Automotive Perimeter Lighting Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 38.48 Billion |

| Market Size (2031) | USD 55.01 Billion |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

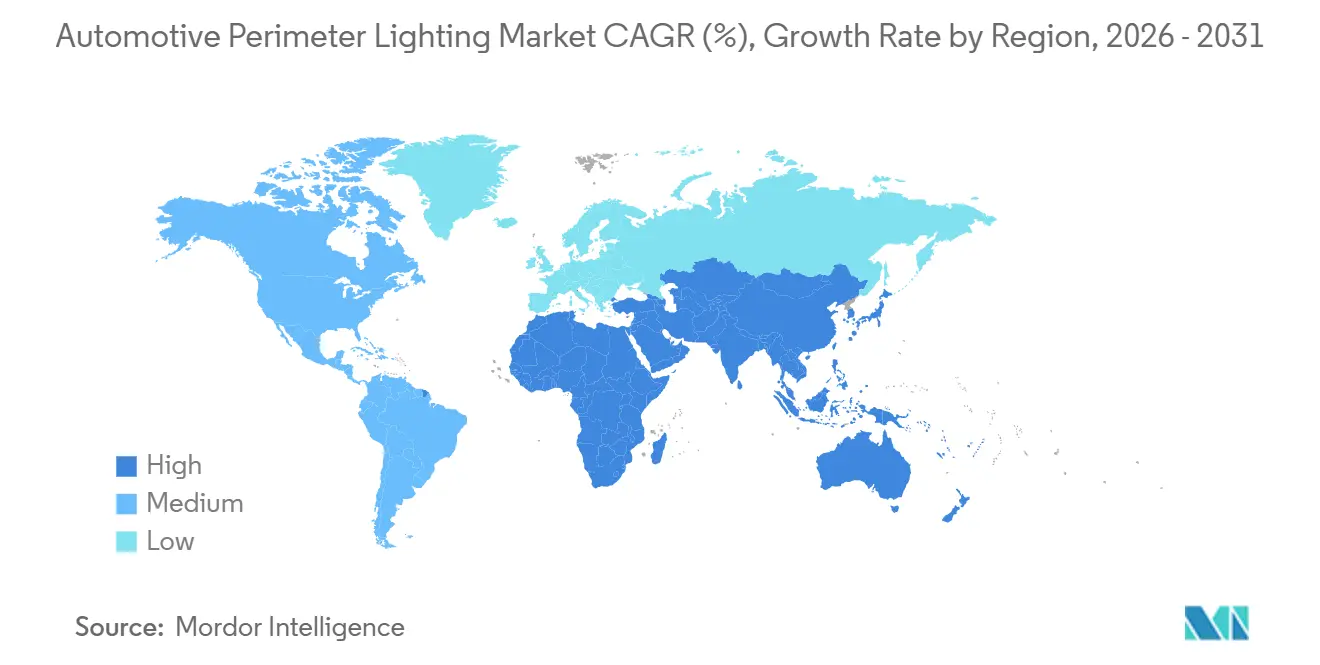

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

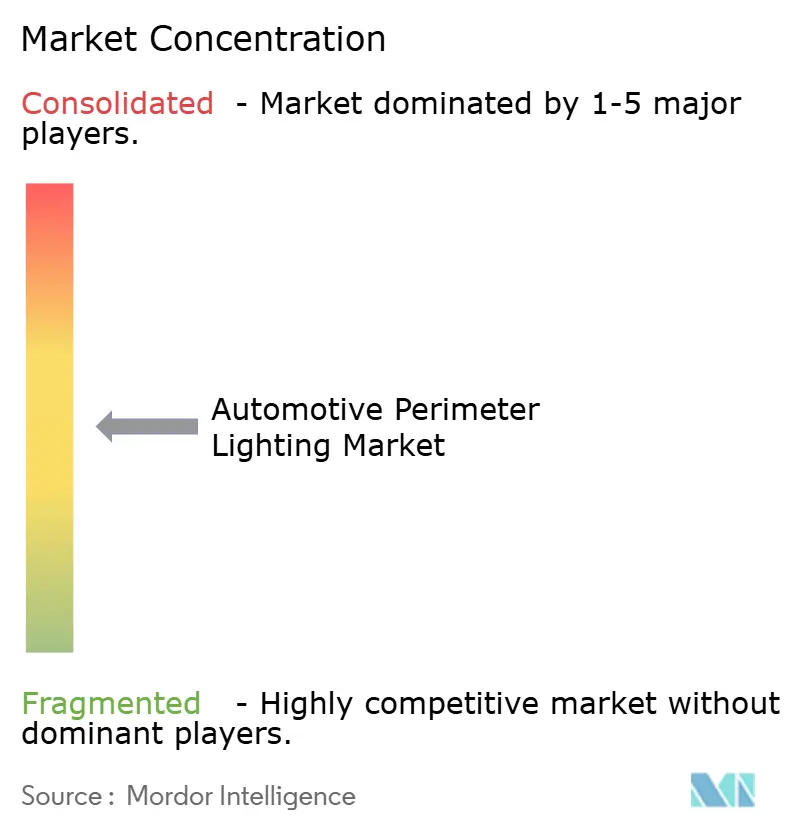

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Perimeter Lighting Market Analysis by Mordor Intelligence

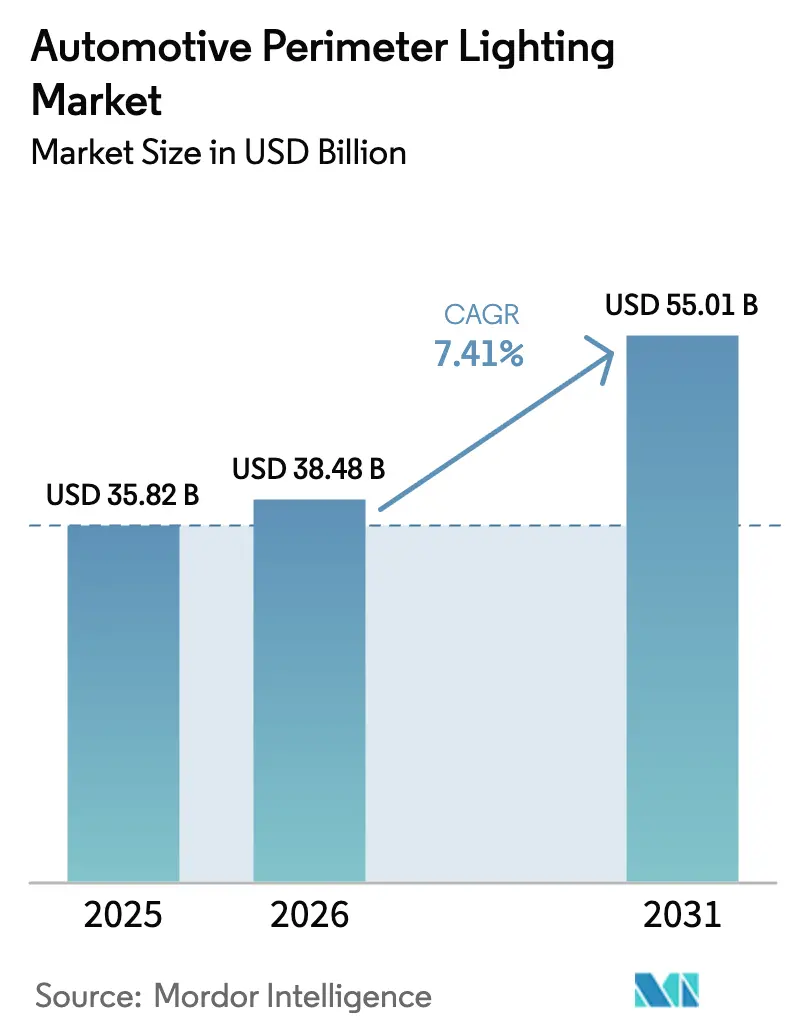

The automotive perimeter lighting market size was valued at USD 35.82 billion in 2025 and is estimated to grow from USD 38.48 billion in 2026 to reach USD 55.01 billion by 2031, at a CAGR of 7.41% during the forecast period (2026-2031). As electrification advances and global lighting regulations tighten, lighting is evolving from a mere safety feature into a dynamic communication tool. Tier 1 suppliers are enhancing headlamps with adaptive matrix LED arrays that possess optical communication capabilities. These advancements allow headlamps to project warning symbols onto the road and sync with advanced driver-assistance systems. Meanwhile, as battery-electric platforms enforce stringent power limits, there's a surging demand for low-power solutions like OLEDs, fiber optics, and micro-LEDs. In recent years, the Asia-Pacific region has maintained a dominant position in global revenue generation. However, looking ahead, the Middle East and Africa are poised to emerge as the fastest-growing regions, driven by the Gulf Cooperation Council's integration of V2X lighting into their new smart transport corridors.

Key Report Takeaways

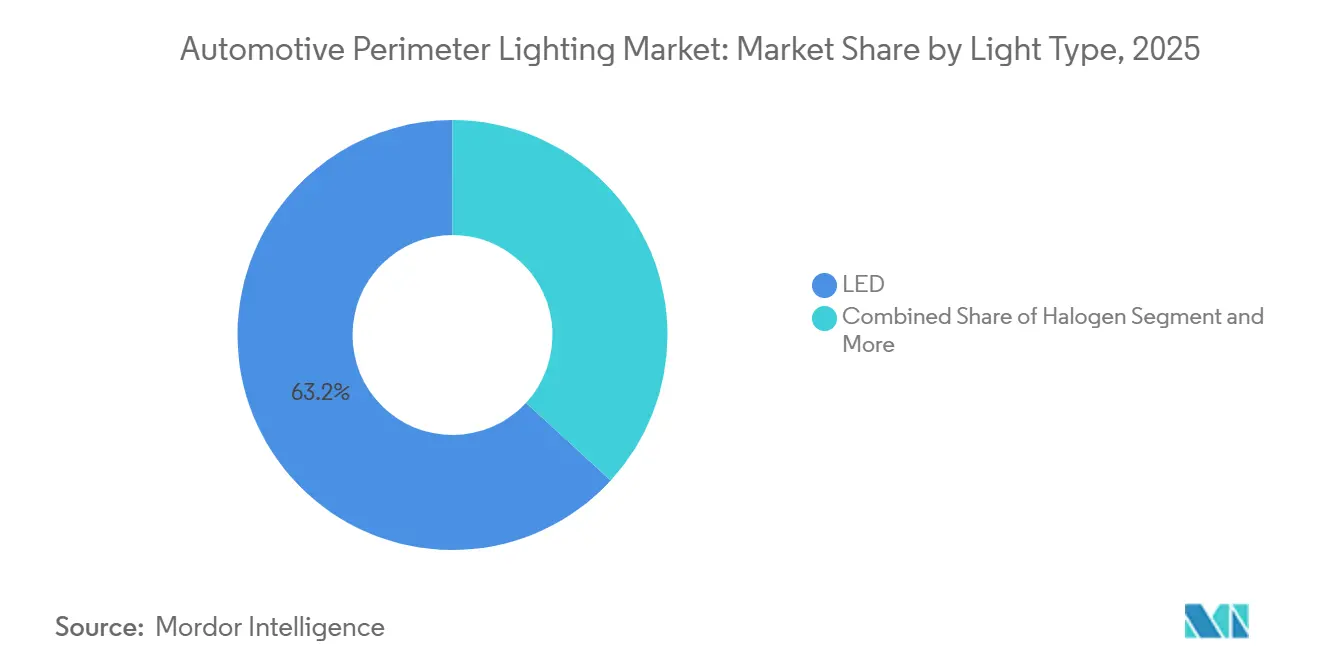

- By light type, LED accounted for 63.17% of the automotive perimeter lighting market share in 2025 and is projected to expand at a 7.43% CAGR through 2031.

- By material, plastics accounted for 57.71% of the automotive perimeter lighting market share in 2025, but fiber and composite substrates are advancing at a 7.51% CAGR through 2031.

- By application, exterior perimeter lighting held 73.37% of the automotive perimeter lighting market share in 2025, whereas interior perimeter lighting is growing the fastest at a 7.55% CAGR through 2031.

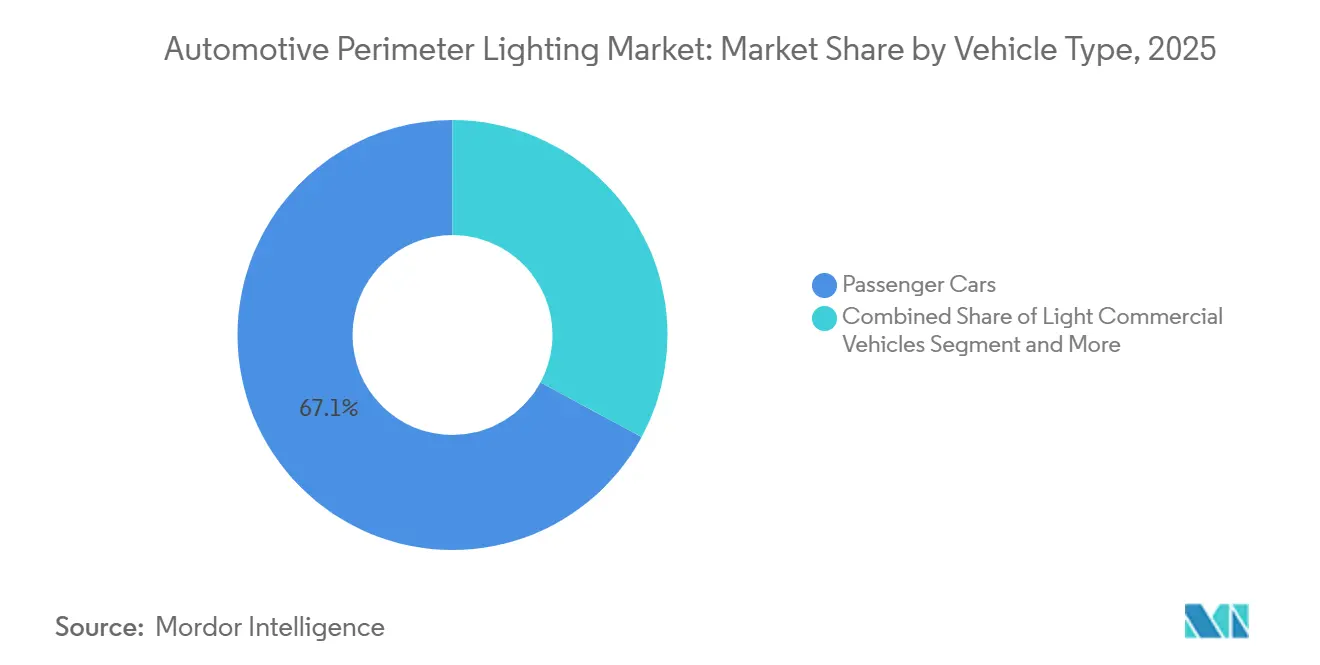

- By vehicle type, passenger cars delivered 67.14% of the automotive perimeter lighting market share in 2025, and light commercial vehicles are forecast to register a 7.44% CAGR through 2031.

- By sales channel, OEM programs represented 77.81% of the automotive perimeter lighting market share in 2025, yet aftermarket upgrades are rising at a 7.48% CAGR through 2031.

- By geography, Asia-Pacific led with a 43.26% share of the automotive perimeter lighting market in 2025, although the Middle East and Africa posted the highest regional CAGR of 7.47% over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Perimeter Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid LED Penetration for Energy-Efficient Illumination | +1.5% | Global, led by Asia Pacific manufacturing scale and North America retrofit demand | Short term (≤ 2 years) |

| Regulatory Mandates for Enhanced Road-Safety Lighting | +1.3% | Global, with early enforcement in EU (UN ECE R48/R149) and China (GB standards) | Medium term (2-4 years) |

| EV Adoption Driving Demand for Low-Power Perimeter Lighting | +1.2% | Asia Pacific core (China, South Korea), spill-over to EU and North America | Medium term (2-4 years) |

| OEM Shift to Modular Front-End Architectures | +1.1% | Global, with platform-sharing strategies in EU and Asia Pacific | Medium term (2-4 years) |

| Software-Defined / V2X Communicative Lighting Platforms | +1.0% | Early adoption in EU and China; regulatory lag in North America | Long term (≥ 4 years) |

| Aftermarket Customization Culture | +0.8% | North America and Europe, niche traction in Middle East luxury segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid LED Penetration for Energy-Efficient Illumination

LED packages, operating at junction temperatures below a certain threshold, achieve an impressive output with high efficiency. This efficiency significantly reduces power consumption compared to halogen lights, freeing up battery capacity for cabin climate controls, as highlighted in Tesla’s recent engineering disclosures [1]“Vehicle Energy Consumption Disclosures 2025,” Tesla Inc., tesla.com . Recently, a significant milestone was reached as Chinese factories lowered LED module prices to a highly competitive level, erasing the economic advantage that had long protected halogen lamps. The European retrofit market gained momentum following regulatory endorsements of street-legal LED replacements, creating substantial opportunities across the region’s extensive vehicle base. Despite these advancements, LED driver chips continued to face prolonged lead times, reflecting ongoing semiconductor supply challenges.

Regulatory Mandates for Enhanced Road-Safety Lighting

United Nations Regulation 48 amendments now oblige new European passenger cars to carry adaptive driving beams from 2025, while China’s GB 25991-2024 adds automatic high-beam control for vehicles over 1,800 kg. Automakers have swapped static halogens for matrix LED arrays that blank out glare zones, and the U.S. National Highway Traffic Safety Administration finally legalized adaptive-beam technology in 2024, unleashing pent-up demand among North American OEMs [2]“FMVSS 108 Final Rule,” National Highway Traffic Safety Administration, nhtsa.gov . Divergent roll-out calendars split global platforms into mandatory-fit regions and option-package regions, raising per-unit costs and fragmenting supply chains. Japan’s new glare-measurement protocol also forced recalibration of beam intensity in 2025, delaying several model releases by one to two quarters.

EV Adoption Driving Demand for Low-Power Lighting

To enhance vehicle range, General Motors' Ultium platform limits exterior-lighting loads to a minimal wattage. This move has led OEMs to adopt OLED tail-lamps and fiber-optic guides, significantly reducing component mass and cutting assembly time per vehicle [3]“Ultium Platform Sustainability Report 2025,” General Motors, gm.com . In early 2026, Hyundai Mobis announced that its third-generation OLED strips achieve high brightness at a very low voltage, allowing seamless integration with standard vehicle electrical systems. LCV fleet operators prefer standardized LED modules for straightforward servicing across diverse brands. Meanwhile, 800-volt propulsion platforms now require additional isolation and EMC shielding, slightly increasing the bill of materials.

Software-Defined / V2X Communicative Lighting Platforms

SAE J3216, published in 2024, defines optical protocols that let headlamps broadcast vehicle intent through modulated light patterns. Koito unveiled a matrix LED headlamp in January 2026, able to project turn-arrow symbols 10 m ahead of the car, and China requires every new passenger vehicle to be V2X-ready from 2026, jump-starting adoption. Hardware integration lifts module cost USD 25-40, while cybersecurity under UN Regulation 155 adds 6-9 months of validation, stretching R&D budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced LED/OLED | -0.9% | Global, with acute pressure in price-sensitive Asia Pacific and South America segments | Short term (≤ 2 years) |

| Semiconductor Supply-Chain Volatility | -0.7% | Global, with bottlenecks in Taiwan and South Korea foundries | Medium term (2-4 years) |

| Cyber-Security & Functional-Safety Certification Hurdles | -0.7% | Global, with stringent enforcement in EU under UN R155/R156 and ISO 26262 | Long term (≥ 4 years) |

| Light-Pollution Compliance Limiting Beam Patterns/Brightness | -0.5% | EU and North America urban zones, emerging in China and Japan municipalities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced LED/OLED & Adaptive Systems

Matrix LED headlamps are significantly more expensive than static units, while OLED tail-lamps also come at a noticeable premium over LED equivalents, restricting their adoption primarily to the premium market segment. In markets like India and Brazil, halogen lights remain the preferred choice for vehicles in the affordable price range. This preference necessitates suppliers to operate dual production lines. In the near future, Valeo is expected to achieve a notable reduction in OLED module costs by increasing production volumes. This development suggests a potential path toward cost parity within a few years, provided there is a substantial increase in orders.

Semiconductor Supply-Chain Volatility for LED Drivers

In early 2025, LED driver ICs, sharing advanced semiconductor lines with consumer electronics, faced significant wait times. This led suppliers to maintain substantial safety stock levels. Complications arose with China-sourced chips due to export controls and tariffs. Additionally, redesigns at larger semiconductor nodes diminished some efficiency gains for LEDs. In late 2025, DENSO and Renesas initiated a dedicated driver-IC line in Japan, targeting a considerable annual output within a few years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Light Type: LED Gains as Automakers Pursue Thin Profiles

LED continued to dominate the automotive perimeter lighting market with a 63.17% share in 2025, and is projected to record a 7.43% CAGR to 2031, outpacing all other sources. Automakers value LED flexibility that removes bulky diffusers, trimming part count almost in half while enabling sculpted 3-D lamp surfaces. Xenon high-intensity discharge and halogen technologies now form a shrinking niche as regulatory deadlines in China and the EU phase them out by 2028. Suppliers are advancing micro-LED arrays, which deliver ten-fold pixel density improvements and pave the way for high-resolution road-surface projections.

The automotive perimeter lighting market size for LED segments is forecast to remain above USD 30 billion throughout the forecast period. Still, LED revenue will triple from a small base as luxury models adopt zone-specific dimming. Micro-LED and laser-phosphor modules, though accounting for under 2% of 2025 volume, absorb a disproportionate share of R&D budget as Koito, Valeo, and HELLA file patents on thermal management and beam-steering optics.

By Material: Fiber and Composites Reduce Front-End Mass

Plastics such as polycarbonate and ABS accounted for 57.71% of the automotive perimeter lighting market share in 2025, driven by well-established molding supply chains. Yet, fiber-reinforced composites are growing at a 7.51% CAGR as OEMs pursue mass savings in battery-electric vehicles. Carbon-fiber-reinforced polycarbonate lenses deliver weight reductions while maintaining impact resistance and optical clarity, attracting premium EV programs. Glass lenses persist on flagship nameplates where long-term scratch resistance is paramount, though shares slip as polycarbonate hard coats replicate glass durability.

The automotive perimeter lighting market share that plastics command is expected to contract marginally as composites gain market share. Suppliers such as Covestro now offer bio-attributed polycarbonate that reduces lifecycle carbon emissions by a minimal amount, aligning with OEM scope-3 emission targets. Fiber-optic light guides further reduce wiring runs and shave 20 seconds off assembly time, though high alignment precision keeps volume restricted to platforms that can justify automated fixtures.

By Application: Interior Lighting Lifts Brand Experience

Exterior perimeter products accounted for 73.37% of the automotive perimeter lighting market share in 2025, as regulations mandate minimum headlamp and DRL content on every vehicle. Interior perimeter lighting, however, is forecast to grow the fastest at a 7.55% CAGR, as premium trims enable customized RGB ambience synchronized with infotainment and driver-wellness applications. Mercedes-Benz already uses interior LEDs to confirm voice commands via color cues, reducing cognitive load.

The automotive perimeter lighting market size tied to exterior fitment will continue to rise in absolute terms. Yet, the revenue mix tilts toward cabins as flexible OLED strips and addressable RGB controllers proliferate. SAE J3216 also influences exterior sub-categories, standardizing communication protocols for pedestrian interaction lights and welcome-logo projections, which open incremental revenue channels for software updates.

By Vehicle Type: LCV Fleets Adopt Unified Modules

Passenger cars supplied 67.14% of the automotive perimeter lighting market share in 2025, reflecting richer content per vehicle, but light commercial vehicles will post a 7.44% CAGR as zero-emission delivery fleets scale up. Amazon’s Rivian-built vans share front-end lighting modules with Ford’s E-Transit, simplifying spare-parts logistics and technician training. Heavy trucks stay price-driven, retaining sealed-beam LEDs that can be swapped roadside in under 10 minutes, though mandates for automatic emergency braking are driving higher-output DRLs.

The automotive perimeter lighting market share for passenger cars may decline as parcel fleets grow. Still, branded pixel signatures on Hyundai and Volkswagen EVs illustrate how automakers make lighting a style cue consumers recognize from 100 m away, nudging voluntary upgrades among LCV operators that want consistent corporate imagery across mixed body styles.

By Sales Channel: Retrofit Rules Spur Aftermarket Upside

OEM programs retained 77.81% of the automotive perimeter lighting market share in 2025, as integrators package lamps with cooling ducts and crash beams into single front-end modules, while aftermarket revenue is rising at a 7.48% CAGR under harmonized retrofit laws. UN Regulation 128 and new NHTSA guidance allow LED drop-in replacements so long as beam patterns stay within tolerance, freeing mainstream retailers to carry compliant kits.

By the end of the forecast period, aftermarket suppliers could see significant growth in the automotive perimeter lighting market. This expansion is fueled by aging fleets in North America and Europe increasingly adopting LED upgrades, which offer substantially longer bulb life compared to traditional options. In response, OEMs are introducing cryptographic authentication to block non-genuine parts, thereby protecting dealer parts revenue. Simultaneously, while enthusiast communities continue to push for RGB under-glow kits, states like California and Arizona are imposing restrictions on brightness levels to address concerns over visual pollution.

Geography Analysis

Asia-Pacific accounted for 43.26% of the automotive perimeter lighting market revenue in 2025, driven by China's strong LED manufacturing capabilities, Japan's advanced OLED research and development, and South Korea's expertise in electronics integration. A regulatory mandate in China requiring adaptive driving beams for heavier vehicles is expected to make matrix LEDs standard equipment across most domestic platforms, ensuring consistent growth in the coming years. Meanwhile, Japan's Koito and Stanley, which hold a significant share of the global OEM headlamp market, are advancing their micro-LED pilot lines. Additionally, Hyundai Mobis has committed substantial investments to expand its OLED production facilities in Cheonan.

The Middle East and Africa will be the fastest-growing region, with a 7.47% CAGR through 2031. Gulf smart-city initiatives, such as Dubai's V2X testbeds, are driving the demand for communicative lighting solutions. Furthermore, Turkey's robust vehicle export activities are prompting local suppliers to enhance their LED module production capacities. In South Africa, the country's role as a right-hand-drive assembly hub for major automakers like BMW and Mercedes-Benz is fostering local lens production to mitigate tariff-related challenges.

Europe and North America remain content-rich markets, albeit with slower growth rates. The EU's General Safety Regulation, which links advanced driver-assistance systems (ADAS) to glare-free lighting, has effectively mandated adaptive matrix LEDs for all new vehicle models. In the United States, regulatory changes now allow adaptive beams and LED retrofit bulbs, creating a significant upgrade market opportunity. In South America, although growth is slower, Brazil's fleet-renewal program is accelerating the transition away from halogen lighting, laying the groundwork for a broader shift to LED technology.

Competitive Landscape

In recent years, major players like Koito, Valeo, HELLA (FORVIA), Magna, and Stanley have dominated the automotive perimeter lighting market, collectively securing a significant share of OEM revenue. Suppliers are courting automaker design studios well in advance of production starts, locking in next-generation EV platforms. They're investing in demo cars that seamlessly integrate V2X beacons, OLED flexibility, and micro-LED resolution. A notable surge in innovation is evident, with an increasing number of auto-lighting patents being filed. This underscores a competitive race, with suppliers increasingly eyeing subscription software revenue streams, particularly as they monetize over-the-air lighting upgrades.

Chinese contenders, Changzhou Xingyu and HASCO Vision, are making significant strides, capitalizing on the domestic EV boom and their inherent cost advantages. In a parallel move, LED chip manufacturers Nichia and Seoul Semiconductor are venturing upstream into module assembly to achieve higher profit margins. Today's competitive edge is not just about technology but also hinges on advanced thermal solutions. Innovations such as vapor-chamber heat spreaders and graphene composites can effectively manage high-power systems without the need for active cooling.

New opportunities are emerging, such as retrofit kits compliant with UN-Reg 128 for older fleets and circadian-algorithm-driven interior wellness lighting. Strategic partnerships are becoming the norm, emphasizing vertical integration. Notable collaborations include DENSO teaming up with Renesas on driver ICs, HELLA joining forces with Plastic Omnium on front-end modules, and Valeo collaborating with Capgemini on advanced lighting software toolchains. Given the trajectory, as software content increasingly overshadows mechanical optics in terms of value, a surge in M&A activity seems imminent.

Automotive Perimeter Lighting Industry Leaders

Samvardha Motherson Group

Gentex Corporation

Koito Manufacturing Co. Ltd

Feniex Industries

HELLA GmbH & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: FORVIA HELLA launched FlatLight daytime-running technology that improves energy efficiency by 40% and weighs 80% less than legacy systems.

- January 2025: Koito presented its High-Definition Adaptive Driving Beam module with pixel-level control for road-surface projections.

Global Automotive Perimeter Lighting Market Report Scope

The scope of the report includes Light Type (LED, Halogen, and More), Material (Plastic, Glass, and More), Application (Interior and Exterior), Vehicle Type (Passenger Cars and More), Sales Channel (OEM and Aftermarket), and Geography.

The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| LED Lights |

| Halogen |

| Xenon |

| Others |

| Plastic |

| Glass |

| Fiber |

| Others |

| Interior Perimeter Lighting |

| Exterior Perimeter Lighting |

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Medium and Heavy Commercial Vehicles (HCV) |

| OEM (Original Equipment Manufacturers) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Light Type | LED Lights | |

| Halogen | ||

| Xenon | ||

| Others | ||

| By Material | Plastic | |

| Glass | ||

| Fiber | ||

| Others | ||

| By Application | Interior Perimeter Lighting | |

| Exterior Perimeter Lighting | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCV) | ||

| Medium and Heavy Commercial Vehicles (HCV) | ||

| By Sales Channel | OEM (Original Equipment Manufacturers) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Automotive Perimeter Lighting market by 2031?

It is forecast to reach USD 55.01 billion by 2031.

Which region is growing the fastest in perimeter lighting demand?

The Middle East and Africa are expected to post the highest CAGR at 7.47% over 2026-2031.

Why are OEMs moving toward OLED in automotive lighting?

OLED supports thin, 3-D lamp surfaces, reduces part count by 30%, and meets strict 50-watt power envelopes on EVs.

How do retrofit regulations affect aftermarket growth?

UN Reg 128 and new FMVSS 108 guidance legalize LED drop-in bulbs, unlocking a USD 1.2 billion upgrade pool in North America and Europe.

Which suppliers currently lead V2X-enabled lighting technology?

Koito, Valeo, and HELLA (FORVIA) invest heavily in matrix LED arrays that project road symbols and communicate intent to other road users.

What is the main supply-chain risk for advanced lighting systems?

Ongoing shortages of 40-nm and 65-nm LED driver ICs lengthen lead times and push suppliers to carry 20-week safety stock.

Page last updated on: