Automotive Operating Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

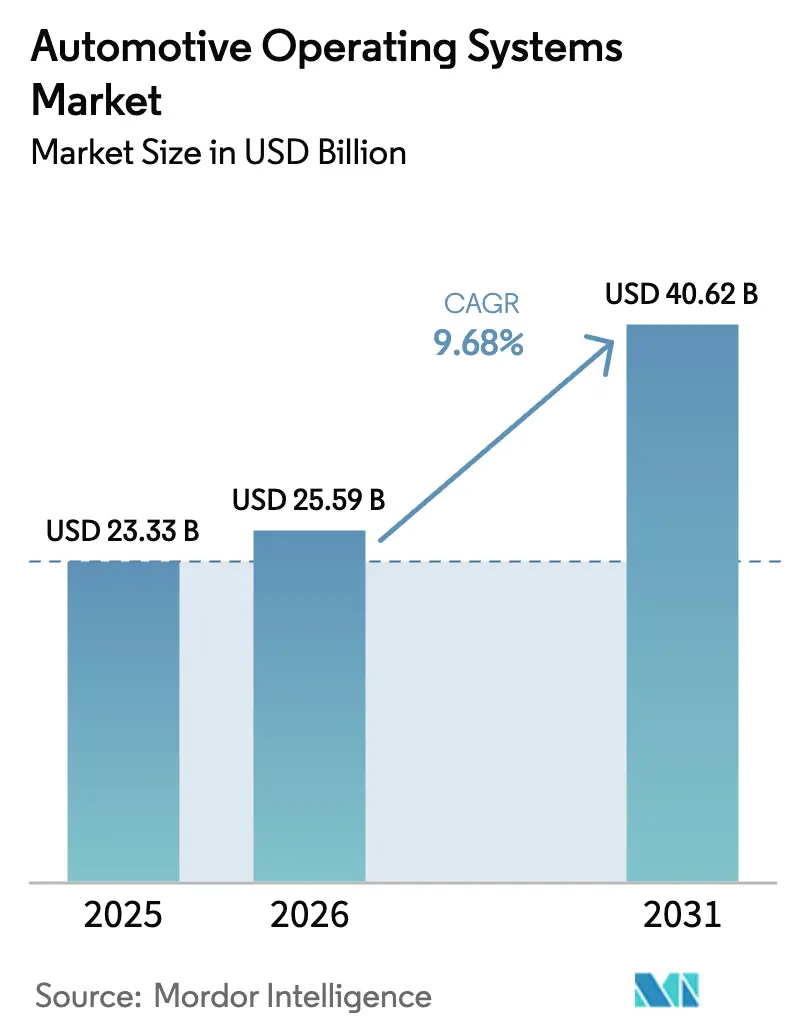

| Market Size (2026) | USD 25.59 Billion |

| Market Size (2031) | USD 40.62 Billion |

| Growth Rate (2026 - 2031) | 9.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Operating Systems Market Analysis by Mordor Intelligence

The automotive operating systems market size is expected to grow from USD 23.33 billion in 2025 to USD 25.59 billion in 2026 and is forecast to reach USD 40.62 billion by 2031 at 9.68% CAGR over 2026-2031. [1]Semiconductor Industry Association, “State of the Industry 2024,” semiconductors.org Growing electrification, ubiquitous connectivity, and rapid AI adoption have made the operating system the core integration layer that links sensors, domain controllers, and cloud back-ends. Cyber-security regulations such as UNECE WP.29 R155 and R156 triggered mandatory software updates and security management capabilities for every new vehicle type sold in UNECE markets from July 2024 forward, accelerating OEM demand for certified software stacks. Semiconductor supply stabilized as global chip revenue rebounded to USD 527 billion in 2024, ensuring the processing headroom needed for next-generation cockpit and autonomy platforms. Asia-Pacific led with 44.9% market share in 2024, propelled by China’s push for home-grown operating systems such as HarmonyOS, which had logged more than 1.2 billion kilometers of on-road usage by late 2024. Competition intensified as tech majors entered the segment, illustrated by Qualcomm and Google’s cloud-native Snapdragon Digital Chassis Workbench that lets developers complete validation entirely online.

Key Report Takeaways

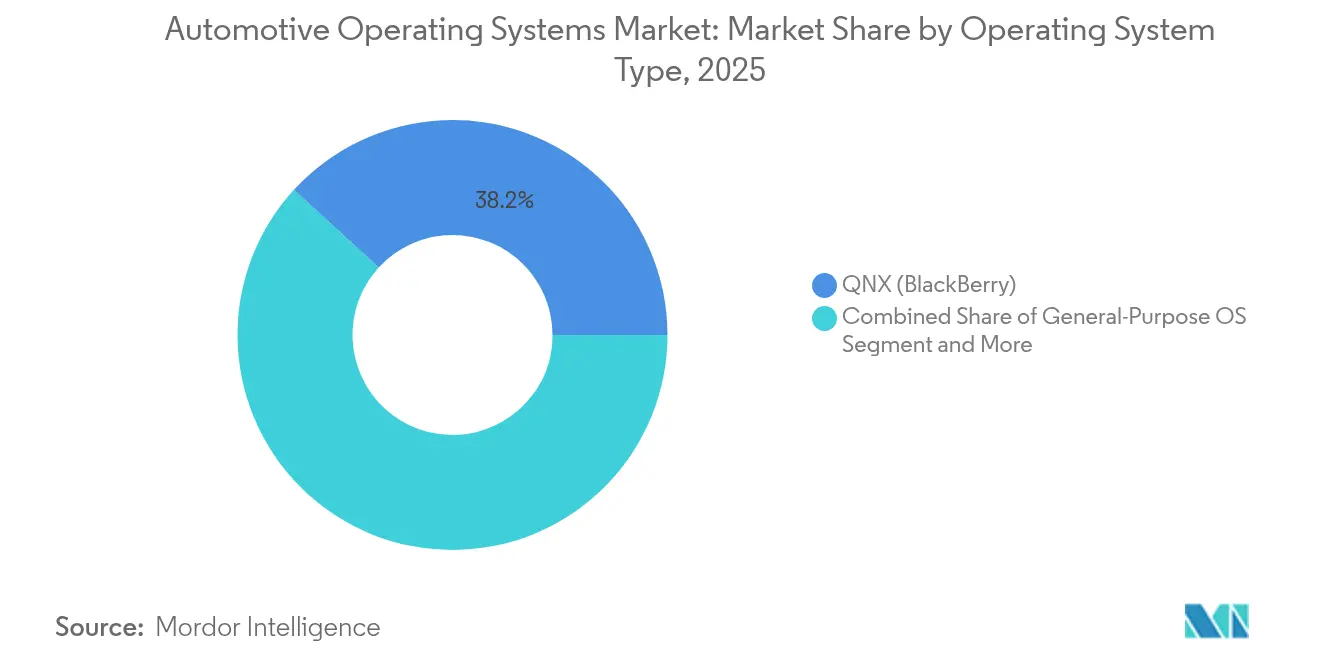

- By operating system type, QNX held 38.20% of the automotive operating systems market share in 2025, while Android Automotive is forecast to grow at a 17.47% CAGR to 2031.

- By vehicle type, passenger cars accounted for 65.70% of the automotive operating systems market in 2025; light commercial vehicles are projected to expand at a 10.12% CAGR through 2031.

- By application, infotainment and digital cockpit led with 42.20% revenue share in 2025; ADAS and autonomous driving applications are advancing at a 16.78% CAGR to 2031.

- By propulsion, ICE platforms accounted for 54.30% of the automotive operating systems market in 2025, but battery electric vehicles are set to grow at a 13.42% CAGR.

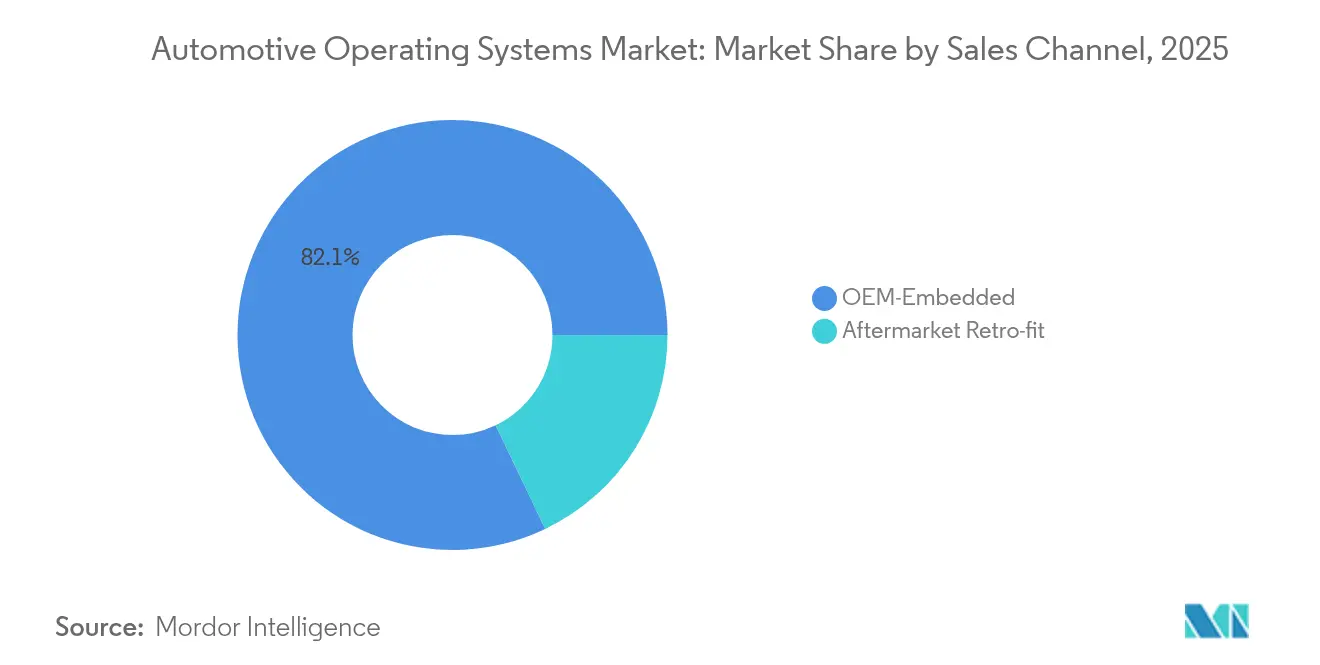

- By sales channel, OEM-installed stacks accounted for 82.10% of the automotive operating systems market in 2025. Aftermarket Retro-fit is advancing at a 7.88% CAGR to 2031.

- By level of autonomy, Level 0-1 accounted for 57.40% of the automotive operating systems market in 2025. However, Level 4-5 prototypes is advancing at a 23.10% CAGR.

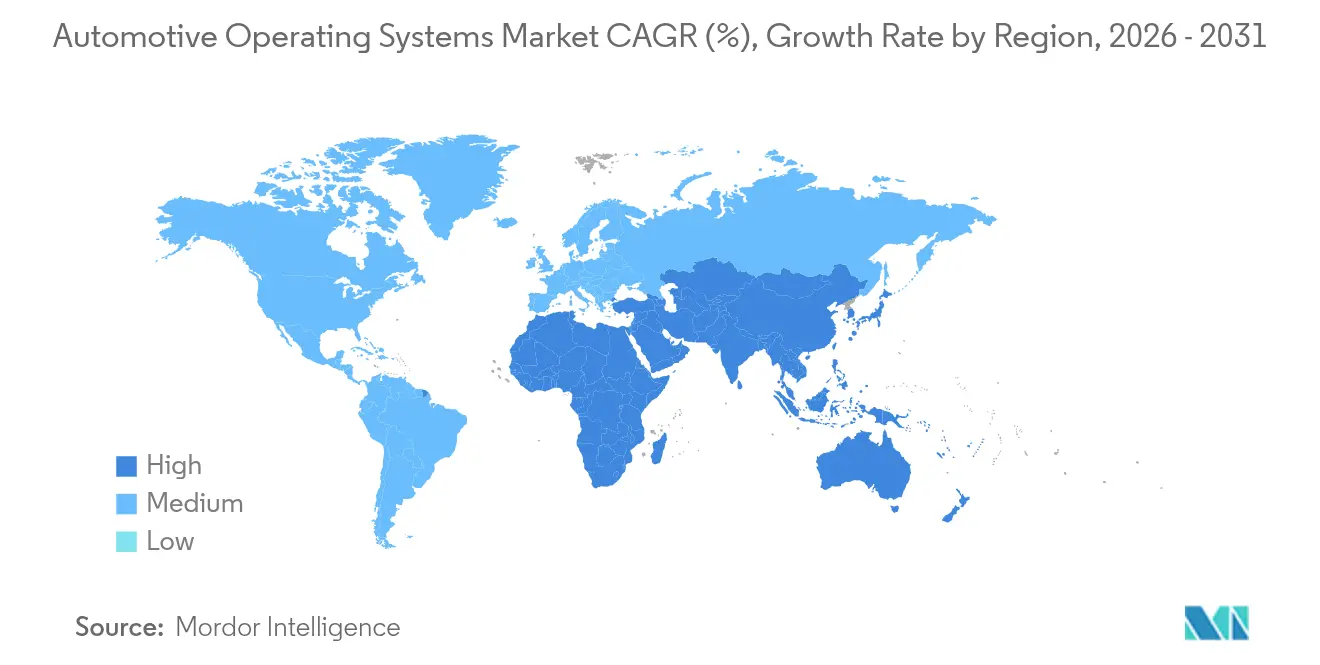

- By geography, Asia-Pacific captured 44.30% of the automotive operating systems market size in 2025; the Middle East and Africa region is expected to post the fastest 11.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Operating Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand surge for connected and autonomous vehicles | +2.1% | Global, with APAC and North America leading | Medium term (2-4 years) |

| AI/ML integration across in-vehicle domains | +1.8% | Global, concentrated in premium segments | Long term (≥ 4 years) |

| Regulatory push on cybersecurity and functional safety | +1.4% | Europe and North America primarily | Short term (≤ 2 years) |

| Transition to software-defined vehicle and OTA update monetization | +2.3% | Global, with early adoption in China and North America | Medium term (2-4 years) |

| Cloud-native virtual validation accelerating OS release cycles | +0.9% | Global, concentrated in major OEM centers | Short term (≤ 2 years) |

| Freemium licensing models expanding developer ecosystem | +0.7% | Global, particularly in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand surge for connected and autonomous vehicles

Level-2 and above automation features have become standard even in mid-segment cars, pushing OEMs to embed deterministic, high-throughput operating systems that can fuse multi-modal sensor inputs in real time. NVIDIA’s DriveOS, shipped with drive-ready AI accelerators, provided OEMs a turnkey safety-certified stack that reduced software validation cycles by 30% in pilot programs. Mercedes-Benz started fitting DriveOS-based compute units in 2024 series models, signalling how premium brands leverage OS choice as a differentiation lever. Hyundai integrated its Connected-Car OS with NVIDIA silicon to prepare 20 million connected vehicles for over-the-air (OTA) feature releases by 2025. These deployments illustrate how the automotive operating systems market is expanding beyond infotainment into autonomous driving compute domains.

AI/ML integration across in-vehicle domains

OEMs now embed on-device machine-learning engines for energy management, cabin personalization, and predictive diagnostics. BMW linked its cloud analytics with edge AI in 2024 to cut unplanned service visits by 30%, using an OS-level abstraction layer that streams sensor data to learning models. Toyota partnered with NTT to feed real-time traffic inputs into a city-scale routing engine that lowered average urban travel times by 20%, requiring operating systems able to orchestrate vehicle-to-cloud data flows under 100 ms latency. HarmonyOS 5.0 integrated neural scene-rendering to deliver immersive 3-D dashboards that learn driver preferences over time. Such roll-outs keep the automotive operating systems market on a steep AI adoption curve.

Regulatory push on cybersecurity and functional safety

UNECE WP.29 R155 and R156 entered full-vehicle enforcement in July 2024, forcing every carmaker selling into UNECE territories to maintain a certified Cybersecurity Management System and Software Update Management System. TÜV SÜD advised OEMs to align ISO 26262 and ISO/SAE 21434 processes early to minimize re-certification costs, prompting suppliers to bake safety-security co-engineering into the OS core. Compliance pressures accelerated purchases of pre-certified kernels such as QNX, which already carried ASIL D credentials and reduced audit time by up to 40% in European programs. [2]BlackBerry Limited, “QNX Software Embedded in 235 Million Vehicles Worldwide,” blackberry.com These mandates are lifting baseline requirements across the automotive operating systems market.

Transition to software-defined vehicle and OTA monetization

Hyundai allocated USD 18 trillion won through 2030 to make every model software-defined, promising lifetime OTA feature upgrades and subscription services. The 2025 SDV survey found that 67% of auto executives already ship OTA updates, and 82% see software revenue as key to customer-experience goals. Qualcomm and Google’s Digital Chassis Workbench demonstrates how cloud toolchains can cut OTA validation cycles from weeks to hours. These developments underline how recurring software revenue streams sustain long-term expansion of the automotive operating systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cyber-security vulnerabilities | -1.6% | Global, with stricter enforcement in Europe | Short term (≤ 2 years) |

| System complexity and legacy integration hurdles | -2.1% | North America and Europe primarily | Medium term (2-4 years) |

| Scarcity of certified automotive-grade software talent | -1.3% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| OEM concerns over platform lock-in and IP leakage | -0.8% | Global, particularly among traditional OEMs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-privacy and cyber-security vulnerabilities

BlackBerry reported blocking 5.2 million automotive-related malware attacks between September and December 2023, half of which relied on never-seen exploits. General Motors halted an Apple CarPlay retrofit project in 2024, citing risks that uncertified software could interfere with drive-train control modules. Europe’s Cyber Resilience Act will impose mandatory security updates for the full vehicle lifecycle, raising compliance costs for smaller vendors. These threats temper near-term growth expectations for the automotive operating systems market.

System complexity and legacy integration hurdles

Vehicles still carry 100+ ECUs, many running proprietary code—even as OEMs migrate toward centralized, zone-based compute. Perforce observed that mixed build environments add 30% effort to DevOps cycles when consolidating legacy modules. Wind River Studio Developer was adopted by Tata Elxsi in 2024 to automate safety analyses and cut software release time by 15%, yet multi-OS hypervisor stacks remain hard to tune. Integration drag therefore subtracts momentum from the automotive operating systems market in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operating System Type: QNX Retains the Safety Core while Android Expands the Consumer Layer

QNX captured 38.20% of the automotive operating systems market share in 2025 on the strength of its ASIL D pedigree in braking, steering, and chassis domains. Android Automotive logged the fastest 17.47% CAGR outlook as OEMs sought familiar user-interface paradigms and effortless cloud tie-ins.

BlackBerry disclosed that its code base shipped inside 235 million vehicles worldwide, reinforcing its entrenched safety position. Yet Ford’s decision to adopt Android for its 2024 cockpit refresh illustrated how consumer-oriented ecosystems are often prioritized over niche real-time kernels. Hypervisor designs such as QNX Hypervisor 8.0 let Android and Linux share silicon with QNX, providing a mixed-criticality bridge that keeps legacy safety code intact while hosting Google Play services. These patterns show the automotive operating systems market adjusting to polarized safety and infotainment demands.

By Vehicle Type: Commercial Fleets Accelerate Digital Uptake

Passenger cars provided 65.70% of the automotive operating systems market size in 2025, thanks to unit scale, yet light commercial vehicles are forecast to compound at 10.12% annually as delivery operators digitize routing, telematics, and predictive maintenance.

Fleet managers now demand OTA-driven uptime gains. Hyundai Mobis selected QNX Hypervisor for a logistics-grade cockpit that runs diagnostics and navigation isolation on a single SoC, cutting BOM cost by 12%. Heavy trucks adopt similar stacks to orchestrate platooning and driver fatigue analytics. Because commercial vehicles log 2–3× the annual mileage of passenger cars, software value per unit is higher, keeping the automotive operating systems market firmly tied to fleet modernization.

By Application: ADAS Overtakes the Dashboard as Growth Engine

Infotainment and digital cockpit still owned 42.20% revenue in 2025, but ADAS and autonomy workloads are on track for a 16.78% CAGR through 2031.

Applied Intuition’s validation suite runs millions of edge-case simulations, feeding certified operating systems that must juggle sensor fusion pipelines under ASIL D rules. Battery management, energy routing, and V2G services are now folded into OS-level scheduling, reflecting how the automotive operating systems market is migrating from single-purpose clusters toward unified compute substrates.

By Propulsion Type: Electric Platforms Redefine Software Scope

ICE architectures still contributed 54.30% of the automotive operating systems market size in 2025, yet battery electric vehicles are accelerating at a 13.42% CAGR as specialized OS modules supervise cell aging, fast-charge currents, and thermal envelopes.

NXP’s BMS reference design achieved ±2 mV accuracy while meeting ASIL D, showcasing the precision electric drivetrains require from the underlying OS. The push to integrate vehicle-to-grid interfaces further expands software footprints, amplifying addressable revenue inside the automotive operating systems market.

By Sales Channel: Aftermarket Seeks Its Place in a Secure-Update World

OEM-installed stacks dominated 82.10% of 2025 shipments, a logical outcome given that cybersecurity rules make uncertified retrofits risky. Aftermarket kits still draw 7.88% CAGR interest as owners of older models pursue wireless smartphone functions.

BMW approved the MMI Pro retrofit that respects iDrive safety layers while adding Android Auto, signalling that aftermarket success hinges on tight OEM collaboration. Regulatory limits on back-door firmware flashes keep growth moderate, but niche demand ensures the automotive operating systems market supports a healthy modification ecosystem.

By Level of Autonomy: L4–L5 Programs Fuel Compute Upsizing

Level 0–1 comfort assists still formed 57.40% of units shipped in 2025. However, Level 4–5 prototypes are scaling at a 23.10% CAGR, soaking up multi-SoC clusters and redundant OS kernels.

Mercedes-Benz obtained Level 3 approval for Drive Pilot in Germany, with QNX partitioning safety logic from Linux-based infotainment. Green Hills INTEGRITY supplied a hypervisor that let ASIL D tasks co-exist with consumer apps in early robotaxi pilots. Such architectures are expected to accelerate revenue concentration at the upper strata of the automotive operating systems market.

Geography Analysis

Asia-Pacific led with 44.30% of the automotive operating systems market size in 2025, anchored by China’s vertically integrated approach that couples HarmonyOS with in-house AI chips. Huawei reported 412,100 end users on its smart-driving suite before 2025, demonstrating how domestic stacks can scale quickly when backed by local supply chains. Japan’s industry ministry facilitated a software alliance between Toyota, Honda, and Nissan to capture 30% of global software-defined vehicle revenue by standardizing middleware layers, an initiative that may raise the region’s stake further.

Europe continued to invest in sovereign software talent even as UNECE cyber-security rules raised compliance costs. Volkswagen’s CARIAD unit built a common vehicle OS and cloud for all group brands, aiming to reduce per-model software effort by 40%. Valeo teamed with AWS in 2025 to migrate validation workflows to cloud-native infrastructure, enabling over-the-air feature releases within days rather than weeks. Red Hat received ASIL-B certification for its in-vehicle Linux, providing an open-source option that aligns with European safety doctrines.

North America remained the testbed for tech-automotive collaboration. Qualcomm and Google offered the browser-based Workbench that compiles, flashes, and tests vehicle code entirely in the cloud, trimming prototyping cycles by 50%. Hyundai pledged USD 21 billion of United States investment, reserving USD 6 billion for autonomous-driving AI research with Boston Dynamics and NVIDIA. Meanwhile, the Middle East and Africa posted an 11.12% CAGR outlook as green-field mobility projects adopted EV-centric OS stacks without legacy constraints, opening whitespace for new entrants in the automotive operating systems market.

Competitive Landscape

The competitive field is moderately concentrated yet dynamic. BlackBerry QNX held the largest installed base and remained the de-facto kernel for safety-critical workloads, shipping inside 235 million vehicles to date. Google’s Android Automotive expanded quickly on the back of consumer-services integration and now powers infotainment on models from Volvo, Ford, and GM.

Qualcomm leverages its Snapdragon Digital Chassis silicon tie-in to lock design wins that bundle OS, connectivity, and cloud services. Huawei, backed by HarmonyOS and self-designed Kirin chips, captured headline contracts with domestic OEMs and has started joint deployments with BMW in China. NVIDIA promotes DriveOS as a purpose-built stack optimized for GPU-heavy autonomy workloads, carving a niche among premium ADAS developers.

Strategic partnerships set the tone. HaleyTek and BlackBerry unveiled a VirtIO-based Generic Automotive Platform in September 2024, enabling agile Android-Automotive cockpit builds on top of a certified hypervisor. Wind River secured a contract with Tata Elxsi for DevSecOps orchestration that will service multiple OEMs, signalling growing demand for cloud-managed pipelines. Li Auto went open source with Halo OS in 2025, giving developers visibility into its zone-controller architecture and potentially accelerating third-party innovation.

White-space remains in domain-specific micro-kernels that optimize battery charging, thermal management, and vehicle-to-grid interactions. Vendors that can provide both ASIL-D assurances and a modern app framework are likely to claim disproportionate share of incremental revenue as the automotive operating systems market pivots to recurring software monetization.

Automotive Operating Systems Industry Leaders

BlackBerry Limited

Alphabet Inc. (Google)

Wind River Systems

Green Hills Software

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hyundai Motor Group confirmed a USD 21 billion United States investment plan for 2025–2028, allocating USD 6 billion to autonomous-driving AI and robotics collaborations with Boston Dynamics and NVIDIA.

- April 2025: Huawei started the HarmonyOS NEXT automotive application pioneer program, partnering with iQIYI, Bilibili, and Tencent Music on native in-car apps.

- March 2025: Li Auto open-sourced its Halo OS, inviting external developers to contribute to its zone-controller framework.

- March 2025: BMW China joined forces with Huawei to integrate HarmonyOS ecosystem services, delivering digital key and HiCar functions through the My BMW App.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study, according to Mordor Intelligence, defines the automotive operating systems market as the value generated from software platforms that coordinate and control a vehicle's electronic domains (infotainment, ADAS, power-train, body, connectivity, and cloud gateways) when the stack is supplied as a distinct licensed or open-source package embedded by the original equipment manufacturer.

Only factory-installed stacks for passenger and commercial vehicles are captured; aftermarket smartphone mirroring apps, stand-alone ECU firmware, and non-automotive embedded OSs are outside the scope.

Segmentation Overview

- By Operating System Type

- Real-Time OS (QNX, AUTOSAR Classic, VxWorks, INTEGRITY)

- General-Purpose OS (Android Automotive, AGL Linux, Windows, HarmonyOS)

- Hypervisor-based Mixed-Criticality Stacks

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- By Application

- Infotainment and Digital Cockpit

- ADAS and Autonomous Driving

- Connected Services and Telematics

- Body Control and Comfort

- Powertrain and Battery Management

- By Propulsion Type

- ICE Vehicles

- Hybrid Vehicles

- Battery Electric Vehicles

- Fuel-Cell Electric Vehicles

- By Sales Channel

- OEM-Embedded

- Aftermarket Retro-fit

- By Level of Autonomy

- Level 0-1

- Level 2

- Level 3

- Level 4-5

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Southeast Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We held structured interviews with vehicle software architects at leading OEMs, kernel developers at Tier 1 integrators, Asian cockpit hardware suppliers, and mobility cloud vendors across North America, Europe, China, Japan, and India. These conversations validated attach rates, typical license fees, over-the-air update cadence, and regional regulatory triggers, filling gaps left by secondary data and grounding the final model.

Desk Research

Analysts started with broad production baselines from sources such as OICA vehicle output tables, IEA's Global EV Outlook, UNECE WP.29 approvals, NHTSA recall filings, and MIIT new-energy vehicle bulletins, which frame the size of the rolling fleet and the shift toward software-defined vehicles. Company filings, investor presentations, and trade association white papers on domain controllers provided price points and attach-rate clues, while news archives accessed through Dow Jones Factiva and company financial snippets from D&B Hoovers helped us benchmark revenue splits. Additional insight came from patent trends on Questel that signal OS migration to zonal architectures. The desk sources listed here are illustrative; many other open documents and proprietary notes supported data collection and cross-checks.

Market-Sizing & Forecasting

A top-down build links annual vehicle production by type with OS adoption ratios that vary by propulsion mix, autonomy level, and regional regulations. Selective supplier roll-ups of per-vehicle average selling price validate and fine-tune totals. Key variables include global light-vehicle output, EV share, proportion of Level 2+ vehicles, cockpit domain controller penetration, and prevailing OS royalty ranges. Multivariate regression, informed by primary expert consensus, projects each driver and feeds an ARIMA overlay to capture cyclical production swings. Where supplier data are thin, weighted regional averages bridge gaps before the values undergo final review.

Data Validation & Update Cycle

Mordor analysts run variance checks against fresh registration data, shipment logs, and cloud activation counts, re-contacting sources when anomalies exceed set thresholds. The model is refreshed every twelve months, with interim updates triggered by material events such as platform launches or regulatory shifts, ensuring clients always receive the latest baseline.

Why Mordor's Automotive Operating Systems Baseline Remains the Trusted Yardstick

Published figures often diverge because firms pick different inclusion rules, currencies, and refresh cadences.

Our disciplined scoping, yearly updates, and variable-level stress tests minimize those gaps for decision-makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 23.33 B (2025) | Mordor Intelligence | - |

| USD 19.57 B (2025) | Global Consultancy A | Excludes ADAS and power-train stacks, focuses mainly on infotainment |

| USD 13.44 B (2024) | Global Consultancy B | Uses older base year and bundles only Android, Linux, QNX licenses |

| USD 12.70 B (2022) | Industry Journal C | Estimates built from device shipments without royalty adjustments |

The comparison shows that scope breadth, timely data, and cross-verified price assumptions drive Mordor's higher yet balanced estimate, giving stakeholders a transparent, reproducible baseline they can trust for strategic planning.

Key Questions Answered in the Report

What is the current size of the automotive operating systems market?

The market was valued at USD 25.59 billion in 2026 and is projected to reach USD 40.62 billion by 2031.

Which operating system holds the largest share in vehicles today?

BlackBerry QNX led with 38.20% market share in 2025, mainly because of its ISO 26262 ASIL D certification for safety-critical domains.

Why are automakers shifting toward Android Automotive OS?

Android Automotive is expanding at an 17.47% CAGR through 2031 because OEMs value its consumer-familiar interface and seamless integration with Google’s cloud ecosystem.

How do UNECE WP.29 R155 and R156 regulations affect software demand?

The rules make cybersecurity and over-the-air update capabilities mandatory for all vehicles registered after July 2024, prompting OEMs to adopt pre-certified operating systems.

Which region leads adoption of software-defined vehicles?

Asia-Pacific commanded 44.30% market share in 2025, driven by China’s rapid deployment of HarmonyOS-based platforms and strong government backing for local software stacks.

What growth rate is expected for battery-electric vehicle operating systems?

Operating systems tailored for battery-electric vehicles are forecast to grow at a 13.42% CAGR through 2031 as specialized battery-management and fast-charging features become standard.

Page last updated on: