Advanced Gear Shifter System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 16.49 Billion |

| Market Size (2030) | USD 24.47 Billion |

| Growth Rate (2025 - 2030) | 8.21% CAGR |

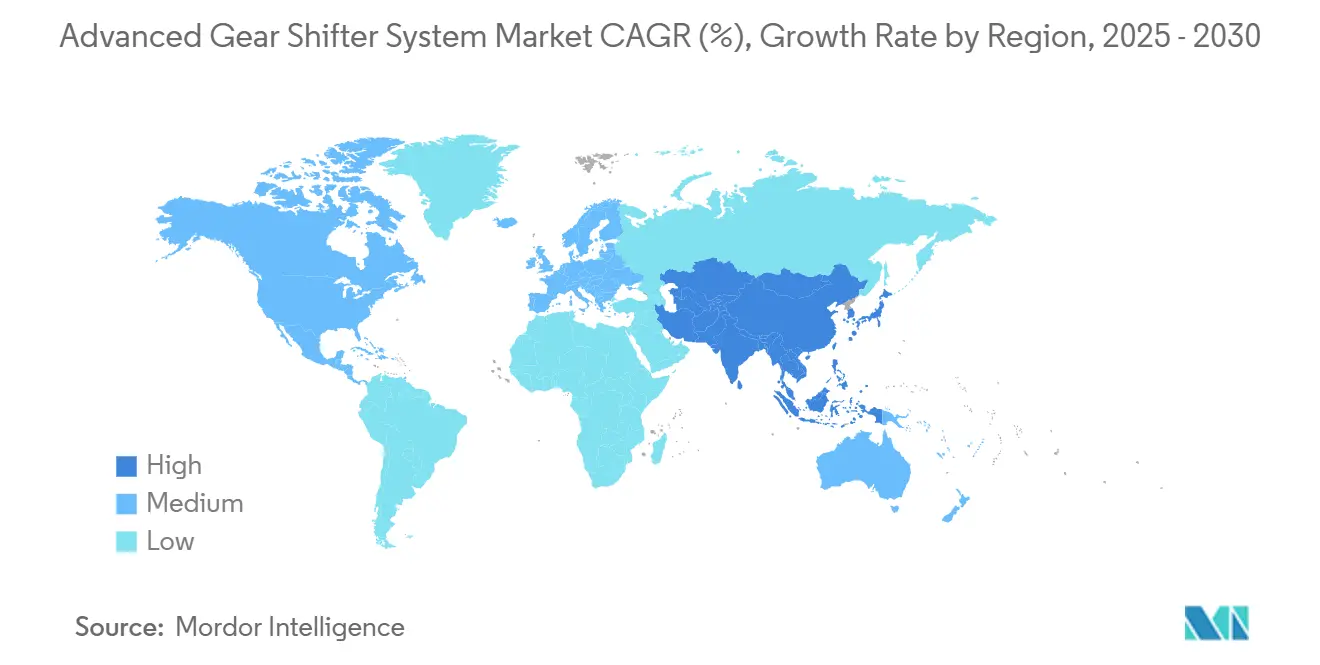

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Gear Shifter System Market Analysis by Mordor Intelligence

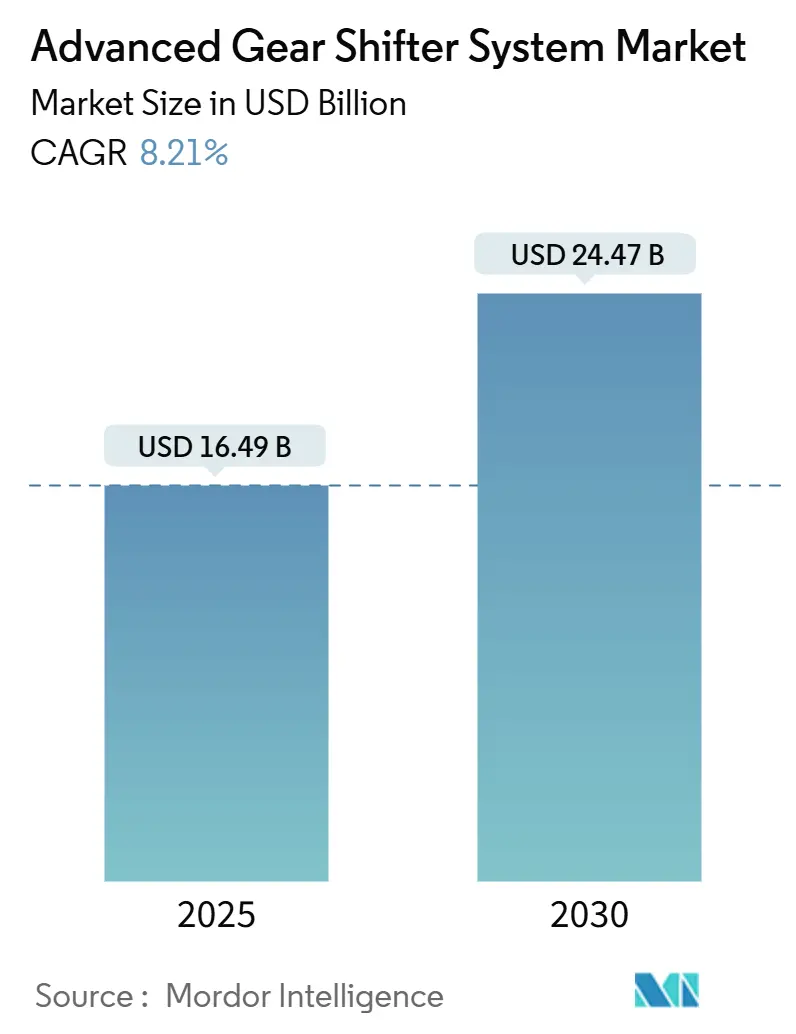

The advanced gear shifter system market size stood at USD 16.49 billion in 2025 and is forecast to post USD 24.47 billion by 2030, advancing at an 8.21% CAGR over the period. This expansion reflects automakers’ accelerated transition from purely mechanical linkages to electronic shift-by-wire architectures, rising electrification, and growing consumer preference for seamless driving convenience. Electronic control units (ECUs), solenoid actuators, and dedicated software are becoming core to transmission design as manufacturers pursue weight reduction, packaging flexibility, and driver-centric user interfaces. Passenger cars remain the volume anchor, yet commercial vehicles show the sharpest uptake of automated manual transmissions as fleets target productivity gains and fuel savings. Competitive dynamics favor Tier-1 suppliers that combine mechanical, electronic, and cybersecurity capabilities into integrated offerings, even as newer software specialists enter via partnerships.

Key Report Takeaways

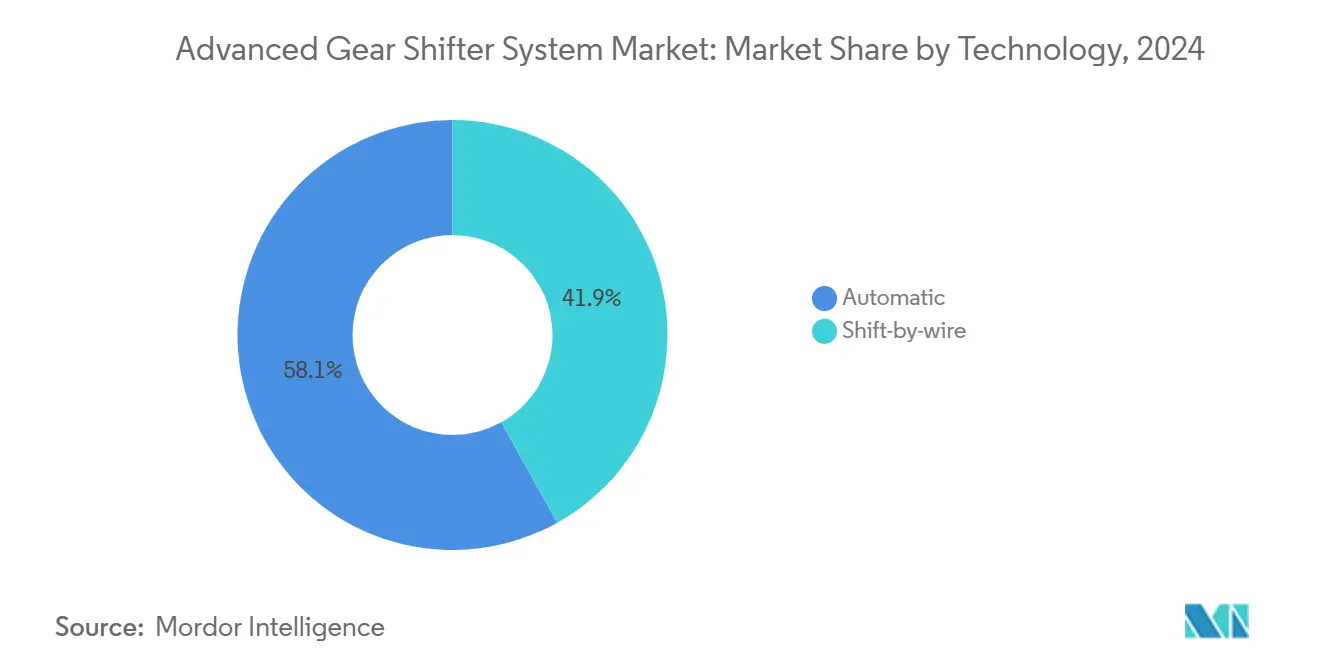

- By technology, automatic transmission shifters commanded 58.11% of the advanced gear shifter system market share in 2024, while shift-by-wire is forecast to grow at a 9.87% CAGR to 2030.

- By vehicle type, passenger cars captured 49.25% of the advanced gear shifter system market share in 2024; medium and heavy commercial vehicles are projected to expand at a 10.12% CAGR through 2030.

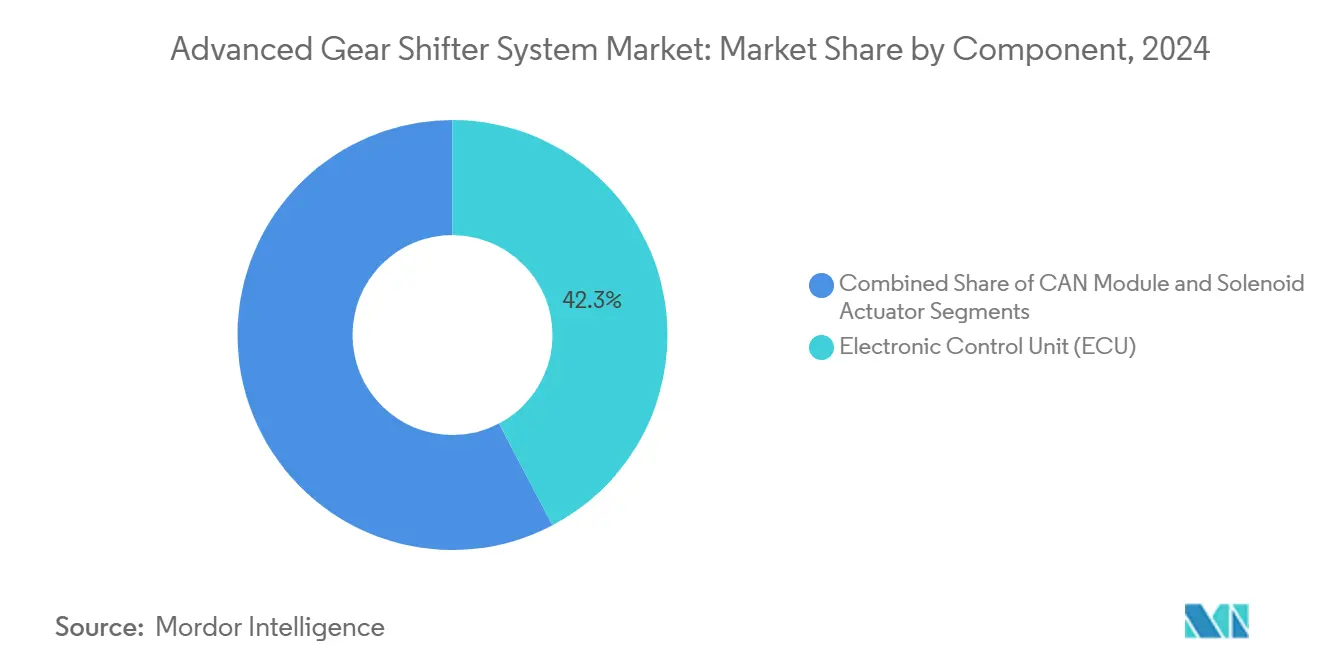

- By component, electronic control units held 42.33% of the advanced gear shifter system market share in 2024; solenoid actuators are advancing at a 9.44% CAGR through 2030.

- By sales channel, OEM installations represented a 73.46% of the advanced gear shifter system market share in 2024 with a 9.06% CAGR outlook to 2030.

- By geography, Asia-Pacific accounted for a 39.14% of the advanced gear shifter system market share in 2024 and is progressing at an 8.74% CAGR to 2030.

Global Advanced Gear Shifter System Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In EV and Hybrid Sales | +2.1% | Global; led by China, EU, North America | Short term (≤ 2 years) |

| Rising Demand for Automatic Transmissions | +1.8% | Global; strongest in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Stricter Fuel-Efficiency Standards | +1.5% | North America and EU; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Premium Vehicles in Emerging Markets | +1.2% | Asia-Pacific core; spill-over to MEA and South America | Medium term (2-4 years) |

| Haptic-Feedback Shifter Integration | +0.9% | North America and EU premium segments | Long term (≥ 4 years) |

| Disability-Friendly Control Regulations | +0.6% | North America and EU; gradual Asia-Pacific adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in EV and Hybrid Vehicle Sales

Battery-electric cars simplify physical gearing but introduce fresh interface opportunities. Hyundai’s Ioniq 5 N uses N e-Shift software to mimic an 8-speed gearbox, marrying driver engagement with single-speed hardware [1]“Ioniq 5 N Technical Highlights,” Hyundai Motor Company, hyundai.com. Ford lodged a patent for haptic EV shifters that recreate clutch resistance digitally. Tesla removed the stalk altogether on Model 3, relying on camera input and steering-wheel buttons. Multi-speed boxes remain viable for heavy-duty EVs where efficiency across gradients justifies complexity, sustaining demand for robust electronic actuation.

Rising Demand for Automatic Transmissions

Automatic transmissions represented a notable share of all gear-changing mechanisms in 2024, reflecting consumers’ growing preference for convenience and efficiency. Uptake accelerates in India, Thailand, and Brazil, where rising incomes make automatic variants affordable. Fleets adopt automated manuals to cut driver fatigue, prompting Eaton’s Endurant platform to secure large North American truck contracts [2]“Endurant Automated Manual Transmissions,” Eaton Corporation, eaton.com. Construction-equipment OEMs mirror the trend by integrating joystick-based shifters that boost operator productivity. Strong regulatory pressure to hit fleetwide CO₂ limits reinforces the move to electronically controlled multi-speed boxes that maintain engines in optimal operating bands.

Stricter Fuel-Efficiency Standards Favoring Shift-by-Wire

EU targets of 37.5% CO₂ reduction by 2030 compared to 2021 levels and the United States CAFE roadmap intensify interest in shift-by-wire, which saves 2-4 kg versus cable systems and permits energy-saving predictive algorithms. Software can pre-select gears using navigation data, traffic feeds, and learned driving patterns. Compliance with ISO 26262 functional-safety and ISO/SAE 21434 cybersecurity frameworks raises engineering complexity yet guarantees reliability, pushing OEM–supplier collaborations deeper.

Growth in Premium Vehicle Penetration in Emerging Markets

China’s luxury deliveries rose sharply in 2024, and discerning buyers increasingly request rotary selectors, paddle shifts, and illuminated console units as both status markers and usability enhancements [3]“Integrated Gear Bearing Technology,” JTEKT Corporation, jtekt.co.jp. Localized production brings costs down, enabling sophisticated systems in upper-mid trims. Southeast Asian and Middle Eastern importers broaden premium specifications for vans and buses, spurring suppliers with in-region R&D hubs to tailor designs that respect local ergonomics and climate requirements.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost, Complex Shift-By-Wire | −1.4% | Global; cost-sensitive segments most affected | Medium term (2-4 years) |

| Semiconductor Shortages for ECUs | −1.2% | Global; acute in Asian manufacturing hubs | Short term (≤ 2 years) |

| Reliability and Redundant Safety Hurdles | −0.8% | Global; stricter in EU and North America | Long term (≥ 4 years) |

| Cybersecurity Certification Delays | −0.7% | North America and EU; spreading worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost and Complexity of Shift-by-Wire

Redundant ECUs, dual-power rails, and rigorous validation add a significant amount to the bill of materials, challenging mid-range vehicles in cost-driven markets. Suppliers must run functional-safety analysis, hardware-software integration, and penetration tests, lengthening development calendars 12-18 months. Smaller firms struggle to fund these processes, slowing overall penetration outside premium tiers.

Semiconductor Shortages for ECUs

Lead times for automotive-grade microcontrollers peaked in 2024 as fabrication capacity lagged demand, forcing redesigns or production halts. Because each shift-by-wire stack may house three microcontrollers for sensing, actuation, and gateway tasks, shortages ripple disproportionately through this category. Chip vendors add 300 mm automotive lines, yet electrification multiplies silicon content faster than capacity ramps, keeping supply fragile.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Shift-by-Wire Drives Innovation Despite Automatic Dominance

Automatic transmission shifters held 58.11% of the advanced gear shifter system market in 2024 on sheer production volumes. Nevertheless, shift-by-wire’s 9.87% CAGR highlights its strategic importance. Luxury SUVs from Mercedes-Benz and Cadillac showcase column-mounted electronic stalks that liberate console real estate while integrating with drive-mode selectors. Weight savings reach 4 kg, assisting OEM carbon targets. Suppliers embed machine-learning firmware that trims energy use by predicting driver intent from throttle cadence.

Adoption accelerates in battery-electric nameplates where legacy mechanical cables offer no benefit. The architecture supports over-the-air recalibration, letting brands roll out new driving modes without physical redesigns. Emerging-market premium compacts import these interfaces, demonstrating the technology’s trickle-down path.

By Vehicle Type: Commercial Vehicles Accelerate Automation Adoption

Passenger cars accounted for 49.25% of the advanced gear shifter system market share in 2024. Yet medium and heavy commercial vehicles are projected to clock the highest 10.12% CAGR as fleets adopt automated manuals pairing gear-geometry efficiency with user simplicity. Eaton’s Endurant HD couples electronic selectors with predictive cruise, enabling 6% fuel savings on long-haul routes. Urban delivery vans adopt push-button modules that occupy less dash space, reducing driver distraction.

Buses and vocational rigs gain from joystick-style controls integrated with telematics. Fleet owners see maintenance cost drops thanks to software-enabled diagnostics pinpointing actuator wear before failure. Regulations mandating accessible cabs further favor low-effort e-shifters.

By Component: Solenoid Actuators Enable Precise Control

ECUs represented 42.33% of the advanced gear shifter system market share in 2024, underscoring their central orchestration role. However, solenoid actuators will outpace at 9.44% CAGR through 2030. Advanced linear-drive solenoids integrate hall-effect sensors that relay position within 0.1 mm, ensuring fault-tolerant engagement. CAN-FD gateways handle higher data throughput to synchronize with ADAS. Suppliers such as JTEKT bundle gear-detent modules with embedded diagnostics, cutting assembly steps, and warranty claims.

Component consolidation is evident as firms merge shifter electronics with transmission mechatronics, reducing harness weight and simplifying OEM logistics. Semiconductor content per actuator climbs as cybersecurity encryption moves to the edge.

By Sales Channel: OEM Integration Dominates Market

OEM installations commanded 73.46% of the advanced gear shifter system market share in 2024 on the back of co-development cycles that marry shifter electronics with drivetrain calibrations. The segment is also set to witness the fastest growth of 9.06% CAGR through 2030. Automakers lock in styling and HMI differentiation—Tesla’s button-based selection and Porsche’s compact toggle exemplify proprietary UX. Aftermarket retrofits remain niche, limited to enthusiast short-throw kits for legacy sports cars. Nonetheless, programmable controller kits appear for classic-car EV conversions, signaling a budding specialty channel.

Regulatory cybersecurity checks increasingly require OEM-backed keys and certificates, making certified dealer upgrades the only compliant path for many jurisdictions and constraining independent workshops.

Geography Analysis

Asia-Pacific generated 39.14% of the advanced gear shifter system market share in 2024 and leads with an 8.74% CAGR to 2030. China’s new-energy vehicle boom stimulates demand for minimalist rotary selectors inside BYD’s and NIO’s latest sedans, while domestic suppliers gain scale through provincial government procurement programs. Japan leverages Kei-car innovation, Suzuki embeds compact electronic levers that free cabin space. South Korean exporters bundle shift-by-wire across premium trims to maintain global competitiveness, aided by national R&D tax credits.

North America remains a pivotal market where a significant share of new light vehicles already ship with automatics. Ford prototypes haptic EV shifters at its Michigan plant, underscoring domestic innovation. The region’s Class 8 truck fleets accelerate the adoption of automated manuals to offset driver shortages. EPA greenhouse-gas Phase 3 regulations further direct OEMs to electronic shift strategies that harmonize with engine downsizing.

Europe champions shift-by-wire in response to 2030 fleet CO₂ caps. German Tier-1s ZF and Continental bundle cybersecurity gateways and CAN-over-Ethernet to secure E/E architectures. The Schaeffler-Vitesco merger creates a vertically integrated player spanning gear actuators to inverter software, reshaping supplier hierarchies. GDPR obligations influence data handling in personalized shifter profiles, requiring on-device processing to minimize cloud exposure. South America and the Middle East & Africa register smaller bases yet display strong premium import growth. Luxury SUV buyers in the Gulf Cooperation Council increasingly expect illuminated crystal rotary dials popularized by European marques, spurring regional showroom adoption.

Competitive Landscape

The advanced gear shifter system market exhibits moderate fragmentation. ZF, BorgWarner, Continental, and JTEKT headline share tables, leveraging long-standing OEM relationships and vertically integrated mechatronics. Continental's spun off Aumovio announcement to focus on software-defined vehicle functions, including cloud-updatable shifter firmware. ZF’s Smart Shift-by-Wire earns production slots on multiple EV skateboards after independent safety-case validation. BorgWarner integrates its eGearDriver module with motor inverters, touting part count savings.

Patent filings for haptic feedback surged year-on-year as suppliers seek defensible differentiation. Partnerships bloom between electronics firms and interface designers—Bosch teams with German haptics specialist Feelbelt to embed vibrotactile cues into compact selectors. Semiconductor giants NXP and Renesas bundle secure bootloaders tailored for shifter ECUs, courting Tier-1s under multi-year supply frameworks that mitigate chip-shortage risk.

Start-ups exploit software gaps: Israeli firm Irridon offers AI-based driver-intent prediction licensed per vehicle, compatible with CAN gateways, while United States newcomer ShiftLogic markets over-the-air calibration tools enabling OEMs to refine gear-change feel post-sale. Defensive acquisitions signal consolidation momentum—Schaeffler’s takeover of Vitesco Systems folds cybersecurity specialists into its drivetrain portfolio.

Advanced Gear Shifter System Industry Leaders

ZF Friedrichshafen AG

BorgWarner Inc.

JTEKT Corporation

Continental AG

Marelli Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: PT Hyundai Motors Indonesia premiered STARGAZER Cartenz and Cartenz X featuring standard shift-by-wire and built-in navigation at Gaikindo Indonesia International Auto Show (GIIAS) 2025.

- April 2023: BYD unveiled the Seal sports sedan equipped with a KOSTAL China gear selector integrating extra comfort-function buttons and a shift-by-wire module already slated for broader premium models.

Global Advanced Gear Shifter System Market Report Scope

| Automatic |

| Shift-by-wire |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Buses and Coaches |

| CAN Module |

| Electronic Control Unit (ECU) |

| Solenoid Actuator |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology | Automatic | |

| Shift-by-wire | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Component | CAN Module | |

| Electronic Control Unit (ECU) | ||

| Solenoid Actuator | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the advanced gear shifter system market in 2025?

The advanced gear shifter system market size is USD 16.49 billion in 2025.

What is the forecast CAGR for advanced gear shifter systems to 2030?

The market is projected to expand at an 8.21% CAGR between 2025 and 2030.

Which region accounts for the biggest demand for advanced gear shifters?

Asia-Pacific leads with a 39.14% revenue share in 2024 and the fastest 8.74% CAGR.

Which vehicle segment is the fastest‐growing adopter of electronic shifters?

Medium and heavy commercial vehicles post the highest 10.12% CAGR as fleets prioritize automated manuals for efficiency and driver comfort.

Page last updated on: