Car Audio Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

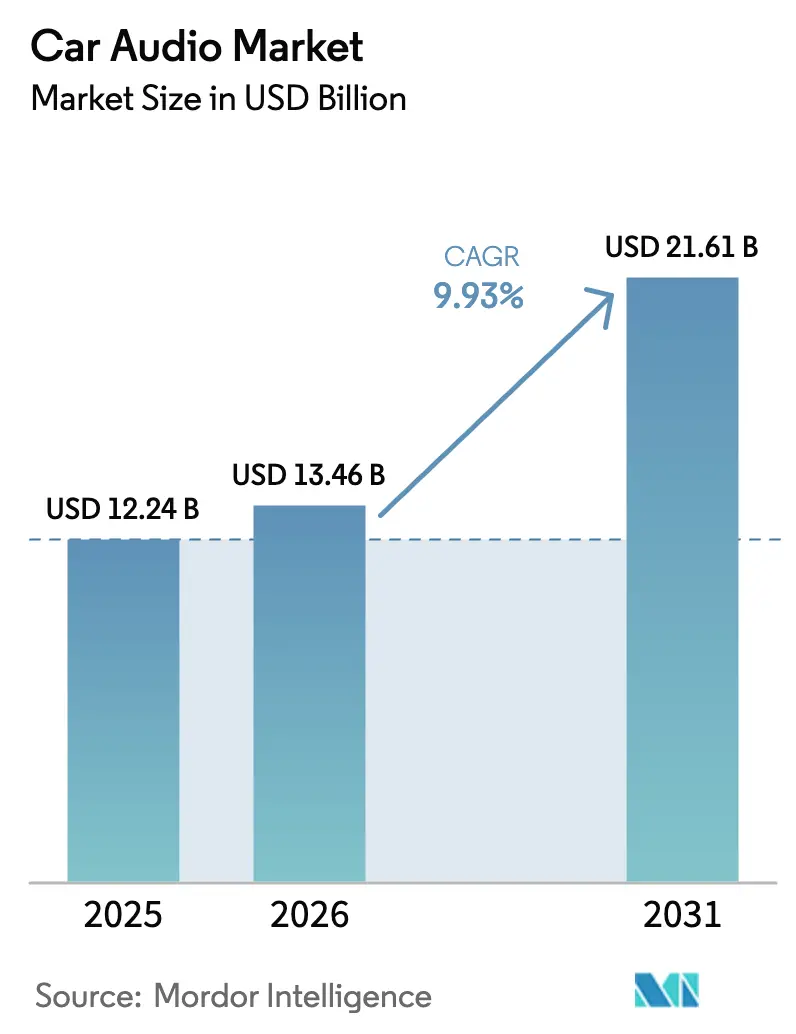

| Market Size (2026) | USD 13.46 Billion |

| Market Size (2031) | USD 21.61 Billion |

| Growth Rate (2026 - 2031) | 9.93% CAGR |

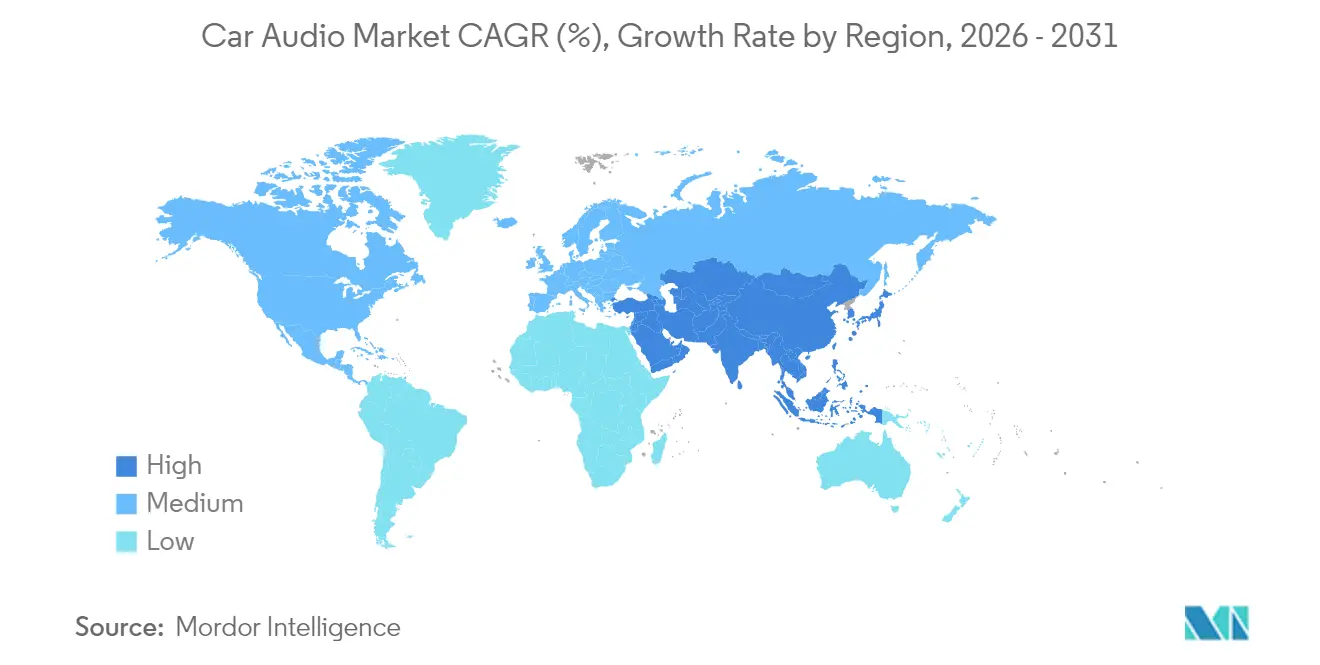

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

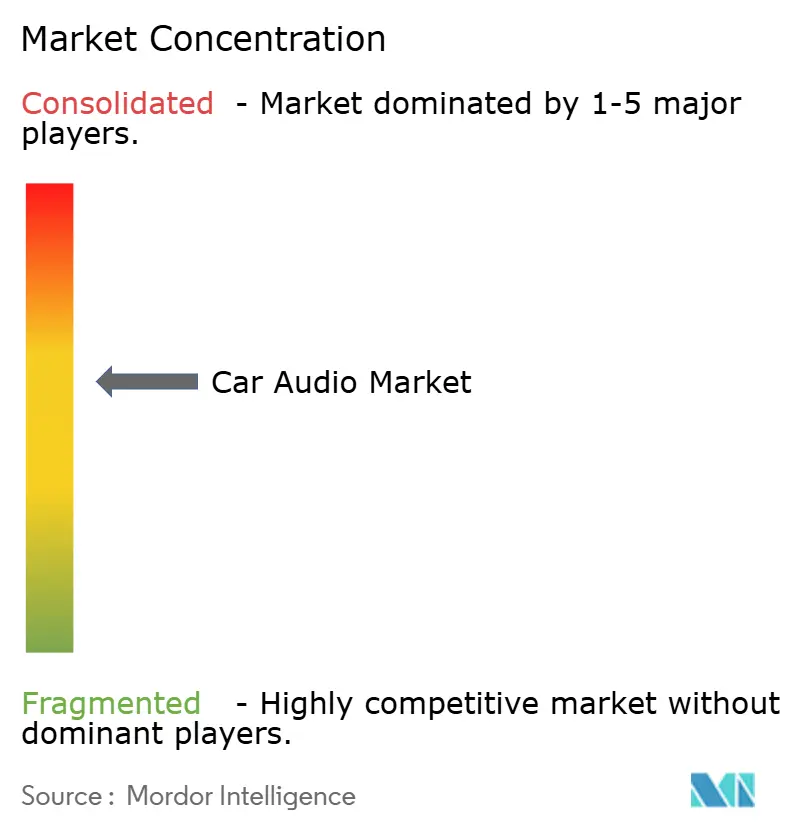

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Car Audio Market Analysis by Mordor Intelligence

The car audio market size was valued at USD 12.24 billion in 2025 and estimated to grow from USD 13.46 billion in 2026 to reach USD 21.61 billion by 2031, at a CAGR of 9.93% during the forecast period (2026-2031). Expansion is propelled by the rapid migration toward software-defined vehicles, growing consumer demand for voice-controlled interfaces, and the upselling of immersive 3-D sound packages. Automakers view premium in-cabin acoustics as a differentiator that supports brand positioning and subscription revenue streams in the car audio market. Suppliers are racing to optimize Class-D amplifiers that conserve battery energy in electric vehicles, while over-the-air (OTA) updates keep in-service fleets current without physical retrofits. Regional momentum is strongest in Asia Pacific, where short product cycles and high electric-vehicle penetration accelerate technology refresh.

Key Report Takeaways

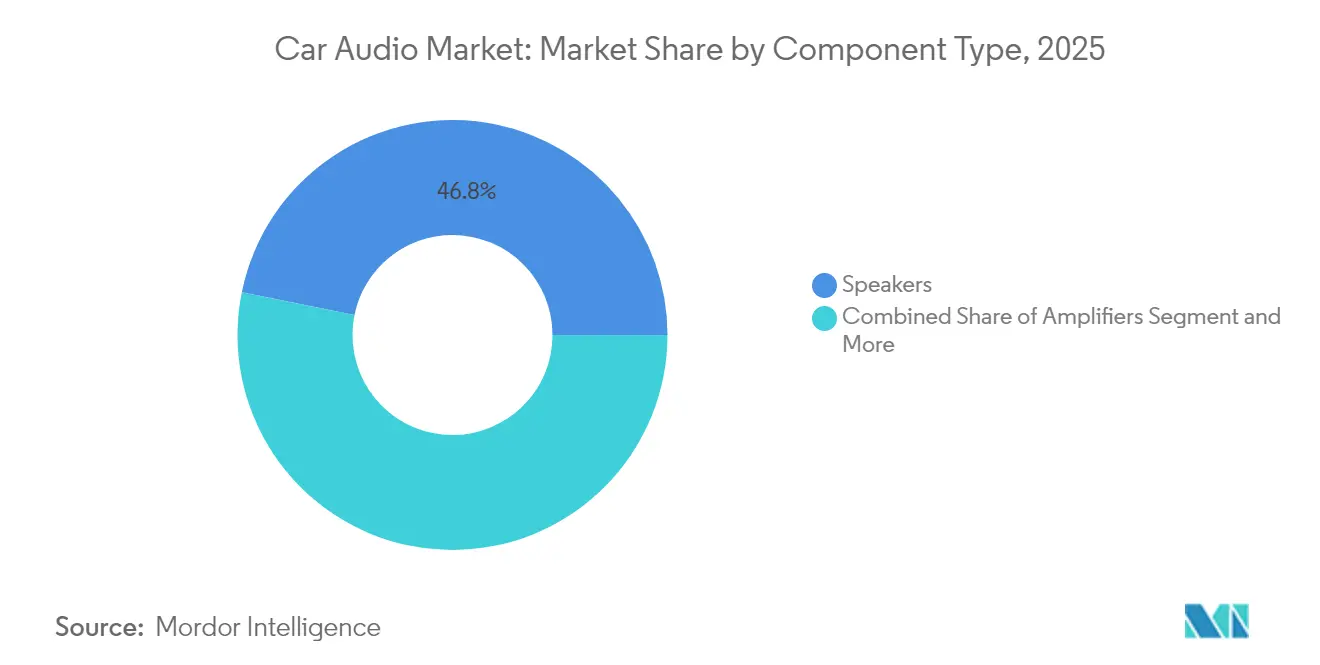

- By component type, speakers led with 46.81% of car audio market share in 2025; Class-D amplifiers are projected to post the fastest 11.41% CAGR through 2031.

- By vehicle type, SUVs captured 41.63% share of the car audio market size in 2025, and are poised to grow at an 11.19% CAGR to 2031.

- By sound-management mode, manual control held 62.74% share of the car audio market size in 2025, while AI-driven personalization is expanding at a 20.06% CAGR.

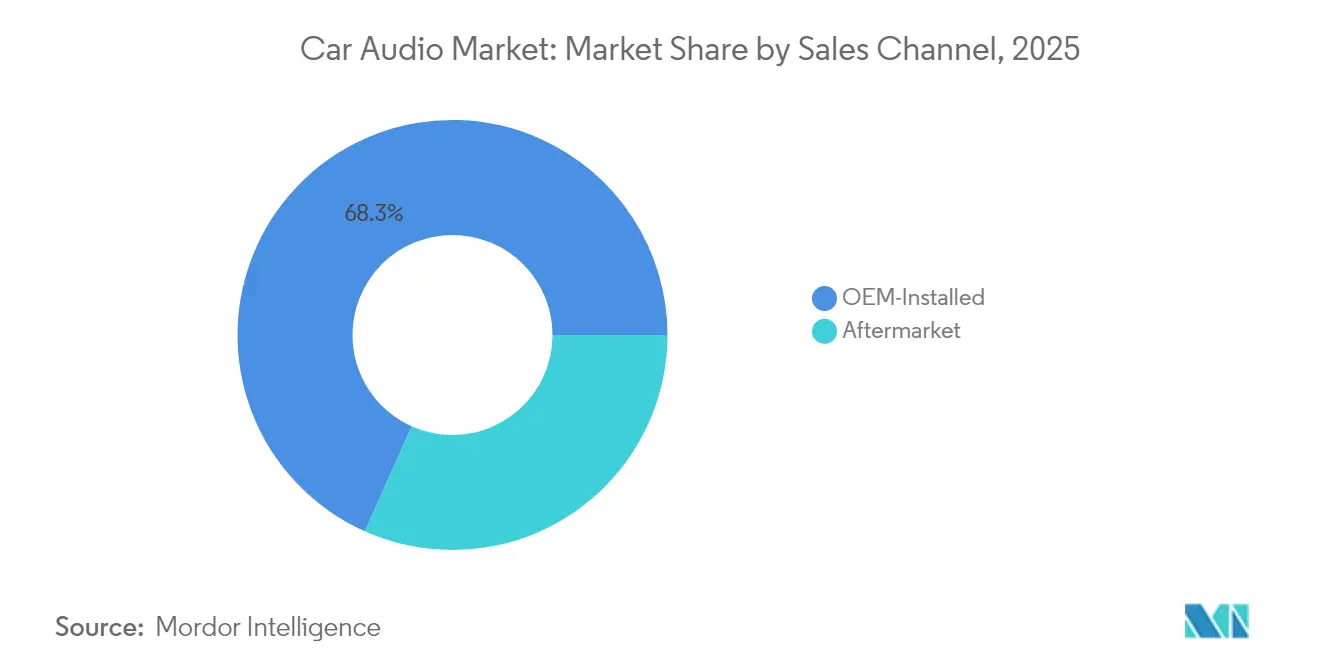

- By sales channel, OEM-installed systems accounted for 68.32% of the car audio market size in 2025; the aftermarket is advancing at a 12.18% CAGR.

- By connectivity technology, wired solutions retained 51.97% of the car audio market share in 2025, yet wireless ultra-wideband is rising at a 15.48% CAGR.

- By geography, Asia Pacific dominated with 43.23% share of the car audio market size in 2025 and the highest 11.14% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Car Audio Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Voice-Controlled Audio Baseline | +2.8% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Class-D Amplifier Migration | +2.1% | Global, concentrated in APAC and North America EV markets | Long term (≥ 4 years) |

| 3-D / Immersive Sound Packages | +1.9% | North America and EU premium segments, expanding to APAC | Medium term (2-4 years) |

| SDV Audio Feature | +1.7% | Global, led by Tesla and Chinese OEMs | Short term (≤ 2 years) |

| Plug-And-Play Upgrade Kits | +1.4% | North America and EU aftermarket, emerging in APAC | Short term (≤ 2 years) |

| Lighter Speaker Designs | +1.2% | Global, priority in EV-focused markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Voice-Controlled Audio Baseline in MY-27 Vehicles

Volkswagen already integrates a ChatGPT-powered assistant in its European portfolio that supports conversational commands[1]“Volkswagen Voice Command Integration,” Volkswagen Newsroom, volkswagen.com. The shift removes physical buttons, frees dashboard space, and enables paid upgrades delivered by voice, influencing innovation across the car audio market.Suppliers must secure AI partnerships early because automakers lock preferred stacks into long development cycles that freeze specifications years ahead. The trend also raises privacy expectations, prompting on-device processing that avoids cloud latency and data exposure.

Class-D Amplifier Migration for EV Efficiency

Electric vehicle architectures cannot tolerate wasted watts. Class-D designs reach 90% efficiency, extending range and reducing thermal load. Asian factories specify Class-D across mid-segment models, pressuring North American badge engineers to follow suit. New silicon integrates one-inductor modulation that cuts part counts and board size, easing packaging in crowded instrument panels. OEM procurement teams prefer suppliers that offer retrofit-ready modules for legacy platforms, ensuring consistent sound reproduction while meeting tougher efficiency mandates. The incremental energy savings, though small per vehicle, scale across millions of units and thus carry strategic weight for fleet-level carbon compliance within the car audio market.

Upselling Of 3-D / Immersive Sound Packages

Immersive surround systems create high-margin options that buyers willingly add at the checkout screen. Dolby Laboratories will equip Cadillac’s 2026 electric lineup with Atmos capabilities, signaling that spatial audio has graduated from concept cars to mainstream luxury[2]“Dolby and General Motors bring Dolby Atmos to Cadillac’s entire 2026 EV lineup,” Dolby Laboratories Investor Relations, dolby.com. Gross profit on software-enabled sound modes often exceeds 60%, sustaining revenue beyond the initial sale. As autonomous functions increase cabin dwell-time, consumers value theater-quality playback that turns vehicles into personal entertainment hubs. Component costs fall with volume, allowing premium features to cascade into mid-price trim levels across the car audio market.

SDV Audio Feature Unlocks Via OTA

Once a vehicle rolls off the line, audio functionality no longer remains static. Automakers now issue OTA updates that activate equalizer presets, additional speaker channels, or adaptive noise cancellation. This service-oriented model can halve development expenditure by shifting late changes into software releases. OTA also provides anonymized user data that guides iterative tuning, influencing future product roadmaps. Early adopters such as global EV specialists demonstrate that paid downloads improve lifetime value, and traditional brands are replicating the blueprint to preserve competitiveness within the car audio market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Security Certification Delays | -2.3% | Global, particularly EU under UN Regulation No. 155 | Short term (≤ 2 years) |

| DSPs and MEMS Mics' Shortage | -1.8% | Global supply chain, concentrated impact in APAC manufacturing | Medium term (2-4 years) |

| Right-to-Repair Margin Squeeze | -1.2% | North America & EU regulatory focus | Medium term (2-4 years) |

| Speaker Count Limitations | -0.9% | Global EV markets, priority in Europe and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SDV Cyber-Security Certification Delays

Since July 2024, all new cars sold in the EU must comply with UN Regulation No. 155. Laboratories such as TÜV SÜD report queues for approval slots, postponing launch schedules and revenue recognition[3]“Mandatory digital shield for all new cars,” TÜV SÜD, tuvsud.com. Smaller audio suppliers lack dedicated cyber teams, stretching project budgets and sometimes leading OEMs to isolate audio domains from high-risk networks, limiting advanced feature integration. Every delay compresses the technology roadmap and reduces the window for monetizing audio upgrades, tempering near-term growth in the car audio market.

Shortage of Automotive-Grade DSPs and MEMS Mics

Automotive qualification requires components that withstand vibration and extreme temperatures for 15 years, conditions that consumer-grade parts cannot meet. Foundry capacity remains tight, particularly for 28-nanometer mixed-signal nodes used in digital signal processors. Lead times of up to 60 weeks force redesigns around second-source silicon, often compromising channel count or processing overhead. Voice-recognition arrays need multiple MEMS microphones, and limited supply compels OEMs to stagger feature rollouts, delaying penetration of AI-driven personalization across the car audio market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Speakers Anchor Acoustic Value

Speakers contributed 46.81% of the car audio market share in 2025, underscoring their role as the primary perception driver of audio quality. Demand rises for slimline diaphragm designs that use lightweight composites, allowing automakers to embed drivers inside headliners and seats without adding mass. Class-D amplifiers follow as the high-growth component at 11.41% CAGR, pushed by electric-vehicle energy budgets that penalize inefficiency. Integration trends favor system-on-chip audio controllers that merge digital processing, amplification, and diagnostics into a single enclosure, reducing wiring weight and assembly time.

Software-defined architectures shift equalization and loudness management from discrete DSP boxes into central compute domains within the car audio market. This simplification frees dashboard real estate, yet places heightened accuracy requirements on speaker cones that must faithfully reproduce algorithmic outputs. Suppliers respond with low-profile woofers that extend frequency response below 30 Hz without the need for bulky enclosures. Piezo-based exciters capable of turning door panels into resonating surfaces enter pilot production, promising up to 90% packaging volume reduction.

By Vehicle Type: SUVs Outperform Other Formats

SUVs accounted for 41.63% of car audio market size in 2025, and hold the highest 11.19% CAGR outlook to 2031. Their larger cabins support additional speaker placements, enabling immersive 19-channel sets that command a premium price. High rooflines ease antenna packaging for wireless subwoofers that maintain bass performance without structural vibration. Hatchbacks and sedans lose share to crossovers, yet they retain volume in cost-sensitive regions where compact body styles remain popular. Sports cars occupy niche positions but often specify flagship audio to justify brand pedigrees.

As electrification proliferates, SUVs transition into lifestyle hubs, hosting work calls, gaming sessions, and streaming content during charging stops. This usage profile increases dwell-time, driving consumer willingness to pay for upgraded sound. Manufacturers leverage modular audio platforms that scale from 8 speakers in entry trims to 24 speakers in luxury variants without rewiring the harness, optimizing margin capture across the car audio market.

By Sound-Management Mode: AI Personalization Scales Quickly

Manual adjustment dominated with 62.74% share of the car audio market size in 2025, yet AI-driven personalization is forecast to expand at 20.06% CAGR. The shift pivots on biometric sensors that detect stress, heart rate, and vocal tone to curate playlists and adjust equalization automatically. Voice recognition remains a transitional mode, bridging manual control and full AI orchestration. Automakers deploy cloud-trained models that run locally to enable latency-free adaptation during tunnels or rural zones with poor connectivity.

Revenue stems from tiered subscription plans that unlock advanced profiles such as fatigue-reduction audio or child-sleep mode, fortifying profitability across the car audio market. Deployments already demonstrate emotional mapping that aligns musical key signatures with driver mood, reinforcing brand differentiation. Early adopters report net-promoter-score gains of up to 15 points, illustrating commercial upside beyond hardware amortization.

By Sales Channel: Aftermarket Returns to Growth

OEM systems contributed to a 68.32% car audio market share in 2025, yet the aftermarket grows at 12.18% CAGR, fueled by do-it-yourself customers purchasing plug-and-play kits online. Cloud-based configurators match vehicle VINs to harness adapters, eliminating installation guesswork. Electric-vehicle owners often seek sub-woofer upgrades to replace engine-noise masking removed with the powertrain switch, providing new replacement cycles.

Brick-and-mortar car-audio specialists pivot from hardware margins to software flashing services that activate surround modes or update amplifier profiles. These trends enlarge total lifetime revenue per vehicle, cementing the aftermarket’s strategic relevance inside the car audio market. The channel dynamics create opportunities for suppliers who can serve both OEM integration requirements and aftermarket customization demands through modular product architectures and flexible distribution strategies.

By Connectivity Technology: Wireless Adoption Accelerates

Wired protocols such as MOST and A2B accounted for 51.97% of the car audio market size in 2025 because they guarantee consistent bandwidth and minimal latency. However, wireless ultra-wideband (UWB) support is rising at 15.48% CAGR; by 2030, wireless is expected to overtake legacy cabling in premium trims. UWB enables centimeter-scale positioning that pairs personal devices to specific seat zones, allowing individualized volume and content streams.

Dual-mode chips now integrate Wi-Fi 7, Bluetooth 5.4, and UWB within a single package, cutting bill-of-materials by approximately 20%. As driverless robo-taxis emerge, contactless sanitization guidelines favor cable-free interiors, accelerating wireless momentum within the car audio market.

Geography Analysis

Asia Pacific led with 43.23% share of the car audio market size in 2025, and is forecast to grow at 11.14% CAGR. Chinese automakers are projected to secure around one-fourth of the global vehicle share by 2030, underpinning volume demand for locally manufactured speakers and amplifiers. National industrial policy subsidizes domestic supply chains, allowing system integrators to cut lead times to 20 months, half the duration of traditional programs. South Korea and Japan augment regional momentum through advanced semiconductor ecosystems that feed Class-D amplifier modules, while India emerges as an assembly hub for entry-segment infotainment head units.

North America is the second-largest buyer, driven by consumer preference for large SUVs and pick-ups that provide abundant cabin space for multi-channel audio. Growth is slower because penetration exceeds 90%, yet upgrade rates remain healthy as OTA functions extend feature life cycles. Dealers bundle subscription trials with new models, converting about 25% of owners into recurring revenue plans.

Europe absorbs stringent cyber rules that lengthen validation cycles. Nevertheless, the bloc sets acoustic design trends that eventually globalize, such as mandated pedestrian warning sounds for electric cars, which require smart amplification and directional speakers. The Middle East and Latin America present smaller baselines but double-digit expansion owing to rising disposable income and grey-market imports of premium head units. Africa remains nascent, yet smartphone integration demand seeds future adoption of cost-optimized wireless audio within the car audio market.

Competitive Landscape

The car audio market is moderately concentrated. Recent transactions reinforce portfolio depth. Harman agreed to acquire Sound United’s consumer brands for USD 350 million in May 2025, extending its premium label roster. Gentex closed its USD 196 million purchase of VOXX International in April 2025, gaining Klipsch and Onkyo product lines that align with vehicle acoustic applications. Dolby secured design wins that embed Atmos across Cadillac’s electric range, demonstrating that algorithm ownership, not hardware, drives margin.

Start-ups focusing on AI voice analytics license models to multiple Tier-1 suppliers, indicating that intellectual property remains fragmented. Incumbents respond by setting up venture funds to lock in early access to promising code bases.

Bargaining power shifts toward automakers adept at in-house software, compelling suppliers to offer open APIs and firmware-over-the-air frameworks. The resulting ecosystem favors firms integrating microphone arrays, amplifiers, and cloud back-ends into cohesive offerings, preserving relevance in the evolving car audio market.

Car Audio Industry Leaders

Bose Corporation

Panasonic Holdings Corporation

Harman International Industries Inc.

Continental AG

Hyundai Mobis Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Harman International announced definitive agreement to acquire Masimo Corporation’s Sound United consumer audio business for USD 350 million.

- April 2025: Gentex Corporation completed acquisition of VOXX International, integrating premium audio brands and iris-biometric modules.

- March 2025: Dolby Laboratories and General Motors confirmed Dolby Atmos rollout across Cadillac’s 2026 electric portfolio, covering the Escalade IQL and Lyriq-V models.

Global Car Audio Market Report Scope

Car audio systems, installed in vehicles, entertain and inform passengers. These systems comprise multiple components, all collaborating to achieve optimal sound quality.

Car Audio System is segmented by component type, vehicle type, sound management, sales channel, and geography. By component type, the market is segmented into speakers, amplifiers, and head units. By vehicle type, the market is segmented into hatchbacks, sedans, sports utility vehicles, and multi-purpose vehicles. By sound management, the market is segmented into voice recognition and manual. By sales channel, the market is segmented into original equipment manufacturers, and aftermarket. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, the market sizing and forecast have been done based on the value (USD) for all the above segments.

| Speakers | 2-Way |

| 3-Way | |

| 4-Way and Coaxial | |

| Amplifiers | Class-AB |

| Class-D | |

| Head Units / DSP | |

| Microphones and ANC Controllers |

| Hatchback |

| Sedan |

| SUVs |

| MPVs |

| Manual |

| Voice Recognition |

| AI-Driven Personalization |

| OEM-Installed |

| Aftermarket |

| Wired (MOST, A2B) |

| Wireless (Bluetooth, Wi-Fi, UWB) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Component Type | Speakers | 2-Way |

| 3-Way | ||

| 4-Way and Coaxial | ||

| Amplifiers | Class-AB | |

| Class-D | ||

| Head Units / DSP | ||

| Microphones and ANC Controllers | ||

| By Vehicle Type | Hatchback | |

| Sedan | ||

| SUVs | ||

| MPVs | ||

| By Sound-Management Mode | Manual | |

| Voice Recognition | ||

| AI-Driven Personalization | ||

| By Sales Channel | OEM-Installed | |

| Aftermarket | ||

| By Connectivity Technology | Wired (MOST, A2B) | |

| Wireless (Bluetooth, Wi-Fi, UWB) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the car audio market?

The car audio market is valued at USD 13.46 billion in 2026.

How fast is the car audio market expected to grow?

It is forecast to expand at a 9.93% CAGR, reaching USD 21.61 billion by 2031.

Which region leads the car audio market?

Asia Pacific accounts for 43.23% of global revenue and exhibits the highest 11.14% CAGR.

Why are Class-D amplifiers important for electric vehicles?

Class-D architectures deliver up to 90% efficiency, reducing battery load and extending driving range.

What role do over-the-air updates play in automotive audio?

OTA updates enable manufacturers to unlock new sound features post-purchase, generating recurring revenue and keeping in-service vehicles current.

Page last updated on: