Acoustic Vehicle Alerting System Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 1.85 Billion |

| Market Size (2031) | USD 3.43 Billion |

| Growth Rate (2026 - 2031) | 13.22% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acoustic Vehicle Alerting System Market Analysis by Mordor Intelligence

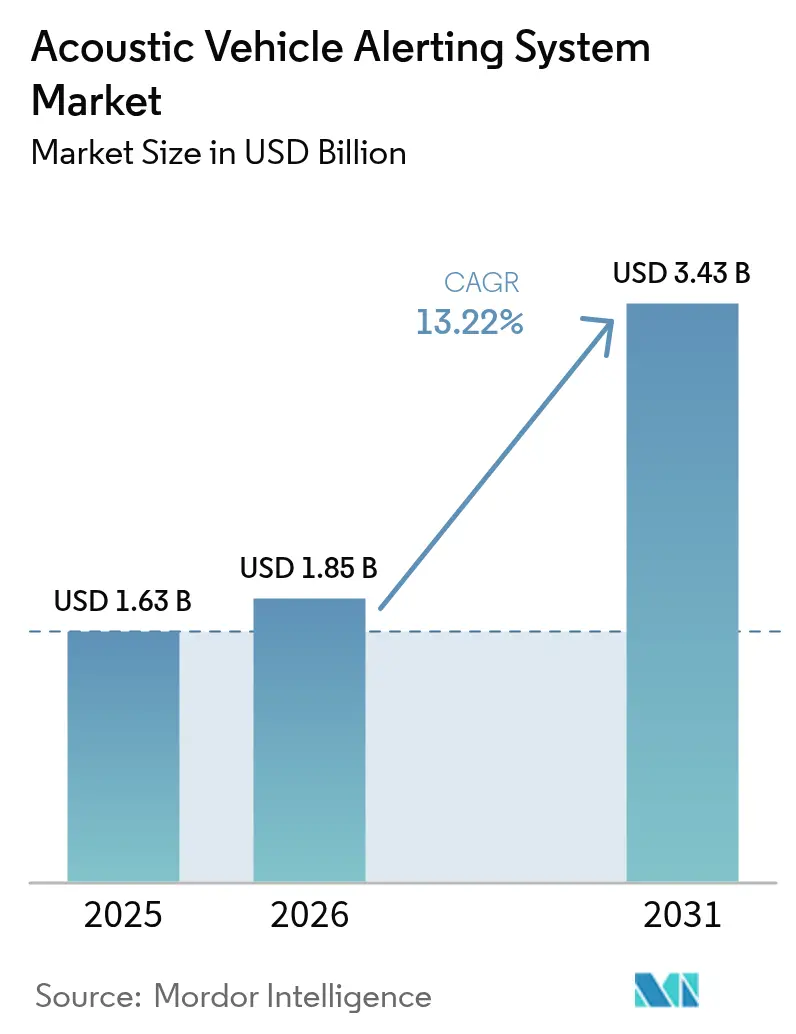

The Acoustic Vehicle Alerting System (AVAS) Market size is expected to grow from USD 1.63 billion in 2025 to USD 1.85 billion in 2026 and is forecast to reach USD 3.43 billion by 2031 at 13.22% CAGR over 2026-2031. Regulatory mandates that require every new electric or hybrid vehicle to emit an artificial sound at low speeds have transformed acoustic alerting from an option into a legal prerequisite, instantly enlarging the addressable Acoustic Vehicle Alerting System Market. Accelerating electric vehicle production, led by China’s 70% share of global output in 2024, gives component suppliers a dependable volume base that supports economies of scale. Asian smart-city pilots are beginning to link Acoustic Vehicle Alerting System Market units with vehicle-to-infrastructure data feeds. This demonstrates a path toward context-aware sound modulation that improves safety while curbing noise pollution. Competitive intensity is rising as traditional Tier-1 suppliers, acoustic specialists, and software players race to optimize cost, transducer efficiency, and branded sound signatures. At the same time, the absence of a globally harmonized acoustic standard adds engineering complexity because every multinational OEM must juggle at least two distinct compliance regimes.

Key Report Takeaways

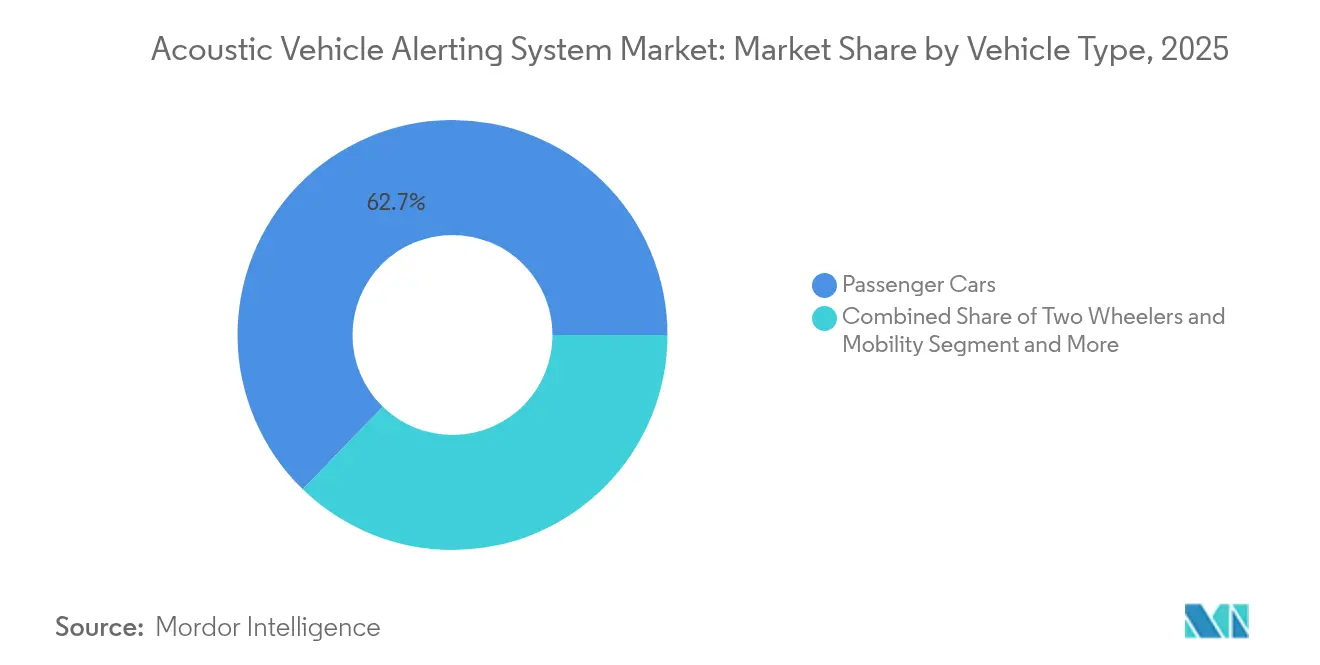

- By vehicle type, passenger cars held 62.74% of the Acoustic Vehicle Alerting System Market share in 2025, while two-wheelers and micromobility vehicles are projected to grow at a 16.94% CAGR by 2031.

- By propulsion, battery electric vehicles accounted for 65.22% of the Acoustic Vehicle Alerting System Market size in 2025 and are expected to post a 14.35% CAGR between 2026 and 2031.

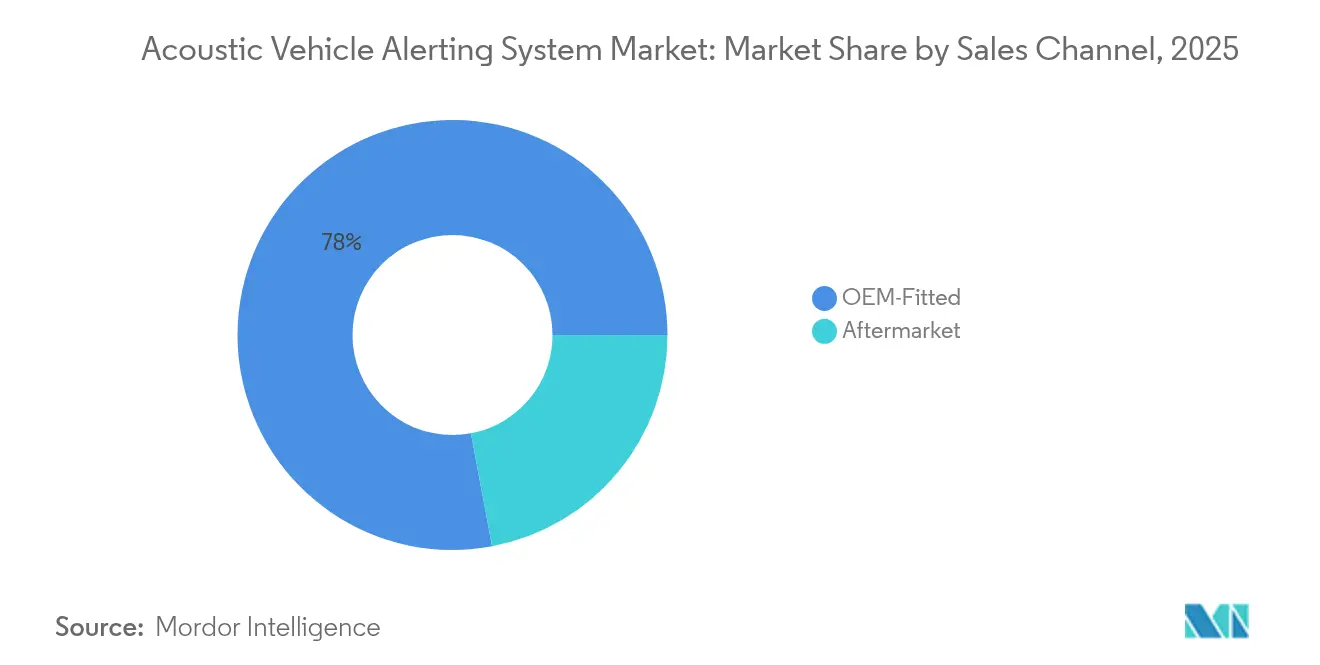

- By sales channel, the OEM-fitted segment captured 77.95% share of the Acoustic Vehicle Alerting System Market size in 2025; the aftermarket segment shows the highest projected CAGR at 16.12% through 2031.

- By system component, speakers led 41.92% in the Acoustic Vehicle Alerting System Market revenue share in 2025, while electronic control units are projected to expand at a 13.55% CAGR through 2031.

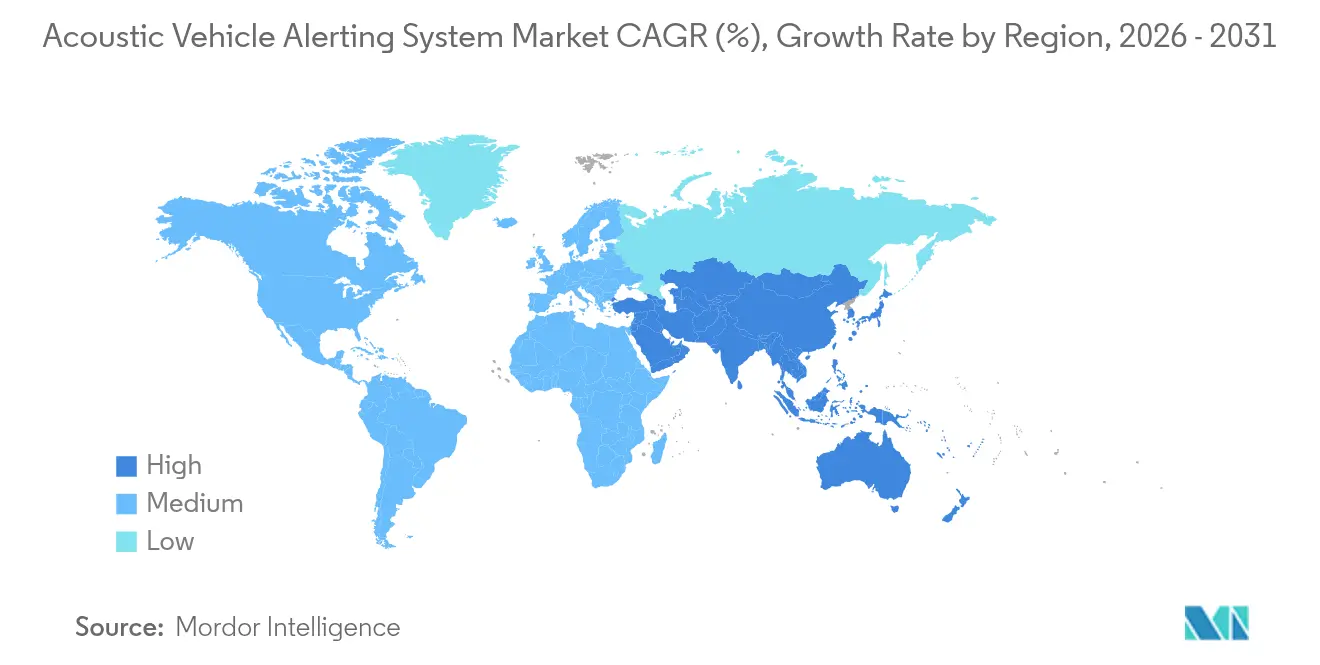

- By region, Asia-Pacific led 43.10% in the Acoustic Vehicle Alerting System Market revenue share in 2025; the same region is on track to expand at a 14.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acoustic Vehicle Alerting System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pedestrian Safety Compliance Mandates | +3.2% | Global, with early adoption in EU, North America, Asia-Pacific | Short term (≤ 2 years) |

| Global EV Production Surge | +2.8% | Global, concentrated in China, EU, North America | Medium term (2-4 years) |

| OEM Focus on Custom Exterior Sound | +1.9% | North America & EU premium segments, expanding to Asia-Pacific | Medium term (2-4 years) |

| AVAS Integration with V2X & Smart Cities | +1.5% | North America, EU, China smart city initiatives | Long term (≥ 4 years) |

| Micromobility EV Category Expansion | +1.1% | EU, North America urban centers, Asia-Pacific emerging | Medium term (2-4 years) |

| Low-Power Transducer Tech Advancements | +0.9% | Global manufacturing hubs, cost-sensitive markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates for Pedestrian-Safety Compliance

Australia will require AVAS on all new electric vehicles starting November 2025, adding to mandates already in force across the EU, Canada, and the United States.[1]“Australia to Mandate EV Alert Sounds from November 2025,”, Royal Automobile Club of Victoria, racv.com.au UNECE Regulation R138 compels vehicles to emit artificial noise at 0–20 km/h, specifying minimum sound levels and gradual frequency shifts correlating with speed unece.org. Canada aligned its CMVSS 141 rule set with these guidelines, synchronising safety expectations throughout North America. Such uniform, non-negotiable rules eliminate demand uncertainty for the AVAS market by making acoustic systems a prerequisite for vehicle registration in regulated zones. With every compliance cycle, OEM purchasing departments lock in higher AVAS volumes, anchoring the forward order books of module suppliers.

Rapid Growth in Global EV Production Volumes

In 2024, global electric car production reached 17.3 million units, up 25% from 2023, with China responsible for more than 70% of the total.[2]“Global EV Outlook 2024,”, International Energy Agency, iea.org Each vehicle built in these plants requires an AVAS module, knitting the fortunes of acoustic suppliers to the robust EV growth curve. Model proliferation is also broadening, with the number of distinct electric car nameplates expected to top 1,000 by 2026, including many large SUVs that generate additional acoustic tuning work. Scaling effects are already driving down transducer and amplifier costs, encouraging faster adoption even in price-sensitive segments. Plug-in hybrids further enlarge the target pool because they must still emit artificial sound whenever the internal-combustion engine is off.

Rising OEM Focus on Brand-Customised Exterior Sound Signatures

General Motors signalled the marketing role of AVAS as early as 2012 when the Chevrolet Volt launched with a unique “Pedestrian Friendly Alert,” setting a precedent for branded exterior sound.[3]“The Evolution of EV Sound Design,”, General Motors Communications, gm.com Honda now plans downloadable “vintage performance” sound packs for its 0 Series EVs, turning AVAS into a software-defined revenue stream. Consumer testing shows that listeners prefer familiar, engine-like timbres to common monotone beeps. As premium brands attach emotional value to sound design, acoustic specialists with psychoacoustic expertise gain a competitive edge. The trend reframes AVAS as a brand-experience enhancer rather than a regulatory expense, boosting willingness to pay in luxury segments.

Integration of AVAS with V2X and Smart-City Infrastructure

The United States has earmarked USD 60 million to seed a national V2X network, enabling vehicles to exchange data with roadside units, traffic lights, and cloud services.[4]“National V2X Deployment Plan,”, U.S. Department of Transportation, transportation.govOnce connected, an AVAS module can calibrate output in real time, raising volume in crowded crosswalks and lowering it in quiet residential zones. Academic trials show that networked AVAS cuts reaction time for pedestrians while reducing ambient noise pollution. Chinese municipalities already test context-aware sound modulation in tier-1 smart-city districts, illustrating future opportunities for public-private platforms that fine-tune acoustic environments. Over the long term, integration with V2X will stretch AVAS functionality well beyond its current standalone status.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Global Sound-Level Standards | -1.80% | Global, particularly affecting multinational OEMs | Short term (≤ 2 years) |

| BOM Cost Pressure for Mass-Market BEVs | -1.40% | Cost-sensitive markets, emerging economies | Medium term (2-4 years) |

| NVH vs. Cabin Quietness Trade-Offs | -0.90% | Premium vehicle segments, North America & EU | Medium term (2-4 years) |

| Low Consumer Awareness in Price-Sensitive Markets | -0.70% | Emerging economies, rural markets globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Globally Harmonised Sound-Level Regulations

UNECE rules serve as a baseline, yet the United States imposes slightly different spectral and decibel targets under FMVSS 141, obliging OEMs to engineer multiple hardware-software variants. That fragmentation raises validation costs and slows simultaneous global launches because each acoustic profile must pass local certification. Working-group negotiations at GlobalAutoRegs continue, but national priorities diverge between pedestrian safety and community noise control, delaying full convergence. The engineering burden lands hardest on mid-tier suppliers that lack the resources to maintain multiple product lines, thereby tempering short-term growth

Incremental BOM Cost Pressure for Mass-Market BEVs

An AVAS kit adds hardware and software expenses when automakers chase price parity with gasoline cars. The pinch is most acute in entry-level models sold in emerging economies where regulatory enforcement can lag. Research into piezoelectric micromachined ultrasonic transducers promises lower-voltage, higher-output solutions that shrink size and cost, but commercial scale is still several years away. Until those gains materialise, budget-constrained consumers may view AVAS as an unwelcome surcharge, restraining uptake in markets where subsidies are fading.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Drive Volume, Two-wheelers and Micromobility Accelerates Growth

In 2025, passenger cars dominated the Acoustic Vehicle Alerting System market, holding a 62.74% share, underscoring the maturity of compliance programs among global OEMs. Suppliers benefit from fleetwide integrations, securing predictable, high-volume contracts that bolster production planning. Two-wheelers and micromobility are witnessing the fastest growth, with a CAGR of 16.94%. This surge is attributed to regulators extending their safety focus to compact urban vehicles. OECD injury statistics highlight a growing number of pedestrian incidents tied to silent two-wheelers, prompting cities to enforce audible warning mandates. Consequently, specialist suppliers catering to these compact form factors are carving out a significant presence in the AVAS market.

Commercial vehicles adopt at a steadier pace, buffered by fleet procurement cycles and the need for ruggedized hardware. Yet the segment’s risk profile in dense delivery corridors still spurs gradual but persistent demand. EU Regulation 168/2013, which sets functional safety rules for L-category vehicles, guarantees that micromobility makers will require acoustics during type approval. The widening scope of regulated vehicle classes cements multi-segment growth for the AVAS market.

By Propulsion Type: BEV Leadership Reinforces Market Foundation

Battery electric vehicles owned 65.22% of the Acoustic Vehicle Alerting System market share in 2025 and carry the highest forecast CAGR at 14.35%, confirming that fully electric drivetrains remain the prime catalyst for acoustic alerting demand. Because BEVs are silent in every low-speed phase, their compliance windows are broader than those of hybrids, making AVAS non-negotiable. Plug-in hybrids contribute incremental volume because their electric-only mode requires artificial sound below 20 km/h.

Design complexity varies by propulsion. BEVs need continuous output management that minimizes battery drain, while PHEVs must toggle the sound on and off when engines start. Hybrid electric vehicles present narrower activation windows yet still create obligatory volume. Each configuration nuance gives control unit suppliers opportunities to differentiate through software efficiency, further deepening the AVAS market.

By Sales Channel: OEM Integration Dominates, Aftermarket Retrofit Accelerates

In 2025, OEM-installed systems represented 77.95% of the Acoustic Vehicle Alerting System market size because most regulations mandate factory compliance certificates at first registration. Direct integration with vehicle control units allows speed-synchronized sound that is impossible with passive add-ons. Unitary demand lets suppliers negotiate long-term agreements that stabilize margins.

As legacy EVs grapple with new regulations, the aftermarket segment is poised for a robust 16.12% CAGR. A mere 20% of registered EVs in Australia are equipped with compliant acoustic kits. This statistic heralds a surge in retrofitting activities, especially with the November 2025 deadline looming. Fleet operators, favoring retrofit kits over complete vehicle replacements, have carved out a lucrative niche for plug-and-play solutions. Consequently, the Acoustic Vehicle Alerting System market has evolved into a dynamic ecosystem, blending high-volume OEM contracts with nimble retrofit specialists, enriching its competitive landscape.

By System Component Type: Speakers Remain Dominant, ECUs Scale Quickly

Speakers captured 41.92% of Acoustic Vehicle Alerting System revenue in 2025, underscoring their role as the primary output element in every acoustic alerting package. OEM programs favor purpose-built automotive loudspeakers because they meet UNECE R138 and FMVSS 141 sound-pressure targets with limited calibration effort. Mature supply chains and standardized form factors let Tier-1 suppliers bundle amplifiers and wiring into cost-efficient modules that streamline assembly lines. Premium brands are upgrading cone materials, voice-coil insulation, and water-resistant housings so exterior mounting points withstand road spray and thermal cycling. This ongoing refinement cements speakers as the volume backbone of the Acoustic Vehicle Alerting System market even as adjacent subsystems evolve.

Electronic control units form the fastest-growing slice, forecast to advance at a 13.55% CAGR from 2026 to 2031 as software-defined architectures become mainstream. Emerging ECUs consolidate signal generation, vehicle-speed sensing, and over-the-air update capability into secure domain controllers that dynamically modulate sound based on V2X inputs. Because these intelligent controllers also host other safety or infotainment features, automakers see them as a route to reduce part counts while unlocking subscription revenue from downloadable acoustic libraries. The transition toward centralised computing is therefore expected to narrow the cost gap between basic and premium Acoustic Vehicle Alerting System offerings, fuelling sustained growth for ECU suppliers through the decade.

Geography Analysis

Asia-Pacific dominates the Acoustic Vehicle Alerting System market with a 43.10% revenue share in 2025 and a leading 14.98% CAGR outlook. China’s GB/T 37153-2018 standard obliges every low-speed BEV, HEV, and FCEV to emit a calibrated sound signature, providing a uniform regulatory bedrock. Coupled with China’s 70% share of global EV manufacturing, this rule guarantees a large local consumption base. Hong Kong’s blanket requirement for AVAS on all electrified vehicles adds another layer of demand, while Japan and India review similar measures that could unlock further volume. Infrastructure pilots in Shanghai and Shenzhen already feed V2X data into Acoustic Vehicle Alerting System controllers, signaling future integration pathways.

North America ranks second in the Acoustic Vehicle Alerting System market, propelled by FMVSS 141 in the United States and Canada's harmonized CMVSS 141 regulation. Federal investment in V2X corridors enhances the technology roadmap and positions the region to pioneer connected acoustic services. Luxury brands headquartered in the United States increasingly monetize customizable sound portfolios, reinforcing high-margin growth within the regional Acoustic Vehicle Alerting System market.

Europe benefits from its early July 2021 mandate that covers every new electric or hybrid vehicle. Regulation 2019/2144 obliges advanced safety systems that protect vulnerable road users, including acoustic alerting devices. European OEMs leverage long-standing acoustics research to overlay musical principles onto compliant noise, creating signature tones that elevate brand perceptions. Additionally, the European Green Deal’s urban noise objectives encourage adaptive Acoustic Vehicle Alerting System outputs that curtail excessive sound in quiet zones, stimulating research into context-aware signal processing

Competitive Landscape

The Acoustic Vehicle Alerting System market is moderately fragmented, with legacy Tier-1 suppliers, niche acoustic innovators, and software-defined vehicle entrants vying for share. Traditional component makers exploit scale, purchasing power, and embedded OEM ties to retain core contracts. They integrate speakers, amplifiers, and control units into a single module, thus reducing assembly steps and cost.

Specialist firms carve out space through psychoacoustics expertise. Their advantage lies in crafting emotive soundscapes that resonate with brand DNA. Patent filings in potassium sodium niobate-based piezoelectric transducers illustrate a shift toward low-voltage, high-density emitters that slash current draw while raising decibel output. Collaborations between Tier-1s and audio studios, alongside white-label software deals, typify today’s partnership matrix.

A third cohort comprises software players focused on over-the-air sound updates, subscription libraries, and data-driven acoustic personalization. HARMAN’s Eclipse-based open platform illustrates how cloud connectivity can streamline AVAS tuning while providing continuous feature monetisation. As vehicles migrate to centralised compute, embedded AVAS functions may become another containerised service, tilting influence toward code rather than hardware and intensifying competition on intellectual property.

Acoustic Vehicle Alerting System Industry Leaders

Harman International

Continental Engineering Services

Kendrion N.V.

Brigade Electronics

HELLA GmbH & Co. KGaA (FORVIA Hella)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: HARMAN launched an open-source connected services platform through the Eclipse Foundation to accelerate software-defined vehicle functions, including cloud-managed AVAS updates.

- April 2024: Australia confirmed mandatory AVAS installation for all new electric vehicles sold after November 2025, creating a sizeable retrofit backlog.

- February 2024: Bosch and Microsoft announced a generative-AI partnership to refine automated driving perception, paving the way for adaptive AVAS controls.

Global Acoustic Vehicle Alerting System Market Report Scope

The acoustic Vehicle Alerting System is designed to generate vehicle warning sounds and alert pedestrians to the presence of electric drive vehicles. The system is installed in vehicles including hybrid vehicles, plug-in hybrid electric vehicles, and battery electric vehicles that are traveling at low speed (20-30 Kmph), beyond which the noise generated by rolling tires can be easily heard.

The acoustic vehicle alert system market is segmented into vehicle type, propulsion, sales channel, and geography. Based on the vehicle type, the market is segmented into passenger cars, two-wheelers, and commercial vehicles. Based on the propulsion, the market is segmented into battery electric vehicles, plug-in hybrid electric vehicles, and hybrid electric vehicles. Based on the sales channel, the market is segmented into OEM and Aftermarket. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the world. For each segmentation, the market sizing and forecast have been done on the basis of value (USD Million).

| Passenger Cars |

| Two-Wheelers and Micromobility |

| Commercial Vehicles |

| Battery Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) |

| Hybrid Electric Vehicles (HEV) |

| OEM-fitted |

| Aftermarket |

| Speakers (External Sound Emitters) |

| Electronic Control Units |

| Software / DSP Algorithms |

| Wiring and Harness |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Two-Wheelers and Micromobility | ||

| Commercial Vehicles | ||

| By Propulsion Type | Battery Electric Vehicles (BEV) | |

| Plug-in Hybrid Electric Vehicles (PHEV) | ||

| Hybrid Electric Vehicles (HEV) | ||

| By Sales Channel | OEM-fitted | |

| Aftermarket | ||

| By System Component | Speakers (External Sound Emitters) | |

| Electronic Control Units | ||

| Software / DSP Algorithms | ||

| Wiring and Harness | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of AVAS market in 2026?

The Acoustic Vehicle Alerting System (AVAS) Market size reached USD 1.85 billion in 2026 and is forecast to reach USD 3.43 billion by 2031.

Which region leads the AVAS market today?

China's dominant EV manufacturing base, coupled with its GB/T 37153-2018 acoustic standard, propels the Asia-Pacific region to command 43.10% of global revenue.

Why are battery electric vehicles so important to AVAS suppliers?

As BEVs operate quietly at low speeds, the implementation of AVAS becomes essential. In 2025, they account for 65.22% of the demand and are projected to expand at a robust CAGR of 14.35%.

How big is the retrofit opportunity?

As new mandates, including Australia's 2025 rule, come into play, the aftermarket segment is witnessing a robust expansion at a 16.12% CAGR, especially since many EVs produced before 2021 were not equipped with factory-installed AVAS.

What future technology trends could reshape AVAS?

V2X networks and cloud platforms will facilitate context-aware sound modulation, and software-defined vehicles will permit over-the-air acoustic updates.

Page last updated on: