Automotive Gearbox Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

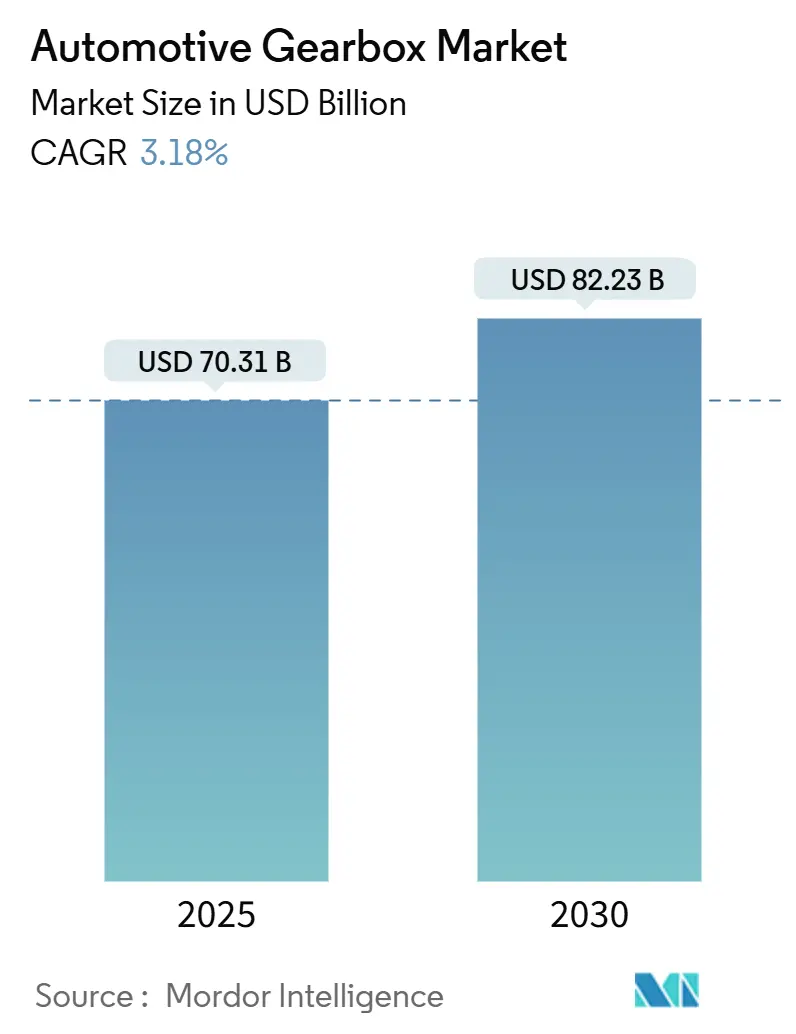

| Market Size (2025) | USD 70.31 Billion |

| Market Size (2030) | USD 82.23 Billion |

| Growth Rate (2025 - 2030) | 3.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

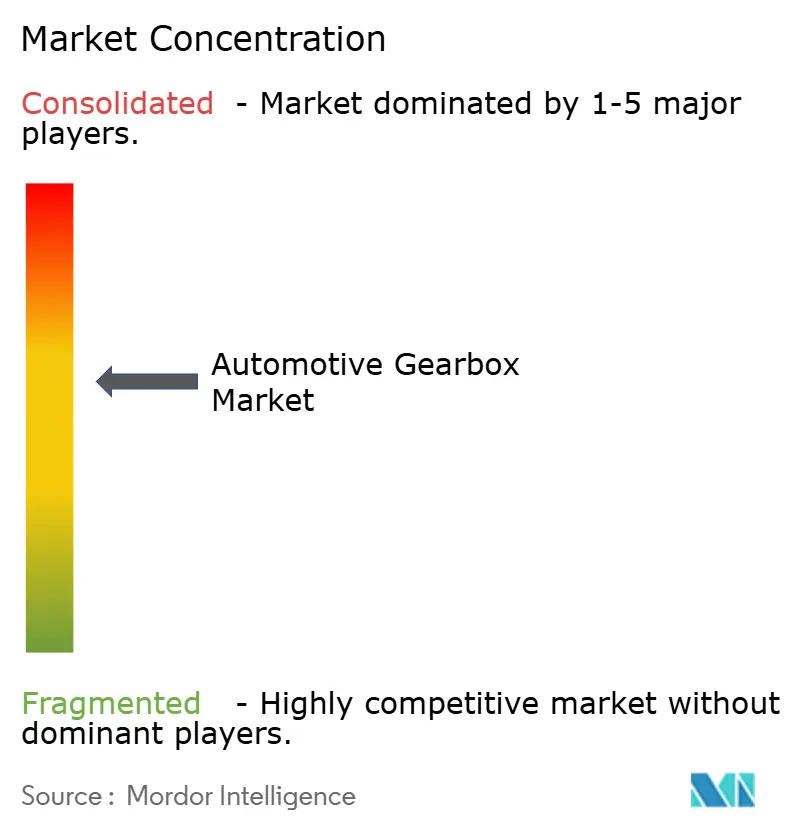

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Gearbox Market Analysis by Mordor Intelligence

The automotive gearbox market stood at USD 70.31 billion in 2025 and is forecast to reach USD 82.23 billion by 2030, reflecting a 3.18% CAGR from 2025 to 2030. Global expansion is steady rather than spectacular because demand splits between resource-intensive, multi-speed solutions for internal-combustion vehicles and the simpler, single-speed layouts preferred in battery electric drivetrains. Volume growth is supported by rising sport-utility and pickup production segments that typically specify 8- to 10-speed boxes for high-torque applications yet tempered by the rapid shift to electrified architectures that avoid traditional gear sets. Competitive positioning revolves around hybrid-capable designs, software-defined control logic, and capital-intensive precision-forging capacity. At the same time, regulatory pressure from Corporate Average Fuel Economy and European CO₂ targets raises near-term demand for high-efficiency multi-speed designs. Over the outlook, suppliers able to straddle combustion and electric value pools capture the bulk of incremental growth.

Key Report Takeaways

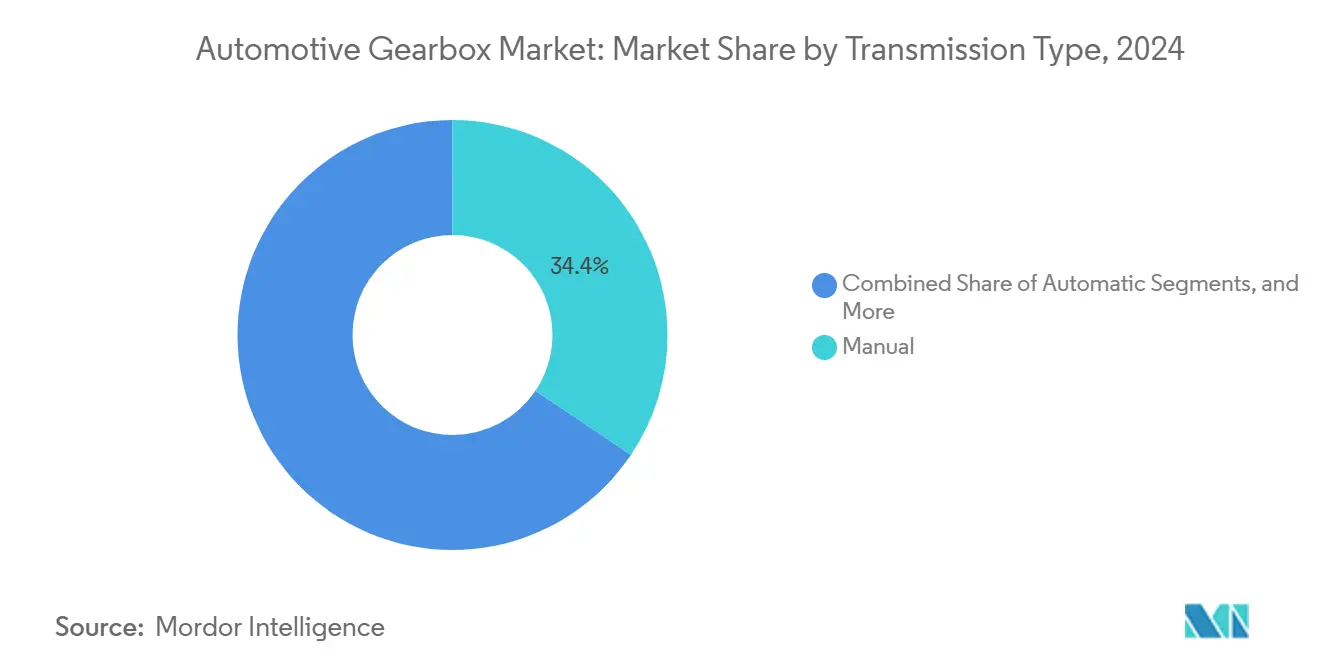

- By transmission type, manual units led 34.42% of the automotive gearbox market share in 2024, whereas dual-clutch technology is advancing at a 6.41% CAGR through 2030.

- By propulsion, internal-combustion engines accounted for 75.26% of the automotive gearbox market share in 2024, while battery electric vehicle demand is expanding at an 8.52% CAGR to 2030.

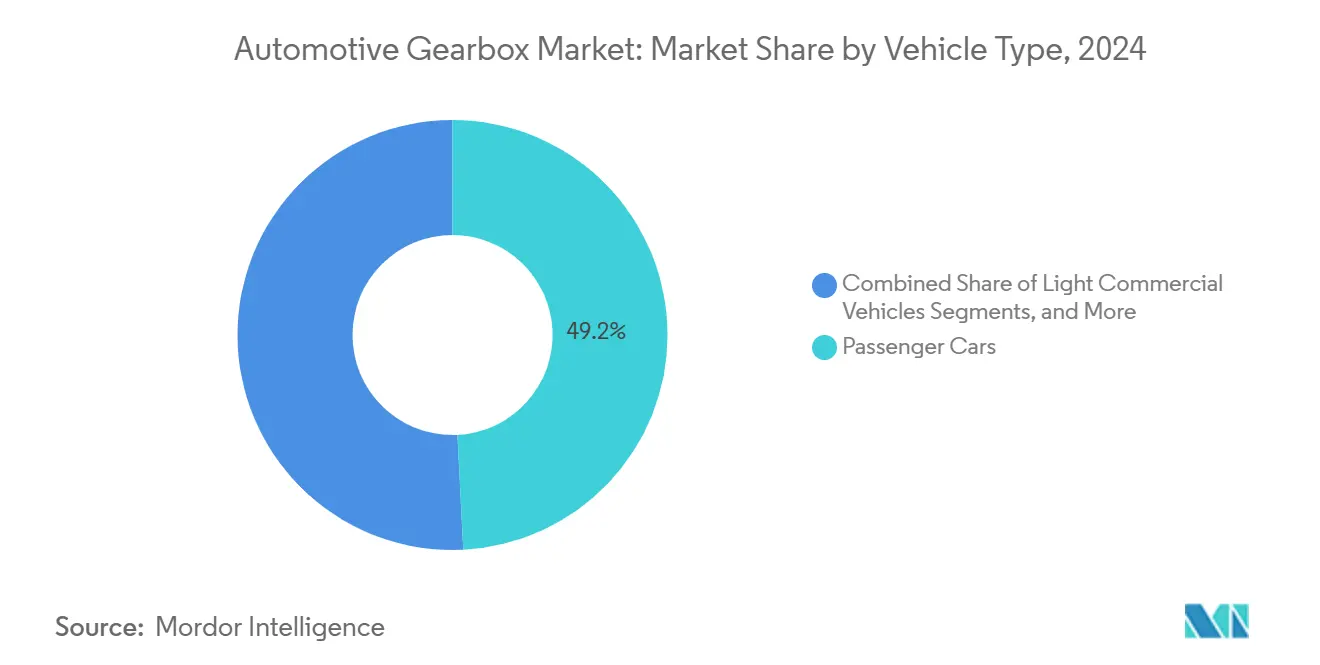

- By vehicle category, passenger cars generated 49.21% of the automotive gearbox market share in 2024, and are progressing at a 7.21% CAGR through 2030.

- By sales channel, OEM deliveries dominated the automotive gearbox market, with 83.38% of the share in 2024, as aftermarket volumes trailed. However, the OEM segment is still forecast to post a 7.23% CAGR to 2030.

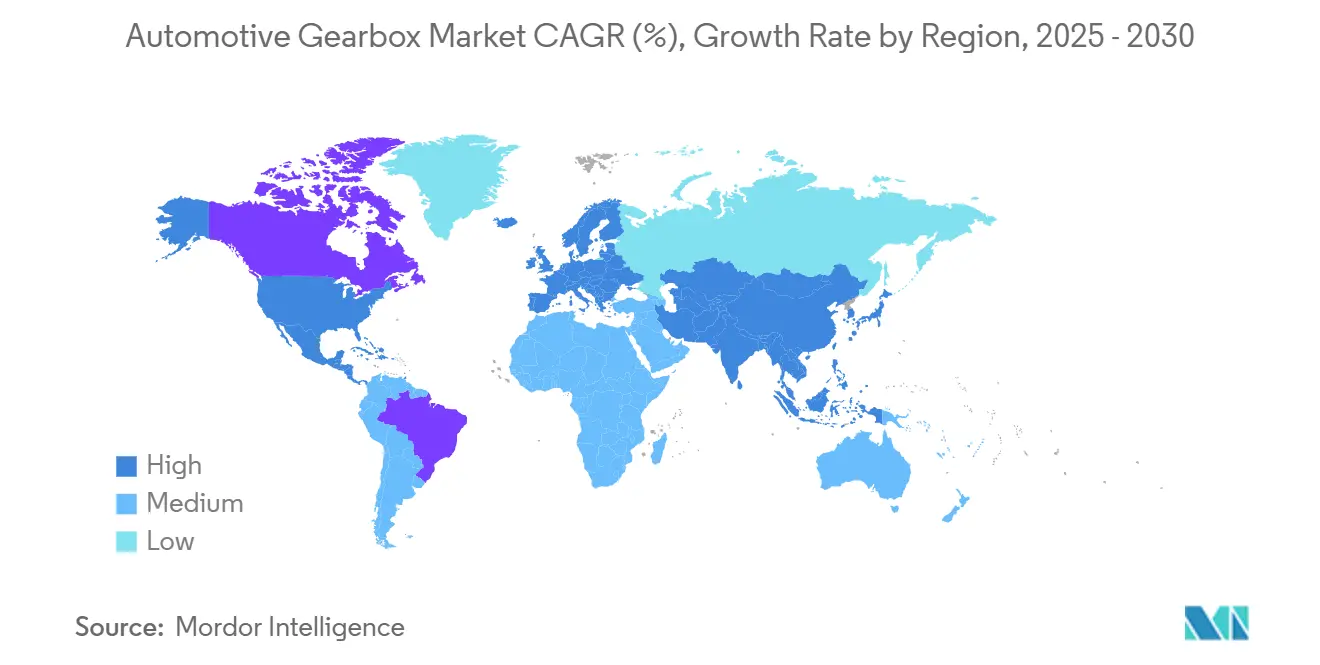

- By geography, Asia-Pacific commanded 43.82% of the automotive gearbox market share in 2024; the region is also the fastest growing, with an 8.72% CAGR through 2030.

Global Automotive Gearbox Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Global SUV and Pickup Output | +1.2% | North America, Asia-Pacific | Medium term (2-4 years) |

| Stricter CO₂ / CAFÉ Mandates | +0.8% | North America, European Union | Long term (≥ 4 years) |

| Rapid Preference for Automatics in China/India | +0.6% | Asia-Pacific (China, India) | Short term (≤ 2 years) |

| OEM Push for Hybrid-Ready Gearboxes | +0.4% | Global, early EU and Japan | Medium term (2-4 years) |

| OTA-Enabled Shift-Logic Upgrades | +0.3% | North America, European Union | Long term (≥ 4 years) |

| Embedded 48-V E-Drive Modules | +0.2% | European Union expanding worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Global Vehicle Production, Especially SUVs and Pickup Trucks

The global shift toward heavier SUVs and pickups is structurally boosting demand for advanced multi-speed automatic gearboxes. Automakers increasingly specify 8–10-speed units to meet drivability and emissions standards, raising per-vehicle gearbox content and supplier margins. As emerging markets adopt larger body styles and premium models pair with dual-clutch systems, the addressable value for gearbox manufacturers expands, reinforcing long-term growth and profitability in the Automotive Gearbox Market.

OEM Preference for Integrated Hybrid-Ready Transmissions

Gearbox manufacturers are increasingly adopting designs that accommodate electric motor inserts, allowing them to cater to internal combustion, hybrid, and plug-in variants without a complete redesign. ZF's 8HP platform exemplifies this modular strategy, enabling OEMs to remain emissions-compliant while postponing expensive platform revamps[1]ZF, “Fourth-Generation 8HP Launch,” ZF Friedrichshafen, zf.com. Suppliers adept at seamless integration, while maintaining the traditional driving experience, are winning long-term contracts, as automakers emphasize flexibility and readiness for regulations in the Automotive Gearbox Market.

Software-Defined Gear-Shifting Logic Enabled by OTA Updates

Transmission control units have become updatable over the air, letting automakers tune shift maps, torque management, and energy-recuperation logic after vehicles leave the factory. Continuous software optimization can deliver real-world fuel-economy gains and tailor drivability to regional preferences, all without physical service visits [2]Continental AG, “Smart Transmission Control Units,” Continental AG, continental.com. The digital layer opens a subscription revenue stream for premium performance modes, while predictive diagnostics lower warranty exposure by flagging gearset wear before failure in the Automotive Gearbox Market.

48-V E-Drive Modules Embedded in Gearboxes Creating New Revenue Pools

Vitesco's 48V, 30 kW e-machines introduce mild-hybrid features such as torque fill, regenerative braking, and stop-start without necessitating a complete overhaul of the powertrain. When integ rated into established gearbox positions (P2/P2.5/P3), these systems achieve up to 15% of fuel savings during urban driving, all while maintaining the vehicle's original structure and ease of service[3]Vitesco, “48-Volt Electric Drive Systems,” Vitesco Technologies, vitisco.com. For traditional suppliers, these embedded e-drives serve as a bridge, capitalizing on the shift towards electrification even as internal combustion engines continue to dominate, thus ensuring their relevance in the changing landscape of drivetrain designs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BEV Proliferation Removing Gear Sets | –0.9% | European Union, China, Global roll-out | Short term (≤ 2 years) |

| Rising R&D and Validation Outlays | –0.7% | Worldwide, hardest on small suppliers | Medium term (2-4 years) |

| Precision-Forging Capacity Constraints | –0.5% | Germany, Japan production hubs | Short term (≤ 2 years) |

| E-Axle Suppliers Cannibalizing Standalone GB | –0.4% | Europe, North America, moving to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

BEV Proliferation Eliminating Conventional Gear Sets

Battery electric vehicles typically use a single reduction gear integrated with the drive motor, eliminating most mechanical components in traditional multi-speed transmissions. As incentives in Europe and China accelerate BEV adoption, demand for standalone gearboxes is declining. This shift pushes traditional transmission suppliers toward integrated e-axles, software-based control systems, and adjacent driveline modules to sustain relevance and revenue in an increasingly electrified market.

Escalating R&D and Validation Costs for Next-Gen AT/DCT

Engineering hybrid-ready automatics now demands advanced cybersecurity, thermal management, and durability under variable load conditions, significantly extending development timelines and increasing validation costs. Larger players like Allison Transmission are absorbing rising R&D outlays, while mid-tier manufacturers face margin pressure without diversified scale. This dynamic is expected to drive supply-side consolidation and licensing activity, as smaller firms struggle to recover capital investments in the Automotive Gearbox Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transmission Type: Manual Dominance Faces Automated Disruption

Manual units retained 34.42% of the automotive gearbox market share in 2024, due to low entry cost and broad acceptance in commercial fleets. Yet dual-clutch systems exhibit the category’s fastest CAGR at 6.41% through 2030, propelled by premium-brand launches requiring both rapid shift times and efficiency gains. The automotive gearbox market size derived from dual-clutch installations is projected to expand consistently as higher-output four-cylinder engines replace six-cylinder layouts.

Growth momentum also favors sophisticated automatics with eight or more ratios that optimize combustion engines for stricter CAFÉ targets. In contrast, basic six-speed automatics become a cost-down option for emerging-market models. Continuously variable transmissions prosper in hybrid small cars, though consumer perception of “rubber-band” throttle response restrains uptake in performance segments. Across segments, hybrid-ready layouts converge on integrated electric-motor cavities, blurring the once-clear lines between classical categories.

By Propulsion Type: ICE Leadership Amid Electric Acceleration

Internal combustion-engine vehicles holda 75.26% share of the automotive gearbox market in 2024, sustaining the largest block of addressable volume even as electric momentum builds. Therefore, the automotive gearbox market size linked to internal combustion platforms still eclipses its electric equivalent, though the gap closes as BEVs race forward at an 8.52% CAGR through 2030.

Hybrid programs generate intricate requirements for torque-split devices, disconnect clutches, and charge-efficient gearmaps, creating a lucrative mid-term sweet spot. In BEVs, the architecture shift toward single-speed reductions compresses unit revenue. Still, it opens pathways for integrated e-axles, planetary reduction hubs, and software-heavy torque-vectoring modules that transmission incumbents are now entering.

By Vehicle Type: Passenger Car Focus Drives Innovation

Passenger cars hold a 49.21% share of the automotive gearbox market in 2024, and are set to grow at a 7.21% CAGR as buyers gravitate to automated drivability and semi-autonomous features that pair naturally with electronically controlled gearboxes. Asia’s compact-SUV boom further enlarges the passenger-car slice, reinforcing scale for multi-ratio, mechatronic boxes.

Light commercial vehicles offer a steady backlog, amplified by e-commerce logistics, but prioritize durability and total cost of ownership. Medium and heavy trucks require torque-converter automatics or manuals rated above 2,000 Nm, keeping specialized OEM-supplier relationships intact. Off-highway niches agriculture and mining seek rugged planetary units, cushioning cyclical exposure to passenger-car swings.

By Sales Channel: OEM Integration Dominates Strategy

OEM pathways hold 83.38% share of the automotive gearbox market in 2024 and will outpace aftermarket additions with a 7.23% CAGR as automakers sign long-term design-in contracts early in platform lifecycles. In many regions, standard warranties stretch to 8-10 years, suppressing immediate replacement activity and further skewing share toward factory-fit volumes.

The aftermarket retains relevance in commercial vehicle re-gear, performance tuning, and off-lease refurbishment, yet shrinking failure rates and longer drain intervals constrict unit turnover. Software-defined upgrades available only via OEM-authenticated channels also tether revenue pools closer to the assembly line.

Geography Analysis

Asia-Pacific secured 43.82% of the automotive gearbox market share in 2024 and is tracking the fastest 8.72% CAGR through 2030, powered by China’s high new-energy-vehicle tally and India’s rapid pivot to automatic transmissions. Domestic suppliers in Japan and South Korea anchor high-precision forging and mechatronics capability, while Thailand and Indonesia scale cost-advantaged assembly for global platforms.

North America maintains its influence thanks to outsized SUV and pickup preferences, segments that demand complex multi-speed units. CAFÉ tightening to 50.4 mpg by 2031 raises immediate gearbox content per vehicle even as Detroit accelerates BEV roadmaps. Canada mirrors these specifications but overlays cold-soak durability protocols that stretch validation cycles.

Europe combines stringent 95 g/km fleet limits with swift electrification targets, a duality that intensifies short-term gearbox upgrades and questions long-term capital allocation for mechanical architectures. Germany’s technical leadership and Eastern Europe’s cost-efficient manufacturing generate an intra-regional balance, though Brexit-related border checks add logistical friction for the United Kingdom inbound components.

Competitive Landscape

ZF Friedrichshafen, Aisin, and BorgWarner spearhead a moderately consolidated field, each leveraging global footprint, in-house electronics, and hybrid-ready blueprints. Collective scale grants bargaining power over steel, aluminum, and semiconductor suppliers, permitting disciplined pricing despite raw-material spikes. Therefore, the automotive gearbox market exhibits moderate rivalry intensity, centered on time-to-market for hybrid-integrated platforms rather than pure mechanical differentiation.

BorgWarner offloaded combustion-centric components to sharpen focus on electric propulsion, while Aisin reshaped ownership structures to unlock independent funding lines for electrification research.

New entrants emphasize software and inverter-gearbox integration, often providing turnkey e-axles that bypass standalone transmissions. Incumbents respond by offering mechatronic assemblies featuring embedded motors and OTA-upgrade-ready controllers, a value proposition rooted in 100-year gear design experience yet dependent on rapid digital upskilling.

Automotive Gearbox Industry Leaders

Aisin Corporation

ZF Friedrichshafen AG

JATCO Ltd.

BorgWarner Inc.

Magna International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: ZF unveiled its '8HP evo' automatic transmission at IAA 2025. This advanced transmission is designed to cater to the increasing demand for hybrid vehicles, offering improved efficiency and performance. By introducing the '8HP evo,' ZF aims to strengthen its position in the evolving automotive market and address the growing need for sustainable mobility solutions.

- September 2025: Dacia introduced the hybrid-G 150 4x4 powertrain for the Duster and Bigster models, combining hybrid tech, LPG bi-fuel, and all-wheel drive. It features a 1.2-litre 48V mild-hybrid engine (140 hp) on the front axle and a 31 hp electric motor on the rear, delivering 154 hp and torque of 230 Nm (gasoline) and 87 Nm (electric).

Global Automotive Gearbox Market Report Scope

| Manual |

| Automatic |

| Automated Manual Transmission (AMT) |

| Dual-Clutch Transmission (DCT) |

| Continuously Variable Transmission (CVT) |

| Internal Combustion Engine (ICE) |

| Hybrid Vehicle |

| Battery Electric Vehicles |

| Plug-in Hybrid Electric Vehicles |

| Fuel Cell Electric Vehicles |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

| Buses & Coaches |

| Off-Highway Vehicles |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East & Africa |

| By Transmission Type | Manual | |

| Automatic | ||

| Automated Manual Transmission (AMT) | ||

| Dual-Clutch Transmission (DCT) | ||

| Continuously Variable Transmission (CVT) | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Hybrid Vehicle | ||

| Battery Electric Vehicles | ||

| Plug-in Hybrid Electric Vehicles | ||

| Fuel Cell Electric Vehicles | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (MHCVs) | ||

| Buses & Coaches | ||

| Off-Highway Vehicles | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

How large is the automotive gearbox market in 2025?

The automotive gearbox market size reached USD 70.31 billion in 2025.

What is the projected automotive gearbox market size by 2030?

The value is forecast to hit USD 82.23 billion by 2030, reflecting a 3.18% CAGR.

Which region holds the largest share of global demand?

Asia-Pacific led with 43.82% automotive gearbox market share in 2024.

Which transmission technology is growing the fastest?

Dual-clutch systems are expanding at an 6.41% CAGR through 2030.

How does electrification affect gearbox suppliers?

BEVs reduce mechanical content, pushing suppliers toward integrated e-axles and hybrid-ready designs.

Page last updated on: