vehicle production, while hybrid powertrains (HEV/PHEV) represent the fastest-growing segment at 1.78% CAGR through 2031. Hybrid systems require sophisticated valve architectures that combine traditional ICE components with advanced thermal management solutions for battery cooling, electric motor temperature control, and integrated cabin heating systems.

ICE applications face gradual market share erosion as electrification mandates intensify, particularly in European and Chinese markets where regulatory pressures accelerate the transition timeline. However, commercial vehicle segments maintain strong ICE demand due to payload and range requirements that favor diesel and emerging hydrogen combustion technologies. Hybrid powertrains benefit from regulatory incentives and consumer acceptance as a bridge technology, with plug-in hybrid variants requiring the most sophisticated valve systems due to their dual-mode operation capabilities.

By Sales Channel: Aftermarket Remains Essential

OEM programs accounted for 75.74% of the 2025 automotive valves market sales, but the aftermarket posts a 1.31% CAGR on the back of older vehicle fleets and multi-platform part commonality. Independent workshops depend on modular valve kits with integrated sensors to service modern powertrains. European consumers keep vehicles for 12 years on average, sustaining demand for replacement exhaust control and high-pressure fuel pump valves that meet Euro 7 durability. In North America, ride-share and delivery fleets pursue preventive maintenance, boosting smart valve retrofits that unlock condition-based service intervals.

EV adoption will eventually curb ICE-specific aftermarket volumes, yet new battery-coolant valves and refrigerant solenoids open fresh categories. Regional e-commerce portals favor tier-two suppliers who bundle diagnostic software alongside physical parts, preserving margins even as distribution structures evolve.

Geography Analysis

Asia–Pacific occupied 52.01% of the 2025 automotive valves market revenue. China’s localization rules and India’s 100% FDI policy anchor investment, while Thailand and Vietnam build supply-chain depth for regional OEM hubs. Hyundai’s USD 3 billion India plan underscores long-term confidence in local valve production, and Indonesia’s export incentives attract pneumatic assembly lines. Cost competitiveness plus vast domestic demand safeguard Asia-Pacific growth despite geopolitical risk. Asia-Pacific is anticipated to witness the fastest growth at 3.08% CAGR during the forecast period.

South America is expected to witness prominent demand for automotive valves. Stellantis’ Brazilian Real 30 billion Brazil project and BYD’s USD 1 billion Turkish plant highlight OEM interest in cost-effective manufacturing zones proximal to raw materials. Brazil’s Rota 2030 program offers tax breaks for low-emission technologies, motivating suppliers to install EGR and coolant-valve production cells. Argentina’s component-localization push widens supplier footprints, balancing currency volatility.

Europe and North America are mature but innovation-intensive. Euro 7 and EPA 29 spark investment in advanced EGR and VVT valves across Germany, France, and the United States. Turkey prospers as a bridge market, having produced 1.4 million vehicles in 2023 and ranking first in European commercial-vehicle output. Middle East & Africa gains traction, led by Saudi Arabia’s USD 2.9 billion 2024 automotive cluster that includes EV cooling-valve lines targeting regional export corridors.

Competitive Landscape

The supply base remains moderately fragmented. Denso, Bosch and BorgWarner leverage extensive ICE portfolios while channeling R&D toward smart thermal-management valves and hydrogen-ready hardware. BorgWarner’s “Charging Forward” targets USD 10 billion EV revenue by 2027, evidencing capital redeployment without abandoning profitable turbo and EGR lines.

Medium players like Valeo and Pierburg specialize in coolant and vacuum valves, partnering with semiconductor vendors to embed diagnostics. Continental’s planned 2025 spin-off of its Automotive unit signals portfolio focus, echoing Aptiv’s earlier electronics tilt. Digital factory programs, such as Continental’s DIAZI, trim lead times and enhance traceability, critical for Euro 7 warranty compliance.

Consolidation accelerates as raw-material inflation and software investments strain smaller Tier 2 suppliers. Recent private-equity deals, including Apollo Fund X’s injection into Tenneco’s clean-air division, give cash-intensive valve programs breathing room for retooling. White-space opportunities cluster around hydrogen-ICE airflow control, integrated thermal-management modules, and OTA-upgradable solenoid valves.

Automotive Valves Industry Leaders

-

Denso Corporation

-

BorgWarner Inc.

-

Robert Bosch GmbH

-

Valeo SE

-

AISIN Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Robert Bosch, LLC announced the addition of 82 automotive aftermarket part numbers across multiple product categories in the first quarter of 2025, expanding coverage to nearly 63 million vehicles in operation. The new part numbers expanded the company's range of sensors, brakes, ignition coils, spark plugs, fuel injectors, valves, and A/C compressors.

- February 2025: Tenneco secured Apollo Fund X investment to scale powertrain valve production and Industry 4.0 upgrades.

- July 2024: Valeo expanded its EGR valve portfolio by introducing 46 new references, bringing its original equipment manufacturing expertise to the automotive aftermarket.

Global Automotive Valves Market Report Scope

Automotive valves are the mechanical component that is used in an internal combustion engine which allows the flow of fuel in and out through the engine cylinder during the operation.

The Automotive Valves Market is segmented by Application Type, vehicle type, function type, Sales channel, and geography. Based on the application type, the market is segmented into Engine Valves, Air Conditioning Valves, Fuel System Valves, EGR Valves, and Others. Based on the Vehicle Type, the market is segmented into Passenger Cars and Commercial Vehicles. Based on the Function Type, the market is segmented into Pneumatic, Hydraulic, and Electric. Based on the Sales Channel, the market is segmented into OEM and Aftermarket. Based on Geography, the market is segmented into North America, Europe, Asia Pacific, and the Rest of the World. For each segment, the market sizing and forecast have been done on the basis of value (USD Billion).

| Engine Valves | Intake Valves |

| Exhaust Valves | |

| Variable Valve-Timing Valves | |

| Cylinder-Deactivation Valves | |

| A/C and Thermal-Management Valves | Expansion Valves |

| Coolant Control Valves | |

| Fuel-System Valves | |

| EGR Valves | |

| Brake and Safety Valves (ABS, Proportioning) |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Pneumatic | Conventional |

| Smart Mechatronic | |

| Hydraulic | Direct-acting |

| Pilot-operated | |

| Electric / Solenoid | Stepper-motor |

| Steel |

| Titanium and Alloys |

| Aluminum Alloys |

| Ceramics and Composites |

| Internal-Combustion Engine (ICE) |

| Hybrid Powertrain (HEV/PHEV) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Turkey |

| Saudi Arabia | |

| UAE | |

| Israel | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Application Type | Engine Valves | Intake Valves |

| Exhaust Valves | ||

| Variable Valve-Timing Valves | ||

| Cylinder-Deactivation Valves | ||

| A/C and Thermal-Management Valves | Expansion Valves | |

| Coolant Control Valves | ||

| Fuel-System Valves | ||

| EGR Valves | ||

| Brake and Safety Valves (ABS, Proportioning) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Function Type | Pneumatic | Conventional |

| Smart Mechatronic | ||

| Hydraulic | Direct-acting | |

| Pilot-operated | ||

| Electric / Solenoid | Stepper-motor | |

| By Material Type | Steel | |

| Titanium and Alloys | ||

| Aluminum Alloys | ||

| Ceramics and Composites | ||

| By Propulsion | Internal-Combustion Engine (ICE) | |

| Hybrid Powertrain (HEV/PHEV) | ||

| Sales Channel | OEM | |

| Aftermarket | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Turkey | |

| Saudi Arabia | ||

| UAE | ||

| Israel | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the automotive valves market?

The market is valued at USD 27.73 billion in 2026 and is projected to reach USD 29.17 billion by 2031.

Which valve segment is expanding fastest?

Electric coolant valves show the highest 6.82% CAGR through 2031, driven by growth in battery-electric and hybrid thermal-management loops.

How will Euro 7 affect valve demand?

Euro 7 raises durability to 8 years/160,000 km and tightens NOx limits, lifting demand for premium EGR and VVT valves that resist corrosion and enable precise combustion control.

Why are commercial vehicles important for valve suppliers?

Medium and heavy commercial vehicles retain ICE powertrains longer and require robust, high-duty valves, posting the strongest 2.06% CAGR among vehicle types.

What role do smart valves play in modern powertrains?

Smart valves integrate sensors and OTA diagnostics, enabling predictive maintenance and precise flow control, supporting OEM moves toward software-defined vehicles.

How does material cost volatility influence valve design?

Rising nickel and titanium prices pressure margins and drive exploration of alternative alloys and additive-manufacturing approaches that balance cost with thermal performance.

Page last updated on: