Industrial Vehicles Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 48.36 Billion |

| Market Size (2031) | USD 61.26 Billion |

| Growth Rate (2026 - 2031) | 4.84% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

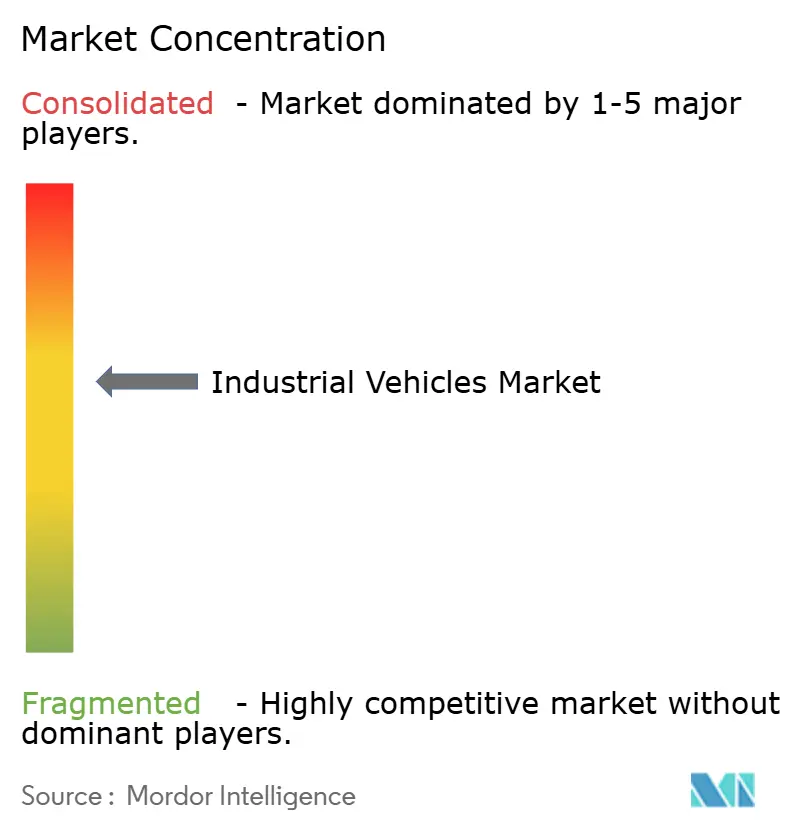

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Vehicles Market Analysis by Mordor Intelligence

The industrial vehicles market size is expected to increase from USD 46.13 billion in 2025 to USD 48.36 billion in 2026 and reach USD 61.26 billion by 2031, growing at a CAGR of 4.84% over 2026-2031. Demand holds steady, yet spending is migrating from internal-combustion platforms toward lithium-ion drivetrains, autonomous navigation, and battery-as-a-service contracts that convert capital outlay into predictable operating expense. Facing significant annual labor turnover, warehouse operators have pivoted their budgets towards autonomous mobile robots and automated guided vehicles. This sub-segment is expanding at a rate nearly double the growth of the broader industrial vehicles market. California's Zero-Emission Forklift Regulation prohibits new internal-combustion purchases and outlines a retirement schedule, aiming to phase out a substantial number of legacy units, thus hastening the shift towards electrification, outpacing general growth trends. Meanwhile, the Asia-Pacific region, boasting a significant revenue share, is on an upward trajectory with notable growth. This momentum is largely fueled by China's commitment to dual-carbon targets and India's expansion of factories, both of which are increasingly dependent on connected, zero-emission equipment.

Key Report Takeaways

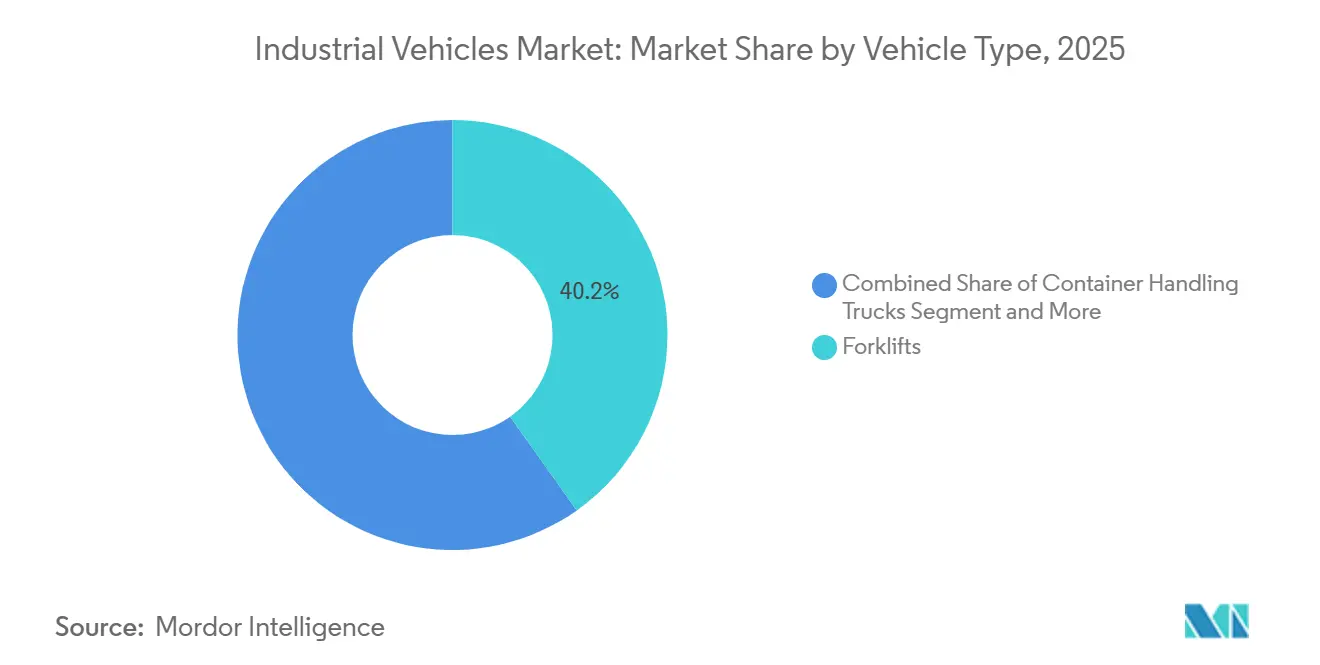

- By vehicle type, forklifts generated 40.15% of the industrial vehicles market in 2025, while automated guided vehicles posted the fastest 9.13% CAGR through 2031.

- By propulsion type, internal-combustion engines dominated with a 85.33% share in 2025, whereas electric drivetrains are expanding at an 8.79% CAGR through 2031.

- By application, warehousing accounted for 39.77% of the industrial vehicles market in 2025 and is also the fastest-growing use case, with a 5.87% CAGR over the forecast period.

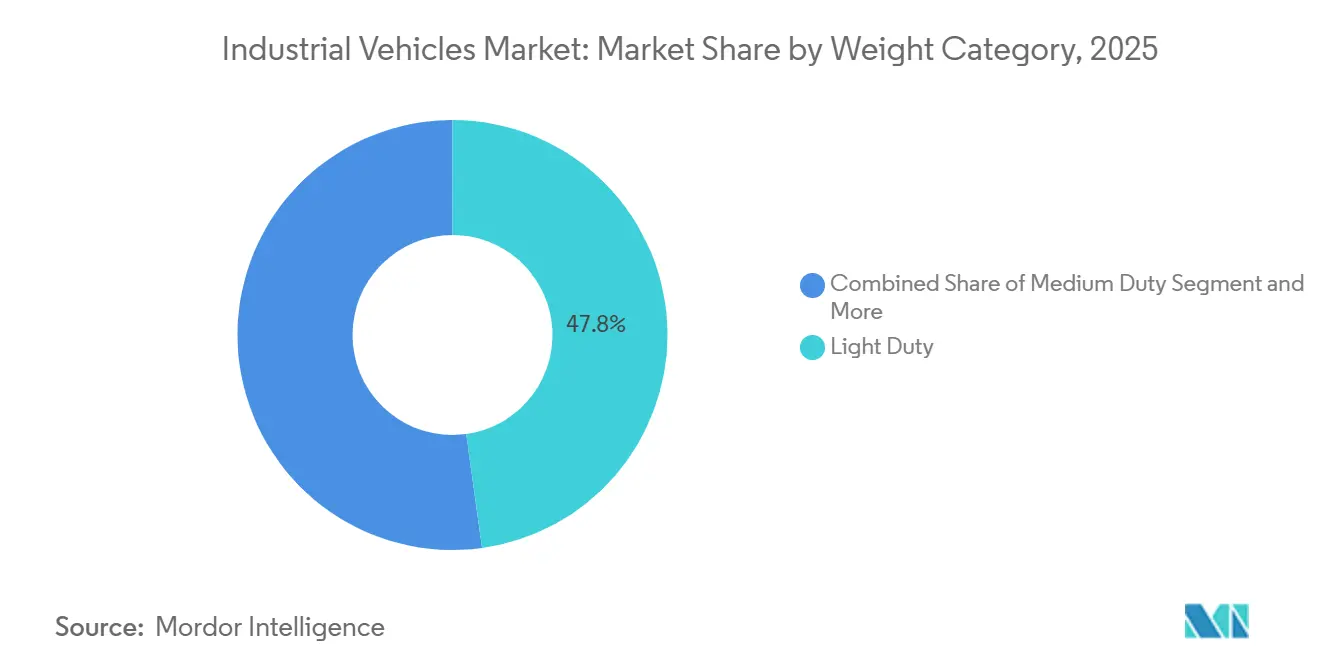

- By weight category, light-duty units captured 47.83% share in 2025, while medium-duty equipment recorded the highest 6.58% CAGR to 2031.

- By level of autonomy, non-autonomous machines held 84.13% of 2025 deployments, yet fully autonomous systems are scaling at an 8.02% CAGR.

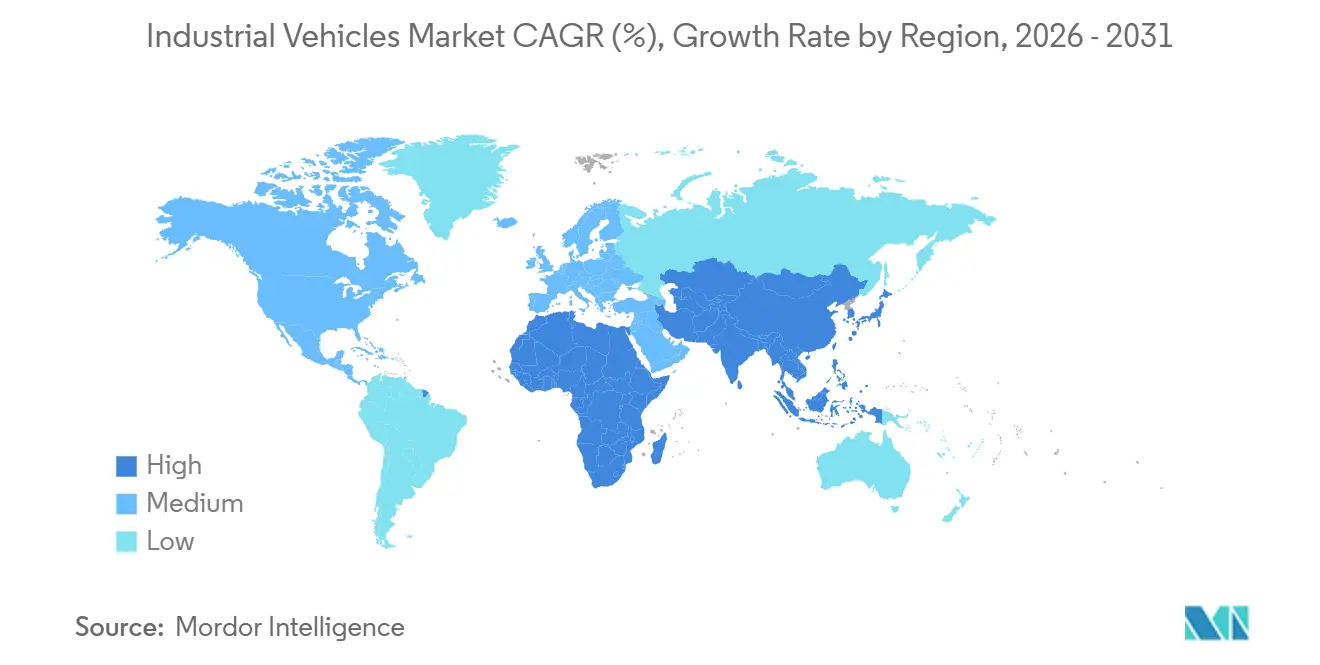

- By geography, Asia-Pacific secured 42.66% revenue share in 2025 and leads growth, with a 6.15% CAGR expected through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Industrial Vehicles Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Fuels Warehousing | +0.7% | North America and Asia-Pacific | Medium term (2-4 years) |

| Regulations Accelerate Electrification | +0.6% | Europe and North America, spreading to Asia-Pacific | Long term (≥ 4 years) |

| Addressing Automation Amid Labor Shortages | +0.5% | Global, acute in developed economies | Short term (≤ 2 years) |

| Integrating Intra-Logistics with Manufacturing | +0.4% | Asia-Pacific factories, EU industrial clusters | Medium term (2-4 years) |

| 5G Networks Enable Fleet Orchestration | +0.3% | North America and Europe early adopters | Long term (≥ 4 years) |

| BaaS Lowers Capital Expenditure Barriers | +0.2% | Developed markets piloting subscription models | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce–Fueled Warehousing Boom

Record online-order volumes require denser storage, faster picking, and continuous fulfillment cycles, prompting operators to add electric reach trucks and autonomous pallet movers able to navigate narrow aisles safely. In 2025, Amazon announced the deployment of over 1 million robots in its worldwide fulfillment and logistics network, highlighting the vast scale of its material-handling operations. Micro-fulfillment nodes in major cities further stimulate demand for compact industrial vehicle solutions that combine high-throughput lifts with advanced vision-guided navigation. Operators pay premiums for equipment that integrates natively with warehouse-execution software, ensuring real-time inventory accuracy. Same-day delivery norms in the United States and parts of Asia-Pacific reinforce capital flows into next-generation fleets that can operate around the clock without emitting exhaust, thereby supporting stringent indoor-air-quality codes.

Emissions Regulations Accelerating Electrification

California's Zero-Emission Forklift Regulation bans new internal-combustion forklifts, phases out large-spark-ignition units, and projects significant health benefits alongside net fleet savings over each forklift's lifecycle. Europe's Fit for 55 package and China's dual-carbon roadmap echo California's intent, driving up lithium-ion adoption rates. BYD's Blade Battery, combined with FLASH chargers, enables quick pit stops, allowing operators to recharge during shift breaks and retire spare batteries. The Environmental Protection Agency reinitiated Tier 5 rulemaking. Concurrently, Iowa's right-to-repair statute broadens service access, highlighting regulatory divergence amidst a unified push for electrification [1]“Electrification Trends in Off-Highway Equipment,”, Association of Equipment Manufacturers, aem.org. Operators unable to finance the shift from internal-combustion fleets face risks of stranded assets and declining resale values.

Automation and Safety Needs Amid Labor Shortages

Logistics firms are grappling with unfilled positions and facing a staggering annual turnover rate, highlighting a persistent staffing crisis. Robotic sorters have significantly reduced labor time per order while achieving an impressive accuracy rate, even with irregular items. Tompkins Robotics’ tSort can handle large volumes of items efficiently, directing them to numerous destinations, while edge-based orchestration keeps latency minimal. As a result, companies are transitioning from labor-assisted processes to entirely unattended operations, ensuring consistent throughput even in the absence of temporary workers. Furthermore, safety regulators have given their stamp of approval to collision-avoidance and remote-teleoperation features, effectively dismantling one of the final hurdles for the widespread adoption of automated guided vehicles in warehouses with mixed traffic.

Battery-as-a-Service Lowering Capex Barriers

Once deterred by the high price of lithium-ion packs, small-fleet owners are now embracing a new model. Battery-as-a-service transforms this hefty upfront investment into manageable monthly fees that cover maintenance, charging hardware, and end-of-life recycling. Hyster-Yale is set to launch its mobile HydroCharge platform. This innovative platform, designed as a trailer-mounted micro-grid, offers opportunity charging at sites lacking dedicated wiring. Just as businesses lease copiers for guaranteed uptime and predictable cash flow, fleet owners trade ownership for these benefits. This operating-expense model is gaining rapid traction in India, Southeast Asia, and Latin America. In these regions, challenges like grid reliability and financing hurdles had previously hampered the transition to electric fleets. Vendors adept at forecasting residual values and embracing circular-economy recycling stand to gain not just a steady stream of subscription revenue but also a competitive edge, sidelining their rivals.

Restraints Impact Analysis of Industrial Vehicles Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Upfront Costs of Automated Vehicles | –0.4% | Global, most acute in price-sensitive regions | Short term (≤ 2 years) |

| Bottlenecks in Battery and Chip Supply | –0.3% | Global, mining and fab capacity centered in Asia-Pacific | Medium term (2-4 years) |

| Cyber-Security Risks in Connected Fleets | –0.2% | Advanced IT markets | Medium term (2-4 years) |

| Legacy Floors Limit AGV Navigation | –0.2% | Older industrial facilities worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Electric / Automated Vehicles

Electric forklifts command a significant premium over their internal-combustion counterparts, with batteries alone potentially adding substantial costs to the final bill. This price hike extends payback periods for operators already grappling with tight margins. Hyster-Yale reported a decline in sales, resulting in a net loss as customers postponed purchases amid macroeconomic uncertainties. In a bid to navigate these challenges, the company is reducing its workforce, targeting annual savings in the long term. Meanwhile, manufacturers that can't finance customers or showcase a lower total cost of ownership face the risk of losing market share to budget-friendly Chinese competitors.

Battery-Metal and Chip Supply Bottlenecks

Lithium carbonate prices experienced a significant surge over a short period. Meanwhile, cobalt logistics faced disruptions due to political uncertainties in the Democratic Republic of Congo. In Indonesia, tightened nickel export quotas limited the diversity of cathode chemistry. Copper prices rose sharply, driven by supply constraints from grid upgrades. Lead times for semiconductors in battery-management systems remain elevated, causing delays. KION highlighted that, despite strong growth in order intake, margins in the EMEA region were squeezed by freight and input inflation. Builders with in-house cell plants or long-term metal contracts can stick to their delivery schedules. In contrast, spot buyers grapple with fluctuating costs, impacting their profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Industrial Vehicles Market Segment Analysis

By Vehicle Type:

Automation Narrows the Gap With ForkliftsForklifts generated 40.15% of the industrial vehicles market size in 2025, sustaining their central role in general material handling. Automated guided vehicles, though smaller in absolute dollars, are pacing at a 9.13% CAGR, benefiting from 24/7 uptime and labor substitution economics. At fully automated terminals, container-handling trucks have seen average selling prices rise. Meanwhile, tow tractors have carved out a niche, primarily serving airport ground support. Incumbents like Toyota Industries, KION, and Jungheinrich face pressure from stagnant forklift volumes, pushing them to innovate with lithium-ion integration and over-the-air diagnostics.

Chinese AGV manufacturers, such as Xunji Zhixing and VisionNav, utilize VNSLAM accuracy to offer competitive pricing and faster delivery cycles, challenging Western brands. KION’s IMOCO and QBIIK software enhance overall equipment effectiveness, underscoring the growing importance of software layers in driving future value beyond hardware. Hyster-Yale’s automated IDA truck combines AI vision, collision-avoidance, and lithium-ion batteries as premium upgrades, potentially doubling revenue per unit when bundled with orchestration software.

By Propulsion Type:

Electric Outpaces All AlternativesThe industrial vehicles market share for internal-combustion engines stood at 85.33% in 2025, yet electrics are expanding at 8.79%, supported by zero-emission rules and falling battery costs. Port Newark has placed an order for hybrid straddle carriers, highlighting the growing trend of hybrid drivetrains in ports. While compressed natural gas forklifts find a niche in petrochemical hubs, infrastructure limitations hinder their broader adoption.

BYD's innovative FLASH charger significantly reduces idle time. This efficiency enables fleets with a single battery to seamlessly cater to multi-shift demands. California's regulatory push is set to further elevate electric vehicle adoption. This underscores the power of regulation in driving adoption, even when the economic benefits are marginal. Vendors lacking a robust lithium-ion lineup may find themselves sidelined, missing out on bids from retailers and food-and-beverage producers that prioritize indoor zero-emission compliance.

By Application:

Warehousing Still Dominates Investment CyclesWarehousing accounted for 39.77% of the industrial vehicles market in 2025 and is growing at 5.87%. E-commerce sellers have significantly increased storage density by using multi-tier mezzanines, which are efficiently managed by autonomous lifts. At Siemens, AutoStore installations achieved a remarkable increase in picking speed and a reduction in space usage. Meanwhile, Puma is achieving 10-fold capacity gains. In manufacturing, where just-in-time sequencing is paramount, KION's Deep PTL system not only synchronizes line-side replenishments with predictive maintenance calls but also enhances overall uptime.

Freight and logistics yards are investing in heavy-duty tow tractors to ensure seamless, round-the-clock cross-docking operations. Simultaneously, the construction sector is channeling funds into rough-terrain telehandlers, a move closely tied to the ongoing infrastructure stimulus. APM Terminals is making a significant commitment with equipment spread across various sites. This includes ship-to-shore cranes and a fully electric fleet at Suape, Brazil, highlighting the momentum of port automation. Vendors with modular software capabilities are adeptly transitioning the same hardware across retail, manufacturing, and port applications, streamlining R&D efforts and minimizing duplication.

By Weight Category:

Versatility Drives Medium-Duty GrowthLight-duty models, covering loads up to 2 tons, accounted for 47.83% of the Industrial Vehicles market in 2025 due to their cost and maneuverability advantages, which suit small warehouses and retail facilities. Yet operators running multi-pallet tasks increasingly choose medium-duty units, which are projected to grow at a 6.58% annual rate through 2031. Advances in battery chemistry mean a 3-ton electric lift can now log a full shift on a single charge, eroding a former stronghold of diesel. Heavy-duty platforms weighing more than 10 tons remain indispensable at steel mills, ports, and lumber yards, but their cycle is tied to capital goods markets and global trade.

Platform modularity blurs category lines: the same base can accept counterweights, longer forks, or taller masts to service multiple payload brackets. Fleets deploy telematics dashboards that track load profiles, guiding data-driven rightsizing and reducing over-spec’d purchases. Energy recovery during mast lowering is now available in medium-duty electric lines, reducing kilowatt-hour consumption. Over time, these innovations allow the industrial vehicles market to transition from capacity-centric buying toward lifecycle-cost optimization.

By Level of Autonomy:

Gradual Transition Toward Full AutomationNon-autonomous equipment still formed 84.13% of 2025 deployments, yet fully autonomous platforms clock an 8.02% growth rate out to 2031. Lufthansa Cargo's 5G network in Los Angeles boosted AGV speeds significantly and eliminated Wi-Fi dead zones that had previously caused delays. Operators benefit from a standardized safety framework under ISO rules, easing legal and insurance challenges.

Hyster-Yale is set to debut automation, featuring tele-operation for handling exceptions, a move that enhances acceptance in warehouses with mixed traffic. Konecranes' CONTROLS emulation tool creates digital twins of entire terminals, enabling Maasvlakte II to refine software before hardware delivery and significantly reducing commissioning time. With the declining costs of private 5G, the shift towards fully driverless operations is poised to quicken. This trend compels lift-truck OEMs to integrate orchestration software into their offerings, moving away from the traditional model of selling standalone vehicles.

Geography Analysis

Asia-Pacific commanded 42.66% of the industrial vehicles market share in 2025 and is expected to grow at 6.15% through 2031. Chinese AGV vendors achieving high navigation accuracy are making significant inroads in grocery, electronics, and cross-border e-commerce fulfillment centers. This push has bolstered Hangcha's sales, moving a substantial number of electric forklifts domestically. In India, production-linked incentives are luring foreign direct investments, particularly in smartphones and auto parts. This influx is spurring warehouse expansions. However, the inconsistent grid power is hindering the adoption of lithium-ion technology, especially outside tier-1 cities. Meanwhile, Japan and South Korea are weaving intra-logistics into their Manufacturing 4.0 strategies. Yet, Toyota Industries faced a setback, with its materials-handling revenue dipping due to settlement costs, underscoring the industry's regulatory vulnerabilities.

North America may have a smaller market volume, but it commands premium pricing. This is largely due to California's stringent zero-emission rules and the anticipated EPA Tier 5 standards, which elevate technical specifications. Port Newark is taking strides towards electrification, with hybrid straddle carriers booked for delivery. Retail giants are pushing the envelope on automation, as evidenced by Walmart's retrofit in Opelousas. In Europe, the trend is unmistakable: Germany champions Industry 4.0 initiatives, and KION, even amidst raw-material inflation, sees its order intake surge to a notable EUR 11.705 billion, leading to strong revenue outcomes.

While South America, the Middle East, and Africa command a smaller share of the industrial vehicles market, they are ripe with green-field opportunities. Brazil's Suape terminal is set to become APM's inaugural fully electric port in Latin America, featuring remote-operated cranes and electric yard tractors. The Port of Montreal, with backing from the Canada Infrastructure Bank, is expanding its Contrecœur facility, adding significant TEU capacity. Meanwhile, Lomé Container Terminal is modernizing with Konecranes' TruConnect, upgrading to remote-monitored reach stackers and empty-container handlers, highlighting the growing traction of digital service contracts, even in markets with modest unit sales volumes.

Competitive Landscape

The industrial vehicles market is moderately concentrated. Toyota Industries, KION, Jungheinrich, and Mitsubishi Logisnext dominate the forklift and warehouse truck sectors, bolstered by extensive dealer service networks. KION enhances customer loyalty and offers predictive maintenance through its software trio—IMOCO4.E, Deep PTL, and QBIIK—with significant returns. Despite Toyota Industries reporting strong revenue, a substantial drop in operating profit followed a U.S. class-action settlement over engine certification issues, underscoring the weight of regulatory challenges even for industry giants [2]“FY 2026 Financial Results,”, Toyota Industries Corporation, toyota-industries.com.

Hyster-Yale undertook a restructuring that included workforce reductions. They shifted Nuvera's fuel-cell R&D focus towards lithium-ion modules and the HydroCharge mobile platform, aiming for significant annual savings. Meanwhile, Chinese firms like BYD, Hangcha, Xunji Zhixing, and VisionNav leverage cost leadership and rapid iteration. BYD's Blade Battery 2.0, boasting a swift recharge capability, positions the company favorably for contracts where minimizing downtime is paramount.

Emerging growth areas spotlight autonomous retrofit kits, subscription-based energy models, and micro-fulfillment solutions. The ISO 3691-4 standard establishes a globally accepted safety benchmark, facilitating multi-vendor fleets without the constraints of proprietary systems. The software domain is becoming a key competitive arena: Konecranes' CONTROLS emulation and digital twin technology mitigated commissioning risks at Maasvlakte II, while Locus Robotics emphasizes output in "picks-per-hour," shifting the focus from hardware to service-level agreements. Vendors transitioning from singular equipment sales to recurring revenue streams in orchestration, analytics, and energy management are poised to outpace those rooted in traditional transactional models.

Industrial Vehicles Industry Leaders

Toyota Industries Corporation

KION Group AG

Jungheinrich AG

Hyster-Yale Materials Handling Inc.

Mitsubishi Logisnext Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Industrial Vehicles Market Companies Covered in this Report

- Toyota Industries Corporation

- KION Group AG

- Jungheinrich AG

- Mitsubishi Logisnext Co. Ltd.

- Hyster-Yale Materials Handling Inc.

- Crown Equipment Corporation

- BYD Company Ltd.

- Hangcha Group Co. Ltd.

- Komatsu Ltd.

- Doosan Industrial Vehicle Co. Ltd.

- Clark Material Handling Company

- Hyundai Construction Equipment Co.

- Caterpillar Inc.

- Raymond Corporation

- JCB Ltd.

Recent Industry Developments in Industrial Vehicles Market

- August 2025: Haulotte introduced the Pulseo HA20 E and HA20 E PRO 20-meter fully electric boom lifts engineered for rough-terrain performance without emissions or engine maintenance.

- June 2025: JLG rebranded its micro electric scissor lifts as ES1330M and ES1530M, complemented by the ES1930M, strengthening its compact offering in North America.

Global Industrial Vehicles Market Report Scope

The industrial vehicles market report is segmented by vehicle type (forklifts, tow tractors, container handling trucks, industrial tractors, automated guided vehicles (AGVs), personnel carriers, scissor lifts, boom lifts, and others), propulsion type (propulsion type (internal combustion engine (ICE), electric, hybrid, and CNG / LPG)), application (manufacturing, warehousing, freight and logistics, construction, agriculture, retail, and others), weight category (light duty, medium duty, and heavy duty), level of autonomy (non-autonomous, semi-autonomous, and fully autonomous), and geography. The market forecasts are provided in terms of value (USD) and volume (units).

Segmentation Overview

| Forklifts |

| Tow Tractors |

| Container Handling Trucks |

| Industrial Tractors |

| Automated Guided Vehicles (AGVs) |

| Personnel Carriers |

| Scissor Lifts |

| Boom Lifts |

| Others |

| Internal Combustion Engine (ICE) |

| Electric |

| Hybrid |

| CNG / LPG |

| Manufacturing | Automotive |

| Chemical | |

| Food and Beverages | |

| Metals and Machinery | |

| Warehousing | |

| Freight and Logistics | |

| Construction | |

| Agriculture | |

| Retail | |

| Others |

| Light Duty |

| Medium Duty |

| Heavy Duty |

| Non-Autonomous |

| Semi-Autonomous |

| Fully Autonomous |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Forklifts | |

| Tow Tractors | ||

| Container Handling Trucks | ||

| Industrial Tractors | ||

| Automated Guided Vehicles (AGVs) | ||

| Personnel Carriers | ||

| Scissor Lifts | ||

| Boom Lifts | ||

| Others | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Electric | ||

| Hybrid | ||

| CNG / LPG | ||

| By Application | Manufacturing | Automotive |

| Chemical | ||

| Food and Beverages | ||

| Metals and Machinery | ||

| Warehousing | ||

| Freight and Logistics | ||

| Construction | ||

| Agriculture | ||

| Retail | ||

| Others | ||

| By Weight Category | Light Duty | |

| Medium Duty | ||

| Heavy Duty | ||

| By Level of Autonomy | Non-Autonomous | |

| Semi-Autonomous | ||

| Fully Autonomous | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Industrial vehicles market in 2026?

The Industrial vehicles market size is USD 48.36 billion in 2026, on its way to USD 61.26 billion by 2031.

Which segment is growing fastest inside material-handling equipment?

Automated guided vehicles post the highest 9.13% CAGR through 2031 as warehouses automate around 24/7 demand.

Why is Asia-Pacific the largest regional opportunity?

Asia-Pacific holds 42.66% of global revenue, driven by China’s electrification mandates and India’s factory expansion programs that increase demand for connected, zero-emission equipment.

How quickly are electric drivetrains displacing internal-combustion models?

Electric units are expanding at 8.79% annually and are projected to exceed a 20% share in regulated regions by 2028.

Page last updated on: