Automotive Acoustic Material Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 5.63 Billion |

| Market Size (2031) | USD 6.95 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

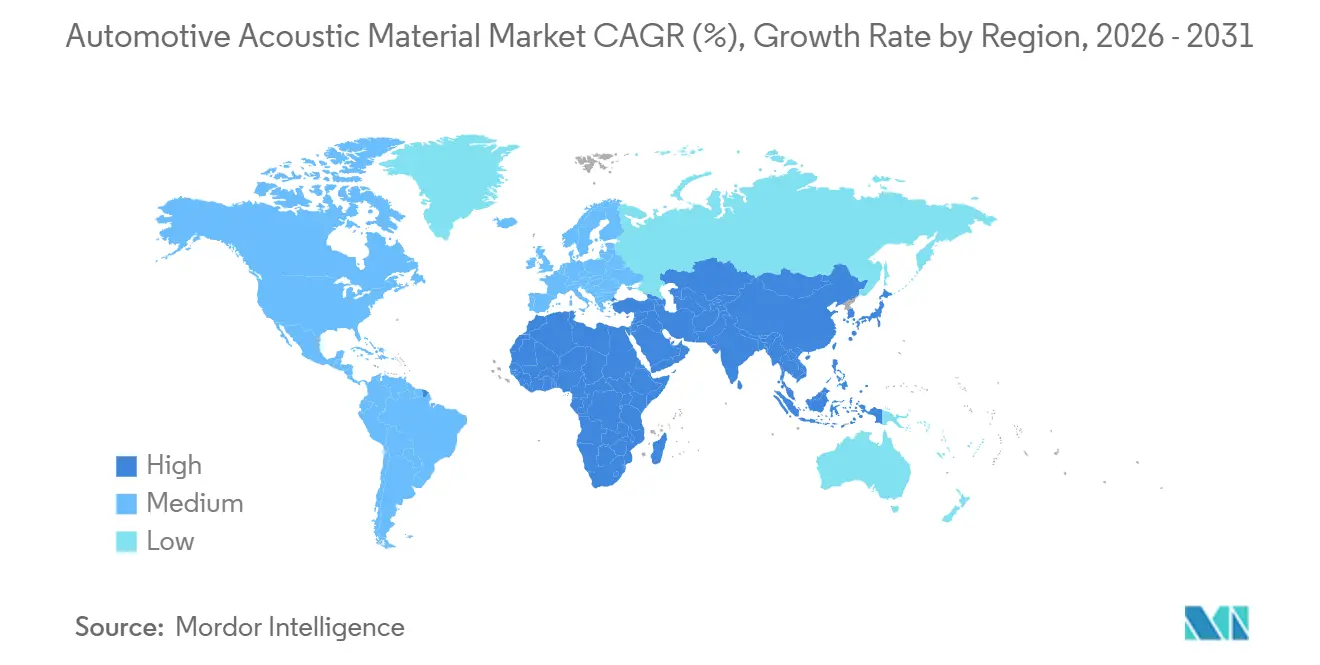

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Acoustic Material Market Analysis by Mordor Intelligence

The automotive acoustic material market size is expected to increase from USD 5.40 billion in 2025 to USD 5.63 billion in 2026 and reach USD 6.95 billion by 2031, reflecting a 4.28% CAGR during the forecast period (2026 to 2031). Increasing electric vehicle production, intensifying interior noise regulations, and the push for lightweight multifunctional composites underpin this steady advance. OEMs focus on integrating thermal and acoustic functions into single-layer packages to free up space in skateboard EV platforms while meeting stringent cabin-noise limits. Polyurethane retains its lead because of proven damping performance, yet polypropylene gains traction as recycling mandates tighten. Geographic growth remains anchored in Asia-Pacific, but the Middle East and Africa outpace global averages as new assembly plants start production. Competitive intensity is shaped by material science breakthroughs and strategic acquisitions that expand regional footprints and diversify product portfolios.

Key Report Takeaways

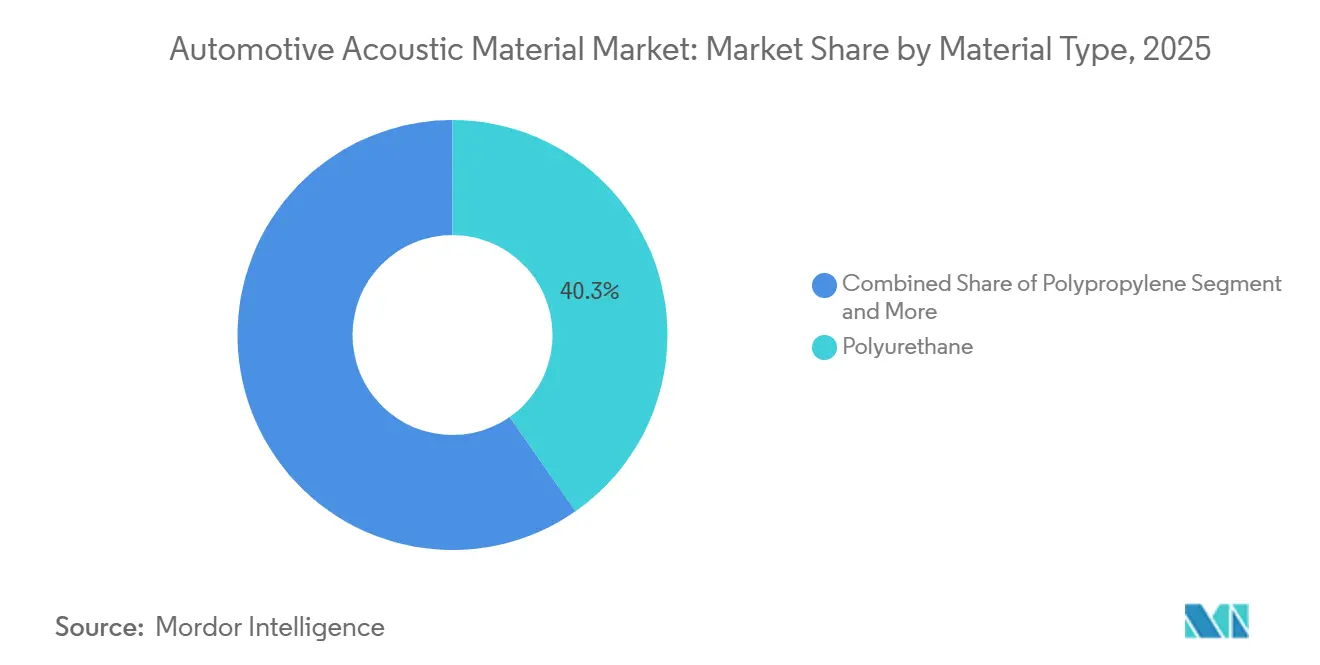

- By material type, polyurethane captured 40.25% of the automotive acoustic material market share in 2025, while polypropylene is forecast to expand at a 6.55% CAGR through 2031.

- By application area, interior systems held 53.18% of the automotive acoustic material market size in 2025, and exterior components are advancing at a 7.58% CAGR to 2031.

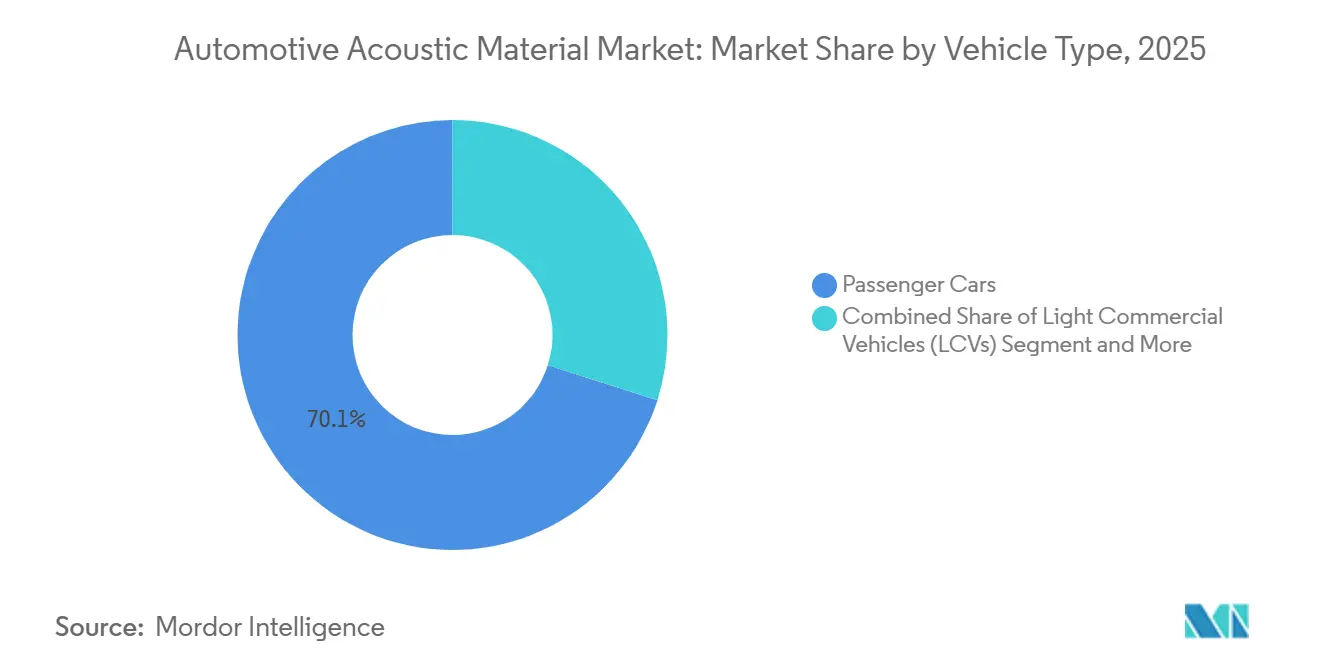

- By vehicle type, passenger cars dominated with a 70.13% share in 2025; light commercial vehicles will record the fastest projected CAGR at 6.13% through 2031.

- By sales channel, OEM supply accounted for 83.44% share in 2025, whereas the aftermarket is expected to grow at a 7.03% CAGR between 2026 and 2031.

- By geography, Asia-Pacific led with 38.16% revenue share in 2025, while the Middle East and Africa are projected to climb at a 5.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Acoustic Material Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Interior Noise Regulations | +1.2% | Global, with the Europe and China leading | Medium term (2-4 years) |

| OEMs Prioritize Lightweight Acoustic Composites | +0.8% | North America and the Europe, expanding to the Asia-Pacific | Long term (≥ 4 years) |

| Urbanization Drives In-Cabin Comfort | +0.7% | Asia-Pacific core, spill-over to the Middle East and Africa | Medium term (2-4 years) |

| Ride-Sharing Fleets Seek Durable NVH | +0.5% | Global urban centers | Long term (≥ 4 years) |

| Bio-Based Foams Meet ESG Demands | +0.4% | Europe leading, expanding globally | Long term (≥ 4 years) |

| Integrated Acoustic Packages Downsize Audio | +0.3% | Premium segments globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Interior Noise Regulations for EVs and HEVs

Electric and hybrid models now face cabin-noise caps under Regulation (EU) 540/2014 and China’s GB 1495-2024 standards, driving an immediate spike in demand for high-density foams, multilayer laminates, and precision-tuned frequency absorbers [1]“Regulation (EU) 540/2014 on the sound level of motor vehicles,” European Commission, ec.europa.eu. OEMs must secure certified materials within a two-year window, creating pricing leverage for suppliers already validated. Product selection increasingly revolves around low-thickness polyurethane composites that block inverter whine without sacrificing foot-well space. Regulations now spill into the aftermarket, compelling replacement parts to match original acoustic specifications, thereby enlarging total addressable demand. Suppliers that align R&D pipelines with certification schedules can command premiums and lock in multiyear contracts.

OEM Shift Toward Lightweight, Multifunctional Acoustic-Thermal Composites

Manufacturers are merging NVH dampers with thermal barriers into single panels that deliver notable mass savings over legacy multilayer stacks. Polypropylene-rich matrices are preferred because they meet recyclability thresholds emerging in Europe’s Circular Economy Action Plan. The shift accelerates strategic partnerships between chemical companies and Tier 1 converters that control advanced bonding lines. Although such composites cost significantly more per square meter, OEMs recoup expenses through reduced fastener counts, faster takt times, and improved range in EVs. Suppliers with integrated compounding and laminating assets gain a competitive edge by hitting tight dimensional tolerances and dual-property targets in one production pass.

Rapid Urbanization Spurring Demand for In-Cabin Comfort in Emerging Asia

India's urban population will hit 675 million by 2035, amplifying driver sensitivity to traffic-borne noise. In India and Southeast Asia, automakers are now equipping mass-market hatchbacks with floor and dash liners, a feature once exclusive to luxury sedans. Local content rules encourage material suppliers to build regional plants, trimming logistics costs and enabling quicker design iterations. Rising disposable income allows mid-segment buyers to pay modest premiums for quieter rides, pushing acoustic specification rates from single-digit to high-teens percentages of BoM value. Commercial fleets delivering last-mile goods in congested cities likewise adopt enhanced NVH packages to reduce driver fatigue and meet occupational safety norms.

Growing Ride-Sharing and Robo-Taxi Fleets Prioritizing Durable NVH Interiors

Waymo, Cruise, and Didi fleet operators expect interior panels to survive half-million-mile duty cycles without acoustic degradation, five times longer than private-use vehicles. Polyurethane foams now integrate durable skins and antimicrobial additives that withstand frequent cleaning. Performance warranties covering acoustic retention become standard in supply contracts, creating recurring revenue streams via maintenance kits. Aftermarket refurb centers source drop-in kits engineered for rapid turnaround, cementing a new specialty niche. Suppliers able to certify long-life acoustics build stronger ties with fleet operators managing large urban deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical Feedstock Supply Volatility | -0.6% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| Space Constraints Limit EV Insulation | -0.4% | Global EV markets | Medium term (2-4 years) |

| Recycling Mandates Increase Material Complexity | -0.3% | Europe leading, expanding to North America | Long term (≥ 4 years) |

| Active Noise Cancellation Reduces Demand | -0.2% | Premium segments globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Volatility in Petrochemical Feedstocks for Foams

Prices for toluene diisocyanate, a key polyurethane precursor, swung significantly during 2025 because of geopolitical tensions affecting Middle Eastern production. Margins for smaller converters without hedging mechanisms experienced a significant contraction. OEMs responded by dual-sourcing and negotiating pass-through clauses, raising procurement complexity. While bio-feedstock routes promise stability, they remain cost-additive and limited in capacity. Suppliers with backward-integrated chemical lines or long-term contracts insulate themselves from near-term shocks and retain preferred-vendor status.

Space Constraints in Skateboard EV Platforms Limiting Insulation Thickness

Next-generation EVs cut the flooring thickness of windows to 15–20 mm to make room for larger battery packs. Traditional fiber mats lose effectiveness at those dimensions, forcing suppliers into micro-perforated films, aerogel hybrids, and metamaterial cells. Such solutions demand new tooling and quality-control protocols, pushing cap-ex budgets higher for Tier 2 vendors. Retrofitting thicker aftermarket kits proves impractical, thereby reinforcing OEM channel dominance. An opportunity opens for innovators who can validate high-transmission-loss products under 300 µm that also meet flammability standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyurethane Leads While Polypropylene Accelerates

Polyurethane remained the anchor at 40.25% share in 2025 because of reliable damping, established supply chains, and broad OEM validation. The automotive acoustic material market benefits from polyurethane’s tuning versatility, enabling bespoke cell structures for specific frequency bands. Yet recyclability pressures and the search for lower density drive polypropylene’s 6.55% CAGR, positioning it as the standout growth vector. Suppliers pivot to PP-rich blends that trim significant mass while meeting flammability codes. Bio-sourced feedstocks emerge but require scaling to match volume contracts, keeping them in pilot phases for now.

Polyurethane producers respond with renewable polyol grades and low-VOC formulations that align with EU REACH thresholds. The automotive acoustic material market size for polyurethane is set for further expansion, reflecting a solid base for incremental innovation. Polypropylene’s rise invites capacity expansions in Asia, where integrated petrochemical complexes cut resin costs. Fiberglass and specialty textiles hold niche roles in commercial and premium interiors, respectively, balancing cost, weight, and aesthetics.

By Application Area: Interior Maturity Meets Exterior Momentum

Interior solutions delivered 53.18% revenue in 2025, a testament to long-standing focus on occupant comfort and regulatory compliance. Door panels, floor carpets, and dash insulators form stable, high-volume programs that anchor supplier cash flows. The automotive acoustic material market continues to innovate in interior trims through composite felts that double as design surfaces, easing assembly and enhancing perceived quality. However, the exterior segment grows faster at 7.58% CAGR, propelled by EV aerodynamics and wind-noise management mandates.

Underbody shields, wheel-arch liners, and A-pillar trims leverage polypropylene and thermoformed PET blends that resist stone impact while dampening broadband noise. The automotive acoustic material market size assigned to exterior components is forecast to grow significantly by 2031. Integrated aero-acoustic modules lower drag and suppress vortex-induced noise, feeding OEM range and cabin-quietness targets in one assembly. Suppliers refine weather-stable composites able to survive thermal cycling and road-salt exposure without acoustic drift, locking in long-term durability claims.

By Vehicle Type: LCV Electrification Spurs New Demand

Passenger cars safeguarded a 70.13% share in 2025, reflecting high global production volume. Their specification depth makes them the mainstay for material innovation and margin scale. Meanwhile, electrified delivery vans push light commercial vehicles (LCVs) toward a 6.13% CAGR as e-commerce ramps up urban shipment frequencies. Fleet buyers specify robust floor mats and firewall panels that damp drive-unit whine and loading-dock clatter. The automotive acoustic material market share differential narrows as LCV programs adopt passenger-car comfort features to satisfy driver-retention policies.

Medium and heavy trucks maintain a steady uptake for roof and sleeper-cab liners that cut fatigue during long hauls. Bus manufacturers pursuing zero-emission fleets integrate low-smoke foams that meet public-transport safety codes, extending supplier reach into mass-transit projects. The automotive acoustic material market size for LCVs will expand significantly by 2031, translating into a notable segment opportunity. Across vehicle types, thin but high-loss laminates address the limited package space inherent in battery-dominant layouts, securing future relevance for passive NVH systems.

By Sales Channel: Aftermarket Builds Momentum

OEM pipelines delivered 83.44% of sales in 2025 as acoustic liners are chosen early in platform development alongside crash and thermal systems. Yet the aftermarket advances with a 7.03% CAGR by 2031, as aging fleets seek cabin upgrades and fleet refurbishments extend service life. Online platforms ship pre-cut kits with peel-and-stick backing, simplifying installation and broadening consumer reach. The automotive acoustic material market benefits when ride-share operators refresh interiors to retain clientele and meet noise targets codified in municipal regulations.

Specialist installers emerge, bundling acoustic re-liner services with detailing and infotainment upgrades. OEM suppliers hedge channel risk by launching branded retrofit lines that guarantee factory-level fit and finish. In emerging markets, informal workshops drive volume for budget foams, though regulatory enforcement gradually steers demand toward certified materials. Sustainable disposal programs for replaced liners become value-adds for professional shops, further professionalizing the aftermarket.

Geography Analysis

Asia-Pacific retained 38.16% of global revenue in 2025, anchored by China’s 12.4 million electric car production count and India’s expanding assembly clusters [2]“China Vehicle Production Statistics 2024,” China Association of Automobile Manufacturers, caam.org.cn. Local acoustic suppliers co-locate near OEM plants in Shanghai, Pune, and Ulsan to meet just-in-time targets and adapt formulations to regional climate conditions. The automotive acoustic material market in China also absorbs local content rules, pushing foreign firms toward joint ventures for capacity scaling. Japan’s hybrid expertise sustains demand for dual-mode barrier-absorber panels, while South Korea’s export-focused OEMs specify global-compliant solutions to serve North American and European destinations.

The Middle East and Africa post the fastest expansion at 5.75% CAGR, led by the industrial development in the United Arab Emirates and Saudi Arabian manufacturing incentives embedded in Vision 2030. New CKD plants in Egypt and Morocco create localized demand for dash insulators and door seals tuned for high ambient temperatures. South Africa leverages established export channels to Europe, requiring materials certified to EU noise and recycling directives. Although infrastructure limitations persist, abundant petrochemical feedstocks underpin regional foam production, cushioning feedstock volatility on local converters.

Europe’s premium brands keep the region at the forefront of acoustic technology. Germany’s OEMs demand ultralight laminates that meet both NVH and sustainability thresholds, spurring suppliers to develop mono-material films compatible with closed-loop recycling. France and Italy prioritize felts made from recycled textile fibers, fitting circular-economy goals, while the United Kingdom nurtures start-ups exploring aerogel-hybrid absorbers. North America’s transition toward electric pickup trucks intensifies the need for wheel-arch and underbody damping to manage tire roar, injecting fresh volume into plants in the United States. Across geographies, the automotive acoustic material market adapts formulations to match varying regulatory distances to curb NOx and noise emissions.

Competitive Landscape

The automotive acoustic material market remains moderately fragmented, with the top five suppliers controlling a significant share of revenue, leaving space for regional specialists and innovative newcomers. BASF, 3M, and Covestro exploit chemical integration to introduce proprietary polyols and isocyanate chemistries that boost absorption per millimeter of thickness. Autoneum, Grupo Antolin, and U-Sonics differentiate through application engineering, securing platform-level awards from global OEMs. Acquisition activity accelerated in 2025 as Autoneum gained 70% of Jiangsu Huanyu, widening its China presence[3]“Acquisition of Jiangsu Huanyu NVH Business,” Autoneum Holding AG, autoneum.com.

Intellectual-property battles center on metamaterial patterns and bio-based formulations that promise weight and sustainability gains. Patent filings for aerogel-laden foams increased over time, signaling next-wave contests over ultra-thin, high-loss products. Regional suppliers in India and Indonesia carve out a share by offering customized dashboard kits tailored to local vehicle top-sellers at cost advantages. ESG credentials become tender differentiators; ISO 14001 certificates and carbon-footprint disclosures now feature in RFQ scorecards.

Strategic collaborations emerge between chemical majors and software firms to jointly develop material-DSP hybrids, blending passive absorbers with active cancellation algorithms integrated at the design stage. Companies able to provide data-rich acoustic simulations shorten OEM validation cycles and lock in early design wins. As mass-market EV volumes climb, tiering blurs: chemical giants acquire converting capacity, while Tier 1s invest in polymer compounding to secure feedstock stability. The automotive acoustic material market thereby rewards vertical synergies and fast-track innovation pipelines.

Automotive Acoustic Material Industry Leaders

Autoneum Holding AG

Grupo Antolin

Auria Solutions

NVH Korea Inc.

Adient plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SEKISUI CHEMICAL CO., LTD. announced that its High Performance Plastics Company has seen its S-LEC™ Sound Acoustic Film SV, a high-performance interlayer film for laminated glass, chosen by Nissan Motor Co., Ltd. for the Patrol model. This film not only offers the traditional sound insulation benefits but also mitigates noise from vibrations.

- May 2025: Autoneum inked a deal to purchase all shares of Chengdu FAW-Sihuan Interior Parts Co., Ltd., a Chinese supplier specializing in acoustic and thermal management for the automotive sector.

Global Automotive Acoustic Material Market Report Scope

The scope includes segmentation by material type (polyurethane, polypropylene, polyvinyl chloride, fiberglass, textiles, rubber, foam, and others), application area (interior and exterior), vehicle type (passenger cars, light commercial vehicles, medium and heavy commercial vehicles, and buses and coaches), and sales channel (OEM and aftermarket). The analysis also covers regional-level segmentation, including North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. Market size and growth forecasts are presented by value in USD.

| Polyurethane |

| Polypropylene |

| Polyvinyl Chloride (PVC) |

| Fiberglass |

| Textiles |

| Rubber |

| Foam |

| Others |

| Interior |

| Exterior |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

| Buses and Coaches |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | Polyurethane | |

| Polypropylene | ||

| Polyvinyl Chloride (PVC) | ||

| Fiberglass | ||

| Textiles | ||

| Rubber | ||

| Foam | ||

| Others | ||

| By Application Area | Interior | |

| Exterior | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (MHCVs) | ||

| Buses and Coaches | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the automotive acoustic material market in 2025?

The automotive acoustic material market size is valued at USD 5.40 billion in 2025.

What CAGR is expected for automotive acoustic materials between 2026 and 2031?

The market is forecast to expand at a 4.28% CAGR through 2031.

Which material leads current demand for vehicle noise control?

Polyurethane holds the largest share at 40.25% because of its proven damping characteristics.

Where is regional growth fastest for acoustic materials?

Middle East and Africa lead growth with a 5.75% CAGR as new manufacturing hubs scale up.

Why are exterior acoustic applications gaining momentum?

High-speed EVs require underbody, wheel-arch, and aerodynamic treatments to curb wind and road noise, driving a 7.58% CAGR in exterior demand.

Page last updated on: