Automotive Metal Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 184.30 Billion |

| Market Size (2030) | USD 234.21 Billion |

| Growth Rate (2025 - 2030) | 4.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Metal Market Analysis by Mordor Intelligence

The automotive metal market size stands at USD 184.3 billion in 2025 and is projected to reach USD 234.21 billion by 2030, delivering a 4.91% CAGR. This headline trajectory conceals powerful shifts that are reshaping supplier strategies, material mixes, and regional sourcing footprints. Regulatory pressure for lighter vehicles, rapid electrification, and new casting technologies are driving aluminum adoption even as steel retains volume leadership. Asia-Pacific’s production dominance amplifies both opportunity and supply-chain risk, while nearshoring in North America and Europe is redrawing trade flows. Competitive intensity centers on technical expertise rather than sheer scale, with incumbents investing in low-carbon production and advanced alloys to defend margins.

Key Report Takeaways

- By product type, steel led with 56.13% of the automotive metal market share in 2024, whereas aluminum is forecast to register an 8.72% CAGR through 2030.

- By application, body structure accounted for a 42.18% share of the automotive metal market size in 2024, while battery-related components are advancing at an 11.27% CAGR to 2030.

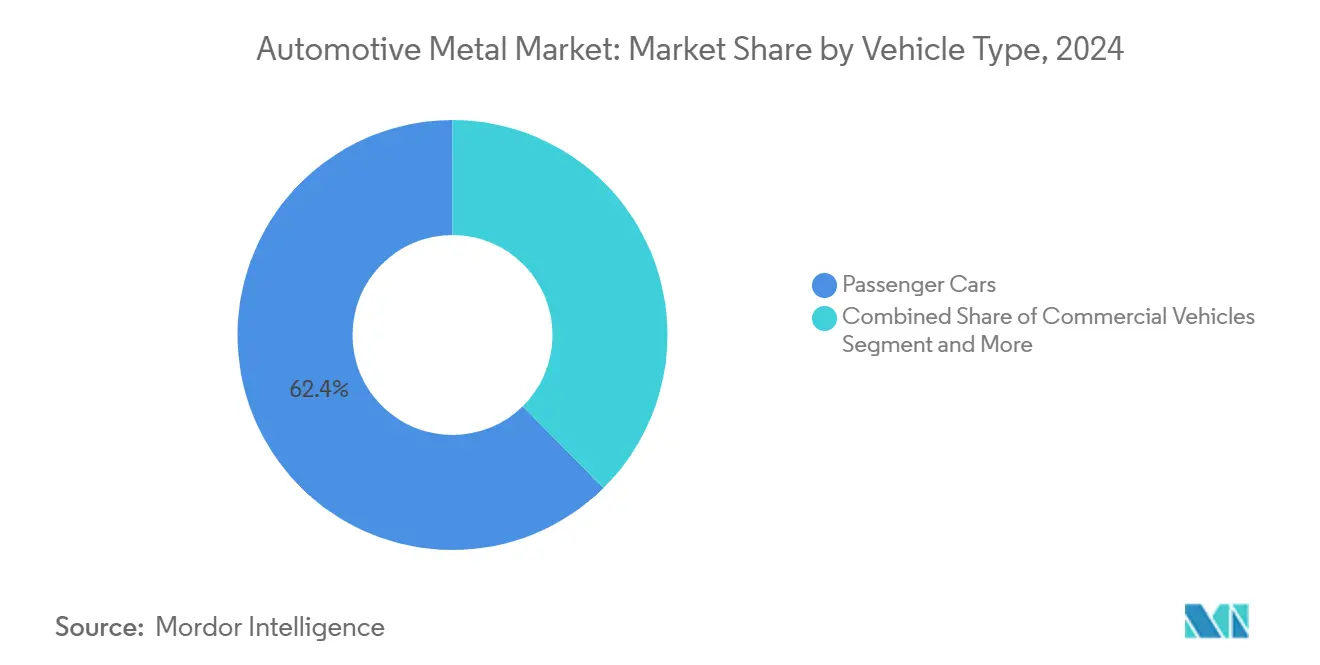

- By vehicle type, passenger cars contributed 62.44% of the automotive metal market share in 2024, and electric passenger cars are set to expand at a 12.59% CAGR through 2030.

- By manufacturing process, stamping held 38.22% share of the automotive metal market size in 2024, whereas high-pressure die casting is growing at a 10.36% CAGR to 2030.

- By geography, Asia-Pacific commanded 45.09% of the automotive metal market in 2024 and is progressing at a 7.94% CAGR, outpacing all other regions.

Global Automotive Metal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Global Fuel-Efficiency and CO₂ Rules | +1.8% | Global with EU and California Leading | Medium Term (2-4 Years) |

| Rapid EV Production Surge | +1.2% | Asia-Pacific Core, Spill-Over to North America and EU | Short Term (≤ 2 Years) |

| OEM Gigacasting Shift | +0.7% | Global with Tesla and Chinese OEMs as Early Adopters | Medium Term (2-4 Years) |

| Green Low-carbon EAF Steel | +0.6% | EU and North America | Long Term (≥ 4 Years) |

| Regional On-shoring of Metal Supply | +0.4% | North America and EU | Medium Term (2-4 Years) |

| Advanced AHSS Weight Savings | +0.3% | Global with Premium Segment Adoption First | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Stricter Global Fuel-Efficiency and CO₂ Rules Driving Lightweight Metals

Regulatory tightening across major automotive markets creates a compliance imperative that transforms material selection from cost optimization to regulatory necessity. The EU's 2024 implementation of 95g CO₂/km fleet averages, coupled with California's Advanced Clean Cars II program requiring 35% zero-emission vehicle sales by 2026, establishes lightweighting as a non-negotiable strategy for market access. This regulatory convergence particularly benefits aluminum, where each kilogram of weight reduction delivers approximately 20kg of lifetime CO₂ savings through reduced fuel consumption. The cascading effect extends beyond direct compliance, as automakers increasingly specify lightweight materials to create regulatory headroom for larger battery packs and enhanced performance features. OEMs report that aluminum-intensive vehicle architectures provide 15-20% better regulatory positioning compared to steel-dominant designs, creating a strategic advantage that justifies premium material costs.

Rapid EV Production Surge Escalating Demand for Aluminum and AHSS

Electric vehicle production scaling creates material demand patterns that diverge sharply from ICE vehicle requirements, with battery pack integration driving structural aluminum consumption and motor housing applications favoring advanced high-strength steels. Tesla's 2024 production of approximately 1.8 million vehicles demonstrates how EV scaling amplifies lightweight material demand beyond traditional automotive applications[1]"Tesla Fourth Quarter 2024 Production, Deliveries & Deployments," Tesla Press Release, tesla.com.. BYD's expansion to 3.6 million vehicle capacity by 2025 represents an additional 200,000 tons of annual aluminum demand, concentrated in battery structural components and thermal management systems. The shift toward 800V electrical architectures requires enhanced electromagnetic shielding, driving AHSS adoption in motor housings and inverter enclosures where magnetic permeability becomes a critical specification. This electrification-driven demand creates supply chain bottlenecks in specialized aluminum alloys, with automotive-grade 6000-series aluminum experiencing 6-month lead times compared to 2-month historical averages.

OEM Giga-Casting Shift Boosting High-Integrity Aluminum Alloys

Megacasting adoption transforms automotive manufacturing by consolidating complex multi-piece assemblies into single aluminum castings, creating demand for specialized alloys combining castability and structural performance. Tesla's implementation of 9,000-ton casting presses for Model Y rear underbody production eliminates 70 individual parts while reducing manufacturing complexity and improving crash performance[2]"The Giga Press: Tesla’s Game-Changing Manufacturing Process Goes Mainstream," Inside EVs, insideevs.com.. Chinese OEMs, including XPeng and Li Auto, have committed to similar megacasting strategies, with XPeng's P7 utilizing single-piece aluminum castings for front and rear structural sections. This manufacturing evolution requires aluminum alloys with enhanced fluidity and reduced porosity, driving development of specialized compositions that maintain strength while enabling complex geometries.

Green/Low-Carbon EAF Steel Gaining Preferential Sourcing Status

Decarbonization mandates across automotive supply chains elevate low-carbon steel from environmental preference to procurement requirement, with electric arc furnace (EAF) steel emerging as the preferred alternative to blast furnace production. ArcelorMittal's 2024 commitment to supply 12 million tons of reduced-carbon steel by 2030, utilizing hydrogen-based direct reduction, reflects industry recognition that carbon intensity becomes a competitive differentiator[3]"ArcelorMittal Sustainability Report 2024," arcelormittal.com.. Nucor's expansion of EAF capacity to 27 million tons annually positions the company to capture automotive demand for low-carbon steel, particularly as Scope 3 emissions reporting requirements intensify. The EU's Carbon Border Adjustment Mechanism, effective in 2026, creates cost advantages for domestically produced EAF steel over imports from high-carbon production regions. This regulatory framework generates a 15-25% cost penalty for traditional blast furnace steel imports, making EAF steel economically attractive beyond environmental considerations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material Price Volatility | -0.8% | Global with Emerging Markets Most Exposed | Short Term (≤ 2 Years) |

| High Capita Expenditure and Energy Intensity | -0.6% | Global with Energy-Intensive Regions Facing Constraints | Medium Term (2-4 Years) |

| Skilled-labor Shortage for Forming Next-Gen Magnesium Alloys | -0.5% | North America, EU, and Asia-Pacific Manufacturing Hubs | Medium Term (2-4 Years) |

| End-of-Life Recyclability Mandates Complicating Metal Mix | -0.4% | EU and Developed Markets with Stringent Recycling Regulations | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility for Aluminum and Steel

Metal price instability creates procurement challenges that extend beyond immediate cost impacts, forcing automakers to implement complex hedging strategies that reduce operational flexibility and increase working capital requirements. Aluminum prices experienced 35% volatility in 2024, driven by Chinese production curtailments and energy cost fluctuations, creating quarterly earnings variability that complicates long-term material commitments. Steel price swings of 28% during the same period, influenced by iron ore supply disruptions and coking coal availability, demonstrate how commodity market dynamics increasingly influence automotive profitability. This volatility particularly impacts smaller OEMs and Tier 1 suppliers who lack the scale to implement sophisticated hedging programs, creating competitive disadvantages that consolidate market share among larger players. The unpredictability forces conservative material planning, reducing innovation adoption rates as procurement teams prioritize cost certainty over performance optimization.

High Cap-Ex and Energy Intensity of Primary Metal Production

Primary metal production's capital intensity and energy requirements create supply constraints that limit capacity expansion responsiveness to automotive demand growth, particularly as environmental regulations increase operational complexity. Aluminum smelting requires approximately 13-15 MWh per ton of production, making energy costs 30-40% of total production expenses and creating vulnerability to electricity price volatility. New aluminum smelter construction requires USD 3-4 billion investment with 4-5 year development timelines, creating supply rigidity that cannot respond quickly to automotive demand surges. Steel production faces similar constraints, with integrated steel mills requiring USD 8-12 billion capital investment and 6-8 year construction periods. These barriers to capacity expansion create structural supply-demand imbalances during periods of rapid automotive growth, particularly in regions with limited existing metal production infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Steel Strength Meets Aluminum Disruption

Steel retained a 56.13% hold on the automotive metal market in 2024 due to entrenched supply chains and third-generation AHSS that provide 1,500 MPa strength without major tool changes. Yet aluminum’s 8.72% CAGR through 2030 underscores a structural pivot toward lighter metals that optimize EV range and regulatory compliance. Aluminum’s growth reflects battery-pack structures and giga-casting, while titanium remains niche in exhaust and suspension because corrosion resistance offsets high unit cost.

Aluminum’s expansion also benefits from closed-loop recycling, where scrap returns to rolling mills within 30 days, lowering carbon footprints by up to 95%. Tesla’s single-piece rear casting replaces 79 stamped steel parts and demonstrates why OEM engineers increasingly benchmark crash performance against aluminum, not steel. Magnesium and composites still face cost and handling barriers, but represent the next frontier as regulators tighten fleet emissions beyond 2030.

By Application: Body Structure Dominance Faces Battery Ascendancy

Body structures consumed 42.18% of the automotive metal market size in 2024 because every vehicle, regardless of drivetrain, requires a stiff crash cage. However, battery-related components expand at an 11.27% CAGR, creating a new demand pillar that bypasses declining powertrain metal requirements. Megacasting compresses the body-in-white footprint, cutting welds and integrating battery trays directly into floor structures, which accelerates aluminum uptake.

Powertrain applications contract in line with the ICE phase-down, while suspension stays resilient through performance and comfort tuning. BYD’s Blade Battery doubles as a load-bearing member, demonstrating how battery enclosures morph into chassis elements that demand alloys with both thermal conductivity and 180 MPa yield strength. The convergence of structural and energy-storage functions blurs traditional application lines and rewards suppliers who can co-engineer mechanical and thermal properties.

By Vehicle Type: Passenger Car Base Enables EV Pivot

Passenger cars delivered 62.44% of the automotive metal market share in 2024, yet the electric subset grows at a 12.59% CAGR that redefines material intensity. Each electric sedan requires 40–60% more aluminum than its ICE peer because battery enclosures, motor housings, and high-voltage busbars replace engine blocks. Honda’s USD 11 billion North American EV program exemplifies how OEMs recalibrate regional metal requirements around domestic content rules.

Commercial vehicles expand more modestly, favoring steel for durability, but electric buses open a new aluminum pull due to oversized battery packs. Two-wheeler and three-wheeler segments skew to Asia-Pacific, where low-cost steel remains prevalent, although urban e-scooters are experimenting with cast aluminum frames to offset battery mass. Vehicle-type dynamics, therefore, hinge on battery size and duty cycle rather than traditional class boundaries.

By Manufacturing Process: Stamping Scale Coexists with Casting Innovation

Stamping processes held 38.22% of the automotive metal market size in 2024 because legacy press lines and die libraries support high-volume steel panels at a competitive cost. Yet high-pressure die casting is racing ahead at a 10.36% CAGR as OEMs install 9,000–16,000-ton presses for front and rear megacastings. XPeng’s P7 uses two castings that replace 164 parts, trimming robot stations and reducing dimensional stack-ups.

Forging stays relevant for crankshafts and control arms, while extrusion finds new life in battery-tray side rails. Rolling remains the sheet-metal backbone for closure panels, but additive manufacturing is surfacing in bracket prototypes where weight reduction justifies powder-bed costs. Process selection is migrating from cost per part to total system cost, including weld elimination and logistics simplification.

Geography Analysis

Asia-Pacific anchored 45.09% of the automotive metal market revenue in 2024 and is expected to grow at a 7.94% CAGR through 2030. China produced 30.2 million vehicles in 2024, consuming roughly 45 million tons of automotive metals. Indonesia’s 1.8 million-ton nickel processing hub reinforces stainless steel supply chains, while Malaysia’s rising assembly volumes lift regional aluminum demand. Asia’s dominance remains tempered by tariff threats and shipping bottlenecks that encourage diversification.

North America benefits from USD 52 billion of announced investments that add rolling mills and recycling centers to meet domestic-content thresholds. U.S. gigafactories drive incremental aluminum consumption, whereas Mexico’s stamping clusters secure new electric SUV programs. Europe’s Carbon Border Adjustment Mechanism from 2026 will advantage local low-carbon EAF steel and incentivize closed-loop aluminum scrap collection. Together, these mature regions demonstrate how policy shapes material trade flows beyond wage differentials.

The Middle East and Africa leverage raw material strengths. The UAE’s 2.6 million-ton Emirates Global Aluminium smelter supplies high-purity billets to European extrusion plants. South Africa’s platinum resources feed catalytic-converter demand during the ICE sunset phase. South America’s center of gravity is Brazil, where local steel mills and lithium reserves in Argentina and Bolivia create synergies as EV supply chains descend on the continent. These emerging regions offer growth avenues that diversify sourcing away from Asia-centric nodes.

Competitive Landscape

The automotive metal market exhibits moderate concentration. The top five suppliers control roughly 45 to 50% of global revenue, allowing specialists to capture niche value pools. ArcelorMittal, Baowu, and POSCO wield integrated steel capacity, yet Novelis and Alcoa gain share in value-added aluminum sheets for body panels. Nucor’s eight-million-ton automotive expansion reflects regionalization trends and proximity advantages.

Competition increasingly hinges on technical collaboration. Novelis closed a USD 2.8 billion acquisition of Aleris automotive assets to deepen recycling loops that cut body-sheet carbon footprints by 50%. POSCO’s USD 3.2 billion venture with GM brings AHSS designed for motor housings directly to North American stamping plants. Such moves illustrate how alloy know-how and customer intimacy outweigh raw tonnage in securing multi-year nomination contracts.

Barriers to entry are rising. Raw-material volatility, capital intensity, and skilled labor shortages deter green-field challengers. Incumbents that invest in hydrogen DRI or scrape-sorting automation protect margins while meeting OEM sustainability scorecards. The competitive outlook favors players that marry metallurgical innovation with regional footprint alignment to de-risk logistics and tariff exposure.

Automotive Metal Industry Leaders

-

ArcelorMittal

-

Baowu Steel Group

-

POSCO

-

Tata Steel

-

Nippon Steel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Gestamp received recognition for lightweight steel innovations in automotive applications, demonstrating 25% weight reduction compared to conventional steel structures while maintaining crash performance standards.

- June 2024: Rio Tinto expanded its automotive-grade aluminum production in Canada, adding specialized alloy capabilities for megacasting applications. The expansion responds to growing demand from North American EV manufacturers.

Global Automotive Metal Market Report Scope

| Aluminum |

| Steel |

| Titanium |

| Other Product Types |

| Powertrain |

| Body Structure |

| Suspension |

| Other Applications |

| Two-Wheeler |

| Three-Wheeler |

| Passenger Cars |

| Commercial Vehicles |

| Buses and Coaches |

| Casting |

| Stamping |

| Extrusion |

| Rolling |

| Forging |

| Other Processes |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Aluminum | |

| Steel | ||

| Titanium | ||

| Other Product Types | ||

| By Application | Powertrain | |

| Body Structure | ||

| Suspension | ||

| Other Applications | ||

| By Vehicle Type | Two-Wheeler | |

| Three-Wheeler | ||

| Passenger Cars | ||

| Commercial Vehicles | ||

| Buses and Coaches | ||

| By Manufacturing Process | Casting | |

| Stamping | ||

| Extrusion | ||

| Rolling | ||

| Forging | ||

| Other Processes | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the automotive metal market and its expected size by 2030?

The automotive metal market stands at USD 184.3 billion in 2025 and should reach USD 234.21 billion by 2030.

Which metal gains the most from vehicle electrification trends?

Aluminum benefits the most because battery enclosures, megacast chassis parts, and thermal management components all prefer lightweight, high-conductivity alloys.

How will stricter CO₂ regulations influence material choices?

Tougher fleet targets favor lighter metals and low-carbon EAF steel, shifting procurement toward aluminum and advanced high-strength steel grades.

Why is high-pressure die casting growing so quickly?

Megacasting consolidates many stampings into one aluminum part, cutting weld points and improving crash performance, which reduces assembly cost and complexity.

Which region leads automotive metal demand growth through 2030?

Asia-Pacific remains the growth engine, driven by China’s EV production surge and Indonesia’s nickel processing expansion.

Page last updated on: