Automotive Camshaft Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

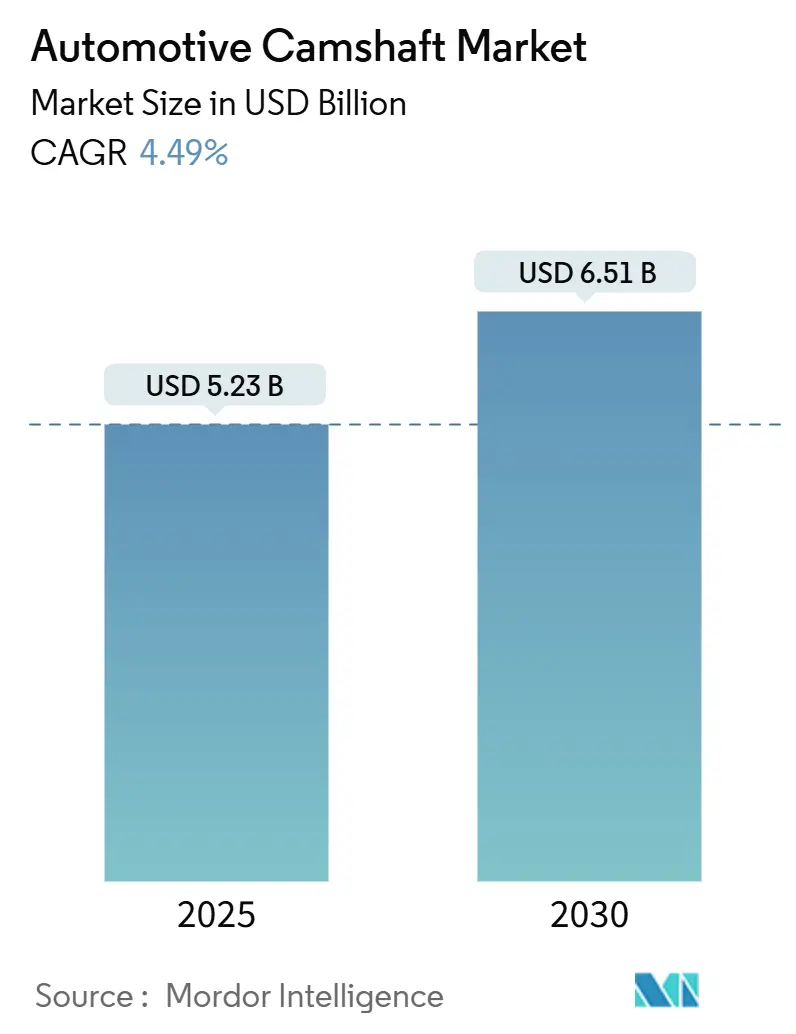

| Market Size (2025) | USD 5.23 Billion |

| Market Size (2030) | USD 6.51 Billion |

| Growth Rate (2025 - 2030) | 4.49% CAGR |

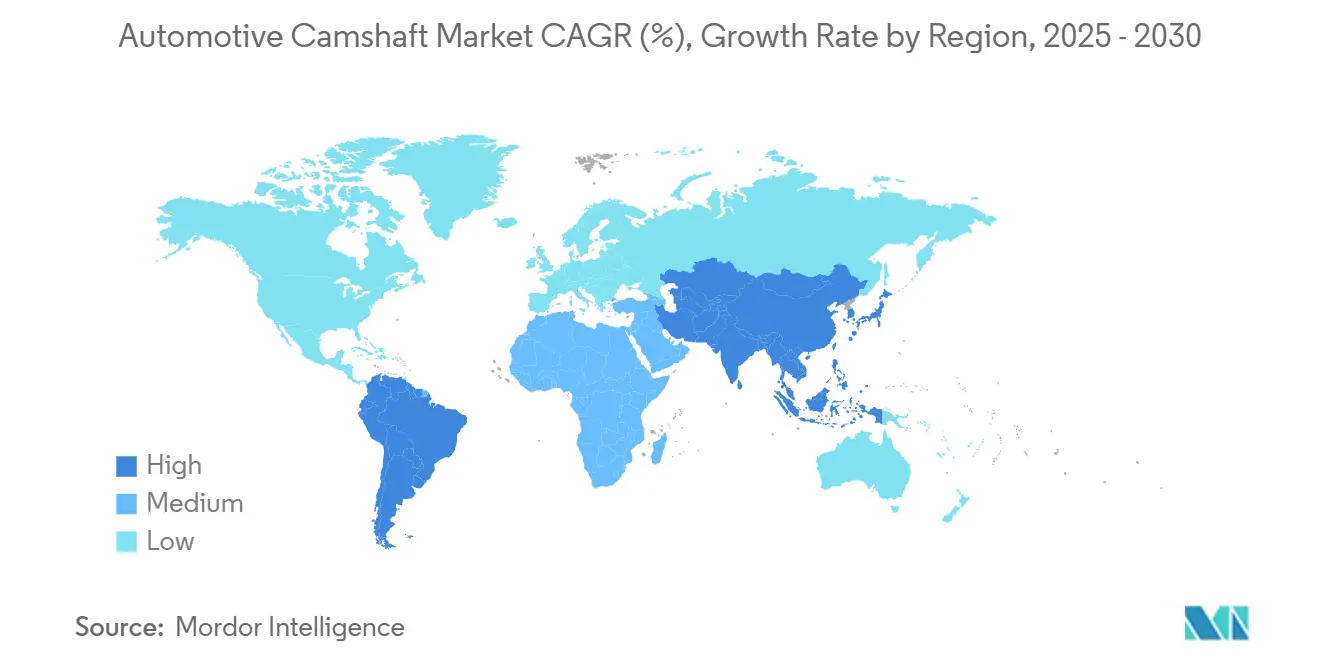

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Camshaft Market Analysis by Mordor Intelligence

The Automotive Camshaft market size stood at USD 5.23 billion in 2025 and is projected to advance at a 4.49% CAGR to USD 6.51 billion by 2030. Sustained demand for internal-combustion components, hybrid powertrain specification changes, and robust passenger-car output in Asia-Pacific underpin near-term expansion. Hybrid models keep camshaft content relevant even as battery-electric adoption grows unevenly across regions. Lightweight, hollow designs and precision machining strengthen average selling prices, while performance-aftermarket activity lifts value per unit. Suppliers that align capacity with Asia-centric vehicle production and hybrid-ready specifications are best placed to navigate the transition.

Key Report Takeaways

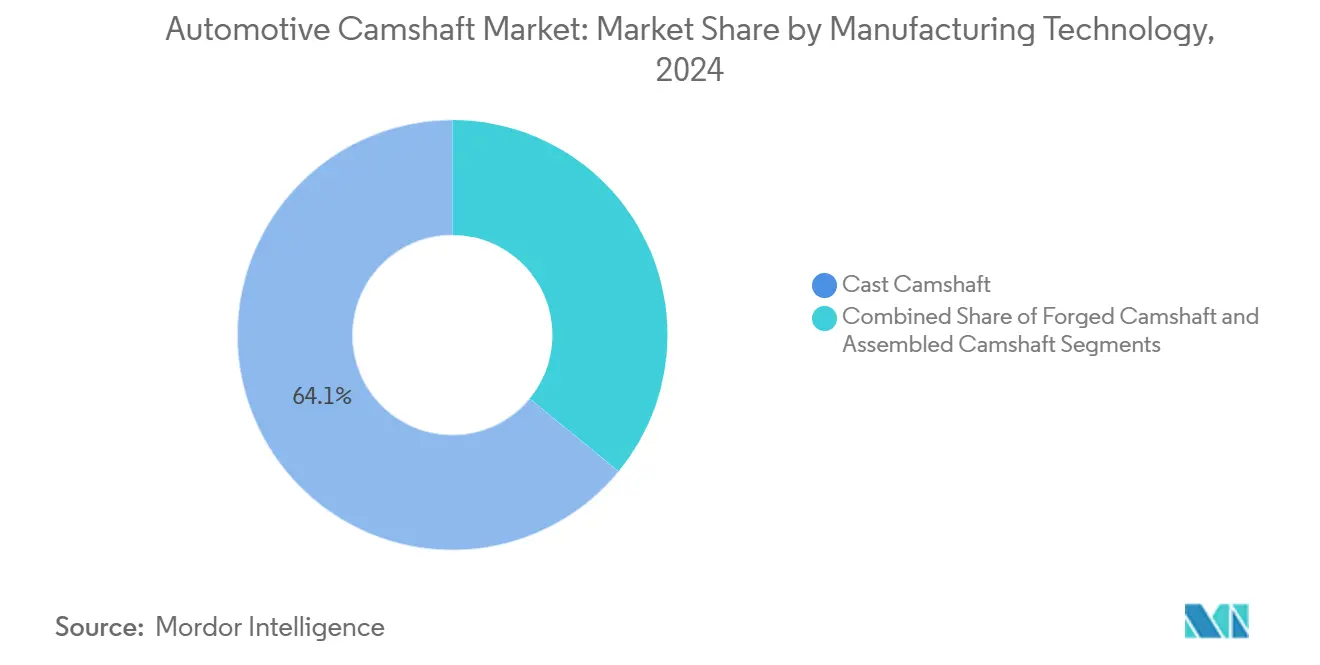

- By manufacturing technology, cast camshafts captured 64.07% of the Automotive Camshaft market share in 2024, whereas assembled camshafts are on track to grow at a 6.18% CAGR through 2030.

- By vehicle type, passenger cars held a 50.12% share of the Automotive Camshaft market size in 2024, while medium and heavy commercial vehicles are forecast to register the fastest 4.78% CAGR to 2030.

- By fuel type, gasoline engines dominated with a 73.37% of the Automotive Camshaft market share in 2024, and the gasoline-mild-hybrid subsegment is projected to expand at a 6.79% CAGR during the outlook period.

- By sales channel, OEM deliveries accounted for 81.63% of the Automotive Camshaft market share in 2024, yet the aftermarket is anticipated to post a 7.12% CAGR over the forecast horizon.

- By geography, Asia-Pacific commanded 45.47% of the Automotive Camshaft market share in 2024, whereas South America is set to be the fastest-growing region with a 5.87% CAGR to 2030.

Market Trends and Insights

Drivers Impact Analysis of Automotive Camshaft Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Passenger-Car and LCV Production | +1.8% | Global, with APAC core leadership | Medium term (2-4 years) |

| DOHC and VVT Architectures | +1.2% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Ageing Vehicle Parc | +0.9% | North America and Europe primarily | Short term (≤ 2 years) |

| Lightweight Hollow/Assembled Cams | +0.6% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Low-Cost Asian Outsourcing | +0.5% | APAC manufacturing, global supply impact | Medium term (2-4 years) |

| Performance-Tuning Boom | +0.3% | North America and Europe aftermarket focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Robust Growth in Global Passenger-Car and LCV Production

Global vehicle output remained resilient. Stable OEM build schedules ensure predictable camshaft volumes, and hybrids preserve valvetrain demand while pure BEV adoption remains geographically uneven. Light-commercial vehicle expansion tied to e-commerce logistics further supports load-bearing gasoline and diesel engines. The concentration of assembly plants in the Asia-Pacific region benefits suppliers near regional hubs, lowering freight costs and shortening lead times. These conditions give manufacturers a multi-year window to refine hybrid-ready product lines before BEV penetration materially erodes ICE volumes.[1]“China - Flash Report, Automotive Production Volume, 2024,” MarkLines, marklines.com

Widespread Adoption of DOHC and VVT Architectures

Dual overhead-cam and variable-valve-timing systems require additional camshafts and precision-machined phasers, raising content per engine. Automakers apply these architectures across segments to boost power density and compliance with stringent emissions rules. The technology shift elevates metallurgical requirements, opening opportunities for premium alloy billets and case-hardening services. Suppliers adept at tight-tolerance grinding capture higher margins as OEMs pay for incremental efficiency gains. Continued rollout across emerging economies sustains orders even as mature markets pivot toward hybrids.

Aging Vehicle Parc Fueling Replacement Demand

The average age of vehicles on U.S. roads surpassed 12 years in 2024, increasing the frequency of major engine rebuilds. Longer ownership cycles heighten demand for replacement camshafts, especially in performance-oriented models where wear accelerates. Aftermarket channels enjoy superior unit economics because pricing is less constrained by OEM cost-down initiatives. Distributors with broad SKU coverage and strong e-commerce presence can capture end-user sales directly. Stable replacement demand also buffers suppliers when new-vehicle production dips.

Lightweight Hollow/Assembled Cams for Hybrid Packaging

Hybrid powertrains intensify packaging constraints, making weight-optimized hollow camshafts attractive. Assembled designs cut mass by approximately 10-15% while permitting integrated oil galleries and sensor mounts, advantages have spurred a 6.18% CAGR outlook for the subsegment. These features align with automaker goals to offset battery weight and extend electric-only range. Early adopters in Japan, the United States, and European premium brands validate the technology, encouraging volume ramp-up and capital investment in friction-welded tubing lines.

Restraints Impact Analysis of Automotive Camshaft Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift to BEVs | -2.1% | Global, led by Europe and China | Long term (≥ 4 years) |

| Raw-Material Price Volatility | -0.8% | Global manufacturing impact | Short term (≤ 2 years) |

| Insourcing and Supply-Base Consolidation | -0.6% | North America and Europe focus | Medium term (2-4 years) |

| Cam-Less Valve-Actuation Technologies | -0.3% | Limited to premium segments initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to BEVs Cutting Long-Term ICE Volumes

Battery-electric vehicles dominated Chinese production in 2024, an advance that eliminates mechanical camshafts from entire powertrains. Similar regulations in Europe accelerate the decline of conventional engines, pressuring suppliers to diversify into hybrids or adjacent components. Plants dedicated to cast camshafts face capacity under-utilization after 2030 unless retooled for alternative products. Capital-intensive foundries carry heightened stranded-asset risk as automakers lock in EV investment cycles.

Raw-Material Price Volatility Squeezing Margins

Fluctuating steel prices create margin pressure for camshaft manufacturers, particularly affecting smaller suppliers with limited hedging capabilities and long-term contract protection. Raw material costs make price volatility a significant profitability risk. Specialty alloys for high-performance cams amplify exposure. Suppliers seek multi-year pricing clauses or index-linked contracts, but often concede margin in exchange for volume security. Inventory optimization and scrap-recycling initiatives partially offset volatility yet require disciplined execution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Automotive Camshaft Market Segment Analysis

By Manufacturing Technology:

Cast Dominance Faces Assembled InnovationThe Automotive Camshaft market size for cast products amounted to 64.07% of global revenue, reflecting mature tooling and low unit costs. High-volume passenger-car programs in Asia-Pacific preserve cast demand, and shared foundry capacity promotes scale economies. Forged camshafts occupy a smaller share, anchored in heavy-duty diesel engines where extreme fatigue resistance justifies premium pricing. Cost awareness in entry-level cars slows migration to pricier alternatives.

Assembled camshafts are forecast to log a 6.18% CAGR, outpacing the broader Automotive Camshaft market. Hollow tubes friction-welded to lobe packs shave up to 15% mass and allow internal oil galleries that improve lubrication. Hybrids benefit from these characteristics because reduced reciprocating mass mitigates NVH penalties from frequent stop-start events. Early adopters in Japan and Germany validate durability, encouraging capital investment in laser-welding and precision-fixturing lines.[2]"Abilities to drive revenue growth with patented technologies in new fiscal." Autocar Professional, segmenty.com

By Vehicle Type:

Passenger Cars Lead While Commercial Segments AcceleratePassenger cars generated 50.12% of the Automotive Camshaft market share in 2024, a position upheld by large-scale production in China, India, and ASEAN nations. Compact and midsize gasoline models rely on twin-cam architectures to meet fuel-economy norms. Electrification progress in Europe moderates growth, yet retrofit options and lower total-cost-of-ownership considerations sustain ICE preference in emerging economies. Suppliers utilize modular lobe designs to span volume programs without bespoke tooling.

Medium and heavy commercial vehicles are projected to achieve a 4.78% CAGR through 2030, lifted by infrastructure spending, commodity logistics, and inter-regional trade. Diesel engines persist due to torque demands and fueling infrastructure, making robust forged or chilled-cast camshafts indispensable. Fleet operators favor engines with extended overhaul intervals, driving interest in nitrided surfaces and enhanced bearing metallurgy. Aftermarket rebuild cycles add a lucrative second-life revenue stream.

By Fuel Type:

Gasoline Dominance With Hybrid IntegrationGasoline engines accounted for 73.37% of the Automotive Camshaft market share in 2024, supported by refining infrastructure availability, cost competitiveness, and performance characteristics aligning with consumer preferences. Direct injection and turbocharging raise stress levels, prompting suppliers to adopt higher-strength alloy castings. The Automotive Camshaft market size for gasoline-mild-hybrid systems is expected to expand, reflecting automaker strategies to improve fuel economy while retaining familiar ICE architecture and manufacturing infrastructure.

Diesel, growing at a 6.79% CAGR, concentrates in commercial vehicles and select pickup models, supporting steady but slower growth. Emissions after-treatment costs cap expansion into small passenger cars, yet heavy-duty applications still profit from superior fuel efficiency. Camshaft vendors serving diesel programs focus on induction-hardened lobes and micro-polished journals to counter elevated cylinder pressures. As hybrid integration gains traction, it brings forth new camshaft specifications, including heightened durability for start-stop operations, refined valve timing to sync with electric motors, and design tweaks to fit battery systems and electric drive components.

By Sales Channel:

OEM Stability Meets Aftermarket GrowthOEM channels maintain 81.63% of the Automotive Camshaft market size in 2024, providing volume stability and predictable demand patterns that support manufacturing scale economies and long-term supplier relationships essential for automotive industry participation. Standardization initiatives streamline part numbers, letting producers amortize tooling across global engine families. Price-down clauses and warranty liability compress margins, spurring investment in automation and inline quality inspection to cut costs.

The aftermarket is poised for a healthy 7.12% CAGR, lifted by an aging vehicle parc and enthusiast upgrades. E-commerce portals and social-media tutorials democratize access to performance cam kits, and specialized retailers bundle matched lifters and springs for end-user convenience. Higher average selling prices offset lower volumes, and direct-to-consumer models enhance profitability. Suppliers leverage rapid prototyping to refresh catalogues with niche grinds tailored to turbocharged engines.

Geography Analysis

APAC Automotive Camshaft Market

Asia-Pacific held 45.47% of the Automotive Camshaft market revenue in 2024, powered by China’s double-digit growth in India’s passenger-vehicle segment. Regional supply chains combine vertically integrated iron foundries with low-cost CNC finishing, leveraging local vendors' pricing. Japan and South Korea add high-precision capacity for premium engines, while Southeast Asia offers tariff-free export zones. Rapid NEV adoption in China poses a long-term threat, yet hybrids and export-oriented ICE production sustain near-term workloads. Policy incentives supporting domestic manufacturing further anchor camshaft demand.

South America Automotive Camshaft Market

South America is forecast to be the fastest-growing territory at a 5.87% CAGR through 2030. Economic stabilization in Brazil and Argentina revives light-vehicle output, and regional trade accords encourage localization of powertrain components. ICE prevalence persists as charging infrastructure develops slowly, prolonging camshaft relevance. Suppliers establishing machining hubs near São Paulo or Córdoba benefit from lower logistics costs and reduced import duties. The region’s commercial-vehicle focus amplifies demand for durable forged designs.

North America and Europe Automotive Camshaft Market

In the United States, pickup and SUV popularity maintains sizeable engine displacement, supporting higher camshaft unit weights. Yet federal incentives for electric models gradually trim volumes. Europe confronts stricter CO₂ targets and urban zero-emission zones, accelerating hybrid adoption and depressing pure ICE builds. Nevertheless, vibrant performance-aftermarket cultures in Germany, the United Kingdom, and the United States generate premium opportunities, while heavy-duty truck segments remain solid.

Competitive Landscape

The Automotive Camshaft market is moderately concentrated, with MAHLE, Thyssenkrupp, and Kautex Textron leading the charge. Scale affords these leaders purchasing power in pig iron, alloying elements, and cutting-tool procurement. Global footprints allow cross-region capacity balancing to mitigate currency and freight volatility. Joint development programs with OEMs on assembled camshafts lock in early design influence, reinforcing incumbent status.

Technology leadership has become the primary differentiator. MAHLE deploys laser-welded hollow shafts for European hybrid engines, achieving double-digit weight savings. Thyssenkrupp’s precision-forged lobes and induction hardening deliver extended durability for U.S. pickup trucks. Kautex Textron leverages composite-over-metal tube technology to integrate oil passageways, reducing secondary machining steps. Smaller regional firms carve niches in performance billet products and vintage-engine restorations, where flexibility and customer intimacy outweigh scale.

Strategic moves include capacity expansions in low-cost geographies and R&D collaboration with actuator specialists exploring cam-less systems. Recent joint ventures across India and Mexico aim to localize finishing operations near OEM assembly plants, cutting lead times by up to two weeks. Patent filings on variable-lift mechanisms and friction-reduction coatings continue to rise, underpinning margin protection amid price pressure. Consolidation remains moderate as diverse engine families and aftermarket channels prevent dominance by a handful of suppliers.

Automotive Camshaft Industry Leaders

-

MAHLE GmbH

-

Thyssenkrupp AG

-

Kautex Textron

-

Precision Camshafts Ltd

-

Linamar Corporation

- *Disclaimer: Major Players sorted in no particular order

Automotive Camshaft Market Companies Covered in this Report

- MAHLE GmbH

- Thyssenkrupp AG

- Kautex Textron (CWC)

- Precision Camshafts Ltd

- JD Norman Industries (Park-Ohio)

- Linamar Corporation

- Hirschvogel Holding GmbH

- Engine Power Components Inc.

- ESTAS Camshaft

- Comp Performance Group

- Crankshaft Machine Company

- Aichi Forge USA Inc.

- Varroc Group

- Shadbolt Cams

- Crower Cams and Equipment Co.

- Schaeffler Technologies AG and Co. KG

- BorgWarner Inc.

- Robert Bosch GmbH

- Eaton Corporation plc

- Hitachi Astemo

- Mitsubishi Motors Powertrain

Recent Industry Developments in Automotive Camshaft Market

- April 2025: Delphi added 56 new part numbers to its North American aftermarket portfolio, including several camshaft sensors designed for nearly 43 million vehicles in operation.

- January 2025: Elgin PRO-STOCK introduced five made-in-USA performance camshaft kits targeting street and track engines.

- December 2024: TVS Motor unveiled the RT-XD4 engine platform featuring a dual overhead camshaft with a split-chamber crankcase for reduced oil consumption.

- October 2024: BGA released the DV5 8 mm camshaft kit (CS2335FK), upgrading lobe durability for PSA engines.

Global Automotive Camshaft Market Report Scope

Segmentation Overview

| Cast Camshaft |

| Forged Camshaft |

| Assembled Camshaft |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Gasoline |

| Diesel |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Manufacturing Technology | Cast Camshaft | |

| Forged Camshaft | ||

| Assembled Camshaft | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the Automotive Camshaft market in 2025?

It is valued at USD 5.23 billion, with a projected 4.49% CAGR through 2030.

Which manufacturing technology leads global revenue?

Cast camshafts dominate with 64.07% share, though assembled designs are the fastest-growing.

Which region will grow fastest through 2030?

South America is expected to post the highest 5.87% CAGR.

Why is aftermarket demand rising?

An aging vehicle parc and performance-tuning culture are driving a 7.12% CAGR in aftermarket sales.

How does electrification affect camshaft suppliers?

Hybrids sustain demand short term, but accelerating BEV adoption in Europe and China will progressively reduce long-term ICE volumes.

Page last updated on: